News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

The Corn & Ethanol Report

By: Daniel Flynn | February 1, 2023

We kickoff the day with MBA 30=Year Mortgage Rate, MBA Mortgage Market Index, MBA Purchase Index, and MBA Mortgage Applications at 6:00 A.M. at 6:00 A.M.., ADP Employment Change at 7:15 A.M., Global Manufacturing PMI, Final at 8{45 A.M., ISM Manufacturing PMI, JOLT’s Job Openings, ISM Manufacturing New Orders, and ISM Manufacturing Spending at 9:00 A.M., EIA Energy Stocks at 9:30 A.M., 17-Week Bill Auction at 1

0:30 A.M., Fed Interest Rate Decision at 1:00 P.M., Fed Press Conference at 1:30 P.M., Cotton System, Dairy Product Sales, Fats & Oils, and Grain Crushings at 2:00 P.M. All traders will be watching the Fed”s next move.

On the Corn Front US Farmers sound alarm on single most catastrophic thing headed for corn crops. Farmers visit Washington DC warning they could go out of business over Mexico’s genetically modified corn ban. Meanwhile, a Chinese Corn Mill project in the USA has been halted on security concerns. The Us had to step in and let the market search in Free Enterprise and Fair Market Value. Brazil’s exports prove that exports to China will be on the low end of their needs. In yesterday’s action the market closed mostly unchanged as doubt continues to loom with COVID19 along with concerns of feed for human consumption. In the overnight electronic session the March corn is currently trading at 677 which is 2 3/3 cents lower. The trading range has been 679 ¼ to 675 ¼.

On the Ethanol Front Stellantis focused on ethanol hybrid vehicles in South America. Stellantis NV (STLA.MI) expects to have in place by the end of the year with the technologies needed to develop ethanol hybrid vehicles in Brazil, the head of the carmaker in South America. This will be another political football as governments continue to, “funding clean energy alternatives.” As the average Joe is worried about the economy. There were no trades in ethanol futures.

Read Full Story »»»

DiscoverGold

DiscoverGold

Certainty. The Energy Report

By: Phil Flynn | February 1, 2023

It’s nice to know, in an uncertain world, that there are some things you can count on. For example, as I predicted yesterday, the White House bashed Exxon Mobil’s blow-out profits, and The Energy Information Administration (EIA) admitted that they have once again massively underestimated oil demand.

How dare Exxon Mobil make a record yearly profit of 55.7 billion dollars as Americans are seeing a record increase in rage anxiety because their electric cars aren’t holding a charge in the cold. The White House expressed outrage and said that oil companies should increase production, but “are instead choosing to plow those profits into padding the pockets of executives and shareholders”. Things are getting so bad that Biden may have to create safe rooms so the EV buyers can scream and cry especially as their electricity costs soar and may find out that getting off of gasoline might not save them any money anyway. Yet Biden has created a lot of green jobs. The kids in the Congo cobalt mines are busier than ever. If Biden wants to keep pushing for more EVs, then he better start finding out more ways to get those mines ready so we can get the rare earth minerals to produce these electric cars that store energy mainly produced with coal and natural gas. And if the White House is serious about oil companies producing more oil, then maybe we should quickly approve the Willow Project.

Bloomberg News reports that, “US President Joe Biden is nearing a critical decision on a massive proposed oil project in northwest Alaska that could unlock 600 million barrels of crude and has drawn the ire of environmentalists who have dubbed it a “carbon bomb.” Biden’s verdict on ConocoPhillips’ $8 billion Willow venture in the National Petroleum Reserve-Alaska is being seen as a litmus test of his commitment to combating climate change. Bloomberg says that, “The project poses a political risk for the president, who has implored oil companies to boost production even as he tries to speed the US transition to emission-free energy. It also presents a new test of Biden’s ability to balance the desires of two oft-competing constituencies: environmentalists and organized labor. The Interior Department is expected in the coming days to release a final environmental impact statement on Willow, ordered after a federal court tossed out the previous analysis and project approval from the Trump administration according to Bloomberg.

Wait, what? President Trump was for it. So, Biden can’t be for it? Or can he. I mean just because the proposed Willow project in the northeast section of the National Petroleum Reserve-Alaska would produce 180,000 barrels of oil each day, create $10 billion in tax and royalty revenues, and create 2,000 construction jobs and 300 permanent ones according to the DC brief then Biden can’t be for it because he helped kill the project because Trump was for it.

So, Biden wants the oil companies to produce more oil but at the same time he stands in their way. And then blame them for record profits as his policies reduce supply and thereby increase profits for big oil. Conoco Phillips must be getting tired of the long approval process and other global investors looking at the United States must be losing confidence that this county is a place to do business when the government continues to make regulatory decisions based on politics and not science or even reality. So Biden wants oil companies to invest their shareholder’s money into projects where they could lose billions of dollars at the whim of this man.

The EIA just can’t seem to get that ol’ oil demand number just right. They adjusted November upward by close to 400,000 barrels a day in November to 20.593m b/d from the previously reported 20.211m b/d. To put that in perspective, that’s about twice as much oil that Willow is expected to produce.

Biden must be upset with BP because they expect to produce less oil. Now wait a minute, I thought he wanted them to produce less oil before he wanted them to produce more. I think he was against oil before he was for it. Yet BP released a report Monday predicting that the world would sharply reduce its reliance on oil and gas, over the next 25 years as countries transition to renewable sources of energy. In its annual energy outlook, BP said that fossil fuels, which it said accounted for 80% of energy usage in 2019, would fall to just 20% by 2050.

Yet despite all of this big-picture drama that has put oil in a secular bull market, the short-term focus is still on the Fed and OPEC. OPEC is expected to stay the course even as they reported they are still having a hard time pumping their quota. OPEC missed their output target by 920,000 barrels a day and that is a worse performance than the month before when they missed the target by only 780,000 barrels a day. Russia and OPEC are showing solidarity and there are predictions that we will see Russian oil production drop by at least a million barrels a day in the coming months.

Prices have moved dramatically. With the Fed talks, speeches and expectations, there is no doubt that if the Fed comes off as more hawkish, oil prices are going to struggle. On the other hand, if they come in the middle of the road, oil prices should make new highs for the move and reestablish its uptrend. Any close above 8050 today for crude oil, should project us sharply higher in the coming weeks.

The report from the American Petroleum Institute was a little bit bearish. Refinery issues helped feed a 6.33 million barrel crude oil increase and surprisingly both gasoline and diesel supply were higher. The API reported that yes, line supplies were up 2.73 and diesel supplies were up 1.53 million barrels!

Dan Molinski of Dow Jones wrote yesterday that, “Natural-gas prices appear to be steadying, up 0.2% at $2.684/mmBtu, which may help the market avoid seeing its largest one-month decline on record. The front-month contract is currently down 40% for the month of January, which would be the largest one-month decline since the month of January 2001, when it fell by 41.6%. But if another bout of selling ensues between now and the end of the trading day at 2:30 pm ET, and prices settle at or below $2.6127/mmBtu, January 2023’s decline would be nearly 42%, and it would go down as natural gas’s worst-performing month percentage-wise on record, with data going back to April 1990.

What makes that more amazing is the EIA reported that U.S. natural gas consumption reached record daily high in late December 2022. On December 23, 2022, natural gas consumption in the U.S. Lower 48 states reached a daily record high of 141.0 billion cubic feet (Bcf), according to estimates from S&P Global Commodity Insights. The previous record was 137.4 Bcf, set on January 1, 2018. Below-normal temperatures in mid-to late December increased demand for natural gas used for residential and commercial space heating and electric power generation. At the same time, natural gas production quickly fell because of mechanical issues caused by cold temperatures.

Scott Disavino at Reuters is reporting potential major progress in reopening Freeport LNG which was a major factor in the natural gas price collapse. He reported that Freeport LNG asked U.S. regulators for approval to add natural gas to one of the three idled units at its liquefied natural gas (LNG) export plant in Texas, a milestone in efforts to restore production after a seven-month outage, according to a federal filing made available on Tuesday.

Read Full Story »»»

DiscoverGold

Today's Futures Heat Map • Strongest: Coffee, Orange Juice, Heating Oil, Sugar

By: Barchart | January 31, 2023

• Today's Futures Heat Map

Strongest: Coffee, Orange Juice, Heating Oil, Sugar

Weakest: Cocoa, Soybean Meal, Corn, Milk

Read Full Story »»»

DiscoverGold

Commodity price changes over the last year...

By: Charlie Bilello | January 31, 2023

• Commodity price changes over the last year...

Sugar: +15%

Heating Oil: +13%

Corn: +9%

Gold: +8%

US CPI: +6.5%

Soybeans: +6%

Silver: +5%

Gasoline: -1%

Wheat: -3%

Copper: -5%

Brent Crude: -5%

Zinc: -6%

WTI Crude: -10%

Coffee: -27%

Cotton: -30%

Natural Gas: -38%

Lumber: -48%

Read Full Story »»»

DiscoverGold

Grains Report: Wheat, Rice, Corn and Oats, Soybeans

By: Jack Scoville | January 31, 2023

• WHEAT

General Comments: Wheat markets were higher yesterday and trends are sideways in all three markets on the daily and weekly charts. The rally came on news that the US and Germany were about to supply tanks to Ukraine, allowing the war to get hotter while the Wheat develops and the Corn maybe gets planted. Russia has a large production although UISDA says it is not nearly as large as Russia says it is. Big Russian production goes against the difficulty of moving grain from the Black Sea due to insurance requirements, but so far the lack of insurance has not increased demand for US Wheat as the Russian Wheat is still moving. The demand for US Wheat in international markets has been a disappointment all year and has been hindered by low prices and aggressive offers from Russia. Ukraine is also looking for new business for its crops and Russia is aggressive in the world market as it looks for cash to fund the war.

Overnight News: The southern Great Plains should get mostly dry conditions. Temperatures should average near to below normal. Northern areas should see mostly dry conditions. Temperatures will average below normal. The Canadian Prairies should see mostly dry conditions. Temperatures should average below normal.

Chart Analysis: Trends in Chicago are mixed, Support is at 744, 729, and 721 March, with resistance at 766, 7672, and 784 March. Trends in Kansas City are mixed to up with objectives of 895 and 910 March. Support is at 871, 866, and 850 March, with resistance at 895, 8901, and 915 March. Trends in Minneapolis are mixed to up with objectives of 933, 961, and 969 March. Support is at 907, 897, and 890 March, and resistance is at 935, 942, and 946 March.

• RICE:

General Comments: Rice was lower yesterday and the daily charts show that futures failed at resistance areas near 1800 again. Demand has been a problem for bullish traders. There is not much going on in the domestic market right now although mills are milling for the domestic market in Arkansas and are bidding for some Rice and although some Rice moved in Texas at what were called very good prices. Demand in general has been slow to moderate for Rice for exports and solid for domestic uses.

Overnight News: The Delta should get isolated showers. Temperatures should be below normal.

Chart Analysis: Trends are mixed. Support is at 1800, 1785, and 1776 March and resistance is at 1825, 1836, and 1840 March.

• CORN AND OATS

General Comments: Corn and Oats closed higher yesterday, mostly in sympathy with the rallies in Wheat and especially the Soy complex. Both markets remain in up trends established in early December. The export demand was solid last week even though demand remains well behind the pace to make USDA objectives. Brazil has been hanging on for its Summer crop although losses are now being reported. Argentina has suffered through some extreme drought. The Brazil Winter crop is harvested and China is buying the surplus. The Summer crop and the Argentine crop is developing under stressful conditions. The next Winter crop is going into the ground in good conditions, but it has been wet so the Soybeans harvest has been delayed and the Corn planting is becoming delayed as well. Weak demand overall for US Corn remains a big problem for the market. There are increasing concerns about demand with the Chinese economic problems caused by the lockdowns creating the possibility of less demand as South America has much better crops this year to compete with the US for sales. China is now moving rapidly to open the economy and allow people to move around with no lockdowns so the demand could start to improve. The improvement might take some time as the Chinese people get Covid, but they should be past this episode in a few weeks and demand might start to improve at that time.

Overnight News:

Chart Analysis: Trends in Corn are mixed to up with objectives of 688 and 701 March. Support is at 675, 669, and 666 March, and resistance is at 689, 693, and 698 March. Trends in Oats are up with objectives of 400 March. Support is at 386, 377, and 372 March, and resistance is at 399, 405, and 411 March.

• SOYBEANS

General Comments: Soybeans and both products were higher yesterday despite the news that Argentina and southern Brazil weather changed to a much wetter pattern for the last week. The pattern in southern Brazil and Argentina is shifting back to dry again. Price trends are turning up for Soybeans and Soybean Meal as the harvest in Brazil starts to expand in central and northern areas. These areas have seen too much rain and the harvest has been slow. The weekly charts show that Soybeans are trying to hold an uptrend line established in October while Soybean Meal seems to be bouncing off or support areas established a few weeks ago. Soybean Oil is in a sideways trend. Production potential for the Brazil is called very strong even with potential problems and losses in the south. Even so, production of less than 150 million tons is possible now although most estimates remain near 153 million tons. Argentine production ideas continue to drop with the drought as planting is delayed and the crops already in the ground are stressed. Production estimates are now closer to 40 million tons than original projections near 50 million. Ideas that Chinese demand will improve, but this could take a few more weeks as a very large part of the population now has Covid. This has delayed a robust economic return for the country.

Overnight News:

Chart Analysis: Trends in Soybeans are mixed to up with objectives of 1557 and 1564 March. Support is at 1513, 1503, and 1487 March, and resistance is at 1538, 1548, and 1556 March. Trends in Soybean Meal are up with objectives of 505.00 and 515.00 March. Support is at 479.00, 472.00, and 468.00 March, and resistance is at 490.00, 496.00, and 502.00 March. Trends in Soybean Oil are mixed. Support is at 5990, 5940, and 5850 March, with resistance at 6220, 6360, and 6470 March.

Read Full Story »»»

DiscoverGold

Softs Report: Cotton, OJ, Coffee, Sugar, Cocoa

By: Jack Scoville | January 31, 2023

• COTTON

General Comments: Cotton was lower and still remains inside the trading range created since the beginning of November. Futures are still showing bad demand fundamentals that have kept prices from rallying through resistance areas. Overall, the demand for US Cotton has not been strong although better demand has developed over the last couple of weeks. Some ideas that demand could soon increase as China could start to open its economy in the next couple of months as Covid outbreaks should start to weaken as people get vaccinated or immune. Covid is now widespread in China so the beneficial economic effects of the opening are being delayed but these effects should start to be felt as the people there achieve immunity over the next few weeks.

Overnight News: The Delta will get isolated to scattered showers and near to below normal temperatures. The Southeast will see isolated to scattered showers and above normal temperatures. Texas will have isolated showers and below normal temperatures. The USDA average price is now 82.89 ct/lb. ICE said that certified stocks are now 8,900 bales, from 8,900 bales yesterday.

Chart Trends: Trends in Cotton are mixed. Support is at 83.20, 82.00, and 81.30 March, with resistance of 87.50, 88.90 and 89.90 March.

• FCOJ

General Comments: FCOJ was higher and trends started to turn up again on the daily charts. Demand should start to improve with the holidays now over and cold air being reported over much of the country. Historically low estimates of production due in part to the hurricanes and in part to the greening disease has hurt production remain in place but are apparently part of the price structure now. The weather remains generally good for production around the world for the next crop but not for production areas in Florida that have been impacted in a big way by the two storms. Brazil has some rain and conditions are rated good. Mostly dry conditions are in the forecast for the coming days.

Overnight News: Florida should get mostly dry conditions. Temperatures will average above normal. Brazil should get scattered showers and near normal temperatures.

Chart Trends: Trends in FCOJ are mixed o up with objectives of 220.00 March. Support is at 207.00, 203.00, and 201.00 March, with resistance at 214.00, 217.00, and 220.00 March.

• COFFEE

General Comments: New York closed higher and London closed lower yesterday with Vietnam back at work after the Lunar New Year and the US Dollar moving a little lower during the session. The charts show that New York is trying to complete a bottom that could be significant to medium range pricing. London weekly charts show a market that has been working a little higher almost every week since November but ran into a little speculative long liquidation along with little new buying interest yesterday. Ideas of big production for Brazil continue due primarily to rains falling in Coffee production areas now and as offers stayed strong from Brazil and increasingly from Vietnam. There are ideas that production potential for Brazil had been overrated and reports of too much rain in Vietnam affected the harvest progress. The weather in Brazil is currently very good for production potential but worse conditions seen earlier in the growing cycle hurt the overall production prospects as did bad weather last year. Ideas are that the market will have more than enough Coffee either way when the next harvest comes in a few months.

Overnight News: ICE certified stocks are higher today at 0.852 million bags. The ICO daily average price is now 167.34 ct/lb. Brazil will get isolated showers in northern areas with near normal temperatures. Central America will get scattered showers. Vietnam will see scattered showers.

Chart Trends: Trends in New York are up with objectives of 172.00 March. Support is at 167.00, 165.00, and 163.00 March, and resistance is at 175.00, 177.00 and 183.00 March. Trends in London are up with objectives of 2040 March. Support is at 2000, 1950, and 1910 March, and resistance is at 2040, 2070, and 2120 March.

• SUGAR

General Comments: New York and London closed higher yesterday and chart patterns indicate that prices can move higher again over the course of this week. Good production prospects are seen for crops in central and northern areas of Brazil, but the south should turn dry again after some rains in the last week or so. The harvest has been delayed in Thailand. Australia and Central America harvests are also delayed but are more active now. Ideas are that India will produce about 34.3 million tons of Sugar this year, about 4% less than the previous outlook.

Overnight News: Brazil will get scattered showers. Temperatures should average near normal. India will get mostly dry conditions and near to above normal temperatures.

Chart Trends: Trends in New York are up with objectives of 2160 March. Support is at 2080, 2050, and 2020 March and resistance is at 2130, 2160, and 2170 March. Trends in London are up with objectives of 573.00 and 603.00 March. Support is at 562.00, 559.00, and 552.00 March and resistance is at 571.00, 579.00, and 582.00 March.

• COCOA

General Comments: New York closed a little lower and London closed a little higher yesterday. Both markets show that futures are in mostly a range trade. Weaker demand shown by the grind data that got released in the last week. Talk is that hot and dry conditions reported in Ivory Coast could curtail mid crop production, but main crop production ideas are strong. Ghana has reported a disease in its Cocoa to hurt production potential there. The rest of West Africa appears to be in good condition. The North American grind was 8.1% lower and the EU and Asian grinds were about 2% lower. Good production is reported for the main crop and traders are worried about the world economy moving forward and how that could affect demand. Supplies of Cocoa are large at ports. The weather is good in Southeast Asia.

Overnight News: Mostly dry conditions are forecast for West Africa. Temperatures will be near normal. Malaysia and Indonesia should see scattered showers. Temperatures should average near normal. Brazil will get scattered showers and near normal temperatures. ICE certified stocks are lower today at 4.961 million bags.

Chart Trends: Trends in New York are mixed. Support is at 2570, 2540, and 2510 March, with resistance at 2650, 2670, and 2700 March. Trends in London are mixed to up with objectives of 2060, 2090, and 2160 March. Support is at 2020, 1990, and 1950 March, with resistance at 2050, 2080, and 2090 March.

Read Full Story »»»

DiscoverGold

FOMC Meetings Begin. The Corn & Ethanol Report

By: Daniel Flynn | January 31, 2023

We kickoff the day with Employment Cost Index QoQ, Employment Cost-Benefits QoQ, and Employment Cost-Wages QoQ, at 7:30 A.M., Redbook YoY at 7:55 A.M., S&P/Case-Schiller Home Price MoM & YoY, House Price Index at 8:00 A.M., Chicago PMI at 8:45 A.M., Consumer Confidence at 9:00 A.M, Dallas Fed Services Index and Dallas Fed Services Revenues at 9:30 A.M., Cattle at 2:00 P.M., API Energy Stocks at 3:30 P.M., and the First of 2 FOMC Meetings with Rate Decision Tomorrow at 1:00 P.M.

On the Corn Front PRO Farmer Analysis reports, Expected large Brazilian corn exports to China in 2023 are worrying Brazil’s meat companies, according to a statement from Santa Catarina’s meat processors lobby Sindicarne. The group said competition from Chinese buyers is already reducing local supplies and making corn used for feed poultry and pork an “overpriced commodity. “Even with the sector being more prepared for negotiations and more attentive to stocks and purchases, there is always competition from the international market,” Sindicarne said. “For 2023 the signs are worrying.” According to Sindicarne, which represents global poultry and pork processors including JBS and BRF, the government must also “do its part” to attract investments aimed at reducing Brazil’s bottlenecks. The group said that while Brazil has created decent logistics network to export grains, there are no railroads connecting grain regions in the central west to southern Brazil, where pork and chicken are typically raised and processed.

Speaking of bottlenecks and the crisis low river levels. The US Army Corps of Engineers has been dredging the Mighty Mississippi 24-hours a day, 7-days a week since July….. ever since low water levels on the river due to drought… Started causing shipping backups. The Corps hopes to be done dredging by the end of the month. I will keep you posted as I receive the news. In yesterday’s action corn prices closed steady to higher following soybeans lead. Argentina had short-term relief to drought stricken areas of Argentina, forecasts expect dryer conditions by the end of the week. The next rain event slated for the middle part of this week across western and southern parts of Argentina, away from the larger producing areas. In the overnight electronic session the March corn is currently trading at 681 ¾ which is 2 cents lower. The trading range has been 683 ½ to 680 ½.

On the Ethanol Front India is blending its way to needing US ethanol news if it can keep on track for more ethanol in gasoline. Meanwhile, attorney generals of seven Midwest states are urging the EPA to respond to the E15 petition. The attorney generals of Iowa, Illinois, Minnesota, Missouri, Nebraska, South Dakota, and Wisconsin are urging the Biden administration to take action on the petition filed by a bipartisan coalition of governors in April 2022 seeking a permanent solution to year-round E15 sales with their states. Ethanol Futures lacking any open interest.

Read Full Story »»»

DiscoverGold

Fed Anxiety. The Energy Report

By: Phil Flynn | January 31, 2023

Forget rising gasoline prices or the fact that there was no more oil released from the Strategic Petroleum Reserve (SPR). The oil and product markets are infected with Fed anxiety. Oh sure, they might be worried about OPEC and the upcoming Russian sanctions and stupid price cap but really it was Fed anxiety that shook the oil trade. To be fair it was not just oil that is infected with fear, The rally in the US dollar led to risk-off selling for many high-flying commodities yesterday and today except for a lot of the grain complex that is getting more concerned about the size of the South American crop against a backdrop of global carryover stocks that are hovering very close to all-time lows.

Yet perhaps the market should be more upbeat about the prospects for the global economy as the International Monetary Fund is raising their forecast for growth and lowering the outlook for inflation. The IMF says that, “Global growth is projected to fall from an estimated 3.4 percent in 2022 to 2.9 percent in 2023, then rise to 3.1 percent in 2024. The forecast for 2023 is 0.2 percentage point higher than predicted in the October 2022 World Economic Outlook (WEO) but below the historical (2000–19) average of 3.8 percent. The rise in central bank rates to fight inflation and Russia’s war in Ukraine continue to weigh on economic activity. The rapid spread of COVID-19 in China dampened growth in 2022, but the recent reopening has paved the way for a faster-than-expected recovery. Global inflation is expected to fall from 8.8 percent in 2022 to 6.6 percent in 2023 and 4.3 percent in 2024, still above pre-pandemic (2017–19) levels of about 3.5 percent.

Yet if we see an uptick in growth, where are we going to get the extra oil to meet a surge in Chinese oil demand? The Biden administration says it wants to crack down on Iran which is skirting oil sanctions but lacks the willpower because they fear an oil price spike. Iran has been laughing at US oil sanctions as they have no respect or fear of the Biden administration.

The Biden administration’s SPR game has come to an end as there was no oil released from the SPR for the third straight week. That should lead to some major US crude oil draws in the coming weeks after US refiners start to come out of maintenance both planned and unplanned. This week, we should see another increase in Cushing, OK supply as refiners are still shut down but with an uptick in exports. Crude supply should see a drawdown in tonight’s American Petroleum Institute report. We should also see a draw in gasoline and distillate and the tightness of product supply has been showing up at your local gas station. While the futures indicate that we will see some relief, the truth is that the oil product market is on a tinder keg. This is key after it was reported that EU imports of non-Russian gasoil and diesel rose sharply last week, helping to build up inventories ahead of the bloc’s impending embargo on Russian oil products.

Oil traders should not be expecting too much news out of the OPEC meeting. Right now they are continuing to stay the course even as the OPEC cartel is warning about historically low spare oil production capacity. OPEC is right, there’s no room for error in the system. It was reported that Russia’s President Vladimir Putin and Saudi Arabia’s Crown Prince Mohamed bin Salman discussed cooperation within OPEC+ to provide stability to the global oil market. That should make the anti-US oil crowd happy as they continue to strengthen Putin and Bin Salman with every barrel of oil and every BCF of gas they do not let us produce.

Venezuela, the Biden administration’s great hope to replace SPR oil, now wants to get paid. I know! That messes things up. It seems that even as they are starting to sell oil after Biden lifted some sanctions, because they owe everybody money, they do not see the cash. Now their state oil firm PDVSA is toughening terms for buyers after a month-long halt to most exports of crude and fuel, demanding prepayment ahead of loadings in either cash, goods, or services, company documents showed according to Reuters. PDVSA’s new Chief Executive Pedro Tellechea put the move in place this month. It reinforces measures implemented last year after several buyers skipped out on payments for oil, which provides most of the South American country’s income.

While green energy madness drives up costs for everyday people and reduces global security, the question should be why the country is against natural gas. Talking about banning gas stoves and not allowing natural gas buildings even though natural gas is the cleanest burning fossil fuel. Yet the US is awash in natural gas and that could help lower the cost of heating and electricity if the government would embrace this fuel. Many forget that Alan Greenspan once warned that the greatest threat to the US economy was our inability to produce natural gas. The US oil and gas industry solved the issue and helped avert a major economic crisis.

Now the Energy Information Administration reports that the proven reserves of natural gas increased 32% in the United States during 2021 according to EIA thanks to US oil and gas producers. Proved reserves of natural gas in the United States grew to a new record of 625.4 trillion cubic feet (Tcf) in 2021, a 32% increase from 2020, according to our recently released Proved Reserves of Crude Oil and Natural Gas in the United States, Year-End 2021 report. U.S. proved reserves had previously decreased 4% in 2020 as a response to prices that fell with decreased consumption during the first year of the COVID-19 pandemic. At year-end 2021, however, five of the eight states with the most proved reserves of natural gas each reported new record volumes, driving the growth nationally. Proved reserves are operator estimates of the volumes of oil and natural gas that geological and engineering data demonstrate with reasonable certainty to be recoverable in future years from known reservoirs under existing economic and operating conditions. Prices heavily affect estimates of proved reserves. The wholesale spot price for natural gas at the U.S. benchmark Henry Hub in Louisiana averaged $3.89 per million British thermal units in 2021, almost doubling from 2020, according to data from Refinitiv.

The EU continued importing from Russia as well, taking 88,000 t/d last week, compared with 80,000 t/d across the whole of last year. The unusually large volumes of non-Russian imports may be difficult to sustain over a prolonged period. But European traders say their storage tanks are relatively full and demand from buyers has been depressed since November, so they are not worried about securing replacements for Russian diesel next month when the EU ban comes into effect. Most see a structural shortfall in Europe once diesel stocks are run down and demand picks up.

India is the only major non-Russian supplier that has not increased shipments to Europe this month. The EU’s daily intake of Indian diesel and gasoil was lower in January than the 2022 average. Supply from non-Russian sources has been back-loaded in January, with last week’s flurry of arrivals coming on the back of a thin patch in the middle of the month. Across January as a whole, the EU has imported around 119,000 t/d from outside Russia.

Non-Russian diesel in Europe has commanded wider premiums over Asian product in January, with front-month Ice gasoil futures around $60/t above front-month Singapore gasoil swaps on average, up from $45/t in December. But it has lost value against US Gulf coast product in recent weeks, which may start to constrict transatlantic trade.

Big oil is big again! The Wall Street Journal reported that Exxon Mobil Corp. rocketed to its highest-ever annual profit last year, riding surging oil prices to resurrect its status as one of America’s most profitable companies and erase billions of dollars of losses incurred during the pandemic. The largest U.S. oil company turned in record annual earnings of $55.7 billion for 2022 in its quarterly earnings Tuesday, outpacing big banks, tech giants, and vaccine makers. Among companies that have reported fourth-quarter earnings, only Apple Inc. and Microsoft Corp. have surpassed Exxon’s profit in fiscal 2022 so far, and only Google parent Alphabet Inc.. And they do not have to drill in the ocean to make those profits and use fossil fuels to make and ship their products! Will anybody complain about Apple and Microsoft’s profits? No, but you can be sure that the Biden administration will once again complain about Exxon’s profits. They will call on them to reduce prices! Will they also accuse Apple of war profiteering? Or using slave labor in China?

Read Full Story »»»

DiscoverGold

Today's Futures Heat Map: Strongest: Lumber, Soybean Meal, Palladium, Orange Juice

By: Barchart | January 30, 2023

• Today's Futures Heat Map

Strongest: Lumber, Soybean Meal, Palladium, Orange Juice

Weakest: Natural Gas, Heating Oil, Gasoline, Cotton

Read Full Story »»»

DiscoverGold

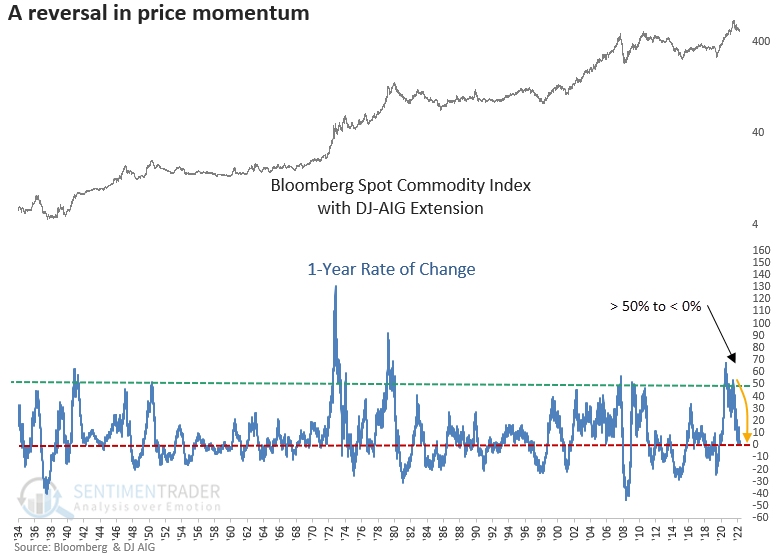

A significant reversal in commodity momentum

By: Dean Christians | January 30, 2023

• For only the eighth time in almost 80 years, the 1-year rate of change for a spot commodity index cycled from > 50% to < 0%. After similar reversals, a commodity index struggled over the next six to twelve months.

Read Full Story »»»

DiscoverGold

Hog Prices Firming Up Through Midday

By: Barchart | January 30, 2023

Hogs have backed off their initial gains for midday, but are still up by 17 to 65 cents so far. The Feb contract is the outlier with a 37 cent loss through midday. USDA’s National Average Base Hog price was 39 cents higher on Monday morning to $70.25. The 1/26 CME Lean Hog Index was $72.64, up by 12 cents.

Dalian Live Hog Prices fell sharply after the Lunar New Year break. Futures were 315 to 790 yuan/MT lower in the front months on Monday. The back months held firm on limited volume and OI, with Jan ’24 closing up by 450 yuan/MT.

Front month pork cutout futures are mixed on the board, with April up by $1.22 but Feb down by 55 cents. USDA’s National Pork Carcass Cutout value dropped $1.42 in the AM update, to $79.04. USDA estimated last week’s FI hog slaughter as 2.536m head through Saturday. That compares to 2.531 million last week and 2.530 million during the same week last year.

Read Full Story »»»

DiscoverGold

Wheats Up Through Midday

By: Barchart | January 30, 2023

The midday wheat market is showing 3 to 6 cent gains across the domestic classes. SRW is trading nearly a dime off the earlier highs, but still 3 to 5 1/2 cents in the black. HRW futures are up 5 3/4 to 6 3/4 cents so far, but March is 7 cents below the session high. MPLS Spring wheat pris are working with midday gains of 2 3/4 to 5 1/4 cents so far.

Weekly inspections data had 445,433 MT of wheat shipments for the week that ended 1/26. That was a weekly increase of 96,040 MT and was up by 67k MT from the same week last year. USDA showed nearly half of the total was spring wheat followed by 117k MT of HRW. Japan was the top destination. The weekly report had 13.222 MMT of wheat shipments for the season through 1/26, compared to 13.616 MMT last year.

Read Full Story »»»

DiscoverGold

Cattle Near Daily Highs At Midday

By: Barchart | January 30, 2023

Live cattle futures are trading triple digits higher so far with April leading the way on a $2.57 gain. USDA confirmed some light catch up business in the WCB on Friday, with sales of $155 - $156. The USDA mentioned activity from $152 to $157 through the week with limited enough volume to not declare a bulk price outside of $155 in NE.

Feeder cattle are trading triple digits higher as well with $1.10 to $1.70 gains through midday. USDA reported light volumes from the OKC Feeder Cattle Auction review citing winter weather. The report had only 2,750 head traded – compared to 9k last week and 11k last year, for prices steady to $3 lower. The CME Feeder Cattle Index for 1/26 was another $0.77 higher to $179.57.

Wholesale Boxed Beef prices were higher in Monday’s AM report with a 7 cent increase to Choice and a $1.14 increase to Select. That had the Chc/Sel spread at $16.15. Last week’s federally inspected cattle slaughter was estimated as 659k head through Saturday. That is up by 13k head from last week and by 4,000 head from the same week last year.

Read Full Story »»»

DiscoverGold

Double Digit Strength From Soy Market

By: Barchart | January 30, 2023

Beans are on the rally through Monday’s midday with gains of as much as 1.4%. Old crop futures are working 20 cents higher. Meal prices are leading the way with 1.9% to 2.4% gains so far. BO prices are also stronger, gaining 1% through midday.

Local Dalian Soybean Prices were weaker after the Lunar New Year break, fading 9 to 22 yuan/MT in the domestic market. The more import competitive Dalian No2 Soybean Prices were sharply higher after China’s week long break, as the front months saw 36 to 52 yuan/MT gains. Dalian bean prices remain inverted (backwardated) across both classes.

USDA reported 1.855 MMT of soybeans were exported during the week that ended 1/26. That was a 16.6k MT increase from last week and was up by 437k MT from the same week last year. China was the top destination with 76% of the total. The weekly update had the season’s accumulated export at 35.989 MMT through 1/26 – trailing last year by just 461,035 MT.

Brazil’s Patria Agronegocios reported the soy harvest as 5.15% complete, compared to last year’s 11.4% pace.

Read Full Story »»»

DiscoverGold

Triple Digit Drop In Cotton Market

By: Barchart | January 30, 2023

So far for Monday the cotton board is in the red with triple digit losses. March is leading the way lower with a 203 point pullback on the board. December cotton is down by 169 points and trading near the session’s low. Crude oil is lower, a bearish potential influence on synthetic fiber prices. Equity futures are lower ahead of the FOMC meeting on Tuesday and Wednesday.

The Cotlook A Index for 1/27 was 75 points stronger to $1.02 40/100/lb. The AWP for cotton was raised 262 points to 75.05 cents per pound.

Read Full Story »»»

DiscoverGold

Arabica Coffee Prices Supported By Supply Concerns

By: Barchart | January 30, 2023

March arabica coffee (KCH23) this morning is up +0.60 (+0.35%), and Mar ICE robusta coffee (RMH23) is down -15 (-0.73%).

Coffee prices this morning are mixed, with arabica climbing to a 1-month high. Concerns about smaller arabica supplies are underpinning prices. Volcafe said because of weak flower blossoms on coffee trees in the Minas Gerais coffee-growing region, it cut its Brazil 2023/24 arabica coffee production estimate to 40.5 mln bags from a July forecast of 49.8 mln bags. Dollar strength today (DXY00) limited gains in coffee prices.

A bullish factor for coffee prices was the January 16 report from Cecafe that showed Brazil's 2022 green coffee exports fell -2.7% y/y to 35.6 mln bags, the lowest in 4 years.

A bullish factor for robusta coffee is shrinking supplies after ICE-monitored robusta coffee inventories today fell to 6,212 lots, the fewest since contract rules changed in 2016.

Robusta also has support after coffee trader Volcafe forecasted that the global 2023/24 robusta coffee market would see a record deficit of 5.6 mln bags as Indonesia, the world's third-largest robusta producer is expected to see its 2023/24 robusta coffee production fall to 9.1 mln bags, the smallest robusta crop in 10 years due to damage from excessive rainfall across its growing regions.

An easing of dry conditions in Brazil may boost coffee yields and is bearish for prices. Somar Meteorologia reported today that Brazil's Minas Gerais region received 72.9 mm of rain last week, or 141% of the historical average. Minas Gerais accounts for about 30% of Brazil's arabica crop.

Abundant arabica coffee supplies are negative for prices. ICE arabica coffee inventories have risen steadily since falling to a 23-year low of 382,695 bags on November 3 and posted a 6-3/4 month high of 870,7224 bags last Thursday. Also, Conab on January 19 forecasted the 2022/23 Brazil arabica crop would rise +14.4% to 37.4 mln bags.

Increased coffee exports from Vietnam, the largest robusta producer, are bearish for robusta prices after the General Statistics Office of Vietnam reported on January 9 that Vietnam's 2022 coffee exports were seen up +13.8% y/y at 1.8 MMT.

On the bullish side for coffee prices was the January 4 report from the Colombia Coffee Growers Federation that showed Colombia's 2022 coffee exports fell -8% y/y to 11.1 mln bags. Colombia is the world's second-biggest producer of arabica coffee beans.

On the bearish side, U.S. green coffee inventories are plentiful after the Green Coffee Association on January 17 reported that U.S. Dec green coffee inventories rose +9.3% y/y to 6.38 mln bags.

The USDA, in its bi-annual report released on December 23, cut its global 2022/23 coffee production estimate by -1.3% to 172.8 mln bags from a June estimate of 175.0 mln bags. In addition, the USDA cut its 2022/23 global coffee ending stocks estimate by -1.7% to 34.1 mln bags from a June estimate of 34.7 mln bags.

The International Coffee Organization (ICO) reported on December 2 that global coffee exports in Oct fell -1.9% y/y to 9.87 mln bags.

In a bullish factor, the USDA's Foreign Agriculture Service (FAS) on November 22 cut its Brazil 2022/23 coffee production forecast by -2.6% to 62.6 mln bags from a prior estimate of 64.3 mln bags. This year was supposed to be the higher-yielding year of Brazil's biennial coffee crop, but coffee output this year was slashed by drought.

Read Full Story »»»

DiscoverGold

Corn Exports? The Corn & Ethanol Report

By: Daniel Flynn | January 30, 2023

We kickoff the day with Dallas Fed Manufacturing Index at 9:30 A.M., Export Inspections at 10:00 A.M., and 4-Week & 8-Week Bill Auction at 10:30 A.M. We will have a busy week ahead of us with the jobs numbers Thursday and Friday.

On the Corn Front we will be watching Export Inspections as US corn exports are expected to pick up. Much needed rains in Southern Brazil that was forecasted this weekend was close to nil. The chance for rain in Southern Brazil is 0% with winds at 4 mph. Central Brazil may have mild delays this week before a drier system moves in. In the overnight electronic session the March corn is currently trading at 683 ½ which is a ½ of a cent higher. The trading range has been 687 ¼ to 682 ½.

On The Ethanol Front BK-H2 Energy, LLC, was welcomed last week by the Renewable Fuels Association as its newest associate member. BK-H2 Energy, LLC, is a consulting company engaged in the transition of diesel/gas and CNG Vehicles to battery electric and hydrogen fuel cells, collaborating with GOLU

Hydrogen Technologies, which developed a way to use ethanol as feedstock to produce low-cost green hydrogen for fuel cell vehicles and electric power required for charging the battery-electric cars and trucks. Give me coal or natural gas any day. To make batteries possible is coal and natural gas not to mention the raw materials we would be forced to import from our enemies. There were no trades in ethanol futures.

Read Full Story »»»

DiscoverGold

Deliveries on Energies/Rapeseed Oil/Nymex & Comex

By: The PRICE Futures Group | January 30, 2023

• Tomorrow, Tues Jan 31st is Last Trading Day for Feb Heating Oil, Rbob, MTF Rapeseed and March Murban Oil.

• Tomorrow, Tues Jan 31st is First Notice Day for Feb Nymex and Comex metals.

Read Full Story »»»

DiscoverGold

It's time to keep an eye on soybeans

By: Jay Kaeppel | January 30, 2023

• In the past 90+ years, soybeans have shown a strong tendency to rally during the year's first half and decline during the second half. They are now entering a typically favorable window. As long as price action holds up, traders may benefit from focusing on the long side of the market. Non-futures traders can also participate by trading an ETF designed to track the price of soybean futures.

Read Full Story »»»

DiscoverGold

Futures performance in January so far: lumber bid and natural gas slid

By: Markets & Mayhem | January 30, 2023

• Futures performance in January so far: lumber bid and natural gas slid

Read Full Story »»»

DiscoverGold

Earthshaking. The Energy Report

By: Phil Flynn | January 30, 2023

Oil prices got a nice pop on Sunday night on reports that Israel sent drones to attack an Iranian military factory. This came just after a 5.9 earthquake hit on the Iranian-Turkey border. Coincidence? Yes, but still earthshaking. Will it be enough to shake the oil market out of its slumber?

After an early Sunday night opening price pop, we started to drop on a risk-off trade as there is a lot of news this week that the trade fears can be earthshaking. OPEC plus has a virtual meeting on February 1 and the Federal Reserve is due to make its announcement on interest rates on Wednesday and that’s making the markets a bit nervous. OPEC is not expected to shake things up and is widely expected to roll over its current production cuts. The Fed decision on interest rates really should not be too much of a surprise even though there are some like Dennis Gartman who believes that the Fed will cut by 50 basis points as opposed top the 25 basis cut that the market expects. Mr. Gartman believes that they feel inflation is still a risk based on Fed statements.

Perhaps it is because they see gasoline prices that have been soaring because of increased demand and low refining capacity and the fact that the market must adjust to the reality that Biden’s SPR releases have ended. Triple AAA says that gasoline prices are at 3.508 a gallon. That is up from $3.423 a week ago and up from $3.363 a year ago.

It’s not just gasoline that is surging. AAA says that, “Diesel prices are at 4.676 which is up from 3.908 a month ago and up from $3.717 a year ago. The trend of gas and diesel should continue higher after Exxon Mobil (XOM.N) pushed back its restart of the Beaumont, Texas, refinery, which has been trying to finish a $2 billion expansion that will make it the second largest in the United States. Right now the market really needs 250,000 barrels per day of all new supplies for the refined products market.

Another concern for oil is the risk that will come with EU sanctions on Russian oil and products that starts on February 5th and that is when the embargo on buying Russian oil starts. This should be a bullish act even if it does not cause the oil supply to tighten overnight. The International Energy Agency executive Fatih Birol says Russian oil output could fall by a million barrels a day in 2023. Now when the SPR releases end, the market will feel a bit of a shock as it could not adjust because of Biden’s misuse of the reserve.

The House is trying to respond to Biden’s misuse and abuse of the Strategic Petroleum Reserve. Reuters reported that, “The U.S. House of Representatives passed a bill on Friday limiting the ability of the energy secretary to tap the strategic oil reserve without developing plans to increase the number of public lands available for oil and gas drilling. Representatives backed the bill 221 to 205, with support from only one Democrat. Joe Biden would veto the legislation should it pass Congress, the White House said this week. The bill is expected to face an uphill battle in the Senate, which, unlike the House, is controlled by Biden’s fellow democrats according to Reuters.

Democrats famously blocked President Trump’s attempt to refill the Strategic Petroleum Reserve (SPR) at about $24.00 a barrel. I wrote at the time that would prove to be a mistake that has cost the taxpayers dearly. Now with Biden using the SPR to manipulate the market for political purposes to lower gasoline prices as he released oil even before the war in Ukraine started, it is starting to backfire and we’re seeing that at the gasoline pump as prices start to rise. It’ll be interesting to see if Biden takes credit for the increase in gas and diesel prices that no doubt Americans are feeling right now.

While gasoline prices and diesel prices are up, we’re actually seeing a break in fertilizer prices which is good news considering the fact that we’re entering a period of extremely tight supplies of grain. Warm temperatures have eased natural gas prices and even though natural gas is popping on a return of cold weather, this morning the drop in prices helps fertilize prices come down.

One of the fuels that have fallen is E85 and if you look at the market that is heavily subsidized, it seems to be the cheapest fuel around. Just forget the fact that you don’t get as much bang for your buck as far as mileage goes. Biden is throwing more money at Agra fuels at a time when food supplies globally are very tight. Grain prices are already high and could get much tighter. Reuters reports that, “Chicago soybeans and corn rose on Monday on concern that drought-damaged crops in Argentina were facing more dry weather. Wheat rose as a cold snap in U.S. grain belts generated concern about possible crop damage, while potential escalations in the Russia-Ukraine war also underpinned prices.

So with food and fuel supplies being the tightest they’ve been almost ever globally, with global spare production capacity for oil nonexistent the risk for commodities is still very much to the upside. Those who were doubting the Chinese reopening are reassessing their earlier predictions we believe that now it’s a good time to put on your hedges going into winter. Even the natural gas market that saw a sea change in fundamentals due to a warm winter, as well as a shutdown of the major export terminal Freeport, could start to find some bottoming action here over the next couple of days.

Read Full Story »»»

DiscoverGold

Soybean oil, wheat and coffee... no trading on margin.

Wheat was strong last week and starting strong tonight.

What I'm Watching In The Grain Markets This Week

By: Barchart | January 29, 2023

I’ve struggled more this week with what to write about than in previous weeks. Of course there is a ton to talk about, but in complete honesty, not much of it has changed from last week.

Yes, I am watching what is happening with the Black Sea Grain Corridor as the West starts sending tanks and other equipment to Ukraine, something Russia calls a ‘blatant provocation.’ With the corridor’s renewal less than 2 months away, it is likely we will start to hear more about a potential closure as Russia knows the corridor is one of the few bargaining chips it has.

I’m also continuing to watch what is happening when it comes to South American production. Harvest looks like it will continue to ramp up across Brazil, with reports of massive soybean yields coming out of Mato Grosso. Some cash traders in the country say the crop in their opinion is working towards 155 mmt, up from the current working trade estimate of around 153 mmt.

Rains in Argentina over the last couple of weeks were relatively decent and relatively widespread, though not enough to cure the drought of course, and not enough to fix the production loss in early planted crops. It will be enough to stabilize later planted production and allow farmers in the country to finish planting corn.

The forecast for the next two weeks turns back dry, with warmer temperatures, making model runs this week for the last half of February that much more important.

And of course, you know I’m trying to gauge Chinese demand as the country reopens and its leaders claim the worst of the Covid infections are over. Many have been surprised recently by the strong pace in soybean sales and shipments, but with many Chinese crushers reportedly running on limited inventory and nearby margins solid, it shouldn’t be surprising importers are ramping up buys.

As of this week China had around 5 mmt of beans purchased from the US but not yet shipped, meaning big export inspections for shipments to China are likely to continue through February. Continued purchases would be bullish, especially with values out of Brazil starting to get cheaper for March forward.

But what I really want to talk about after thinking about it for some time is the situation in corn…

When thinking about the outlook for corn a Robert Frost poem popped into my head. Me, not really a Frost fan was surprised by this, but nonetheless once I googled it, I realized it fit perfectly:

The Road Not Taken

Robert Frost

Two roads diverged in a yellow wood,

And sorry I could not travel both

And be one traveler, long I stood

And looked down one as far as I could

To where it bent in the undergrowth;

While the poem itself is better known for its final lines talking about choosing the road less traveled, the first stanza encapsulates my feelings towards the corn market perfectly. In my opinion we are standing at a fork in the road, one leading to an incredibly bullish outlook, the other, potentially the opposite.

And while I know we can only go down one road, recognizing where it leads only once we get there, I feel like we’re currently standing at the fork, staring at a divergence that could have tremendous implications for price direction.

The knowns in the market feel somewhat comfortable. Thanks to a massive year over year increase in production, Brazil was able to export around 1 billion bushels more into the global market since last summer. Corn demand for ethanol looks like it will stay relatively steady for the most part, as plants continue to try to produce themselves into profitability. Feed demand looks like it could be reduced slightly for wheat feedings, but that appears to be more of a global factor than a domestic one.

Where the paths split is influenced almost solely by exports, with the implications being huge when it comes to price.

Path one is the bullish path, probably the corn growers favorite, and feels like the one most farmers and traders are positioned for. With the surprising reduction in corn production earlier this month, we have lost our buffer when it comes to an uptick in demand.

Yes, export pace is abysmal at best, still running around half of what it was a year ago, but the US is now the cheapest and most reliable supplier for the next several months.

Some analysts in the industry believe the absence of competition combined with an uptick in demand from China and other end users coming in for coverage could result in the US needing to supply upwards of 300 million bushels a month into the global market from February or March out into July, double our recent pace.

This with no loss seen in Brazilian second crop corn production. A production issue in Brazil this year would result in the US being the supplier of necessity well beyond July, something our current supply would have a difficult time supporting.

The second path is the path ‘old corn’ used to take, you know, corn before 2021, inflation, several production issues and a huge spike in demand happened. Down that path exports remain lukewarm at best. Yes, we get demand, we see an uptick in sales pace from both a seasonal standpoint and purely from the fact that our top buyers are running well-behind last year when it comes to purchases, Japan and China the most notable, with purchases down 59% and 68% from a year ago. But it’s nothing better than the current pace, steady, but still barely enough to meet current USDA projections.

My gut tells me we head down path two, I feel like Brazilian exports have replaced US bushels in a big way and that global end users have known the world market would be in this situation for several months, yet don’t seem overly concerned.

However, Brazil is just now beginning to plant its Safrinha crop, which is responsible for 2/3rds or more of its total production, meaning we have a whole lot of time left to be holding our breath. US production matters as well of course, keeping a risk premium necessary.

Going forward, I think the market remains very aware of the two directions we could take, but with demand able to show up seemingly overnight, the threat of path one will keep us supported well into spring.

In the end, I’ve never felt so torn about market potential than I do right now when it comes to corn. Beans have relatively known fundamentals, with the tight supply situation becoming more of a US issue than a global one in the coming months. Wheat, much the same. But corn, corn is likely to keep me up at night wondering what happens and how to manage it for quite some time.

Read Full Story »»»

DiscoverGold

Wheat Rally Has More Steam

By: Barchart | January 28, 2023

Howdy market watchers! And just like that, we’re already one month into the new year.

For the markets, it has been a rollercoaster start, which likely foreshadows what is to come over the next 11 months.

We appreciate everyone who joined our Sidwell Strategies Marketing Meeting this past week. We had a great turnout and even better conversations about ideas and strategies for the year ahead.

We will be scheduling additional meetings this spring, but as always, feel free to give us a call to discuss insights and ideas for your operation. In addition to market outlook, we talked a lot about break evens and desirable profit levels to consider in making risk management and marketing decisions. Have you ever thought about how much profit you’d like to make, within reason? Of course more is more, but when is enough enough to take some risk off the table? Our team has been pulling historical data to aide your decision making.

We also introduced our Farm Marketing Dashboard to increase your visibility over marketing decisions, what-if scenarios and profit per bushel as actions are taken. Schedule a meeting so that we can introduce this very effective tool to you and your family for the year ahead.

It was a firmer week for agriculture and equity markets while another rocky one for energy contracts. After unjustified technical selling on Monday across grains, it was all up from there for the rest of the week. The US dollar largely chopped sideways holding the January 18th low, but closing lower on the week. US grain exports were strong this week with wheat and soybeans at the top of expectations and corn within expectations. Despite being on Lunar New Year holidays this week, China did purchase US soybeans. This brings China’s purchase of US soybeans to 28.2 million metric tonnes versus 25.4 MMT last year.

Rains in Argentina have continued to pressure soybeans lower. However, there are also rains in the north of Brazil that could delay harvests and may add some underlying support. The recent selloff in soybeans have turned charts looking slightly more bullish after this week’s rebound. Front month contracts are likely to sustain more gains than the November new crop contract. New crop soybean futures closed the week just above $13.51. If we rebound to $13.74 area next week, I believe this is a good area to protect some of your intended acres.

With elevated volatility and premiums higher, selling new crop call options is a good way to lower the cost of downside protection. This goes for new crop corn and wheat in addition to soybeans. Front month corn contracts look much more bullish versus new crop corn with March and May closing above the 200-day moving average. There is a gap above on December corn futures at $5.94 ½ after Monday’s low at $5.83 ¾ exactly held the prior January 12th low.

With Friday’s breakdown in the crude oil market and Argentina rains improving conditions despite indisputable permanent damage in parts of the country, I’m getting increasingly concerned that the $5.95-5.99 on the December new crop contract may be as far up as we get until the next catalyst.

The wheat market was one of the more exciting markets to trade this week for the first time in quite some time. This is amidst welcome moisture across the southern plains largely in the form of snow. That moisture however did not stop the start of short covering by managed funds largely in response to trade headlines. News that Australia’s wheat crop is a new record and likely to result in greater exports created some headwinds early in the week, but couldn’t overcome the news of strong US exports, tensions in the Black Sea and escalating wheat price inflation in China and India.

For the latter, domestic wheat prices in India made new record highs this past week, up seven percent in January alone. Prices last year were up 37 percent following the severe drought. While India’s new crop harvest begins in March with supplies expected to be plentiful, it doesn’t relieve the short-term pinch. There is a similar case in China with the government releasing wheat from reserves.

Chicago and Kansas City wheat contracts posted an inside day on Tuesday after Monday’s selloff followed by a textbook break out to the upside and follow through. Chicago wheat finished Friday with another inside day. Monday’s move will likely see follow through in that direction on Tuesday. KC wheat however made a new high on Friday above Thursday’s high. Both March and May KC wheat contracts closed above the 50-day moving average. July new crop KC wheat basically closed right at the 50-day moving average and within a penny of the prior day’s high.

All else equal, KC wheat charts, in particular, look set to move higher. The $8.75-8.80-level could likely be the next stop. This should be an area for producers to consider downside protection. $8.95 could also be in the cards and we will just have to see how the charts are developing once we’re at $8.80. Again, what is your breakeven and how much (per bushel) do you “want” and “need” to make? We have ideas and so give us a call to get orders ready for this market move.

The cattle market appreciated the early week selloff in feed grains. Feeders made a much needed rebound Monday following on Friday’s turnaround after a 6-session plummet. However, after Monday’s move, the market largely stalled though holding gains to finish out the week.

Tuesday’s semi-annual USDA report on beef cow and calf crop inventory will likely be a market mover. We know that numbers will be tighter, but will the beef cow count in 2022 already be down at 2014 levels or will it take another year? Heifer retention will also be down with the drought far from over and hay supplies down 30 percent across the southern plains. March feeders are likely to stall around $184.00-184.15 as it now looks.

While there are plenty of bulls in the cattle market, I would caution against riding out the next couple of months without protection. This year is definitely different than others, but it is likely to be more volatile as well. Note the FOMC meets this week to decide on interest rates and will announce the decision on February 1st at 1 PM. We are likely to see a 25-basis point increase. Any more than that could see a surprise reaction from the equity market that could transfer through to the cattle market. We will need more fat cattle cash trade this next week to excite live cattle futures.

US GDP for the fourth quarter of 2022 increased at an annual rate of 2.9 percent, compared to 3.2 percent in the third quarter, driven by increases in inventory investment and consumer spending, but offset by declining investment in housing. It is a rare occasion that US and China GDP growth are similar percentages, a sign of the continued toll government reactions to COVID have had on both economies.

Give me a call for strategies to trade these key events coming up before year’s end and get a plan for 2023. If you’re ready to trade commodity markets, give me a call at (580) 232-2272 or stop by my office to get your account set up and discuss risk management and marketing solutions to pursue your objectives. Self-trading accounts are also available. It is never too late to start and there is no operation too small to get a risk management and marketing plan in place.

Read Full Story »»»

DiscoverGold

Today's Futures Heat Map

By: Barchart | January 27, 2023

• Today's Futures Heat Map

Strongest: Lumber, Coffee, Sugar, Nasdaq 100 E-Mini

Weakest: Heating Oil, Palladium, Crude Oil, Silver

Read Full Story »»»

DiscoverGold

Grains Report: Wheat, Rice, Corn and Oats, Soybeans

By: Jack Scoville | January 27, 2023

• WHEAT

General Comments: Wheat markets were higher yesterday and trends are now sideways in all three markets. Big Russian production goes against the difficulty of moving grain from the Black Sea due to insurance requirements, but so far the lack of insurance has not increased demand for US Wheat as the Russian Wheat is still moving. There are still ideas of weak demand and big Russian production that should help foster price weakness in the world market. The demand for US Wheat in international markets has been a disappointment all year and has been hindered by low prices and aggressive offers from Russia. Ukraine is also looking for new business for its crops and Russia is aggressive in the world market as it looks for cash to fund the war. The demand for US Wheat still needs to show up and there is still not enough demand news to help support futures.

Overnight News: The southern Great Plains should get isolated showers. Temperatures should average near to below normal. Northern areas should see scattered snow showers. Temperatures will average near to above normal. The Canadian Prairies should see mostly dry conditions. Temperatures should average above normal.

Chart Analysis: Trends in Chicago are mixed, Support is at 739, 721, and 713 March, with resistance at 760, 766, and 772 March. Trends in Kansas City are mixed. Support is at 842, 828, and 811 March, with resistance at 876, 895, and 901 March. Trends in Minneapolis are mixed. Support is at 885, 876, and 882 March, and resistance is at 925, 930, and 942 March.

• RICE:

General Comments: Rice was higher again yesterday. Futures appear poised to test resistance above the market now. Demand should be a problem for bullish traders moving forward. There is not much going on in the domestic market right now although some Rice moved in Texas at what were called very good prices. Demand in general has been slow to moderate for Rice for both exports and domestic uses.

Overnight News: The Delta should get isolated showers. Temperatures should be near normal.

Chart Analysis: Trends are mixed to up with objectives of 1854 and 1906 March. Support is at 1814, 1801, and 1785 March and resistance is at 1840, 1852, and 1864 March.

• CORN AND OATS

General Comments: Corn and Oats closed higher yesterday. The export demand was solid last week even though demand remains well behind the pace to make USDA objectives. Brazil has been hanging on for its Summer crop but Argentina has suffered through some extreme drought. The Brazil Winter crop is harvested. The Summer crop and gthe Argentine crop is developing under stressful conditions. Weak demand overall for US Corn remains a big problem for the market. There are increasing concerns about demand with the Chinese economic problems caused by the lockdowns creating the possibility of less demand as South America has much better crops this year to compete with the US for sales. China is now moving rapidly to open the economy and allow people to move around with no lockdowns so the demand could start to improve. The improvement might take some time as the Chinese people get Covid, but they should be past this episode in a few weeks and demand might start to improve at that time.

Overnight News:

Chart Analysis: Trends in Corn are mixed. Support is at 673, 669, and 661 March, and resistance is at 685, 689, and 692 March. Trends in Oats are mixed to up with objectives of 386, 391, and 400 March. Support is at 377, 375, and 368 March, and resistance is at 386, 390, and 392 March.

• SOYBEANS

General Comments: Soybeans and the products were all higher yesterday despite the news that Argentina and southern Brazil weather changed to a much wetter pattern over the weekend. More precipitation is expected. Price trends are mw mixed for Soybeans and Soybean Meal as the harvest in Brazil starts to expand in central and northern areas. Current forecasts suggest that the showers currently in the forecast for early this week will make a real dent in the drought. Central and northern Brazil remain in very good condition with scattered showers reported. Production potential for the Brazil is called very strong even with potential problems and losses in the south. Even so, production of less than 150 million tons is possible now although most estimates remain near 153 million tons. Argentine production ideas continue to drop with the drought as planting is delayed and the crops already in the ground are stressed. Production estimates are now closer to 40 million tons than original projections near 50 million. There was news that China has started to ease Covid restrictions after some demonstrations by the Chinese people. Ideas that Chinese demand will improve, but this could take some time as a very large part of the population now has Covid. This has delayed a robust economic return for the country.

Overnight News:

Chart Analysis: Trends in Soybeans are mixed. Support is at 1503, 1474, and 1468 March, and resistance is at 1537, 1548, and 1556 March. Trends in Soybean Meal are mixed. Support is at 453.00, 444.00, and 435.00 March, and resistance is at 463.00, 467.00, and 469.00 March. Trends in Soybean Oil are mixed. Support is at 6000, 5940, and 5850 March, with resistance at 6360, 6470, and 6520 March.

Read Full Story »»»

DiscoverGold

Softs Report: Cotton, OJ, Coffee, Sugar, Cocoa

By: Jack Scoville | January 27, 2023

• COTTON

General Comments: Cotton was moderately higher yesterday and still remains inside the trading range created over the last couple of months. Futures have been stuck in the same trading range since the beginning of November but are showing bad demand fundamentals. Overall, the demand for US Cotton has not been strong. Some ideas that demand could soon increase as China could start to open its economy in the next couple of months were hurt by news of Covid outbreaks in China. Covid is now widespread in China so the beneficial economic effects of the opening are being delayed but these effects should start to be felt as the people there achieve immunity over the next few weeks.

Overnight News: The Delta will get scattered showers and above normal temperatures. The Southeast will see mostly dry conditions and near to below normal temperatures. Texas will have mostly dry conditions and below normal temperatures. The USDA average price is now 85.64 ct/lb. ICE said that certified stocks are now 8,900 bales, from 8,900 bales yesterday. USDA on Thursday morning said that weekly net Upland Cotton export sales were 213,700 bales this year and 6,100 bales next year. Net Pima sales were 5,400 bales this year and 0 bales next year.

Chart Trends: Trends in Cotton are mixed. Support is at 85.60, 83.20, and 82.00 March, with resistance of 89.00, 89.90 and 92.10 March.

• FCOJ

General Comments: FCOJ was higher yesterday. Trends are mixed as the market seems to be falling back into a trading range after making a spike high after the reports were released. Demand should start to improve now with the holidays now over. Historically low estimates of production due in part to the hurricanes and in part to the greening disease has hurt production remain in place but are apparently part of the price structure now. The weather remains generally good for production around the world for the next crop but not for production areas in Florida that have been impacted in a big way by the two storms. Brazil has some rain and conditions are rated good. Mostly dry conditions are in the forecast for the coming days.

Overnight News: Florida should get mostly dry conditions. Temperatures will average above normal. Brazil should get scattered showers and near normal temperatures.

Chart Trends: Trends in FCOJ are mixed. Support is at 201.00, 197.00, and 194.00 March, with resistance at 209.00, 214.00, and 217.00 March.

• COFFEE

General Comments: New York and London closed higher yesterday. The activity in London was diminished as Vietnam and much of Southeast Asia is closed for the Tet holiday or Lunar New Year. Ideas of big production for Brazil continue due primarily to rains falling in Coffee production areas now and as offers stayed strong from Brazil and increasingly from Vietnam. Ideas are that the buy side needs Coffee now. There are ideas that production potential for Brazil had been overrated and reports of too much rain in Vietnam affected the harvest progress. The weather in Brazil is currently very good for production potential but worse conditions seen earlier in the growing cycle hurt the overall production prospects as did bad weather last year. Ideas are that the market will have more than enough Coffee either way when the next harvest comes in a few months.

Overnight News: ICE certified stocks are higher today at 0.870 million70ags. The ICO daily average price is now 164.14 ct/lb. Brazil will get isolated showers in northern areas with near normal temperatures. Central America will get scattered showers. Vietnam will see scattered showers.

Chart Trends: Trends in New York are mixed to up with objectives of 172.00 March. Support is at 159.00, 155.00, and 152.00 March, and resistance is at 169.00, 173.00 and 178.00 March. Trends in London are mixed to up with objectives of 1950 and 2040 March. Support is at 1930, 1910, and 1890 March, and resistance is at 2020, 2060, and 2100 March.

• SUGAR

General Comments: New York and London closed higher yesterday on buying seen in most commodities markets. Rains have returned to much of southern Brazil since the weekend. Cane production prospects should be improved. Good production prospects are seen for crops in central and northern areas. The harvest has been delayed in Thailand. Australia and Central America harvests are also delayed. There is talk that production in India will be reduced this year after some bad weather and reduced yields reported in Maharashtra. Ideas are that India will produce about 34.3 million tons of Sugar this year, about 4% less than the previous outlook.

Overnight News: Brazil will get scattered showers. Temperatures should average near normal. India will get mostly dry conditions and near to above normal temperatures.

Chart Trends: Trends in New York are up with objectives of 2100 and 2160 March. Support is at 2020, 1980, and 1950 March and resistance is at 2080, 2120, and 2150 March. Trends in London are mixed to up with objectives of 573.00 and 603.00 March. Support is at 549.00, 541.00, and 537.00 March and resistance is at 559.00, 562.00, and 565.00 March.

• COCOA

General Comments: New York and London closed higher again yesterday. Weaker demand shown by the grind data that got released last week. Talk is that hot and dry conditions reported in Ivory Coast could curtail mid crop production, but main crop production ideas are strong. Ghana has reported a disease in its Cocoa to hurt production potential there. The rest of West Africa appears to be in good condition. The North American grind was 8.1% lower and the EU and Asian grinds were about 2% lower. Good production is reported for the main crop and traders are worried about the world economy moving forward and how that could affect demand. Supplies of Cocoa are large at ports. The weather is good in Southeast Asia.