News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Some people (ie Canadian's) can still buy it on the EM.

Bingo - fat fingers

On second thought how can this trade while on the Expert market?

Anybody has any info as to why this sudden increase in price.

Only one trade but increase 27,900% on 8000 shares.

maybe someone hit the wrong button, lol.

Interesting for sure, maybe new custodian perhaps… would be nice.

WOW, that's what I call a massive increase in share price!!

Does anybody know what's behind it?

Correct - no longer a custodianship play, just a worthless dead shell entombed in the expert market unfortunately.

Does that mean it is no longer a custodian play?

Should have known given their 1st responses on Twitter and an email were Condescending Chastising of anybody that didn't know all of Nevada law. They were asking on ZHU If one of the other custodians would take this over using the information omni might have received? As far as I can tell this ticker would have no is no debt or old owner challenges.... Low Is float and now almost no market cap. I got out enough to break even but it sucks is that omni presented itself as Experienced

I hope they find this OMNI guy and throw him in jail for the rest of this life!!!!!!!!!

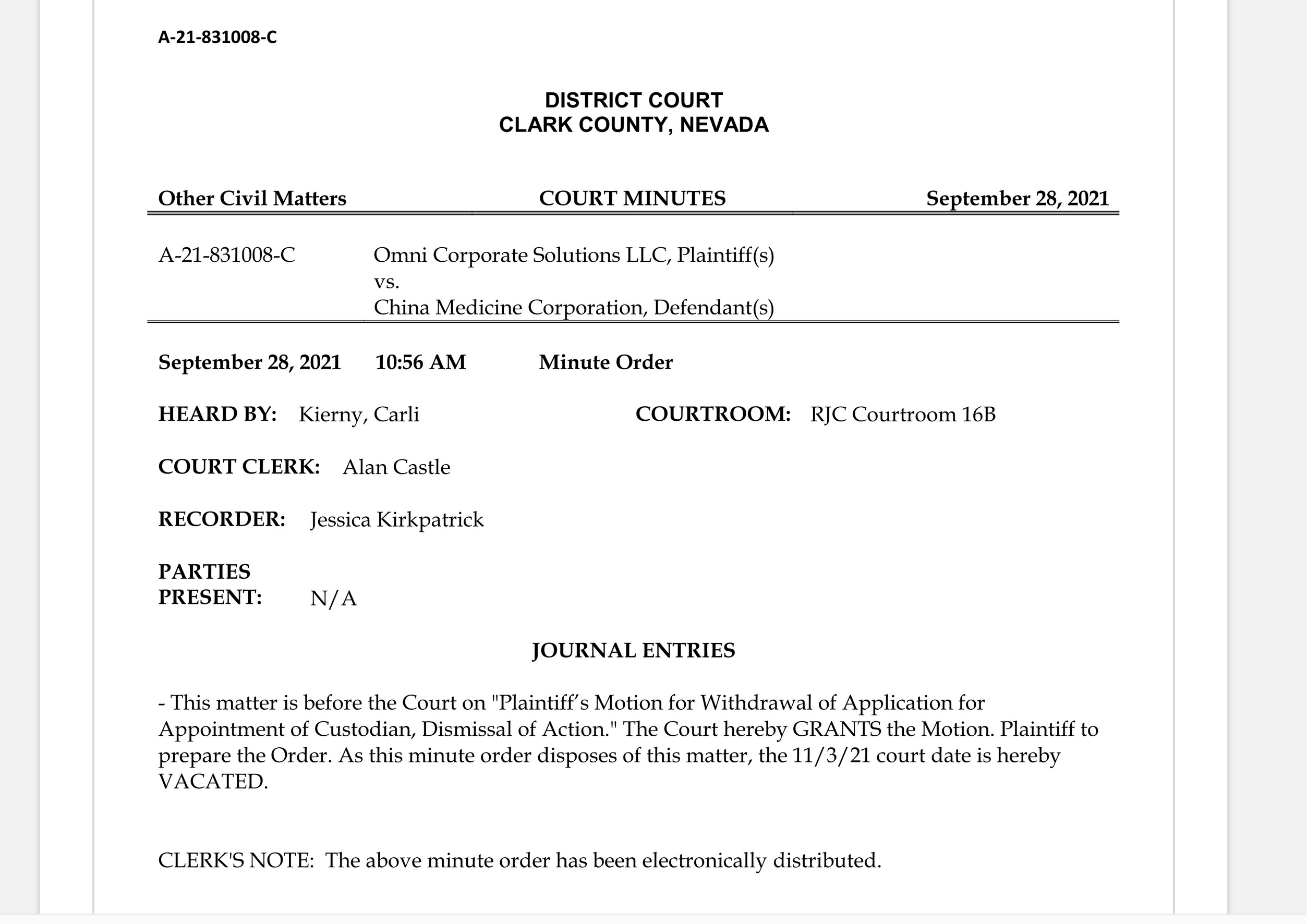

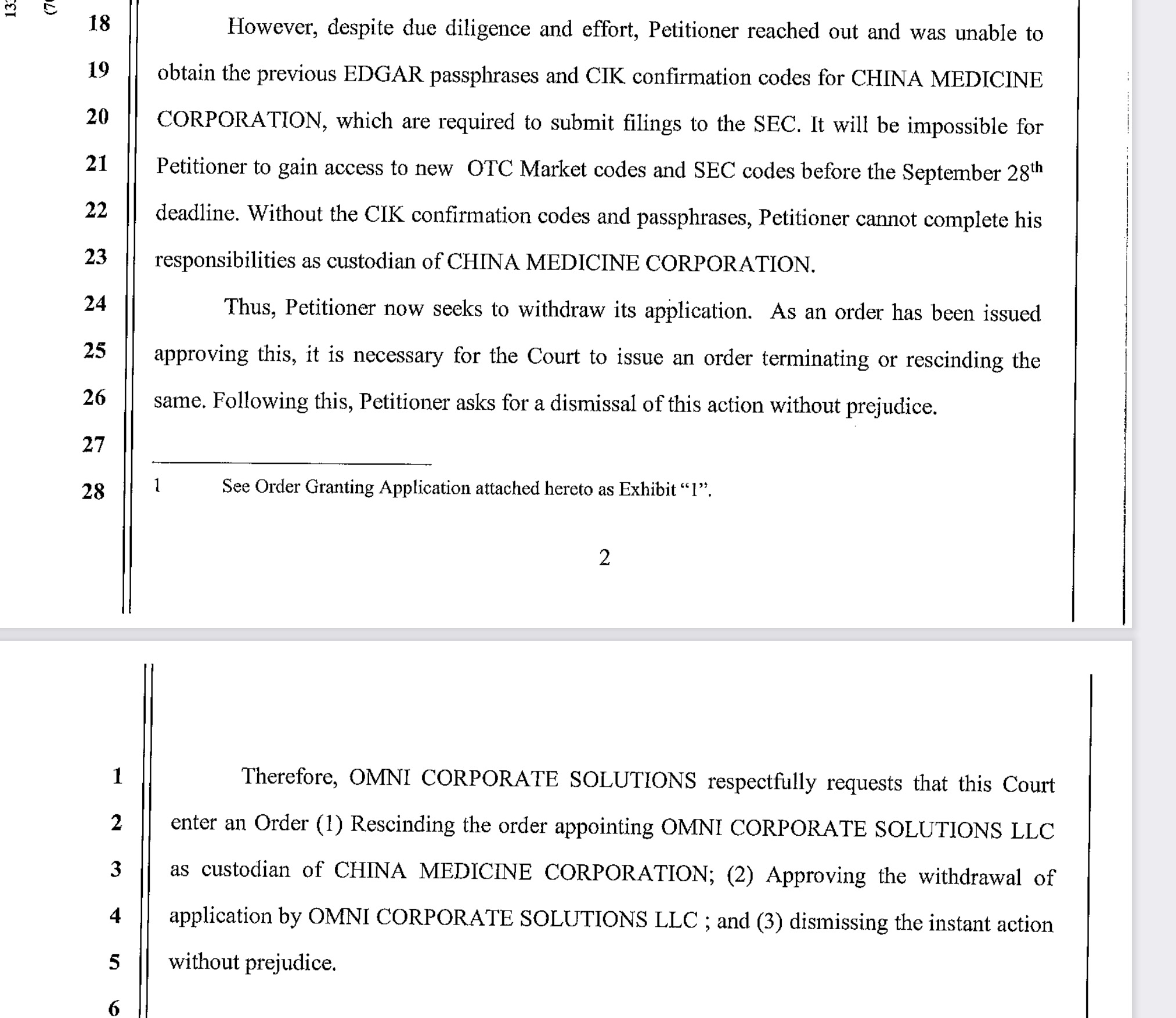

Motion for Withdrawal of Application as Custodian. Welp, that ended exactly as badly as all the months of silence and inaction led us to believe.

finally an update at Clark County Courts, but nothing new that would indicate any tangible progress since May.

I don’t see anything either.

seems to be a lot of activity today.

Was there any news or something posted? I don't see any updates on OTCMarkets.

I know, I added!!!!!!!

Yes I am one of them who are worried and/or upset about the lack of updates.

Let's hope they are telling the truth....

I emailed Omni Corp and they replied telling me they are still working on every ticker. That's all they could say as the SEC is closely watching them. Idk if that helps but I was getting curious myself so I sent the email.Im personally taking the risk and believing them and staying in their tickers. I get why people are worried and/or upset about the lack of updates though.

I guess people still trying to buy will say anything. Talking about needing a update when one just came out and is pinned at the top of the board.

Sadly I agree with you.

Unbelievable - I own a lot of this crap.......

It seems like Omni has disappeared. All their tickets are slowly tanking

Update would be nice. Starting to think he doesn't know what he's doing.

Hopefully the 1st step towards great things.

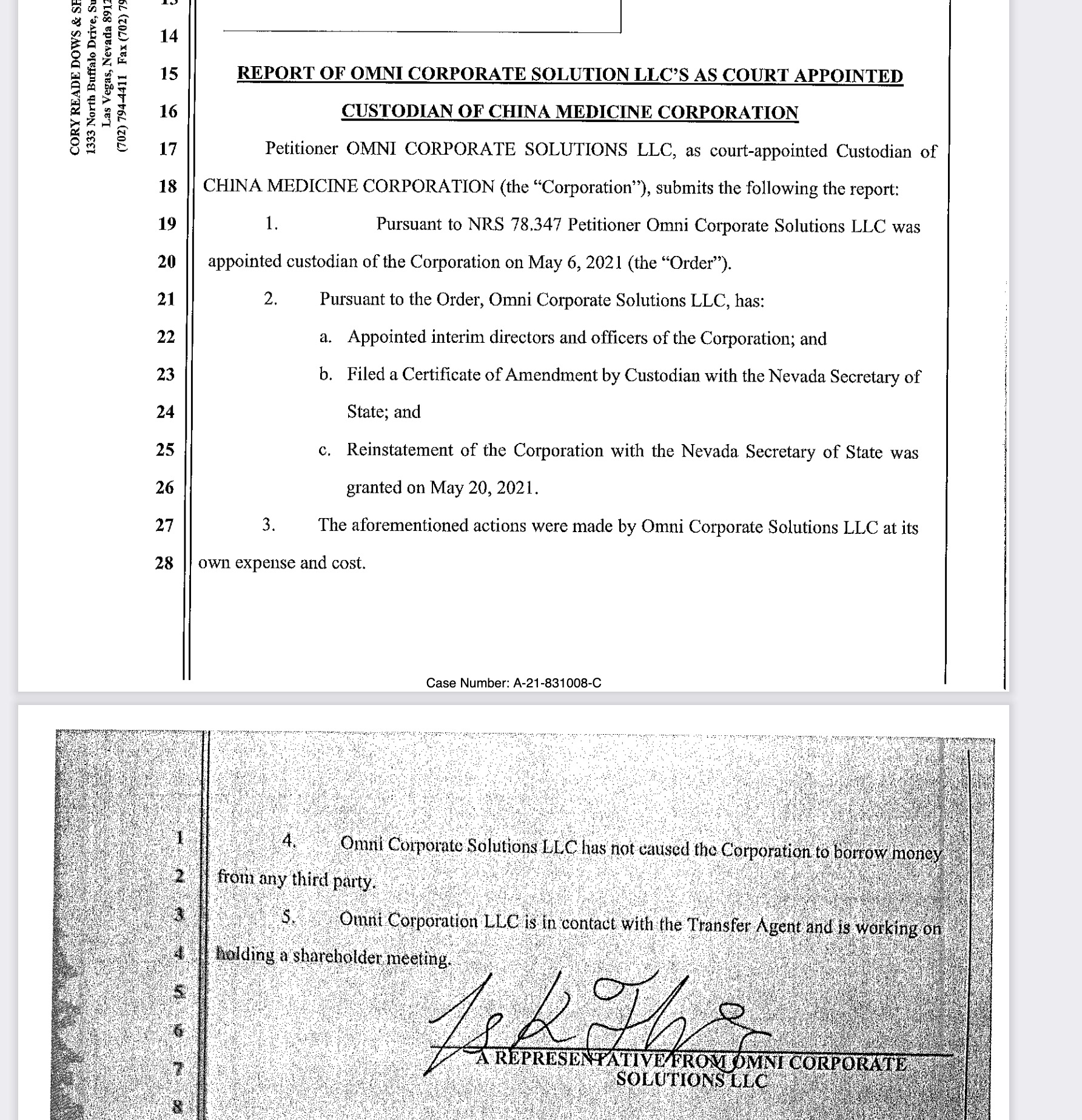

$CHME New officer was just added.

$CHME

— SHORT SQUEEZED (@ShortSqueezed1) May 20, 2021

Officers just added

8 Million float > https://t.co/H1goilIcsh pic.twitter.com/YOfhDflnon

Lol, L2 going crazy, all over the place. $CHME

ROCK N SOCK EM ROBOTS

I have no idea what's going to happen here - these all play out differently, and they're a patience game, the low floaters especially. There's no easy off-ramp when trading in early-stage low float custodianships - you just have to wait it out and see what happens. With any custodianship, it could be weeks, months, or over a year. I get a small position in all the low-float custos I can find if I can get in on the ground floor - some work out, others don't. I'm out of the habit of posting very often on any board unless there's something factual to report (court update, filing, etc.) so I'm going to leave it at that until there's an update on the stock....

GLTA!

H

When you're talking half. a billion cap I would think the number of companies that would reverse merger opposed to IPO or spak etc would be almost non existent.

You think little CHME will pick up some investors soon or will it have to wait until an actual completed merger?

Omni Still silent

That can happen if the wrong company comes in for sure - see recent Lazar shell BRR* for an example.

A very high market cap shell does need a big ticket reverse merger to sustain the price.

Back to an earlier question I was Thinking about. If a new merger company comes in and the exaggerated market cap value Shows the company having a 200 P/E Or other "out there" ratio... New investors would not want to buy because it is perceived to be way overvalued (By that time it not a speculative lotto play)... Wouldn't that eventually lead to A sell off from frustrated investors not seeing gains. Starting out with A falling stock price I can't imagine would be good for any company. Just the crazy kind of things I think of cause on the surface.. It doesnt make sense.

Most custodians don't tweet about their business at all - the "king of SPACs" David Lazar never lets a word out about any of his custodianships outside of court documents and filings with NVSOS, SEC, and OTC Markets. It's frankly better not to discuss pertinent information about stocks on twitter unless one has filed with the SEC to indicate that publicly available information will be made available on social media. Lots of companies and custodians are fudging this regulation and there's been very little enforcement, but really it's best to let the filings do the talking.

That said, Omni was very active on twitter and stocktwits for several weeks and then hasn't had anything to say about any tickers at all since May 4th - that's just a week, so it doesn't seem like a big deal.

There are definitely a lot of things that don't make sense here. Just the fact that if this was one of George's play, It would probly already be up 500%. It also seems like Omni has gone silent for some reason. They never even posted that they got custodianship of C HMP and had that come from someone else. Is that in about self not a good sign for their particular stock custodian ships?

P.s. You've been real good about schooling some of us on Nuances of these trades.

Well, if you look closely at the fundamentals -- especially debt -- of OTC-traded companies, you'll find that clean shells usually have the best balance sheets in pink sheets by a mile. They might not have any revenue, but they're not saddled with millions of dollars in insurmountable toxic debt. As I'm sure you know, pink sheet stock pumpers often use *revenues* outside the context of profitability to come up with wildly inflated valuations, pretending that such valuations are based on fundamentals, when they're clearly not: a company losing millions a year that's just a share selling scam has terrible fundamentals regardless of revenues.

I'd say maybe one out of 500 OTC stocks at best is anything resembling profitable. Old shells like CHME, where the debt is probably invalid due to the statute of limitations expiring, are among the only OTC stocks with potential of a good company coming in and adding value. It's not the norm, but it does happen. But ironically enough, the rare profitable reverse merger companies in the OTCs are often scrutinized for their fundamentals (i.e. "they only made $50,000 in profits this quarter" - BZW* is a good example of this) while train wreck companies with endless millions in convertible debt get higher valuations due to hype/pumps and nothing more. It's all a cesspool, but I do find that clean shells are appealing exactly because they have the chance to start anew with that rare good company that might reverse merge into the shell... Just my opinion...

H

But they had a product, Production, infrastructure Exponential growth sales And were considered the leader in their technology. PLUS, Musk Had already been part of a very successful multi billion dollar company, People assume there was money to keep his operations expanding.

Nobody knows what's going into these things. Most that do are not going to have multi million dollar revenues or profits or have billion dollar Manufacturing facilities. I understand having a high valuation May help a new company but I can also see be a detriment down the road.

Think TSLA! They had NO profit and were worth billions.

In the "real" world market place, MOST Stocks Value Are hypothetically valued based on a price per earnings(or other type) ratio. I realize there are the outliers that defy reasonable ratios but most don't trade beyond A certain multiple range. In theory I hear you saying that these shells can be worth millions if not billions and it doesn't matter. If a new company coming in Ends up being way over valued for its earnings or profit.... Wouldn't that keep the price from increasing for quite a while which could leave it stagnant. It would seem silly for a company with 2 million in annual profit to be trading for a market cap of 100 million.

These reverse mergers do have value though - in some instances a lot of value.

Just because they do not have operations or a current business makes them valuable. They are hopefully a clean shell and companies will pay for that.

Yes, custodian applicants have to be shareholders, but typically if there's front loading of common shares it happens more than a few days before an application.

The custodian sometimes, not always, winds up with the conrol bloc and sells it. Yes, custodians can make a lot of money doing this if the custodianship is successful and if they're able to bring the company current and sell the shell. If there are problems with the shell, their investment in legal, court, and accounting fees is all for nothing. They're far from risk free. Custodians don't give away preferred stock though - a typical clean shell costs the incoming company between $150,000 and $250,000 in cash. Then the formerly private company, which is going public through a publicly traded shell, will grant shares to its stakeholders in the formerly private company. This just makes sense - they're not bringing their private company into the shell just for the benefit of legacy shareholders of the shell.

I don't understand your last question - custodianship stocks are like any other stocks: the price goes up when there are more buyers than sellers, and it goes down when there are more sellers than buyers.

That was a sarcastic commentary on all these reverse mergers that have no value but have 50 million dollar market caps.

I do not pump stocks.......

Everybody here should go around posting and all the other reverse mergers that a large Stock evaluation is preferred... And little old CHME is over here with barely any value in it whatsoever. Come help us to pump this up and make it mergable!!! ;)

My understanding is a custodian has to show financial interest in the company so that's why I'm assuming the price of these stocks shoot up A-day or few before they announce a court date. And you're saying the custodian can sell these preferred or get a commission of sorts for his role. Sounds like these guys doing these reverse mergers are Super duper cleaning up financially on these plays!!! Given the custodian is supposed to have the general shareholder interest at heart. It doesn't seem quite right that he can just give a bunch of preferred shares to just anybody wanting to take this over. Shouldn't it cost the company coming inSomething more given they're going to be given controlling interest? Just doesn't seem quite right, does it?

If the higher valuation is coveted, What's to keep these stocks from being pushed to just increase indefinitely? Is any cap evaluation too much?

|

Followers

|

32

|

Posters

|

|

|

Posts (Today)

|

0

|

Posts (Total)

|

607

|

|

Created

|

11/30/06

|

Type

|

Free

|

| Moderators | |||

| Volume | |

| Day Range: | |

| Bid Price | |

| Ask Price | |

| Last Trade Time: |