Suppose we entered into a December 2012 futures contract, today, for $100. Now go forward one month. The same December 2012 future contract could still be $100, but it might also have increased to $110 (this implies normal backwardation) or it might have decreased to $90 (implies contango). The definitions are as follows:

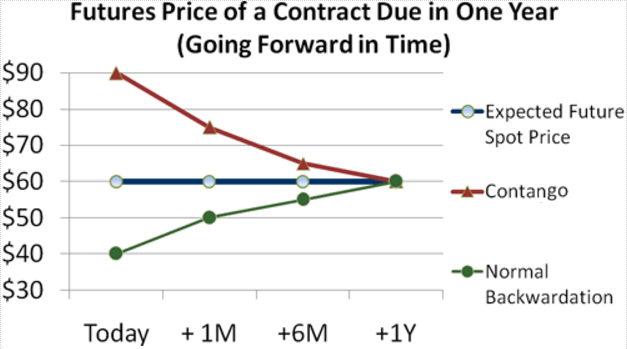

Contango is when the futures price is above the expected future spot price. Because the futures price must converge on the expected future spot price, contango implies that futures prices are falling over time as new information brings them into line with the expected future spot price......(weather could affect future spot price bringing it down because of lack of demand for future ng needs) Normal backwardation is when the futures price is below the expected future spot price. This is desirable for speculators who are "net long" in their positions: they want the futures price to increase. So, normal backwardation is when the futures prices are increasing. Consider a futures contract that we purchase today, due in exactly one year. Assume the expected future spot price is $60 (see the blue flat line in Figure 2 below). If today's cost for the one-year futures contract is $90 (the red line), the futures price is above the expected future spot price. This is a contango scenario. Unless the expected future spot price changes, the contract price must drop. If we go forward in time one month, note that we will be referring to an 11-month contract; in six months, it will be a six-month contract.

News

News  Market Data

Market Data  Discover

Discover