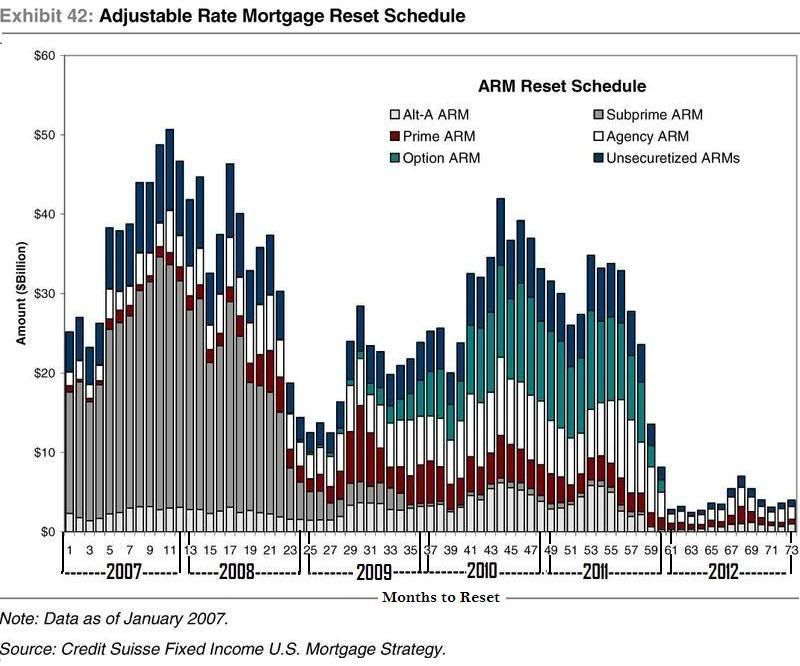

Does anyone have any information on the rates that these option arms are resetting to? It looks like there is a peak in option arms coming up late nest year but I haven't seen anything about the actual result of the resets in rates for these mortgages. It's possible that many of the resets may well come in at very reasonable interest rates given the current rate environment. My son just obtained a 30 year fixed at 4.625% and didn't have to buy it down.

Certainly there will be a large wave of additional defaults but I'm betting that the industry could be surprised re the number of mortgage holders that will come out way ahead when they actually fix their rates.

I totally forgot about that!!! Thanks for reminding me. I'll have to get my chart now.

Notice last time it was mostly the subprime arms. Now its the prime arms and option arms in 2010! So if the arm adjusts to over 7% we could have the same mess all over again!

I'm sure borrowers got 4% rates on the 5/1 arms..so those might jump to 7+ % next year!

Yesterday, Moody’s released its commercial real estate index and reported that nationwide prices for all types of commercial real estate (CRE) plunged by 8.6% in April from March and now stand 25.3% below a year ago, and are off 29.5% from their October 2007 peak.

The Moody’s/REAL CPPI is a repeat sales index constructed very much along the same lines as the Case-Schiller index of residential real estate prices. In the graph below, Calculated Risk http://www.calculatedriskblog.com/2009/06/cre-and-residential-re-prices.html has overlaid the Case-Schiller index on the graph from the Moody’s report. It clearly appears that CRE prices follow housing prices with about an 18-month lag.

This is consistent with other findings that investment in CRE (i.e. new building of offices and stores) follows residential investment by about the same period. While the CRE price decline started later than that for houses, it is happening at a much faster rate.

While the all property index shows a monthly change, the sub-indexes by property type are only available on a quarterly change basis. Relative to three months ago, office building prices have been particularly hard hit, plunging 18.6%. Prices of retail buildings have fallen by 12.9%.

By comparison prices for Apartments and Industrial space have held up well, dropping by just 0.4% each. However, on a year-over-year basis they are both down sharply, Industrial space by 12.3% and Apartments by 16.1%. On a year-over-year basis, retail space has lost 18.5% of its value while office space has plunged by 28.9%.

The reason why the value of CRE is falling is not a mystery. If stores are closing, then they will not be paying rent, and landlords will not be in a position to get rent increases from the remaining stores. If a company is laying off lots of people it will have lots of empty cubicles and offices, and will be looking to sublet its existing space, competing directly with the landlords trying to rent out existing space.

In addition, as recently as the second half of last year, construction of new commercial real estate was still very robust, meaning that there is lots of new space that has recently come on line. Still, a 8.6% decline in a single month is startling and is very bad news for REITs like Mack-Cali (CLI: 21.96 -0.20 -0.90%), Liberty Properties (LRY: 22.62 -0.20 -0.88%), Post Properties (PPS: 13.55 -0.05 -0.37%) and Cousins Properties (CUZ: 8.32 +0.20 +2.46%).

We have already seen commercial delinquencies and foreclosures start to rise, and this will be a major headache for the banks going forward. Many small- and mid-sized banks ($1-10 billion in assets) are very heavily exposed to CRE. This could cause them to be the guest of honor at one of the Friday night pizza parties put on by the FDIC. However, individually these banks do not threaten the financial system the way the stress-tested 19 would if they failed.

News

News  Market Data

Market Data  Discover

Discover