Saturday, February 10, 2024 3:57:04 AM

However, I remind you that we are here to legalize every action if possible, to avoid do-overs, knowing that the conservator has the Incidental Power: "Zing!" that allows it to twist or unwind everything that has been done.

Primarily because this is what they really had in mind (Separate Account. July 20, 2011 CFR 1237.12 for a follow-on plan: Recap. "It supplements"). For instance, the capital distributions that went through, despite being restricted, are applied towards the exceptions in the law/CFR (Reduce the SPS/Recap).

Something that can't be done with the Securities Law violations, for which we request a monetary settlement.

In this case, because both handouts are related to the Funding Commitment with SPS (don't call it "credit line" but "financing line of their operations" as per the Charter dynamics and as a last resort -Section Purposes-. Captured in the SPSPA with "upon Capital Deficiency", that is, upon negative Net Worth) and, taking into consideration that the 2nd UST backup of FnF in the Charter Act inserted by HERA, allows an infinite dividend rate on SPS, it can be argued that the Warrant and the initial $1B SPS were a higher compensation on the SPS and not an "entry fee", primarily because FnF are entitled to tap the UST for funds as a last resort, without any shame.

So, no "entry fees" necessary.

This allows them to remain outstanding. Then, when talking about whether they will be eventually executed or monetized:

-Both securities were issued for free and thus, their value was debited from the shareholders' pockets (Additional Paid-In Capital account), which reduced the Core Capital. A breach of the conservator's Rehab power. Then, all part of its "Zing!" power.

-The rates originally set forth in the UST backup of FnF subsection (c) in Fannie Mae, prevail. Estimated at a weighted-average 1.8% cumulative dividend rate on SPS until they were fully repaid, estimated in Dec 2013 and Dec 2014, respectively (Separate Account). Then, "Zing!".

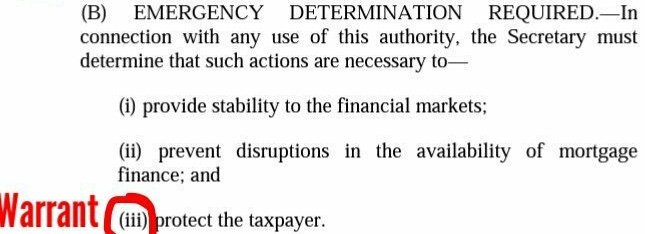

-The Warrant was issued for free to skip the prerequisite (iii) on purchases in the UST's authority in the Charter Act: "to protect the taxpayer", that is, a collateral of its investment in SPS.

The trick to make the UST get a compensation worth a 79.9% stake in FnF, for only $0.00001 per share, either as "entry fee" or a higher yield on SPS, was declared "gross" and snubbed. Then, the security Warrant is considered to have been purchased at a $0 cost, in order to make this security be subject to the aforementioned prerequisite of "collateral".

-Let alone the Warrant prospectus clause 7: non-trasferable, that can be assigned (transferred) to any Person in the clause 2.1, because "the right the receive shares" that is what can be "assigned", is the security Warrant itself.

Two confronting clauses make it void to all effects.

FEATURED ZenaTech, Inc. (NASDAQ: ZENA) Launchs IQ Nano Drone for Commercial Indoor Use • Oct 10, 2024 8:09 AM

FEATURED CBD Life Sciences Inc. (CBDL) Targets Alibaba as the Next Retail Giant for Wholesale Expansion of Top-Selling CBD Products • Oct 10, 2024 8:00 AM

Foremost Lithium Announces Option Agreement with Denison on 10 Uranium Projects Spanning over 330,000 Acres in the Athabasca Basin, Saskatchewan • FAT • Oct 10, 2024 5:51 AM

Element79 Gold Corp. Reports Significant Progress in Community Relations and Development Efforts in Chachas, Peru • ELEM • Oct 9, 2024 10:30 AM

Unitronix Corp Launches Share Buyback Initiative • UTRX • Oct 9, 2024 9:10 AM

BASANITE INDUSTRIES, LLC RECEIVES U.S. PATENT FOR ITS BASAFLEX™ BASALT FIBER COMPOSITE REBAR AND METHOD OF MANUFACTURING • BASA • Oct 9, 2024 7:30 AM