News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Bernanke on Fire-Sale Prices

by CalculatedRisk

the gist of it is that the Fed will buy mortgages at or near the full value of the mortgage (plus interest???) and the Fed will then hold those mortgages until they mature, regardless what the asset price is. Say a dishwasher from Detroit bought a $300,000 townhouse subprime. His mortgages is owned by FNM, FRE, JPM, MS, etc. The Fed will pay the full value of the mortgage 300k plus a kickback to the seller. If the house after raped for metal is worth $5k, then the Fed will hold the mortgage until it is paid of IF, I REPEAT IF it is paid off. It will not get foreclosed on and will probably sit on the books forever until the asset price inflates to the full value of the mortgage. 20yrs, 30yrs, 50yrs, 100yrs. You see what I'm getting at. Who pays the property taxes on that real estate, maintains it, etc. What if the cost of gov. ownership is more than what it gains in value?

Now we see why the banks pushed to get Paulson into the Treasury so quickly. Just before the first shoe dropped. They needed an inside guy to fix the mess and get the financial institutions covered before he leaves and you bet he will leave once he has this set in motion, thus why no one can challenge the $700bil bailout. Lock it in and have the taxpayer suffer.

From Reuters: Bernanke's comments on asset auction process

I believe that under the Treasury program, auctions and other mechanisms could be devised that will give the market good information on what the hold-to-maturity price is for a large class of mortgage-related assets. If the Treasury bids for and then buys assets at a price close to the hold-to-maturity price, there will be substantial benefits.

Banks will have a basis for valuing those assets and will not have to use fire sale prices. Their capital will not be unreasonably marked down.

Originally I expected the plan to have two components: 1) buy troubled assets from institutions, and 2) an RFC type recapitalization plan. However the plan did not include the recapitalization provision, so the clear intent is to pay premium prices (to current market prices) for troubled assets to recapitalize the institutions (with no equity participation for taxpayers).

Bernanke and Paulson are clearly arguing the current market prices are wrong - that they are "fire sale prices".

Krugman has more: Getting real — and letting the cat out of the bag

[T]he key question is what price Treasury pays for the assets. And here we have Bernanke effectively saying that it’s going to pay above-market prices — prices that allegedly reflect “hold-to-maturity” value, but still more than private investors are willing to pay.

...

[T]he plan only helps the financial situation if Treasury pays prices well above market — that is, if it is in effect injecting capital into financial firms, at taxpayers’ expense.

What possible justification can there be for doing this without acquiring an equity stake?

No equity stake, no deal.

One thing is clear - something we all guessed correctly - is that the intention of the plan is to pay premium prices for troubled assets to recapitalize the banks. It’s still not clear how the price mechanism will work, and unfortunately Paulson and Bernanke are unable to describe how this will work.

Except Paulson did say they would hire “really good asset managers” to determine the price. A little sarcasm: I suppose these are asset managers that have been shorting financials for the last couple of years (hat tip Seminole).

synopsis of the congressional plan. so far we have come from the inception of the Fed to reign in hyperinflation, to Congress trying to reign in the Fed.

The important part of the congressional plan seems to latch itself to the financial institutions that are dumping the bad assets on the taxpayers. taking a stake in wall street if you will. what the banks are crying about is that this will hamper their recovery, dilute their shareholders (a.k.a. the insiders). caps executive bonuses, or axes them completely. all in all not friendly to the banks. in fact they may choose not to fork over the bad debt to the Fed if it means forking over a share of the pie. Congress does not know the culture of these institutions. Enron's culture pales in comparison to BSC, GS, LEH, etc. They will go down in pride than lose face, admit they were wrong, in fact they will sell you how they were right in going down and get you to place one last bet before the ship sinks.

This plan does not give the banks much incentive other than their survival to sell their debt. If they do agree to it it means they will increase fees to clients. Remember the days before electronic trading when commissions for trades were 5-10% of capital, when the markets were so illiquid that the spread on bid and ask were 10% of the stock price!

Might not get that bad, its a huge global economy, but it underlays the trend to protectionism, to a recessionary economy that plans to be multi year, over regulation stifles growth, but it puts a floor in on a bust, so do you want to sacrifice future economic growth to slow and stop the deflation?

in the deregulative economy you have more opportunities to advance and advance quickly, but at greater risk, and at the downside that when you do risk you loose almost everything. you have the choice of not risking and playing it safe but the net result is that inflation will increase at a rate faster than the safe level you grow at so you will get wiped out over the long term, you have to risk.

in a regulative economy there are less opportunities to advance and advancement is slowed by regulation which caps your ability to grow the further you advance. you have to work harder the more you advance as asset reallocation is used to support the economy so it doesn't fall under. everyone gets bailed out. economy recovers faster but at the cost of your future production, or higher taxes presently, so you are forced to pay down debt sooner and not pass it off, so less growth over the next few years in hopes that over the next 10-20 there will be a more substantial and stable economy that we can start deregulating again.

whew.. this is getting too long... I'll leave it here for now.

Treasury Disputes Democrat On Changes in Bailout

TREASURY DISPUTES DEMOCRAT ON CHANGES IN BAILOUT

| 22 Sep 2008 | 09:48 AM ET

The negotiations over a $700 billion Wall Street bailout plan took a new turn when the Treasury disputed a claim by a key Democrat that it had agreed to changes in the rescue proposal.

Barney Frank, chairman of the House of Representatives Financial Services Committee, told CNBC that the Bush administration has accepted changes to its bailout plan that would give the government a stake in institutions unloading assets under the plan.

But the Treasury, responding to the Frank interview, told CNBC that there was no such deal on equity stakes.

Frank, a Massachusetts Democrat, also said the administration has agreed that the plan should include more efforts to prevent home foreclosures and that an oversight board should be created to monitor the bailout.

On reducing foreclosures, Frank said, "The foreclosure piece is agreed on. There was Republican congressional opposition but the administration accepted it. "They've accepted our views on oversight ... There is some contention now over compensation and corporate governance."

It was the latest step in fast-moving negotiations between Congress and the administration over a massive program designed to address the worst U.S. financial crisis since the Great Depression.

Financial markets remained volatile as investors waited to see the outcome of the bailout talks in Washington.

U.S. stocks were sharply lower, while European stocks edged higher. Asian stocks closed higher .

The US dollar fell and Treasury debt prices edged up. Oil prices soared.

"We need to see more details from the rescue package. What is missing is the price the U.S. authorities are going to pay for the toxic assets," said Heino Ruland, analyst at FrankfurtFinanz.

Meanwhile, the Federal Reserve agreed to let the investment banks Goldman Sach and Morgan Stanley convert into more conventional depositary institutions.

By agreeing to much tighter Fed regulation as bank holding companies, Goldman Sachs and Morgan Stanley moved to avoid the fate of rivals that either collapsed or were taken over in the worst financial crisis to sweep Wall Street since the Great Depression.

Morgan Stanley went a step further and struck a deal with Japan's largest bank, Mitsubishi UFJ Financial Group. MUFJ agreed to buy up to a 20 percent stake, sending Morgan Stanley shares up sharply.

For Investors

# Is It Time to Buy Stocks Now?

# Measuring Risk in Volatile Times

# What the Experts Think You Should Do

# Is Your Money-Market Fund Safe? Find Out

# Slideshow: Biggest Chapter 11 Cases in US History

# Eight Tips for Investing in Hard Times

# Need Safety? Take a Look at Bonds

# What If You're a Client of Lehman, Merrill or AIG?

# Have an AIG Insurance Policy? Don't Fret

# How You Can Protect Your Money

The Democratic counterproposal allows Treasury to buy troubled assets from any financial institution but requires Treasury to report regularly to Congress and disclose publicly each Friday the total assets held and total assets bought and sold that week.

Companies unloading troubled assets onto Treasury could not offer executives pay incentives deemed "inappropriate or excessive" by the Treasury secretary.

In addition, executive incentive pay based on profits or other benchmarks later proven to be inaccurate could be taken away, or clawed back, under the Democrats' language.

Democrats also want to create an oversight board to include the chairmen of the Federal Reserve, Federal Deposit Insurance Corp and Securities and Exchange Commission to limit the Treasury's broad powers under the plan.

The "Emergency Oversight Board" would monitor the bailout and make recommendations to the Treasury secretary.

In addition to the Fed, FDIC and SEC chairmen, the board would include one non-government member appointed by Congress' majority leadership, and one appointed by minority leadership.

A key Senate Republican has significant reservations about the plan, said his spokesman Monday.

Alabama Sen. Richard Shelby, top Republican on the banking committee, remains unconvinced that Treasury's proposal strikes a balance between the interests of the taxpayer and the economy, said spokesman Jonathan Graffeo.

Shelby is concerned that the plan "would reward Wall Street while doing nothing for homeowners or for local financial institutions ...

He will continue to work with Chairman Dodd to see whether there is a way forward," Graffeo said.

Under the Senate Democrats' proposal, Treasury could not buy, or commit to buy, any troubled assets unless it gets "contingent shares" in the asset-selling institution "equal in value to the purchase price of the assets to be purchased." The contingent shares could be shares in the financial institution, its parent or holding company, or a related institution, according to the draft language.

If shares in the asset-selling company were not publicly traded, Treasury could take senior debt instead of shares.

If Treasury later disposed of the troubled assets and got less money for them than it paid initially, the contingent shares would help cover the loss, the language said.

The Democrats' proposal calls for the entity that manages the troubled assets bought under the plan to work to prevent foreclosures and protect homeownership through loan modifications and use of related federal programs.

—Reuters contributed to this report.

© 2008 CNBC

THIS....

#msg-32344624

From Hyde to Jekkyll: Goldman And Morgan Morph Into Banks

by Dr Joe Duarte September 22, 2008

excerpt... it's the same thing I've been told from a few other sources as well.

According to the Post "Had the Treasury and Fed not quickly stepped into the fray- on Thursday- morning with a quick $105 billion injection of liquidity, the Dow could have collapsed to the 8,300-level - a 22 percent decline! - while the clang of the opening bell was still echoing around the cavernous exchange floor."

The Post added: " According to traders, who spoke on the condition of anonymity, money market funds were inundated with $500 billion in sell orders prior to the opening. The total money-market capitalization was roughly $4 trillion that morning. The panicked selling was directly linked to the seizing up of the credit markets - including a $52 billion constriction in commercial paper - and the rumors of additional money market funds "breaking the buck," or dropping below $1 net asset value."

The announcement of government backing settled those fears as well as the 100 billion overnight repo. Markets will probably settle back down to pre repo levels again as it was a none event and Asian and European liquidation continues.

Short-Sale Restrictions and Inverse ETFs

Friday September 19, 7:00 pm ET

By John Gabriel

ahhh. the real lowdown on the inverse etfs, not shorting but engaging in trading of swaps.

There's a palpable sense of fear and uncertainty in the markets today. This helped lead to a number of unprecedented government actions this week including a wide sweeping ban on short sales of 799 financial stocks, tapping into a $50 billion fund to guarantee money market assets, and discussions of creating a Resolution Trust-like vehicle to help shore up the balance sheets of struggling financial institutions. Following the announcement of the ban on short sales, two ProShares inverse funds (including the widely held UltraShort Financials ProShares (NasdaqGS:SKF - News)) ceased trading for a couple hours this morning in order to give the issuer a chance to sort through the implications of these government actions. In this article, we will attempt to shed some light on the situation by addressing the major questions about what happened this morning and how the Securities and Exchange Commission's restriction on short selling financial stocks will affect exchange-traded funds in the future.

If these funds use swaps agreements to replicate inverse returns on their stated benchmarks, then why are short-selling restrictions on individual financial stocks affecting and Short Financials ProShares (AMEX:SEF - News)?

It's true that these ETFs don't actually engage in short selling to produce inverse returns on their stated benchmarks--they typically use swaps and futures, which are contracts to pay a fixed amount of interest in return for a counterparty paying the return on an agreed-upon index (in this case, the Dow Jones U.S. Financials). However, issuers like ProShares cannot find willing counterparties to the swaps they would need to write, as the counterparty would need to hedge the position by shorting financials. With the short-selling restriction in place, there aren't any counterparties willing to assume this huge risk. Keep in mind that most often the counterparties we are referring to are investment banks, such as Goldman Sachs (NYSE:GS - News), Morgan Stanley (NYSE:MS - News), and Merrill Lynch (NYSE:MER - News)--each of which are dealing with their own issues amid the credit crises.

Ostensibly there's an exemption for the ETF/ETN market makers that create and redeem shares to short shares as part of an ETF portfolio hedge, but ProShares does not short equities in any of its portfolios nor does its prospectus explicitly reserve the right to short equities. The language of the emergency order also makes it difficult to tell if a broker-dealer would be allowed to short financial stocks in order to hedge an ETF's swap position. At this stage in the game, with the capital constraints and confidence issues that these firms are currently facing, banks taking the other side of ProShares' swaps may just not want to risk incurring the SEC's wrath.

The bottom line is this: The lack of counterparties means that new swap agreements are extremely difficult to obtain, so no new assets can be invested and no more shares created (see ProShares' press release).

Why did SKF and SEF stop trading?

As previously discussed, due to the short-selling ban on financial stocks, there are no counterparties willing to buy/write the issuers' swap agreements, as the wide sweeping ban on shorting financial stocks means that the counterparty would be unable to hedge away its exposure. The shares of these ProShares ETFs did resume trading in the financial markets today, but they seem to be trading at prices that are not in line with their intraday indicative values. This is to be expected, however, based on the simple laws of supply and demand. Viewed as one of the remaining avenues to gain short exposure to the financial sector, the demand for the SKF and SEF were expected to explode. Essentially, all who were covering their existing short positions in response to the ban were expected to attempt to gain short exposure via these inverse financial sector ETFs.

Thus, ProShares contacted the American Stock Exchange this morning to note that it was not planning to create new shares in light of the SEC's unprecedented ban on shorting 799 financial stocks. The AMEX responded by halting trading on the securities to prevent huge diversions between the indicative benchmark value and market price.

What are the likely effects of this until the end of the short-selling ban on Oct. 2?

As long as investment banks are concerned about capital reserves and the amount of risk on their books, they are unlikely to write swaps that short financials. Thus, existing shares of these inverse financial ETFs should continue trading, but new shares will not be created.

According to its prospectus, ProShares invests in only derivatives (including options, swaps, and forwards), so it does not actually short the stocks itself. An emergency amendment to the prospectus that would allow the issuers to engage in short selling is a possibility, but unlikely in our view.

So long as ProShares is unable to find counterparties to short the index, it will continue to allow only redemptions and not creation of new shares. This will prevent the ETFs from trading at a discount, but it will allow them to trade at a substantial premium (as no authorized participants can arbitrage the premium away by creating new shares and selling them until the premium disappears). We've already noticed the SKF trade at a 5%-6% premium over net asset value.

Even if investment banks stabilize and become willing to take risk onto their balance sheets before Oct. 2, the expenses on these funds will increase substantially as counterparties demand much higher interest payments to take on the unhedgeable risk. This cost would be expressed in the fund's expense ratio.

In our opinion, the only hope of clearing this up before Oct. 2 is either an SEC clarification that broker/dealers can short stocks to hedge derivatives bought by ETF market makers, or a change to the ETF prospectuses that allows the funds themselves to short stocks directly.

What else can I do in the meantime?

Although investors cannot currently short sell individual financial stocks, there is no ban on shorting ETFs that court exposure to the sector, such as the Financial Select Sector SPDR (AMEX:XLF - News) (long financials) or the Ultra Financials ProShares (AMEX:UYG - News) (double-long financials). Individuals could short UYG instead of buying SKF, although we'd note that this leaves open the potential for bigger losses over multiday periods due to the compounding of leveraged daily returns. The Rydex Inverse 2x S&P Select Sector Financial (AMEX:RFN - News) is still trading and creating new shares, although it is also likely to have trouble finding willing counterparties if it faces a wave of new assets flooding in to short financials.

Investors who already own SKF or SEF can sell the funds at any time because trading has recommenced, and since redemptions are still allowed, there is little risk of selling at a discount. In fact, there may be a good chance of selling at a significant premium sometime before this situation resolves itself.

Will any other short ETFs be affected?

There is a chance that other short ETFs such as UltraShort S&P 500 ProShares (AMEX:SDS - News) may have similar trouble if they face a sudden influx of assets necessitating a large number of new swap agreements. However, these funds are not as large as UltraShort Financials (in terms of assets under management), and their underlying indexes have only a 15%-20% stake in the financial shares that cannot be shorted. Thus the risk to a counterparty from entering into those swaps with ProShares is much smaller than on the financial indexes, so broker/dealers are much more likely to continue entering swap agreements on the broad market indexes. The market for these broad index swaps is also much more liquid, so ProShares would be able to find more potential counterparties than with the financial sector index swaps, where the firm represents a much larger portion of the market.

ETF Analyst Bradley Kay contributed to this article.

Oil Futures Hit $130 per Barrel

welcome hyperinflation, usd sell off, flight to quality. all major currencies are substantially higher against the dollar right now.

by CalculatedRisk

From MarketWatch: Crude futures set for biggest daily price leap ever

Crude futures leaped as much as $25 per barrel, or 24.3%, shortly before the New York close Monday, to tap a high of $130 per barrel.

the index ETFs have to take the funds received and put them into the market. So if you are shorting an Index like QQQQ you are in effect borrowing its shares and selling them into the market. In turn the Fund that runs the EFT has to sell an equivalent basket of stocks to track your trade. With the restriction on selling short financial stocks, they cannot do this and correctly track the respective index. as a result the ETF beta starts to approach zero.

options and futures are still far game, and not traded by most retail investors. take from that what you will.

I'm looking at the possibility of buying SKF ahead of the 2 week window when all the options will price in the lifting of the short ban and the can get back to business as usual.

What's to stop the Black Boxes from shorting index ETFs, options and futures and then buying back all the components back except those they want to short acccording to their proportional representation?

NY Times Makes a Funny

by CalculatedRisk

From David Herszenhorn at the NY Times: $700 Billion Is Sought for Wall Street in Massive Bailout

The ultimate price tag of the bailout is virtually impossible to know, in part because of the possibility that taxpayers could profit from the effort, especially if the market stabilizes and real estate prices rise.

emphasis added

I hope you laughed. I did. A little gallows humor.

And, yes the cost is still unknown, but there is no way that the taxpayers will profit. My initial estimate is that the direct costs of the Paulson plan will be $700 billion to taxpayers. That is about double the cost of the S&L crisis (compared to GDP).

Why $700 billion?

The plan only limits the Treasury to "$700,000,000,000 outstanding at any one time", so the total purchases can exceed $700 billion. In fact, every time the Treasury sells some securities, they will probably plow the net proceeds back into more troubled assets until the entire $700 billion is gone.

Think of a drunk gambler at a slot machine. He starts with $100 and slowly loses. Every now and then he wins some money, but he keeps putting the coins back into the slot until he has lost everything. That is how this plan will work.

Unless there is a dramatic changes, there will be no upside participation in the financial companies for taxpayers, and the taxpayers will recapitalize the banks by, in Krugman's words, "having taxpayers pay premium prices for lousy assets".

Note: I believe a Reverse Dutch Auction is inappropriate for these assets (it won't lower the price much). This is because these auctions only work when the sellers have very similar goods to sell. In this case, if the asset class is defined broadly, then the characteristics will vary too widely been assets, and the Treasury will just end up buying the worst available assets.

And, if the asset class is defined narrowly, there won't be enough sellers for a reverse Dutch Auction to work.

Krugman: Cash for Trash

by CalculatedRisk

Professor Krugman writes in the NY Times: Cash for Trash. A few excerpts:

How does this resolve the crisis?

Well, it might — might — break the vicious circle of deleveraging ... Even that isn’t clear ... And even if the vicious circle is limited, the financial system will still be crippled by inadequate capital.

Or rather, it will be crippled by inadequate capital unless the federal government hugely overpays for the assets it buys, giving financial firms — and their stockholders and executives — a giant windfall at taxpayer expense. Did I mention that I’m not happy with this plan?

emphasis added

I believe this is exactly the plan - to buy assets at premium prices and thereby recapitalize the banks. As I noted earlier, this will probably be successful in getting the banks to lend again, but that "success" would come at an astronomical cost to taxpayers. And there would probably be other unintended consequences.

The logic of the crisis seems to call for an intervention ... but ... the financial system needs more capital. And if the government is going to provide capital to financial firms, it should get what people who provide capital are entitled to — a share in ownership, so that all the gains if the rescue plan works don’t go to the people who made the mess in the first place.

The current plan is vague, opaque, has almost no oversight, puts the taxpayers at extreme risk and encourages future moral hazard.

A better plan would be transparent (all deals would be publicized), involve a share in ownership for the taxpayers, and have substantial oversight. We can do better.

ban on short selling. competitive with dilution. I think that financials are upset that they are trying to raise capital through the issuance of new shares and they are competing with short sellers for a bunch of bagholding buyers that are averaging down so they don't feel so wiped out. they probably begged the SEC to put the policy in place to pump up the shares, because retail shareholders will only loose so many shirts before they give up and go elsewhere with their money. think airline stocks and how terrible they have been to shareholders over the last 40 years.

I think this 2 week ban will no do much for stability, instead it will just add volatility to the market.

Bailout Plan Threat to Dollar ?

Posted by Barry Ritholtz on Monday, September 22, 2008 | 06:15 AM

Today's most noteworthy MSM piece is this Bloomberg article, titled. Dollar May Get `Crushed' as Traders Weigh Up Bailout.

Excerpt:

Treasury Secretary Henry Paulson's plan to end the rout in U.S. financial markets may derail the dollar's three-month rally as investors weigh the costs of the rescue.

The combination of spending $700 billion on soured mortgage-related assets and providing $400 billion to guarantee money-market mutual funds will boost U.S. borrowing as much as $1 trillion, according to Barclays Capital interest-rate strategist Michael Pond in New York. While the rescue may restore investor confidence to battered financial markets, traders will again focus on the twin budget and current-account deficits and negative real U.S. interest rates.

"As we get to the other side of this, the dollar will get crushed,'' said John Taylor, chairman of New York-based International Foreign Exchange Concepts Inc., the world's biggest currency hedge-fund firm, which manages about $15 billion. . .

"The downdraft on the dollar from the hit to the balance sheet of the U.S. government will dwarf the short-term gains from solving the banking crisis,'' said David Woo, London-based global head of foreign-exchange strategy at Barclays, the third- biggest currency trader, according to a 2008 survey by Euromoney Institutional Investor Plc.

Warning: Your currency may be smaller than it appears in the mirror . . .

Source:

Dollar May Get `Crushed' as Traders Weigh Up Bailout

Bo Nielsen and Anchalee Worrachate

Bloomberg, September 22, 2008

http://bloomberg.com/apps/news?pid=20601087&sid=arSYa87HCb9U&

G7 nations welcome U.S. bank bailout

Mon Sep 22, 2008 8:48am EDT

look on the bright side. at least its no a trillion dollars. ;-P

this is weak dollar inflate away the problems to boost the economy policy. while in the short term it is good as you get a recovery, you pay for it by getting slower growth rates went the economy does recover. look at the last recover post the 2001-02 recession. it was inflated away with weak dollar + inflation.

the problems are that policies that big business lured congress to institute to cap wage inflation means we won't get an interest rate spiral up, but expect a lot of mini recessions to come as more and more people get stuck in on the poor side as the middle class gets whittled away.

By James Mackenzie

PARIS (Reuters) - Group of Seven nations welcomed the $700 billion U.S. markets bailout plan on Monday but there was no sign that other governments saw any need to follow Washington in setting up rescue packages of their own.

"We will be in a telephone conference to consider and very probably express our support for the American plan," French Economy Minister Christine Lagarde told RMC radio in an interview, without giving more details.

U.S. Treasury Secretary Henry Paulson said on Sunday he was "aggressively" encouraging other countries to put in place similar schemes to the plan announced on Friday which sent global stock markets soaring.

The world's big central banks have already joined in a coordinated move with the U.S. Federal Reserve to pump hundreds of billions of dollars in extra funding into markets to prevent the world financial system from seizing up in a credit freeze.

But U.S. allies within the G7 club of wealthy nations appeared more guarded about the need to follow Washington's lead and set up funds to buy bad debts from struggling banks.

"At the moment, I don't think Japan needs to launch a program similar to that of the United States," Japanese Vice Finance Minister Kazuyuki Sugimoto told reporters in Tokyo, echoing similar comments from France, Britain, Germany and the European Union.

"The government thinks measures like those taken in the United States are not necessary (in Germany)," German government spokesman Ulrich Wilhelm told a regular news conference.

However contacts have been intense as government leaders try to come up with a unified response to a financial crisis widely seen as the worst since the 1930s.

French President Nicolas Sarkozy, whose country holds the rotating EU presidency is visiting the United States this week for a United Nations meeting and is expected to talk to U.S. officials about the crisis.

British Prime Minister Gordon Brown said last week he was in touch with Sarkozy about formulating a joint EU response and a government spokesman said on Britain would take "whatever action is necessary in the interest of financial stability".

European leaders have repeatedly said that their banks were better balanced than their U.S. counterparts and do not face the dramatic problems that led to the collapse of Lehman Brothers and the forced sale or rescue of other Wall Street institutions.

(Reporting by Paris, London, Tokyo, Berlin bureaus, editing by Mike Peacock)

© Thomson Reuters 2008 All rights reserved

Ameribank folds, twelfth closure this year

By John Letzing

Last update: 7:38 p.m. EDT Sept. 19, 2008

SAN FRANCISCO (MarketWatch) -- Northfork, West Virginia-based Ameribank Inc. has been closed, the Federal Deposit Insurance Corporation said late Friday, marking the 12th bank closure so far this year. Deposits at Ameribank's Ohio branches have been transferred to The Citizens Savings Bank, while Ameribank's Ohio branches will reopen Saturday as Citizens Bank branches, the FDIC said. Ameribank's West Virginia deposits have been transferred to Pioneer Community Bank, and Ameribank's West Virginia branches will reopen as Pioneer branches.

What's happened is way too big to have been orchestrated by agents outside of the system.

selling usd against the jpy and eur today. I think that there is a lost of trust in free markets and perception of future dilution of the dollar.

I think that a lot of funds are going to roll their shorts over to the options market, start writing calls on existing longs or buying puts.

so how long before the Fed bans option hedging strategies? treasuries spiked today. huge drops in price. good opportunity to buy something a little safer

so with the ban on short selling and 100bil in 1day repos from yesterday (due today) a global short squeeze is in play. did the fed transfer financial losses onto hedge funds? I don't think they thought their cunning plan all the way through.

a lot of hedge funds will implode because of this and they will be forced to trim their losses and unwind their winning assets to pay off their clients.

its never good when the rules of the game get changed, and especially without preparation. I'm not an avid short seller, its like saying you are a communist in these markets, but its the way they went about it.

this will send a lot of shorts in to overvalued positions, and buyer greed will keep a lot of people holding their existing positions, making the markets ripe for selling in 2 weeks.

I'm also pointing to yields on treasuries, spiking they way they did. if enough market manipulation occurs like this then interest rates are going much higher. that will hurt more underperforming banks.

Terror Attack on US Financials? Details of SEC Short Ban

Posted by Barry Ritholtz on Friday, September 19, 2008 | 05:54 AM

in Bailouts | Markets | Psychology/Sentiment | Short Selling | Trading

Last night, we discussed the absurdity of banning all short sales. The details of the SEC action have been released (see below). The specifics are a "temporary halt in short selling in 799 financial institutions" until October 2nd.

I have been trying to contextualize this, and I keep coming back to what seemed like a wild theory yesterday that seems a whole lot less wild today. During the day, I had an interesting phone conversation with Joe Besecker of Emerald Asset Management. (We used to do schtick together on Power Lunch, and made for an amusing financial comedy team).

But Joe is a good money manager, a great stock picker, and a thoughtful guy. He raised an intriguing issue: None of the many hedgies he knew were pressing their bets recently. The bear raids on the banks and brokers were NOT a case of piling on by US based hedge funds. And from what he was seeing and hearing about in terms of order flow, the vast majority of the financial short selling the past week or so were being done overseas. It appears that the lion's share of shorting was coming out of overseas bourses such as London and Dubai.It may not be a coincidence that the financial short selling ban is both here and in London.

Then there is another coincidence: The huge increase in shorting of the financials occurred on the anniversary of 9/11. And on top of that, the same institutions attacked on 9/11/01 were the ones suffering in recent days.

Joe asked the question: Is anyone investigating whether this is a case of financial terrorism? He wanted to know if someone was at least looking into this question (Joe is buds with Jim Cramer, and mentioned it to him, who then omitted to cite in his column that this was Joe's theory, not his own).

Anyway, its an interesting theory, one that seemed kinda out there -- until last night's emergency action. Nothing else really explains the insanity of banning short sales -- except for Joe Besecker's questions. I can think of 3 possibilities: 1) Extreme idiocy and incompetance -- not unthinkable fom the gang that couldn't shoot striaght in DC thse days; 2) Following the impetuous Fannie/Freddie rescue, the timing of this certainly has political overtones. We will see if it gets extended a month from October 2nd to November 5th. 3) Some other factor, possibly finacial terrorism.

~~~

The grand irony of all this is that Naked Shorting has been very profitable for the big broker dealers, like Morgan And Goldman and Merrill and Lehman. They have looked the other way for years, and the SEC has been AWOL on this issue.

Short sales require a locate (shares to borrow) and then a subsequent delivery. It should take less than 3 days to deliver the borrowed shares, but instead, delivery is often delayed indefinitely. Failure to deliver leads to a margin charge, which can be as high as 9-15%.

If you want to know who to blame for the past 5 years of naked shorting, you only have two places to look: The Financial brokers themselves, and the nonfeasance of a feckless SEC.

Previously:

SEC: Ban All Short Selling (September 18, 2008)

http://bigpicture.typepad.com/comments/2008/09/sec-ban-all-sho.html

Fed better lower the Fund rate. They keep denying the bond market but it has been right for years running now. They should worry less about shorts and more about monetary policy and credit expansion contraction. Pretty soon the Fed will force you to buy 80% bonds 20% stocks all domestic. Lol.

Weekly Unemployment Claims Increase to 455,000

y CalculatedRisk

The DOL reports on weekly unemployment insurance claims:

In the week ending Sept. 13, the advance figure for seasonally adjusted initial claims was 455,000, an increase of 10,000 from the previous week's unrevised figure of 445,000. The 4-week moving average was 445,000, an increase of 5,000 from the previous week's unrevised average of 440,000.

Weekly Unemployment Claims Click on graph for larger image in new window.

The graph shows weekly claims. The four moving average is at 440,000.

This is a very high level, and indicates continued weakness in the labor market.

Central banks' $247 billion deal

Fed and others will pump billions into markets to soothe global financial upheaval.

its a crisis rules don't apply. make you wonder who has who against the ropes, the banks or the governments.

NEW YORK (CNN) -- Central banks around the world are pumping billions of dollars into money markets in a coordinated bid to calm global financial upheaval.

The package of up to $247 billion comes from the U.S. Federal Reserve, the European Central Bank, the Swiss National Bank, the Bank of England, the Bank of Canada and the Bank of Japan.

The injection of cash, which amounts to an expansion of up to $180 billion in available funds, is an effort to fuel economic activity.

With major financial and insurance institutions teetering, commercial banks have tightened their lending policies and increased interest rates, taking billions of dollars out of the economy.

Under the plan, the European Central Bank will inject up to $110 billion, the Swiss National Bank up to $27 billion, the Bank of Japan up to $60 billion, the Bank of England up to $40 billion and the Bank of Canada up to $10 billion.

"We're very grateful that the rescue package has been put on the table, because frankly the world's inter-bank markets are just simply not working in the manner that they should do," said David Buik of the BGC Partners brokerage firm in London.

"There's a wholesale mistrust ... amongst everybody." "It is essential that the central banks do stand there and massage the trust back into action," Buik said. "Without them, we would be in unbelievably uncontrollable turmoil."

Markets react

Britain's Lloyds TSB has announced a $22 billion deal to take over struggling HBOS, the UK's biggest mortgage lender. The government said it would facilitate the deal by overriding anti-monopoly regulations.

News of the central banks' plan cheered stock markets in Europe, with Britain's FTSE-100 up nearly 1.9%, Germany's DAX up nearly 1.5% and France's CAC 40 index up 1.6%. Russia's main stock exchanges suspended trading for a second consecutive day as the government tried to stop plunging in share prices and restore confidence.

Hong Kong's Hang Seng sank more than 7% at one point on Thursday, but closed flat as Asia shares staged an afternoon comeback to partially recoup losses.

On Wednesday, the Dow Jones industrials tumbled 449 points -- its second worst day of the year, but only the second worst day this week. The Nasdaq and the S&P also suffered drops of more than 4%.

The sell-off came in the wake of investment bank Lehman Brothers' (LEH, Fortune 500) bankruptcy, Merrill Lynch (MER, Fortune 500)'s sale to Bank of America (BAC, Fortune 500), and the U.S. government announcing an $85 billion plan to bail out insurance giant American International Group (AIG, Fortune 500) (AIG).

American financial investor Jim Rogers told CNN: "It's going to get worse. There are going to be more bankruptcies. There's going to be a big cleanout in the financial system."

"It's a complete collapse of confidence," Francis Lun, general manager of Fulbright Securities Ltd in Hong Kong, told The Associated Press. "The financial crisis in the U.S. is hitting everyone, everyone is running for cover. If the largest insurance company can fail, than no one is safe."

Bank deals

The remaining two Wall Street investment banks were hit particularly hard on Wednesday with Morgan Stanley (MS, Fortune 500) down 29% and Goldman Sachs (GS, Fortune 500) down 21%. (Full story)

British bank Barclays said it had reached a deal Wednesday to purchase key units of U.S. investment bank Lehman Brothers for $1.75 billion. The deal came just two days after Barclays walked away from talks to buy the beleaguered financial institution in its entirety.

Barclays will acquire Lehman's North American investment banking and capital markets businesses for $250 million in cash. Barclays will also purchase Lehman's New York headquarters and two data centers in New Jersey at their current market value estimated at $1.5 billion, a company statement said. To top of page

more reinflation, LIBOR and 90d tbills coming back up.

(CNN) -- Central banks around the world are pumping billions of dollars into money markets in a coordinated bid to calm global financial upheaval.

A South Korean investor watches a stock price board at the Korea Stock Exchange in Seoul.

A South Korean investor watches a stock price board at the Korea Stock Exchange in Seoul.

The package of up to $247 billion comes from the U.S. Federal Reserve, the European Central Bank, the Swiss National Bank, the Bank of England, the Bank of Canada and the Bank of Japan.

The injection of cash, which amounts to an expansion of up to $180 billion in available funds, is an effort to fuel economic activity.

With major financial and insurance institutions teetering, commercial banks have tightened their lending policies and increased interest rates, taking billions of dollars out of the economy.

Under the plan, the European Central Bank will inject up to $110 billion, the Swiss National Bank up to $27 billion, the Bank of Japan up to $60 billion, the Bank of England up to $40 billion and the Bank of Canada up to $10 billion.

"We're very grateful that the rescue package has been put on the table, because frankly the world's inter-bank markets are just simply not working in the manner that they should do," said David Buik of the BGC Partners brokerage firm in London. "There's a wholesale mistrust ... amongst everybody."

"It is essential that the central banks do stand there and massage the trust back into action," Buik said. "Without them, we would be in unbelievably uncontrollable turmoil."

Don't Miss

* Lloyds to take over UK mortgage lender HBOS

* Analysis: Banks vulnerable as 'rotten' foundations crumble

* CNN/Money: Fed rescues AIG with $85B loan

Britain's Lloyds TSB has announced a $22 billion deal to take over struggling HBOS, the UK's biggest mortgage lender. The government said it would facilitate the deal by overriding anti-monopoly regulations.

News of the central banks' plan cheered stock markets in Europe, with Britain's FTSE-100 up nearly 1.9 percent, Germany's DAX up nearly 1.5 percent and France's CAC 40 index up 1.6 percent.

Russia's main stock exchanges suspended trading for a second consecutive day as the government tried to stop plunging in share prices and restore confidence.

Hong Kong's Hang Seng sank more than 7 percent at one point on Thursday, but closed flat as Asia shares staged an afternoon comeback to partially recoup losses.

On Wednesday, the Dow Jones industrials tumbled 449 points -- its second worst day of the year, but only the second worst day this week. The Nasdaq and the S&P also suffered drops of more than 4 percent.

The sell-off came in the wake of investment bank Lehman Brothers' bankruptcy, Merrill Lynch's sale to Bank of America, and the U.S. government announcing an $85 billion plan to bail out insurance giant American International Group (AIG).

American financial investor Jim Rogers told CNN: "It's going to get worse. There are going to be more bankruptcies. There's going to be a big cleanout in the financial system." Video Watch Jim Rogers describe where he is investing his money »

"It's a complete collapse of confidence," Francis Lun, general manager of Fulbright Securities Ltd in Hong Kong, told The Associated Press. "The financial crisis in the U.S. is hitting everyone, everyone is running for cover. If the largest insurance company can fail, than no one is safe."

The remaining two Wall Street investment banks were hit particularly hard on Wednesday with Morgan Stanley down 29 percent and Goldman Sachs down 21 percent.

British bank Barclays said it had reached a deal Wednesday to purchase key units of U.S. investment bank Lehman Brothers for $1.75 billion.

The deal came just two days after Barclays walked away from talks to buy the beleaguered financial institution in its entirety.

advertisement

Barclays will acquire Lehman's North American investment banking and capital markets businesses for $250 million in cash.

Barclays will also purchase Lehman's New York headquarters and two data centers in New Jersey at their current market value estimated at $1.5 billion, a company statement said.

Conclusions and Implications

An application of the basic principles of most

money and banking textbooks to predict the

outcome of the 1992 reduction in reserve requirements

on transaction deposits would be in error

on certain points and misleading on others. First,

most textbooks would categorize the change as

an example of expansionary monetary policy.

However, as indicated in this article, short-term

interest rates generally rose after the announcement

rather than fell, as an expansion in monetary

policy would suggest. Thus, the predicted change

suggested by most textbooks in the area would be

in error. Second, textbook discussions would generally

ignore the impact that the change was likely

to have on bank stock prices. However, according

to statements of Federal Reserve officials, the 1992

reserve requirement change was intended to

improve the anticipated profitability of depository

institutions. Moreover, there is extensive evidence

indicating that prior changes in reserve requirements

were associated with subsequent changes

in bank stock returns. Textbook emphasis on monetary

policy considerations would have ignored

this impact altogether.

Finally, from a regulatory perspective, reserve

requirements are traditionally viewed as making

depository institutions relatively safer. Thus, a

reduction in these requirements should suggest

greater concerns about the financial health of such

institutions. Yet evidence in this article indicates

that the exact opposite occurred. Following the

1992 announcement of the reserve requirement

reduction, the TED spread—a traditional proxy for

the risk of deposit institutions—narrowed significantly

rather than increased. This outcome suggests

to us that financial markets did not view the

change as increasing the riskiness of depository

institutions, as tradition might suggest.

This article argues that reserve requirement

ratio changes should not be viewed simply as a tool

for monetary policy or as a tool used to directly

alter the liquidity of financial institutions. This view

raises the question, What is the purpose of the

reserve requirement ratio? We believe that the

value of reserve requirements, as a source of liquidity

or a tool of monetary policy, is indeed recognized

today to be less than previously thought by many

central banks. As evidence in support of this view,

some central banks—such as those in Canada,

Great Britain, and New Zealand—have recently

eliminated cash reserve requirements altogether.5

Even in the United States, the Federal Reserve has

recently allowed depository institutions to reduce

the cost of reserve requirements by sweeping

reservable accounts into nonreservable accounts.6

Thus, one could argue that reserve requirements

have effectively been reduced in the United States.7

http://www.frbatlanta.org/filelegacydocs/erq402_hein.pdf

don't know. crystal ball broken. more things from funny web domain names:

http://www.nakedcapitalism.com/2007/12/credit-crunch-charts.html

http://peltiertech.com/WordPress/2008/05/30/magazine-quality-chart-economist/

http://www.financialarmageddon.com/2007/12/off-the-charts.html?no_prefetch=1

your fast with that. so what are we at a 1987 market environment? 1985-1988 was a commodity run and after the spread hit near 300bps in 1987 with the stock crash gold fell for years.

let's see if this helps

http://krugman.blogs.nytimes.com/2008/03/12/mission-not-accomplished-not-yet-anyway/

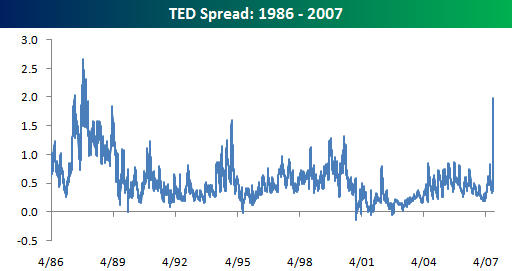

TED spread is the difference in yields between inter-bank and U.S. Government loans.

Initially, the TED spread was the difference between the interest rate for the three month U.S. Treasuries contract and three month Eurodollars contract as represented by the London Inter Bank Offered Rate (LIBOR). However, since the Chicago Mercantile Exchange dropped the T-bill futures, the TED spread is now calculated as the difference between the three month T-bill interest rate and three month LIBOR. The TED spread is a measure of liquidity and shows the degree to which banks are willing to lend money to one another.

The TED spread can be used as an indicator of credit risk. This is because U.S. T-bills are considered risk free while the LIBOR rate reflects the credit risk of lending to commercial banks. As the TED spread increases, the risk of default (also known as counterparty risk) is considered to be increasing, and investors will have a preference for safe investments. As the spread decreases, the risk of default is considered to be decreasing.[1]

The name originates from the initialism of "T-Bill" and "ED"—the ticker symbol for the Eurodollar futures contract. The size of the spread is usually denominated in basis points (bps), e.g. when T-Bills trade at 5.10% and ED trades at 5.50%, the TED spread is said to trade at 40bps. The value of the TED spread fluctuates over time but is often between 10 and 50 basis points (0.1% and 0.5%). A rising TED spread often foretells a downturn in the U.S. stock market as liquidity is withdrawn.

During 2007, the credit crunch, which many believe was caused by the U.S. subprime mortgage securities meltdown, ballooned the TED spread to a region of 150-200bps, and it reached a high of 250bps at the end of the year. On September 17, 2008, the TED spread closed at 302bps.

http://en.wikipedia.org/wiki/TED_spread

chart updates late but its 300 bps now highest in 5 years as far as I can tell. Still digging.

You can see 90 day tbills are worst ever. this is a major credit recession. lot of money is getting wiped out. if it stands to reason we should be months away from a bottom. might require some more selling off, but we are close. I think WB and WM need to get resolved first.

Libor jump, TED spread show extent of credit crisis

5:37p ET September 17, 2008 (MarketWatch)

SAN FRANCISCO (MarketWatch) -- A closely watched measure of global borrowing costs made its biggest jump in nine years Wednesday and another lending risk gauge rose to a level not seen since Black Monday in October of 1987, as banks grew increasingly wary to lend to each other and sell-shocked investors sought refuge in safe-haven short-term Treasury bills.

Three-month Libor in U.S. dollars jumped 19 basis points to 3.0625% -- the biggest jump since September 1999. The London Interbank Offered Rate, known as the Libor, measures the interest rate at which banks are willing to lend to each other overnight or for longer periods.

"The Libor rise is simply the result of continued concern over the health of the banking system. Banks are demanding higher rates to lend to each other. In fact, the term Libor markets have effectively seized up with very little trading happening," said Joe Burke, fixed income market maker at Interactive Brokers Group.

According to some estimates, loans and derivative contracts totaling roughly $150 trillion -- more than $20,000 for every person on Earth -- are indexed or tied to Libor in some way.

As a result, big changes in the Libor rate have major global implications for the cost of borrowing.

The financial sector was thrown into turmoil in recent days, as the bankruptcy of Wall Street icon Lehman Brothers was followed a few days later by news overnight that the federal government effectively took control of American International Group, receiving a 79.9% stake in the company. AIG's $85 billion loan from the Federal Reserve must be repaid over two years at an interest rate of 8.5 percentage points over the Libor rate. See full story.

Overnight rate down, but TED spread up

The bank-to-bank cost of borrowing U.S. dollars overnight fell 1.4% to 5.03% Wednesday, according to the British Bankers Association.

On Tuesday, the overnight rate hit a seven-year high of 6.4375%, more than doubling from Monday in what was reportedly the biggest jump on record.

"Money markets are still volatile but the pressure has eased since yesterday," the BBA said on its Web site.

But other measures showed an increase in pressure.

The so-called TED spread widened to 302 basis points Wednesday, said Burke.

That's a few ticks higher than it was on the day of the Oct. 20, 1987 stock market collapse, when it rose as high as 300 basis points.

The TED spread is the difference between what the Treasury pays to borrow for three months and the amount banks charge each other for loans, measured by the spread between the interest rate on a three-month U.S. Treasury bill and the three-month Libor rate.

"Prior to the crisis, normal is below 25 basis points for the TED spread," wrote Marc Chandler, head of global currency strategy for Brown Brothers Harriman, in a note to clients Wednesday.

On Wednesday, rates on three-month bills, among the most popular assets for investors seeking higher quality, plunged to 0.11%, the lowest on record. See Bond Report.

The Libor rise, coupled with "the flight to quality in Treasuries has resulted in a TED spread that is roughly 100 basis points higher than it was after the Bear Stearns collapse in March," Burke said.

"The interesting thing is that there is no thought that the weaker players have been flushed out and that things will normalize. The mind set is clearly one of 'which bank is next?'" he added.

Stock market investors apparently asked the same question. Shares of Morgan Stanley plunged 24.2 % Wednesday after it pre-announced earnings and investors reacted to a speculation the company may be compelled to hunt for a suitor if the stock continues to fall. See full story.

CNBC.com reported Morgan was forced to announce quarterly results early after spreads on its credit default swaps rose sharply on Tuesday. The bank's CDS spreads continued to rise Wednesday.

CDS are a common type of derivative contract that pay out in the event of default. When the difference, or spread, between rates on these contracts and rates on U.S. Treasury bonds increases, that suggests investors are willing to pay more to protect against defaults.

At midday Eastern time, Morgan Stanley's CDS spread was up 182.5 basis points and Goldman Sachs' was up 92.5 basis points, according to Credit Default Research. By late afternoon, the spreads had widened even further.

CDS spreads on UBS AG, Merrill Lynch and Wachovia Corp. were all up more than 50 basis points at midday, the Credit Default Research data showed.

The cost of insuring against a U.S. Treasury default was also higher.

The Treasury Department announced Wednesday that it would provide cash to the Federal Reserve through a new auction program to fund the central bank's operations to provide liquidity to financial markets. See full story.

"We were bemused last week when we say the price of insuring U.S. Treasurys, via credit default swaps, rose to 18 basis points, a little above the cost of insuring Japanese government bonds and more than twice German bunds," said Brown Brothers Harriman's Chandler.

"Today, following the AIG development, the cost of insuring Treasurys has risen to about 30 basis points, according to some indicative prices," he said.

Treasury 3-Month Bill Rates Drop to Lowest Since at Least 1954

By Sandra Hernandez

Sept. 17 (Bloomberg) -- U.S. Treasury three-month bill rates dropped to the lowest since at least 1954 as a loss of confidence in credit markets prompted investors to abandon higher-yielding assets for the safety of the shortest-term government securities.

Investors pushed the rate as low as 0.233 percent on concern that credit market losses will widen after the bankruptcy of Lehman Brothers Holdings Inc. and the federal takeover of American International Group Inc. The rate banks charge each other for short-term loans relative to Treasury bills rose to the highest since the stock market crash of 1987.

``People are extremely cautious with respect to who they're lending money to at the moment,'' said Richard Bryant, a Treasury trader at Citigroup Global Markets Inc., one of the primary dealers that trade government securities with the Federal Reserve. ``They're willing to buy very short-dated Treasury instruments and forgo returns and in some cases pay for the privilege of knowing their money is safe.''

Three-month bill rates fell 32 basis points to 0.38 percent at 10:26 a.m. in New York. They had dropped to 0.3867 percent on March 20, after the Fed and Treasury engineered the takeover of Bear Stearns Cos.

Bills pared their gains after the Treasury said it will sell $40 billion in 35-day securities through a series of special auctions at the request of the Fed so the central bank can expand its balance sheet after the takeover of AIG. The securities will be similar to cash management bills.

Money Markets

Reserve Primary Fund, the oldest U.S. money-market fund, yesterday became the first in 14 years to expose investors to losses after writing off $785 million of debt issued by Lehman.

Shareholders in Reserve Primary Fund pulled more than 60 percent of the fund's $64.8 billion in assets in the two days since Lehman folded. Losses on the securities firm's debt forced the fund to break the buck, meaning its net asset value fell below the $1 a share price paid by investors.

``The panic going round the money market world is what they've been investing in is not as safe as they thought it would be,'' said Dominic Konstam, the head of interest-rate strategy in New York at Credit Suisse Securities USA LLC, another primary dealer. ``If the banks don't want to lend to each other they don't want to lend to the banks. That means where else are they going to put their money -- they're going to put it in T-bills for safety.''

Borrowing in Dollars

The cost of borrowing in dollars for three months jumped the most since 1999 as banks hoard cash. The London interbank offered rate, or Libor, rose 19 basis points to 3.06 percent, the British Bankers' Association said today. The increase is the biggest since Sept. 29, 1999, during the run-up to the new millennium.

The difference between what the U.S. government and banks pay to borrow in dollars for three months, the so-called TED spread, widened to the most since the October 1987 stock-market crash as bill rates tumbled. The spread widened as much as 64 basis points to 283 basis points. It was as low as 75 basis points on May 27.

``I'm extremely worried about what is happening to the money market mutual funds that have announced they've broken the buck,'' said Ajay Rajadhyaksha, head of fixed income strategy at Barclays Capital Inc. in New York. ``That unfortunately can spiral in the sense that it makes it more difficult for all companies to raise short term money because the money-market funds tend to be buyers of short term debt.''

`Under the Carpet'

Treasuries had declined earlier as the Fed's $85 billion loan to AIG allayed concern that a collapse of the insurer would destabilize the financial system. Barclays Plc, the U.K.'s third-biggest bank, will acquire Lehman's North American investment-banking business for $1.75 billion, three days after abandoning plans to buy the entire firm.

Central banks around the world pumped more than $280 billion into the financial system this week as they sought to ease a credit-market seizure. The Fed made the loan to AIG, the biggest U.S. insurer by assets, in exchange for control.

The AIG rescue ``smacks of sweeping the problem under the carpet rather than solving it in a structural sense,'' said Padhraic Garvey, head of investment-grade debt strategy at ING Bank NV in Amsterdam, in a note to clients. ``At least the Lehman saga has gone some way toward a clean-up. We are still in the midst of the flight-to-quality environment.''

HBOS Plc, the U.K.'s biggest mortgage lender, slid as much as 52 percent today on speculation it may not have access to funding. The shares rebounded, surging as much as 18 percent, as HBOS said it's in ``advanced'' takeover talks with Lloyds TSB Group Plc.

To contact the reporters on this story: Sandra Hernandez in New York at shernandez4@bloomberg.net; Agnes Lovasz in London at alovasz@bloomberg.net

Last Updated: September 17, 2008 10:29 EDT

TED Spread hit 290bp. highest in the last 4 years. I head that t bills reversed today. people paying interest to buy tbills. yes, like in Japan back in the 90s. you pay interest to save money, get interest to borrow money. deflation.

bwwwwaahahahahahaa... i got nothing.

Treasury Said to Be Considering AIG Conservatorship (Update1)

By Craig Torres and Elizabeth Hester

Sept. 16 (Bloomberg) -- The U.S. Treasury is considering taking over American International Group Inc. under a conservatorship as one option to address the insurer's crisis, according to two people briefed on the discussions.

Executives from AIG, bankers and Treasury and Federal Reserve officials are meeting today on the company's situation at the New York Fed. A number of options are under being discussed to fill a shortfall of $75 billion to $100 billion in funding, one of the people said. The talks are continuing, he said.

Goldman Sachs Group Inc. and JPMorgan Chase & Co., which have been leading efforts to find a private-sector solution, informed the Fed that such an effort would be difficult, the person said. Under another option, the Fed would extend a loan to New York-based AIG, according to a person informed of the matter.

Treasury Secretary Henry Paulson earlier this month seized Fannie Mae and Freddie Mac and put them into conservatorships, where officials will oversee the firms and aim to protect their assets.

Treasury spokeswoman Michele Davis declined to comment. David Neustadt, a spokesman for New York State Insurance Superintendent Eric Dinallo, had no immediate comment.

To contact the reporters on this story: Elizabeth Hester in New York at ehester@bloomberg.net; Craig Torres in Washington at ctorres3@bloomberg.net.

Bond market was right, traders wrong, not rate drop...

Press Release

Federal Reserve Press Release

Release Date: September 16, 2008

For immediate release

The Federal Open Market Committee decided today to keep its target for the federal funds rate at 2 percent.

Strains in financial markets have increased significantly and labor markets have weakened further. Economic growth appears to have slowed recently, partly reflecting a softening of household spending. Tight credit conditions, the ongoing housing contraction, and some slowing in export growth are likely to weigh on economic growth over the next few quarters. Over time, the substantial easing of monetary policy, combined with ongoing measures to foster market liquidity, should help to promote moderate economic growth.

Inflation has been high, spurred by the earlier increases in the prices of energy and some other commodities. The Committee expects inflation to moderate later this year and next year, but the inflation outlook remains highly uncertain.

The downside risks to growth and the upside risks to inflation are both of significant concern to the Committee. The Committee will monitor economic and financial developments carefully and will act as needed to promote sustainable economic growth and price stability.

Voting for the FOMC monetary policy action were: Ben S. Bernanke, Chairman; Christine M. Cumming; Elizabeth A. Duke; Richard W. Fisher; Donald L. Kohn; Randall S. Kroszner; Sandra Pianalto; Charles I. Plosser; Gary H. Stern; and Kevin M. Warsh. Ms. Cumming voted as the alternate for Timothy F. Geithner.

WSJ says Bank of America overpaid for Merrill Lynch

all stock deal between BAC and MER means shareholder dilution. They don't have the cash. This financial storm in no wheres near done yet.

Posted Sep 16th 2008 7:45AM by Zac Bissonnette

Filed under: Deals, Bank of America (BAC), Merrill Lynch (MER)

The Wall Street Journal's 'Heard on the Street' column (subscription required) thinks that Bank of America (NYSE: BAC) is overpaying for Merrill Lynch (NYSE: MER).

But here's where it gets interesting: because it's an all-stock deal scheduled to close in the first quarter of 2009, the more bearish Wall Street is on the deal, the less Bank of America will pay! When it was first announced, the deal was thought to pay Merrill shareholders a significant premium. But by the end of trading on Monday, shares of Merrill were trading at $17.06, essentially flat for the day and just 46 cents above the stock's lowest point since 1996. That's because Bank of America's stock tanked about 20% on the day.

But the Journal points out that the deal was agreed to in haste, and adds that "Mr. Lewis has the business he wanted: Merrill's private-client operation, which Sanford Bernstein estimates is valued at $26.7 billion. But assume Merrill's BlackRock stake is valued at $14 billion, and BofA's original price implied almost $10 billion for the risky investment bank. Given the precarious environment, Mr. Lewis has paid too generous a price."

There are also questions about how achievable Bank of America's projections of cost savings are.

Much of how the acquisition pans out will likely depend on as yet unpredictable macroeconomic factors but, for now, I'll cast my lot with the skeptics. Big acquisitions rarely pan out, and estimates of synergy are nearly always too optimistic.

Tags: BAC, Bank of America, BankOfAmerica, MER, Merrill Lynch, MerrillLynch

Fannie, Freddie Takeover Diminishes Financing Options for Banks

Dead banks walking. Reminiscent of the start of the Japanese Depression.

By Caroline Salas

Enlarge Image/Details

Sept. 15 (Bloomberg) -- Treasury Secretary Henry Paulson's decision to seize Fannie Mae and Freddie Mac may choke off the biggest source of funding for financial companies suffering from the collapse of the subprime mortgage market.

When Paulson took control of Fannie and Freddie on Sept. 7, he scrapped dividends on the preferred stock of the government- sponsored enterprises. He also said the U.S. would buy as much as $200 billion of new securities that would rank ahead of existing issues.

The plan sent shares tumbling on concern it will become a model for financial institutions reeling from $511 billion of writedowns and credit losses since the start of 2007. Financial companies raised $361 billion in capital to replenish their balance sheets, data compiled by Bloomberg show. Banks with the 10 biggest writedowns sold at least $85 billion of preferred securities, or 47 percent of the total, the data show.

Paulson's ``decision has been devastating to the market,' said Marilyn Cohen, President of Envision Capital Management in Los Angeles, which oversees $200 million in fixed-income assets. ``We all thought they would never help exacerbate the banking crisis and that's exactly what they did.'

Cohen, whose clients own Fannie and Freddie preferred shares that are now ``about the cost of a cappuccino,' is ``absolutely not' interested in buying more of the securities from financial institutions, she said.

Prices Tumble

Concern about financial companies' ability to raise capital escalated after Lehman Brothers Holdings Inc. today said it will file for bankruptcy protection and Merrill Lynch & Co. agreed to be bought by Bank of America Corp. American International Group Inc. the insurer struggling to avoid credit downgrades, is seeking a $40 billion bridge loan from the Federal Reserve as it tries to sell assets, the New York Times reported.

Preferred stock ranks behind bonds and ahead of common shares in a company's capital structure. Unlike common stock, the securities pay either a fixed- or floating-rate dividend, and can have a set maturity or no due date.

As investors abandoned preferred stocks, prices of the fixed-rate portion of the market fell an average of 13 cents last week to an average 67.1 cents on the dollar, the lowest in at least a decade, according to Merrill Lynch index data. That pushed the average yield to 10.8 percent from 8.8 percent on Sept. 5 and 7.9 percent at the end of last year.

Paulson said his rescue of Fannie and Freddie shouldn't have negative implications for the wider market. Fannie said last week it will pay third-quarter dividends on the securities.

Not a `Proxy'

``Preferred stock investors should recognize that the GSEs are unlike any other financial institutions and consequently GSE preferred stocks are not a good proxy for financial institution preferred stock more broadly,' Paulson said in a Sept. 7 statement. ``The broader market for preferred stock issuance should continue to remain available for well-capitalized institutions.'

The Treasury needed to bail out Fannie and Freddie because they own or guarantee more than $12 trillion of mortgages, or about half the U.S. home-loan market. The takeover came four months after the government pressed Fannie to raise $4.25 billion with preferred stock after mortgage-market losses. Freddie agreed to raise $5.5 billion, though it never did.

Washington-based Fannie's preferred stock plunged more than 75 percent last week, and securities sold by McLean, Virginia- based Freddie tumbled 85 percent, New York-based Merrill's index data show. Of the top 50 issuers in the index, 46 fell.

`Hands Scorched'

Preferred stock has been the main source of new money for banks after the collapse of the subprime mortgage market last year caused credit markets to seize up.

Of the $49.1 billion raised by New York-based Citigroup Inc., about $40.6 billion was in preferred securities, Bloomberg data show. Bank of America, in Charlotte, North Carolina, sold $16.7 billion of preferreds, or 77 percent of its total new money.

New York-based JPMorgan Chase & Co., Merrill, and Lehman issued the securities, as did London-based Barclays Plc.

``Buyers have gotten their hands scorched,' said Michael Donelan, who manages $2 billion of bonds at Ryan Labs Inc., a money management and research firm in New York. He isn't interested in buying preferreds from a financial institution. ``The demand for capital is going to be so huge. We're not going to buy something and then' watch it fall, he said.

Lehman Collateral

Lehman's $2 billion offering in June wasn't enough to prevent the 158-year-old firm from filing for bankruptcy. Its common shares plummeted 94 percent on the New York Stock Exchange this year through Sept. 12. Its fixed-rate preferred lost 47 percent.

Moody's Investors Service said last week it may lower the company's credit ratings. Lehman said a downgrade would force it to come up with at least $4.4 billion in collateral postings. Mark Lane, a spokesman for Lehman, declined to comment.

Washington Mutual Inc., facing as much as $19 billion in bad home loans, was slammed by a 36 percent drop in its common stock last week. Fitch Ratings cut WaMu's debt to BBB- from BBB, citing a lack of ``flexibility' to add capital. Brad Russell, a spokesman for Seattle-based WaMu, declined to comment.

The company said in a Sept. 11 statement that it is significantly above the ``well capitalized' regulatory designation.

Wachovia Corp.'s fixed-rate preferred shares tumbled 24 percent and AIG lost 39 percent last week. Wachovia reported a record loss of $9.11 billion for the second-quarter, more than it ever earned in a year. AIG posted three quarterly losses totaling $18.5 billion.

Elise Wilkinson, a spokeswoman for Charlotte-based Wachovia, didn't return a phone call seeking comment. Peter Tulupman, a spokesman for AIG of New York, declined to comment.

Preferred stock offerings are ``just not in the cards for anyone given the current state of the market,' said Scott Sprinzen, an analyst at Standard & Poor's in New York who covers finance companies. ``The economics are not at all attractive.'

To contact the reporter on this story: Caroline Salas in New York at csalas1@bloomberg.net

Last Updated: September 15, 2008 02:32 EDT

S&P Lowers WaMu Credit Rating to Junk

by CalculatedRisk

From Bloomberg: WaMu Rating Lowered to Junk by S&P on Mortgage Losses (hat tip Justin)

Washington Mutual Inc. ... had its credit rating cut to junk by Standard & Poor's because of the deteriorating housing market.

...

``Increasing market turmoil and the related impact from managing its concentrated mortgage franchise in this troubled housing and credit cycle led to the downgrade,'' S&P wrote.

And the beat goes on ...

LEH selling NYX positions. Probably reason for fallout in commodities.

Next on deck for a blow up Wachovia, Wamu.

CDS swaps haves reached their highest since the BSC bailout.

btw - sliced some fingers open this weekend. typing with one hand. forgive my slow typing.

JPM default swaps jumped to 190bps, AIG wants Fed help and will get denied, futures down on S&P -47. Fed may cut by .25 tomorrow, maybe before open today even. MER going off and downgrading everyone except BAC. lol

But not one of these financials are looking at offers from private funds because it means losing control of their companies. And they aren't going to the Fed for emergency funds. They are begging for free fed money, taxpayer money. Greed and Pride are the down falls of these companies.

Wow Dollar -300 pips vs Yen at open. Major gap down in currency market. That is a lot of money pulled out of US markets.

It did hit the previous low back in Sept 4th. So will that be support for a run up? Expect the Euro Gold and probably Oil to move as well.

Probably on news that Barclays walked from the Lehman table.

http://ap.google.com/article/ALeqM5j12hiaDX0-3jvsfNj247sUyBiqHgD936LAF81

LONDON (AP) — Barclays PLC has pulled out of talks to buy parts of Lehman Brothers Holdings Inc., according to a person at the British bank with knowledge of the negotiations. The move complicates efforts to find a buyer for Lehman and save it from collapse.

The person, who spoke on condition of anonymity, citing company policy, said the decision was "very unlikely" to change.

The person said that while Lehman was attractive, the investment bank did not meet what he described as Barclay's stringent requirements.

U.S. government officials and top Wall Street bankers are trying to sell Lehman and avert a collapse that could severely disrupt global markets.

This aprt is my favorite...

"Upon the default of the counterparty, [traded] derivatives would be immediately repriced, with spreads widening dramatically," said the Barclays report.

One side would suddenly be trapped with staggering losses on their books. Yet the winners would be unable to collect their prize from the insolvent bank in the middle. It would take years to unravel all the claims in court.

It makes you wonder why they took these bets in the first place. I say bets because they are not investments. They are a bastardized form of hedging that goes well beyond speculation.