News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

>>> Hawkins, Inc. blends, manufactures, and distributes various chemical products. The company operates in two segments, Industrial and Water Treatment. The Industrial segment provides industrial chemicals, products, and services primarily to the agriculture, energy, electronics, food, chemical processing, pharmaceutical, medical device, and plating industries. This segment primarily offers acids, alkalis, and industrial and food-grade salts. It also receives, stores, and distributes various chemicals in bulk, including liquid caustic soda, sulfuric acid, hydrochloric acid, phosphoric acid, potassium hydroxide, and aqua ammonia. In addition, this segment manufactures sodium hypochlorite, agricultural products, and certain food-grade products comprising liquid phosphate, lactates, and other blended products; repackages water treatment and bulk industrial chemicals; and performs custom blending of certain chemicals, and contract and private label bleach packaging. It primarily conducts its operations through distribution centers and terminal operations. The Water Treatment segment provides chemicals, equipment, and solutions for potable water, municipal and industrial wastewater, industrial process water, and non-residential swimming pool water. Hawkins, Inc. was founded in 1938 and is headquartered in Roseville, Minnesota. <<<

>>> LyondellBasell Industries N.V., together with its subsidiaries, manufactures chemicals and polymers; refines crude oil; produces gasoline blending components; and develops and licenses technologies for production of polymers. Its Olefins and Polyolefins segment offers olefins, including ethylene, propylene, and butadiene; polyolefins, which include high density polyethylene, low density polyethylene, linear low density polyethylene, and polypropylene (PP); specialty polyolefins comprising PP compounds, catalloy process resins, and polybutene-1 resins; and aromatics, which include benzene. The company?s Intermediates and Derivatives segment provides propylene oxide (PO); PO co-products, such as styrene monomers and tertiary butyl alcohol; PO derivatives consisting of propylene glycol, propylene glycol ethers, and butanediol; acetyls, including methanol, acetic acid, and vinyl acetate monomers; ethylene derivatives, such as ethylene oxide, ethylene glycol, ethylene glycol ethers, and ethanol; and oxyfuels, which include methyl tertiary butyl ether and ethyl tertiary butyl ether. Its Refining segment offers gasoline and components, ultra low sulfur diesel, jet fuel, and lube oils. The company?s Technology segment develops and licenses chemical, polyolefin, and other process technologies, as well as provides associated engineering and other services. This segment also develops, manufactures, and sells polyolefin catalysts. The company operates in Americas, Europe, Asia, and internationally. LyondellBasell Industries N.V. was founded in 2005 and is based in Rotterdam, the Netherlands. <<<

>>> 4 ways to invest in commodities -- and why you should

6/13/2014

By Carolyn Bigda

Kiplinger

http://money.msn.com/exchange-traded-fund/4-ways-to-invest-in-commodities-and-why-you-should

4 ways to invest in commodities -- and why you should

Because commodities such as coffee, oil and gold don't usually move in sync with the stock market, they can help diversify your investment mix.

Coffee beans are prepared for roasting at the Cafe Primavera facility in Itapira, Brazil, on Monday, Feb. 10, 2014. © Paulo Fridman, Bloomberg via Getty Images

.

For the first time since 2010, commodities are showing signs of life. So far this year, a diversified package of commodities is outpacing both the stock and bond markets. But if you hold some of these basic materials in your portfolio -- or are tempted to get back in now -- you'll want to be careful about how you ride the turnaround.

Beyond improving performance, there are two good reasons to hold some commodities -- or, to be more precise, investments that track the price of commodities.

Diversification is one. Research shows that commodities typically don't move in sync with stocks and bonds, and that's holding true now. Year to date, the Dow Jones-UBS Commodity index, which tracks 20 commodity markets, including corn, gold and oil, has gained 7.9 percent, whipping the return of Standard & Poor's 500 Index ($INX +0.31%) by 5.3 percentage points and the Barclays U.S. Aggregate Bond index by 4.5 percentage points (all returns are through May 22).

Commodities can also act as a type of insurance policy against sudden spikes in the price of goods. Inflation in the U.S. has been tame lately, but severe weather and political events have helped push up prices of certain raw materials.

For example, the Indonesian government's decision in January to halt nickel-ore exports propelled the price of the metal (which is used to make stainless steel) to a gain of more than 40 percent so far this year. And a drought in Brazil, the world's largest coffee producer, has helped lift the price of arabica coffee by more than 80 percent since November. Some commodities also serve as safe havens against geopolitical uncertainties. From the beginning of the year through mid-March, when the Russia-Ukraine standoff reached a crescendo, gold climbed 13 percent.

But commodity prices are notoriously volatile, and other trends could serve to keep a limit on prices and maybe even drive them down. One development to watch is slowing growth in China, a major importer of raw materials.

Gold in particular is known for having long boom and bust cycles, and as the U.S. economy improves, fewer investors may seek out the yellow metal as a safe haven. After rallying in the first ten weeks of 2014, gold, at $1,294 per ounce, has fallen 7 percent since mid-March. Paul Christopher, chief international strategist at Wells Fargo Advisors, believes the price could tumble to as low as $1,200 by the end of the year. "We've been advising clients to start unloading," he says.

All of which suggests the road ahead for commodities could be bumpy. Chris Philips, a senior analyst in the investment strategy group at Vanguard, says it's a good idea to keep 5 to 10 percent of your portfolio in commodities -- but only if you're willing to hold on for the long term.

That may be easier to do with a mutual fund or exchange-traded fund that invests across multiple commodities markets. If you bet on a single commodity, you stand a good chance of getting spooked and selling at the wrong time. Recently, Vanguard studied the gains investors earned in SPDR Gold Shares (GLD +0.26%, news), the largest ETF that tracks the price of gold. Vanguard found that from November 2004 (when the fund launched) through February of this year, investors earned an average of 3.2 percentage points per year less than the fund's stated return, mostly because of poor timing decisions. (Investors tended to bail out after prices fell and buy in long after a rebound had started.)

4 great commodities investments to consider

Most commodities funds and ETFs own futures contracts (an agreement to buy or sell a commodity for a set price at a future date). Futures contracts are easier to own than the physical commodity, which must be stored somewhere (and perhaps fed as well). But because of quirks in futures trading, fund performance does not always match that of the underlying commodity. To get around that, some funds buy contracts with varying maturities (rather than just roll over contracts from month to month as they expire, which is what usually happens).

Harbor Commodity Real Return Strategy (HACMX +0.31%, news) is one example of a fund that has done this successfully. The mutual fund, which mirrors the Dow Jones-UBS Commodity index, returned an annualized 6.5 percent over the past five years. That beat 85 percent of the funds in its category, according to Morningstar. Reasonable fees also help. The fund charges just 0.94 percent annually, compared with an average of 1.34 percent for its peer group.

Real Return provides an additional buffer against inflation by buying Treasury inflation-protected securities with the cash it doesn't use to purchase futures contracts. In 2013, when the risk of rising interest rates sent bonds packing, Real Return plummeted a staggering 14.9 percent. But manager Mihir Worah has since shortened the average duration (a measure of a bond's sensitivity to changes in interest rates) for the fund's TIPS. And so far this year, Real Return has gained 10.1 percent.

Exchange-traded PowerShares DB Commodity Index Tracking (DBC 0.00%, news) also buys futures, in its case to track an index of 14 commodities that are weighted based on the economic heft of the good (measured by how much of the commodity is produced and stored globally). The approach is akin to weighting stocks in an index based on company market values.

Year to date, DB has returned a meager 2.9 percent, lagging its index by more than a quarter of a percentage point. But DB also has a record of coming out ahead in down periods, including in 2012, when the fund gained 3.5 percent and its average peer fell 0.5 percent. The fund charges annual fees of 0.85 percent, about average for commodity ETFs.

GreenHaven Continuous Commodity Index (GCC +0.61%, news) takes a different approach to assembling its portfolio. Unlike most of its peers, the ETF does not follow an index with a type of market-weight strategy. Instead, it tracks an index that equally weights futures contracts for 17 commodities.

Equal weighting gives sectors with a smaller economic punch, such as agriculture, more influence over returns. GreenHaven struggled during most of the past three years, but it has returned 11.9 percent so far this year. It has also done a good job of tracking its index.

One final option worth mentioning: Elements Rogers International Commodity (RJI +0.47%, news). This is an exchange-traded note, which is essentially a debt instrument that promises to give you the return of an index. As such, when you invest in an ETN you take on the credit risk of the lender. But Rogers is issued by an agency of the Swedish government, which carries the strongest rating of any ETN issuer, according to Morningstar.

Rogers provides exposure to a whopping 37 commodities, making it one of the most broadly diversified of its peers. From 2008, the ETN's first full year, through 2013, it landed in the top half of its category each year. Annual fees are 0.75 percent.

<<<

Sigma Aldrich -- >>> Dow Chemical and Sigma-Aldrich Sign Supply Pact

By Zacks Equity Research

https://finance.yahoo.com/news/dow-chemical-sigma-aldrich-sign-205638105.html

The Dow Chemical Company’s (DOW) subsidiary – Dow AgroSciences – and Sigma-Aldrich Corporation (SIAL) have signed a manufacturing license and supply agreement, under which, Sigma-Aldrich will make zinc finger nuclease (:ZFN) reagents for use with EXZACT Precision Technology. The financial terms of the agreement were undisclosed.

Per the agreement, Sigma-Aldrich will act as exclusive manufacturer and supplier of ZFN reagents for the platform. The EXZACT Precision Technology is a multi-technology platform that helps in targeted genome modification in plants. The technology is developed by Dow AgroSciences for application in plants. Dow AgroSciences’ platform employs Sangamo Biosciences’ (SGMO) ZFN technology, which the former has licensed for use in plants.

In their decision to integrate ZFNs into their seeds and traits pipeline, Dow chose Sigma-Aldrich, based on the latter’s expertise in manufacturing ZFN reagents as part of the CompoZr platform and its excellent reputation for servicing clients in the Life Sciences market.

Dow AgroSciences is committed to discovering, developing, and bringing to market crop protection and plant biotechnology solutions for the growing world. Recently, Dow AgroSciences has launched a food security initiative in Africa in collaboration with AMPATH, an Indiana University-led consortium.

Through the initiative, Dow AgroSciences and AMPATH will educate the people in Africa to fight hunger by offering local farmers with agricultural knowledge that will help them to improve their crop yield and hence their quality of life. <<<

>>> Rockwood Holdings, Inc. (ROC) develops, manufactures, and markets various specialty chemicals for industrial and commercial applications primarily in Germany, the United States, and Europe. The company operates in two segments, Lithium and Surface Treatment. The Lithium segment offers basic lithium compounds comprising lithium carbonate, which is used as a fluxing agent for enamels, glass, and ceramic production; lithium hydroxide for the use in high performance greases; lithium nitrate for the rubber industry; lithium chloride, which is principally used in gas and air treatment; and potash, a by-product of lithium brine. It also offers special salts that include lithium phosphate, which is used as a catalyst for chemical reactions; lithium bromide that is used for air conditioning applications; and lithium carbonate for pharmaceutical applications, as well as butyllithium/lithium metal products that is used as a polymerization initiator for synthetic rubber and thermoplastic elastomers. In addition, this segment provides battery products for electronic applications in disposable and rechargeable batter industries; lithium compounds and other products for life science applications, such as special reagents for the synthesis of drug intermediates, and for the flavor and fragrances industry; and special metal compounds for X-ray diagnostic systems and airbag applications in chemical, pharmaceutical, metallurgical, automotive, electronics, and pyrotechnical industries. The Surface Treatment segment offers various metal surface treatment products; cleaners, iron phosphates, coolants, paint strippers, and flocculants; corrosion protection products that comprise waxes, which are used to protect airframes; maintenance chemicals for aircraft engines and turbines; and sealants for airplanes. This segment serves automotive, aerospace, and general, as well as steel and metal-working industries. Rockwood Holdings, Inc. was incorporated in 2000 and is based in Princeton, New Jersey. <<<

Stepan, Balchem -- >>> 2 Hidden Gems in the Chemical Space

By Philip Saglimbeni

March 5, 2014

http://www.fool.com/investing/general/2014/03/05/2-hidden-gems-in-the-chemical-space.aspx

When it comes to growth investing, companies operating in trendy industries are among the most popular stock choices among investors. As a result, the majority of long-term investors overlook many utilitarian, small-cap companies. This scenario is a positive for investors seeking value along with growth, as it often means great growth at cheaper valuations.

Perhaps no industry is more overlooked than the chemicals space. The primary reason is that the industry creates products designed to operate behind the scenes and out of the public's purview.

Balchem (NASDAQ: BCPC ) and Stepan (NYSE: SCL ) are two of the best long-term investments in the space; both offer great growth, solid dividend performance and currently trade at relatively cheap valuation multiples.

Exciting growth

While Balchem's and Stepan's chemical businesses may be boring, the growth both companies have been churning out is anything but. In fact, Balchem and Stepan are expected to continue to grow at robust rates going forward. The following is a breakdown of the companies' projected growth in 2014 compared to industry behemoth Dow Chemical (NYSE: DOW ) :

Company

Revenue Growth

EPS Growth

Balchem 9.4% 15.9%

Dow Chemical 3.4% 18.1%

Stepan 6.3% 21.4%

Both Balchem and Stepan are projected to grow sales in 2014 at much faster rates than larger peer Dow Chemical. Even though Balchem is expected to lag both competitors in the earnings-per-share category, 15.9% growth in EPS is still admirable.

Additionally, considering the above-average growth, forward-looking valuation multiples for Balchem and Stepan are not too expensive. Balchem's forward P/E of 24.8 and Stepan's forward P/E of 12.1 are lower than many popular growth stocks growing at comparable levels.

Perhaps most impressive is that despite superior growth all around, Stepan's forward P/E of 12.2 is still cheaper than Dow Chemical's 14.1.

Growth drivers

For Balchem, continued success in its animal nutrition and health department is important. The company's latest expanded alliance with Versus Animal Nutrition assures this. Versus, formerly a supplier to Western Canada only, is now teaming up with Balchem to offer the company's animal nutrient and mineral solutions to all parts of Canada, which vastly expands the company's business in the region.

Additionally, Balchem recently announced an agreement with Taminco to construct and operate a choline chloride facility in Louisiana. Together, Balchem and Taminco will invest to build the facility into a large scale producer of choline chloride, servicing consumers around the world. The facility is expected to go online in 2015.

On the other hand, Stepan's growth in 2014 is expected to come primarily from improving economic conditions around the world as well as positive trends in the company's main consumer markets. Continued global growth in polypol, which is used as energy saving insulant in foam installation, is expected to add significant volume growth in Stepan's polymer segment.

Additionally, the company's latest acquisition of Bayer's North American polyester resin business is now fully integrated and is set to contribute a full year of operation under Stepan control.

On continued international expansion, President and CEO F. Quinn Stepan Jr, explained, "We plan to build a new plant in China to participate [in] what we expect will become the largest polyol market in the world. Overall, the health of our balance sheet remains strong and will facilitate investments in growth and efficiency opportunities. And that will deliver value to you, our shareholders."

Dividend champions

Also worth noting are both companies' impressive track record of paying dividends to investors. Balchem is especially impressive in this regard. Although the company only pays a dividend of $0.26, equal to a yield of 0.50%, Balchem has raised its dividend every year in the last decade and has averaged annual dividend growth of 34.3% in that time.

Stepan's dividend of $0.68, equal to a yield of 1.10%, is more substantial. However, despite consistently raising its dividend each year, the company has only averaged annual dividend growth of 5.5% in the last decade.

Source: Balchem

Bottom line

Flashy companies in trendy industries are not investors' only options for growth. Often times, the smaller and lesser-known companies are better alternatives, particularly because they usually carry significantly less headline risk.

Balchem and Stepan are perfect examples of the benefits of boring but beautiful growth companies. With practical and reliable business mixes, both companies look like viable long-term investments currently trading at value prices.

<<<

Small Cap Materials ETF -- >>> Small-Cap Materials Stocks: Lots of Room for Growth

By Selena Maranjian

December 27, 2013

http://www.fool.com/investing/etf/2013/12/27/small-cap-materials-stocks-lots-of-room-for-growth.aspx

Exchange-traded funds offer a convenient way to invest in sectors or niches that interest you. If you'd like to add some small-cap materials stocks to your portfolio, but don't have the time or expertise to hand-pick a few, the PowerShares S&P Small-Cap Materials ETF (NASDAQ: PSCM ) could save you a lot of trouble. Instead of trying to figure out which small-cap materials stocks will perform best, you can use this ETF to invest in lots of them simultaneously.

The basics

ETFs often sport lower expense ratios than their mutual fund cousins. This ETF, focused on small-cap materials stocks, sports a relatively low expense ratio -- an annual fee -- of 0.29%. The fund is fairly small, too, so if you're thinking of buying, beware of possibly large spreads between its bid and ask prices. Consider using a limit order if you want to buy in.

This ETF is young, but it has topped the world market over the past three years. As with most investments, of course, we can't expect outstanding performances in every quarter or year. Investors with conviction need to wait for their holdings to deliver.

Why small-cap materials stocks?

As the global economic recovery gains traction, demand should grow for materials used in construction, manufacturing, and infrastructure projects. Thus, small-cap materials stocks stand to benefit. And small companies have more ability to grow briskly.

More than a handful of small-cap materials stocks had strong performances over the past year. AK Steel Holding (NYSE: AKS ) , for example, soared 81%. Some expect the recovering auto industry and price hikes to benefit the company, and Goldman Sachs blessed it with a positive outlook last month, too. Bears don't like AK Steel's pension and health-care obligations to retirees, though, and worry that carmakers might decrease their demand for steel in favor of lighter carbon fiber. (The auto industry generates about half of AK Steel's revenue.)

Flotek Industries (NYSE: FTK ) , a drilling and production-related specialist, gained 69%. Its third-quarter revenue jumped 25%, while net income was below year-ago levels. The company's chemical sales were hurt by the flooding in Colorado earlier this year, but management noted that, "The acquisition of Florida Chemical is already providing both marketing and production synergies that should lead to meaningful revenue and profit growth in the quarters ahead."

Globe Specialty Materials (NASDAQ: GSM ) , specializing in silicon metals and alloys, surged 34%. The company topped some expectations for revenue in its recently reported quarter, but revenue dropped 14%. China was blamed, in part, for dumping a lot of silicon in Canada. Globe Specialty Materials has announced a stock buyback plan, valued at up to $75 million. It has also boosted its capacity by acquiring Siltech.

Other small-cap materials stocks didn't do quite as well during the last year, but could see their fortunes change in the coming years. Stillwater Mining (NYSE: SWC ) dropped 3%, as the sole public U.S. producer of platinum and palladium has profited from platinum-group metals pricing increases. Those are due, in part, to growing auto sales, and also to labor unrest in South Africa, a competing production region. Stillwater Mining has a new CEO and, in its last quarter, reported a net loss, though revenue growth was robust. It also greatly reduced the value of its Argentinean copper reserves.

The big picture

If you're interested in adding some small-cap materials stocks to your portfolio, consider doing so via an ETF. A well-chosen ETF can grant you instant diversification across any industry or group of companies -- and make investing in and profiting from it that much easier.

<<<

>>> Chemtura Corporation, together with its subsidiaries, engages in the manufacture and sale of specialty chemical solutions and consumer products worldwide. Its Industrial Performance Products segment provides products, such as petroleum additives that provide detergency, friction modification, and corrosion protection in automotive and industrial lubricants and greases, synthetic finished lubricants, synthetic base-stocks and greases used in aviation, industrial, and refrigeration applications; castable urethane pre-polymers engineered to provide abrasion resistance and durability in industrial and recreational applications; and polyurethane dispersions and urethane pre-polymers used in various types of coatings, such as wood floor finishes, glass fiber coatings, and textile treatments. The company's Industrial Engineered Products segment offers catalyst components, surface treatments, flame retardants and a bromine based product line used as agricultural and pharmaceutical intermediates, completion fluids for oil and gas extraction, and mercury control products for coal fired power stations. Its Consumer Products segment provides recreational water purification products, such as sanitizers, algaecides, biocides, oxidizers, pH balancers, mineral balancers, and other specialty chemicals and accessories; and specialty and multi-purpose cleaners. The company's Chemtura AgroSolutions segment produces seed treatments, fungicides, miticides, insecticides, growth regulators, and herbicides. The company has a strategic alliance with Isagro S.p.A. It serves various industries, such as agriculture, automotive, building and construction, electronics, lubricants, packaging, plastics, pool and spa chemicals, and transportation. Chemtura Corporation was founded in 1900 and is headquartered in Philadelphia, Pennsylvania. <<<

Westlake Chemical -- >>> Westlake Upgraded to Strong Buy

By Zacks Equity Research

January 15, 2014

http://finance.yahoo.com/news/westlake-upgraded-strong-buy-201005460.html

On Jan 15, Zacks Investment Research upgraded specialty chemicals company Westlake Chemical Corp. (NYSE:WLK) to a Zacks Rank #1 (Strong Buy).

Why Upgraded?

Westlake posted strong third-quarter 2013 results on healthy gains from higher pricing and lower feedstock costs, stemming from North American shale gas production. The company’s earnings for the quarter climbed to $2.54 per share from $1.30 per share a year ago, outshining the Zacks Consensus Estimate of $2.21. Profit zoomed roughly 96% year over year to $170.3 million.

Westlake has delivered positive earnings surprises in the last four quarters with an average beat of 20.61%. The company's long-term estimated earnings per share growth rate is 6%.

Revenues rose roughly 22% year over year to around $1,004 million in the quarter, beating the Zacks Consensus Estimate of $935 million. In the quarter, Westlake benefited from increased sales volumes for styrene and caustic, higher selling prices and contributions from its specialty PVC pipe business (acquired in May 2013).

Westlake also saw higher olefins and vinyls integrated product margins in the third quarter, thanks to higher selling prices for key products. Increased ethylene production at the company’s Lake Charles complex also contributed to olefins margin expansion.

Sales from Westlake’s Olefins segment jumped roughly 26% year over year to $679.3 million in the third quarter. The Vinyls segment recorded sales increase of around 15% year over year to $324.8 million.

Following the release of the third quarter results, the Zacks Consensus Estimate for 2013 for Westlake has gone up 7.3% to $8.65 per share. The Zacks Consensus Estimate for 2014 has also increased 4.4% to $9.47.

Westlake begun operations at its new chlor-alkali plant located at its vinyls manufacturing complex in Geismar, La. on Dec 27. The new plant uses membrane technology and has an annual production capacity of 350,000 electrochemical units (ECU's).

Westlake expects continued cost benefits from North American shale gas production. The company continues to invest to capture this cost advantage. The company is committed to boost shareholder returns through higher dividend payouts. This is evident as Westlake’s Board declared a 20% hike in its quarterly dividend to 22.5 cents per share from the previous payout of 18.75 cents per share in Aug 2013.

Other Stocks to Consider

Other companies in the specialty chemical space with favorable Zacks Rank are Chemtura Corp. (NYSE:CHMT), A. Schulman, Inc. (NASD:SHLM) and PolyOne Corp. (NYSE:POL). All these carry a Zacks Rank #2 (Buy).

<<<

>>> RPM International Inc. manufactures, markets, and sells specialty chemical products for industrial and consumer markets in the United States and internationally. The company operates through two segments, Industrial and Consumer. The Industrial segment offers waterproofing and institutional roofing systems; sealants, tapes, and foams; residential home weatherization systems; roofing and building maintenance and related services; insulated building cladding materials; industrial adhesives and sealants; concrete and masonry additives, and related construction chemicals; polymer flooring systems; and industrial and commercial tile systems. This segment also provides fiberglass reinforced plastic gratings and shapes for industrial platforms, staircases, and walkways; corrosion-control coatings, containment linings, fireproofing and soundproofing products, and heat and cryogenic insulation products; bridge expansion joints, bridge deck and parking deck membranes, curb and channel drains, highway markings, protective coatings, and concrete repairs; fluorescent colorants and pigments; shellac-based-specialty coatings for industrial and pharmaceutical uses, edible glazes, and food coatings; exterior insulating and finishing systems; and fire and water damage restoration, and carpet cleaning and disinfecting products. The Consumer segment manufactures and markets professional use and do-it-yourself (DIY) products for various consumer applications, including home improvement and personal leisure activities. This segment offers nail care enamels, coating components, specialty products for paint contractors and the DIYers, deck and fence restoration products, metallic and faux finish coatings, hobby paints and cements, caulks, sealants, adhesives, and insulating foams, as well as spackling, glazing, and other general patch and repair products. It sells its products directly, as well as through distributors. The company was founded in 1947 and is headquartered in Medina, Ohio. <<<

>>> PPG Industries, Inc. operates as a coatings and specialty products company. The company's Performance Coatings segment offers coatings products for automotive and commercial transport/fleet repair and refurbishing, light industrial coatings, and specialty coatings for signs; supplies sealants, coatings, technical cleaners and transparencies for commercial, military, regional jet and general aviation aircraft and transparent armor for military land vehicles; and coatings and finishes for the protection of metals and structures to metal fabricators, heavy duty maintenance contractors, and manufacturers of ships, bridges, rail cars, and shipping containers. Its Industrial Coatings segment offers industrial and automotive coatings for manufacturing companies; and packaging coatings and inks to the manufacturers of aerosol, food, and beverage containers. The company's Architectural Coatings ? Europe, Middle East, and Africa segment provides coatings used by painting and maintenance contractors and by consumers for decoration and maintenance of residential and commercial building structures, as well as purchased sundries to painting contractors and consumers. Its Optical and Specialty Materials segment offers Transitions lenses, optical lens materials, and sunlenses; amorphous precipitated silicas for tire, battery separator, and other end-use markets; and Teslin substrate used in applications, such as radio frequency identification tags and labels, e-passports, drivers? licenses, and identification cards. The company's Glass segment supplies flat glass and continuous-strand fiber glass products for commercial and residential construction and the wind energy, energy infrastructure, transportation, and electronics industries. PPG Industries sells its products through company-owned stores, home centers, paint dealers, and independent distributors, as well as directly to customers worldwide. The company was founded in 1883 and is headquartered in Pittsburgh, Pennsylvania. <<<

>>> PolyOne Corporation provides specialized polymer materials, services, and solutions with operations in specialty polymer formulations, color and additive systems, polymer distribution, and specialty vinyl resins. The company operates in four segments: Global Specialty Engineered Materials; Global Color, Additives, and Inks; Performance Products and Solutions; and PolyOne Distribution. The Global Specialty Engineered Materials segment offers custom polymer formulations, services, and solutions for designers, assemblers, and processors of thermoplastic materials across various markets and end-use applications. The Global Color, Additives, and Inks segment provides specialized color and additive concentrates, inks, latexes, performance enhancing additives, liquid colorants, and fluoropolymer and silicone colorants. The Performance Products and Solutions segment offers vinyl formulations and alloys, and specialty coating materials based on vinyl to various manufacturers of plastic parts and consumer-oriented products. This segment also provides materials testing and component analysis, custom compound development, colorant and additive, design assistance, structural analysis, process simulations, and extruder screw design services, as well as offers contract manufacturing services to polymer marketers. The PolyOne Distribution segment distributes approximately 3,500 grades of engineering and commodity grade resins to custom injection molders and extruders. The company primarily serves appliance, consumer, healthcare, transportation, building and construction, packaging, wire and cable, electrical and electronics, industrial, and textiles markets. PolyOne Corporation sells its products worldwide through direct sales personnel, sales agents, and distributors. The company was founded in 1927 and is headquartered in Avon Lake, Ohio. <<<

>>> NewMarket Corporation, through its subsidiaries, engages in the petroleum additives and real estate development businesses. It operates in two segments, Petroleum Additives and Real Estate Development. The Petroleum Additives segment develops, manufactures, and blends lubricant additives that are used in various vehicle and industrial applications, including engine oils, transmission fluids, gear oils, hydraulic oils, turbine oils, and in other applications where metal-to-metal moving parts are utilized. This segment also manufactures engine oil, driveline, and industrial additives. It offers petroleum additives to oil companies and refineries, original equipment manufacturers (OEMs), and other specialty chemical companies. In addition, this segment offers fuel additives that are used to enhance the oil refining process and the performance of gasoline, diesel, biofuels, and other fuels to stringent industry, government, OEM, and individual customers. The Real Estate Development segment owns and manages approximately 64 acres of real estate property in Richmond, Virginia. The company has operations in the United States, Europe, Asia, Latin America, Australia, the Middle East, and Canada. NewMarket Corporation was founded in 1887 and is headquartered in Richmond, Virginia. <<<

WR Grace -- >>> Grace's Chapter 11 Reorganization Plan Effective: GRA Added To Post-Bankruptcy Stock Index

Feb. 11, 2014

About: GRA, Includes: AAL, DOW, KODK

http://seekingalpha.com/article/2012091-graces-chapter-11-reorganization-plan-effective-gra-added-to-post-bankruptcy-stock-index?source=yahoo

After nearly thirteen long years operating under Chapter 11 protection, chemical & construction icon W.R. Grace & Co. has finally emerged from bankruptcy. The information provided below details Grace's history, Chapter 11 reorganization and post-bankruptcy stock prospects. GRA is the most recent addition to The Turnaround Letter's Post-Bankruptcy Stock IndexTM, which reflects the post-bankruptcy investing climate by tracking the 20 largest post-bankruptcy stocks within the four-year span immediately after their emergence. Other recent additions to the Index include American Airlines (AAL) and Eastman Kodak (KODK).

Corporate Background

Today's Grace is a premier specialty chemicals and materials provider. The Company dates back to 1854, when William Russell launched operations in Peru. Twenty years later, Grace relocated to The Big Apple and was formally chartered and incorporated in 1872 and 1899, respectively. Grace launched its NYSE listing in 1953, and the Company first entered the specialty chemicals industry the following year with its acquisition of Dewey & Almy Chemical Company and Davison Chemical Company. These purchases specifically established the Company's catalysts, packaging, silicas and construction product lines.

Chapter 11 Filing

This bankruptcy was the result of an increase in the number of personal injury and property damage claims asserted against the Company as a result of exposure to asbestos contained in certain previously-manufactured products. In 2000, asbestos-related claims against the Company rose 81%, with an even higher rate of increase during the first three months of 2001 - seriously threatening Grace's core business operations.

The Company ultimately concluded that the only way to define and resolve its asbestos liabilities, while preserving the value and viability of core business operations, was a reorganization under Chapter 11 of the Bankruptcy Code. As of its April 2001 petition date, W.R. Grace was a defendant in approximately 70,000 asbestos-related lawsuits related to property damage and personal injury claimants. Grace's April 2001 Chapter 11 filing included 62 of the Company's domestic entities but none of its foreign subsidiaries.

After nearly ten contentious years operating under Chapter 11 protection, the U.S. Bankruptcy Court entered an order confirming the First Amended Joint Plan of Reorganization, as modified and filed by Grace, the Official Committee of Asbestos Personal Injury Claimants, the asbestos personal injury Future Claimants Representative and the Official Committee of Equity Security Holders. In her opinion, Judge Judith Fitzgerald resolved all outstanding objections to the Joint Plan in favor of Grace and its co-proponents.

As a result of the asbestos-related nature of the proceeding, Grace also needed U.S. District Court approval of its Plan. In January 2012, the District Court issued an order denying all objections and confirming the Plan in its entirety. The District Court reaffirmed its January 2012 confirmation order on June 11, 2012 following a motion for reconsideration. The District Court order states, "Having now reviewed several thousand pages of party briefing and having had the benefit of two oral arguments, the Court finds that the parties' Objections are denied, and…the Joint Plan is confirmed in its entirety."

During 2013, five separate appeals were argued before the Third Circuit Court of Appeals. The Court denied four appeals in the third quarter of 2013; and, in the fourth quarter, the Company settled a fifth appeal relating to the amount of interest payable on its pre-petition bank debt and recorded a $129 million charge.

The Plan finally became effective on February 3, 2014 after Grace's $2.6 billion bankruptcy lumbered on for nearly 13 years - more than double the average stint of the majority of asbestos-related Chapter 11 filings, as detailed below:

•Interior finishings retailer Armstrong World Industries, Inc. ($4.2 billion in assets) from December 2000 through October 2006.

•Energy services provider The Babcock & Wilcox Company (a subsidiary of McDermott International, Inc.) from February 2000 through February 2006.

•Machinery and auto parts manufacturer Eagle-Picher Industries, Inc. ($479 million in assets) from January 1991 through November 1996.

•Automotive parts manufacturer Federal-Mogul Corporation ($10.1 billion in assets) from October 2001 through December 2007.

•Composite materials provider Keene Corp. (with $132 million in assets) from December 1993 through July 1996.

•Building products manufacturer Manville Corp. ($2.8 billion in assets) from August 1982 through November 1988.

•Mineral products supplier Owens Corning ($6.5 billion in assets) from October 2000 through September 2006.

•Materials manufacturer Raytech Corp. ($73 million in assets) from March 1989 through July 2006.

•Steel tubing/products manufacturer UNR Industries, Inc. (with $219 million in assets) from July 1982 through September 1989.

•Building products manufacturer USG Corporation ($3.2 billion in assets) from June 2001 through June 2006.

Key Terms of Reorganization Plan

Grace's confirmed and effective Plan establishes two asbestos trusts, under Section 524(g) of the U.S. Bankruptcy Code, to compensate personal injury claimants and property owners. Funds for the trusts will come from a variety of sources, including cash, warrants to purchase the Company's common stock, deferred payment obligations, insurance proceeds and payments from successor companies.

Upon the Plan's effective date, the personal injury trust was funded with the following: A) $557.75 million in cash from Grace; B) a warrant to acquire 10 million shares of Grace's common stock at an exercise price of $17.00 per share, expiring one year after effective date; C) rights to all proceeds under all of Grace's insurance policies that are available for payment of personal injury claims; D) $42.13 million in cash from a subsidiary of Fresenius AG, pursuant to the terms of a settlement agreement resolving asbestos-related, successor liability and fraudulent transfer claims against Fresenius; and E) $856.82 million in cash and 18 million shares of Sealed Air Corporation's common stock paid by Cryovac, Inc., a wholly-owned subsidiary of Sealed Air, pursuant to the terms of a settlement agreement resolving asbestos-related, successor liability and fraudulent transfer claims against Cryovac and Sealed Air.

The Company is obligated to make $110 million in deferred payments to the personal injury trust for five years beginning in 2019 and $100 million annually for ten years beginning in 2024, which obligation is secured by Grace's obligation to issue 77,372,257 shares of the Company's common stock to the asbestos trusts in the event of default.

All property damage claims have been channeled to the property damage trust for resolution, and the property damage trust contains two accounts: the property damage account and the Zonolite attic insulation property damage account. Following the effective date, unresolved and future non-Zonolite attic insulation property damage claims are to be litigated pursuant to procedures to be approved by the U.S. Bankruptcy Court and, to the extent such property damage claims are determined to be allowed claims, are to be paid in cash by the property damage trust.

On the effective date, the Zonolite attic insulation property damage account of the property damage trust was funded with approximately $34.36 million in cash from Cryovac and Fresenius. Grace is obligated to make a payment of $30 million in cash to the Zonolite attic insulation property damage account on the third anniversary of the effective date and to make upto ten contingent deferred payments of $8 million annually to the Zonolite attic insulation property damage account during the 20-year period beginning on the fifth anniversary of the effective date (with each such payment due only if the assets of the Zonolite attic insulation property damage account fall below $10 million during the preceding year).

The property damage trust is to resolve U.S. Zonolite attic insulation property damage claims that qualify for payment by paying 55% of the claimed amount, but in no event is the property damage trust to pay more per claim than 55% of $7,500 (as adjusted for inflation each year after the fifth anniversary of the effective date).

Concurrent with effectiveness of this Plan, the Company entered into a credit agreement with Goldman Sachs Bank USA, as administrative agent that provides for the following: a $250 million revolving facility due 2019, a $150 million multicurrency revolving facility due 2019, a $700 million term loan due 2021, a 150 million euro term loan due 2021 and a $250 million delayed draw term loan facility due 2021.

Post-Bankruptcy Outlook

Grace emerges from Chapter 11 protection as a publicly-traded entity (GRA). As of December 31, 2013, the Company estimated its consolidated assets to be $5,398.4 million; consolidated liabilities to be $4,827.2 million and stockholders' equity of $571.2 million. The Turnaround Letter has long maintained that post-bankruptcy stocks represent an interesting investing sector because they operate in such an inefficient niche and often move independent of the overall market. Although some companies take advantage of the Chapter 11 process to reshape businesses and balance sheets - to ultimately emerge as stronger, more competitive entities - investors are often biased against post-bankruptcy situations. As a result, these companies can be undervalued and, in select situations, represent an appealing turnaround investing opportunity.

New Generation Research's Post-Bankruptcy Stock IndexTM monitors the market capitalization of the 20-largest post-bankruptcy stocks, and GRA will now be added to the Index - joining other recent additions AMR and Eastman Kodak. Since its inception on January 1, 2012, the Index has significantly outperformed, gaining 92.6% versus 42.7% for the S&P 500 Index. In terms of recent performance, post-bankruptcy stocks have very slightly underperformed the S&P, 19.2% to 19.5%, over the past twelve months. The Index's post-bankruptcy stocks underperformed over the first part of last year but caught up later in the year, outperforming the S&P over the last three- and six-month periods (see graphic below).

As of February 3, 2014, 77,063,385 shares of Grace's common stock were issued and outstanding; and an aggregate of 87,372,257 shares of the Company's common stock are reserved for future issuance in respect of claims and interests filed and allowed under the Plan. Grace has been quick to address post-bankruptcy investor sentiment. Just two days after emergence, its board authorized a $500-million share repurchase program to be completed over the next 12 to 24 months. Fred Festa, chair and CEO, comments, "This program demonstrates our commitment to increasing long-term shareholder value. Our strong balance sheet and cash flow provide the financial flexibility both to invest in growth and return capital to shareholders."

Although Grace's long-term post-bankruptcy financial health and investing appeal remain to be seen, I do like current prospects for this sector, as a whole--which is why I recently highlighted ten stock picks within the chemical industry. Many chemical companies appear to be well-positioned to profit from the continuing economic rebound in the United States and other parts of the world. Increased industrial activity will boost demand for numerous chemical products. Moreover, low natural gas prices in the U.S. are a boon to domestic chemical producers since they use gas as both an energy source and a raw material. For example, Dow Chemical (DOW) looks even more attractive now in light of the news that activist hedge fund manager Dan Loeb has taken a big position in the stock. Learn more about my favorite value stock opportunities within the chemical sector.

<<<

>>> LyondellBasell Industries N.V., together with its subsidiaries, manufacturers and sells chemicals and polymers; refines crude oil; produces gasoline blending components; and develops and licenses technologies for the production of polymers. The company?s Olefins and Polyolefins segment offers olefins, including ethylene, propylene, and butadiene; polyolefins that comprise polypropylene (PP), high density polyethylene, low density polyethylene, and linear low density polyethylene; aromatics, which include benzene; and specialty polyolefins, such as catalloy process resins, as well as PP compounds and polybutene-1 resins. Its Intermediates and Derivatives segment provides propylene oxide (PO); PO co-products, including styrene monomers, tertiary butyl alcohol, and its derivative isobutylene; PO derivatives, which consists of propylene glycol, propylene glycol ethers, and butanediol; acetyls, such as methanol, acetic acid, and vinyl acetate monomers; and ethylene derivatives, including ethylene oxide, ethylene glycol, ethylene glycol ethers, and ethanol. This segment also provides gasoline blending components, such as methyl tertiary butyl ether and ethyl tertiary butyl ether. The company?s Refining segment offers gasoline and components, ultra low sulfur diesel, jet fuel, lube oils, and alkylate. Its Technology segment develops and licenses chemical, polyolefin, and other process technologies, as well as associated engineering and other services. This segment also develops, manufactures, and sells polyolefin catalysts. LyondellBasell Industries N.V. operates in the Americas, Europe, Asia, and internationally. The company was founded in 2005 and is based in Rotterdam, the Netherlands. <<<

>>> FMC Corporation, a diversified chemical company, provides solutions and products for agricultural, consumer, and industrial markets. It operates in three segments: Agricultural Products, Specialty Chemicals, and Industrial Chemicals. The Agricultural Products segment develops, markets, and sells crop protection chemicals, including insecticides, herbicides, and fungicides. Its insecticides are used to protect various crops comprising cotton, sugarcane, rice, corn, soybeans, cereals, fruits, and vegetables from insects, as well as for non-agricultural applications, including pest control for home, garden, and other specialty markets. This segment?s herbicides are used to protect crops from weed growth, as well as for non-agricultural applications, such as turf and roadsides; and fungicides are used to protect fruits and vegetables crops from fungal disease. The Specialty Chemicals segment is involved in biopolymer and lithium businesses. This segment offers food ingredients that are used to enhance texture, color, structure, and physical stability; pharmaceutical additives for binding, encapsulation, and disintegrant applications; ultrapure biopolymers for medical devices; and lithium for energy storage, specialty polymers, and pharmaceutical synthesis. The Industrial Chemicals segment manufactures a range of inorganic materials, including soda ash, hydrogen peroxide, specialty peroxygens, zeolites, and silicates. Its soda ash is used in glass, chemicals, and detergents; peroxygens are used in pulp and paper, chemical processing, detergents, antimicrobial disinfectants, electronics, polymers, and environmental applications; and zeolites and silicates are used in tires, detergents, and pulp and paper. The company operates in North America, Europe, the Middle East, Africa, Latin America, and the Asia Pacific. FMC Corporation was founded in 1883 and is headquartered in Philadelphia, Pennsylvania. <<<

>>> DAVOS: Novozymes Plants Seeds for the Future.

By Jonathan Buck

January 23, 2014

http://blogs.barrons.com/stockstowatchtoday/2014/01/23/davos-novozymes-plants-seeds-for-the-future/?mod=yahoobarrons&ru=yahoo

Novozymes (NVZMY) looks set to deliver a steadier performance for shareholders in 2014.

The company’s stock has jumped about 37% in the past 12 months, a performance it seems unlikely to replicate this year. Its American depository receipts closed Wednesday at $43.74, just off their 52-week high of $44.05. But the company, which produces industrial enzymes and micro-organisms that are used in everything from food to biopharmaceuticals, can still generate healthy returns for shareholders – as much as 10% or more in the next 12 months.

At Wednesday’s close, the stock trades at more than 30 times forecast 2014 earnings of $1.40 per share. It looks pricey, but Novozymes has traded at similar levels for long periods in the past. On forecast 2015 earnings, it trades at a multiple of 28.

But analysts aren’t convinced. Many are neutral on the stock and a consensus price target compiled from analysts’ estimates of $40.51 suggests it can fall about 10%. The more optimistic have price targets approaching $50, suggesting upside of roughly 14%.

The Bagsvaerd, Denmark-based company, which has a market value approaching $14 billion, predicts juicier profit margins in 2014 and cites an alliance with Monsanto (MON) for the optimism. It reported its profit margin will grow to between 25% and 26% this year from 24.7% in 2013.

Profits rose 6% in 2013, in line with expectations, on sales that increased 5% to 11.75 billion Danish krone ($2.15 billion), but Novozymes expects stronger earnings in coming years. It predicts growth of 6% to 9% in 2014 and it is aiming for 10% or more in 2015 and beyond.

Part of its optimism comes from the deal with Monsanto. The two companies in December agreed to develop bioagricultural products that allow farmers to increase crop yields. Under the terms of the deal, Novozymes receives $300 million from Monsanto in recognition of its ongoing business and microbial capabilities.

As soon as regulators clear the deal – and Novozymes CEO Peder Holk Nielsen expects no stumbling blocks – the company will hit the ground running. Timing is still uncertain, but the alliance could have products ready to market in time for the spring planting season in the northern hemisphere, Nielsen said in an interview on the sidelines of the World Economic Forum in Davos.

Nielsen sees potential for the venture with Monsanto to market bioagricultural products to countries outside North America and to target seeds not just to regions or farms but to individual fields. The technology can produce good results in rich soils but outstanding results in “distressed soils or lighter soils” such as those found in emerging markets, Nielsen said.

He expects the venture will have an impact on revenue from 2015 onward. “The bigger bet is on the other side of 2020,” he said.

“Farmers from now until 2050 are going to produce more food than farmers have for the last 10,000 years,” he adds.

Bioagriculture and cellulosic ethanol have the potential to transform Novozymes, but Nielsen cautions that both also could fall flat if scientists don’t understand the science of bio-ag products or if the take-up of biofuel fails to live up to expectations.

But right now the future looks encouraging. In the absence of acquisitions, the company also plans to buy back up to about $365 million of shares.

Shareholders could bring in a bumper harvest in the medium term.

<<<

>>> PolyOne's Turkey Facility Comes Online

By Zacks Equity Research

December 17, 2013

http://finance.yahoo.com/news/polyones-turkey-facility-comes-online-153004628.html

Specialty polymer materials maker PolyOne Corporation (POL) has commenced production in its new facility in Turkey. Based in Istanbul, the facility has been geared to offer high-level production, service and flexibility characteristics required by the company’s customers.

The operations involve increased capabilities to better serve PolyOne’s customers with an extended portfolio of specialty polymer formulations. Apart from offering state-of-the-art manufacturing, the new location provides a specially designed layout for customer meetings, training and collaboration.

PolyOne is seeing increasing demand for its solutions in Turkey. It is among the fastest growing markets for thermoplastics globally. According to the Turkish plastics industry association – Pagev – the country’s plastics industry is growing at more than 10% annually. PolyOne’s specialty polymer solutions address the needs of original equipment manufacturers and plastics processors in the region.

PolyOne, which currently retains a Zacks Rank #3 (Hold), is a leading provider of specialized polymer materials, services and solutions. It has annual sales of $2.9 billion and operations around the world.

PolyOne reported healthy third-quarter 2013 results in Oct 2013. Its profit from continuing operations went up roughly 20% year over year to $23.2 million or 24 cents per share. Adjusted earnings jumped 29% year over year to 36 cents per share.

Revenues shot up 43% year over year to $1 billion from $708 million a year ago on the heels of the acquisitions of Spartech and Glasforms and organic growth across specialty and distribution businesses.

PolyOne believes that it can continue to deliver double-digit adjusted earnings per share growth in the final quarter of 2013. Based on its current trajectory of organic growth and upside from Spartech synergy capture, the company backed its target of achieving adjusted earnings of $2.50 per share by 2015.

Other companies in the chemical and related industries worth considering include Asahi Kasei Corporation (AHKSY), Westlake Chemical Corp. (WLK) and A. Schulman, Inc. (SHLM). While Asahi Kasei holds a Zacks Rank #1 (Strong Buy), both Westlake Chemical and A. Schulman carry a Zacks Rank #2 (Buy).

<<<

>>> Sigma-Aldrich Collaborates With CatScI

By Zacks Equity Research

November 6, 2013

http://finance.yahoo.com/news/sigma-aldrich-collaborates-catsci-232503356.html

Sigma-Aldrich Corporation (SIAL) announced that its custom manufacturing services business unit – SAFC Commercial – has entered into a services agreement with CatScI Ltd. With the deal in place, SAFC customers will get access to metal removal, recovery and recycling services along with immediate access to new reactions, homogeneous and heterogeneous catalysis, biocatalysts, solvent selection and process development.

The partnership will leverage CatScI’s expertise in catalyzed reactions and complex chemical processes and SAFC’s process development, scale-up, and manufacturing know-how.

CatScI provides novel solutions and caters to all types of challenging synthetic chemistry problems. The company has a strong technology platform and provides differentiated services in a cost and time efficient manner. CatScI provides expertise in both chemo and bio-catalysis and the customers can take advantage of it for the suggestion, screening, selection, development and optimization of reactions and processes.

Catalysis is gaining importance in the pharmaceutical industry and about 90% of chemicals now require the use of catalytic processes in their manufacture. With chemical processes becoming more and more complex, industrial chemists look forward to employing catalysis to achieve concise and economical processes in R&D and production.

CatScI is a UK-based catalysis company that aims at maximizing yield, optimizing quality, reducing waste and minimizing chemical development costs through reaction understanding. Sigma-Aldrich is a lab chemical and life sciences company focused on enhancing human health and safety.

Sigma-Aldrich currently maintains a Zacks Rank #3 (Hold).

Other companies in the specialty chemical industry worth considering are Ecolab Inc. (ECL), Ferro Corporation (FOE), and HB Fuller Co. (FUL). All of them carry a Zacks Rank #2 (Buy).

<<<

Specialty Chemicals -- >>> Investing in Specialty Chemicals Companies Whose End Markets Have Sustainable Demand Characteristics: Expert Analyst Chris Kapsch Discusses Where Investors are Gravitating in the Sector

Wall Street Transcript

Jul 24, 2013

http://finance.yahoo.com/news/investing-specialty-chemicals-companies-whose-153200383.html

67 WALL STREET, New York - July 24, 2013 - The Wall Street Transcript has just published its Agricultural & Specialty Chemicals Report offering a timely review of the sector to serious investors and industry executives. This special feature contains expert industry commentary through in-depth interviews with public company CEOs and Equity Analysts. The full issue is available by calling (212) 952-7433 or via The Wall Street Transcript Online.

Topics covered: Crop Yield Management - U.S. Corn Crop - Chemicals Companies Pricing Power - Fertilizers, Paints and Coatings, and Petrochemicals - Emerging Market Demand - Specialty Chemicals and Fertilizer Pricing Power

Companies include: Avery Dennison Corporation (AVY), Monsanto Co. (MON), W.R. Grace & Co. (GRA), Hexcel Corp. (HXL), American Vanguard Corp. (AVD), Polypore International Inc. (PPO), OM Group Inc. (OMG), Albemarle Corp. (ALB) and many more.

In the following excerpt from the Agricultural & Specialty Chemicals Report, an expert analyst discusses the outlook for the sector for investors:

TWST: What is the level of investor interest in specialty chemicals at the moment, and do you think investors are correctly assessing the opportunities for investment in this sector?

Mr. Kapsch: The specialty chemical industry remains highly fragmented and eclectic in nature, and therefore investment themes are very company and stock-specific.

Currently, there is a disparity across the valuation spectrum across the group, with investors gravitating to those names whose end markets have sustainable demand characteristics or that exhibit fundamentals with sustainable demand characteristics, such as aerospace or those that are exposed to end markets where there's increasing evidence of a positive inflection off of cyclical troughs, such as construction and automotive. So it seems like investors are gravitating toward those names the most, which I think is probably prudent at this juncture.

However, this inclination has left a lot of other names, many with other positive investment merits, behind in terms of valuation metrics, thus somewhat out of favor. So there are longer-term investment opportunities in the companies that have less near-term visibility with respect to their end market profiles at this point in the economic cycle.

TWST: What is your outlook for M&A in the specialty chemicals sector over in the short- to midterm?

Mr. Kapsch: Reflecting on the fragmented nature of the space, and given that corporate balance sheets are generally healthy, companies' free cash flow is relatively strong, and considering the unprecedented cheap financing right now, companies should be inclined to engage in M&A activity as a way of accretively benefiting equity shareholders. So I think there's a good chance of increasing activity in the chemicals space, particularly if boards have any confidence that economic recovery looking...

<<<

Cereplast -- >>> Cereplast Provides an Overview of the First Half of 2013 and an Outlook for the Remainder of the Year

Press Release: Cereplast, Inc

Jul 30, 2013

http://finance.yahoo.com/news/cereplast-provides-overview-first-half-120000360.html

SEYMOUR, Ind., July 30, 2013 (GLOBE NEWSWIRE) -- Cereplast, Inc. (CERP) (the "Company"), a leading manufacturer of proprietary biobased, compostable and sustainable bioplastics, today is providing a shareholder update including an overview of the first half of 2013 and an outlook for the remainder of the year. The Company has made great strides over the past seven months and anticipates continued growth and success during the rest of 2013.

Compared to 2012, revenue for the first 6 months of 2013 experienced major growth, with the expected number to top approximately $1.7MM compared to about $0.2MM in 2012, reflecting a nearly 800% increase. This growth was fueled by the passing of Italian legislation that will require merchants to replace traditional single-use plastic bags with bioplastic and other alternatives. Severe sanctions will be imposed upon merchants that do not comply. Although this legislation is pending enforcement, management expects it to go into full effect in the fall of 2013. Upon enforcement, the Company believes that there will be a substantial increase in demand for its bioplastic resins. For the past 18 months, the Company has nurtured a group of over 70 Italian companies that have completed multiple successful tests with various grades of Cereplast Compostables(R) blown film resins. The Company estimates that the potential addressable market for their blown film resins in Italy is approximately $50 million per year. The Company has ample production capacity to serve such a demand.

Cereplast's office in Hyderabad, India has been actively educating local converters and introducing Cereplast resins. The demand is starting to accumulate, and several agreements are currently underway. India is one of the largest consumers of plastic polymers in the world, and the potential volume for bioplastic sales in the country is quite significant as they adopt bioplastic alternatives to conventional plastics, India is also very sensitive to the environment and has experienced firsthand the calamities created by excess industrialization and carbon dioxide emissions.

In the United States, the Company is working on over ten new projects both for Cereplast Compostables(R) resins and Cereplast Sustainables(R) resins. The steady increase in oil pricing is fueling a renewed interest in Cereplast resins and with two new business development managers dedicated to the domestic market, Management is confident to see measurable results before the end of Q3.

The Cereplast Research and Development department commercialized two new resins including Biopropylene A150D, an injection molding grade manufactured with 51% post-industrial algae biomass, and Compostable 2020D, an extrusion blow molding resin. Two new patents were granted and applications have been filed to protect the Company's new innovation in nano materials and algae biobased resins. The Company also incorporated a new, wholly owned subsidiary Algaeplast vehicle to develop algae-related research.

On the corporate side, the Company adopted an aggressive approach and filed legal actions against certain clients for their 2011 unpaid purchases. The Company was already successful in recouping valuable inventory in Italy as a settlement for outstanding receivables and is optimistic about the overall outcome of these pending actions.

"We are optimistic for the remainder of the year," said Mr. Frederic Scheer, Cereplast's Chairman and Chief Executive Officer. "Growth is expected to continue and increase and we believe that our growth projections will contribute to a stronger share price. The fundamentals of the company are excellent and our Management team is working to exceed our shareholders' revenue expectations."

About Cereplast, Inc.

Cereplast, Inc. (CERP) designs and manufactures proprietary biobased, sustainable bioplastics which are used as substitutes for traditional plastics in all major converting processes - such as injection molding, thermoforming, blow molding and extrusions - at a pricing structure that is competitive with traditional plastics. On the cutting-edge of biobased plastic material development, Cereplast now offers resins to meet a variety of customer demands. Cereplast Compostables(R) resins are ideally suited for single-use applications where high biobased content and compostability are advantageous, especially in the food service industry. Cereplast Sustainables(R) resins combine high biobased content with the durability and endurance of traditional plastic, making them ideal for applications in industries such as automotive, consumer electronics and packaging. Learn more at www.cereplast.com. You may also visit the Cereplast social networking pages at Facebook.com/Cereplast, Twitter.com/Cereplast and Youtube.com/Cereplastinc.

<<<

W. R. Grace - profile -

>>> W. R. Grace & Co. engages in the production and sale of specialty chemicals and materials worldwide. Its Grace Catalysts Technologies segment offers fluid catalytic cracking (FCC) catalysts for the production of transportation fuels, such as gasoline and diesel fuels, and other petroleum-based products; FCC additives; hydro processing catalysts used in process reactors to upgrade heavy oils; polyolefin catalysts and catalyst supports for the production of polypropylene and polyethylene thermoplastic resins; and chemical catalysts used in industrial, environmental, and consumer applications. The company?s Grace Materials Technologies segment offers silica-based and silica-alumina-based engineered materials used in industrial and consumer, coatings and print media, pharmaceutical, and life science and related applications; and packaging materials, such as can and closure sealants, and coatings for cans and closures. This segment also provides polyolefin catalysts and catalyst supports for use in the manufacture of polyethylene and polypropylene resins; and chromatography columns and consumables, and CO2 adsorbents used in anesthesiology and mine safety applications. The company?s Grace Construction Products segment offers specialty construction chemicals and materials, including concrete admixtures and polymeric fibers; additives used in cement processing; products for architectural concrete; admixtures for masonry concrete; process control solutions for ready mix concrete; building materials for new construction and renovation/repair projects that include waterproofing membranes, specialty grouts, and air and vapor barriers, and other products for preventative and repair applications; and fire protection products. W. R. Grace & Co. was founded in 1854 and is headquartered in Columbia, Maryland. On April 2, 2001, W. R. Grace & Co. filed a voluntary petition for reorganization under Chapter 11 in the United States Bankruptcy Court for the District of Delaware. <<<

WD-40 Company - profile -

>>> WD-40 Company (WDFC) engages in the provision of consumer products worldwide. It offers multi-purpose maintenance products under the WD-40 brand for household, marine, automotive, construction, repair, sporting goods, gardening, and various industrial applications; multi-purpose drip oil and spray lubricant products, and other specialty maintenance products under the 3-IN-ONE brand for household, locksmithing, HVAC, marine, farming, construction, and jewelry manufacturing applications; and industrial grade and specialty maintenance products that include lubricants, penetrants, degreasers, and cleaners under the Blue Works brand for various industrial applications. The company also provides specialty problem solving products, which comprise penetrants, water resistant silicone sprays, corrosion inhibitors, and rust removers under the WD-40 Specialist name; and bicycle maintenance products that include wet and dry chain lubricants, heavy-duty degreasers, foaming bike wash, and frame protectants under the WD-40 Bike name for avid cyclists, bike enthusiasts, and mechanics. In addition, it offers homecare and cleaning products, such as liquid mildew stain removers and automatic toilet bowl cleaners under the X-14 brand; automatic toilet bowl cleaners under the 2000 Flushes brand; room and rug deodorizers in the form of powder, aerosol foam, and trigger spray under the Carpet Fresh brand; aerosol carpet stain removers, and liquid trigger carpet stain and odor eliminators under the Spot Shot brand; carpet and household cleaners, and rug and room deodorizers under the 1001 brand; and heavy-duty hand cleaner products in bar soap and liquid form under Lava and Solvol brands. The company sells its products primarily through mass retail and home center stores, warehouse club stores, grocery stores, hardware stores, automotive parts outlets, and industrial distributors and suppliers. WD-40 Company was founded in 1953 and is headquartered in San Diego, California. <<<

Westlake Chemicals - profile -

>>> Westlake Chemical Corporation (WLK) manufactures and markets basic chemicals, vinyls, polymers, and fabricated building products. It operates in two segments, Olefins and Vinyls. The Olefins segment provides ethylene, polyethylene, styrene monomer, and various ethylene co-products, such as chemical grade propylene, crude butadiene, pyrolysis gasoline, and hydrogen. The Vinyls segment offers polyvinyl chloride (PVC), vinyl chloride monomer, ethylene dichloride, chlorine, caustic soda, and ethylene. This segment also manufactures and sells building products fabricated from PVC, including pipe, fence and deck, and window and door components. The company?s products are used in various applications, which include consumer and industrial markets, such as flexible and rigid packaging, automotive products, coatings, and residential and commercial construction, as well as in other durable and non-durable goods. Westlake Chemical Corporation provides its products for chemical processors, plastics fabricators, construction contractors, municipalities, and supply warehouses in the United States, Canada, Singapore, Switzerland, and internationally. The company was founded in 1985 and is headquartered in Houston, Texas. <<<

Valspar - profile -

>>> The Valspar Corporation (VAL) manufactures and distributes various coatings, paints, and related products worldwide. The company operates in two segments, Coatings and Paints. The Coatings segment offers decorative and protective coatings for metal, wood, and plastic primarily for original equipment manufacturing customers. Its products include primers, topcoats, varnishes, sprays, stains, fillers, and other coatings for various customers in manufacturing industries, such as agricultural and construction equipment, appliances, building products, furniture, metal fabrication, metal packaging, and transportation. This segment also offers coatings for interior and exterior metal packaging containers comprising food containers and beverage cans; coatings for aerosol and paint cans; and crowns for glass bottles, plastic packaging, and bottle closures. In addition, it provides coatings that are applied to metal coils; general industrial products, including powder, liquid, and electrodeposition coating technologies; and wood products, including decorative and protective coatings for wood furniture, building products, cabinets, and floors, as well as color design manufacturing and technical services. The Paints segment offers consumer paints consisting of interior and exterior decorative paints, stains, primers, varnishes, and floor paints, as well as specialty decorative products, such as enamels, aerosols, and faux finishes that are used in do-it-yourself and professional markets. It also offers automotive refinish and aerosol spray paints. This segment distributes its products through home centers, hardware wholesalers, distributors, retailers, independent dealers, body shops, and company-owned stores. The Valspar Corporation also manufactures and sells specialty polymers and colorants, as well as sells furniture protection plans, and furniture care and repair products under the Guardsman brand. The company was founded in 1806 and is headquartered in Minneapolis, Minnesota. <<<

Sensient -- >>> Sensient : Solid Growth And Much Cheaper Than The Competition

Jul 2 2013

by: Matthew Frankel

http://seekingalpha.com/article/1530992-sensient-solid-growth-and-much-cheaper-than-the-competition?source=yahoo

Sensient Technologies (SXT) has lagged the S&P 500 so far this year, with shares up just 7%. Despite rising revenues and increasing profit margins, this maker of colors, flavors, and fragrances has not managed to keep up with its competition. For example, International Flavors & Fragrances (IFF) is perhaps the closest comparison to Sensient and is up about 15% so far in 2013. Does this mean that Sensient is one of the bargains in this industry, or would investors be better off putting their money in one of the alternatives?

About Sensient

As mentioned, Sensient is a manufacturer of various products related to colors, flavors, and fragrances. The company's operations are categorized into two segments, the Flavors & Fragrances Group and the Color Group.

Flavors & Fragrances include products that are meant to enhance or alter the flavor or aroma of a customer's products. Most of this segment is geared toward the food industry, but also produces flavorings for the pharmaceutical business. Products made by the segment include flavor-delivery systems, essential oils, natural and artificial flavors, aroma chemicals, and the company's dehydrated flavors business, Sensient Dehydrated Flavors. The dehydrated products include onion and garlic-based seasonings as well as a line of other spices and dehydrated vegetables.

The Color Group produces a variety of colorings for beverages, processed foods, confections, pet foods, cosmetics, and more. The group operates under several trade names such as Sensient Food Colors, Sensient Pharmaceutical Technologies, Sensient Paper Colors, and Sensient Cosmetic Technologies.

Growth

After a small contraction in revenues brought on by the recession, Sensient has grown its revenues every year since 2009 and is projected to grow by 5% this year. Additionally, profit margins have been widening in recent years, and this trend is also projected to continue due to increased demand for their products which leads to greater pricing power. The company is expecting operating margins of 17.2% this year, up from 17.0% in 2012.

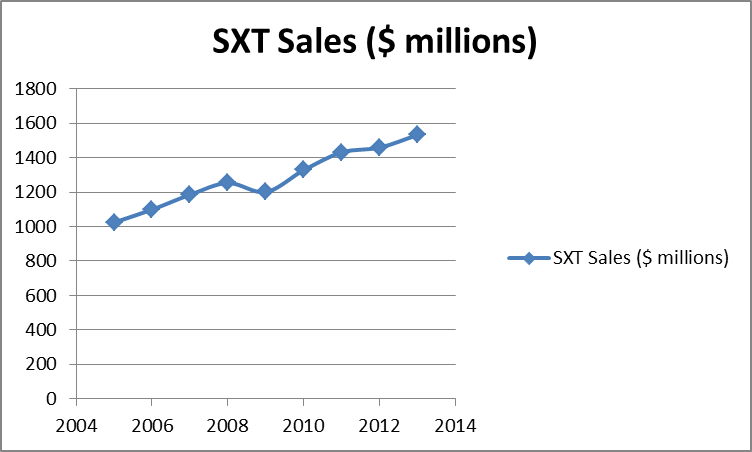

(click to enlarge)

Sensient's recent trend is toward more natural colors and flavorings, recognizing the changing desires of consumers. Currently, the company produces a mix of natural and synthetic products and has expressed its intention to invest significant capital in research and development over the next few years in order to make this transition, as well as to increase its production capacity as global demand grows.

Looking at the chart above, other than the peak recessionary years, Sensient's growth actually seems very linear (and maybe even predictable). If you believe (as I do) that the economic recovery will continue for the next several years, there is no reason to think this growth pattern will change, especially with increased R&D spending. A further increase in sales should also lead to further improvement in Sensient's profit margins, which will translate to a very nice earnings growth rate.

Valuation and alternatives

Sensient currently trades at a significant discount to its competitors. Shares trade at 15.3 times last year's earnings, which due to the previously mentioned combination of higher revenues and wider margins are expected to grow by just over 6% this year. However, the consensus estimates call for earnings growth to increase significantly beyond this year, as current R&D efforts begin to pay off. The median estimates are $3.00 and $3.27 per share for 2014 and 2015, respectively, for annual earnings growth of 11.1% and 9%.