News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

>>> Calls Persist for Negative U.S. Yields Even as Fed Signals Pause

Bloomberg

By Vivien Lou Chen

November 3, 2019

https://www.bloomberg.com/news/articles/2019-11-03/calls-persist-for-negative-u-s-yields-even-as-fed-signals-pause?srnd=premium

Belly of curve could go below zero by 2021: BofA’s Braizinha

Moody’s Analytics also raises prospect of sub-zero yields

The Federal Reserve may be hinting at a pause in its policy easing, but Bruno Braizinha at Bank of America Corp. sees a risk that yields on some Treasuries will go negative by 2021 as the U.S. central bank cuts rates all the way to zero.

While that may seem like a remote scenario to some, the strategist says the market can’t ignore the possibility that 5- and 7-year yields -- both presently within a few basis points of 1.60% -- could fall below zero. He says now’s the time to hedge against that prospect.

Braizinha wrote about the risk of sub-1% yields in the U.S. just ahead of August’s historic Treasuries rally, which drove 10-year yields as low as 1.43% on Sept. 3. That rate has since rebounded to around 1.71%, but his central view is that the benchmark yield will go even lower -- to around 1.25% -- in the next three months. In addition to that, he also sees the Fed being forced to return to near-zero rates amid a deterioration in the American economy and an eventual realization by investors that a U.S.-China trade deal won’t be a panacea.

Yields in belly of Treasury curve have fallen over the past year

“It’s important to acknowledge those risks and not overlook these scenarios,” he said by phone. “All the positive sentiment on trade is fading, and what’s changed now is that it’s more likely that at some point the Fed is going to have to cut again.”

A day after the Fed signaled a pause on Oct. 30, yields plummeted across the curve. In Braizinha’s view, the moves reflected a bias that permeated the bond market based on expectations for worsening economic data, lower yields and a flatter curve.

Yields regained some of that ground on Friday amid stronger-than-expected American jobs data and positive developments on the U.S.-China trade relationship, although a poor reading on the Institute for Supply Management’s factory gauge created a slightly more mixed view.

To get to negative yields in the belly of the curve, Braizinha says the Fed would need to push its target to around zero -- from 1.50% to 1.75% currently -- like it did a decade ago in the midst of the global financial crisis. Rates on Treasuries out to around three years would then be “anchored around 10 basis points to 15 basis points” in his view, while demand for dollar duration would send 5- and 7-year yields negative.

The Bank of America analyst, who recommends betting on 30-year Treasuries in anticipation that yields will go much lower, is not alone in contemplating negative Treasury yields.

Ryan Sweet, head of monetary policy research at Moody’s Analytics, said he also sees a risk that Treasury yields could go below zero if the U.S. falls into recession. And, according to him, this could happen even if the Fed doesn’t cut its target below zero.

In the options market, meanwhile, some traders have been hedging in the past month against the possibility of U.S. policy rates heading to zero or even negative levels.

Bank of America currently expects one additional Fed rate cut in the first quarter and “there are still many hurdles to get to negative interest rate policy in the U.S.,” according to Braizinha. One of these is that “it is not clear that it worked as it was intended” in other economies.

“What I find more likely is that we reach a policy exhaustion point where the Fed cuts down to near zero, which requires only six 25-basis-point moves, and the curve continues to be pressured by lower long-term inflation expectations and global duration demand,” he said.

<<<

>>> Fed’s Plan to Buy Treasury Bills Could Be an Expensive Ordeal

Bloomberg

By Alex Harris

October 11, 2019

https://www.bloomberg.com/news/articles/2019-10-11/fed-s-plan-to-buy-treasury-bills-could-be-an-expensive-ordeal

Bank to buy $60 billion of 5- to 52-week securities per month

Short-term investors may be reluctant to part with securities

The Federal Reserve’s attempt to keep U.S. funding markets calm by rebuilding its cache of bank reserves could be expensive.

The Fed said Friday it will begin buying $60 billion of Treasury bills per month -- with maturities ranging from five weeks to a year -- at least through the second quarter of 2020 to improve its control over the benchmark rate it uses to guide monetary policy. It’s the central bank’s latest measure meant to prevent a repeat of the mid-September turmoil that rocked money markets.

But the Fed may have to pay up to convince people to part with the securities since investors are clamoring to hold bills. Money funds’ holdings of them topped $1 trillion in September, according to Peter Crane, president of Crane Data LLC. “Funds love them,” Crane said.

Debbie Cunningham, chief investment officer of global money markets at Federated Investors Inc., said if the company started to sell Treasury bills, it may be from shorter-dated holdings that it can easily invest in the market for repurchase agreements.

“That will be the exception rather than the norm,” Cunningham said in an interview. “They’re going to have to be buying them from other participants.”

Money-market funds continue to see inflows

Money-market reforms from 2016 spurred record inflows into government funds, driving demand for assets like repurchase agreements, Treasury bills and short-term agency debt. Regulations also require daily and weekly liquidity thresholds for money-market funds, and T-bills can satisfy those requirements.

“Everybody’s got bills somewhere, but it’s shaking those out in size that the Fed wants,” said Blake Gwinn, strategist at NatWest Markets. “I’m wondering what kind of premium the Fed is going to have to pay to get them.”

Even though primary dealer holdings of Treasuries are about $190 billion, their T-bill levels are quite low by comparison: around $7 billion. There’s not enough bills to buy just from the primary dealers, and so the Fed is going to have to convince other investors -- like money funds or corporations -- to part with their T-bills.

However, money markets -- particularly the government ones -- need the Treasuries, both as an investment vehicle, but also because they satisfy fund liquidity requirements. Fed purchases could drive yields down. If a money manager’s objective is to generate as much yield as possible for investors, why sell to the Fed at a lower rate? All that’s going to happen is the fund has to reinvest it in bills at a lower rate, reducing the yield the fund offers investors.

In addition to the Treasury bill purchases, the central bank said Friday that it will continue to conduct overnight and term repo operations through January, if not longer. The Fed has done liquidity injections like these since Sept. 17, and they’ve helped calm this vital funding market.

<<<

>>> QE, or Not QE? Impact of Fed Bond-Buying Will Depend on Treasury

Bloomberg

Rich Miller

October 11, 2019

https://www.bloomberg.com/news/articles/2019-10-11/qe-or-not-qe-impact-of-fed-bond-buying-will-depend-on-treasury?srnd=premium

Shift in Treasury sales to bills might depress long-term rates

Powell insists Fed not undertaking quantitative easing

The Federal Reserve insists its planned hoovering-up of Treasury securities is a “technical” measure that isn’t quantitative easing and won’t meaningfully impact the economy. But that may depend on how the Treasury Department responds to the central bank’s plan.

If the Treasury reacts by stepping up its issuance of Treasury bills and cutting back on sales of longer-dated securities, that would tend to put downward pressure on long-term interest rates -- which is exactly what the Fed’s crisis-era QE programs were intended to do.

But if the Treasury keeps its issuance plans the way they are now, then the Fed’s massive buying risks squeezes in the bills market that could push up prices.

“The impact the Fed’s purchases have is dependent on what the Treasury Department does with issuance,’’ Drew Matus, chief market strategist for MetLife Investment Management, said in an email.

“If they boost bill issuance and cut note and bond issuance, it could have a stimulative effect on the economy,’’ said Matus, who once worked on the New York Fed’s open market desk that implements the central bank’s interest-rate intentions.

Fed to ramp up purchases of Treasury bills, but is it QE?

The interplay between the politically-independent Fed and Treasury highlights the difficulties of carrying out monetary policy in a world where rates are low and central banks are more dependent on asset purchases to manage their economies.

A Treasury spokesman declined to comment on what the department intends to do. The Treasury is slated to announce its quarterly refunding plans on Oct. 30, a few hours before the Fed concludes a policy meeting.

The Fed said on Friday that it will begin buying $60 billion of Treasury bills per month to improve its control over the benchmark interest rate it uses to guide monetary policy after turmoil rocked money markets in September.

Purchases will continue “at least into the second quarter of next year,’’ the central bank said in a statement.

“If you stretch purchases into the second quarter, that amounts to at least $400 billion,’’ said Thomas Costerg, senior U.S. economist at Pictet Wealth Management in Geneva.

In foreshadowing the Fed’s decision earlier this week, Chairman Jerome Powell repeatedly maintained that any planned securities buying would not be a resumption of QE.

Not QE

“In no sense is this QE,’’ Powell told the National Association for Business Economics conference in Denver on Oct. 8.

Under quantitative easing, the Fed bought bonds to lower long-term borrowing costs and boost stock prices and the economy during and after the financial crisis.

Powell argued that the Federal Open Market Committee was not out to spur the economy by resuming growth of its balance sheet, as was the case under its crisis-era buying campaign.

Fed to buy $60 billion of Treasury bills per month

Instead, it is responding to last month’s strains in short-term money markets by supplying more liquidity in the form of bank reserves.

As if to hammer that message home, the Fed is creating those reserves through purchases of bills with a maturity of one year or less, rather than buying longer-term Treasury debt, as it did under QE.

“The committee’s apparent concern with how the public would perceive today’s announcement seems heightened enough to conclude that it was a primary consideration in deciding which sector of the Treasury market they would purchase,’’ Michael Feroli, chief U.S. economist for JPMorgan Chase & Co., said in a note on Friday.

Trump Attacks

Some of that concern may also be political. President Donald Trump has repeatedly accused the Fed of keeping monetary policy too tight and at various points has urged it to resume asset purchases.

Some Fed watchers concur with Powell’s assessment of what the Fed is up to.

“This is not QE or even QE lite,’’ Krishna Guha, vice chairman of Evercore ISI, said in an Oct. 8 note. “The central bank is responding to market demand for central bank reserves with minimal duration as it did before 2007.’’

The September scramble for reserves was triggered by a combination of corporate tax payments and the settlement of Treasury debt sales that temporarily sent the rate on overnight securities repurchase agreements as high as 10%.

Wrightson ICAP LLC chief economist Lou Crandall said that a lot depends on how the Treasury responds.

“If they cut coupon issuance, then guess what, this is QE,’’ he said. If the Treasury doesn’t, then it runs the risk of spawning turmoil in the bills market.

“I don’t know which of their allergies give them the worst rash,’’ he said in discussing the Treasury’s options.

<<<

>>> Top Two Threats to the Treasury Market’s Big Year Are Converging

Bloomberg

By Emily Barrett

October 12, 2019

Sell-off puts best Treasuries performance since 2011 at risk

Yields may climb with progress on trade talks, Brexit

https://www.bloomberg.com/news/articles/2019-10-12/top-two-threats-to-the-treasury-market-s-big-year-are-converging?srnd=premium

Two serious threats to this year’s stellar performance in Treasuries are closing in on the market: steps toward a U.S.-China trade deal and a light at the end of the Brexit tunnel.

Treasury yields took flight this week on hints of a partial trade pact, and late Friday President Donald Trump said he and his counterpart Xi Jinping could sign an accord as soon as next month. Prospects for a deal between the U.K. and European Union also looked firmer, as the EU’s chief negotiator signaled readiness to delve into the details of an Oct. 31 exit.

All year, investors have known that the case for Treasuries largely hinged on these major geopolitical quandaries. Now, credible progress on both could catch Treasury bulls seriously offside, and derail a market on track for its best annual return since 2011.

If a worst-case scenario is no longer in play, global growth could improve, the Federal Reserve could be less inclined to ease, and yields in major government bond markets could have more scope to rise.

“There was a decent long in the market that is going to get tested,” said Gary Cameron, portfolio manager at Garda Capital. “I don’t think we have a bear market, but the buy-dips environment we’ve been in since last September is late stage.”

Cameron expects that if this week’s positive signals are sustained, the U.S. 10-year yield could hit 1.90%. The benchmark ended Friday at 1.73%, after rising 20 basis points this week, its second-biggest sell-off this year. Moreover, traders in futures markets have been paring back their wagers on further Fed easing. Pricing of fed fund contracts show that the odds of a cut this month have gone from near-certain to close to a coin flip.

Investors will get plenty of live feedback from central bankers on how they’re viewing the geopolitical landscape next week. Highlights will be toward the back end, with speeches from New York Fed President John Williams and Vice Chairman Richard Clarida, who’s signaled openness to a further easing this year. Both have emphasized the Fed’s data-dependent stance.

Foremost among the potentially market-moving economic reports on the way is retail sales, which investors will watch for confirmation that consumption can continue to support U.S. growth. Economists are looking for Wednesday’s report to show a 0.3% monthly increase in spending for September, slowing from 0.4% the prior month.

“Retail sales will be pretty important,” said Cameron, adding that “the U.S. is the last bastion of reasonable growth it seems in the world right now.”

What to Watch

Monday is Columbus Day, a recommended holiday for the U.S. bond market.

Here’s the economic calendar:

Oct. 15: Empire manufacturing

Oct. 16: MBA Mortgage applications; retail sales; NAHB housing market index; business inventories; Federal Reserve Beige Book; Treasury International Capital flows

Oct. 17: Building permits; housing starts; Philadelphia Fed business outlook; initial jobless claims; industrial/manufacturing production and capacity utilization; Bloomberg consumer comfort; Bloomberg economic expectations

Oct. 18: Leading index

Fed speakers are prevalent:

Oct. 15: St. Louis Fed’s James Bullard; Atlanta Fed’s Raphael Bostic; Kansas City Fed’s Esther George; San Francisco Fed’s Mary Daly

Oct. 16: Chicago Fed’s Charles Evans; Dallas Fed’s Robert Kaplan; Fed Governor Lael Brainard

Oct. 17: Evans, Governor Michelle Bowman; New York Fed’s John Williams

Oct. 18: Kaplan; George; Vice Chairman Richard Clarida

Here’s the Treasury auction schedule:

Oct. 15: $45 billion of 3-month bills; $42 billion of 6-month bills

Oct. 17: 4- and 8-week bills; $17 billion 5-year TIPS reopening

<<<

>>> A $40 Billion Pile of Leveraged Loans Is Battered by Big Losses

By Katherine Doherty

October 9, 2019

https://www.bloomberg.com/news/articles/2019-10-09/a-40-billion-pile-of-leveraged-loans-is-battered-by-big-losses

Sudden drops reflect growing distaste for shakier issues

Energy leads list of losers with $12 billion of loans affected

Barely noticed in a corner of the financial markets, leveraged loans originally worth about $40 billion are staging their own private meltdown.

Loans tied to more than 50 companies have lost at least 10 percentage points of face value in just three months, according to data compiled by Bloomberg. Some have dropped a lot more, with lenders lucky to get back just two-thirds of their investment if they tried to sell.

The list is growing as lenders and credit raters lose patience amid the slowing economy with borrowers that took on mountains of debt to fund private equity buyouts, dividends and other transactions that didn’t improve earnings.

The companies range across sectors, from energy to health care to communications. The biggest losers as of Tuesday included Amneal Pharmaceuticals LLC, whose $2.7 billion loan due 2025 has sunk to about 80 cents on the dollar, and Seadrill Operating LP, whose $2.6 billion loan maturing in 2021 fetches around 53 cents. The biggest losses in terms of total value included Deluxe Entertainment Services Group Inc., whose first-lien loan dropped as much as 77 cents in three months to 12.5 cents -- more than $600 million.

Cuspy Corporations

It’s hardly a full-blown apocalypse for the junk-rated leveraged loan market, which totals $1.2 trillion. But it does reflect a shift in sentiment, and perhaps a latent market risk, as speculation about a recession spurs investors to flee shaky names.

“People want the well-performing loans, and are more wary of taking chances on the situations that have turned negative,” said Andrew Sveen, co-director of bank loans at Eaton Vance Management.

Energy is the hardest-hit sector on the list, with more than $12 billion of loans falling more than 10 cents on the dollar. Consumer and health care follow, comprising around $8 billion and $5 billion of loans outstanding, respectively.

Leveraged Losers

Some of the drops track the slide in a borrower’s financial fortunes, and some were made worse by downgrades to the CCC bucket by ratings firms.

In turn, the downgrades can trigger selling by money managers who are limited from holding such names once they fall below a certain ratings threshold. This includes collateralized loan obligations, groups of loans that asset managers package into bonds. Most CLOs can’t hold more than 7.5% of their portfolios in loans rated CCC.

The CLO market has mushroomed in recent years as investors have clamored for higher yields, and CLOs are the biggest holders of loans to junk-rated companies. Concerns are mounting about how the structures owning so much of corporate America’s debt will react if a recession hits and more downgrades hit.

When now-bankrupt Deluxe Entertainment was looking for a loan to keep it afloat, its lenders, comprised mostly of CLOs, were prohibited from providing the company with more capital because of legal limitations. Their hands were tied after the company was downgraded three notches to CCC- by S&P Global Ratings. Deluxe wound up in Chapter 11 bankruptcy.

<<<

>>> Repo Market Is Telling Washington That Deficits Still Do Matter

Bloomberg

By Liz McCormick and Saleha Mohsin

October 8, 2019

https://www.bloomberg.com/news/articles/2019-10-08/mmt-is-all-the-rage-but-repo-spike-shows-deficits-still-matter?srnd=premium

Bond dealers choke on Treasuries as U.S. goes deeper into red

‘There’s no down time on the supply front,’ FTN’s Vogel says

These days, you’d be hard-pressed to find many people in Washington who are all that worried about the U.S. budget deficit. Republicans seem more interested in tax cuts, Democrats have ambitious spending plans for everything from health care to infrastructure, and Modern Monetary Theory, a manifesto for free-spending governments, is all the rage in progressive circles.

But on Wall Street, bond dealers provided a small, but pointed reminder that, just maybe, debt and deficits do matter after all.

It came in the form of a sudden spike in interest rates for repurchase agreements, or repos, a normally obscure part of finance that keeps the global capital markets spinning. Plenty of factors helped cause liquidity to dry up, but one that’s getting more attention is concern that dealers are starting to choke on Treasuries as the U.S. government goes deeper into the red.

The argument goes like this: Primary dealers, which are obligated to bid at U.S. debt auctions, have absorbed more and more Treasuries to finance the Trump administration’s tax cuts as investor demand has waned. Typically, they rely on repos to fund those purchases by putting up the debt as collateral.

The problem is that with the financial system already inundated by over $16 trillion of Treasuries, banks constrained by crisis-era rules have fewer incentives to participate in repo. Simply put, there was too much new debt flooding the financial system and not enough money, causing lenders to jack up repo rates. The Federal Reserve has moved to inject much-needed cash on a temporary basis, but if left unchecked, the flood of supply in coming months and years could ultimately result in higher borrowing costs for the U.S.

“There’s no down time on the supply front,” said Jim Vogel, a strategist at FTN Financial who’s been following debt markets for over three decades.

The Treasury’s next slate of debt sales comes this week, with a combined $78 billion of 3-, 10- and 30-year auctions starting Tuesday. Yields on the benchmark 10-year note are currently at 1.52%.

Of course, supply wasn’t the only issue. The situation was compounded by corporate tax payments that also siphoned cash out of the banking system.

And to be fair, nobody is suggesting the U.S. faces any imminent problems financing itself. Everywhere you look, government borrowing costs in bond markets around the world are at historic lows. The dollar remains the world’s reserve currency, and with the global economy showing signs of weakness, investors are still likely turn to Treasuries for safe harbor.

Economists Worry That MMT Is Winning the Argument in Washington

Nevertheless, the mid-September repo upheaval is a clear sign there might actually be limits on just how much debt the U.S. can take before triggering more frequent disruptions. Deficits aren’t exactly new, but they do add up. Since the crisis, the market for Treasury debt has roughly tripled in size.

And the fiscal balance has only gotten worse under President Donald Trump. The deficit surpassed $1 trillion in the first 11 months of the fiscal year, which just ended last month. And the Congressional Budget Office forecasts the shortfall this fiscal year will exceed $1 trillion. That all means the Treasury will need to keep increasing its debt auctions to fund the budget shortfalls.

In the coming decade, debt as a percentage of the gross domestic product will reach 100%, CBO estimates show. That would be greater than any time since just after World War II. Before the financial crisis, debt-to-GDP was about 40%.

The growth was more than manageable in the years after the crisis because the Fed bought significant amounts of Treasuries (from dealers post-auction) with its quantitative easing, or QE. Some argue the Fed used QE to “monetize” the debt, which pumped trillions of dollars worth of cheap cash into the banking system and kept U.S. funding costs artificially low. Whatever the case, there’s little doubt the buying helped dealers clear their inventories.

That started to change in late 2017, when the Fed began to gradually unwind those purchases, reduce the size of its balance sheet and drain the excess cash held in bank reserves. The Fed now holds roughly $3.9 trillion in assets, down from $4.5 trillion in January 2015. More than half of the total is in Treasuries.

Without the Fed, which was arguably the biggest buyer of U.S. debt during the QE era, dealers have had to pick up the slack. In May, primary dealers’ outright positions in Treasuries reached an all-time high of almost $300 billion -- more than double what they were the previous year.

What’s more, post-crisis rules have led banks to prefer cash over Treasuries, which contributed to the liquidity issues in repo markets, according to Michael de Pass, head of Treasuries trading at Citadel Securities.

“The Fed has shrunk its balance sheet in a meaningful way, resulting in reduced reserves in the system,” he said. The cash squeeze has “been further exacerbated by increased issuance, resulting in high levels of Treasury collateral settling into the market.”

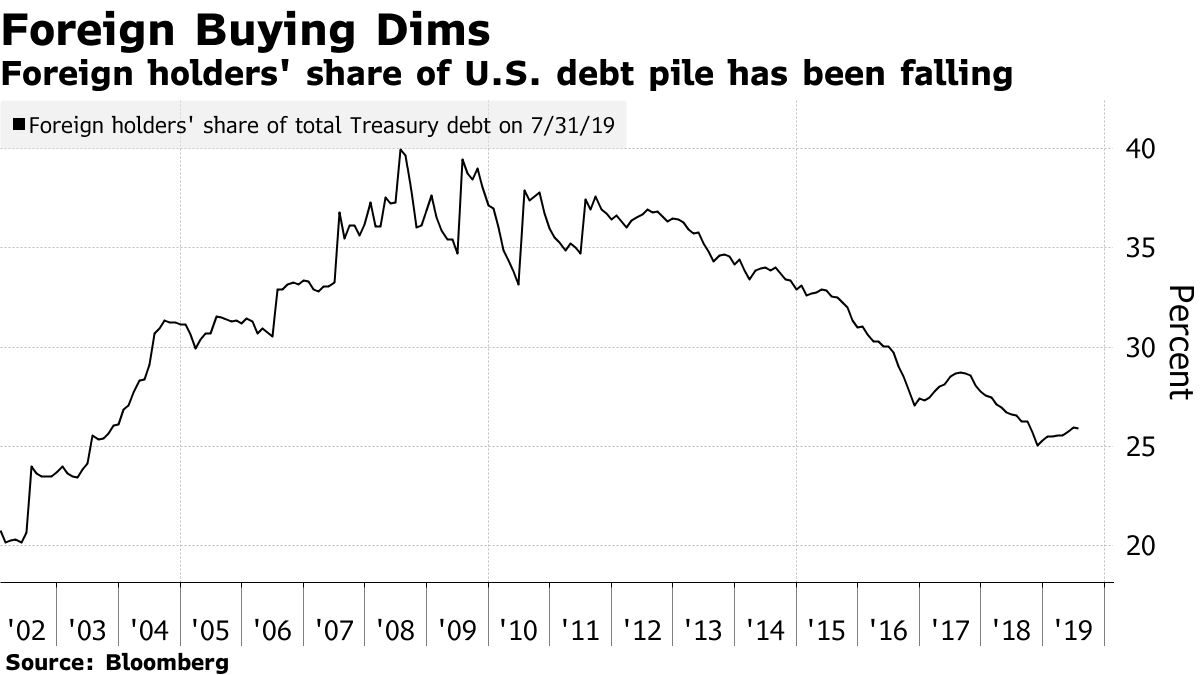

Dealers aren’t getting as much help from foreign investors to soak up all that additional supply. Big creditors like China and Japan have slowed their buying of Treasuries in recent years. Overall, the share of foreign official holdings has shrunk to just over 25% this year, from a high of about 40% in 2008.

Foreign holders' share of U.S. debt pile has been falling

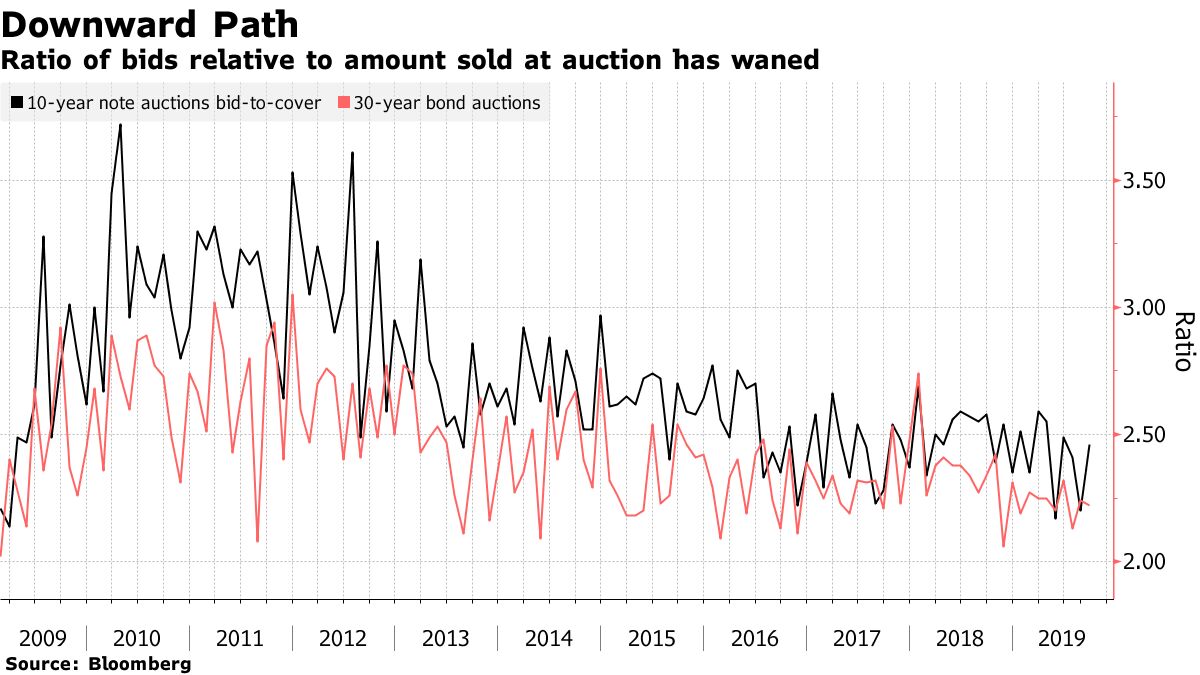

That waning appetite been reflected in the amount of bids investors submit versus the actual amount sold, known as the bid-to-cover ratio.

According to an analysis by John Canavan, Oxford Economics’ lead analyst, the ratio for 3-, 10- and 30-year debt sold each month has fallen to 2.39. That’s down from 2.89 times in January 2018, just before the Treasury began boosting its sales, and far lower than a high of 3.48 times in December 2011.

So-called auction tails, which occur when yields on debt issued at auction exceed prevailing levels in the market at the time of sale, have become more common as well. In layman’s terms, it’s a sign investors need to be paid more to take on new debt. That’s been true especially for longer-maturity debt, like the 10-year note and the 30-year bond.

“The debt has become more difficult to digest as the rise in Treasury issuance is outpacing the rise in demand, and overall there’s been a decline in recent years in foreign demand,” Canavan said.

Ratio of bids relative to amount sold at auction has waned

There’s little to suggest the U.S. will suddenly decide to embrace fiscal restraint, either under Trump or a Democratic administration.

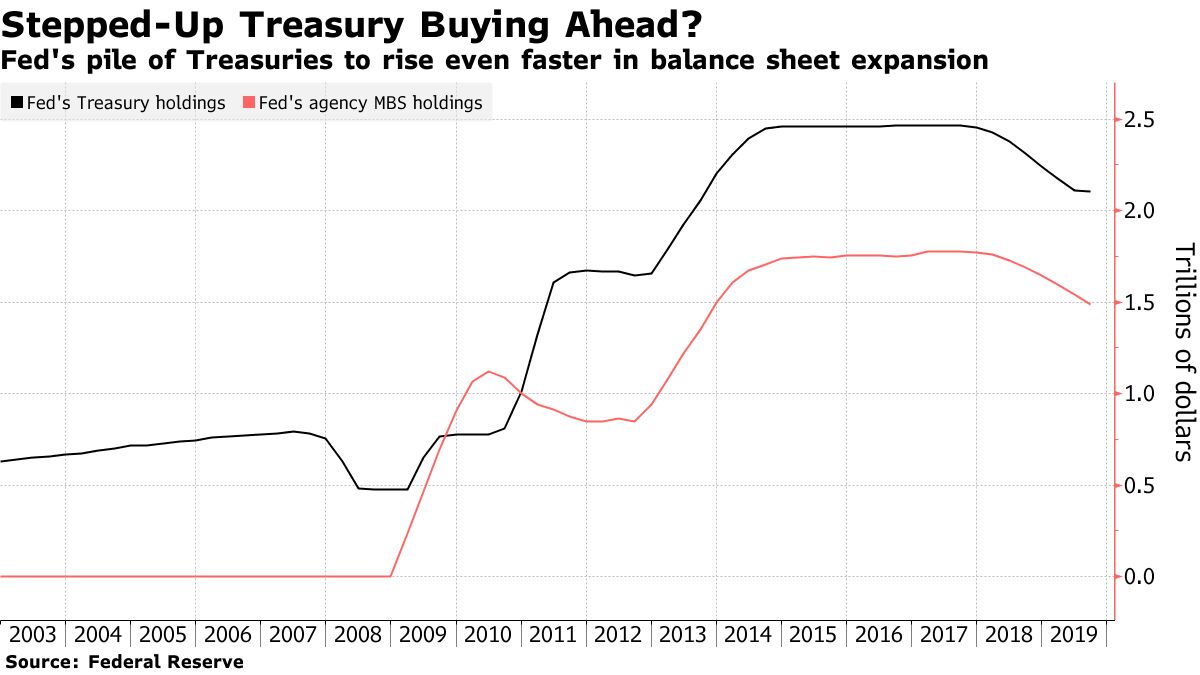

So for many market watchers, the most likely near-term solution to the supply problem is for the Fed to start increasing its debt purchases in a systematic way once more. (Following the recent repo turmoil, the Fed has been providing repo financing on a temporary basis.)

Historically, pumping lots of cash into the system has come with the risk of spurring too much inflationary pressure. But after a decade of ultra-low inflation, that isn’t much of a concern today. The purchases would not only replenish bank reserves and help dealers off-load Treasury collateral, but it would also keep a lid on funding costs as the U.S. runs up the deficit.

Former Fed officials Joseph Gagnon and Brian Sack say the central bank should buy enough Treasuries to build up a buffer of extra reserves, with outright purchases totaling $250 billion over the next two quarters.

“More Fed buying may finally give some relief to the supply issues that the market so needs,” Vogel said.

Fed's pile of Treasuries to rise even faster in balance sheet expansion

When it comes to financing America’s deficit though, it’s not the Fed that Julius Baer’s Markus Allenspach is worried about.

“There’s going to be saturation by investors at some point,” said Allenspach, head of fixed-income research and a member of the firm’s investment committee. “Yes, there is a global search for yield, but we believe we may be past the peak of this hunt for safe assets.”

<<<

>>> CLOs Stuffed Full of Private Debt to Risky Companies Are Booming

Bloomberg

By Lisa Lee

October 2, 2019

https://investorshub.advfn.com/secure/post_new.aspx?board_id=31578

Middle-market collateralized loan obligation assets hit record

Some warn lack of transparency, liquidity puts buyers at risk

It’s a marriage between two of Wall Street’s hottest products.

Collateralized loan obligations -- typically chock-full of broadly-syndicated debt -- are increasingly being stuffed with private loans made to highly leveraged medium-sized companies with limited access to bank financing. Known as middle-market CLOs, the asset class has ballooned to $57 billion, from just $20 billion six years ago. Five new entrants this year -- including Owl Rock Capital and PennantPark Investment Advisers -- suggest issuance is only set to increase.

The frenzied growth is another example of how banks, insurance companies and pension funds continue to reach for higher-paying securities in the face of almost $15 trillion of negative-yielding debt around the world. Middle-market CLOs can offer premiums of as much as 200 basis points versus their garden-variety peers, in part due to the reduced liquidity that comes with direct lending, which bypasses traditional capital markets. Analysts say the products could saddle investors with even steeper losses if credit conditions sour.

“Some investors want the excess return to take on the illiquidity of the underlying middle-market loans,” said Michael Herzig, a portfolio manager at THL Credit. “You can’t trade a middle-market CLO the way you can broadly-syndicated ones. You really have to be diligent and careful when you structure.”

Reaching New Heights

Outstanding U.S. middle-market CLOs have surged to a record $57 billion

About $10.4 billion of new middle-market CLOs have priced this year, according to data compiled by Bloomberg, near last year’s pace, which was the fastest since the financial crisis. Still, that’s dwarfed by about $80 billion of traditional CLO issuance. The $57 billion of middle-market CLOs outstanding compares to more than $600 billion of the conventional variant.

There are plenty of distinctions between middle-market and more typical CLOs that pool syndicated loans. For one, the firms that make the private loans are also the ones that oversee the securitizations. The combination of origination, underwriting and management fees is a potentially lucrative setup.

But the arrangement also means they’re forced to keep a slice of the securities they offer in what is known as risk retention. These are rules intended to align lender and investor interests -- largely to prevent a repeat of the subprime mortgage fiasco.

“In a middle-market CLO versus one in the broadly-syndicated market, the active management isn’t centered on discretionary trading of the loans within the portfolio,” said Vivek Mathew, head of asset management and funding at Antares Capital, one of the largest middle-market lenders with $26 billion of assets. “It’s originating the loans and actively managing the underlying assets from a credit perspective, including working them out if they begin to struggle.”

Major Players

Middle-market loans also tend to carry more safeguards -- known as covenants -- than broadly-syndicated loans, where investors have recently started to push back against some of the riskiest financings.

Only about 30% of middle-market debt is covenant lite, versus 70% to 80% for loans sold to investors, according to Michael Boyle, a managing director at Bain Capital Credit.

On the other hand, the underlying debt in middle-market CLOs tends to be smaller in size, as many borrowers have annual earnings of $100 million or less. That makes the debt significantly less liquid compared to traditional loans. In addition, it makes the CLO bonds themselves harder to sell.

“If you decide you don’t like what the CLO manager is doing, you’ll pay a higher price to exit the position,” said Dave Preston, a CLO analyst at Wells Fargo.

The anatomy of a CLO: A look inside the deals funding corporate America

Many of the new entrants issuing middle-market CLOs are already major players elsewhere, including business development company FS KKR Capital and conventional CLO manager THL, which sold its first middle-market securitization in March.

The A rated chunk of Bain Capital’s middle-market collateralized loan obligation from August pays an interest rate of 3.6% over the London interbank offered rate, according to data compiled by Bloomberg. The similar-rated tranche of its most recent conventional CLO from September yields 2.85% over the benchmark. Corporate bonds with comparable rankings pay an average of about 2.64%, according to Bloomberg Barclays index data.

Still, some are steering clear of middle-market CLOs given the difficulty conducting due diligence on the underlying companies. Investors have good reason to be wary, according to Jason Merrill, an investment specialist at Penn Mutual Asset Management, which oversees about $28 billion, largely on behalf of insurers.

“One of the lessons we were supposed to learn from the financial crisis is that it’s important to understand the collateral and understand the risks,” Merrill said. “We do deep analysis when we look at credits, and that’s harder to do with middle-market CLOs,” he said, adding that it has “caused us to shy away from the middle-market space.”

That’s why it’s critical for investors to choose a firm whose lending and management approach aligns with their own, according to Bain Capital’s Boyle.

“There’s less collateral overlap than in the broadly-syndicated market,” said Boyle. “Finding the right asset manager really matters.”

For now, there’s little sign of a supply slowdown anytime soon. Middle-market lenders say CLO issuance is an increasingly popular source of term financing as they seek to expand their private-credit business. And fundraising for North America-focused direct lending is booming.

New money reached $6 billion in the third quarter, bringing this year’s total to $22.6 billion, according to London-based research firm Preqin. That compares to $16.2 billion a year ago. Fundraising typically jumps in the fourth quarter, and cash raised may come close to the record $36.3 billion of inflows in 2017.

“There’s been more competition but there’s still growth opportunity in direct lending,” said Craig Packer, co-founder of Owl Rock, which manages $13 billion of assets. We’ve seen investor appetite for our CLOs, and we expect to do more.”

<<<

>>> Wall Street Falls in Love Again With Companies Loaded Up on Debt

Bloomberg

By Sarah Ponczek and Molly Smith

September 29, 2019

It’s a victory of sorts for the Fed as officials cut rates

Inexpensive financing will help most indebted companies

https://www.bloomberg.com/news/articles/2019-09-29/wall-street-falls-in-love-again-with-companies-loaded-up-on-debt?srnd=premium

The Federal Reserve’s new round of interest-rate reductions just might be working. At least, that’s what one obscure, but key, stock market indicator suggests.

For the first time since 2016, companies with fragile balance sheets are outperforming their sturdier peers and the broad market, a pair of Goldman Sachs indexes show. That’s a clear sign that the rate cuts are shoring up investor confidence in heavily indebted companies -- the segment of corporate America that’s perhaps most at risk to any downturn that hits the U.S. economy.

The outperformance is so stark that a pure measure of leverage is the top equity factor this year among 10 styles tracked by Bloomberg. It’s a big turnaround for traders who had recently pushed relative valuations for financially solid firms to a 16-year high.

The change in heart comes as the Fed seeks to stoke growth by reducing borrowing costs, reacting to signals that the U.S. economic expansion is slowing. With long-term Treasury yields reaching a record low last month, investors may be betting that all that inexpensive debt financing will help those companies expand and drive future earnings growth.

“Money is a lot cheaper to borrow and close to free in some cases,” said Sylvia Jablonski, the head of capital markets at Direxion, which manages $13 billion. “As long as that goes into the investment of the firm and helps the firm grow and increases capex in a positive way, then I think it could be something that’s positive for those firms.”

Companies with weak balance sheets have outperformed sturdier peers

Take the performance of Edison International and Carmax Inc., for example, members of the S&P 500 Index with some of the highest ratios of net debt to earnings, according to data compiled by Bloomberg. Both are up more than 30% this year, trouncing the S&P 500’s 18% return.

That’s not to say there’s hasn’t been a ton of hand wringing about soaring corporate debt levels and the fallout to come when things go south. Even the Fed’s rate cut, while helpful in the short term, runs the risk of merely delaying the reckoning that will surely arrive for overzealous borrowers.

Goldman Sachs pointed out that net leverage -- which measures how much companies owe for every dollar of earnings after subtracting cash on hand -- for the median company in the S&P 500 spiked to a record in the second quarter. JPMorgan also flagged growing debt levels this month as a risk, saying leverage metrics are worsening.

But rather than fret, equity investors are taking a chance on riskier firms. A Goldman Sachs basket of companies with weak balance sheets has bested a gauge of strong balance sheet firms for four straight months. Up 20% year-to-date, the group of firms with more fragile finances is on track to beat the S&P 500 for the first time since 2016.

The U.S. economy is growing at a pace above interest rate levels

One reason for the faith? Extremely low borrowing costs. A divided Fed cut interest rates for the second time in two months on Sept. 18, reducing its federal funds target by a quarter percentage point to a range of 1.75% to 2%.

Interest rates in the U.S. aren’t high compared to the pace of economic growth, a dynamic that means companies should be able to easily meet debt payments, according to Joseph LaVorgna, the chief economist for the Americas at Natixis.

“If yields remain under nominal activity, a broad-based pickup in corporate defaults is unlikely,” he wrote to clients this month.

Companies have been on a refinancing tear in September, issuing bonds with lower interest rates and buying back more expensive securities. The U.S. investment grade market, with about $155 billion priced this month, has already surpassed last September’s total, and more companies are looking to refinance with borrowing costs still low.

Of course bond investors are still being selective. In recent weeks, riskier companies have been forced to either offer higher interest rates or dangle sweeteners to drum up demand. At least four planned sales this month have been yanked from the market entirely.

Investment-grade and high-yield corporate borrowing costs near record lows

The latest bout of strength in highly levered stocks may also be evidence of a trade gone too far instead of any particular love for finance chiefs who have borrowed a lot.

Earlier this year, valuations of firms with healthy finances versus those of their weaker peers had reached some of the highest levels since 1980, and Goldman Sachs said the phenomenon was due for a reversal amid more accommodative monetary policy.

And of course not all investors are keen on highly leveraged stocks. Sandy Pomeroy, manager of the Neuberger Berman Equity Income Fund, is sticking to companies with “squeaky clean” balance sheets. Whittier Trust, with $13.5 billion of assets under management, has a bias toward high quality growth shares.

“Leverage is not a winning stock picking attribute,” Sandip Bhagat, Whittier Trust’s chief investment officer, said in an interview at Bloomberg’s New York headquarters. “The higher the leverage, the lousier the fundamentals, the lower quality the company is depicting. Don’t get tricked by it.”

But Barbara Reinhard, head of asset allocation for multi-asset strategies at Voya Investment Management, and Michael Kelly, global head of multi-asset at PineBridge Investment, both pointed to a thawing of trade tensions between the U.S. and China as supportive for highly indebted companies.

“A more predictable trade environment will lead to better business conditions, so you have some deeper pockets of credit and the stock market finding buyers,” said Kelly, whose firm manages $97 billion. “It’s a little safer to wander out in the waters.”

<<<

>>> Why I'm Worried About the Repo Market

It’s hard to predict how the financial system will handle shocks.

Bloomberg

By Narayana Kocherlakota

September 25, 2019

https://www.bloomberg.com/opinion/articles/2019-09-25/why-i-m-worried-about-the-repo-market

(Narayana Kocherlakota is a Bloomberg Opinion columnist. He is a professor of economics at the University of Rochester and was president of the Federal Reserve Bank of Minneapolis from 2009 to 2015.)

The recent unrest in money markets, which briefly caused short-term interest rates to get out of the Federal Reserve’s control, won’t undermine the central bank’s ability to achieve its longer-term economic goals. That said, it does signal that something’s very wrong with the financial system.

To understand what’s going on, let’s return to a simple model. Suppose there’s only one big bank. It has a choice of what to do with most of its assets: It can keep them on deposit at the Fed, earning the interest rate that the central bank pays on excess reserves; or it can take more risk and earn more return by investing in securities or loans. In this world, all the assets earn the same “risk-adjusted” return, which the Fed effectively determines by setting the interest rates on excess reserves.

Now let’s take a step closer to reality. There are two groups of banks, “tight” ones that hold few excess reserves, and “flush” ones that hold a lot. Flush banks can lend reserves to tight banks in the federal funds market, a focal point of the Fed’s monetary policy. As long as this lending happens freely, all assets will still have the same risk-adjusted return, and the one-bank model will still be a good indicator of how the many-bank world will respond to the Fed’s policies and to various shocks.

In recent days, though, that crucial free-lending condition hasn’t held. On the contrary, a convergence of events -- a deadline on corporate-tax payments and the settlement of a big Treasury auction -- created a sudden and severe shortage of reserves. As a result, interest rates diverged sharply in markets where they should be the same. In the repo market, where participants borrow and lend against the collateral of Treasuries and other securities, they shot up above 5%. And in the federal funds market, they breached the upper bound of the Fed’s 2%-to-2.25% target range.

The deeper issue is that, since the 2008 crisis, regulatory reforms -- such as requirements that banks hold a certain amount of liquid assets, and maintain a minimum leverage ratio (equity capital as a percent of total assets) -- have constrained the ability of flush banks to lend, and of tight banks to borrow. Such constraints interact in complicated ways with financial market conditions. For example, European banks must report their leverage ratios as of the last day of each quarter, so they reduce their repo activity to make those ratios look better. As a result, even when excess reserves seem abundant, funding costs for banks may exceed the interest rate that the Fed controls.

This isn’t necessarily a problem for the Fed’s monetary policy, because the central bank can inject cash into various markets to bring interest rates into line. That’s precisely what the Fed has been doing in the repo market. And it can make the fix more permanent by creating what’s called a standing repo facility, which means the Fed will inject sufficient funds every day, as needed, to ensure that the federal funds rate stays in what it deems the appropriate range.

What’s harder to understand is how money markets will respond to future shocks. As the experience of the past couple weeks has shown, the simple single-bank model no longer works. Reserves are siloed in the flush banks, so the financial system is acting more like it has $1.3 billion in excess reserves than the actual $1.3 trillion. The design of regulation has disrupted some of the system’s most basic functions. The people who oversee it all should be far from sanguine about what the repercussions might be.

<<<

>>> Repo Market’s Liquidity Crisis Has Been a Decade in the Making

Bloomberg

By Liz McCormick, Matthew Boesler, and Craig Torres

September 22, 2019

https://investorshub.advfn.com/secure/post_new.aspx?board_id=31578

It sounds crazy: even National Public Radio is talking about repo rates.

In normal times, not even Wall Street thinks too much about the arcana of short-term money markets.

But over the past week, the Federal Reserve has had to work unusually hard to rein in a key policy rate after overnight repo lending dried up. Suddenly, everyone is asking the same question: what does it mean?

The answer is sobering. Despite assurances by the Fed and others to the contrary, the stress in the market for repurchase agreements, or repos, has exposed some fundamental weaknesses in the nation’s financial system which have been a decade in the making. While they don’t pose a significant problem during good times, the risk is clear: without a permanent fix, sudden cash shortages could lead to broader financial market turmoil in a downturn.

“The machine of liquidity management is just not oiled anymore,” GLMX Chief Executive Officer Glenn Havlicek, who runs a trading platform for repo securities and has four decades of experience in funding markets.

The repo market is important because it serves as the grease that keeps the global capital markets spinning. In a repo, firms borrow cash from each other by putting up securities like Treasuries as collateral. When the agreement expires, the borrower “repurchases” the collateral and returns the cash, though in practice repos are often rolled over day after day.

Hedge funds often use repos to finance purchases of higher-yielding assets, while dealers that are obligated to bid for Treasuries at U.S. debt auctions use them as a way to avoid putting up their own capital.

Participants point the finger at two structural changes that have drained too much cash from the system and made the repo market more prone to seizing up: crisis-era monetary policies and financial regulations designed to curb risk-taking. They contend that those two forces, rather than a mere confluence of technical factors, are what’s really behind this past week’s disruptions.

The first has to do with the unwinding of the Fed’s quantitative easing program, or QE. Simply put, after buying trillions of dollars of bonds to pump cheap money into the banking system, the Fed reversed course and started reducing its holdings (and thus draining cash) in October 2017 as the economy strengthened. It stopped altogether last month.

Fed was forced to temporarily expand balance sheet after 1.5-year unwind

The problem is that, in reducing the asset side of its ledger, the Fed has also had to shrink its liabilities to balance its balance sheet. Those liabilities consist of currency in circulation, which has naturally increased with the economy, and bank reserves, which have fallen.

Of course, that in itself wouldn’t be enough to cause a scarcity of cash in the banking system since firms in aggregate still have over a trillion dollars in reserves. But because of post-crisis rules such as Dodd-Frank and Basel III, banks have been forced to set aside much of those same reserves to meet the more stringent requirements, putting a strain on the available cash they can use. What’s more, capital constraints have made taking large positions in short-term money markets far less lucrative.

“The Fed wanted the market to restructure to a new equilibrium and institutions to figure out how to fund themselves,” said Julia Coronado, president of Macropolicy Perspectives. But “if you have an excess reserve system, you are by definition a primary source of liquidity. And when you squeeze funding markets, you are usually squeezing hedge funds and other investors that may have to cut positions which can spark broader volatility.”

JPMorgan CEO Jamie Dimon summed up the conundrum last week, saying that “banks have a tremendous amount of liquidity, but also have a tremendous amount of restraints on how they use that liquidity.”

The swelling U.S. deficit caused by President Donald Trump’s tax cuts hasn’t helped matters. For one, the money that investors and dealers lend to the government in the form of bond purchases takes money out of the banking system. For another, dealers at Treasury auctions have increasingly turned from lenders to borrowers in the repo market to absorb the additional supply. This year, net issuance will reach roughly $1.2 trillion, after $1.3 trillion last year, according to JPMorgan. In 2017, it was less than half that.

Growing budget deficit pushed inventories of Treasuries to record highs

Those liquidity constraints came into full view over the past few days when corporate tax payments, big Treasury auctions and maneuvers by financial firms to manage their capital requirements prior to quarter-end drained cash available for repo transactions. The overnight lending rate quickly shot up to 10% and the Fed temporarily lost control of its benchmark rate.

In the past, the Fed has disputed the idea that its balance-sheet unwind left bank reserves in short supply. And at his post-policy news conference on Sept. 18, Fed Chairman Jerome Powell sidestepped questions about whether he felt bank regulations were a catalyst for the market turmoil.

Instead, the Fed has opted for a temporary fix. On Friday, the New York Fed announced a series of overnight and term operations over the next three weeks to boost short-term liquidity. That follows four straight days of repo transactions, something it hasn’t done in a decade.

A number of investors, strategists and at least one former Fed official have come out to warn that more may need to be done.

“Maybe we have gotten some hints that reserves are no longer ample,” said Michael Feroli, JPMorgan’s chief economist. “The longer the Fed goes without making changes, the more often you might have these type of incidences.”

Earlier this year, TD Securities’ Priya Misra predicted the Fed would have to resume its bond purchases as a permanent solution. She says this past week’s events have convinced many of her skeptical clients to come around to the idea. They are now asking her “how much” the Fed will need to buy.

While no decisions have been made, Boston Fed President Eric Rosengren acknowledged last week that permanently expanding the Fed’s balance sheet is one option on the table and the one he personally prefers. (The other two being continued ad-hoc interventions or a so-called standing repo facility, which would make cash loans available on a daily basis.)

Growing the balance sheet might also be the easier one, particularly after the New York Fed stumbled out of the gate as it tried to come to the rescue on Tuesday, says GMLX’s Havlicek.

“The repo market isn’t used to being prime time,” in terms of liquidity management, he said. And, the Fed is “out of practice.”

<<<

Back to QE - >>> Potter Warns Fed May Have to Buy More Debt to Calm Market

Bloomberg

By Matthew Boesler and Alex Harris

September 20, 2019

https://www.bloomberg.com/news/articles/2019-09-20/potter-said-to-warn-fed-may-have-to-buy-more-debt-to-calm-market?srnd=fixed-income

Former head of NY Fed’s trading desk speaks with BofA clients

Recommendations go beyond New York Fed’s announcement Friday

A former top Federal Reserve official, who oversaw the U.S. central bank’s trading desk, has warned that the type of actions taken so far to quell this week’s turmoil in money markets may not be enough to keep conditions calm and fresh debt purchases may be needed.

Simon Potter, the former New York Fed executive, made the remarks during a conference call that Bank of America hosted for its clients, according to three people who listened.

Potter cautioned that policy makers may have to expand the central bank’s balance sheet through outright purchases of U.S. Treasury securities, to ensure stable liquidity conditions at the end of the quarter as well as at year-end, said the people, who declined to be named because the call was private.

The recommendation follows a week of intense upheaval in money markets during which short-term interest rates spiked and pulled the Fed’s policy benchmark rate outside its target range. It also goes beyond what the New York Fed has promised so far to keep the situation in check going forward.

A spokeswoman for the New York Fed declined to comment on Potter’s remarks. Potter and Bank of America also declined to comment.

The reserve bank announced later Friday that it would offer so-called term repurchase agreements over the upcoming quarter-end, which would allow financial institutions to borrow cash from the Fed either overnight or for two-week periods, secured by Treasury collateral.

Potter was abruptly dismissed in May by New York Fed President John Williams, who assumed the top post at the bank in June 2018. The departure of Potter, a 21-year veteran of the institution, raised concerns about Williams -- a widely-respected monetary economist -- because of his relative lack of experience with financial markets. The New York Fed has yet to announce Potter’s successor.

The New York Fed was forced to intervene in money markets with overnight cash loans for the first time in a decade on Tuesday, Wednesday, Thursday and Friday to contain short-term interest rates. Surges in the rate on overnight repo loans normally occur only at quarter-end and sometimes month-end.

This mid-month jump was attributed to a confluence of events that knocked cash reserves in the banking system out of balance with the volume of securities on dealer balance sheets: a corporate tax payment date, settlement of last week’s Treasury auctions, and last week’s bond-market sell-off, in which investors sold securities back to dealers.

From the beginning of last year to July, the Fed partially unwound the $4.5 trillion portfolio of bonds it had amassed in the years following the financial crisis. The reduction drained cash reserves from the banking system.

This week’s turmoil raised questions about whether the Fed went too far in removing cash from the financial system, and focused attention on when the central bank would begin resuming balance-sheet expansion to keep pace with the needs of a growing economy.

“We’re going to be very closely monitoring market developments and assessing their implications for the appropriate level of reserves and we’re going to be assessing, you know, the question of when it will be appropriate to resume the organic growth of our balance sheet,” Fed Chair Jerome Powell told reporters Wednesday after the central bank cut interest rates for a second time this year.

“It is certainly possible that we will need to resume the organic growth of the balance sheet earlier than we thought,” Powell said.

<<<

>>> Get a Grip. The Fed Can Handle the Repo Market

The central bank has plenty of options.

Bloomberg

By Bill Dudley

September 20, 2019

https://www.bloomberg.com/news/articles/2019-09-20/how-the-fed-can-handle-the-repo-market?srnd=premium

Chill out.

Bill Dudley is a senior research scholar at Princeton University’s Center for Economic Policy Studies. He served as president of the Federal Reserve Bank of New York from 2009 to 2018, and as vice chairman of the Federal Open Market Committee. He was previously chief U.S. economist at Goldman Sachs.

One of the world’s most important interest rates has had a tumultuous week. Thanks to a sudden shortage of dollars in a separate market, the federal funds rate – the focal point of the U.S. Federal Reserve’s monetary policy – briefly breached the 2%-to-2.25% range that the central bank was targeting.

The aberration has generated a lot of concern. My advice: Don’t worry, the Fed can handle it.

Let’s start with what happened. The cash crunch occurred in a large and central piece of the financial system -- the “repo” market, where participants borrow and lend money against the collateral of various securities. Banks, hedge funds and other investors use it as a source of funds to buy U.S. Treasuries and other assets. Corporations and money-market funds use it as a safe place to park cash and earn a return.

Early this week, a confluence of events threw the repo market out of whack. First, until last month, the central bank had been paring down the securities portfolio it built up after the 2008 crisis, and this process had been soaking up the cash reserves that banks keep on deposit at the Fed. Second, a September 15 deadline for paying corporate taxes further depleted reserves. Finally, the settlement of a large Treasury auction created added demand for cash to pay for the government securities. When the cash flows into the Treasury’s account at the Fed, this drains reserves from the banking system. The imbalance of supply and demand caused repo rates to spike above 5% on Tuesday, more than double the level of the previous week. This, in turn, affected rates in the federal funds market, where banks lend reserves to one another.

The incident is not a harbinger of deeper market problems or a larger crisis. Rather, it provides a useful signal for the Fed, which has been seeking the right level of reserves for the smooth functioning of financial markets. For a long time, this wasn’t an issue: The Fed’s securities purchases, known as quantitative easing, had ensured that the supply of cash was always more than needed. Now, though, as the central bank has reduced its holdings, it’s discovering that various changes have increased the amount of reserves that banks want to hold. These include liquidity regulations, which require banks to hold more cash-like assets, and the Fed’s decision to pay interest on reserves, which makes it less costly for banks to leave cash parked at the central bank.

So what should the Fed do? It has a number of options, some of which will take longer than others to implement.

The primary short-term fix is what the Fed has already been doing: providing the cash that the market needs. Specifically, the New York Fed’s open market desk has increased the supply of reserves by lending money against securities in the repo market. This is one way that the desk can help ensure that the federal funds rate stays within its target range. The Federal Open Markets Committee in Washington D.C. sets the target, and the New York Fed is supposed to hit it. When this doesn’t happen, that’s a problem. I experienced this first hand when I was the System Open Market Account Manager during the financial crisis.

Another short-term fix is to reduce the rate that the Fed pays on reserves. On its own, this won’t address the imbalance in the repo market. But it will help prevent the pressure on repo rates from pushing the federal funds rate above the top end of the Fed’s target range. The Federal Open Markets Committee did this on Wednesday, when it lowered the interest rate on reserves by 0.30 percentage point - 0.05 percentage point more than it lowered its target for the federal funds rate.

One longer-term fix is for the Fed to boost its securities holdings more permanently, thereby increasing the supply of reserves to a level somewhat above the underlying demand from banks. Chairman Jerome Powell hinted at this on Wednesday, and I expect the central bank to announce something in the near future. There probably wasn’t sufficient time to prepare a detailed proposal this week, given that the pressure in the repo market wasn’t evident until Monday. And officials will have to communicate carefully, so the move won’t be confused with quantitative easing. Although the Fed’s balance sheet grows in both cases, the intent is completely different. To signal this, the Fed could focus on adding shorter-term obligations such as Treasury bills, as opposed to the longer-duration assets typically involved in QE.

Fourth, the Fed will likely consider a standing facility for the repo market – in which the central bank would stand ready to lend against Treasury or agency securities at a rate generally above the market and the federal funds target. This would provide a safety valve to mitigate upward pressure on repo rates. Fed officials have been exploring such a mechanism for some time. This week’s events should increase support for putting it in place.

<<<

>>> Fed Injects Cash for Third Day as Calm Returns to Funding Market

Bloomberg

By Liz McCormick and Alex Harris

September 18, 2019

https://www.bloomberg.com/news/articles/2019-09-18/fed-plans-to-intervene-in-repo-market-for-a-third-straight-day?srnd=premium

Thursday’s $75 billion dose followed similar amount Wednesday

Fed’s actions this week are easing pressure in a key market

The Federal Reserve added a third dose of liquidity to a vital corner of the funding markets Thursday, helping rates retreat further as investors warn that fresh bouts of stress remain possible in the weeks ahead.

The New York Fed injected another $75 billion Thursday through an overnight repo operation. That followed a dose of the same size on Wednesday and $53.2 billion on Tuesday. The operations, commonplace in pre-financial crisis times, temporarily add cash, with the Fed taking government securities as collateral.

The latest addition of liquidity -- with the Fed making clear it’s ready to do more as needed -- follows the Federal Open Market Committee’s move Wednesday to reduce the interest rate on excess reserves, or IOER, by more than their main interest rate -- all attempts to quell money-market stresses.

The operations have calmed the funding market, with repo rates declining to more normal levels after jumping to 10% Tuesday, four times where it was last week. Overnight general collateral repurchase agreement rates continued to retreat Thursday, trading around 2%, according to ICAP. Still, most investors say more Fed action is needed for a permanent fix, with gauges of dollar funding costs measured through the current swaps market showing pressures building again given disappointment over the steps the central bank took.

The effective fed funds rate was set at 2.25% as of Wednesday. It was at 2.30% Tuesday, above the top of the Fed’s target range of 2% to 2.25% before policy makers lowered their benchmark rate on Wednesday.

“We expect these episodes of funding stresses to become more frequent with demand for funding and U.S. Treasury supply forecast to increase heading into year-end and the Fed’s reserve levels likely to drop further,” Jerome Schneider, head of short-term bond portfolios at Pacific Investment Management Co., wrote in a note Wednesday with his colleagues.

Given the added supply, banks’ holdings of Treasuries have risen and are increasingly being financed by money market funds investing in repo, which leaves “U.S. funding markets more fragile,” Schneider wrote. He said this adds to other reasons why the Fed needs to do more to engineer a long-term fix.

After policy makers wrapped up a two-day meeting Wednesday, Fed Chairman Jerome Powell said the central bank will keep doing these repo operations if that’s what it takes to get markets back on track. He spoke hours after the effective fed funds rate busted through the central bank’s cap, evidence Powell and his colleagues were losing their grip on one of their most important levers for controlling the financial system.

Fed’s First-in-a-Decade Intervention Will Be Repeated Wednesday

With Repo Market Still on Edge, Fed Preps Second Blast of Cash

‘This Is Crazy!’: Fed’s Repo Madness Sends Wall Street Reeling

Fed Injects Liquidity Into Markets as Key Rate Busts Through Cap

Powell also said the Fed would provide a sufficient supply of bank reserves so that frequent operations like the ones they’ve done this week aren’t required.

The only way “to permanently alleviate the funding stress is to rebuild the buffer of reserves in the system,“ according to Morgan Stanley strategist Matthew Hornbach.

Relying on repo operations doesn’t resolve the issue of reserves declining as the Treasury rebuilds balances, Hornbach wrote in a note. Having regular operations will also increase market uncertainty as the Fed could halt purchases at any time, while the size of its buying will have to expand over time as reserves drop, he said.

“It is certainly possible that we’ll need to resume the organic growth of the balance sheet sooner than we thought,” Powell said, referring to the central bank potentially buying securities again to permanently increase reserves and ensure liquidity in the banking sector.

Many strategists had predicted the Fed would take even more aggressive measures to reduce the pressures. One idea that’s gotten a fair amount of attention is something called a standing fixed-rate repo facility -- a permanent way to ease funding pressures, as opposed to the ad-hoc operations the Fed has used this week. Many analysts even predicted a Wednesday announcement that the Fed would start expanding its balance sheet.

That didn’t happen. However, with the Fed apparently ready to keep injecting liquidity whenever it’s needed, “it’s enough for now,” said Jon Hill of BMO Capital Markets.

“This week’s dramatic moves in the short-term funding markets serve as a case in point for the need to carefully consider liquidity in the financial system,” Rick Rieder, global chief investment officer of fixed income at BlackRock Inc., wrote in a note.

“All of this funding market gyration points to the increasingly obvious fact that the end of Fed reserve draining is insufficient to stabilize these markets,” he said.

<<<

>>> A Divided Fed May Be Reluctant to Forecast More Cuts

Bloomberg

By Steve Matthews

September 18, 2019

https://www.bloomberg.com/news/articles/2019-09-18/divided-fed-reluctant-to-forecast-more-cuts-decision-day-guide?srnd=premium

FOMC expected to lower rates but dots may send hawkish signal

Oil-price spike reinforces sense geopolitical risks are rising

Under pressure from Wall Street and President Donald Trump, the Federal Reserve is widely expected to reduce interest rates on Wednesday for a second straight meeting, but its sharply divided policy panel may be reluctant to forecast further cuts.

The Federal Open Market Committee is likely to lower rates a quarter percentage point to insure against risks from a global slowdown and uncertainty over Trump’s trade policies, while forecasting no more reductions this year, according to economists surveyed by Bloomberg.

The meeting comes a day after the Fed’s New York branch injected billions of dollars in cash to quell a surge in short-term rates that was pushing up its benchmark rate, threatening to drive up borrowing costs for companies and consumers. The spike, while not suggestive of an imminent financial crisis, highlighted how the Fed was losing control over short-term lending.

The policy statement and updated quarterly forecasts will be released at 2 p.m. in Washington and Chairman Jerome Powell will brief the press 30 minutes later.

“It is a very divided group,’’ said Carl Tannenbaum, chief economist with Northern Trust Corp. in Chicago. “If participants are not seeing a deterioration in growth, how far are they willing to push? It is not a sure thing they will do more.’’

Markets have priced in nearly 1% point of cuts over the next year

The median interest-rate projections in the “dot plot’’ -- which displays the forecasts of the 17 Fed policy makers -- is likely to be unchanged for December after Wednesday’s expected cut, according to the Bloomberg survey. By contrast, investors are projecting another quarter point reduction by the end of this year.

Kansas City Fed President Esther George and Boston’s Eric Rosengren are likely to dissent, as they did against the rate cut in July, favoring no move. Another possible dissenter is St. Louis Fed President James Bullard, who may favor a half-point cut in the face of rising uncertainties.

What Bloomberg Economists Say

“Bloomberg Economics expects policy makers to cut rates in steady 25 basis-point increments until the yield curve is no longer inverted. We believe this means rate cuts in September, October and December -- although officials may hesitate to fully telegraph such intentions.”

-- Carl Riccadonna, Yelena Shulyatyeva, Andrew Husby and Eliza Winger

That said, most economists surveyed by Bloomberg expect the FOMC statement to stick with language that signals a bias to continued easing, probably via references to uncertainty over the outlook and a commitment to “act as appropriate” to sustain the expansion.

Division at the Fed

After a period of quiet and consensus, FOMC dissents are on the rise

“There are two fundamentally different views of the economy,’’ said Lindsey Piegza, chief economist at Stifel Nicolaus & Co. Inc. in Chicago. That will be reflected by a “growing in the dispersion of the dots and increasingly muddying the policy message for investors.’’

A small cut won’t be applauded by Trump, who last week said the Fed’s “boneheads’’ should reduce rates to zero or lower.

Read more: Key Trump Quotes on Powell as Fed Remains in the Firing Line

Volatility in oil prices after attacks on key Saudi Arabian facilities over the weekend reinforces the growing risks in the global economy, though the FOMC may be reluctant to adjust views to fast-changing events.

The committee could ratify the view that rates will be lower for longer by edging its estimate of the so-called neutral rate which neither spurs nor brakes the economy. It has fallen to 2.5% from 4% in early 2014 amid a global decline in borrowing costs that’s seen them slip into negative territory in Europe and Japan.

Falling Rates

FOMC median estimate of long run or neutral funds rate has steadily dropped

Statement Language

FOMC divisions make drafting the statement a challenge. Recent data have supported its forecasts for more than 2% economic growth this year, and some reports have surprised to the upside. Yet U.S. payroll growth has slowed and manufactured contracted in August for the first time in three years.

“They have been using boilerplate language ‘solid’ in describing the labor market, but that’s becoming harder to support and could be downgraded,” said Neil Dutta, head of U.S. economics at Renaissance Macro Research. Market measures of inflation expectations could also be downgraded, he said.

FOMC may tweak message after jobs slowdown last month

Powell, who in July referred to the rate cut as a “mid-cycle adjustment’’ rather than a long string of cuts, is likely to be asked about Trump’s call for zero rates and ex-New York Fed President Bill Dudley’s recent controversial column suggesting his former colleagues don’t cut rates to avoid enabling the trade war.

IOER, Balance-Sheet Tweaks

The Fed may announce a couple of technical adjustments to its balance sheet and the interest it pays banks on reserves after a sharp rise in money-market rates led the New York Fed to take action on Tuesday via its first overnight injection of cash in a decade.

It could make another adjustment to the interest rate it pays on excess reserves by reducing it by more than amount it cuts the fund rate. IOER is currently at 2.1% and the Fed may lower that by a bit more than the amount it cuts the target range for its benchmark federal funds rate -- currently 2% to 2.25% -- to better anchor money market rates.

Read more: Fed’s First-in-a-Decade Intervention

Separately, following the Fed’s decision in July to call an early halt to the gradual shrinking of its balance sheet, it may also say it is going to start allowing it to grow again to keep pace with growth in the economy, said Jonathan Wright, a professor at Johns Hopkins University and former Fed economist. The Fed has previously discussed this in terms of a process that could begin further down the road.

A third option to reduce pressure in money markets could be a new tool called a standing overnight repo facility. Such an instrument has been previously discussed and the FOMC was briefed on it in June, though minutes of the meeting showed that policy makers wanted more work done to figure out what it would do and how it would work.

<<<

>>> Fed Injects Liquidity Into Markets as Key Rate Busts Through Cap

Bloomberg

By Alex Harris and Liz McCormick

September 18, 2019

https://www.bloomberg.com/news/articles/2019-09-18/overnight-u-s-funding-rate-at-2-8-elevated-for-a-third-day?srnd=premium

The Fed will buy up to $75 billion of securities later Wednesday morning.

U.S. money markets showed some signs of calm as the Federal Reserve injected another $75 billion of liquidity and key rates pulled back from troubling levels.

Although the U.S. money-market interest rate remained elevated for a third straight day -- after spiking to a record 10% Tuesday -- it came back down to 2.8% early Wednesday even before the Fed accepted billions of dollars worth of Treasuries and other securities.

Now attention turns to this afternoon’s Federal Open Market Committee decision to see what, if any, further action policy makers take to calm the overnight lending business and ensure higher rates don’t harm other parts of the economy.

They’ll likely have to do something because the New York Fed said Wednesday that the effective fed funds rate busted through policy makers’ 2.25% cap the day before, coming in at 2.3%. That’s bad because it shows the Fed losing its grip on short-term interest rates, undermining its ability to guide the financial system.

“These money markets are a very powerful part of the financial system and everything flows through,” said John Herrmann at MUFG Securities in New York. “What the Fed has been doing so far to address the issues is like being a fire department chasing the fire instead of sort of installing fire hydrants through facility. They need to do more.”

The Fed dose of cash Wednesday follows a $53.2 billion liquidity injection Tuesday, the first in a decade and an attempt to restore order within the underpinnings of U.S. markets.

<<<

>>> Fed’s First-in-a-Decade Intervention Will Be Repeated Wednesday

By Liz McCormick and Alex Harris

September 17, 2019

https://www.bloomberg.com/news/articles/2019-09-17/new-york-fed-announces-operation-to-ease-money-market-rates?srnd=premium

Central bank is taking action after a key lending rate spiked

Turmoil signals the Fed is losing control of short-term rates

The Federal Reserve took action to calm money markets, injecting billions in cash to quell a surge in short-term rates that was pushing up its policy benchmark rate and threatening to drive up borrowing costs for companies and consumers. The central bank also said it’s willing to spend another $75 billion Wednesday.

While the spike wasn’t evidence of any sort of imminent financial crisis, it highlighted how the Fed was losing control over short-term lending, one of its key tools for implementing monetary policy. It also indicated Wall Street is struggling to absorb record sales of Treasury debt to fund a swelling U.S. budget deficit. What’s more, many dealers have curtailed trading because of safeguards implemented after the 2008 crisis, making these markets more prone to volatility.

Money markets saw funding shortages Monday and Tuesday, driving the rate on one-day loans backed by Treasury bonds -- known as repurchase agreements, or repos -- as high as 10%, about four times greater than last week’s levels, according to ICAP data.

More importantly, the turmoil in the repo market caused a key benchmark for policy makers -- known as the effective fed funds rate -- to jump to 2.25%, an increase that, if left unchecked, could have started impacting broader borrowing costs in the economy. Because that’s at the top of the range where Fed officials want the rate to be, they are likely to make yet another tweak to a key part of their policy tool set -- something called the interest on excess reserves rate -- to try to get things back on track when they meet Wednesday to set their benchmarks.

But the central bank didn’t wait until then to do something, resorting to a money-market operation it hasn’t deployed in a decade. The New York Fed bought $53.2 billion of securities on Tuesday, hoping to quell the liquidity squeeze. It appeared to help. For instance, the cost to borrow dollars for one week while lending euros retreated after almost doubling Monday.

Late Tuesday, the New York Fed said it would conduct another overnight repo operation of up to $75 billion Wednesday morning.

For repo traders, hedge funds and others that rely on that market for financing, the intervention came none too soon.