Friday, February 09, 2024 1:59:07 AM

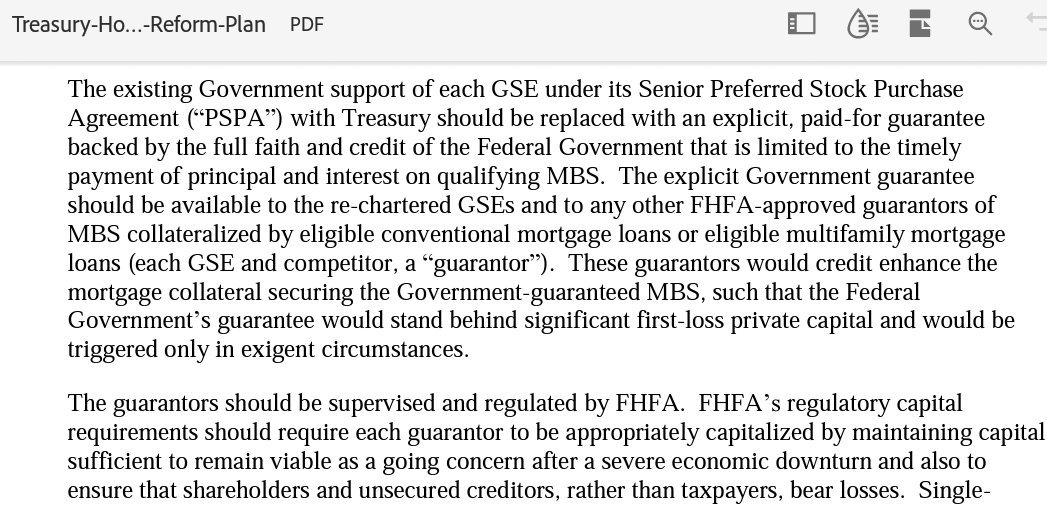

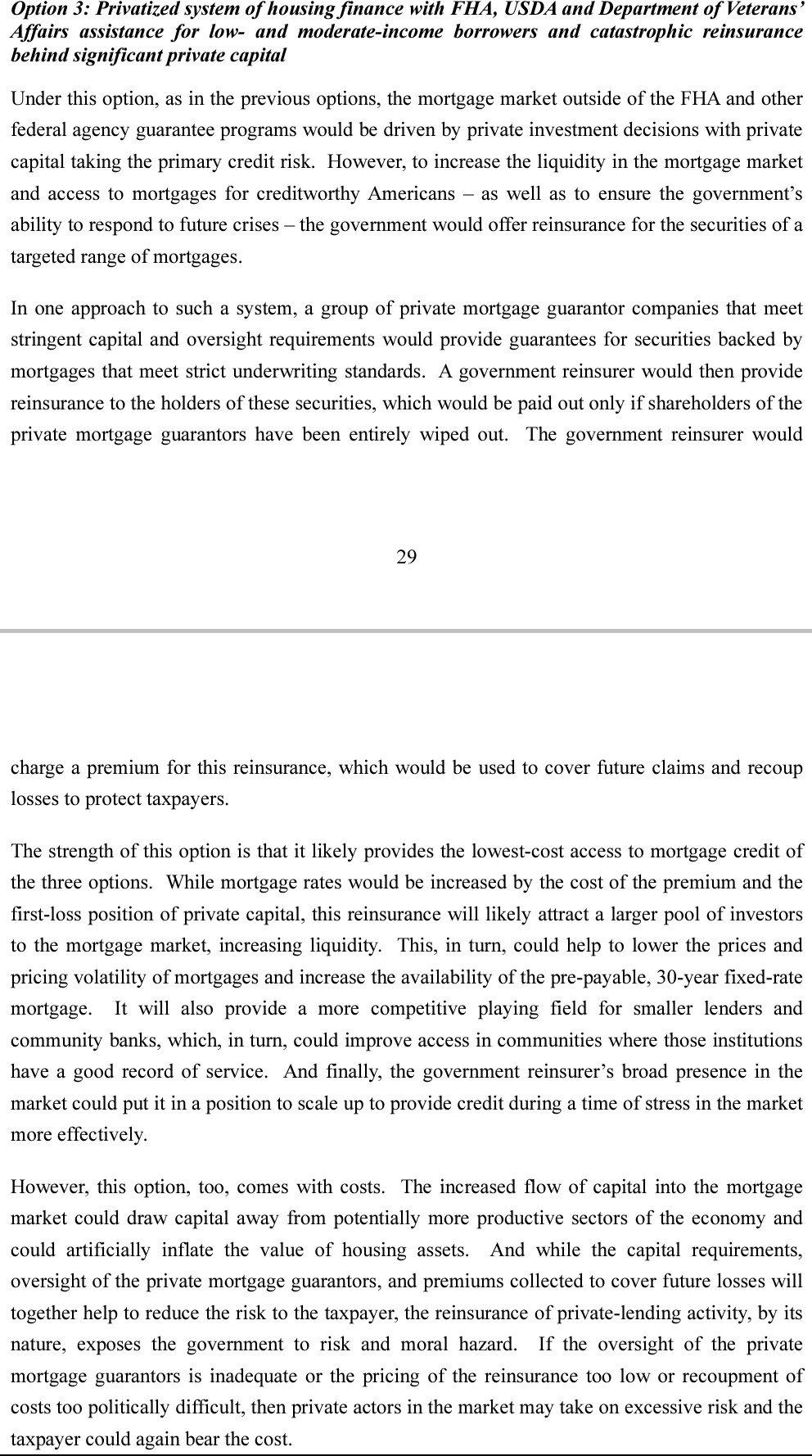

This has nothing to do with the Government Catastrophic-Loss Reinsurance in a Privatized Housing Finance System, option 3 out of the 3 options chosen by the Treasury for the release from Conservatorship in a 2011 Report to Congress, at the request of the Wall Street Reform and Consumer Protection Act (Dodd-Frank law).

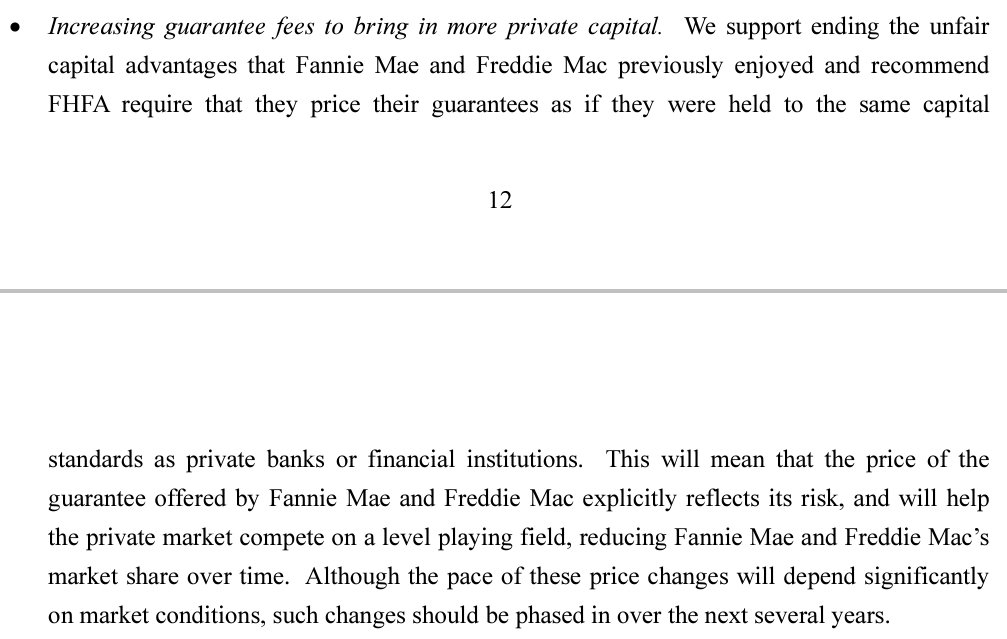

At the time, the Treasury recommended guarantee fee increases to remove their advantages in capital standards (the so called Basel framework for capital requirements, now in place for FnF)

DeMarco began to work on it right away (May 2011)

UMBS, CSP,...

And the latest, their commingled securities unveiled on June 2022 for this Government Castastrophic-Loss Reinsurance (resecuritizations), suitable for private reinsurance as well (Source). We can read in the Freddie Mac press release that it was first priced at 50 bps because the FHFA was thinking of the China-sponsored plan submitted by Trump/Mnuchin, but just a few days later it was changed for 9.375 bps to reflect the Privatized Housing Finance System FnF were bound for.

This reinsurance was not meant to make FnF reinsure each other's UMBS as we can see today, with one using the UMBS of the other guarantor inside its own UMBS. A shameful attempt to syphon off revenues from Freddie Mac to Fannie Mae and make up for its losses in the sale of unvervalued assets to Goldman Sachs and Co.

This way, the CEO of Fannie Mae doesn't have to worry about competing with Freddie Mac, if the extortion of money from Freddie Mac goes on (Currently $105B, net, at 9.375 bps), as shown in the data of monthly volume in Fannie Mae with two consecutive months of month-on-month declines, versus the strong growth posted by Freddie Mac. This is because these Resecuritizations don't appear in their Guarantee Portfolios.

Obviously the commingled securities are meant to bring in private capital in the Guaranty Mortgage Securitization Market, to help new guarantors sell their products, at least initially.

We have other examples of attempt to supplant the law in force, like recently the representative from Tennessee, Mr. Ogles, introducing in Congress this bill:

H.R. 5549 (IH) - End of GSE Conservatorship Preparation Act of 2023.

To require the Secretary of the Treasury to submit to the Congress completed proposals for the termination of the conservatorships of Fannie Mae and Freddie Mac, and for other purposes.

More detail about representative Davidson's remark. What better way to supplant the law in force, than calling the SPSPA amendment where Mnuchin required to the Treasury a report on September 2021 "a statutory requirement"..."it's the law".

Can you imagine the Goldman Sachs alumni Mnuchin and Calabria, enacting laws sat at a table?

Rep.Davidson again asks UST for a report to Congress due Sept 2021, required by Mnuchin/Calabria (Jan 2021 SPSPA amndt)

— Conservatives against Trump (@CarlosVignote) February 8, 2024

"A statutory requirement...The law"(False)

The report for the release was submitted on Feb2011, at the request of the Dodd-Frank law.#Fanniegate @TheJusticeDept https://t.co/VU9tmWGRGx pic.twitter.com/izcTR4YYCE

Avant Technologies Engages Wired4Tech to Evaluate the Performance of Next Generation AI Server Technology • AVAI • May 23, 2024 8:00 AM

Branded Legacy, Inc. Unveils Collaboration with Celebrity Tattoo Artist Kat Tat for New Tattoo Aftercare Product • BLEG • May 22, 2024 8:30 AM

"Defo's Morning Briefing" Set to Debut for "GreenliteTV" • GRNL • May 21, 2024 2:28 PM

North Bay Resources Announces 50/50 JV at Fran Gold Project, British Columbia; Initiates NI 43-101 Resources Estimate and Bulk Sample • NBRI • May 21, 2024 9:07 AM

Greenlite Ventures Inks Deal to Acquire No Limit Technology • GRNL • May 17, 2024 3:00 PM

Music Licensing, Inc. (OTC: SONG) Subsidiary Pro Music Rights Secures Final Judgment of $114,081.30 USD, Demonstrating Strength of Licensing Agreements • SONGD • May 17, 2024 11:00 AM