On the "too vested" Volker, comment. Seems to me, he is there because there would be a number including Biden who see him as the best for the job at this time. That said then, as i said before, we basically have two options: Trust the guys in charge are doing their honest best, or go with QAnon. What else can we do unless there is solid evidence a guy like Volker is not really doing what he thinks is best. Or solid evidence he is wrong. What he thinks is best still could be wrong, of course. One version of an old joke could be, put 100 economists into one room and you get 105 opinions of what to do in any situation. This from Krugman of 2015 likely is also close enough to be applicable today:

Is The Economy Self-Correcting? (Wonkish)

November 30, 2015 2:02 pm November 30, 2015 2:02 pm

What I want to focus on in this post is the suggestion by Brad DeLong .. https://equitablegrowth.org/must-read-paul-krugman-demand-supply-and-macroeconomic-models/ .. that I missed a failed implication of Hicksian analysis — that demand shocks should be short-term in their effect. Actually, and very unusually, I think Brad has this wrong. The proposition of a long-run tendency toward full employment isn’t a primitive axiom in IS-LM. It’s derived from the model, under certain assumptions. But there’s good reason to believe that even under “normal” conditions it’s a very weak, slow process. And under liquidity trap conditions it’s not a process we expect to see operate at all.

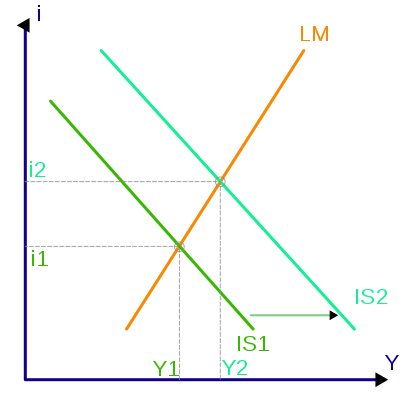

[Insert: IS–LM model, or Hicks–Hansen model, is a two-dimensional macroeconomic tool that shows the relationship between interest rates and assets market (also known as real output in goods and services market plus money market). The intersection of the "investment–saving" (IS) and "liquidity preference–money supply" (LM) curves models "general equilibrium" where supposed simultaneous equilibria occur in both the goods and the asset markets.[1] Yet two equivalent interpretations are possible: first, the IS–LM model explains changes in national income when the price level is fixed in the short-run; second, the IS–LM model shows why an aggregate demand curve can shift.[2] Hence, this tool is sometimes used not only to analyse economic fluctuations but also to suggest potential levels for appropriate stabilisation policies.[3] https://en.wikipedia.org/wiki/IS%E2%80%93LM_model ]

How is the self-correction of an economy to its long-run equilibrium supposed to work? In textbook analysis, the story is that falling prices raise the real money supply, pushing down interest rates, and hence restoring employment.

So how rapidly would we expect this process to work? Let’s take the most favorable assumption, which is that of a constant velocity of money. Under those conditions, holding the money supply fixed would also hold nominal GDP fixed, so that a one percent fall in the price level would raise real output by one percent. The question then is how responsive prices are to the output gap.

Well, Blanchard, Cerutti and Summers .. https://www.imf.org/external/pubs/ft/wp/2015/wp15230.pdf .. have a new paper that estimates an an “anchored expectations” Phillips curve (aka an old-fashioned, pre-Friedman/Phelps curve), and finds the coefficient on unemployment for the US to be about -.25. That’s for unemployment; on output, given Okun’s Law, the coefficient should be only half that. This implies a half-life for output gaps of around 6 years.

[ Okun's Law is an empirically observed relationship between unemployment and losses in a country's production. It predicts that a 1% increase in unemployment will usually be associated with a 2% drop in gross domestic product (GDP). https://www.investopedia.com/terms/o/okunslaw.asp ]

The long run is pretty long, in other words; we might not all be dead, but most of us will be hitting mandatory retirement.

And that’s assuming constant velocity. With interest rates dropping, part of the fall in prices should translate into a fall in velocity rather than a rise in real output, so the implied speed of adjustment should be even lower.

But wait, it gets worse: at the zero lower bound the process doesn’t work at all. In a liquidity trap,

[ A liquidity trap is a contradictory economic situation in which interest rates are very low (e.g., close to 0%) and savings rates are high, rendering monetary policy ineffective. P - First described by economist John Maynard Keynes, during a liquidity trap consumers choose to avoid bonds and keep their funds in cash savings because of the prevailing belief that interest rates could soon rise (which would push bond prices down). Because bonds have an inverse relationship to interest rates, many consumers do not want to hold an asset with a price that is expected to decline. At the same time, central bank efforts to spur economic activity are hampered as they are unable to lower interest rates further to incentivize investors and consumers. https://www.investopedia.com/terms/l/liquiditytrap.asp]

the proposition of a self-correcting economy falls down — in fact, what more flexible prices would do, arguably, is bring on a debt-deflation spiral.

Yes, a sufficiently large price fall could bring about expectations of future inflation — but that’s not the droid we’re looking for mechanism we’re talking about here.

You might ask, given this logic, why actual slumps usually don’t last all that long. The answer is, first, that the shocks causing slumps are often temporary; but second, in practice central banks don’t sit there passively, holding the money supply constant, but in fact push back against slumps with expansionary policy. The economy isn’t self-correcting, at least on a time scale that matters; it relies on Uncle Alan, or Uncle Ben, or Aunt Janet to get back to full employment.

Which brings us back to the liquidity trap, in which the central bank loses most if not all of its traction. Nothing about basic macro models says that there should be a fast return to long-run equilibrium under those conditions, so the failure to see such a fast return is actually a point in favor of the model, not a failure.

Economics 100, was easy. Skip class learn from the textbook more than you felt you did from the ex-American embassy guy .. https://investorshub.advfn.com/boards/read_msg.aspx?message_id=170096630 . My personal cycle in learning it for decades since has been read, understand some, forget most, revisit repeat.

News

News  Market Data

Market Data  Discover

Discover