Deceitful Robert-Katie Buehler make the whole thing up. Robert refuses to unveil his real name. Likely, he is a well-known reporter who has been hired for the Fanniegate scandal, just watching the number of comments on Ihub and the fact that he claims to be attending the trial daily. Hand in hand, only two people in the world is attending this trial, where they only talk about "he said, she said" and nothing about finance and the laws in force. Then, there is that Twitter guy FnFGatefun that can't be taken seriously, likely the FnFreddie user that writes here to shamelessly praise the attorneys and call them "patriots". No serious reporter has informed about the staged trial involving the FHFA and the hedge funds, but also the DOJ gave the go ahead to the farce and remains as a party behind the scenes. In the prior trial, a Bloomberg senior reporter claimed to be in the courthouse cafeteria at the time, but no word about it this time around. At least, he had lunch for free that day.

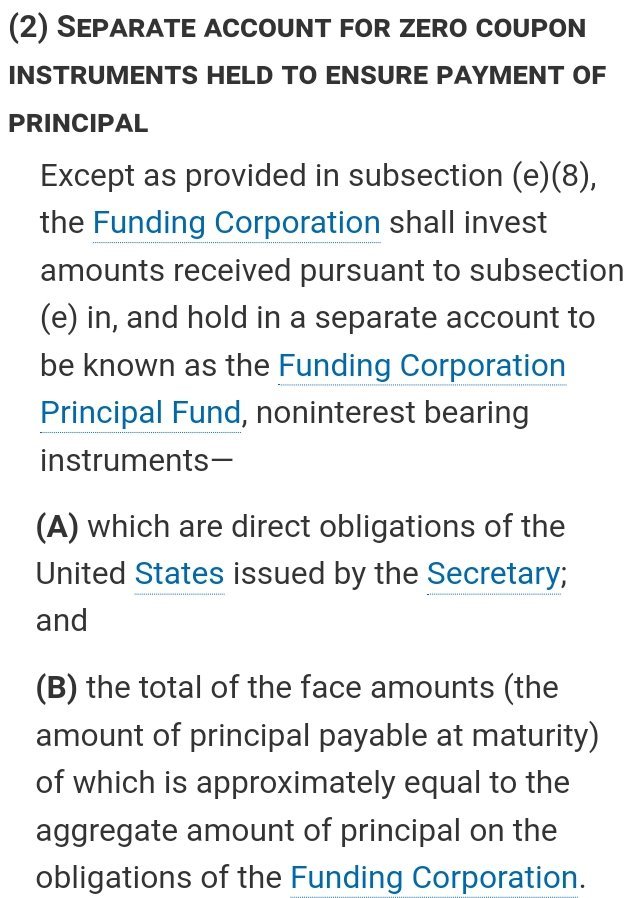

The whole phony trial aims to repeat a thousand times that the PA was improperly amended with the NWS dividend. They are obsessed with making the 10% dividend prevail. When, the dividend is struck down and the 10% rate too. FnF are not ordinary businesses and they have a cheap backup from Treasury at rates that take into consideration the rates as of the last month to the purchase, in exchange for their Public Mission (estimated at a weighted-average 1.8% dividend rate, applying a 0.5% spread over Treasuries at the time. The same occurred with the FHLBs, 10% interest rate with a 0.299% spread. You can take the same 10% rate 20 years later, because it isn't the same spread over Treasuries) The 10% dividend is an obsession of the plotters from the onset. This way, it depletes capital in FnF and increases the capital needs and stock offerings for the hedge funds and investment banks. All day with the 10% contractual rate. There is no contract between Federal Agencies to begin with. The only contract with the government is called Charter Act, where FnF enjoy a low cost borrowing scheme from Treasury as a last resort (section Purposes: "the operations shall be financed by private capital to the maximum extent feasible") among other privileges, and everything you see can be changed using the FHFA-C's Incidental Powers: "any action authorized by this section", in other words, there is other plan behind the scenes. Primarily, they can't understand that the 10% dividend inflicts the same damage on the enteprises as the NWS dividend: the reduction of their Core Capital, and that's a breach of the conservator's rehab power, related to the soundness of FnF (capital levels), have positive balance in the Retained Earnings accounts ($-216 billion as of June 30, 2023) that absorb future losses, reduce the debenture SPS with the taxpayer, etc. Actually, the 10% dividend caused greater damage, because 11 quarters out of 16 quarters prior the 3rd amendment, either in its entirety or part of it, the 10% dividend increased the capital deficiency (negative Net Worth) in Freddie Mac, more draw requests to UST to pay the dividend to Treasury (circular flow), more SPS, reduction of the funding commitment (death spiral) and also it caused public outcry at a time when the harassment on the enteprises was the daily bread and butter back then. So, the UST was taking away more core capital than the core capital generated during the quarter. This is why now, we can't unwind this separate account to see the Total Comprehensive Income generated during conservatorship, by simply cancelling the SPS outstanding, when a profit arises. Analysis posted here. I guess that the figures with Fannie Mae are far worse and maybe it's 15 out of 16 quarters. So, the PA was impeccably amended to enact the NWS dividend, as the fastest speed for the separate account plan that was repaying the SPS at the time, and it continued for their Recapitalization thanks to the July 20, 2011 CFR 1237.12. DeMarco and Sandra Thompson, who arrived to the FHFA in 2013 as Deputy Dtr in charge of capital adequacy matters, will never admit that they've been carrying out a Separate Account plan, nowadays the 3rd phase with the gifted SPS, considered a joke, primarily because their motive could be no other than to make up for the $30 billion in losses of the principal of the RefCorp obligation the UST bought from the Funding Corporation that bailed the FHLBanks out in 1989. Sandra Thompson at the FDIC at the time and DeMarco at GAO (then, at the UST), thought that the FHLBanks only had the obligation to pay interests on the RefCorp bonds (read the FHFA press release on the day that the obligation was satisfied, mixing up "obligation" a noun with "obligation" a debenture) , and not that the monies set aside in a Separate Account (statutory provision: Separate account) invested in zero-coupon Treasury Notes, are meant to pay down the principal of the obligation too. They will take the Separate Account plan to their graves. Huge pressure from the hedge funds nowadays. The Separate Account is set forth in the law and basic finance, and no document or words are necessary. A dividend depletes capital and this is why they are restricted by law as a Prompt Corrective Action in the FHEFSSA's Restriction on Capital Distributions that they shamelessly have covered up all along. The gang called The Tipp-Ex Gang. Not only they have covered up many things like the fact that the NWS was a dividend, the low cost UST backup in the Charter, Fee Limitation of the United States, etc., but also, after the coverup, they have substituted it, like the 2011 mandate by the Dodd-Frank law about "recommendations on ending the conservatorship" and the UST-HUD's report as a result: Housing Finance System revamp: "stringent capital requirements", substituted by the September 2019 Mnuchin's Housing Reform plan, with a Govt Explicit Guarantee that satisfies China, and pursuant to a Presidential Memorandum to give it some sort of formality.

What lies behind is JPS holders reluctant to use their dividend suspended by law and finance, for the recapitalization of financial enterprises. They rather bring the whole company down with them, rather than see their dividend kept by the company. These rebels play the fool because it's unacceptable to consider that they don't understand that a JPS is a made-up hybrid financial instrument with the only purpose of recapitalization of enterprises upon undercapitalized. This is why an obligation (debenture) is recorded in Equity and core capital (loss-absorbing capacity, capital adequacy-related), like all other items recorded in core capital (Retained Earnings account, Additional Paid-In Capital, common stocks, JPS) and why the cumulative dividend SPS is not recorded in core capital (no loss-absorbing capacity). Due to the risk of dividend suspension, the JPS gets a higher dividend rate than the interest rate on similar obligations by the same issuer. The capital requirements today are greater than the ones in 2008, after the FHFA imposed the Basel framework, where the Minimum Leverage capital requierement is Tier 1 Capital greater than 2.5% of adjusted Total Assets, whereas for the banks it's 3%. So, if there are changes in the capital requirement, it should be higher, not lower, as the plotters now claim, to match the international standard Basel. The Risk-Based capital requirement, Total Capital greater than 8% of RWA, is the same as the banks', and it's lower than the Leverage Capital requirement, yet, the plotters keep on complaining about this requirement when it's the other the one that marks the Undercapitalized threshold and it's higher than the risk-based capital requierement that marks Adequately Capitalized threshold.

One thing is clear: our negotiator has requested $3.9 per stock (0.5% IRR on a $50 JPS during 15 years) to each counterparty for Punitive Damages: the plotters peddling the government theft story in formal documents and the DOJ.

News

News  Market Data

Market Data  Discover

Discover