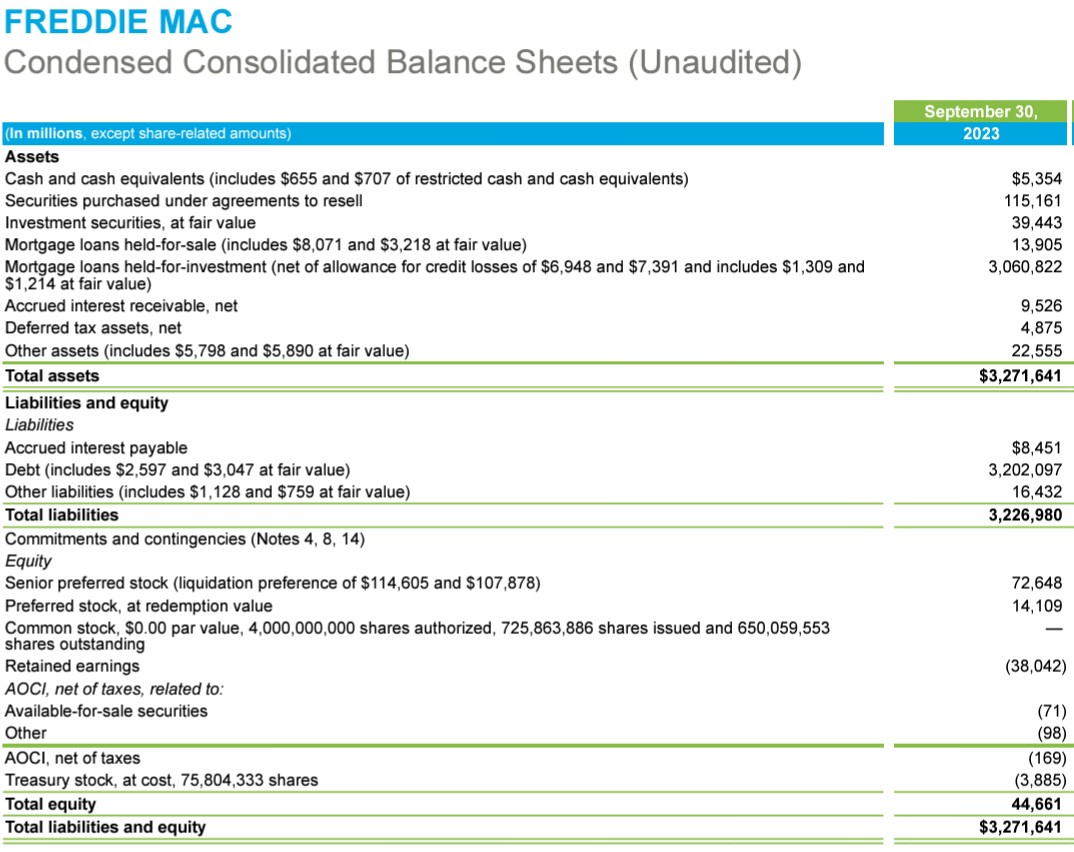

So with the retained capital increasing, is the liability listed under the "Non-Redeemable Preferred Stock", or does it go to Shareholder Equity? Shouldn't there be a separate line item for Liquidation Preference that Treasury can demand redemption? If redeemed, that wipes out all of the shareholder equity.

ASC 505-10-50-4 - "An entity that issues preferred stock (or other senior stock) that has a preference in

involuntary liquidation considerably in excess of the par or stated value of the shares shall

disclose the liquidation preference of the stock (the relationship between the preference in

liquidation and the par or stated value of the shares). 3 That disclosure shall be made in the

equity section of the statement of financial position in the aggregate, either parenthetically or “in

short,” rather than on a per-share basis or through disclosure in the notes"

I'm no financial expert, but I'm calling shenanigans on FnF balance sheets.

News

News  Market Data

Market Data  Discover

Discover