News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

10 huge reasons why you need to radar AMBS!!!!!

1. AMBS acquired an exclusive option to license the LymPro Alzheimer's Diagnostic Blood Test from Memory Dx, LLC (MDx), formerly known as Provista Life Sciences, LLC

2. AMBS had Positive animal proof-of concept data for MANF in the multi-billion dollar Myocardial Infarction market;

3. AMBS Secured the license for the NuroPro Parkinson's diagnostic blood test;

4. AMBS Successfully concluded its research collaboration with Banyan Biomarkers, showing positive proof-of concept data for MANF in Traumatic Brain Injury.

5. AMBS anticipates announcing interim results from on-going delivery experiments by the end of October.

6. AMBS has a Parkinson’s disease program, comprised of an early detection diagnostic blood test and a disease-modifying protein drug candidate. AMBS owns the rights to a potential cure for Parkinson’s—a promising therapeutic protein known as MANF that prevents a type of cell death called apoptosis. That program is currently funded by a research grant from the Michael J. Fox Foundation for Parkinson’s research...

7. AMBS also owns the license to a groundbreaking diagnostic platform called NuroPro for Parkinson’s that allows neurologists to accurately diagnose and track the progression of Parkinson’s disease in patients. The Companies believe that Amarantus’ NuroPro test for Parkinson’s disease could be on market in certain regions as early as 2013.

8. Over $30MM has already been invested in the research and development of AMBS product candidates from biopharmaceutical companies, non-profit organizations, academic researchers and government agencies, including the National Institutes of Health.

9. According to a2011 report by Visiongain, the market for Parkinson's disease drugs could grow to a value of $3.75BB by 2015; AMBS is working on a candidate in the disease-modifying drug class which, if successful, could grab significant market share as well as substantially grow the overall Parkinson’s drug market. There are currently no diagnostic tests available for Parkinson’s disease, thus making AMBS test a first of its kind product capable of gaining a market leading position.

10. AMBS announced Drug Test Results & the publication of positive, peer-reviewed efficacy data for MANF in an animal model of myocardial infarction. The results were published in The Journal of Biological Chemistry (JBC) by the Glembotski Lab at the San Diego State University's (SDSU) Department of Biology and the SDSU Heart Institute. The research paper entitled "Mesencephalic astrocyte-derived neurotrophic factor (MANF) protects the heart from Ischemic damage and is selectively secreted upon ER calcium depletion" reports a ~44% reduction in infarct zone size in MANF-treated mice when compared with controls. View results at http://www.jbc.org/content/early/2012/05/29/jbc.M112.356345.short

ICOA continues to follow through with it's new Business Plan with a barrage of Pr's in the Month of July 2012!

IENT is a Lottery Ticket and when Wild Bill gets around to doing the financials everyone will realize what a gem this company is. Until then, buy a ticket and wait.

I came across this great website for stock market videos.

http://www.stock-tv.com

I second that notion

Etrade does a good job w pennies as it has Etrade Pro. Thumbs up imo.

Thanks Cube, I agree Etrade also has some pretty clean trading platforms as well. For day trading though I always use the sterling platform, but I can't trade penny stocks with it, and even if I could it wouldn't be worth it with commission at 0.005 per share per trade.

I like Etrade and they do a good job with the L2 and mobile pro.

Ameritrade is an awful broker.. Their chart feeds/ data go out EVERY day.. EOM

good morning my friend :) watchem close!

Good morning Awaken, got them on my watch list!

GM brother. GDSI VHGI BUCS VRCV radar

Good morning!

>>>IENT is a Buy based on TA alone according to barcharts.com

http://barchart.com/quotes/stocks/IENT

Thanks DOllarland

AlumiFuel Power Executive, David Cade, Exclusive Interview on Stock Traders Talk Radio

Early production stage hydrogen generation company AlumiFuel Power Corporation (OTCBB: AFPW) (the "Company") will be a featured guest in an exclusive live interview Sunday at 7pm EDT.

The STT Radio Exclusive Interview will be held on Sunday, April 1, 2012 at 7:00pm EDT, and can be heard live at the IHub Auditorium http://www.investorshub.advfn.com/boards/auditorium.aspx. Additionally, the show can be heard live directly from the STT Live Page at http://www.stocktraderstalk.com/live (refresh when show starts) or at http://www.blogtalkradio.com/stocktraderstalk. You may also call into the show to listen at (347) 215-7181 and follow the prompts to listen live. An archived recorded version of the interview can be found and heard on the homepage of STT at http://www.stocktraderstalk.com indefinitely following the live interview.

This interview will discuss the Company's hydrogen generation technology and business plans.

About Stock Traders Talk

Stock Traders Talk Radio is a centralized portal for investors. We specialize in LIVE radio interviews and believe that when a CEO has the ability to demonstrate their passion, and talking points about their company it serves as the ultimate delivery platform. Press Releases have value; however, they lack the ability for a CEO to connect with shareholders and potential shareholders.

Stock Traders Talk Radio is a comprehensive uncensored approach to analyzing OTC stocks, with additional focuses on penny stocks in play, world markets, SEC and Regulations and interesting ROI opportunities.

Listeners can interact with the show via our main chat room at http://www.stocktraderstalk.com

About AlumiFuel Power Corporation

AlumiFuel Power Corporation, operating through its subsidiaries, is an early production stage alternative energy company that generates hydrogen gas and steam/heat through the chemical reaction of aluminum, water, and proprietary additives. This technology is ideally suited for multiple applications requiring on-site, on-demand fuel sources, serving National Security and commercial customers. The Company's hydrogen feeds fuel cells for portable and back-up power; fills inflatable devices such as weather balloons; can replace costly, hard-to-handle and high pressure K-Cylinders; and provides fuel for flameless heater applications. Its hydrogen/heat output is also being designed and developed to drive fuel cell-based and turbine-based undersea propulsion systems and auxiliary power systems. The Company has significant differentiators in performance, adaptability, safety and cost-effectiveness in its target market applications, with no external power required and no toxic chemicals or by-products.

Safe Harbor for Forward-looking Statements

This news release may contain forward-looking statements that are made pursuant to the "safe harbor" provisions of the Private Securities Litigation Reform Act of 1995. While these statements are made to convey to the public the company's progress, business opportunities and growth prospects, they are based on management's current beliefs and assumptions as to future events. However, since the company's operations and business prospects are always subject to risk and uncertainties, the forward-looking events and circumstances discussed in this news release might not occur, and actual results could differ materially from those described, anticipated or implied. For a more complete discussion of such risks and uncertainties, please refer to the company's filings with the Securities and Exchange Commission.

http://ih.advfn.com/p.php?pid=nmona&article=51847693&symbol=AFPW

Good morning bro!

happy friday!

Here's a summary - lots of great info.

http://investorshub.advfn.com/boards/read_msg.aspx?message_id=73759781

I do know that there is a seller that is just about done (less than 25k shares left to sell), and then much smoother sailing. From the chat, it sounds like we should see some news by next week.

I missed it, how did it go?

Good morning!

Live Chat with SMKY's CEO is scheduled for Tuesday night.

Go to http://www.smkycorp.com for details.

Hot Stocks and Upcoming Moverz: $AGCZ, $IENT Astonishing DD-Extremely Undervalued *Pot. Long Term Hold* http://tinyurl.com/6rp4f5o, $CDYY, $DEYU

BullQuake Tweet

https://twitter.com/#!/BullQuake/status/184242234982543360

Cut in half and it's all algorithms and bots.

FUTURES DOW +35.00 S&P+ 3.45 NQ + 9.40

NeuroMetrix initiated with a Buy at Dawson James; target $3 (0.78 ) : Dawson James initiates NURO with a Buy and price target of $3 saying the co has completed an impressive turnaround over the past several years, introducing new products with more potentially to come in the near future, re-structuring its legacy business to optimize cash flow, "and bolstering its balance sheet to provide financial resources for future growth". Firm says that perhaps due to its small market capitalization as well as a lack of understanding of the Company's recent turnaround, NURO shares have still underperformed the market as a whole this year and currently trade at a discount to its industry peer group in the medical device market, based on several valuation metrics.

Post Unavailable

ETF Spotlight: PowerShares Buyback Achievers ETF

By JT

Buybacks are back in play. Looking to boost shareholder value, a number of companies have announced share repurchase agreements to buy back shares on the open market. Betting on one’s own company is usually a safe bet for executives, one which increases the earnings per share for a firm, and allows for a very good return on invested capital.

For stockholders, buybacks also push off a tax liability into the future. Theoretically, a dividend payment is inferior to share repurchases because of the tax liability paid by investors. Share repurchases increase shareholder’s ownership of a firm without taxes.

Buyback Achievers ETF (PKW)

The PowerShares Buyback Achievers ETF seeks to find companies buying back stock in much the same way some investors seek out dividend-paying firms. The rules-based ETF operates very simply on a few basic rules:

Included companies have to be incorporated in the United States

Each firm must trade on US exchanges

Firms must buy back 5% or more of their common stock in the trailing 12-month period

The requirements fuel higher turnover than other funds. Companies that repurchase 5% of their equity each year are quite rare – few can afford such a repurchase strategy for very long. More likely, companies meet criteria only for one or two years before cash outlays for share repurchase are scuttled as cash on hand is diminished.

Investment Methodology & Weighting

Any stocks meeting the three criteria above are put into the Buyback Achievers portfolio. Investments are market cap weighted, and capped at 5% of the portfolio.

The fund holds some 291 different firms, far more than one might expect given the very selective requirements for total share repurchases.

Personally, I like the fund’s inclusion requirements combined with the market cap weighting. Limiting the fund to companies that repurchase more than 5% of their common stock means it avoids firms that buy back shares solely to cover up stock option compensation to insiders. Also, the market cap weighting virtually ensures the fund is never taken by corporate diluters, who would find it very difficult to steal billions of dollars in shares by diluting the stock.

The 5% threshold is a bar set high enough that no stock will “accidentally” find itself as a position in the index. For a company to repurchase 5% of its equity, corporate leaders would have to view their company as a good wager at the current share price.

Industry Weight

Major holdings include consumer cyclicals (25.1%), technology (18.54%), health care (15.78%), industrials (11.65%), and consumer defensive stocks (8.33%). The heavy weighting of the fund to cyclical stocks makes this a fund for a turnaround.

Fees and Expenses

The fund carries a .7% annual expense ratio, which is higher than most market-cap weighted funds (Here are the 5 lowest cost ETFs). However, its small size and intriguing strategy make it inherently less cost-effective than large funds. Turnover and research costs undoubtedly add to the costs of managing this particular ETF.

Fund Performance

At the end of the day, it all comes down to total return. Here are the 5-year returns for PKW, as well as two other popular exchange-traded funds:

PowerShares Buyback Achievers ETF (PKW): 23.42%

SPDR S&P 500 ETF (SPY): 11.77%

SPDR S&P500 Dividend ETF (SDY): 11.59%

Interestingly, the PKW ETF has bested both the S&P500 index as well as the S&P500 Dividend Index, which currently holds the 62 highest-yielding S&P500 components (more types of High Yield ETFs). As share repurchases are often compared to the alternative, dividends, it is interesting to see a buyback fund perform twice as well over the 5-year period as one of the most popular dividend ETFs. This is especially vexing since dividends provide half the total market return over long periods of time and yet, PKW’s buyback strategy exceeds even the dividend payers in SDY.

See the chart below, which compares the price of the funds over time:

PKW, SDY, SPY

Be sure to note that this performance chart above does not include dividends. We can conclude from the share price performance that total returns from the buyback fund are almost exclusively from appreciation in the fund NAV. This only confirms the view that most companies cannot sustain both a high dividend yield and 5% repurchases of common stock every year.

There are a few reasons why total returns for PKW outpace both the SPY and SDY ETFs:

Exposure – The PKW fund is unlikely to invest heavily in financial firms. While financial firms were among the largest buyers of their own equity before the financial crisis, few banks ever repurchased more than 5% of their equity in any given year. This fund is unlikely to hold major banks in the future, given that repurchases are now governed by the Federal Reserve’s stress test results. At the time of writing, the PKW fund held only 8.22% of its assets in financial services firms, compared to 13% for the S&P500 index. If seeking a combination of financials and extremely high yield, check out Preferred Stock ETFs.

Leverage – Companies that repurchase shares increase their operating leverage by decreasing their cash position to buy back stock on the open market. In a recovery, companies that consistently repurchase shares will perform better than average. However, in down markets, companies that repurchase share are unlikely to outperform.

Timing – The 5-year period is very forgiving to the PKW ETF. In 2009, at the bottom of the market, the fund held companies that were most active in doubling down their bets on their own equity. Anyone who purchased shares in 2009 should have done quite well in the following years. Likewise, the 3 year period from 2006 to 2009 sent the PKW index falling faster than the S&P500 index as fund holdings were purchasing shares at prices in excess of the value on the market – essentially wasting money on falling stock.

Bottom Line

This is a fund that I would expect to outperform a broad market index such as the S&P500 index over the longest of investment horizons. The methodology favors firms that are most confident about future earnings power. The exit strategy is also clearly defined, as the fund sells positions once the buyout bank balance runs too thin to sustain purchases. Repurchase agreements often send stock prices soaring as companies repurchase shares on the open market.

http://seekingalpha.com/article/441761-etf-spotlight-powershares-buyback-achievers-etf

News Highlights: Top Equities Stories Of The Day

Apple To Announce Plans For Cash Balance

Apple will hold a conference call to announce what it plans to do with its roughly $100 billion in cash, a move to address investor concerns that the stockpile hasn't been put to good use.

Misys Agrees GBP1.27B Bid From Vista Equity

Vista Equity says it has agreed a recommended cash acquisition of U.K. banking software firm Misys, valuing the company at GBP1.27 billion.

UPS Reaches Deal To Buy TNT Express

UPS says it has reached an agreement to acquire TNT Express in a deal valuing the Dutch package shipper at around EUR5.16 billion.

Credit Suisse Lifts Offer On Own Debt

Credit Suisse says it will increase the amount of its own debt it will exchange for securities that qualify as capital under tighter banking rules to $5.19 billion, due to investor interest.

Five Banks Unite For Hedging Tool

Five banks have joined forces to create a hedging tool designed to improve the health of their balance sheets and protect them against market sell-offs, the Financial Times reports.

Rusal 2011 Net Falls 92%, Swings To 4Q Net Loss

Rusal swings to 4Q net loss in 2011, the Russian aluminum giant says, because of lower aluminum prices and high debt-servicing costs.

Reliance Communications Unit Seeks Singapore IPO

India's Flag Telecom, owned by Reliance Communications, files for an IPO on the Singapore Exchange, the Business Standard newspaper reports. The company seeks to raise up to $1.5 billion.

Carrefour Temporarily Closes Chinese Store

Carrefour temporarily closes an outlet in the Chinese city of Zhengzhou, after a state-owned television network reported that the store sold expired chicken and labeled regular chicken as the more expensive free-range variety.

Total, China Reach Shale-Gas And Refining Deals

French oil company Total unveils new pacts on shale-gas and refining operations with China, adding that Chinese authorities now own a 2% stake in the company.

GM Views Peugeot Deal As Start Of New Strategy

General Motors and France's Peugeot Citroen aim to begin joint development of at least two passenger cars by this fall. The cars are likely to go on sale by 2016.

BT Plans Pension Injection Of Up To GBP1.5B

U.K. telecommunications firm BT Group plans an early payment to cut a GBP5.4 billion deficit in Britain's largest private sector retirement scheme, the Sunday Times reports.

GDSI was up 40% this am, with a pull back to fill the gap. Watching for a possible bounce from here..

IENT slowly shaping up 0.02 x 0.025.. DD report coming soon

PSPF interesting find: 0.0019 x 0.0021

http://ih.advfn.com/p.php?pid=nmona&article=51191589

Bank of America owns 4.8 MILLION PSPF shares!!!

Let the reverse merger speculation run wild! wink

Do a search of BAC Director Michael Didovic(the man who signed the SEC filing).

Global Digital Solutions Announces Submission of Outstanding Project Bids in Excess of $6.5 Million

http://ih.advfn.com/p.php?pid=nmona&article=51627897&symbol=GDSI

I agree Cube it could go slightly lower, imo natural gas is looking extremely cheap so I would expect that we rally temporarily from the current prices. Only a matter of time imo

Us Jobless Claims Drop By 14,000 In Week

Initial jobless claims tumble by 14,000 to a seasonally adjusted 351,000 in the week ending March 10, much higher than the 5,000-claim drop expected economists and the latest sign that the labor market is improving.

You can play it long and I feel it is bottom. If could hit lower but not for long and they will likely rally it anyhow....they always find a reason and the rally would be short lived.

It is possible and it would limely be a good buy.

Cramer's Mad Money - The Magnificent 7 Spec Stocks (3/14/12)

Stocks discussed on the in-depth session of Jim Cramer's Mad Money TV Program, Wednesday March 14.

The Magnificent 7 Spec Stocks: Pharmacyclics (PCYC), Medivation (MDVN), Idenix (IDIX), Vivus (VVUS), Arctic Cat (ACAT), Conn's (CONN), Health Stream (HSTM)

On the 7th anniversary of Mad Money, Cramer discussed the 7 top-performing speculative stocks in the last 7 years.

1. Pharmacyclics (PCYC), has jumped from $5 to $25

2. Medivation (MDVN) has risen from $16 to $70, a 320% gain

3. Idenix (IDIX) has gone from $3 to $11 for a 277% gain.

4. Vivus (VVUS) has run from $6 to $27.

5. Arctic Cat (ACAT) has seen a 204% gain

6. Conn's (CONN) has risen from $4.56 to $14 for a 211% gain

7. HealthStream (HSTM) has seen a 192% gain.

Apple (AAPL), JPMorgan (JPM), IBM (IBM), Caterpillar (CAT), Molycorp (MCP), Regions Financial (RF), First Horizon (FHN), Francesca (FRAN)

Even though the Dow was meandering, up only 16 points, there is reason to be confident in the current market, whose leaders represent diverse sectors. Apple (AAPL) is innovating constantly, JPMorgan (JPM) is strong, IBM (IBM) is a well-run international consulting company, Caterpillar (CAT) is solid in spite of China faltering. Cramer would look for a return in construction.

Cramer took some calls:

Molycorp (MCP) is not a good stock, and is challenged when it comes to profits.

Regions Financial (RF) is okay, but not as well-managed as First Horizon (FHN)

Francesca's Holdings (FRAN) has seen a big gain and it is worth taking profits.

7 Stocks That Have Risen The Most in 7 Years: Monster Beverage (MNST), Regeneron (REGN), Medivation (MDVN), Green Mountain Coffee Roasters (GMCR), SXC (SXCI), Questcor (QCOR), Priceline (PCLN)

Cramer discussed the 7 fastest rising stocks in the 7 years since Mad Money has been on air.

1. Monster Beverage (MNST) has risen 1,637%

2. Regeneron (REGN) has risen 1,755% (Cramer recommended this stock during the first week Mad Money was broadcast)

3. Medivation (MDVN) up $1,800

4. Green Mountain Coffee Roasters (GMCR) up 2,731%

5. SXC (SXCI) up 2,800%

6. Priceline (PCLN) 2,850%

7. Questcor (QCOR) up 7,066%

Mad Mail: Microsoft (MSFT), Yahoo (YHOO), Sirius XM Radio (SIRI), Deckers (DECK), Lowe's (LOW), Home Depot (HD), Starbucks (SBUX), SPDR Gold Trust (GLD)

Microsoft (MSFT) is good, Yahoo (YHOO) is just okay and Sirius XM Radio (SIRI) is pure speculation.

Deckers (DECK) has suffered because warm weather was bad for Uggs sales. While the company has diversified into other shoes, the brands weren't introduced fast enough.

Starbucks (SBUX) has run a lot, so Cramer would put on half a position now and another half when it pulls back, because he thinks 2012 will be great for SBUX.

Lowe's (LOW) restructuring is working, but Cramer still prefers Home Depot (HD). He would buy LOW on a pullback.

Gold could go down another $100 to $150 before it bottoms. Gold miners should not be bought. Cramer's gold pick is still SPDR Gold Trust (GLD).

http://seekingalpha.com/article/435531-cramer-s-mad-money-the-magnificent-7-spec-stocks-3-14-12

Have The Natural Gas ETFs Finally Bottomed Out?

Although many energy commodities are surging, natural gas is still feeling the pain of weak prices. The commodity remains under pressure as new supplies of the key fuel are brought online all the time, making the historic oversupply situation even more of an issue. It also hasn’t helped that the winter has been unseasonably warm across much of the nation, reducing demand for the product as a key input for power plants as well.

These trends have pushed some more intrepid investors to predict a bottom in natural gas prices, declaring that eventually, this rough bear market in prices, which has seen the value of front month natural gas contracts decline from about $12/mm BTU in 2008 down to its current price around the $2.5 mark, has to end. Yet while investors continually call for the bottom in natural gas prices, the key commodity just keeps falling. In fact, prices have fallen by 50% in the past one year period and they are now near a 10 year low while inventories look to approach the highest winter close since 1983 when they hit 2.1 trillion cubic feet (read Commodity ETFs Plunge On Supply Forecast).

As a result of this, the outlook for natural gas still looks shaky going forward, especially given broad uncertainty over CNG and LNG implementation on a large scale. With this overhang, natural gas may not have reached a bottom just yet, especially if more gas supplies are brought online or if weather remains unfavorable to demand. On the other hand, a supply shock—be it in the form of weather or regulation—coupled with increased demand from new gas uses could make some investors look back on this time as the moment to buy (read Three ETFs For An Iranian Crisis).

While no one knows for sure which path will be the case, at least investors still have a plethora of options to play the fuel. Below, we highlight some of the pros and cons of each approach as well as a brief discussion of what investors can expect to see in each of these natural gas ETFs:

Natural Gas Futures ETFs

For investors seeking direct exposure to natural gas prices, the United States Natural Gas Fund (UNG) will be tough to beat. The fund sees volume of close to four million shares a day and has AUM of nearly $900 million, suggesting tight bid ask spreads for the product. However, the fund has seen heavy contango in recent months and years, coupled with the general decline in value of natural gas prices. Thanks to this, UNG has lost about 52% over the past 52 weeks including more than one-third of its value in the past three months alone (see Inside The Forgotten Energy ETFs).

Beyond UNG, there are a number of other options as well, including the fund’s cousin the United States 12 Month Natural Gas Fund (UNL). This product sees slightly less in contango thanks to its approach which spreads out exposure across 12 months of the curve, helping to push the fund down ‘just’ 42.5% over the past 52 weeks, although it does see tiny volumes in comparison. In addition to this choice, investors also have the iPath DJ-UBS Natural Gas TR Sub Index ETN (GAZ) for those seeking the ETN structure, Teucrium’s Natural Gas Fund (NAGS) which spreads out exposure across multiple points on the curve, and the iPath Seasonal Natural Gas ETN (DCNG) which only offers exposure to December contracts.

Natural Gas Equity ETFs

Given the uncertain future of the commodity, as well as recent price weakness, some investors may want to play natural gas via an equity route instead. This path may see less volatility than commodities, and also help to avoid the contango issue too. On this front, investors currently have two options; the First Trust ISE Revere Natural Gas Index Fund (FCG) and the brand new Market Vectors Unconventional Oil & Gas ETF (FRAK).

FCG holds 30 securities in total, charging investors 60 basis points a year for access to its basket of natural gas focused stocks. The product has a heavy focus on exploration and production firms as these securities make up nearly 80% of the total exposure. From a performance perspective, the fund is down just 14% over the past year but is up 6.6% in the past quarter. FRAK on the other hand could see some of same key risk/reward points as FCG but could also see a heavy influence from the oil shale market as well. Still, the product has a similar 80% focus on energy exploration companies so it could be another way to play the natural gas market (read Is HAP The Best Commodity Producer ETF?).

Short Natural Gas ETN

Given the oversupply situation and the lack of new uses for large amounts of natural gas at this time, some may want to take a short position in natural gas. Until recently, this was tough to do with ETPs but appears to have changed with the launch of the VelocityShares 3x Inverse Natural Gas ETN (DGAZ). The note looks to provide triple the daily inverse performance of natural gas futures while collateralizing the investment with a purchase of short-term Treasury bills. This could make DGAZ a great pick for those who think that the oversupply situation in the natural gas market has further to run and that prices of the important fuel are headed sharply lower again this year.

http://seekingalpha.com/article/420991-have-the-natural-gas-etfs-finally-bottomed-out

Looks like Gold fell through support at the 200ma, we may get a pull back to 1600 flat now.

U.S. Treasuries Bubble: Beginning To Burst?

The trade has been talked about by many of the most reputable fund managers. People, including myself in a December 2009 article, have anticipated the top for several years now. Yet those who have been short US Treasuries have been treated to constantly declining yields. For the first time in a long time, increased slack in the Treasury market manifested itself yesterday with yields leaping upward.

A 2.5 standard deviation move in 10yr yields broke the yield above the 200 DMA and was a rare example of Treasuries being more sensitive to the 'risk-on' trade than equities in the past few years. We think this seemingly minor shift in correlation strengths is an indicator of building selling pressure in Treasuries. Treasury yields have lagged as equities have rallied over the past few months, yet the general stabilization in financial markets and the macroeconomy should gradually begin to take its toll on UST demand over the course of 2012.

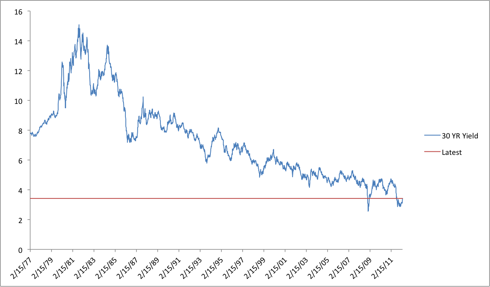

To be sure, not all signals have turned green, though that should be good news if you're looking for an entry point. As more signals begin to point against Treasuries, they will serve as price catalysts and confirmation that the trade is playing out as expected. Here are two time series, the first of the 30 yr bond and the second of the 10 yr note, showing the massive secular downtrend in UST yields over the past 5 decades.

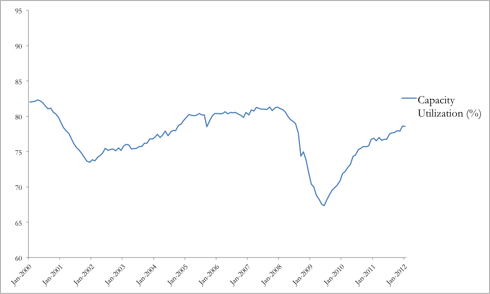

Theoretically, the price floor is a 0% yield, though in actuality inflation will cause nominal yields of about 2% to be real yields of 0%. We are extremely close to negative yields on the 10 yr and investors in Treasuries of all maturities are getting an insulting level of compensation for lending their money to the US government. As inflation returns to normal levels, capacity utilization returns to pre-recession 'normal' levels, and employment begins to pick up, money will inevitably flow from a multi-year hibernation in USTs back to the equity market.

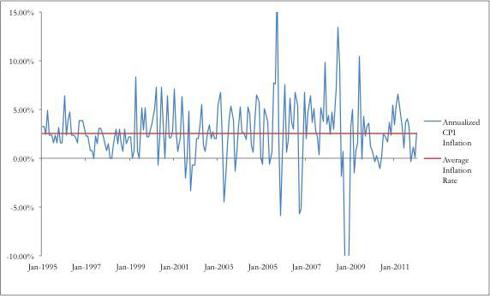

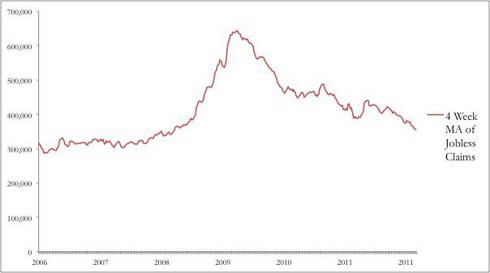

Below are some long-term charts of Annualized CPI, Capacity Utilization, and the 4-week Moving Average of Weekly Jobless Claims. Observe that all three charts are in the process of returning to pre-recessionary levels.

Though investors in the short-UST trade have been disappointed by a number of 'false starts' over the past 3 years, we are confident that the stabilization of the US economy will begin to put a bid into Treasury risk premiums. US economic data hasn't been the only thing hurting Treasuries. Last week's relatively benign Greek default and restructuring has credibly shown investors that European officials are dedicated and able to resolve peripheral debt problems without disorderly outcomes.

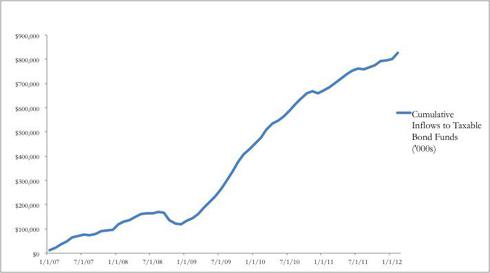

Observe the relatively calm response in the Spanish and Italian bond markets that followed ISDA's announcement of a Greek CDS payout. As uncertainty resolves itself, the safety trade underlying Treasury demand will begin to unwind. The accumulation of fund flows into mutual funds invested in taxable bonds has begun to peak. Observe the declining 2nd derivative:

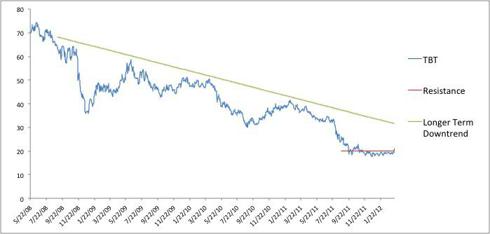

The strange undercurrents of the past few days in the UST market may be harbingers of coming price action. Our favorite way to play the trade is a position in the levered ETF TBT which is built to perform roughly two times the inverse of the longer end of the UST curve. Since rate increases should hit the longer maturities harder, and because the eventual withdrawal of the Fed's Operation Twist should accelerate the effect of rate increases, we prefer to bet against the outer maturities.

Another option we are less interested in is the PST, which is a levered short of 7-10yr weighted average maturities. Below is a chart of the TBT, which broke above the technically important $20 level yesterday. Note that a break above the longer term down trend (perhaps in the neighborhood of $30) should signal a confirmation that a turnaround in the Treasury market is occurring.

We see two key risks to the short Treasuries thesis. First, the trade could play out over too lengthy a timeframe for the position to meaningfully outperform. As you see in the charts at the top of the page, the decline in yields has been a two generation event and there is a chance that large price movements might only take place at very lengthy increments.

Further, despite the fact we've endured a 3 year bottoming period, it's obviously possible that there could be several years ahead of low yields. We continue to think this is unlikely simply because of the radical divergence between bonds and the equity markets over the past year. While equities have 're-risked', bonds have been stuck in the basement.

These kinds of disjunctions tend to resolve themselves in a speedy manner. As investors realize that the US economy has turned the corner and Europe becomes less of a headline threat, we expect to see a semi-panicked drop down in UST prices sometime this year. Beyond this initial movement, further action on the position might take longer to manifest.

The other main risk is that Baby Boomer fund flows continue to drive demand for USTs and facilitate continued divergence from equities over the next 5-10 years. As Baby Boomers de-risk their retirement portfolios, bonds may be the beneficiaries. We view this as unlikely mainly because the amount of funds flowing out of Treasuries (as the temporary safety trade of the past few years reverses) should outweigh the portfolio readjustment inflows from Baby Boomers.

http://seekingalpha.com/article/435411-u-s-treasuries-bubble-beginning-to-burst

S&P 500 Vs. U.S. Dollar Index

As we have noted in prior reports and posts, there have been a number of abnormalities taking place in recent weeks regarding the rally in the S&P 500. Whether it is the recent underperformance of the Russell 2000 or the divergence in the DJ Transports, trends we typically expect to see as the market rallies haven't really transpired.

Another notable aspect of the rally over the last week or so is that it has been accompanied by strength in the dollar. Over the last ten years, we have grown accustomed to rallies in equities being accompanied by a weak dollar, but over the last two weeks, both the dollar and S&P 500 are up. Even over the last year, the inverse correlation between the two assets has not been as pronounced. In fact, at the end of 2011, we saw a similar trend when the dollar and the S&P 500 both rallied in step with each other until the dollar took a breather in January.

While the divergence between the S&P 500 and small caps and transports is generally considered a negative, outside of the last ten years, rallies in equities usually occurred hand in hand with a run higher in the dollar. So while continued divergence between the S&P 500 and small caps and transports would be a negative if it continues, we would view the strength in the dollar as a positive for equities.

The New Apple TV Will Finish What The Mac Started: Killing Off Discs

By MG Siegler

I remember watching the HD DVD vs. Blu-ray wars closely a few years back. I wanted one to win so I could go out and buy a next generation movie player. But the battle went on and on, and by the time Blu-ray won, I had set my sights on a new frontier: digital distribution. I never did get that Blu-ray player. And now I’m quite certain I never will. The new 1080p Apple TV (AAPL) is here.

To be clear, because of the way it’s compressed, iTunes 1080p content is not equal to the 1080p picture you’ll get from a Blu-ray disc. It’s very close, but it’s not quite there yet. I imagine it will get there as digital compression technology continues to improve. But even if it doesn’t, this is something that won’t mean a thing to the vast majority of consumers. Thanks to the marketing of television sets over the years, they know “1080p”. They don’t know that the quality can be inconstant. Fair or not, it won’t matter.

That’s one reason why the new Apple TV is such a huge win here. Previously, it was limited to displaying 720p content which undoubtedly gave some would-be purchasers pause. But a new chip (a single-core A5), some 1080p content in iTunes, and the same $99 price changes that.

But there are cheap Blu-ray players out there now, so why does the Apple TV trump those? And what about other boxes like the Roku, which can also do 1080p streaming content? One word: AirPlay.

Having used the previous iteration of the Apple TV almost a year now, I’m absolutely infatuated with AirPlay. The love affair is so deep that I’m sickened to think about going on the road and it not being available in most hotel rooms. It absolutely should be. And if we can just get past some open WiFi issues (imagine someone pushing content to another, unsuspecting room), and some greedy hotel chains (who love their rip-off pay-per-view content), it will be. The boxes should be as ubiquitous in hotel rooms as iPod/iPhone chargers now are.

AirPlay is one of those things that still seems like magic every time you use it. How on Earth am I streaming an HD movie wirelessly from my iPhone or iPad to my television while I continue to use that device? If it’s possible, why does anything need wires anymore?

I think people are often tricked when they first hear about the Apple TV. Certainly, Apple does everything in their power to downplay its importance to the company. And yes, that probably has something to do with other, more substantial television hardware coming down the line. Right now, people look at the Apple TV and think, “okay, cool, a tiny device to access iTunes content from my television”. At $200 to $300, it made little sense. At $99, it made some sense. But it still lacked that killer feature.

The true key to the Apple TV is AirPlay. And the latest version supports 1080p streaming as well. And soon, with the release of OS X Mountain Lion, you’ll be able to AirPlay your entire desktop to your television. Meanwhile, the potential for gaming here is just starting to be tapped.

There’s no reason why every person with an iOS device (and soon a Mac) shouldn’t get an Apple TV. And that’s a problem for the makers of Blu-ray players. Again, just slightly better quality will no longer be enough. Apple’s latest Apple TV is going to continue the trend they began with the MacBook Air — the killing off of optical discs.

As for the rest of the new Apple TV, it’s great, just like the last version was. The outside looks the exact same and it’s just as easy to set up. The included aluminum remote control is still pretty lame (try searching, or doing anything that involves typing with it), but you can get around this if you have an iOS device — get the Remote app ASAP.

Alongside the new Apple TV announcement, Apple rolled out new software for the device. It’s a significant improvement over the previous software. You’ll note right away how app-y everything looks. When you consider this along with the fact that the Apple TV technically runs a version of iOS, it’s clearly only a matter of time before more apps come to the device. Currently, Apple has a very limited set of third-party partners (Netflix, MLB.TV, etc) on the device. But they could easily open it up. (Though, again, they may not ever have to thanks to AirPlay.)

The good news is that the Apple TV software update also works on the last iteration of the Apple TV. So unless you really want access to 1080p content, there’s not a huge incentive to buy a new one. (Even with the new software, the older Apple TV is limited to 720p.)

And because Apple has moved all of their TV catalog and much of their movie catalog to iCloud (some studio deals are still being negotiated, but sound close to being done), all applicable HD content can be automatically upgraded to 1080p from 720p (SD content will remain SD).

So no, Apple didn’t give a huge incentive for current Apple TV owners to upgrade to the newer box. But they gave a huge incentive to millions of people without an Apple TV to get one. And that’s bad news for Blu-ray.

http://seekingalpha.com/article/435611-the-new-apple-tv-will-finish-what-the-mac-started-killing-off-discs

Wall Street Breakfast: Must-Know News

After banker's tirade, what next for Goldman? The buzz yesterday centered on Greg Smith's very-public resignation letter from Goldman Sachs (GS), in which Smith used The New York Times as a platform to launch a blistering attack on Goldman's "toxic and destructive" culture. Also making the rounds was a blog post by James Whittaker explaining why he left Google (GOOG). If you haven't read the two letters yet, you should (Smith, Whittaker). In their own ways, each is going after his ex-employer for no longer putting its customers first. But now that ex-Goldman exec Smith has had his Jerry Maguire moment, the real question is whether his letter to the masses will have any effect on Goldman's business.

Cisco in talks with NDS. Cisco (CSCO) is in advanced talks to buy NDS for $5B, according to a report in Israel's Calcalist financial newspaper. That purchase price is roughly a 35% premium to NDS' value when it delisted from the stock exchange in 2009. NDS, which develops software for multi-channel television networks, is jointly owned by News Corp. (NWS) and P-E firm Permira.

Treasury to sell some bank holdings. The Treasury said yesterday it plans to sell its preferred stock position in six community banks as it works to unwind bailout programs. The Treasury will conduct public auctions to sell its stock in Banner Corp (BANR), First Financial Holdings (FFCH), MainSource Financial (MSFG), Seacoast Banking (SBCF), Wilshire Bancorp (WIBC) and WSFS Financial (WSFS).

UBS cuts bonus pool. UBS (UBS) cut its 2011 bonus pool by 40% to 2.6B Swiss francs ($2.8B) to reflect tough market conditions that hurt results at its investment bank. CEO Sergio Ermotti's overall compensation was 6.35M Swiss francs, of which 4.6M francs was a bonus.

China's hard landing. China is already in a hard landing, according to Adrian Mowat, JPMorgan's chief Asian and emerging-market strategist. "If you look at the Chinese data, you should stop debating about a hard landing... Car sales are down, cement production is down, steel production is down, construction stocks are down. It’s not a debate anymore, it’s a fact." Separately, inside sources said China is easing lending curbs at three of the nation's four biggest banks after data showed new loan growth at a four-year low.

Apple keeps climbing. Apple (AAPL) gained another 3.8% yesterday, hitting a new high of $589.58. The behemoth is now worth almost $550B, nearly twice as much as Microsoft. In addition to a bullish Morgan Stanley note early yesterday, shares also got a boost from Canaccord's Mike Walkley, who reported shipping wait times for the new iPad have risen to 2-3 weeks. Walkley now expects Apple to sell 65.6M iPads this year, and 90.6M next year.

Samsung claim rejected by court. A Dutch court rejected an attempt by Samsung (SSNLF.PK) to get the iPhone and iPad banned, stating the patents Samsung was asserting must be licensed on FRAND terms. Of interest is the court's claim that Apple (AAPL) doesn't need a FRAND license since it uses Qualcomm (QCOM) chips, and Qualcomm has licensed Samsung's patents. Such a ruling could give Apple motivation to continue using Qualcomm chips in future iPhones and iPads.

Gartner raises chip estimates. Gartner expects chip sales to rise 4% in 2012 to $316B. That's above a prior forecast for 2.2% growth, and is the result of growing optimism that demand will begin rebounding in Q2 following a tough inventory correction. DRAM sales are expected to rise slightly after falling 25% last year, while NAND flash memory sales are expected to rise 18%.

Corporate cash pile grows. U.S. companies are sitting on a massive $1.2T cash pile, Moody’s said in a new report, and more than half of it is stashed overseas. The tax code is to blame and it will get worse without “permanent tax reform that lowers taxes on overseas profits,” Moody’s wrote. Apple (AAPL) is a major factor: In 2011, overall corporate cash would actually have decreased by $6B if not for Apple’s $46B increase.

Fitch affirms U.K. rating. Fitch affirmed the U.K.'s credit rating at AAA, but revised its outlook to negative from stable. The agency had mostly positive things to say about the country's attempts at budget reform, but cautioned there is "very limited fiscal space to absorb further adverse economic shocks."

SNB holds rates steady. The Swiss National Bank held rates steady at 0-0.25%, as expected, and said it "will continue to enforce the minimum exchange rate of CHF 1.20 per euro with the utmost determination." The SNB cautioned that in the "Swiss mortgage and real estate market for residential property there are growing signs of imbalances. Should these imbalances increase further, this could lead to considerable risks to financial stability."

RBI leaves rates unchanged. The Reserve Bank of India kept its repurchase rate at 8.5%, as expected, after inflation accelerated. RBI reiterated that future actions will be toward lowering rates, though remaining inflation risks "will influence both the timing and magnitude of future rate actions.”

Feedback or story tip? Please direct message SA Editor Rachael Granby »

Today's Markets:

In Asia, Japan +0.7% to 10123. Hong Kong +0.2% to 21354. China -0.7% to 2374. India flat at 17676.

In Europe, at midday, London -0.1%. Paris flat. Frankfurt +0.3%.

Futures at 7:00: Dow +0.1%. S&P +0.1%. Nasdaq +0.2%. Crude flat at $105.46. Gold +0.1% to $1644.50.

Thursday's economic calendar:

8:30 Producer Price Index

8:30 Initial Jobless Claims

8:30 Empire State Mfg Survey

9:00 Treasury International Capital

10:00 Philly Fed Business Outlook

10:30 EIA Natural Gas Inventory

4:30 PM Money Supply

4:30 PM Fed Balance Sheet

Notable earnings before Thursday's open: AMCX, ROST

http://seekingalpha.com/article/435791-wall-street-breakfast-must-know-news

|

Followers

|

1

|

Posters

|

|

|

Posts (Today)

|

0

|

Posts (Total)

|

198

|

|

Created

|

02/29/12

|

Type

|

Free

|

| Moderators | |||

| Volume | |

| Day Range: | |

| Bid Price | |

| Ask Price | |

| Last Trade Time: |