News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

It sounds like the Fed's plan for eventually tapering QE (which is currently running at $120 bil/month) may be aided by the arrival of the free spending Dems and their MMT fiscal spending plans. This will take up the slack in stimulus as the Fed tapers QE. So that's another reason for the Feds to favor a Dem sweep in this election.

Using fiscal policy (increasing deficit spending and decreasing taxes)

would be similar to the 2014-15 period when the Fed was fairly desperate to start tapering down QE and reduce its own bloated balance sheet. They got House Speaker Paul Ryan to reverse course and end the 'Sequester', and begin running much bigger deficits. Then a few years later came Trump's big tax cuts.

The stimulating effect from these bigger budget deficits and the tax cuts provided cover for the Fed's attempt to normalize interest rates and reduce its balance sheet. Nice try, and it almost worked, but the economy began weakening, made worse by Trump's trade war with China, so the Fed had to throw in the towel on rate normalization. Then the 'repo' problem appeared in the Fall of 2019, and the Fed had to restart QE. Of course then came Covid and mega QE.

Using the spendthrift Dems and MMT while the Fed tapers QE might work for a while, but how long can the US run deficits of 2-3 trillion/year before faith is lost in the dollar? Clearly the system is circling the drain, but they can probably keep it circling for a number of years before there is a final crisis. All the trillions in liquidity may keep the stock market buoyant, but looking longer term it seems best to start transitioning to hard assets like gold, land, rural real estate, etc.

>>> Fed looks to 2013 for future strategies in tapering asset purchases

Yahoo Finance

by Brian Cheung

January 7, 2021

https://finance.yahoo.com/news/fed-looks-to-2013-for-future-strategies-in-tapering-asset-purchases-120448382.html

The Federal Reserve may dust off its playbook from 2013 if it shifts to tapering its aggressive asset purchase program.

Currently, the central bank is snatching up $80 billion in U.S. Treasury bonds and $40 billion in agency mortgage-backed securities per month.

The Fed’s latest guidance, from Dec. 16, noted that the so-called quantitative easing program would continue at least at that pace until the economy looks like it has made “substantial further progress” in the recovery.

But minutes from that December meeting note that a “number” of Fed officials are already thinking about how to wind down those purchases once that “progress” is made.

Those unnamed Fed officials said they would like to “follow a sequence similar to the one implemented during the large-scale purchase program in 2013 and 2014.”

At the time, then-Fed Chairman Ben Bernanke announced in December 2013 that it would be notching down its monthly pace of purchases from $85 billion per month to $75 billion per month. The Federal Open Market Committee (FOMC) clarified that the program was not on a “preset course,” and that further slowing those purchases would only happen if the economy was ready for it.

JPMorgan’s Michael Feroli noted that the FOMC minutes for December 2020 show that the Jerome Powell-led Fed would similarly like to have its purchases “set on cruise control.” Feroli wrote Wednesday that the 2013 and 2014 reference also means the tapering process could go on for about 10 months. Analysts at Evercore ISI project a 12-month taper.

“Guidance on asset purchases remains pretty vague at this point and it appears future decisions will remain discretionary,” Feroli said in a note.

A cautionary tale

But the 2013 experience is also a cautionary tale of the perils of Fed communication.

The Fed had been debating its approach to tapering for months leading up to the December announcement, and Bernanke in May 2013 let it slip that a “step down” in quantitative easing could happen. The remark triggered a spike in bond yields and falling stock prices in an episode now known as the “taper tantrum.”

“A taper tantrum is now a real risk,” Jefferies economist Aneta Markowska told Yahoo Finance on Wednesday, forecasting a U.S. 10-year Treasury bond reaching 2% by the end of 2021.

The 10-year broke through the 1% mark on Wednesday morning, on the heels of the Georgia runoff election results that resulted in Democratic control of the Senate.

For the Fed’s part, policymakers are not yet on the same page about the timing for when to kick off any tapering. The minutes noted that two Fed policymakers favored a more stimulative quantitative easing program that would tilt its purchases toward longer-dated bonds.

In remarks this week, Fed officials sent mixed messages on whether or not the next steps on asset purchases would be a ramping up or a winding down of the program.

“These comments created an unhelpful mini-cacophony that is more than usually problematic given subsequent political and fiscal developments,” Evercore’s Krishna Guha and Ernie Tedeschi wrote Wednesday.

The analysts advocated for Fed leadership to more clearly signal its intention on where quantitative easing is headed, marking now as a “sensitive moment” for the Fed.

The next scheduled policy-setting meeting will be Jan. 26 and 27.

<<<

>>> Fed policy in 2021: Three things to watch

Yahoo Finance

Brian Cheung

December 28, 2020

https://finance.yahoo.com/news/federal-reserve-policy-in-2021-3-things-to-watch-113851008.html

It has been a long year for the Federal Reserve.

Since the first cases of COVID-19 in the United States, the central bank has slashed interest rates to zero, restarted its quantitative easing program, and opened up a slew of emergency loan facilities to backstop markets ranging from corporate debt to municipal bonds.

The beginning of the new year will be a critical inflection point for the U.S. economy. With case counts surging across the country, the Fed will attempt to bridge the next few months until widespread vaccination and herd immunity are achieved.

With interest rates near-zero and likely to stay there through the end of 2023, that means a need for other, unconventional monetary policy tools.

“There is more that we can do, certainly,” Fed Chairman Jerome Powell said December 16, adding that the second half of 2021 should see the economy “performing strongly.”

So what should markets be watching for from the Federal Reserve next year?

Emergency loan facilities

As COVID-19 began ripping through the country in March, the Fed moved to backstop several financial markets and stand up new programs offering credit to business borrowers.

Several of the programs will expire on December 31, at the order of U.S. Treasury Secretary Steven Mnuchin. But if economic conditions worsen next year, the Fed will face a difficult question: whether or not to re-open the facilities.

Three programs in particular will pose legal and political challenges to the Fed: the Municipal Liquidity Facility (loans to state and local governments), the Main Street Lending Program (loans to small- and medium-sized businesses), and the Corporate Credit Facilities (liquidity for corporate debt markets).

Language buried in the over 5,000-page government spending bill, which includes COVID-19 relief, would bar the Fed from either resurrecting those three programs or anything the “same as” those programs.

But current and former Fed officials have been vocal about their desire to keep those emergency programs available into 2021.

A Treasury Secretary Janet Yellen, pending Senate confirmation, could work with the Fed on other programs in the future. But the new statutory limitations may entangle the Fed in political backlash if it attempts to toe the line on re-opening something close to the three facilities in question.

"How effective that narrowing will be, in terms of freeing up the Fed to do what it most wants to do? It depends on how aggressive the Fed's lawyers want to be,” said Columbia Law professor Kathryn Judge.

Quantitative easing

The Fed’s massive pile of assets totals more than $7 trillion, the consequence of an aggressive pace of quantitative easing in the face of the crisis. The latest guidance from the Federal Open Market Committee makes it clear that its balance sheet will only get bigger until “substantial further progress” is made on the recovery.

More specifically, that means at least $120 billion in monthly purchases ($40 billion in agency mortgage-backed securities and $80 billion in U.S. Treasuries).

“Any time we feel like the economy could use stronger accommodation, we would be prepared to provide it,” Powell said on December 16.

But the Fed has not clarified exactly how it could adjust those purchases. Powell entertained the idea of, for example, targeting longer-dated purchases to push down longer-term borrowing costs.

Similarly, the Fed has not spelled out what a better-than-expected 2021 may mean for its asset purchases. “Substantial further progress” may mean a tapering of its asset purchases would come before the Fed lifts off from zero-interest rates.

The imprecise language, however, will keep Fed watchers and investors guessing on where inflation and unemployment will have to land before quantitative easing is pared back.

“It’s hard to infer when tapering will begin, but we would still pin that sometime around the end of next year,” JPMorgan’s Michael Feroli wrote on December 16.

Reflation may be around the bend

For both interest rate policy and quantitative easing, the Fed will be using inflation as its guiding star to get to the destination of an economy at maximum employment.

In the face of the downside risk of rising COVID-19 cases, the Fed hopes that widespread vaccination and a return to normal will spur consumption that could bring some modest price increases.

A new policy adopted by the Fed in August articulates that the Fed would tolerate inflation “moderately” above its 2% target, meaning that reflation in a possible second half recovery would not trigger an interest rate hike.

Core personal consumption expenditures, the Fed’s preferred measure of inflation, clocked in at just 1.4% in November.

The end game is to keep policy accommodative and give the economy ample time to pull the unemployed back into jobs. As of November, the economy remained 9.8 million jobs short of its pre-pandemic level in February.

“We are committed to allowing the economy to run until we find out what maximum employment means experientially,” San Francisco Fed President Mary Daly said in September.

Constance Hunter, chief economist at KPMG, told Yahoo Finance that she would not expect a rate hike for another year or year and a half.

“A lot of this depends on how broad-based the recovery is, but assuming we can get some reflation going then that would mean they might start changing their language and changing their asset purchases so that we can have slightly tighter monetary conditions going into 2022,” Hunter said.

<<<

>>> Bets on World of Negative Interest Rates End With Capitulation

Bloomberg

by Ruth Carson and Greg Ritchie

December 15, 2020

https://finance.yahoo.com/news/bets-world-negative-interest-rates-084540722.html

(Bloomberg) -- At the height of the pandemic, it seemed only a matter of time before negative interest rates -- the last resort of central banks -- ruled global markets.

A controversial strategy that’s yielded mixed results in the euro-area and Japan, traders still piled on bets earlier this year that central banks from New Zealand to the U.K., and even the U.S., were destined to follow suit. The three were among those that most aggressively cut rates through the worst of the virus-induced lockdowns. Yet all ultimately stopped short of going negative.

Traders now see a sub-zero move as increasingly unlikely, with policy makers largely favoring a “new conventional” mix of bond purchases and sector-specific aid programs. Of course, trillions of dollars of debt continue to trade with negative yields, effectively guaranteeing a loss for those who hold them to maturity. But with optimism returning about global growth, bond investors are shifting their attention to bets that yields will go higher, not lower.

“Central banks who don’t already have negative interest rates are going to be very cautious about crossing that rubicon,” said James Ashley, head of international market strategy at Goldman Sachs Asset Management. If policy makers need to prop up growth, “would it not be more prudent simply to rely on the unconventional tools like large scale asset purchases.”

Bold Experiment

Considered one of the boldest monetary experiments of the 21st century, negative rates were adopted in the wake of the financial crisis to drive borrowing costs lower and penalize banks that hoard cash rather than lending it out. The consequences for bond markets were far-reaching and long-lasting as trading was stymied and yields tumbled. The world’s stockpile of negative-yielding debt climbed above $18 trillion this month, a record, with rates on Spanish 10-year bonds sliding below 0% for the first time.

But despite the sub-zero strategy, both Europe and Japan have seen muted growth and failed to boost inflation to central banks’ targets. In fact, negative rates may have eaten into bank profits and hurt savers. As Federal Reserve Chairman Jerome Powell put it in May, “the evidence on negative rates is mixed.”

“The Fed has investigated a lot of BOJ and ECB policies,” said Kenta Inoue, senior market economist at Mitsubishi UFJ Morgan Stanley Securities in Tokyo. “At this point in time, there is no evidence suggesting that negative rates policy has a positive impact on the economy as well as markets.”

In a way, the holdout central bankers were saved from having to make the decision to go negative by both the success of alternative policies and an improvement in the global economic backdrop. The flood of liquidity to the financial system -- spearheaded by the Fed -- pushed borrowing costs lower, and rapid progress on vaccine development brought forward expectations of a return to normal.

Positive Shift

In money markets, traders have erased bets on negative rates next year in both the U.S. and New Zealand. And while their U.K. counterparts still expect rate cuts to combat the economic blow dealt by the coronavirus and Brexit, the Bank of England is seen stopping at zero.

Indeed, higher bond yields are now seen in the U.S. and New Zealand, with some strategists from Bank of America to Societe Generale looking for 10-year Treasuries to advance toward 1.5% by the end of 2021.

The vocal pushback from U.S. policy makers on the likelihood of negative rates and economic optimism have seen investors switch to bets on a steeper yield curve, albeit with limits. The benchmark Treasury yield has about tripled from its March low to 0.90% Tuesday.

“Since the Federal Reserve has signaled that it would not cut interest rates below zero, Treasuries have a floor at 0%,” said Saxo Bank strategist Althea Spinozzi. “2021 is going to be all about a yield-curve steepener.”

New Zealand Story

The situation is similar in New Zealand. China’s economic rebound, the Reserve Bank of New Zealand’s more favorable outlook on the economy and a new lending program have slashed expectations for even one more rate move in Wellington, let alone a reduction below zero. The RBNZ has a record-low rate of 0.25%.

Swap markets are pricing just a 30% chance of a 25 basis point cut by the end of 2021, after pricing in almost 50 basis points of cuts in November. And the 10-year government bond yield was trading around 0.87% on Tuesday, about double the September low of 0.44%.

“The hurdle for doing negative rates is going to be very high,” said Bank of New Zealand strategist Nick Smyth. New Zealand bonds are losing their premium to peers and there’s the potential for 10-year yields to climb to 1.5% if Treasuries retreat, he added.

Brexit Blues

Still, the risk of a no-deal Brexit could revive bets on negative rates in the U.K. Although the BOE is currently seen lowering rates by 10 basis points in early 2022, pricing has see-sawed with Brexit headlines, with traders betting on a cut as soon as May last week.

The move comes after Monetary Policy Committee member Michael Saunders flagged room for more cuts, and colleague Silvana Tenreyro said evidence is “supportive” of a sub-zero rates policy.

“We see the BOE taking the bank rate negative next year,” said Peter Schaffrik, a global strategist at RBC Europe Ltd. “Even a Brexit deal is a huge disruption from the status quo, so the odds of negative rates will be lower but not by a lot.”

To be sure, BOE Governor Andrew Bailey has made a point that doesn’t chime with the market movements: that sub-zero rates might be more effective during an economic recovery rather than a slump. Ranko Berich, head of market analysis at Monex Europe Ltd., finds bets on negative rates rising in tandem with expectations of a no-deal Brexit puzzling for this reason.

“The BOE’s own communication has made clear the MPC views negative rates as a tool best used at a time when banks are less worried about balance sheet risks, ideally the initial upswing phases of a recovery,” he said. “This suggests they would be highly unlikely to take rates negative as a knee-jerk reaction to a no-deal Brexit, which is precisely the kind of shock that would get banks worries about balance sheet risks.”

For now, though, the market is being driven by Brexit talks. Concern about the impact of no-deal on the U.K. economy has kept a lid on the nation’s bond yields, with gilts’ performance regularly out of step with peers. The 10-year benchmark yield traded at around 0.24% Tuesday, having fallen as low as 0.15% last week, and investors see more downside as a distinct possibility.

“Gilts offer limited protection, given yields are already low, but they’ll still fall further in a bad Brexit outcome as negative rates becomes the base case,” said John Roe, head of multi-asset funds at Legal & General Investment Management. “We don’t see negative interest rates as a problem per se. We just see it as an outcome that’s positive for gilts, which means it’s dangerous to be short.”

<<<

>>> The Bull Market That Won’t Die

BY JAMES RICKARDS

OCTOBER 28, 2020

https://dailyreckoning.com/the-bull-market-that-wont-die/

The Bull Market That Won’t Die

Investors have been hearing for years that “interest rates are near all-time lows,” and “rates have nowhere to go but up,” and finally, that “the bond bear market is right around the corner.”

These warnings have come from notable bond gurus including Bill Gross, Jeff Gundlach and PIMCO’s Chief Investment Officer Dan Ivascyn.

Investors are told that the time has come to dump bonds, short them if you can, and brace for much higher interest rates.

There’s only one problem with these warnings. The bond gurus have been dead wrong for years, and they’re wrong again now. Rates are going lower, and the bond market rally that began in 1981 has further to run. The bull market still has legs.

To paraphrase Mark Twain, reports of the death of the bond market rally have been “greatly exaggerated.”

The key is to spot the inflection points in each bear move and buy the bonds in time to reap huge gains in the next rally.

That’s where the market is now, at an inflection point. Investors who ignore the bear market mantra and buy bonds at these levels stand to make enormous gains in the coming rally.

“The Much Feared Bond Bear Market Never Materializes”

Let’s look at the record. The 10-year U.S. Treasury Note had a yield-to-maturity of 3.64% on February 11, 2011. That soon fell to 1.83% by September 23, 2011. Then the yield spiked to 2.23% on March 16, 2012. It fell back again to 1.46% on June 1, 2012.

Yields spiked again to 3.0% on December 27, 2013. Then yields fell back to 1.68% by January 30, 2015. And, so it continued through 2016 and 2017. Yields staged one last major back-up reaching 3.22% on October 5, 2018, before crashing once again to 0.54% on July 31, 2020.

Notice the pattern? Yes, yields are back up with some regularity. But they have never broken through the 3.25% level in nine years. The much feared bond bear market never materializes.

When yields get above 3%, the economy stalls out, disinflation takes over, the Fed panics and either “pauses” rate hikes or cuts rates resulting in yields coming back down to earth. Every time yields fall, bond investors make huge capital gains.

That’s exactly why the opportunity to go long Treasuries is so attractive. With all of the big players (hedge funds, banks, wealth managers) leaning on one side of the boat, it only takes a small perturbation causing lower yields and higher prices to trigger a massive short-covering rally, where these short investors scramble to exit their positions and buy bonds to cut their losses.

That’s not all. This technical history exhibits a pattern called “lower lows.” The rate spikes run out of steam around 3%, but each rate collapse goes lower than the one before. The history of rate bottoms is 1.46% on June 1, 2012, 1.36% on July 8, 2016, and the recent low of 0.54% on July 31, 2020.

Every time the bears say yields are going to the moon, they crash to a new low. That means bigger gains for investors.

Basic Bond Math

A bit of bond math is always helpful in these discussions since it’s counterintuitive for many investors. Yields and prices move in opposite directions. When bond yields go up, bond prices go down. When bond yields go down, bond prices go up.

Investors hoping for higher yields may not realize that the bond prices in their portfolio go down when that happens.

The best trading strategy is to buy a bond just when yields spike, and then hold it as yields fall back down to earth. That way, you keep the high yield on your bond and accrue huge capital gains as market yields decline. You can hold the bond to maturity, of course, but you can also sell it for a gain, move to the sidelines with cash and buy a new bond when yields get toppy again. Wash, rinse and repeat.

There’s another bit of bond math that is not intuitive to most investors. It’s called convexity or duration. In plain English, it means that as interest rates get lower, the capital gains get larger for each basis point decline in rates.

As an example, rates can decline from 3.50% to 3.25%. They can also decline from 1.00% to 0.75%. In each case, interest rates dropped by the same 0.25%. And, in each case, an outstanding bond would realize a capital gain.

But, the capital gain is larger in the second case than the first. Not all interest rate declines are created equal. Gains are bigger when rates are lower. Right now, rates are quite low, so the potential for capital gains is spectacular.

But, with rates so low already, what is the potential for rates to fall even more?

Rates on 10-year Treasuries rose from 0.513% on August 4 to 0.848% on October 22. Rates are 0.768% as of today. Right now, my models are telling me that bond yields will continue to fall, which means that bond prices will continue to rise.

Don’t Buy Into the Consensus

What’s been driving this increase in rates? The answer is simple. Markets expect a new deficit spending stimulus package from Congress. The package is still under negotiation, but the expectation is that it will be around $2 trillion, comparable to the $3 trillion of spending packages passed between March and June, during the worst stages of the pandemic.

Markets expect that this much new debt will flood the markets with new Treasury borrowings, which will drive bond prices lower. Markets also expect that this much stimulus will be inflationary because the Fed may have to monetize the new debt. The combination of more supply with a higher risk premium for inflation will result in much higher yields.

Both assumptions are probably wrong. The spending package depends on the election.

Democrats are confident that Joe Biden will win, so they are holding out, both to avoid giving Republicans a pre-election win and to get a better deal under President Biden.

Republicans take the opposite view and are holding out for a more conservative package under a reelected President Trump. The result is a stalemate.

My forecast is that Trump will win, and markets will be disappointed at the size (and spending priorities) of any package that results. This will cause rates to crash again.

Too Much Debt for Stimulus to Work

Even if a large spending package passes in the next few days or shortly after the election, it will not have the inflationary impact markets expect. Congress knows how to spend, but they do not know how to provide stimulus.

In fact, stimulus in the Keynesian sense is impossible when government debt levels are 130% of GDP. Research shows that any stimulus effect goes into reverse when debt-to-GDP levels pass 90%.

What you end up with is more spending, higher debt, but lower growth. Everyday Americans respond not by spending more but by saving more in anticipation of higher taxes or inflation down the road.

The short-term impact of that is not inflation, but disinflation or outright deflation. That means lower rates and bigger capital gains for Treasury bond investors.

As for rates being “low,” they’re not. It’s true that nominal interest rates (the kind you see on screens and TV) are near all-time lows. But real interest rates (nominal rates minus inflation) are quite high by historical standards. Real rates have to go much lower to help growth.

With inflation dropping, that means nominal rates have to go deeply negative in order to get real rates low enough to help. My forecast is for 10-year Treasury note rates to go to negative 0.50% or lower over the next year. That means large capital gains for investors in Treasury bonds.

Don’t go along with the crowd on this one. If you’re on the wrong side of this overcrowded trade, you could get trampled.

Regards,

Jim Rickards

for The Daily Reckoning

<<<

>>> Bond Defaults Deliver 99% Losses in New Era of U.S. Bankruptcies

Bloomberg

By Jeremy Hill and Max Reyes

October 26, 2020

https://www.bloomberg.com/news/articles/2020-10-26/bond-defaults-deliver-99-losses-in-new-era-of-u-s-bankruptcies

Market prices, derivative auctions imply debt may be worthless

High borrowings, weak protections leading to low recoveries

Three cents. Two cents. Even a mere 0.125 cents on the dollar.

More and more, these are the kinds of scraps that bondholders are fighting over as companies go belly up.

Bankruptcy filings are surging due to the economic fallout of Covid-19, and many lenders are coming to the realization that their claims are almost completely worthless. Instead of recouping, say, 40 cents for every dollar owed, as has been the norm for years, unsecured creditors now face the unenviable prospect of walking away with just pennies -- if that.

While few could have foreseen the pandemic’s toll on the economy, the depth of investors’ pain from corporate distress was all too predictable. Desperate to generate higher returns during a decade of rock-bottom interest rates, money managers bargained away legal protections, accepted ever-widening loopholes, and turned a blind eye to questionable earnings projections. Corporations, for their part, took full advantage and gorged on astronomical amounts of debt that many now cannot repay or refinance.

It’s a stark reminder of the long-lasting repercussions of the Federal Reserve’s unprecedented easy-money policies. Ultralow rates helped risky companies sell bonds with fewer safeguards, which creditors seeking higher returns were happy to accept. Now, amid a new bout of economic pain, the effects of those policies are coming to bear.

Debt issued by the owner of Men’s Wearhouse, which filed for court protection in August, traded this month for less than 2 cents on the dollar. When J.C. Penney Co. went bankrupt, an auction held for holders of default protection found the retailer’s lowest-priced debt was worth just 0.125 cents on the dollar. For Neiman Marcus Group Inc., that figure was 3 cents.

CDS Sadness

Credit default swap auctions portend steeper-than-usual losses

The loose lending terms that investors have agreed to mean that by the time corporations file for bankruptcy now, they’ve often exhausted their options for fixing their debt loads out of court. They’ve swapped their old notes for new ones, often borrowing against even more of their assets in the process. Some have taken brand names, trademarks, and even whole businesses out of the reach of existing creditors and borrowed against those too. While creditors always do worse in economic downturns than in better times, in previous downturns, lenders had more power to press companies into bankruptcy sooner, stemming some of their losses.

The pandemic is upending industries like retail and energy, making it unclear how much assets like stores and oil wells will be worth in the future. The underlying problem for many companies, though, is that they have astronomical levels of debt after borrowing with abandon over the previous decade, then topping up with more to get them through the pandemic.

For bondholders, the kind of liabilities that companies have added makes the problem worse. Loans have been a particularly cheap form of debt for many companies over the last decade. Those borrowings are usually secured by assets, leaving many corporations with more secured debt than they’ve had historically. That means that unsecured bondholders end up with less when borrowers go broke.

“We’ll see companies gradually hitting the wall -- it’s just a question of when and how fast,” said Dan Zwirn, founder of Arena Investors, a $1.7 billion investment firm with an emphasis on credit. “There’s just going to be way more downside.”

Record Lows

The recent low values for bonds in credit derivatives auctions signal that in future bankruptcies owners of unsecured bonds, not to mention loans, may suffer a bigger hit than usual, according to research from Barclays Plc. The median value for companies’ cheapest debt in credit derivatives auctions this year is just 3.5 cents on the dollar, a record low and far below the 23.4 cent median for 2005 through 2019.

The value of a company’s bonds in an auction for credit derivatives payouts doesn’t necessarily equal how much money bondholders will actually recover when a bankruptcy is complete. But lower auction values do tend to correlate to lower recoveries, according to Barclays. Lower market values also reflect investor concerns.

The auctions represent the value of a company’s cheapest unsecured bond, although usually most of a borrower’s unsecured notes trade around the same price in bankruptcy, according to Barclays. When a company defaults or files for bankruptcy, an investor that bought a credit default swap receives a payout equal to 100 cents on the dollar minus the auction value of the cheapest-to-deliver security.

Loan Pain

It’s not just bond investors that will suffer from low recoveries. Amid the pandemic downturn, loan investors could find themselves losing 40 to 45 cents on the dollar, compared with historical averages of 30 to 35 cents, according to Barclays.

One factor that is hurting money managers is the erosion of investor protections known as covenants, as more and more high yield and leveraged loan deals are covenant-lite, meaning they feature minimal such safeguards. When corporations had more restrictive covenants, borrowers had less room to fix their debt outside of court, sending them into bankruptcy closer to the first sign of trouble.

Now companies have more leeway to seek extra financing when they’re in trouble, and to give lenders providing additional funds the right to jump to the front of the line if the company does go bankrupt.

“Covenant-lite paper usually means by the time you get back to the table with the borrower, the house is on fire,” said Sanjeev Khemlani, a senior managing director at FTI Consulting. “All of that extra time you had before, that’s just gone away.”

Oaktree Deal Crushed a Leveraged Loan and Exposed Market’s Woes

Investors that bought a J. Crew Group Inc. term loan at par back in 2014 may have thought they were making a relatively safe bet, since it was secured debt. When the company started struggling a few years later, it moved intellectual property including its brand name into a new entity, a move enabled by relatively loose covenants.

The company then exchanged some of its existing bonds for new notes secured by the intellectual property as well as preferred stock and equity in its parent company, as part of a broad restructuring. Loan investors ended up suffering: after the company filed for bankruptcy in May, the 2014 obligation was worth less than 50 cents on the dollar, according to Bloomberg loan valuation estimates. (J. Crew exited bankruptcy in September.)

FTI’s Khemlani, who advises lenders with senior claims on borrowers’ assets, said investors should make an effort to “put some teeth” into their agreements with borrowers now as they fall into distress, regaining some lost protection.

In addition to shifting assets, companies have also been doing more distressed exchanges in recent years, where troubled corporations offer creditors new, debt that often ranks higher in the repayment pecking order in exchange for relief like lower principal or later maturities or both. Creditors that participate can stem their losses in the event of a bankruptcy, but investors that sit the deal out can end up worse off.

The popularity of distressed exchanges has also contributed to a general rise in secured debt in companies’ capital structures. That means that more investors -- holders of loans and secured bonds -- are fighting for the same scraps when a company files for bankruptcy. Almost 20% of the debt in the U.S. high-yield bond market is now in some way secured, according to Barclays, versus just 6% in 2000. The number of businesses that had taken out just loans and no other form of debt almost doubled between 2013 and 2017, according to JPMorgan Chase & Co. data.

<<<

>>> How to invest for income now

Tactical multi-asset investing takes on low rates and bad news

BY ADAM KRAMER, PORTFOLIO MANAGER,

FIDELITY VIEWPOINTS

05/01/2020

Key takeaways

Multi-asset income strategies may help investors seek income despite low interest rates.

Professional investment managers may find opportunities when markets misprice assets in reaction to bad news.

Opportunities exist now in investment-grade corporate bonds, high-yield bonds, dividend-paying stocks, convertible bonds, and Treasury inflation-protected securities.

With interest rates at historic lows and some companies reducing or eliminating dividends, it's a challenging time for investors who seek income from their portfolios. Challenging, though, is not the same as impossible. A professionally managed, tactical approach to income investing that can look for opportunities in a wide variety of asset classes may help income-seeking investors achieve their goals, despite low rates.

In fact, economic uncertainty and anxiety about the spread of COVID-19 make this a good time for tactical investing. That's because when uncertainty is high, markets may temporarily misprice assets based on short-term events and overlook other factors, such as how much investors might earn over a longer term on those assets.

For professional managers who can identify those mispricings, the combination of abundant bad news and the freedom to invest in a wide variety of assets can present opportunities. Rather than overreact to bad news, tactical managers can seek assets they believe have the potential to outperform if the bad news "turns out not to be so bad after all." Even if reality turns out as negative as markets expect, prices shouldn't fall much because investors anticipated it. Keeping an eye out for mispricings can also help avoid assets where not enough bad news may be priced in and prices are too high.

Looking for opportunities

The forces that drive financial markets are always in motion. Economic growth increases and slows. Investors' enthusiasm for certain asset classes or companies rises and falls. New technologies arise, while older ones fade away. Unforeseeable events can act on global economies in unexpected ways. Because market conditions constantly change, the investments that deliver the highest returns today may not be the ones that do so next month or next year. That's why multi-asset income strategies that can invest across a wide variety of asset classes may be able to deliver more consistent returns and a better balance between risk and return than those with fewer options to choose from.

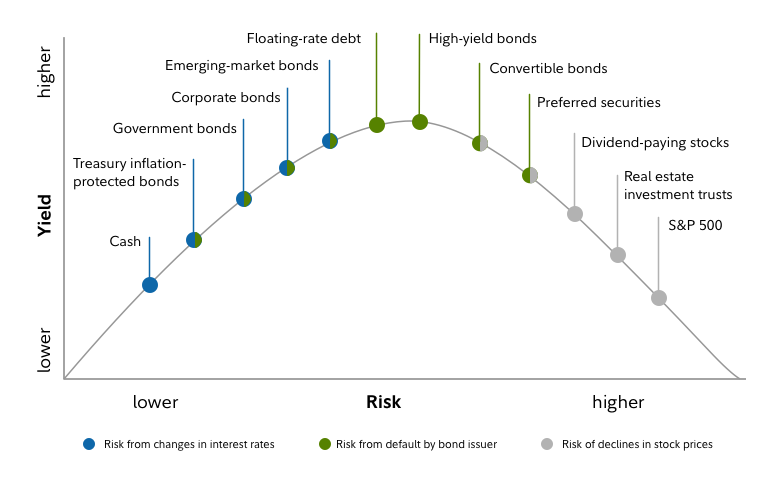

How yields and risks of popular investment choices compare

The data in the chart is described in the text.

For illustrative purposes only.

Source: Fidelity Investments

The chart above depicts general long-term directional and ranking relationships among a number of asset classes on the dimensions of yield and beta. Beta is estimated in comparison to US common stocks as represented by the S&P 500 index. The relationships and relative rankings among these asset classes will vary over time.

Finding opportunities now

As the US Treasury, Federal Reserve, and federal government continue to be pragmatic and supportive of the economy, the coronavirus pandemic has created opportunities within many income-oriented US asset class. As concerns over the economic impact of the virus's spread prompted many investors to sell assets, prices of many bonds as well as stocks dropped to levels not seen since the global financial crisis. Assets sold off with little regard for fundamentals and since then, professional investment managers have been buying those that offer income and value on the expectation that if events turn out better than expected, their prices could rise in addition to paying interest and dividend income.

While many companies' operations have been severely reduced, dividend-paying US large-cap stocks present opportunities for managers of income strategies who practice careful security selection and seek companies with strong balance sheets that pay sustainable dividends. Many of these stocks' prices fell significantly during widespread selling that accompanied the spread of COVID-19 around the world. They include consumer staples, pharmaceuticals, and information technology companies, and also companies in sectors such as materials and energy that have historically performed well as the economy emerges from recession.

Some dividend-paying stocks related to the transportation of oil and refined products also offer opportunities. Oil tanker operators are an example of how the ability to spot mispriced assets can benefit income-seeking investors. Theirs were among the first stocks to move lower as the coronavirus spread in China and oil demand fell. Oil production cuts are generally a negative for oil tankers because there's less cargo for them to carry. However, demand and prices have fallen faster than production, and oil companies are storing crude oil on ships. That means more need for ships than expected. Despite plunging global oil demand, these companies will soon start declaring their first quarter dividends and should have a much better situation than previously expected.

Preferred stocks have been very expensive but are now priced near their historical averages. Most US preferreds are in banks which are in much better shape than they were during the financial crisis.

Remember, though, as we've seen this year, stock markets are volatile and can decline significantly.

Many high-quality companies' investment-grade corporate bonds offer opportunities, including those from defense contractors, regulated utilities, and large US banks. Many of these bonds are now selling at discounts. Unusually, these bonds' prices fell along with stocks during the March COVID-19-related sell-off. Since then, prices of many highly rated bonds have recovered, but BBB-rated investment-grade corporate bonds offer both attractive prices and income, with many yielding near 4%, as of April 29, 2020.

Some high-yield bonds with credit ratings of BB and B also present opportunities, particularly those issued by cable, telecommunications, packaging, and industrial companies. Many of these bonds are selling at a discount, with yields of 6% and 9%, respectively, as of April 29, 2020.

To be sure, bonds of less than investment-grade quality involve greater risk of default or price changes due to changes in the credit quality of the issuer. Because of these risks, careful security selection by professional managers is important.

Convertible bonds issued by companies in industries such as technology and health care, whose underlying stocks had been expensive are currently more reasonably priced, at close to their averages over the past 25 years. Many new bonds offering attractive yields are being issued as companies seek to adjust to the new COVID-19 reality.

Convertible bond prices can fall if interest rates rise and stock prices decline, but they are less sensitive to such changes than both stocks and traditional corporate bonds. While bad news can help create opportunities, too much of it can have the opposite effect. Too much bad news has been priced into US Treasurys, which have rallied and no longer look attractive. While they can act as hedges to protect investors in down markets, they currently offer little yield.

Treasury inflation protected securities (TIPS), which adjust to the consumer price index, can be an attractive alternative to Treasurys. When real yields move lower, TIPS have historically done well. In the COVID-19 world, financial markets are pricing in very little future inflation due to falling oil prices and reduced business and consumer spending. This is reflected in declining real yields which give TIPS a better balance between risk and reward than nominal Treasuries looking out over the next year or two.

Finding ideas

Investors interested in these strategies should research professionally managed mutual funds. You can run screens using the Mutual Fund Screener on Fidelity.com. Below are the results of some illustrative mutual fund screens (these are not recommendations of Adam Kramer or Fidelity).

Multi-asset class income funds

Fidelity funds

Fidelity® Multi-Asset Income Fund (FMSDX)

Non-Fidelity funds

BlackRock Multi-Asset Income Portfolio (BAICX)

American Century Multi-Asset Income Fund (AMJVX)

Invesco Multi-Asset Income Fund (PIAFX)

<<<

>>> A ‘Buy Everything’ Rally Beckons in World of Yield Curve Control

Bloomberg

By William Shaw and Todd White

June 21, 2020

https://www.bloomberg.com/news/articles/2020-06-21/a-buy-everything-rally-beckons-in-world-of-yield-curve-control?srnd=premium

Fed and BOE may follow Japan, Australia in targeting yields

Move could boost bonds, credit, equities and carry trades

Federal Reserve Chair Jerome Powell said the usefulness of the policy “remains an open question” on June 10.

As central banks pump trillions into the world economy, investors are setting their sights on what could be the next big thing in global monetary policy: yield curve control.

The strategy, which involves using bond purchases to pin down yields on certain maturities to a specific target, was once deemed an extreme and unusual measure, only deployed by the Bank of Japan four years ago after it became clear that a two-decade deflationary spiral wasn’t going away.

No longer. This year, the Reserve Bank of Australia adopted its own version. And despite officials’ attempts to cool it, speculation is rife that the U.S. Federal Reserve and Bank of England will follow later this year.

Should yield curve control go global, it would cement markets’ perception of central banks as the buyers of last resort, boosting risk appetite, lowering volatility and intensifying a broader hunt for yield. While money managers caution that such an environment could fuel reckless investment already stoked by a flood of fiscal and monetary stimulus, they nonetheless see benefits rippling across credit, equities, gold and emerging markets.

“It depends on the form and the price but broadly speaking it’s the green light to carry on with the QE trade -- buy everything regardless of valuation,” said James Athey, who manages $3.1 billion at Aberdeen Standard Investments in London.

Boost for Bonds

While the BOE didn’t discuss yield curve control on Thursday, some analysts think it could ultimately target five-year notes at a rate of 0.1%, flattening the yields out until that maturity.

That could send money flowing into shorter maturity bonds and trigger a sell-off in volatility. Demand for shorter maturities could drive up rates on longer peers -- a mixed blessing for pension funds and life insurers, which could see their existing holdings devalued, but be able to buy new assets for less.

Pre-Curve Control

Talk of negative rates from BOE has held down short-end U.K. bond yields

Federal Reserve Chair Jerome Powell said the usefulness of the policy “remains an open question” on June 10. While most expect a low-yield target for shorter maturities, potentially as soon as September, Societe Generale SA sees a case for focusing further out the curve. Five- and seven-year Treasuries may rally if the Fed looks to go beyond controlling just the front end.

Where central banks set their target will be key, and could send assets swinging either way. A 50-basis-point target on the 10-year Treasury yield would spark a bond rally and flatten the curve alongside a probable rise in equities. However, a full percentage point could see bonds bear steepen and trigger a sell-off in shares, said Aberdeen Standard’s Athey.

Credit Surge

Capping interest rates would help by ensuring corporate borrowers continue to benefit from attractive financing rates. Lower yields in longer maturities would assist investment-grade companies, which tend to issue longer-dated debt than lower-rated borrowers. Meanwhile, junk borrowers would reap the rewards of the general boost to market sentiment.

Companies with high debt loads such as airlines and energy could get a lift, said Charles Diebel, who manages $2.6 billion at Mediolanum SpA in Dublin. U.K. banks could also gain as lenders will have escaped the crushing effect of negative interest rates.

Yields on company bonds have already benefited from policy support

“It will allow the whole rating spectrum of fixed income credits to borrow at incredibly cheap absolute levels during a time of much uncertainty and would certainly be very bullish,” said Azhar Hussain, head of global credit at Royal London Asset Management.

Carry Trade

Lower rates in the U.S. could weaken the dollar and help riskier currencies like the South African rand and Mexican peso. Carry trades involving the Indonesian rupee and the Russian ruble could also benefit, as well as Group-of-10 currencies like the Australian dollar and Norwegian krone, according to Vasileios Gkionakis, head of foreign-exchange strategy at Banque Lombard Odier & Cie SA in Geneva.

Traders in South Africa's currency love events that weaken the dollar

The move could also send dollars flowing into carry trades targeting U.S. assets. These could include mortgage-backed securities, as well as sovereign, supranational and agency bonds.

Bubble Risk

Of course, such a widespread bullish outlook comes with risks, especially at a time when asset valuations are near extremes. A rally in U.S. stocks has pushed estimated price-to-earnings to the highest in almost two decades.

Meanwhile, 10-year yields are negative for nine of 25 developed markets tracked by Bloomberg, while the rest stand well below their one-year averages. It’s a precarious bubble that could eventually burst, should the wall stimulus spur inflation down the road and eat into investors’ profits.

While most asset classes stand to gain from a global wave of yield curve control, investors may want to heed lessons and challenges from different regions.

Since the BOJ started the policy in 2016, it has largely succeeded in tethering the 10-year rate at around 0%. As for the RBA, it began pinning the three-year yield at 0.25% in March. Yields on longer maturity bonds rocketed then eased after the announcement, and the spread between three-year and 10-year yields remains around 30 basis points wider than in mid-February.

Introduction of yield curve control pushed Australia's bond curve steeper

For the European Central Bank, the challenge would be the multiple interest-rate curves under its remit. The ECB has acknowledged the importance of keeping borrowing costs low across all bond maturities, without committing to an explicit yield curve control policy.

Regardless, the notion that central banks are approaching some sort of curve control is here to stay. A key lesson from the 2008 crisis was that policy makers need to intervene quickly, and investors now expect them to consider any weapon at their disposal.

“Policy makers tightened up the banking system so much that the markets became too big to fail,” said Mark Nash, the head of fixed income at Merian Global Investors in London. “Now they have no choice but to keep them working.”

<<<

>>> Brawls Erupt in U.S. Debt Markets After Borrowers Get Desperate

Bloomberg

By Sally Bakewell, Claire Boston, and Katherine Doherty

June 11, 2020

https://www.bloomberg.com/news/articles/2020-06-11/brawls-erupt-in-u-s-debt-markets-after-borrowers-get-desperate?srnd=premium

Credit-market feuds getting uglier, dirtier and more vicious

Weak covenants open door to asset transfers, other moves

A massive wave of corporate distress is pitting beleaguered companies against their lenders in brawls that are shaping up to be nastier than ever before.

Desperate firms and their private equity owners are seeking to take advantage of years of weakening creditor protections to help cut obligations and raise cash after the coronavirus outbreak brought businesses to a standstill. Be it via allowances written into borrowing documents when times were good or simply loopholes in deal terms, they’re siphoning collateral and transferring assets while pushing deeply discounted debt swaps onto investors, who risk seeing the value of their bonds and loans plunge if they don’t go along.

Still, money managers aren’t just rolling over. Credit powerhouses like GSO Capital Partners, BlackRock Inc. and HPS Investment Partners have lined up scores of lawyers and financial advisers to defend their interests, often finding themselves at odds with one another as they fight for the biggest piece of a shrinking pie. As the gloves come off, industry veterans say tensions are as high as they’ve ever seen.

“You have more and more aggressive people holding this stuff and private equity firms have gamed every nook of credit agreements,” said Dan Zwirn, chief executive officer of Arena Investors, which manages $1.4 billion. “As people get desperate, there are going to be a lot more of these.”

The conflicts underscore how the legacy of the last crisis is being felt as the current one unfolds. The Federal Reserve’s relentless interest-rate cutting and quantitative easing spurred a surge in demand for higher-yielding assets, helping risky companies sell debt with fewer lender safeguards. Now, amid a fresh bout of economic pain, the effects of those policies are coming to bear.

Corporate Stress

Global corporate default tally spikes as pandemic takes hold

One such fight recently played out between Sinclair Broadcast Group Inc. and its creditors.

The company through a subsidiary sold $1.8 billion of unsecured notes last year to fund the acquisition of Walt Disney Co.’s regional sports networks. Those securities have plunged as the pandemic left stations with no professional sporting events to televise.

Relatively loose provisions in the bond documents helped embolden Sinclair to pursue a debt exchange that asked holders to take a 40% haircut and swap into debt secured by the company’s assets.

Lenders late last month balked at the terms, and a group led by Shenkman Capital Management organized to block the exchange. The response from Sinclair was ominous: the company said it was weighing other options including a possible maneuver that would shift company collateral out of creditor reach if the exchange offer was not successful.

The potential moves were “threats” that appeared designed to pressure lenders, according to Covenant Review, which called the outstanding bond’s safeguards among the weakest it had ever seen.

“Issuers are being more aggressive in the way they are going about debt exchanges; they’re looking for additional ways to coerce bondholders that haven’t been interested in participating,” said Scott Josefsberg, an analyst at the debt research firm. “But investors are putting up a fight so far.”

Sinclair ultimately exchanged around 3.6% of eligible notes.

A representative for the broadcaster had no immediate comment, while Shenkman declined to comment beyond confirming its role leading the creditor group.

Read more: Unreadable fine print in leveraged loans sparks market backlash

Sinclair’s exchange offer was hardly the only one to provoke the ire of investors in recent weeks.

SM Energy Co.’s efforts to get creditors to swap their bonds into new securities at 50% to 65% of face value have faced significant pushback. With only about 10% of note holders agreeing to tender last month, the oil and gas driller struck a separate agreement with a group of creditors led by BlackRock.

The side deal was designed to backstop the exchange, and the BlackRock-led group got better terms for swapping its debt versus what was offered to other creditors. The move infuriated other lenders, who organized with law firm Weil Gotshal & Manges to oppose the deal.

Bondholders that accept the exchange must agree to eliminate almost all restrictive covenants on the existing debt, which would hurt anyone who doesn’t participate. The deadline for the tender has been extended to June 12.

SM Energy, BlackRock and Weil Gotshal & Manges didn’t respond to requests seeking comment.

Revlon Clash

Analysts have been warning investors for years that weakening protections would ultimately have costs as investors ceded more and more ground to borrowers. Yet despite the recent surge in corporate stress, a Moody’s Investors Service gauge of bond covenant quality remained near the weakest on record in April. A similar tracker for loans reached its lowest ever in the fourth quarter, the most recent data available.

Lender safeguards played a major role in Revlon Inc.’s contentious $1.8 billion debt overhaul last month.

Creditors including Brigade Capital Management and HPS had organized to block the company’s refinancing plan because it allowed the firm to siphon off collateral and use it to back new debt. Supporters of the plan included Ares Management Corp. and Angelo Gordon & Co.

The deal needed more than 50% of the holders signed on to close. At first, opposing lenders held a blocking position with a majority of the outstanding loan amount opting out. But Revlon secured a new $65 million revolving credit facility from the supportive lenders -- which the company says was permitted under its covenants -- ultimately giving it enough backing to push the deal through.

Some lenders continue to contest the transaction, arguing that Revlon needed the majority of debt holders of every tranche to agree, and maintaining that the company breached covenants when it moved certain intellectual property to secure a $200 million loan last year, according to people with knowledge of the matter.

Still any creditors that chose not to participate in the refinancing were demoted from having a first-priority claim on company assets to a third-lien claim.

“Revlon is strengthening its balance sheet and increasing liquidity to better deal with the issues at hand, including Covid-19,” Chief Financial Officer Victoria Dolan said in a statement to Bloomberg. “This group of objecting lenders is trying to block that. We are confident that we will overcome this effort to hurt our company.”

Representatives for Brigade, HPS, Ares and Angelo Gordon declined to comment.

Read more: Revlon lenders allege default with debt deal nearing close

Transactions involving collateral transfers have been among the most fiercely contested between creditors and private equity firms scrambling to protect their investments.

Paul Singer’s Elliott Management Corp. last month became locked in a fight with lenders of global bookings operator Travelport, which Elliott bought last year with Siris Capital Group. The owners shifted intellectual property estimated to be worth more than $1 billion to an unrestricted subsidiary -- putting it out of reach of the creditors -- to help it raise cash.

Lenders led by GSO demanded that Travelport unwind the transaction for violating indenture agreements, and declared the step a default. The owners, who argue it was permitted, told them they would reverse the asset transfer if the creditors provided roughly $500 million of new financing and rolled up some existing debt holdings at a discount.

The dispute has gotten so heated, Bank of America Corp. last month surrendered its role as administrator of Travelport’s loan to avoid taking a side in the feud, while Kirkland & Ellis recently resigned as the company’s legal representation, according to people familiar with the matter.

With the sides at loggerheads, the private equity owners supplied the financing themselves in a loan backed by the disputed collateral, a move that’s likely to further inflame the situation.

Representatives for Travelport, Elliott, Siris, GSO and Bank of America declined to comment, while Kirkland & Ellis didn’t have an immediate comment.

‘Fight Like Dogs’

Industry veterans say creditors should no longer be surprised when private equity sponsors use asset transfers, spinoffs, carve outs and other such moves following a number of high profile and hotly contested maneuvers in recent years.

“Anyone professing to be shocked by it probably hasn’t been around very long,” said Philip Brendel, a senior credit analyst at Bloomberg Intelligence.

Yet with creditors so far showing little appetite to push for stronger covenants in borrowing documents, market watchers warn to expect more brawls in the months and years ahead.

“Rates were suppressed long after they should have been; it drove yield hunger and a non-bank explosion that created misalignments,” Arena Investors’ Zwirn said. “Now they’re learning once again, there are consequences. We are at just the beginning of this thing. They’re going to fight like dogs to avoid those consequences.”

<<<

>>> Why It’s Time to Rethink Bonds

Barron's

by Gail MarksJarvis

June 7, 2020

https://www.barrons.com/articles/with-rates-so-low-income-investors-need-to-rethink-bonds-51591404975?siteid=yhoof2&yptr=yahoo

Already-beleaguered income investors are facing a tough decade. Ten years ago, investors were bemoaning a 3.8% yield on the 10-year Treasury, because a decade before that, they were yielding 6.4%. Recently, 10-year Treasuries yielded 0.88%.

“We are at a pretty bleak starting point for income investors,” says Michael Fredericks, manager of the $16 billion BlackRock Multi-Asset Income Portfolio fund (ticker: BAICX).

Fredericks has analyzed decades of bond performance using the Barclays Aggregate Bond Index, or AGG, and found that the 10-year Treasury yield at the start of a decade gives a reliable clue to what’s to come during the next nine years. The starting Treasury yield is almost identical to the annual total return over the decade. For example, the 10-year Treasury was yielding 3.8% on Jan. 1, 2010, and the annualized return through the decade was 3.75%. “This suggests that with the 10-year Treasury yielding 0.8% today, the returns for the AGG over the next 10 years will likely be incredibly low,” he says.

“Advisors should be telling their clients that they aren’t going to generate the income they have in the past from Treasuries, or even corporate or high-yield bonds,” adds Adrian Cronje, chief investment officer of Atlanta financial advisory firm Balentine.

Investors—especially retirees and other conservative investors—need to shift how they view bonds. Instead of relying on bonds for income, investors should embrace bonds as ballast. That means settling for low yields from Treasuries and high-quality corporate and municipal bonds, while tapping total return in stock and bond portfolios for income.

Barron’s spoke to advisors, analysts, and fund managers to assess the best strategy for bond investors today. Here’s what they said.

Don’t overdo risk. Investors have gone further out on the risk curve, allocating larger portions of their portfolio to high-yield, emerging-market debt, and bank-loan funds. That risk taking hurt badly in the coronavirus market rout between Feb. 19 and March 23. Among some of the biggest exchange-traded funds, the iShares iBoxx $ High Yield Corp Bond (HYG) plunged 22%; the Invesco Senior Loan (BKLN) fell 21%; the iShares Preferred and Income Securities (PFF) lost 27%; and the (ICVT) dropped 24%.

“Most investors don’t need an allocation to bank loans, preferred stock, or convertibles,” says Morningstar analyst Alex Bryan.

One ETF, such as the iShares Core Total USD Bond Market ETF (IUSB), which invests in Treasuries, mortgage-backed securities, and investment-grade and high-yield bonds, could offer enough diversification. Alternatively, Bryan suggests mimicking the makeup of that fund with more specific ETFs, to more easily add or reduce positions in, say, high-yield.

Don’t ignore Treasuries. Yes, Treasury bonds are yielding next to nothing, but yields drop when prices rise—which means investors can still find that bonds offer steadiness, and possibly positive returns, when stocks fall. “I’m not using corporate bonds at the moment,” says Sue Stevens, an advisor in Deerfield, Ill. “The bond portion of a portfolio should just be safe.” The Vanguard Intermediate-Term Treasury ETF (VGIT) has gained 7.3% so far this year, Stevens notes, while the Vanguard S&P 500 ETF (VOO), is down more than 2.5%.

If the economy weakens and the Federal Reserve lowers interest rates, both long-term and intermediate-term ETFs will likely have nice gains. In a report last week, Bank of America Securities economists wrote that they expect the Fed to guide rates lower in September, “once the initial bounce from reopening subsides and it becomes apparent that the economy is in for a slow and bumpy recovery.” That could make Treasury bonds maturing in five to seven years a sweet spot for investors: Intermediate-term Treasury ETFs, such as the Vanguard Intermediate-Term Treasury ETF (VGIT) or the iShares 3-7 Year Treasury Bond ETF (IEI), could gain value.

Worried about rates rising during a recovery? Stick with shorter-term Treasury funds, such as the iShares 1-3 Year Treasury Bond (SHY). Financial planner Lewis Altfest advises some people to park cash in money-market funds or certificates of deposit for a couple of years—yields are not much lower than Treasuries, and there is little to no risk if rates rise.

Beware the urge to bargain-hunt. There aren’t many bargains out there. Spreads, the difference between yields on investment-grade corporate bonds and Treasuries with the same duration, are just 5% below their highs for the year, notes DoubleLine deputy chief investment officer Jeffrey Sherman. One of the biggest corporate bond ETFs, iShares iBoxx $ Investment Grade Corporate Bond (LQD), plunged 17%, but rebounded sharply and is up 5% year-to-date.

In the March decline, it was possible to pick up high-quality corporate bonds at ultracheap prices, but those opportunities have passed, says Warren Pierson of Baird Funds. There is still “reasonable value in the market,” he says, but fund managers have to hunt for it. Even high-yield bonds have recovered much of their losses. The iShares $ High Yield ETF is only down 2.3% for the year despite a loss of 21.5% just a few months ago.

Sherman says that with the Fed purchasing ETFs that invest in both high-yield and investment grade bonds, investors have begun feeling inappropriately safe: “The Fed is not guaranteeing default positions.”

<<<

>>> Muni Bonds Set for Best Month Since 2009, Shaking Off Fiscal Hit

Bloomberg

By Fola Akinnibi

May 22, 2020

https://www.bloomberg.com/news/articles/2020-05-22/muni-bonds-set-for-best-month-since-2009-shaking-off-fiscal-hit

Tax-free debt heads for 2.7% gain in May, erasing 2020’s loss

Fed intervention, rebound sends cash flooding back in

Municipal bonds are set for their biggest monthly gain since 2009, underscoring the disconnect between the $3.9 trillion market and the economic collapse that’s driving states and cities toward what may be the worst fiscal crisis in decades.

The securities have returned 2.7% so far in May, according to the Bloomberg Barclays index. The rally wiped out the record-setting loss that hammered investors in March and is driving yields back toward the lowest in more than 60 years, with those on benchmark 10-year tax-exempt debt sliding 5 basis points Friday to 0.83%.

The advance has been spurred by an influx of cash into even the riskiest municipal bond funds since the Federal Reserve moved to backstop the market to prevent another liquidity crisis.

Patrick Luby, a municipal-bond analyst with CreditSights Inc., said that investor sentiment has grown less negative as much of the country slowly reopens from the coronavirus shutdowns. At the same time, he said, states and cities are expected to take the steps needed to balance budgets battered by the drop in tax collections.

“The serious and thoughtful way in which many issuers are beginning to wrestle with what are going to be really painful decisions from a financial and human perspective is constructive to the market,” Luby said.

Despite grim news, muni bonds rally back into yearly gain

The market has been whipsawed by unprecedented volatility over the last two months as investors sought to gauge how the shutdown will affect the finances of the thousands of governments and businesses that stand behind municipal bonds. That includes public transit agencies, airports, hospitals and colleges, among others that have been deeply affected by the closing of much of the economy.

With unemployment surging and retail businesses closed, states and cities are predicting hundreds of billions of dollars in budget shortfalls over the next few years. While House Democrats have proposed extending them some $1 trillion in aid, whether any such help will be approved by the Republican-controlled Senate is uncertain.

Even so, the bonds backed by states and cities are among the least likely to default, since governments have the ability to raise taxes and bond payments make up a relatively small share of their budgets.

No state has defaulted since the Great Depression and just a few local governments went bankrupt during the last recession. Since 1970, only about $72 billion of the municipal bonds rated by Moody’s Investors Service defaulted, with about $66.5 billion of that from the bankrupted governments of Detroit, Jefferson County, Alabama, and Puerto Rico, according to a December report from investment firm VanEck.

Still, the muncipal market is dominated by individual investors, who tend to become skittish and withdraw their money when bad news piles up, a phenomenon that analysts refer to as “headline risk.”

“Prices move up or down with greater velocity when you’ve got less liquidity,” said Luby. “There’s still a an enormous amount of uncertainty in the market.”

<<<

>>> Vanguard’s $50 Billion Woman Found Winners in Bond-Market Chaos

Bloomberg

By Liz McCormick

May 20, 2020

https://www.bloomberg.com/news/articles/2020-05-20/vanguard-s-50-billion-woman-found-winners-in-bond-market-chaos?srnd=premium

Wright-Casparius has several funds outperforming most peers

Industry veteran is one of 27 women heading bond funds, ETFs

Vanguard's Wright-Casparius Found Opportunities in Less-Traded Treasuries

Vanguard's Wright-Casparius Found Opportunities in Less-Traded Treasuries

One of the worst-ever bouts of dislocation in the U.S. bond market generated some winning trades for Vanguard Group’s Inc.’s Gemma Wright-Casparius.

As liquidity disappeared amid the pandemic-sparked mayhem in March, the veteran fixed-income portfolio manager saw opportunities, including in older, less-traded Treasuries. The market for these securities had all but vanished after a popular trade that exploits price differences between cash Treasuries and futures blew up.

For Wright-Casparius, the sole head of four actively managed mutual funds with combined assets of about $50 billion, the undervalued securities presented a bargain. As she and a handful of senior colleagues continued to work on the firm’s trading desk in Malvern, Pennsylvania, Wright-Casparius also deemed that inflation expectations had become too dire and increased mortgage-debt holdings. Things soon got so desperate for the bond market that the Federal Reserve stepped in to support it.

Her wagers have paid off, with several of her funds beating most of their peers in 2020. Now, the portfolio manager, who’s been in finance for about 40 years, envisions a long road to economic revival as the nation endures the steepest levels of joblessness since the Great Depression.

“The market gave you some lemons early in March, and we tried to capitalize on that,” Wright-Casparius said in an interview. Going forward, “there’s still a lot of unanswered questions, especially regarding consumer behavior, so the economic recovery should be slow and gradual.”

The $7.2 billion Vanguard Intermediate-Term Treasury Fund, among the four she runs on her own, has returned 7.2% this year -- beating 89% of its peers, according to data compiled by Bloomberg. Her $9.2 billion Short-Term Treasury Fund is outpacing 90% of rivals.

It is part of a select universe of just 31 U.S. fixed-income mutual funds and exchange-traded funds tracked by Morningstar Inc. that were run exclusively by women as of May 1. That tally, helmed by 27 women, is out of more than 2,500 fixed-income funds, with over 2,200 managers, followed by Morningstar. For taxable funds alone, the list shrinks to 16 women.

For women in asset management, progress has been slow, despite widespread focus on the importance of diversity. Even passive funds, a booming area of money management that was once a hot-spot for female talent, have seen the percentage of women managers drop over the past decade.

Women Fail to Gain Ground in Funds World Despite Diversity Push

Still, Wright-Casparius is positive on the prospects for women and is as excited about what she does as when she began her career. Before switching over to asset management, she worked at investment banks including Barclays Plc, where she was director of fixed-income research. She joined Vanguard in 2011.

The two largest holdings in Wright-Casparius’s Intermediate-Term fund as of March 31 were a 0.63% coupon inflation-linked Treasury and a 2.88% coupon regular Treasury, both of which were originally issued in 2018 and mature in 2023, data compiled by Bloomberg show. The fund purchased the former last quarter and added to the latter position during the period, according to the data.

Older securities -- known as off-the-runs -- are tougher to trade even under normal conditions, and were hit hardest by the evaporation of liquidity in March. A blow-up of basis trades -- which exploit price differences between cash Treasuries and futures -- helped stoke the turmoil. That left some off-the-run prices too depressed relative to benchmarks, according to the Vanguard team.

“The volatility in March was breathtaking,” she said. “While part of my management is taking a very long term view, we had dislocations in the Treasury market space and we took advantage.”

‘Accommodative for Years’

The world’s biggest economy will merely hobble back as states and businesses gradually reopen, requiring years of monetary support, in the estimate of Wright-Casparius and her colleagues at the $5.3 trillion asset manager.

U.S. Economy Adds to Grim Records, Signaling Yearslong Recovery

They see the benchmark 10-year Treasury yield bumping around in a range and slowly gliding higher to about 1%, from around 0.7% now. But that level will only be attained by late-2021, when growth finally returns to pre-virus levels and inflation rebounds above the Fed’s 2% target, Wright-Casparius says. Increased government borrowing will help boost long-term yields, said the Queens, New York, native.

The move toward a steeper yield curve -- the gap between 2- and 10-year rates has expanded to about 50 basis points from just above 30 at the start of the year -- will gradually gain momentum, she adds.

“Initially, we see the curve and rates range-bound -- and then toward the recovery phase we are looking for slightly higher yields and slightly steeper curve,” she said.

Vanguard’s downbeat view toward the U.S. growth trajectory is shared by several market veterans and Fed officials. Fed Chairman Jerome Powell says the economy faces unprecedented downside risks that could do lasting damage to households and businesses. The recovery process could stretch through until the end of next year and depend on the delivery of a vaccine, according to Powell.

The central bank has cut rates to near zero and ramped up Treasury purchases to calm markets. It’s also been buying debt in other asset classes, ballooning its balance sheet by more than $2.5 trillion this year.

“The Fed will be accommodative for years,” Wright-Casparius said.

<<<

>>> When United Pawned Old Jets, Bond Traders Sent a Stark Warning

Bloomberg

By Sally Bakewell

May 8, 2020

https://www.bloomberg.com/news/articles/2020-05-09/when-united-pawned-old-jets-bond-traders-sent-a-stark-warning?srnd=premium

Airline pulls $2.25 billion of junk bonds backed by planes

Firms are pledging collateral in bid to raise cash on shutdown

Late on Friday, after some 48 hours of frantic attempts to lure investors to their faltering bond sale, executives at United Airlines let it be known that the deal was dead.

It was an odd moment, stuck smack in the middle of one of the busiest corporate bond booms ever, a period in which investors have shown themselves to be receptive to almost any debt offer backed by good collateral. But this last part was where United got in trouble. For collateral, it had scraped together 360 old jets, some of which analysts considered would be nearly worthless in a few years.

In balking at the deal, investors sent a clear message to CFOs across the country: Don’t try to pawn second-tier assets. Bring us the crown jewels because, regardless of how much Washington policymakers are helping corporate America weather the economic shutdown, the risk of default remains high for all but the most financially solid companies.

“All collateral is not created equal,” said John McClain, a money manager at Diamond Hill Capital Management.

United Air Scraps $2.25 Billion Bond Deal After Terms Disappoint

United Airlines’ attempt to raise $2.25 billion of bonds follows efforts by other virus-stricken companies to mortgage anything they can get their hands on to persuade debt investors to lend them money. In a bid to replace revenue wiped out by the virus pandemic, they’ve pledged private islands in the Caribbean and the Bahamas, cruise ships, movie theaters and even spare engines.

Collateral has been an important safeguard for investors, who have bought billions of dollars of debt from struggling companies in recent weeks. They can seize it if a borrower falters and can’t pay them back in cash. But the United deal shows investors have their limits in who they’ll lend to.

“The collateral issues were too difficult to overcome,” Roger King, an analyst at debt research firm CreditSights, said of the United deal. Borrowers “keep throwing stuff overboard, hoping they can reach the port before there’s nothing left,” he said, likening it to the book “Around the World in 80 Days.”

Companies have been furiously tapping the bond market to shore up liquidity, following unprecedented action by the Federal Reserve last month pledging to buy certain debt. The companies are in dire enough shape that the secured-debt deals are essentially “quasi-rescue trades,” said Ben Burton, head of U.S. leveraged finance syndicate at Barclays Plc.

Gimme Shelter

Sales of secured U.S. high-yield bonds have tripled this year

There’s nothing unusual about struggling borrowers posting swathes of assets against their borrowings. Ford Motor Co. had to mortgage virtually everything it had in 2006 to avoid bankruptcy, arranging some $23.4 billion of debt by putting up all major assets including its blue oval logo. It’s also not unusual for borrowers and lenders to joust over the value of the collateral and whether it’s even accessible to claim.

But in the current depressed environment, even seemingly highly prized collateral is leaving some investors cold. Demand for United Airline’s bonds, for which unofficial price discussions rose to a yield of about 11%, had been weak over the concerns that its collateral wasn’t valuable enough to compensate for the risks.