News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

ProShares ETFs – New 4PM Close of Trading

--------------------------------------------------------------------------------

< Back to News

Beginning Wednesday, October 8, 2008, trading in ProShares ETFs on the NYSE Alternext U.S. (formerly the American Stock Exchange or Amex) will close at 4 p.m. ET rather than 4:15 p.m.

We are making this change in anticipation of the transfer of all 64 ProShares from NYSE Alternext to the NYSE Arca trading platform, where all trading closes at 4 p.m. The NYSE Euronext, owner of NYSE Arca, completed its acquisition of the Amex on October 1, 2008 and changed the Amex's name to NYSE Alternext U.S. NYSE Euronext has indicated that they intend to move all exchange traded products to NYSE Arca in the fourth quarter of 2008.

Oct 3, 2008

GS bought the wachovia monkey wrench. short term that hurts them but they are eyeing the bailout prize now. so the game changed to steal a current meme. they temporarily catch the toxic CDO bug so they get the cure Doctor Paulson is dishing out for free.

I'm curious to see,once the short selling ban comes off how the puts get repriced and what that does to SKF. I think everyone is anticipating it ahead of Thursday.

The Export Slowdown

by CalculatedRisk

http://calculatedrisk.blogspot.com/2008/10/export-slowdown.html

Some things I'm noticing. First imports are rising. Good for our economy. US business exporting products are turnning a profit. A profit we keep inside US borders I hope because exports are more expensive.

The second is that exports are sinking. but falling inline with imports. That is key to Baltic Dry index and Dry Bulk shippers. See when they are shipping goods to the US but going back empty on the route home, they only get a one way profit. Balanced trade mean profit both ways. That is good for shippers.

Third is that this Christmas will be bad for retailers as exports are weak and US producers I don't think have really ramped up enough to support US sales this year. Next year will be different.

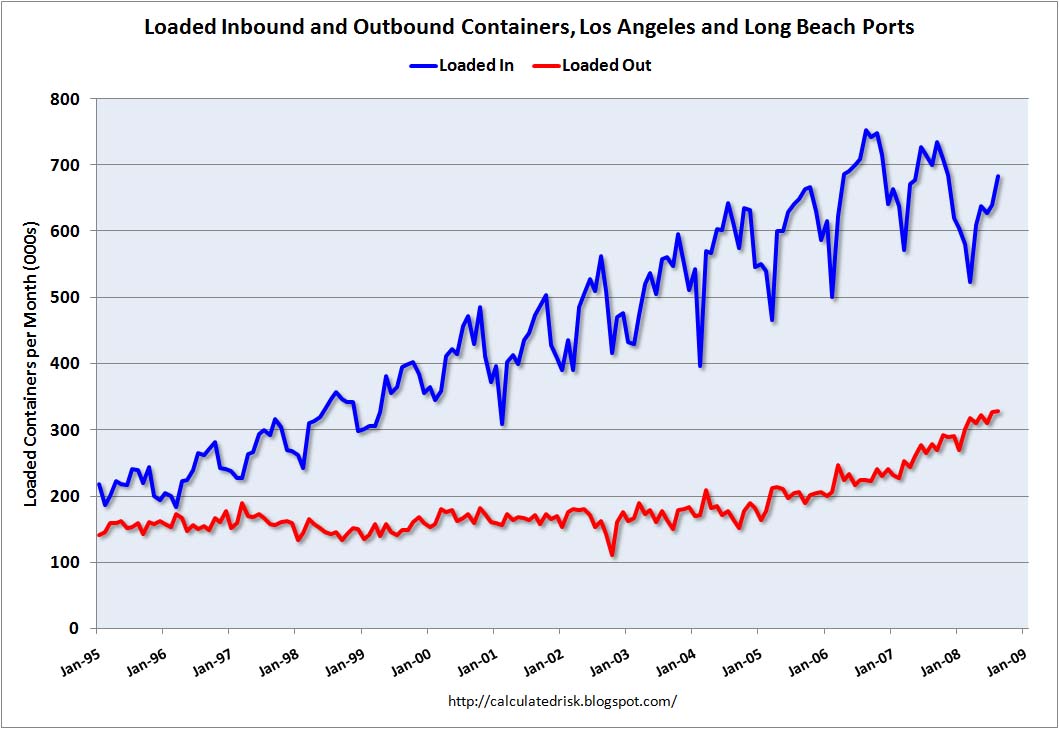

This graph shows the combined loaded inbound and outbound traffic at the ports of Long Beach and Los Angeles in TEUs (TEUs: 20-foot equivalent units or 20-foot-long cargo container). Although containers tell us nothing about value, container traffic does give us an idea of the volume of goods being exported and imported.

West Coast Port Traffic

Inbound traffic grew quickly for a number of years, but appears to be declining (there is a strong seasonal component). Inbound traffic is off about 6% from 2007 (using the last two months of July and August).

Outbound traffic was flat for years, but has been increasing the last few years. Outbound traffic is up 20% from 2007.

However it appears export growth will be slowing. From the WSJ: Slowing Export Machine Is Starting to Sputter

Export growth is expected to fall sharply in coming months ... Many U.S. producers are already seeing a slump in new orders ... The outlook has dimmed so quickly that economists are having a hard time keeping their projections current.

...

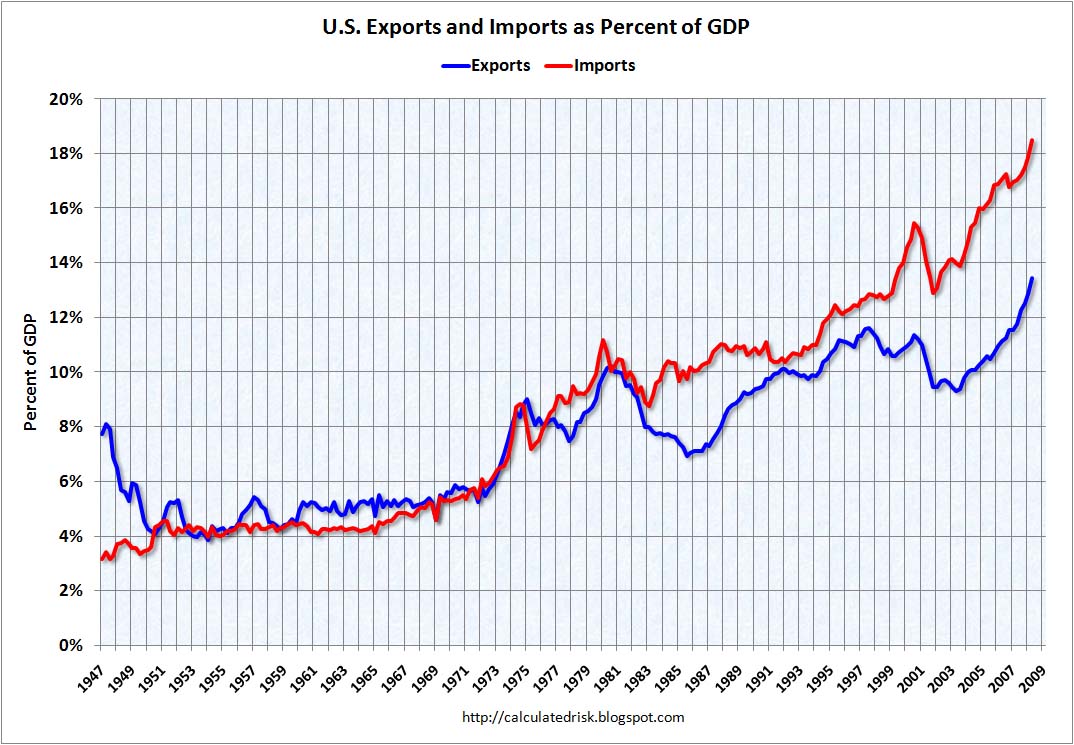

The upshot is that exports will no longer serve as the counterweight to weakness in the domestic economy. Over the past year, real goods exports surged by $114 billion, or 12%, up across every major category. They now make up nearly 13.5% of gross domestic product, the highest percentage since World War II.

Exports Imports as Percent of GDPThe second graph shows imports and exports as a percent of GDP since 1947 through Q2 2008.

Over the years, both exports and imports have increased as a percent of GDP. Exports now make up almost 13.5% of GDP (imports as a percent of GDP are at 18.5%). With the decline in oil prices - and the weaker U.S. economy - imports as a percent of GDP will probably decline over the next year.

With the global slowdown, export growth will also slow, and might even decline too. This has been a key source of strength for the U.S. economy, and especially for manufacturing employment.

XLF traded 15.xx today

SKF is trading very much less than 200, where it was when XLF was trading 17.xx back in July.

SKF has got to be undervalued here, doesn't it?

updated the iBox

cleaned up a bit and put up the big charts I'm watching. I'm going to overhaul that iBox make it more informative

LOL HAHAHAHAHAHAHAHAAAAAHHHHHHHH!!!!!111!1ONE!!!!

Lehman Brothers CEO Got Punched In The Face

Farking priceless

Dick "It Wasn't My Fault" Fuld, the CEO of bankrupt investment bank Lehman Brothers, (seen here being heckled after testifying on Capitol Hill) was apparently punched in the face while working out in Lehman gym on the Sunday following the bankruptcy, according to CNBC's Vicki Ward.

Fuld testified before the House Oversight Committee yesterday, blaming everyone but himself for Lehman's collapse, an attitude that prompted Ward to confirm reports that he'd been punched in the face and to side with the attacker:

“From two very senior sources – one incredibly senior source – that he went to the gym after … Lehman was announced as going under. He was on a treadmill with a heart monitor on. Someone was in the corner, pumping iron and he walked over and he knocked him out cold. And frankly after having watched this, I’d have done the same too.”

http://consumerist.com/5060063/lehman-brothers-ceo-got-punched-in-the-face

Financial mess flowchart

Online bank customers create damaging 'silent runs'

* 12:30 07 October 2008

* NewScientist.com news service

* New Scientist staff and Reuters

The ease with which technology allows customers to move their money around by internet or phone has introduced a new financial phenomenon – the "silent run" on a bank.

Within hours, telephone and internet banking customers can remove huge amounts of money from a bank rumoured to be in trouble, without telltale queues, or any other outward sign of the flood of cash.

The bank Fortis, focus of a cross-border rescue by Benelux governments last week, was in part a victim of a silent bank run. That, along with a dramatic fall in its stock prompted an emergency cash injection of 11.2 billion euros and the Dutch government to fully nationalise the bank's Netherlands operations.

In the Great Depression between 1929 and 1933, much of the damage was caused by runs on banks that gained momentum as people saw lines of customers waiting to salvage cash. In Fortis's case, much of the outflow came at the click of a mouse.

'Banana republic'

The bank said it lost about 3% of its deposits from consumer and business clients, or about 5 billion euros ($7 billion).

British bank Northern Rock suffered the first run on a major British bank for more than 140 years last September, with panicked customers lining up at branches over three days. Scenes one politician said made Britain look like "a banana republic".

But branch withdrawals quickly slowed after the UK government guaranteed savings. The most serious damage was done by internet, postal and telephone withdrawals that continued to flood away. By the end of 2007, more than half the bank's retail deposits were gone – only a third via branches.

The silent online run may spare banks the damaging PR of queues outside branches. But funds can be moved more quickly and in far larger quantities with the click of a mouse or a telephone call.

Damaging speed

The speed at which that happens is one of the concerns behind recent scrambles by European governments to increase guarantees on deposits. Ireland and Denmark have offered blanket guarantees to savers, and pressure is mounting on others to follow as savers rush to put their cash in these safe havens.

Executives say that in any silent run the most damaging aspect is the speed at which business customers can move.

"The so-called silent run on the bank – it's real," says Carlos Evans, an executive at fourth-largest US bank Wachovia. The troubled bank is soon to be bought by a rival in a government-backed rescue plan.

Evans said withdrawals started picking up on September 26 and over subsequent days. "You go from being weakened to in trouble in a matter of days. I don't think people understand how quickly events unfolded," he says.

I do waiting for that 90% up day for the turn around. Can't really have that without a short squeeze. markets are all farked up.

I like these investment tools charts. the have a lot of great data. Like this in regards to short sales. Want to know why the ban on shorts. Because the retail investors was getting into the act. My guess is that they saw that as a lot of capital that the banks could get their hands on.

total short sales

retail short sales

member short sales

no bidders out there. did you look at up/down volume statistics? NYSE and Nas were like 38 to 1 first hour today

Investment Tools Index of 12 Shipping

(Water Transportation) Companies (The Blue line is a 20 day Donchian channel, red line is a 5 day exponential average, green line is a 20 day exponential average.

Bottomed? we will need to see where this goes

static chart

updating chart

must have been a lot of request recently for that one. good to see them keeping up on it.

Stockcharts has added $TED to its catalog. Backfilling to come, they said

yeah too bad the credit crunch didn't happen before the overbuild of cargo ships. I think what may happen next is a flood of ships being sent to salvage because the companies are not able to break even on charters.

in regards to crude tankers, there was a serious build up expected for 2009, but a lot of these newbuilds are bought on credit. Its the option to buy that they are purchasing. With the way things are going a lot of companies are walking away from the contracts because their credit lines evaporated.

looks like a burning house

some move on baltic dry index

Re: leveraged ETFs and Counterparty Risk:

You may recall I have wondered about this and even called ProShares about it. I never got decent answers to my questions.

This guy got answers. But I wonder if there are holes in this story?

===========================

Hidden Credit Risks of ETFs

In these tumultuous times it is critical to understand what you own.

by John Gabriel | 2008-09-19 04:00:00

Most exchange-traded products are index investments, backed by the actual portfolio of equities or bonds. Although an investor may be taking on the underlying risks of those portfolio holdings, they are not exposed to any risk from the issuer's financial state. For example, if State Street were to go bankrupt (unlikely, even in these tumultuous times), investors in the SPDRs ETF would be made whole by their claims on the underlying stock investments held by the unit trust.

However, not all exchange-traded products have this safety. Exchange-traded notes, or ETNs, are actually promissory notes with no claim on an underlying portfolio, so they are only as trustworthy as the debt of their backing bank. Morningstar's director of ETF analysis, Scott Burns, recently wrote an article on ETNs and the credit risk that they face.

Besides ETNs' inherent credit risk, some ETFs also posses a certain amount of credit risk. Some ETFs cannot invest directly in their underlying assets, relying on swaps, futures, or other derivatives to match the return on their index. These derivatives open those ETFs to counterparty risk, the risk that the institution on the other side of their trade will default, which could leave a fund with no return on its assets or even a loss. The ETFs vulnerable to counterparty risk fall into two major categories: leveraged funds and commodities funds.

Leveraged ETFs

ProShares and Rydex are the two biggest issuers of leveraged funds, which seek to provide some multiple of the return on an index or sector. Examples include UltraShort Financials ProShares, which seeks to provide twice the opposite of the daily return of the U.S. financials sector, and the Ultra S&P500 ProShares, which seeks to provide twice the daily return of the S&P 500 Index. These ETFs cannot invest directly in a basket of equities twice the size of their index or short-sell their entire portfolio due to restrictions on the investments allowed in a U.S. mutual fund structure, so they instead use swap derivatives to capture the desired daily leveraged returns. These index swaps are contracts traded through investment banks where one party offers to pay a fixed interest payment on a set date in the future in return for the other party offering to pay the return on an agreed-upon index such as the S&P 500. Leveraged ETFs keep the bulk of their assets in cash as collateral, then enter swap agreements based upon their asset values that replicate the desired multiple of an index's return.

The bank that issues the swap contract frequently guarantees the payments and oversees posting of collateral by both parties, but that is little comfort when investment banks are collapsing. Also, if a major counterparty defaults, as American International Group was threatening to earlier this week, the investment bank may not have enough capital to make the other parties whole and may be forced into default.

Although this seems like a lot of risk, there are mitigants. The first bit of good news is that, even if the swap contract is defaulted upon, the fund still holds all of its cash assets. The most a fund could lose is the return owed through a swap contract; it will never lose principal. The second bit of good news is that these swap contracts are very short-term, never written for more than 30-day periods. This gives leveraged ETFs some agility and allows them to quickly close out any exposure to investment banks that look to be edging toward bankruptcy.

We talked to representatives from both ProShares and Rydex and they indicated that their short-term contracts enabled them to minimize their funds' exposure to the collapse of Lehman Brothers and could cover the tiny losses any funds might have sustained. Still, a very swift collapse of a major investment bank or hedge fund in the near future cannot be ruled out (even with recent government moves), and it would almost certainly cause these funds to lose some of their returns, although fortunately the principal would remain secure.

Commodities ETFs

Commodities ETFs also frequently use derivatives rather than directly investing in the underlying assets. This is because it would not be practical to take custody of millions of barrels of crude oil, tons of coal, or bushels of corn in an effort to match benchmark returns. In order to replicate their stated index returns, commodity-based funds invest in futures, forwards, and swap contracts without actually taking physical delivery.

One of the largest and best-known commodities ETFs is United States Oil Fund. This fund--which is often used by institutions as an easily accessible hedging vehicle--is designed to track the movements of both light and sweet crude oil. Its portfolio consists primarily of listed crude oil futures contracts and other oil-related futures, forwards, and swaps, which are collateralized by cash, cash equivalents, and U.S. government obligations with remaining maturities of less than two years. There should be no concern here, as the fund's exposure is collateralized on a dollar-for-dollar basis with extremely liquid assets.

However, digging further, we notice that a portion of the fund's trades might be in over-the-counter contracts with investment banks, which are not as liquid as exchange-traded oil futures contracts, thus exposing the fund to credit risk associated with its counterparties. This exposure may have built up in the past, when forward contracts through investment banks were cheaper than exchange-traded contracts or could be based upon more obscure underlying assets. Although this type of counterparty risk may be present, we think commodities fund managers will seek to minimize their exposure to investment banks. They will likely sacrifice cost advantages for greater security by moving the portfolios fully into exchange-traded futures. Exchanges ensure each day that futures contracts are fully collateralized, and they require all counterparties to supply enough collateral that there is nearly zero risk of default. This rather pleasant option for commodities ETFs should help them avoid any troubles with counterparty defaults through this crisis, although it may reduce the profitability of the fund sponsors.

ETF Analyst Bradley Kay contributed to this article.

($LIBOR:$UST1M)

Credit to Author:

http://stockcharts.com/def/servlet/Favorites.CServlet?obj=ID369857&cmd=show[s152086914]&disp=P

apparently, this is what the markets have decided to watch.

Is there a chart somewhere?

Three-month dollar London interbank offered rates (Libor) moved higher to 4.3338 percent and overnight dollar Libor slid almost 70 basis points to 1.9963 percent , according to the British Bankers Association's latest daily fixing.

The spread of three-month dollar Libor over anticipated policy rates blew out by more than 25 basis points to 286.875 basis points, reflecting the underlying stress in money markets, particularly for 'term' funding.

Quote of the Day: Fair Value Accounting

Posted by Barry Ritholtz on Wednesday, October 01, 2008 |

IMO this whole market has been floating on the hot air. Where the SEC would not stand for th cheating of Enron, WorldCom and their ilk independently, when an industry collectively risks the global economy it will turn its head and go so far as to promote the false meme that all is well.

2008 has been an insulting year for the investor. Never has there been such a collectively undermining of free market capitalism. I'm not mentioning the socialization of FRE, and FNM or the $700 billion bailout, or Buffets glee to create a bottom, but the fact that the banks can outright cook the books the whole time their houses are burning and point out that things are not as bad as they seem. That the Fed and Treasury will follow suit. That I actually can believe because the Fed and Treasury have a stake in all of this as well. But that the SEC ignores this and goes so far as to ban shorting because they feel that financials are undervalued. It make me feel like I just found out that the roulette wheel, that the dealer is pressing the red button out in the open and every sees it but with some jedi mind trick is able to convince people that if they call him on it he will walk away and they won't have a chance to win back their money, so they better just keep playing.

It makes one want to leave the market entirely. It will be a cold day in hell if I ever buy a financial stock in the future. But then again you can't win if you don't play.

Wachovia went out with a book value of $75 billion. Citi paid $2 billion. Could it be that asset values are overstated, not understated?

-Michael Rapoport, Dow Jones

Gee, I dunno. Better obscure them as soon as possible . . .

Source:

Lying Bank Accounting

http://norris.blogs.nytimes.com/2008/09/30/lying-bank-accounting/

BDI broke down. Hit 3217 today. That is not good for the dry shippers. I expect a few of them to start going bankrupt is prices stay as low as they are. Last years newbuild glut killed them. Best course of action is to take older builds and sell them for salvage. Instant cash and bolsters survivability.

In other news here is a thought experiment using MACD unconventionally. Mapping MACD range over bear and bull markets. It's a poor mans VIX if you ask me. But volatility goes hand in hand with bear markets. Not that you can't have volatility in bull markets just that you rarely have complacency in bear markets.

Bull markets are inherently complacent as people systematically contribute monthly to 401ks and institutional funds. The short term trading that these funds do to try to capture small profits give you the day to day noise and makes it difficult to see the trend. That trend was the steady influx of money into the markets. Complacent influx. Small traders race into markets trying to catch a single stock rally, they represent a penny's worth in regards to the capital that flowed into th market on a timely basis. Long term daily charts like this can compress that noise and drown out the swings. You can then see the forest from the trees.

Te bear is not done. MACD has not significantly diverged from falling prices. In fact MACD seems to be sideways below zero confirming the long term downtrend.

Short ban terminates at 11:59 p.m. EDT Oct. 2

The short ban on financials is due to expire. Makes me think that this whole short ban Paulson plan, House Rejection was orchestrated.

Also I am considering that the big drop we had this Monday was go to a shift in strategies for short sellers who used to borrow shares to sell into the market shifting to options strategies where they buy puts exercise them to sell into the market. It might be more costly but has a similar effect and as much of a profit margin.

10 Things To Expect From The New Post-Apocalyptic Economy

Kiplinger's has put together a list of 10 things that you, fair consumer, can expect from our new post-wall-street-apocalypse economy. Should you be scared? Maybe.

Here's a quick summary of the article, which can be found here:

1. A much less leveraged economy — Cash will be the thing to have.

2. More modest rewards — Less risk-taking means slower growth, slower appreciation of property value, etc.

3. A feast for bottom fishers — If you've got patience and cash, there will be a feast for you amongst the wreckage.

4. Fewer financial firms — Big banks are swallowing the smaller ones.

5. More government oversight of financial markets. — They're gonna be watching.

6. But a revival of private financial firms — Kiplinger's doesn't think that investment banks are gone for good.

7. Simpler forms of securitizing debt — Nor do they think that the secondary mortgage market is gone for good. They say it will be back, but it won't be as 'exotic'

8. Greater scrutiny of executive compensation — Shareholders are annoyed. Very annoyed.

9. Higher taxes and/or a bigger federal deficit — Someone has to pay to run the bilge pump.

10. Higher long-term interest rates — You saw that one coming, didn't you?

Hey, it turns out that the new post-apocalyptic economy is pretty much just the old traditional economy — but with a debt hangover.

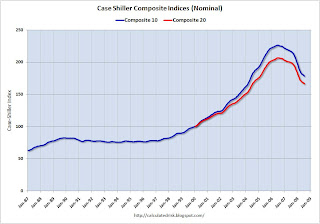

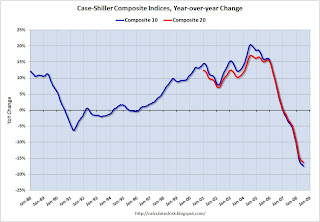

Case-Shiller: House Prices Declined in July

by CalculatedRisk

Housing is the key. And house prices are still falling sharply ...

S&P/Case-Shiller released their monthly Home Price Indices for July this morning. This includes prices for 20 individual cities, and two composite indices (10 cities and 20 cities). Note: This is not the quarterly national house price index.

Case-Shiller House Prices Indices Click on graph for larger image in new window.

The first graph shows the nominal Composite 10 and Composite 20 indices (the Composite 20 was started in January 2000).

The Composite 10 index was off 12.3% annual rate in July (from June), and is off 21.1% from the peak.

The Composite 20 index was off 10.1% annual rate in July (from June), and is off 19.5% from the peak.

Prices are still falling, and will probably continue to fall for some time.

The second graph shows the Year over year change in both indices.

The Composite 10 is off 17.5% over the last year.

The Composite 20 is off 16.3% over the last year.

Home Prices in 20 U.S. Cities Declined 16.3% in July (Update1)

I don't think the market cares about these metrics anymore. seems like its a junkie just looking for that big fix from Congress to pass. More fall out in housing prices means that more mortgages go into negative equity, means more foreclosures, means more defaults and more toxic CDOs\CDSs. This is far from over and regardless if we get $700 billion its not going to put much of a dent in the short term. As housing prices continue to fall over the next 3 months nothing can be done over that time. This will get worse before it gets better.

By Bob Willis

Enlarge Image/Details

Sept. 30 (Bloomberg) -- House prices in 20 U.S. cities declined in July at the fastest pace on record, signaling the worst housing recession in a generation had yet to trough even before this month's credit crisis.

The S&P/Case-Shiller home-price index dropped 16.3 percent from a year earlier, more than forecast, after a 15.9 percent decline in June. The gauge has fallen every month since January 2007, and year-over-year records began in 2001.

The housing slump is at the center of the meltdown in financial markets as declining demand pushes down property values and causes foreclosures to mount. Banks will probably stiffen lending rules even more in coming months to limit losses, indicating residential real estate will keep contracting and consumer spending will continue to falter.

``The fact that house prices quickened their slide before the worst point in credit markets hit this month does not bode well,'' said Derek Holt, an economist at Scotia Capital Inc. in Toronto.

Home prices decreased 0.9 percent in July from the prior month after declining 0.5 percent in June, the report showed. The figures aren't adjusted for seasonal effects so economists prefer to focus on year-over-year changes instead of month-to-month.

More Cities Down

Prices dropped in 13 cities month-over-month, compared with 11 in June. Las Vegas saw values fall 2.8 percent in July, the largest decline.

Economists forecast the 20-city index would fall 16 percent from a year earlier, according to the median of 23 estimates in a Bloomberg News survey. Projections ranged from declines of 14.5 percent to 16.5 percent.

Compared with a year earlier, all 20 areas showed a decrease in prices in July, led by a 30 percent drop in Las Vegas and a 29 percent decline in Phoenix.

``While some cities did show some marginal improvement over last month's data, there is still very little evidence of any particular region experiencing an absolute turnaround,'' David Blitzer, chairman of the index committee at S&P, said in a statement.

Robert Shiller, chief economist at MacroMarkets LLC and a professor at Yale University, and Karl Case, an economics professor at Wellesley College, created the home-price index based on research from the 1980s.

Other Measures

Other reports show price declines continue. The National Association of Realtors said Sept. 24 that the median price of an existing home fell 9.5 percent in August from a year earlier, compared with an 8 percent drop in July. The following day, the Commerce Department said the median price of new homes fell 6.2 percent in August from a year earlier, following a 4.6 percent drop the prior month.

Sales of previously owned homes fell 2.2 percent in August from the prior month and were 32 percent below their historic high reached in September 2005. Declining home construction has subtracted from growth since the first quarter of 2006, pushing the economy to the brink of a downturn.

U.S. homebuilders, buffeted by at least $19 billion in losses since 2006, will ask lawmakers to pass a $15,000 tax credit for all homebuyers, replacing a $7,500 incentive enacted earlier this year that they contend failed to stimulate demand.

``Our members are really hurting,'' Jerry Howard, the chief executive officer of the National Association of Home Builders, said in an interview yesterday. ``The tax credit passed in July seems to have failed to have sparked interest.''

To contact the reporter on this story: Bob Willis in Washington at bwillis@bloomberg.net

Last Updated: September 30, 2008 09:17 EDT

Loose money was the problem all along. It isn't a part of the long term solution.

I thought the market would signal a few days in advance how critically they need/want to accelerate the multi-trillion dollar bailout for the Federal Reserve banking system that has failed us so miserably.

speculating - 15th bank to fail National City on deck IMHO.

No shortage of willing audience members for The Peanut Gallery these days.

news is opinion and everybody has one. I pretty much assumed that this is what would happen in this economy. There is not a single society that is purely socialist or capitalist. Pure capitalism is like pure democracy is acts like a sociopath. when policy can be put forth and voted on that the majority will prevail it's only a matter of time before the majority will discover that its survivability to is eliminate all minority groups through policy.

In a free capitalist market monopolies would prevail everywhere as there would be no regulative bodies to protect smaller companies, consumers, etc. Socialism begins when the first policy is put into effect. Government by its nature is socialist for its own survivability.

I think that everyone is the world is shocked that the bastion of capitalism has resorted to heavily regulating the markets and absorbing losses the way a Russia or China would. The nature of capitalism would be that no one is too big to fail and that the banks would learn their lesson when the carnage destroyed the worst offenders. Those that survived would be more cautious. Laws of survival. I don't think anything that happen were mistakes. I'm still a strong proponent of free market capitalism even in the current environment.

but I think that the writers here and a lot of other people have to realize that the economic system is very dynamic, it can regulate and deregulate as needed. It can adapt to the environment as needed. The problem is that the regulation and deregulation should be used to protect from bubbles and bursts. Regulate more as markets expand and deregulate more as they suffer.

What we should be doing in freeing up restrictions on wages, housing affordability, mortgage approval etc. Yeah it sounds crazy right now because we just came out of that environment and this is the result. But it works as long as we are willing to increase restriction as markets improve. Imagine how these CDOs would trade if in 2003-2005 when real estate prices started accelerating that we increased closing costs, increase property taxes, sales taxes, increased restriction on mortgage approval availability. housing prices would have not moved at a parabolic rate and it would result in a successive crash. Sure expansion would not have been great but we would probably still be in an expansion today and not talking about bailouts.

Humans... they will never figure it out.

Yahoo News trolls this web site in Lebanon - can you believe it?

Dar Al-Hayat

America Pays for its Mistakes

Michel Morkos Al-Hayat - 29/09/08/

When the US Administration interferes a few times to save its national economy, at times bailing out major financial institutions and at others drafting rescue plans to float the economy, this means it has previously given up - for undisclosed reasons - its fundamental mission of protecting the economy. Instead of regulating markets and controlling large financial institutions, it has left investment banks prey to more debts and money markets under the pressure of hectic speculations.

Two months ago (July 26), Congress passed a bill to set up a $300 billion fund that provides citizens with soft loans to settle mortgage payments. Currently, the US Administration suggested a $700 billion program to save Wall Street. Through these two programs, the US government acquired two mortgage giants, Fannie Mae and Freddie Mac, and controlled American International Group, the largest insurance company in the world. At the same time, many mergers occurred within the private sector: Bank of America took over Merrill Lynch for $50 billion and JP Morgan acquired Washington Mutual. In addition, the shares of Goldman Sachs and Morgan Stanley fell and Lehman Brothers filed for bankruptcy.

Facing these financial crashes, along with the severe losses in world stock markets - with Wall Street leading the way - the US bailout plan comes amidst the continuous and following crises. This clearly indicates a (previous) huge letdown in the financial policy applied to US banks. It also shows the world-class US stock markets dealing with non-solvable money instruments.

Tracking the seeds of the US mortgage crisis sheds light on the gaps in the lenders' use of unsecured money instruments. Low-interest mortgages created an active real estate market. Thus, houses increased in value and were turned into mortgaged assets in order to achieve the welfare of households, owners of houses. With the expansion of mortgage lending; with loans offered to buy cars and luxurious furniture, to restore homes, and travel, banks issued bonds against their mortgages and sold them for global investors in return for revenues. Investors then sold or pledged them to investment or hedge funds in view to buying more such bonds. These same bonds are a result of mortgages or loans for durable goods, such as cars.

Mistakes started to pile up. The first one resulted from the expansion in lending at interests linked to the rates set by the Federal Reserve, which increased from one percent at the time to 4.5 percent at the start of the crisis last year. The second mistake was attracting the borrower with bank facilities on one hand and false facilities on the other: settlements for the first three years were only limited to the interest rate. With the rise of the non-fixed interest rate, some borrowers were unable to settle the due payments and faced high fines that increased their inability to pay.

The confusion in the assets guaranteeing the loan or the bonds was the third mistake. Lenders viewed mortgaged houses as a guarantee for their loans, while the owner of the mortgage bonds thinks they are his as well. When the regulations enforced insurance on mortgage bonds, major insurance companies took the burden of the bonds, which were considered pretty crash-proof.

Everything was dependent on the main borrower and his financial solvability. When that borrower defaulted on his payments, the bonds turned into a burden and became bad bonds. Lenders, in need of liquidity, crashed; hedge funds, investors and, consequently, mortgage bonds insurance companies suffered losses.

In short, banks were very lenient. Loans for a single house mortgage became 30 more than the real house value. Newsweek's Fareed Zacharia says that the ratio of corporate debts to share capital stands at 35 to 1.

The crisis is bound to end the dispute over saving the economy. But an administration like the American one must in the first place regulate banking operations and money markets where the reckless competition led to the crash of the world economy and threatens it now with recession and paralysis.

Not all US institutions incurred damages; not all economic activities faced losses. To redress the economy, the mistakes of the past must be first avoided. For economic freedom does not mean chaos.

http://english.daralhayat.com/business/09-2008/Article-20080929-ae93217f-c0a8-10ed-01ae-81abf7cc1eec/story.html

Dar Al-Hayat's English website is a primary source of information for all English-speaking readers seeking an alternative perspective and in-depth reporting on the Middle East and the Arab world.

Contact Us:

Dar Al-Hayat

Dar Al-Hayat Bldg; Maarad St; Riad Solh Sq.

PO Box: 11-1242

Beirut; Lebanon

Tel: +961 1 987990/1/2/3/4

Fax: +961 1 983921

Inquiries: information@alhayat.com

Webmaster: dhwebmaster@alhayat.com

Press Release

Federal Reserve Press Release

Central Banking System is going to flood the market

Release Date: September 29, 2008

For release at 10:00 a.m. EDT

In response to continued strains in short-term funding markets, central banks today are announcing further coordinated actions to expand significantly the capacity to provide U.S. dollar liquidity. Central banks will continue to work together closely and are prepared to take appropriate steps as needed to address funding pressures.

Federal Reserve Actions

The Federal Reserve announced today several initiatives to support financial stability and to maintain a stable flow of credit to the economy during this period of significant strain in global markets.

We will continue to adapt these liquidity facilities as necessary and will keep them in place as long as circumstances require.

Actions by the Federal Reserve include: (1) an increase in the size of the 84-day maturity Term Auction Facility (TAF) auctions to $75 billion per auction from $25 billion beginning with the October 6 auction, (2) two forward TAF auctions totaling $150 billion that will be conducted in November to provide term funding over year-end, and (3) an increase in swap authorization limits with the Bank of Canada, Bank of England, Bank of Japan, Danmarks Nationalbank (National Bank of Denmark), European Central Bank (ECB), Norges Bank (Bank of Norway), Reserve Bank of Australia, Sveriges Riksbank (Bank of Sweden), and Swiss National Bank to a total of $620 billion, from $290 billion previously.

These steps are being undertaken to mitigate pressures evident in the term funding markets both in the United States and abroad. By committing to provide a very large quantity of term funding, the Federal Reserve actions should reassure financial market participants that financing will be available against good collateral, lessening concerns about funding and rollover risk.

84-Day Maturity TAF Auctions

The increase to $75 billion per auction will triple the supply of 84-day maturity credit to $225 billion from $75 billion. TAF credit at the 28-day maturity will remain at $75 billion. The total amount of TAF credit available in the 28-day and 84-day auction cycles will double to $300 billion from $150 billion.

Forward TAF Auctions

The forward TAF auctions are a new program designed to provide reassurance to market participants that term funding will be available over year-end. The timing and terms of the two forward TAF auctions will be determined after consultations with depository institutions that utilize the TAF program.

It is anticipated that there will be two auctions in November totaling $150 billion. These auctions will provide short-term (one- to two-week term) TAF credit over year-end.

Foreign Exchange Swap Lines

The Federal Open Market Committee (FOMC) has authorized a $330 billion expansion of its temporary reciprocal currency arrangements (swap lines). This increased capacity will be available to provide funding for U.S. dollar liquidity operations by the other central banks. The FOMC has authorized increases in all of the temporary swap facilities with other central banks. These larger facilities will now support the provision of U.S. dollar liquidity in amounts of up to $30 billion by the Bank of Canada, $80 billion by the Bank of England, $120 billion by the Bank of Japan, $15 billion by Danmarks Nationalbank, $240 billion by the ECB, $15 billion by the Norges Bank, $30 billion by the Reserve Bank of Australia, $30 billion by the Sveriges Riksbank, and $60 billion by the Swiss National Bank. As a result of these actions, the total size of outstanding swap lines is $620 billion.

All of the temporary reciprocal swap facilities have been authorized through April 30, 2009.

Dollar funding rates abroad have been elevated relative to dollar funding rates available in the United States, reflecting a structural dollar funding shortfall outside of the United States. The increase in the amount of foreign exchange swap authorization limits will enable many central banks to increase the amount of dollar funding that they can provide in their home markets. This should help to improve the distribution of dollar liquidity around the globe.

charting BDI...

In the overall Great Global Expansion since the turn of the century BDI is in a rising channel for rates. If the BDI finds support at 3270 then it should signal that the US recession will stay somewhat isolated to this region and expansion in other regions will compensate. I'm not saying that the rest of the world will not feel the effects of a credit crunch in the US, but that our view of the crisis is someone skewed because we re at the epicenter of it. Which means recovery or expansion in the rest of the world will help lift the US out of the crisis.

14th WB Wachovia - sale before failure?

Wachovia is being preemptive of possible failure. Much like WAMU integrated itself into JPM late last week.

Wachovia sinks as investors weigh its fate

Shares plummet more than 50% ahead of bell as Citi and Wells Fargo bid for troubled bank, according to reports.

September 29, 2008: 7:46 AM ET

NEW YORK (CNNMoney.com) -- Wachovia stock lost more than half its value in pre-market trading Monday as investors mulled the fate of the bank, including a potential merger with one of its peers - Citigroup or Wells Fargo.

Wachovia (WB, Fortune 500) shares, which have lost nearly half of their value in the last week alone, plummeted another 58% before the opening bell.

The Charlotte, N.C.-based bank was reportedly in talks to sell itself to either Citigroup (C, Fortune 500) or Wells Fargo (WFC, Fortune 500). By Sunday evening, a bidding war between the two banking giants was underway, several news outlets reported.

Spain's Banco Santander (STD) had also been mentioned as a possible bidder heading into the weekend.

The talks come as concerns have grown about Wachovia's viability, despite a breakthrough reached Sunday by Congressional negotiators on a $700 billion bailout for the financial system.

Government refuses guarantee

Sunday's report in The New York Times added that the Federal Reserve and Treasury Department were also participating in the discussions, but that the government was refusing to help bidders by guaranteeing a part of Wachovia's assets the way it did for Bear Stearns in March, when it was sold to JPMorgan Chase (JPM, Fortune 500).

The government was also not ready to take over Wachovia the way it did Washington Mutual (JPM, Fortune 500) last week, the Times reported, unless the bank's financial position deteriorates more rapidly. The Seattle-based WaMu ultimately collapsed and was seized by federal bank regulators before it was subsequently sold to JPMorgan.

Talks were reportedly held as late as Sunday evening, but no deal had been struck by Monday morning.

Speculation that either Citigroup or Wells Fargo may only bid a few dollars a share for Wachovia also helped send Wachovia's stock lower, the Times reported.

Also unclear, the Times said, was whether the banks would bid for all of Wachovia or pieces. Wachovia's retail banking operations would help Citigroup and Wells Fargo expand their branch networks, the Times said.

Spokespeople for Citigroup, Wachovia and Wells Fargo declined to comment on the matter when talk of a possible deal first emerged on Friday.

Morgan Stanley deal unlikely

This wouldn't, however, be the first time that Wachovia has been mentioned eyeing a deal. A little over a week ago, there was rampant speculation that Morgan Stanley and Wachovia were reportedly discussing a merger. A deal between the two firms looks increasingly unlikely, though, after Morgan Stanley (MS, Fortune 500) agreed to sell up to a fifth of itself to Mitsubishi UFJ Financial Group (MUFG), one of Japan's largest banks, earlier this week.

Following a string of high-profile collapses of banks in recent weeks, there has been increasing speculation that Wachovia could be the next one to go.

Wachovia reported losses during the past two quarters due in large part to its exposure to the U.S. mortgage market. Some analysts have cited the company's ill-timed 2006 acquisition of the California mortgage lender Golden West Financial Corp. for its current woes.

A Wachovia representative stressed in a statement on Friday that it has a "strong retail franchise and large and stable deposit base," adding that it was working to strengthen both its capital and liquidity.

Were Wachovia to enter a deal, it would mark yet another big shake-up of the nation's banking industry, which has undergone a dramatic transformation in the past two weeks, including the demise of Lehman Brothers, the acquisition of Merrill Lynch by Bank of America (BAC, Fortune 500) and the failure of Washington Mutual and its subsequent purchase by JPMorgan Chase. To top of page

Where we are in the global recession as related to the Baltic Dry Index (BDI)

I've mentioned that the BDI is a leading indicator of economic expansion and contraction. Shipping prices are very volatile, they are usualy the first to feel the impact of expansion or contraction in trade and the wild swings in the rates of shipping can signal when it becomes too costly to conduct trade.

Now keep in mind that BDI signals global impact of trade.

I think the BDI can show us where we are in the recession we are in now. I don't care for the metric that you need successive negative GDP to get a recession as GDP is a measure that is not free market based. It is more prone to manipulation.

It seems that 2009 might be the bottom of the current recession by a number of factors.

BDI - First BDI has not bottomed. It might be another few months of bottoming before businesses feel comfortable enough to take on credit and start expanding again.

Bailout - Its going to be at least 3 months before the bailout is capable of moving CDO off the books of financials and into taxpayer hands. Probably 6-9 months before enough is converted that credit expansion can start up again.

SPX - following credit contraction in step as compared to the 2002 recession. Makes me feel that markets have much further to go before a bottom is in place. A few more bank failures in the next 3-6 months along with slow consumer spending to spook investors out of stocks.

rising bond prices can represent that investors are seeking safety in less risky investments but can also represent that credit is scarce and the government is either unwilling to or unable to expand credit. When the credit contraction occurred in early 2000 the flight to quality started and did not abate until mid 2003 when well after the recession. Yield cannot determine bottoms in expansion or contractions because amidst a contractions bond investors are still skittish and are distrusting of any signs that the contractions are over. again the flight to quality was a mean s of preserving capital and safety. they are not going to be willing to take a risk at finding a market bottom so they wait out the storm. yield can signal a contraction early but not a recovery. lot to markets like BDI and S&P500 to signal a recovery.

Wachovia and Nation City on deck for the next failure, next week might be a two fer.

Update from MarketWatch: Counterparty credit risk jumps on Wachovia concern

The CDR Counterparty Risk Index, which tracks credit-default swaps on leading banks and brokerage firms, surged more than 100 basis points to 430.2, close to a record. A basis point is one one-hundredth of a percentage point.

...

Credit-default swap spreads on Wachovia widened by 827.2 basis points and now trade between 28% and 33% "upfront," according to CDR.

...

"Wachovia is now trading at distressed levels, raising the specter of another major U.S. bank failure in the near future," CDR said in a statement.

National City stock is now off 50%.

Wachovia is off 30%.

Reader BR notes that investors are reacting to JPM's marks on WaMu's loan portfolio. These published marks will force the regionals to write down the value of their paper too.

As I mentioned earler, investors appear to be asking "Who is next?"

I don't think either of these banks will be seized today, but based on the pace of failures, I'd guess a bank failure is likely.

13th bank failure -- WAMU!!!

13 is a real unlucky number. Biggest bank failure, dwarfs IndyMac. That is why they negotiated it with JP Morgan ahead of time. This would have been a market routing event again. Now I'm seeing why the shorting ban. there is a lot of bad news this past two weeks.

Regulators seize Washington Mutual and JPMorgan mops up

Robin Sidel and David Enrich | September 27, 2008

IN what is by far the largest bank failure in US history, federal regulators seized Washington Mutual and struck a deal to sell the bulk of its operations to JPMorgan Chase.

The collapse of the Seattle thrift, which was triggered by a wave of deposit withdrawals, marks a new low point in the country's financial crisis. But the deal, as constructed by the Federal Deposit Insurance Corporation, could hold some glimmers of hope for the beleaguered banking system because it averts any hit to the bank insurance fund.

Instead, JPMorgan agreed to pay $US1.9 billion ($2.3 billion) to the Government for WaMu's banking operations and will assume the loan portfolio of the $US307 billion thrift. The full cost to JPMorgan will be much higher, because it plans to write down about $US31 billion of the bad loans and raise $US8 billion in new capital. All WaMu depositors will have access to their cash, but holders of more than $US30 billion in debt and preferred stock are likely to recover little or nothing.

The deal will vault JPMorgan into first place in nationwide deposits and greatly expand its franchise.

The fact that no bank was willing to buy WaMu until it failed shows how badly confidence has eroded in a banking system awash with record profits just a few years ago. Faced with deepening losses on mortgages, credit cards and other loans, big and small banks across the country are struggling with what many bank executives say is a crisis far deeper than the savings-and-loan debacle.

The seizure of Washington Mutual is likely to send tremors through the thrift industry. Many of WaMu's smaller brethren are also struggling with a wave of bad loans and some have already been ordered by regulators to raise capital and stop growing. Many community and regional financial institutions are also slashing dividends, selling branches and reining in lending.

WaMu has suffered huge losses but still boasts a strong deposit base and a network of 2239 branches that bigger banks would have paid dearly for when times were good. In March, with the credit crisis in full bloom, JPMorgan offered to acquire WaMu but was spurned in favour of a $US7 billion infusion led by TPG, a highly regarded private equity firm. TPG, led by investor David Bonderman, said it would lose $US1.35 billion, wiping out its investment.

This is the second time that JPMorgan, the second-largest US bank by market capitalisation, has been a buyer of last resort. In March, the New York company agreed to purchase Bear Stearns, getting a $US29 billion backstop from the federal Government.

DIC chairman Sheila Bair said that WaMu's downward spiral "could have posed significant challenges without a ready buyer."

Referring to JPMorgan's willingness to buy WaMu and absorb its shaky loans amid continuing debate over the $US700 billion bailout package, she added: "Some are coming to Washington for help, others are coming to Washington to help."

While WaMu has been struggling since last year, its demise occurred with breathtaking speed.

Starting on September 15, the day that Lehman filed for bankruptcy protection, WaMu's customers began heading for the exits.

Over the next 10 days, they yanked a total of $US16.7 billion in deposits out of the bank, according to the Office of Thrift Supervision.

Regulators also hustled to shut down WaMu faster than they have with other failing banks this year.

Normally, when the FDIC and another regulatory agency are preparing to take over a bank, the FDIC will solicit bids for the bank on Tuesday or Wednesday and then seize it on Friday evening, after the bank's branches have closed for the weekend.

In WaMu's case, the FDIC set a Wednesday evening deadline for interested parties to submit their offers for various parts ofWaMu.

Twenty-four hours later, they were already preparing to seize the bank.

Earlier this month, Treasury Secretary Henry Paulson made it clear to WaMu that the company should have accepted the takeover deal offered by JPMorgan earlier this year, according to a person close to WaMu.

Federal regulators said the exodus of deposits left WaMu "with insufficient liquidity to meet its obligations".

As a result, WaMu was in "an unsafe and unsound condition to transact business", according to the OTS.

With mortgage losses mounting and its stock price plunging, WaMu has been scrambling over the past month to find a solution.

Last week, it put itself on the auction block. A number of banks -- including Citigroup, Wells Fargo and Banco Santander -- pored over WaMu's books, but the bank did not receive any offers.

This week, WaMu's outside bankers approached a group of private equity funds to gauge their interest in a deal. Those talks were viewed as a last-ditch effort.

Also this week, the FDIC took the step of reaching out to banks, asking them to express interest in taking over some or all of WaMu, according to people familiar with the matter. Those bids were due at 6pm on Wednesday.

JPMorgan's takeover of WaMu's deposits represents a huge blow for private equity firm TPG, which led the deal to inject $US7 billion into the thrift earlier this year.

"Obviously, we are dissatisfied with the loss to our partners from our investment in Washington Mutual," said a TPG spokesman.

"The unprecedented turmoil in global financial markets and resulting macro crisis of confidence has radically changed the dynamics for all financial institutions, and led to widespread losses among investors throughout the sector."

The deal is a bold move for James Dimon, JPMorgan's chairman and chief executive, who has emerged as one of the banking industry's most powerful executives during the current credit crisis.

Just six months ago, JPMorgan swept in to acquire Bear Stearns as the brokerage firm was collapsing and heading for bankruptcy.

Although JPMorgan has also been hurt by the credit crisis, it has one of the strongest balance sheets in the industry despite exposure to many of the banking businesses that are feeling pain.

Additional reporting: Dan Fitzpatrick, Damian Paletta and Peter Lattman

but it is credit expansion which is what the global economy runs on. and it devalues the dollar improving US exports. playing devils advocate. I don't like it but the current banking system and the economy running on it.

We're still ~60 S&P500 points off the lows so Congress seems to feel like there's some breathing room and the partisans take the opportunity to throw elbows around.

There's nothing fundamentally sound about the government taking bad paper off private investors books.

Lawmakers split over bailout

Democrats say they reached bipartisan agreement on set of principles, but Republican balk. White House meeting contentious.

By Tami Luhby, CNNMoney.com senior writer

Last Updated: September 25, 2008: 6:59 PM ET

NEW YORK (CNNMoney.com) -- Chaos erupted on Thursday in the negotiations over the proposed financial bailout as lawmakers bickered over competing counterproposals to the Bush administration's $700 billion rescue plan.

A meeting at the White House between President Bush, congressional leaders and the presidential candidates was meant to speed approval of an agreement, but instead revealed deep divisions between Democrats and Republicans.

Earlier in the day, congressional negotiators said they had agreed to a set of principles on revisions to the rescue plan, which calls for the Treasury Department to buy up bad mortgage securities from banks in an effort to get them to lend again.

The proposal will help homeowners, curb executive pay packages at participating firms and provide oversight of Treasury's actions, said Sen. Christopher Dodd, D-Conn., a key architect of the congressional effort, in a lunchtime address.

"We've reached a fundamental agreement on a set of principles, one, for taxpayers, which is tremendously important," he said. "We're very confident we can act expeditiously."

Details on the plans

The principles call for Congress to make $250 billion available immediately with $100 billion available, if needed, without requiring additional congressional approval, said two senior Democratic aides familiar with the negotiations. The second half of $350 billion would then become available by a special approval of Congress.

On executive compensation, the draft would require limits on compensation for executives of any company participating in the bailout. These caps would apply for as long as the company is in the program. This would include some language to limit excess "golden parachutes."

Treasury will also get an equity stake in the companies being helped by the bailout, though what type remains to be worked out.

Still to be worked out is whether to allow bankruptcy judges to modify mortgage terms, a provision backed by many Democrats and community activists but opposed by Republicans and the banking industry.

The bankruptcy provision is not the only sticking point, however. House Republicans are not on board, according to Minority Leader Rep. John Boehner, R-Ohio.

"House Republicans have not agreed to any plan at this point," Boehner said.

Instead, they issued a statement of economic rescue principles that calls for Wall Street to fund the recovery by injecting private capital - not taxpayer dollars - into the financial markets. Easing tax laws would prompt investors to put in their own dollars, they said.

The plan also calls for: participating firms to disclose the value of the mortgage assets on their books, ending Fannie Mae and Freddie Mac's securitization of "unsound mortgages," reviewing the performance of the credit rating agencies and having the Securities and Exchange Commission audit failed companies to ensure their financial standing was accurately portrayed.

House Republicans also want to create a panel to make recommendations for reforming the financial industry by year's end.

Meanwhile, the ranking Republican on the Senate Banking Committee has another idea. Sen. Richard Shelby, R-Ala., said he doesn't support the Treasury plan until there is serious consideration of alternatives. He proposed Thursday adding funds to the Federal Reserve and Treasury to allow them to lend more to financial institutions.

Bush still hopeful

Before the afternoon meeting, Bush said he expects a deal "very shortly."

After, a counselor to the president said "we're getting closer. There's some more that has to be done. It's going to be a consensus plan at the end of the day."

"Both sides are going to have to work hard to get to an agreement," presidential counselor Ed Gillespie said on CNN.

Administration officials have spent countless hours this week behind closed doors with and in public hearings before Congress. Lawmakers were hoping to have a deal agreeable to both parties hammered out before Thursday's meeting at the White House.

On Wednesday night, Bush took the nation's airwaves in a prime-time address in which he laid out a looming economic disaster.

"The government's top economic experts warn that, without immediate action by Congress, America could slip into a financial panic and a distressing scenario would unfold," Bush said. "More banks could fail, including some in your community. The stock market would drop even more, which would reduce the value of your retirement account. The value of your home could plummet. Foreclosures would rise dramatically."

CNN Correspondent Kate Bolduan and Congressional Producer Deirdre Walsh contributed to this report. To top of page

First Published: September 25, 2008: 1:28 PM ET

Agreement Reached on Bailout

Ahead of High-Level Meeting

Proposal Breaks $700 Billion Into Installments

By GREG HITT, DEBORAH SOLOMON and DAMIAN PALETTA

A bipartisan group of House and Senate lawmakers left a two-hour-plus meeting in the U.S. Capitol on Thursday saying they have a "fundamental agreement" on a $700 billion plan to bail out U.S. financial markets.

The lawmakers didn't offer details of the plan, but the proposed bill would approve the fund, but would pay the money out in installments, with $250 billion in bailout funds available immediately, people familiar with the matter said.

Lawmakers also agreed that limits on "golden parachutes" and use of warrants would apply to all companies, these people said. However, changes to bankruptcy laws still unresolved. The details still need to be ironed out with the White House.

Republican Sen. Robert Bennett of Utah expressed optimism that lawmakers have a "plan that will pass the House and Senate."

[Congressional leaders reached an agreement on a bailout package.] Reuters

Rep. Barney Frank, second from left, and Sen. Chris Dodd, third from right, spoke with reporters after congressional leaders said an agreement was reached on a bailout package.

"We came to agreements on a lot of the important issues," House Financial Services Chairman Barney Frank (D., Mass.) said at a press conference featuring most of those who attended the meeting. Sen. Bob Corker (R., Tenn.) said: "I believe that we will pass this legislation before the markets open on Monday."

Frank's Senate counterpart, Banking Committee Chairman Christopher Dodd (D., Conn.) said lawmakers plan to "act expeditiously" to pass legislation allowing the federal government to buy billions of dollars in distressed assets. The final legislation is expected to vastly expand on a Treasury proposal issued last weekend. It potentially includes some limits on executive compensation for companies that sell their assets to the government and some way for the government to recoup the money it spends to help free illiquid credit markets.

"I believe we are on track to pass it," Mr. Frank said following the meeting.

Lawmakers said they plan to talk to members of their parties in both the House and Senate before a meeting scheduled at the White House later Thursday to discuss the legislation with the Bush administration.

A dramatic flurry of activity, including a prime-time address by President George W. Bush late Wednesday, appeared to galvanize efforts to finalize the administration's $700 billion financial-markets bailout, despite continuing tensions and an occasionally heated debate on Capitol Hill.

Democratic leaders hoped to nail down details of the measure Thursday, ahead of an extraordinary summit meeting in the afternoon at the White House, which will bring together Republican and Democratic presidential nominees, along with Mr. Bush and top leaders from Congress.

Hours before the meeting, the White House said "significant progress" has been made. "We have made progress every day, and we are closer today to a conclusion than we were yesterday," said White House spokeswoman Dana Perino.

Sen. John McCain (R., Ariz.), Sen. Barack Obama (D., Ill.) and congressional leaders from both parties will meet Mr. Bush at the White House late Thursday afternoon. The meeting will be a chance to "have everybody get together and hopefully start driving to a conclusion," Ms. Perino said. "I can't tell you if we would have a final deal by then, or [if] it would emerge right after that."

Sens. McCain and Obama addressed the issue at a Clinton Global Initiative event Thursday morning. Sen. McCain said "the whole nation was in danger" and that time was short and doing nothing wasn't an option. Sen. McCain said he would carry to Washington five improvements to Treasury's rescue plan: greater accountability from a bipartisan board with oversight; a path for taxpayer recovery of funds; complete transparency in review of legislation -- all details made available online; absolutely no earmarks to be included in bill; and curbs on Wall Street executives' ability to profit from the bill.

Sen. Obama said that a "failure to act" on the bailout plan would have "grave consequences." But he said that it is "outrageous" that taxpayers must bear the burden for Wall Street "greed and risk," adding that the American people must not reward Wall Street executives.

Much is still uncertain and the contours of a likely bill could change. But the outlines of a potential compromise began to emerge late Wednesday after congressional leaders started considering restrictions on the bailout plan that could break the pool of money into installments.

Former New York City Mayor Rudy Giuliani says a Wall Street bailout is urgently needed, but should be followed by an investigation. Giuliani, who attended the World Business Forum at Radio City Music Hall, speaks with Kelsey Hubbard. (Sept. 24)

A likely bill would include limits on executive pay in situations where the government puts a large amount of money into a failing institution. In certain cases, the government could receive warrants that would give it the right to acquire shares in the company. Also included is beefed-up oversight through the Government Accountability Office, an investigative arm of Congress.

Likely not included is a controversial idea to let judges alter the terms of mortgages during bankruptcy proceedings.

"Without immediate action by Congress, America could slip into a financial panic and a distressing scenario would unfold," Mr. Bush said in a 12-minute address in which he warned in stark language about the danger of delay. Mr. Bush endorsed several of the changes that have been demanded in recent days from the right and left. He said the bill "should be enacted as soon as possible."

The basic building blocks of the bailout plan as initially proposed remain intact: Democratic leaders are still proposing to authorize Treasury to borrow up to $700 billion to buy hard-to-sell assets from troubled financial institutions. The goal is to calm financial markets by removing the toxic assets, mostly mortgages, which lie at the heart of the crisis. If a final deal is struck, it would represent one of the biggest government bailouts in U.S. history.

Whether the Bush administration will agree to the entire Democratic wish list of provisions isn't clear. Its room to maneuver will be limited, having urged Congress this week to act quickly to forestall financial calamity.

One scenario being discussed by Democrats would be to establish benchmarks to periodically measure the bailout's performance. Those benchmarks would have to be met before further allotments of government money could be used -- in effect, potentially breaking the bailout funds into several installments. The administration doesn't want Congress to split up dispersing the funds, particularly if that would require returning for continual congressional approval, according to people familiar with the matter.

There is less resistance to the idea of having an independent oversight board approve the installments, depending on who sits on the board. But the hope within the administration is that beefed-up oversight will negate the idea, these people said.

Congressional officials don't expect to forge a final deal Thursday morning. But they do expect to sort through remaining details on a handful of issues, including executive-pay limits, housing, equity stakes and the plan to have staged drawdowns on the $700 billion. That would set the stage for a final compromise to be pieced together at the White House later in the day, if all of the parties invited to the meeting can be satisfied.

New Wrinkle

Unknown still is the reaction from rank-and-file lawmakers, particularly conservatives, many of whom have been strongly opposed to the plan. Treasury Secretary Henry Paulson and Federal Reserve Chairman Ben Bernanke testified once again before skeptical members of Congress -- both Democrats and Republicans -- following a similar hearing Tuesday in the Senate.

Adding to the pressure on lawmakers to do a deal, billionaire investor Warren Buffett said he wouldn't have considered investing in Goldman Sachs Groups Inc., a move he announced Tuesday night, if he didn't think the bailout would be approved. "I really do think Congress will do the right thing, when it's terribly important, and they will do it fast," he said. "They will haggle but they have the national interest at heart."

The idea to set benchmarks to measure the plan's success was a new wrinkle that emerged Wednesday, when Democratic party leaders started debating the possibility. Any benchmarking plan, however, itself remains a rough outline. A key issue would be deciding how to judge whether the benchmarks were being met, and whether that authority would reside with the administration or with an independent board that would be created to oversee the rescue plan.

Democratic leaders have discussed holding a quick vote on perhaps one-third of the funds sought by the administration, with a second vote later on the rest. That option is considered less likely, although congressional aides and lawmakers cautioned that nothing has been ruled out.

Amid uncertainty during the day over the continued political wrangling in Washington, investors around the world snapped up short-term Treasury bills, one of the safest investments around. The yield on the one-month T-bill fell to 0.01% early Wednesday morning -- meaning that, in return for safety for their money, investors were willing to accept almost no return whatsoever -- and ended the day at 0.2%.

Republicans are concerned about the overall cost of the plan, and the broad powers it would give the Treasury to intervene in the marketplace. Rep. Eric Cantor, a conservative Republican from Virginia, has floated the idea that the government could insure mortgage assets, rather than buying them outright. Such a move would essentially provide a government guarantee for the assets at a certain price.

Treasury had considered a similar plan but rejected it in favor of buying the distressed assets. Mr. Paulson viewed that as a quicker and more efficient way to get to the root of the problem, according to people familiar with the matter.

Democrats, meanwhile, are pressing for action to help homeowners and families in dire straits, not just Wall Street bankers.

It's impossible to handicap the bill's actual prospects, in part because lawmakers are grappling with the complicated political calculus created by the November elections. Still, party leaders have said they're committed to passing the bill in some form.

Addressing the Joint Economic Committee, Bernanke discusses the reasons behind the agency's actions concerning Fannie Mae and Freddie Mac as well as AIG.

Democratic and Republican leaders prepared to work though the weekend and into next week if necessary. "We'll finish it when it's ready," said House Speaker Nancy Pelosi, a California Democrat. She has been buffered by anger within the House Democratic Caucus over the costly bailout Mr. Bush is demanding. Some Democrats don't want to do a deal with the White House, but she has pressed forward. "We're going to get it right."

The White House and its Republican allies have made an uneasy peace with Democratic leaders of the House and Senate, who have committed to carry the proposal forward. Late Wednesday, Speaker Pelosi and House Minority Leader John Boehner (R., Ohio) issued a joint statement vowing to "work cooperatively and on a bipartisan basis." The two party leaders stressed their commitment to improve oversight of the bailout and protect taxpayer interests.

But in addition to the new changes they are seeking, Democrats are also urging the White House to deliver Republican votes for the package. "We are not taking ownership of this," Mrs. Pelosi said.

The risk for the White House is that Mr. Bush, with his popularity at 30%, just a few points above its all-time low, won't be able to seal the deal. In that case, the administration might have to make more significant concessions to Democrats, in turn further endangering Republican support.

Give-and-Take

In give-and-take on Capitol Hill Wednesday, Mr. Paulson signaled his intention to relent on another key Democratic demand: that limits should be imposed on the compensation of executives at firms participating in the program. Mr. Paulson had previously argued against pay limits, suggesting they might deter companies from participating in the bailout. That argument proved to be a political loser.

"We must find a way to address [executive pay] in the legislation, but without undermining the effectiveness of the legislation," Mr. Paulson told the House Financial Services Committee.

Mr. Paulson has publicly resisted the notion of dividing the $700 billion plan into several parts, saying markets need a big number to instill confidence that the plan will succeed. Privately, however, there was growing acknowledgment within the administration Wednesday that the money might be released in stages.

One big concern: Having to continually ask Congress for money would breed uncertainty in the markets and potentially undermine the program, a senior administration official said. Another top administration official suggested the administration is willing to support the idea, so "long as it's done in a way that doesn't render the program ineffective."

Lawmakers continued to unload their frustration on Messrs. Bernanke and Paulson during hearings Wednesday. Mr. Bernanke, stepping beyond his usually cautious and measured tone, upped the ante, warning the nation faced "grave threats to financial stability." He detailed how nearly every sector of the economy, already under intense stress, would worsen if faced with further financial-market uncertainty.

—Michael R. Crittenden, Henry Pulizzi, Sudeep Reddy, John D. McKinnon and Michael R. Crittenden contributed to this article.

Write to Greg Hitt at greg.hitt@wsj.com, Deborah Solomon at deborah.solomon@wsj.com and Damian Paletta at damian.paletta@wsj.com

nice call, seems the song and dance on capital hill was a show for voters. paulson comes along with a outlandish proposal. 700bil, total authority, not executive reign in. congress whines about it for two days and they come up with a middle of the road agreement that caps executives, and lets congress oversee it.

the end result taxpayer feel they got something out of the deal but they still cough up 700billion and pay more that what the mortgages are worth. Oh and pump the stock market up and they will feel happy about it all lol.

I mean it is all about psychology, because rationally its a terrible deal and damages the taxpayer and the firms can walk away from all the toxic cdos like it never happened.

but emotionally I feel I guess its better this way, stock market is up so everyone else thinks its good too.

economically the taxpayer burden will weaken the dollar long term, cut export to the US, good luck buying a nissan or volvo, us manufacturers will be happy. chinese goods will suffer. US manufacturing will strengthen.

short term it might give the dollar a boost as foreign money flows back in.

I think there is still a lot of foreclosures to go over the next 9-12 months. consumption this holiday season will be weaker than last year. but money flow will trump actual sales and wall street will tell investor to no be so glum about it just get in for the election year\xmas rally.

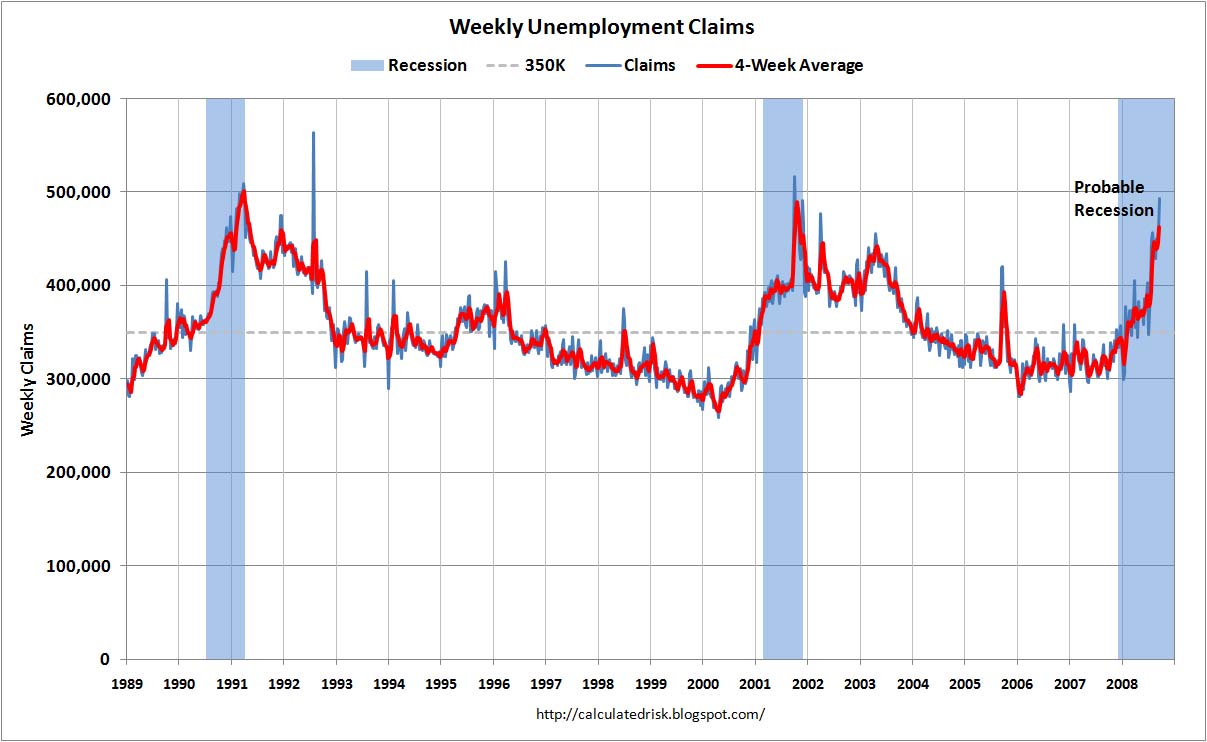

Weekly Unemployment Claims Jump to 493,000

by CalculatedRisk

The DOL reports on weekly unemployment insurance claims:

In the week ending Sept. 20, the advance figure for seasonally adjusted initial claims was 493,000, an increase of 32,000 from the previous week's revised figure of 461,000. It is estimated that the effects of Hurricane Gustav in Louisiana and the effects of Hurricane Ike in Texas added approximately 50,000 claims to the total. The 4-week moving average was 462,500, an increase of 16,000 from the previous week's revised average of 446,500.

I added the SPX chart to show why we might not be at the bottom yet. Mid 2009 I believe. Looks at when the market bottoms and when Unemployment claims does. Also note that when Unemployment claims starts to rise the markets start to top

This graph shows weekly claims. The four moving average is at 462,500.

Some of the jump in unemployment claims is a result of the hurricanes - and should be temporary - but away from the financial crisis this shows there are significant weaknesses in the labor market and real economy.

History lesson, Warren Buffet and Solomon Brothers... strangely relevant.

http://chinese-school.netfirms.com/Warren-Buffett-Salomon.html

Warren Buffett's Wild Ride at Salomon

October 27, 1997

Warren Buffett's Wild Ride at Salomon A harrowing, bizarre tale of misdeeds and mistakes that pushed Salomon to the brink and produced the "most important day" in Warren Buffett's life.

Carol J. Loomis

Reporter Associate: Maria Atanasov

As Sanford I. Weill, 64, the dealmaking CEO of Travelers Group, steps up to his biggest acquisition ever--the purchase of Salomon Inc. for $9 billion--a famous Wall Street figure, Warren E. Buffett, 67, steps out of Salomon. His days there began almost precisely a decade ago, in the early fall of 1987, when his company, Berkshire Hathaway, became Salomon's largest shareholder and he moved in as a director. But that was training-wheels stuff, nothing to the high-wire unicycle act that came later: Buffett was physically, emotionally, and really at Salomon for nine months in 1991 and 1992, when the firm's trading illegalities created a giant sucking sound that brought him in to run the place.