As a juror, which part can not be understood here. Being charged twice as much or taking profits forever. Which part is not theft here? The treasury basically took the playbook from a mafia. Charge usury rates, then take all for profits, claiming that they are there to protect the neighborhood.

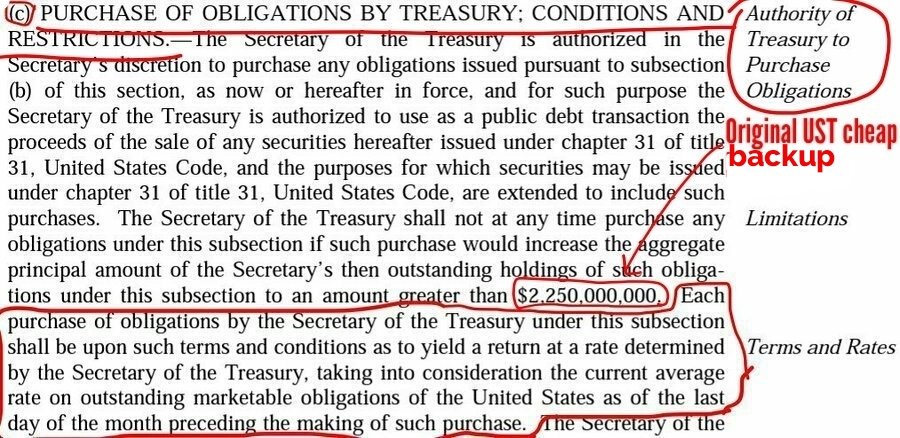

Robert makes all up, using alleged witnesses to peddle the MOB's diatribe, contending that FnF have to pay a commitment fee to UST for the funding commitment, when the Charter Act PROHIBITS the United States from assessing and collecting a fee or charge on the securities or assets of FnF, in the clause entitled Fee Limitation, Other than the LOW COST rate on redeemable obligations (subsection c), which is the dividend rate on SPS and in an amount updated in the SPSPA thanks to the subsection (l) inserted in the Charter Act by HERA. A second UST backup with an unlimited rate and in an unlimited amount. 2 UST backups of FnF, instead of having Congress updating the outdated limit in the original UST backup, that paved the way for the plan of deception with a Separate Account plan. So, they must be talking about another Charter Act. Just revoke this one and charter new private corporations with all your add-ons. E.g. the CRT currently forbidden in the clause Credit Enhancement, for which we request a refund of the CRT expenses, net. The UST backup of FnF is free of charge in exchange for their Public Mission in the section Purposes (secondary market operations: countercyclical role, charge less to low- and moderate-income families), until FnF actually use this "special borrowing right from Treasury" (quote from the SCOTUS-appointed amicus, Professor Nielson, representing the FHFA during the oral arguments) Robert, if that's his real name, shamelessly conceals that the SPS get a dividend, not interests. This is because a dividend is a distribution of earnings, restricted in the FHEFSSA's Restriction on Capital Distributions, and unavailable funds with deficit in their Retained Earnings accounts. No worries because they are cumulative dividends. A NWS dividend is also a breach of the conservator's power of Rehabilitation of FnF, and rehabilitation means to restore them to a sound and solvent condition, that is, capital levels. It isn't related to the rehabilitation of the taxpayer. Hello? This is why the exceptions to the aforementioned restriction on capital distributions, kicked off: funds applied towards the reduction of the SPS and, once the SPS were fully repaid in late 2013 and 2014, the FHFA had already enacted on July 20, 2011, the CFR 1237.12: for their Recapitalization. The interests of the taxpayer is to have FnF Adequately Capitalized. This CFR 1237.12 states that

(c) it supplements and shall not replace or affect the restriction on capital distribution in the FHEFSSA.

So, you can't think that one exception to a restriction is to deplete their capital with dividends to the taxpayer, because you would be affecting the original restriction on capital restriction by statute. This is why I posted that the 4 exceptions in the CFR mean the same: their recapitalization, and deplete capital for a recapitalization means that you are doing it in a separate account, using the FHFA-C's Incidental Power "best interests of FHFA", which includes lying about it, and eventually, it'll be returned because it needs to be recorded on their balance sheets. The same occurs with today's SPS LP increase for free. Another capital distribution in its statutory definition that is restricted, and the exceptions kick off: for their recapitalization. Like with the dividends, it means that the common equity is held in escrow, which is very easy to see with these gifted SPS had they been recorded on the Balance Sheets, because they carry an offset with reduction of Retained Earnings accounts. This offset is the representation of the Common Equity held in escrow at a glance (Retained Earnings is part of the Common Equity). The separate account would have been spotted and the investors would have seen that the same common equity held in escrow occurred with the dividend payments, if they didn't see it before in the legislative wording (dividends restricted, funds applied towards the reduction of the SPS) But the gifted SPS are missing on the balance sheets: a Financial Statement fraud for which we request a compensation, along with other 7 Securities Law violations. The restriction on capital distributions by regulation and statute, were explained yesterday here.

So many valid points on the abuse. All for just 7 cents is atrocious. The Treasury really hates the GSEs and the corruption runs through the country in all places sadddddd

News

News  Market Data

Market Data  Discover

Discover