Simple: the contraction of the economy after the 2008 crisis.

I've really grown tired of this simplistic explanation, especially because it doesn't agree with the facts of the market the product is meant to serve.

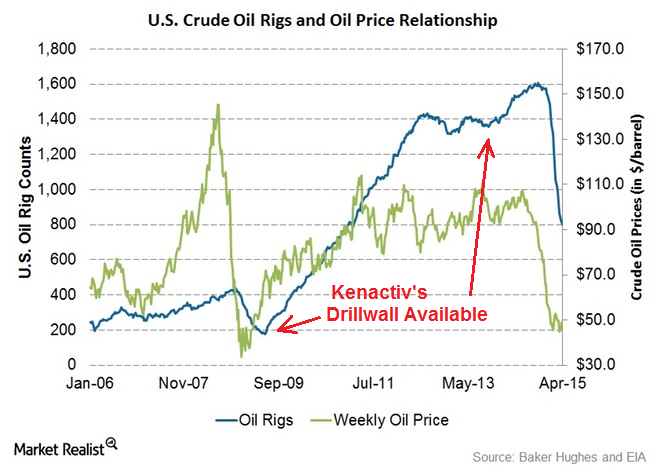

Between 2009 and 2013 (Kenactiv bankruptcy Oct, 2013,) the number of U.S. Oil Rigs increased from approximately 2009 to roughly 1400, a 600% increase:

By early-2010, the number of oil rigs equaled the 400 rigs from before the recession, and the number tripled from there, yet Kenactiv was still showing large losses in 2013.

Now, with $30 oil and the the February, 2016 rig data from Baker-Hughes (also the data source in the chart above) showing 571 U.S. rigs, why should we expect HEMP to do any better using the same people to sell the same products?

One final question:

If the Drillwall and Kenaf were such great products, why didn't anyone outbid Perlowin for the equipment and also make the winning bid on the land and building? After just a little maintenance, they would have had a fully operational plant by mid-2014 manufacturing fiber and Drillwall with another year or so of sales before the oil market crashed, but while the rest of the economy was slowly improving.

News

News  Market Data

Market Data  Discover

Discover