"THE GOP's BILL IS "A SENSIBLE FRAMEWORK" - BUT "STILL A DEFICIT EXPLODING TAX CUT" FOR THE RICH AND CORPORATIONS"

February 25, 2016 by Nick Shaxson 16 Comments

We’ve mentioned the incidence question several times before, but TJN’s Director John Christensen was at a debate .. https://www.eventbrite.co.uk/e/should-we-call-time-on-corporation-tax-a-seminar-hosted-by-the-appg-on-responsible-tax-tickets-21254715426 .. in London last night on the future of the corporate income tax, alongside Mike Devereux of the Oxford Centre for Business Taxation; Helen Miller of the Institute for Fiscal Studies; Simon Walker of the Institute of Directors, and Margaret Hodge, chair of the UK All Party Parliamentary Group on Tax.

It was a wide-ranging discussion, but one question that came up repeatedly was the question of the ‘incidence’ of the corporate income. Put most crudely, is it corporate shareholders who ultimately shoulder the tax charge, or is it workers? There are a number of people who claim that research demonstrates that the tax charge falls squarely on workers: as a top UK tax official put it .. https://www.gov.uk/government/speeches/speech-by-david-gauke-exchequer-secretary-to-the-treasury-to-the-hundred-group-london :

“The consensus, among economists at least, is that it’s predominantly the employee who foots the bill [for the corporation tax.]”

It is this claim that is the great incidence hoax. There is no such consensus: and we argue that the opposite is true.

Who pays the corporate income tax? The tax ‘incidence’ hoax

Some politicians and pundits like to claim that the burden (or “incidence”) of corporate taxes falls mainly on workers – implying that the corporate tax is a bad, regressive tax that strikes the poor hardest.

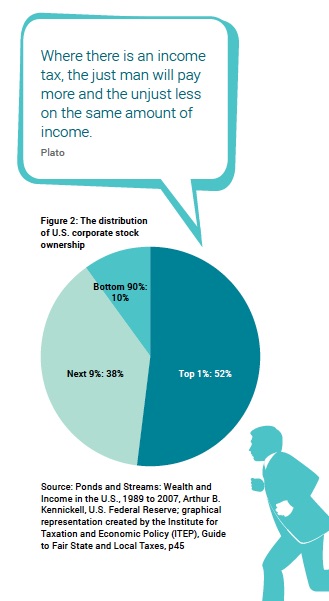

-- “Most, if not all, of the corporate income tax is borne by shareholders in the form of reduced stock dividends, and high-income Americans receive the lion’s share of these dividends.” Citizens for Tax Justice, Washington, D.C, 201321 --

This is quite untrue – as one leading US economist puts it, ‘there is simply no persuasive evidence of a link between corporate taxation and wages’. But the argument is commonly made so it is worth addressing here, in theory and in practice.

First, the theory. Those who claim that the burden falls not on owners/shareholders but on ‘workers’ need to answer the questions below.

* Do they seriously believe that corporate bosses, in this era of weak collective bargaining, would voluntarily pass the benefits of a tax cut onto their workers, instead of feeding the share price and their own stock options? All the evidence points the other way.

* Corporate bosses always behave as if tax burdens fall on shareholders. Would they spend so much time and energy finding clever ways to dodge tax if they believed that taxes didn’t fall ultimately on their shareholders, to whom they are accountable?

* If corporate taxes don’t fall on shareholders, then why do shareholders and investment intermediaries behave as if they do? It is easy to demonstrate that share prices respond strongly to sudden unexpected changes in expected corporate tax bills.

* Corporations are sitting on oceans of idle cash, as Section explains. Wages are stagnant in many countries: when, exactly, are corporate bosses planning to pass these idle cash hoards on to “workers?” And how would tax cuts change their behaviour?

* If wage rates are set in labour markets, as classical theories suggest, then why would companies change their pay policies by ignoring labour markets and instead responding directly to corporate tax changes? Why haven’t they paid them more already?

* Why do the proponents of tax cuts focus only on the narrow issue of labour anyway? The fact that corporation taxes fall (as they do) on different groups in different ways is only a first step in exploring the distributional implications of these taxes. This should instead be viewed in the context of broader society: do or can corporation taxes make the whole tax system more progressive?

* Who are the “workers” on whom these corporate taxes fall, anyway? If it’s a profitable capital-intensive firm with a small wage bill and high returns to capital, it will be mathematically impossible for anything more than a small slice of the tax burden to fall on ‘workers.’ If it’s a hedge fund, or a single-person shell company set up as a vehicle to help its owner avoid tax, then if there is a portion of the corporate tax charge that falls on ‘workers,’ then it would make the system more progressive overall anyway. If it is highly paid bankers, then corporate taxes will curb the wealth-extracting bonus culture that has fostered widespread risk-taking at taxpayers’ expense.

* Many of the ‘incidence’ arguments rest on the idea that corporate taxes scare away ‘investment.’ But as Section 3.3 explains, tax-sensitive investment is by definition the least useful stuff: accounting nonsense and papershuffling that does not involve very much employment creation at all.

* If corporate taxes force wages down, doesn’t this sit uncomfortably with the fact that effective corporate tax rates have fallen steadily in most countries of the world since the 1980s (see the Introduction), but wages have fallen too, while corporate profits have soared?

* Tax cuts increase the economic resources of corporations. Corporate bosses manage those resources, so tax cuts increase the powers of corporate bosses. Leaving aside the economic arguments, how could corporate tax cuts not boost political inequalities? Now consider how all this plays out internationally. Will tax rises choke off foreign investment, hurting workers? Consider an African oilfield or a gasfield in Australia. A corporate tax won’t scare away the oil company: they will go where the oil is, not where the tax breaks are. This is true of many profitable investment opportunities: an Indian telecommunications licence, say, or a supermarket franchise in Turkey. These are all largely immobile, rooted in the local economy, and won’t flee if taxed. And those relatively few that do, in a world awash with idle corporate capital looking for investment returns (Section 7), will generally be replaced soon enough.

And now, the evidence

On the evidence side, all the lobbying and corporate opinion wielded in support of the proposition that the corporate tax burden largely falls on workers has muddied the debate. Yet as the footnote here .. http://www.taxjustice.net/wp-content/uploads/2013/04/Ten_Reasons_Full_Report.pdf .. shows, numerous independent bodies have concluded after exhaustive studies that the burden largely falls on the owners of capital — that is, predominantly wealthy people.

In short, the corporate tax falls largely on wealthy capital owners. It is a powerful and precious vehicle for reducing inequality, within and between countries. Given the role that corporate taxes play in curbing economic inequalities, and the growing literature highlighting the fact that higher inequality tends to cause lower economic growth, there is a plausible case for suggesting that corporate tax cuts may hurt economic growth.

The key footnote from the last section is this (FN 24):

The idea that the corporate tax could fall on workers stems partly from the idea that in an open economy, the corporate tax will scare away investment, thus hurting workers. But this does not hold up in the evidence, particularly in larger economies. See, for instance,

Distribution of Household Income and Federal Taxes, U.S. Congressional Budget Office, 2012, p16, which works on the basis that 75 percent of the burden of the corporate tax falls on capital.

Also see Corporate Tax Incidence: Review of General Equilibrium Estimates and Analysis, U.S. CBO, May 2012, Jennifer C. Gravelle, highlighting models that either find “capital bears the majority of the corporate tax burden” or that “even in an open economy, capital could bear virtually the entire tax burden and that the open-economy assumption is not sufficient to shift the burden of the corporate tax from capital to labor.”

Gravelle, Jane G. and Kent A. Smetters. 2006. “Does the Open Economy Assumption Really Mean That Labor Bears the Burden of a Capital Income Tax.” Advances in Economic Analysis & Policy vol. 6:1.

Also see In search of corporate tax incidence, Kimberley A. Clausing, Tax Law Review, 2012 (“there is simply no clear and persuasive evidence of a link between corporate taxation and wages.”)

See also How the TPC distributes the corporate income tax, Urban Institute and Urban-Brookings Tax Policy Center, Sept 13, 2012, which finds that 80 percent of the burden falls on capital.

The U.S. Treasury uses a rate of 82 percent: see Distributing the Corporate Income Tax: Revised U.S. Treasury Methodology, May 17, 2012. Higher corporate cash piles in recent years presumably will shift the burder still further away from workers.

See also Sharing the Burden: Empirical Evidence on Corporate Tax Incidence, Nadja Dwenger, Pia Rattenhuber, Viktor Steiner, Max Planck Institute for Tax Law and Public Finance, Working Paper 2011 – 14 October 2011, which finds empirically that labour bears 19-29 percent of the burden of the corporate income tax. In small countries and tax havens, tax rates will have more impact on wages, but even then — and this applies to large as well as small countries — these effects, such as they are, will disproportionately impact the skilled, highly remunerated professions such as accountancy and law firms, meaning that tax cuts will tend to increase inequality.

News

News  Market Data

Market Data  Discover

Discover