Tuesday, February 01, 2022 8:54:14 AM

Morning Markets. . . .

.

.

.

.

Futures Reverse Gains As Nail-biting Volatility Enters February

by Tyler Durden

Tuesday, Feb 01, 2022 - 07:50 AM

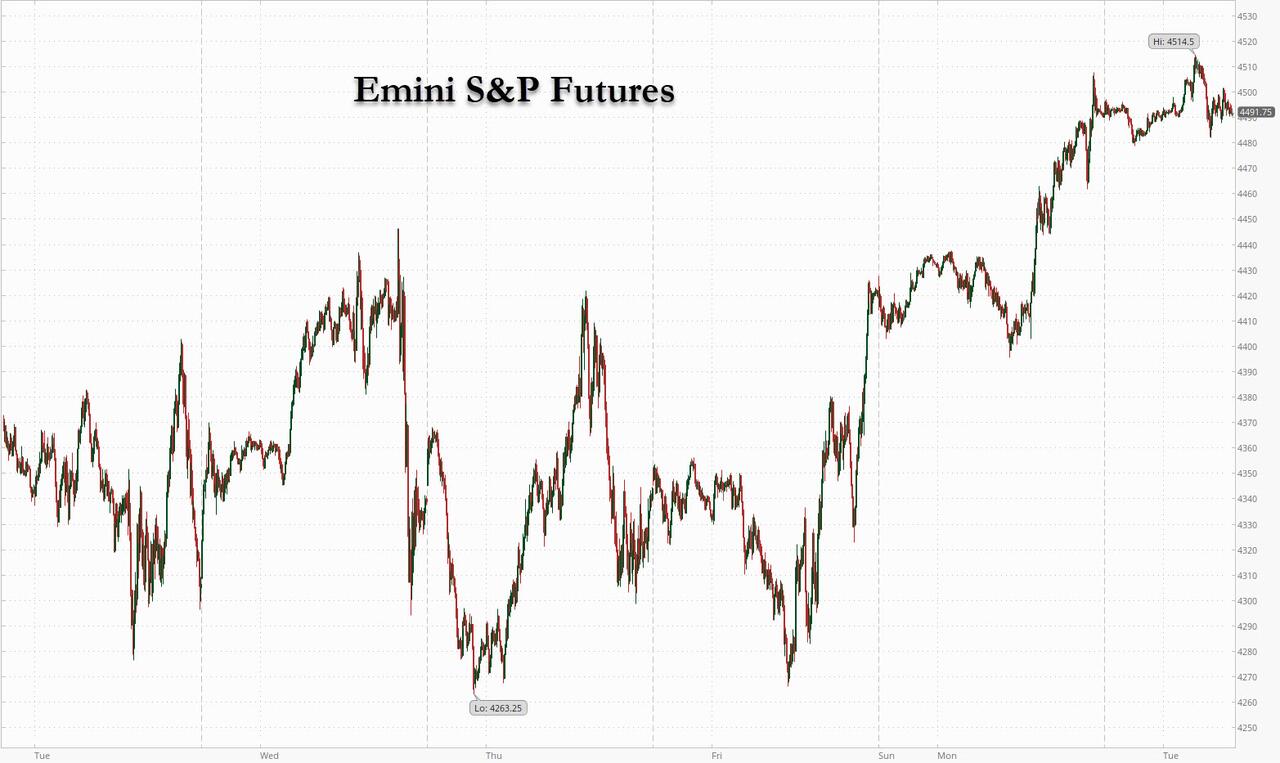

World stocks began the new month on firmer ground, after a volatile January, as reassuring comments from Federal Reserve officials helped to calm rate-hike jitters even though US futures failed to extend recent gains. After closing out January with a furious two-day, dip-buying meltup thanks to a flood of inbound month-end rebalancing, US index futures briefly traded through Monday’s highs, backed by decent rally in European equities where financials outperformed, boosted by solid UBS earnings, before dipping lower as the volatility seen in past days lingered. At 7:00am ET, emini S&P futures traded 0.23%, or 10.5 points lower, Nasdaq futures were also red, some 31 points or 0.15% lower, and Dow futures dropped 0.2% as investors weighed cautious rate-hike commentary from Fed officials and awaited earnings from firms including Alphabet and General Motors. Treasuries climbed and the dollar weakened. Oil fell, but held close to seven-year highs.

Videogame makers were in focus after Sony said it will buy Bungie, the developer behind the popular Destiny and Halo game franchises, for $3.6 billion. In another busy day ahead for earnings, AMD rose in premarket trading amid expectations its results Tuesday will show market-share gains. Other notable premarket movers:

UPS (UPS US) rose 7.3% premarket as the postal firm benefited from higher prices and rising holiday deliveries to post profit that beat analyst estimates.

Spire (SPIR US) shares gain as much as 27% in premarket trading after the satellite-imaging and data company released preliminary 4Q numbers ahead of analysts’ targets and guided toward higher 2022 revenue.

Harley-Davidson (HOG US) shares have valuation support at current levels, while the market appears to be pricing in an overly negative outlook, Morgan Stanley writes, upgrading stock to equal-weight. Shares up 0.8% premarket.

Knightscope (KSCP US) declines 14% in premarket trading, set to come down from a high reached on Monday as retail investors piled into the security-camera and robotics company, tripping two trading halts along the way.

Earnings season has provided a healthy breadth of beats so far: of the 182 companies in the S&P 500 that have reported earnings so far this season, more than 82% have beaten or met,

“Investors continue to buy the dips almost everywhere this week, with market sentiment boosted by a strong earning season so far where most companies have beaten expectations,” says Pierre Veyret, technical analyst at ActivTrades. “Technically speaking, most indices have registered solid rebounds over major support zones and are now challenging key resistance levels.”

In a jawboning fest on monday, four Fed officials said they’ll back interest-rate increases at a pace that doesn’t disrupt the economy, calming markets unnerved by previous hawkish messages from the central bank. Investors are now debating whether the rally that pared the worst monthly rout in the S&P 500 since March 2020 will continue. They are also focusing on earnings releases to gauge the strength of the economic recovery.

“Good news is that some Fed officials are finally out trying to soothe investors’ nerves saying that they still want to avoid unnecessarily disrupting the U.S. economy,” Ipek Ozkardeskaya, a senior analyst at Swissquote, wrote in a note. “But what will really make the difference is the quantitative tightening and given the steep rise in Fed’s balance sheet since March 2020, even halting the growth would be an abrupt change.”

In Europe, the Stoxx Europe 600 Index rose 1%, led by financial services and basic-resource stocks. UBS shares surged 6% after the lender beat estimates. Telecoms were the only industry group in red. European tech stocks rallied again, with the Stoxx Tech Index rising as much as 2.1%, among the top-performing sectoral gauge in Europe. Sector added to 3.5% gain Monday, lifted higher by overnight rally in the U.S., with the Nasdaq 100 Index +3.4%. Semiconductor makers and pandemic winners lead gains, with BE Semi +4.5%, Deliveroo +3%, ASMI +2.8%, ASML +2.6% and Just Eat Takeaway.com +2.8%. Here are some of the biggest European movers today:

UBS shares gained as much as 7.5% in early European trading, the biggest intraday gain since April 2020, after the Swiss lender posted largely better-than-expected results and analysts cheered the new financial targets.

HeidelbergCement shares rise as much as 4.7% after the company reported preliminary 4Q revenue that Stifel analyst Tobias Woerner says was “reassuring.”

Faurecia shares rise as much as 4.4% as the shares resume trading after being suspended all of Monday ahead of the closing of the Hella acquisition. The deal is a key milestone that allows the French auto parts firm to start implementing synergies, says Citi analyst Gabriel Adler (buy).

Ubisoft shares rise as much as 3.7% in positive readacross after Sony said it will buy U.S. video game developer Bungie for $3.6b. The acquisition indicates the sector is consolidating, says Citi (buy).

Hexagon shares soar as much as 23%, the most since 2009, after it signs deal with a commercial truck maker to provide battery packs for electric heavy-duty vehicles.

Shares in U.K. clothing retailer Joules plunge as much as 34%, to the lowest since April 2020, after reporting that revenue and profit before tax for the 9 weeks to Jan. 30 fell short of the board’s expectations.

Saipem falls as much as 15%, extending Monday’s 30% plunge, as brokers including Mediobanca downgrade the oil drilling specialist after it warned on 2021 earnings and said it would hold discussions with creditors and shareholders for financing.

Earlier in the session, Asian stocks rose as the latest remarks from Federal Reserve officials helped ease fears of aggressive U.S. monetary tightening. The MSCI Asia Pacific Index added as much as 0.5%, with the information-technology and financial sectors providing the biggest boosts. Japan’s Keyence and Murata Manufacturing contributed most to the advance, with both releasing quarterly earnings results after market closed in Tokyo. Equity gauges in New Zealand and India led gains, with many markets in the rest of Asia shut for holidays. China, Hong Kong, South Korea, Singapore and Taiwan were among bourses closed for the Lunar New Year break. “Now that markets are finding calm, buying is kicking into individual stocks of companies that have reported solid earnings or are expected to,” said Shogo Maekawa, a strategist at JP Morgan Asset Management in Tokyo. Asian shares may extend gains if U.S. data this week on employment and ISM manufacturing don’t rattle the market, Maekawa added. Fed officials said they want to avoid unnecessarily disrupting the economy as they prepare to start raising rates, mitigating market concern over a 50 basis-point move in March. “You always want to go gradually,” Kansas City Fed President Esther George told the Economic Club of Indiana. Asia’s stock benchmark fell 4.4% in January, its biggest such drop since July, hit by concern that faster-than-expected U.S. rate hikes will cool the global economic recovery.

Japanese stocks pared large morning gains, with the Topix finishing little changed, as automakers slid. Chemical and machinery makers also dragged on the Topix, which wiped out a gain of as much as 1.3%. The Nikkei closed 0.3% higher, paring a 1.5% advance, with TDK and Shionogi the biggest boosts. Both gauges had risen about 3% over the previous two sessions. “There’s a lot of tussle between buyers and sellers due to month-end and month-start trading,” said Hiroshi Namioka, chief strategist at T&D Asset Management. “Shares of companies with robust earnings are being bought, but those without any specific leads to go on seem to be exposed to selling pressure.”

Indian stocks rose after the annual federal budget pledged to step up spending in a bid to support a business recovery in Asia’s third-largest economy. The S&P BSE Sensex climbed 1.5%, its biggest advance in a month, to 58,862.57 in Mumbai. The NSE Nifty 50 Index rose 1.4%. Fifteen of the 19 sector indexes compiled by BSE Ltd. rose, led by a gauge of metal stocks that jumped the most in six months. Finance Minister Nirmala Sitharaman’s strong push for infrastructure-led growth and investment centered around sectors like railways, roadways, logistics and energy will benefit most metal companies, according to Priyesh Ruparelia, a vice president at ICRA Ltd. A measure of capital goods companies also jumped the most in a year. The nation plans to boost capital spending by 35% to 7.5 trillion rupees ($100 billion) in the next financial year that starts in April in a bid to sustain a recovery in growth disrupted by the pandemic. “With growth-oriented focus intact in the budget, we expect economic and capital market buoyancy to remain,” said Vijay Chandok, managing director at ICICI Securities Ltd.

Waves of volatility have swept across markets after the Fed signaled swifter monetary-policy tightening to curb inflation than many had expected. Investors need to “get used to this up and down volatility” as there’ll likely be more of it, Nancy Davis, chief investment officer at Quadratic Capital Management, said on Bloomberg Television.

In rates, Treasuries bull flattened as spreads unwound a portion of Monday’s steepening move with yields richer by up to 3.5bp across long-end of the curve. US Treasury yields were richer by 2bp to 3.5bp across the curve with 2s10s, 5s30s spreads both flatter by almost 1bp each; 10-year yields around 1.75%, with bunds lagging by 1.5bp and gilts outperforming by 1bp in the sector. In European bonds, focus remains on the front-end of the curve as rate hike premium continues to build -- German 2-year yields are cheaper by almost 4bp on the day, trading above the European Central Bank’s deposit rate for the first time since 2015. Gilts outperform in early London session. IG dollar issuance slate includes Kommuninvest $1b 2Y SOFR; two companies priced $1.8b Monday as sales activity continues to drop off in volatile backdrop.

In FX, Bloomberg Dollar Spot index falls 0.3%. NOK, CHF and SEK outperform in G-10, CAD and euro lag. The Bloomberg Dollar Spot Index slumped as the greenback weakened against all of its Group-of-10 peers. Gains were led by the Swiss franc, which advanced a second day as it rebounded after adverse month-end flows; Scandinavian currencies were also among the top gainers amid supportive risk sentiment. The euro headed for a third day of gains, boosted by an unwind of the latest rally for downside exposure through options; the common currency rose by as much as 0.3% to 1.1269, raising questions on whether its latest weakness was more down to month-end flows rather than hawkish Fed bets. French inflation rose 3.3% from a year earlier in January, a sharper gain than the 2.9% economists estimated following December’s 3.4% advance. The pound rallied against a broadly weaker dollar, with domestic focus remaining on the Bank of England’s meeting this week. Figures showed U.K. house prices registered their strongest start to the year since 2005, before mortgage data due later Tuesday. The Aussie reversed an earlier loss after the RBA said it’s ready to be patient on interest rates even as it ceased its bond-purchase program. Overnight- indexed swaps continued to price in four rate hikes by the central bank this year. The Kiwi also advanced, in part on purchases against Aussie post RBA. Japan’s bonds extended a decline to a fourth day amid growing speculation that the central bank will step in to slow a rise in yields. The yen gained for third day.

Crypto markets were varied in which Bitcoin traded sideways around 38.5k and Ethereum gained over 2%.

In commodities, crude futures fade a sharp drop. WTI finds support near $87 before recovering back on to a $88-handle. Brent trades flat near $89.20. Most base metals trade in the green; LME nickel rises 1.3%, outperforming peers, LME lead and tin lags. Spot gold rises roughly $10 to trade near $1,807/oz

U.S. economic data slate includes January Markit manufacturing PMI (9:45am), ISM manufacturing, December construction spending and JOLTS job openings (10am); while AMD, Alphabet, Electronic Arts, Exxon, General Motors, Gilead, PayPal, Stanley Black & Decker, Starbucks and UPS are among companies reporting results.

Market Snapshot

S&P 500 futures down 0.3% to 4,490.00

STOXX Europe 600 up 0.8% to 472.72

MXAP up 0.4% to 185.38

MXAPJ up 0.3% to 606.58

Nikkei up 0.3% to 27,078.48

Topix little changed at 1,896.06

Hang Seng Index up 1.1% to 23,802.26

Shanghai Composite down 1.0% to 3,361.44

Sensex up 1.3% to 58,793.71

Australia S&P/ASX 200 up 0.5% to 7,006.04

Kospi up 1.9% to 2,663.34

Brent Futures down 0.9% to $88.45/bbl

Gold spot up 0.5% to $1,805.93

U.S. Dollar Index down 0.16% to 96.38

German 10Y yield little changed at -0.01%

Euro up 0.2% to $1.1258

Brent Futures down 0.9% to $88.45/bbl

Top Overnight News from Bloomberg

Money markets are wagering on the BOE raising rates five times by 25 basis points and a move of that magnitude from the ECB by December. That spurred a renewed selloff in bonds across the continent on Monday, and challenges ECB policy makers including President Christine Lagarde who have pushed back against the idea of raising borrowing costs this year

Euro-area manufacturers are taking a more aggressive approach to price setting -- another signal that inflation won’t slow quickly after stronger- than-expected readings from the region’s biggest economies. Output prices rose at the second-fastest rate on record in January, according to a survey of purchasing managers by IHS Markit released Tuesday. While there were some signs of supply- chain problems easing, robust demand allowed firms to pass on higher costs to customers

German joblessness fell at a much faster pace than anticipated in January as the economy comes to terms with coronavirus curbs to contain surging infections. Unemployment in Europe’s largest economy declined by 48,000, pushing the jobless rate down to 5.1%. Economists had forecast a drop of just 6,000

A more detailed look at global markets courtesy of Newsquawk

Asian stocks were positive but with upside limited amid mass holiday closures for the Lunar New Year. ASX 200 (+0.5%) rose above 7,000 with the index further underpinned as the RBA stuck to a dovish tone. Nikkei 225 (+0.3%) was kept afloat after lower unemployment although retraced gains as JPY strengthened. Nifty 50 (+1.4%) outperformed as focus in India centred on earnings and the budget announcement.

Top Asian News

Europe Is Losing Nuclear Power Just When It Really Needs Energy

Winners and Losers in India’s Budget Aiming to Bolster Growth

Widespread Bullying, Harassment Detailed in Rio Tinto Report

India Plans Record Borrowing to Fund Modi’s Growth Ambitions

European bourses are firmer taking impetus from the holiday-thinned APAC handover and Monday's US close; albeit, benchmarks are off best levels, Euro Stoxx 50 +1.0%. Sectors are all in the green though Telecom lags while Basic Resources, Banks and Tech do well amid base metals, UBS (+7.0%) earnings and the NQ/NXPI read-across respectively. Stateside, US futures are relatively contained but have moved directionally with European peers, the NQ remains the current modest outperformer.

Top European News

U.K. Mortgage Approvals Rise to 71k in Dec. Vs. Est. 66k

Slovenia Mulls Law on Swiss-Franc Loans Slammed by Lenders, ECB

Europe Is Losing Nuclear Power Just When It Really Needs Energy

Putin Meets Orban Amid Diplomatic Flurry: Ukraine Update

In FX, DXY sheds more Fed rate hike premium and month end rebalancing momentum. Franc rebounds firmly as yields recede and SNB President Jordan sets sights on keeping track of inflation. Sterling underpinned by risk appetite and firm UK macro releases. Kiwi turns table on Aussie after encouraging NZ trade data and RBA pledges patience on tightening after confirming removal of QE. Rouble on front foot ahead of call between Russia’s Foreign Minister Lavrov and US Secretary of State Blinken, but Lira lurching after Turkey’s manufacturing PMI slows to the brink of stagnation. BoJ is under less pressure to shift yield target than market thinks, sources cited by Reuters say. Sources say the central bank has many tools to combat rising yields; BoJ currently prefers market operations.

In commodities, WTI and Brent are pivoting the mid-point of ~USD 1.50/bbl ranges that have seen a test of yesterday's trough for Brent at worst thus far. Total OPEC+ production was lower by 824k/BPD than the required production in December, via JTC cited by Energy Intel's Bakr; overall compliance in December was 122%. Goldman Sachs, on OPEC+, sees growing potential for a faster ramp-up, given the pace of the recent rally and likely pressures from importing nations. Spot gold/silver are firmer picking up from the pressure seen in recent sessions. Though, gold remains near the USD 1800/oz mark and as such the 200-, 100- & 50-DMAs.

US Event Calendar

9:45am: Jan. Markit US Manufacturing PMI, est. 55.0, prior 55.0

10am: Dec. JOLTs Job Openings, est. 10.3m, prior 10.6m

10am: Dec. Construction Spending MoM, est. 0.6%, prior 0.4%

10am: Jan. ISM Manufacturing, est. 57.5, prior 58.7, revised 58.8

10am: Jan. ISM Employment, est. 53.0, prior 54.2, revised 53.9

10am: Jan. ISM New Orders, est. 58.0, prior 60.4, revised 61.0

10am: Jan. ISM Prices Paid, est. 67.0, prior 68.2

.............

Have a Great Day

Weird-looking cat Wilfred goes viral with Michael Rapaport voiceover

.

.

.

.

.

.

.

.

.

.

.

. . . .

.

.

.

.

Futures Reverse Gains As Nail-biting Volatility Enters February

by Tyler Durden

Tuesday, Feb 01, 2022 - 07:50 AM

World stocks began the new month on firmer ground, after a volatile January, as reassuring comments from Federal Reserve officials helped to calm rate-hike jitters even though US futures failed to extend recent gains. After closing out January with a furious two-day, dip-buying meltup thanks to a flood of inbound month-end rebalancing, US index futures briefly traded through Monday’s highs, backed by decent rally in European equities where financials outperformed, boosted by solid UBS earnings, before dipping lower as the volatility seen in past days lingered. At 7:00am ET, emini S&P futures traded 0.23%, or 10.5 points lower, Nasdaq futures were also red, some 31 points or 0.15% lower, and Dow futures dropped 0.2% as investors weighed cautious rate-hike commentary from Fed officials and awaited earnings from firms including Alphabet and General Motors. Treasuries climbed and the dollar weakened. Oil fell, but held close to seven-year highs.

Videogame makers were in focus after Sony said it will buy Bungie, the developer behind the popular Destiny and Halo game franchises, for $3.6 billion. In another busy day ahead for earnings, AMD rose in premarket trading amid expectations its results Tuesday will show market-share gains. Other notable premarket movers:

UPS (UPS US) rose 7.3% premarket as the postal firm benefited from higher prices and rising holiday deliveries to post profit that beat analyst estimates.

Spire (SPIR US) shares gain as much as 27% in premarket trading after the satellite-imaging and data company released preliminary 4Q numbers ahead of analysts’ targets and guided toward higher 2022 revenue.

Harley-Davidson (HOG US) shares have valuation support at current levels, while the market appears to be pricing in an overly negative outlook, Morgan Stanley writes, upgrading stock to equal-weight. Shares up 0.8% premarket.

Knightscope (KSCP US) declines 14% in premarket trading, set to come down from a high reached on Monday as retail investors piled into the security-camera and robotics company, tripping two trading halts along the way.

Earnings season has provided a healthy breadth of beats so far: of the 182 companies in the S&P 500 that have reported earnings so far this season, more than 82% have beaten or met,

“Investors continue to buy the dips almost everywhere this week, with market sentiment boosted by a strong earning season so far where most companies have beaten expectations,” says Pierre Veyret, technical analyst at ActivTrades. “Technically speaking, most indices have registered solid rebounds over major support zones and are now challenging key resistance levels.”

In a jawboning fest on monday, four Fed officials said they’ll back interest-rate increases at a pace that doesn’t disrupt the economy, calming markets unnerved by previous hawkish messages from the central bank. Investors are now debating whether the rally that pared the worst monthly rout in the S&P 500 since March 2020 will continue. They are also focusing on earnings releases to gauge the strength of the economic recovery.

“Good news is that some Fed officials are finally out trying to soothe investors’ nerves saying that they still want to avoid unnecessarily disrupting the U.S. economy,” Ipek Ozkardeskaya, a senior analyst at Swissquote, wrote in a note. “But what will really make the difference is the quantitative tightening and given the steep rise in Fed’s balance sheet since March 2020, even halting the growth would be an abrupt change.”

In Europe, the Stoxx Europe 600 Index rose 1%, led by financial services and basic-resource stocks. UBS shares surged 6% after the lender beat estimates. Telecoms were the only industry group in red. European tech stocks rallied again, with the Stoxx Tech Index rising as much as 2.1%, among the top-performing sectoral gauge in Europe. Sector added to 3.5% gain Monday, lifted higher by overnight rally in the U.S., with the Nasdaq 100 Index +3.4%. Semiconductor makers and pandemic winners lead gains, with BE Semi +4.5%, Deliveroo +3%, ASMI +2.8%, ASML +2.6% and Just Eat Takeaway.com +2.8%. Here are some of the biggest European movers today:

UBS shares gained as much as 7.5% in early European trading, the biggest intraday gain since April 2020, after the Swiss lender posted largely better-than-expected results and analysts cheered the new financial targets.

HeidelbergCement shares rise as much as 4.7% after the company reported preliminary 4Q revenue that Stifel analyst Tobias Woerner says was “reassuring.”

Faurecia shares rise as much as 4.4% as the shares resume trading after being suspended all of Monday ahead of the closing of the Hella acquisition. The deal is a key milestone that allows the French auto parts firm to start implementing synergies, says Citi analyst Gabriel Adler (buy).

Ubisoft shares rise as much as 3.7% in positive readacross after Sony said it will buy U.S. video game developer Bungie for $3.6b. The acquisition indicates the sector is consolidating, says Citi (buy).

Hexagon shares soar as much as 23%, the most since 2009, after it signs deal with a commercial truck maker to provide battery packs for electric heavy-duty vehicles.

Shares in U.K. clothing retailer Joules plunge as much as 34%, to the lowest since April 2020, after reporting that revenue and profit before tax for the 9 weeks to Jan. 30 fell short of the board’s expectations.

Saipem falls as much as 15%, extending Monday’s 30% plunge, as brokers including Mediobanca downgrade the oil drilling specialist after it warned on 2021 earnings and said it would hold discussions with creditors and shareholders for financing.

Earlier in the session, Asian stocks rose as the latest remarks from Federal Reserve officials helped ease fears of aggressive U.S. monetary tightening. The MSCI Asia Pacific Index added as much as 0.5%, with the information-technology and financial sectors providing the biggest boosts. Japan’s Keyence and Murata Manufacturing contributed most to the advance, with both releasing quarterly earnings results after market closed in Tokyo. Equity gauges in New Zealand and India led gains, with many markets in the rest of Asia shut for holidays. China, Hong Kong, South Korea, Singapore and Taiwan were among bourses closed for the Lunar New Year break. “Now that markets are finding calm, buying is kicking into individual stocks of companies that have reported solid earnings or are expected to,” said Shogo Maekawa, a strategist at JP Morgan Asset Management in Tokyo. Asian shares may extend gains if U.S. data this week on employment and ISM manufacturing don’t rattle the market, Maekawa added. Fed officials said they want to avoid unnecessarily disrupting the economy as they prepare to start raising rates, mitigating market concern over a 50 basis-point move in March. “You always want to go gradually,” Kansas City Fed President Esther George told the Economic Club of Indiana. Asia’s stock benchmark fell 4.4% in January, its biggest such drop since July, hit by concern that faster-than-expected U.S. rate hikes will cool the global economic recovery.

Japanese stocks pared large morning gains, with the Topix finishing little changed, as automakers slid. Chemical and machinery makers also dragged on the Topix, which wiped out a gain of as much as 1.3%. The Nikkei closed 0.3% higher, paring a 1.5% advance, with TDK and Shionogi the biggest boosts. Both gauges had risen about 3% over the previous two sessions. “There’s a lot of tussle between buyers and sellers due to month-end and month-start trading,” said Hiroshi Namioka, chief strategist at T&D Asset Management. “Shares of companies with robust earnings are being bought, but those without any specific leads to go on seem to be exposed to selling pressure.”

Indian stocks rose after the annual federal budget pledged to step up spending in a bid to support a business recovery in Asia’s third-largest economy. The S&P BSE Sensex climbed 1.5%, its biggest advance in a month, to 58,862.57 in Mumbai. The NSE Nifty 50 Index rose 1.4%. Fifteen of the 19 sector indexes compiled by BSE Ltd. rose, led by a gauge of metal stocks that jumped the most in six months. Finance Minister Nirmala Sitharaman’s strong push for infrastructure-led growth and investment centered around sectors like railways, roadways, logistics and energy will benefit most metal companies, according to Priyesh Ruparelia, a vice president at ICRA Ltd. A measure of capital goods companies also jumped the most in a year. The nation plans to boost capital spending by 35% to 7.5 trillion rupees ($100 billion) in the next financial year that starts in April in a bid to sustain a recovery in growth disrupted by the pandemic. “With growth-oriented focus intact in the budget, we expect economic and capital market buoyancy to remain,” said Vijay Chandok, managing director at ICICI Securities Ltd.

Waves of volatility have swept across markets after the Fed signaled swifter monetary-policy tightening to curb inflation than many had expected. Investors need to “get used to this up and down volatility” as there’ll likely be more of it, Nancy Davis, chief investment officer at Quadratic Capital Management, said on Bloomberg Television.

In rates, Treasuries bull flattened as spreads unwound a portion of Monday’s steepening move with yields richer by up to 3.5bp across long-end of the curve. US Treasury yields were richer by 2bp to 3.5bp across the curve with 2s10s, 5s30s spreads both flatter by almost 1bp each; 10-year yields around 1.75%, with bunds lagging by 1.5bp and gilts outperforming by 1bp in the sector. In European bonds, focus remains on the front-end of the curve as rate hike premium continues to build -- German 2-year yields are cheaper by almost 4bp on the day, trading above the European Central Bank’s deposit rate for the first time since 2015. Gilts outperform in early London session. IG dollar issuance slate includes Kommuninvest $1b 2Y SOFR; two companies priced $1.8b Monday as sales activity continues to drop off in volatile backdrop.

In FX, Bloomberg Dollar Spot index falls 0.3%. NOK, CHF and SEK outperform in G-10, CAD and euro lag. The Bloomberg Dollar Spot Index slumped as the greenback weakened against all of its Group-of-10 peers. Gains were led by the Swiss franc, which advanced a second day as it rebounded after adverse month-end flows; Scandinavian currencies were also among the top gainers amid supportive risk sentiment. The euro headed for a third day of gains, boosted by an unwind of the latest rally for downside exposure through options; the common currency rose by as much as 0.3% to 1.1269, raising questions on whether its latest weakness was more down to month-end flows rather than hawkish Fed bets. French inflation rose 3.3% from a year earlier in January, a sharper gain than the 2.9% economists estimated following December’s 3.4% advance. The pound rallied against a broadly weaker dollar, with domestic focus remaining on the Bank of England’s meeting this week. Figures showed U.K. house prices registered their strongest start to the year since 2005, before mortgage data due later Tuesday. The Aussie reversed an earlier loss after the RBA said it’s ready to be patient on interest rates even as it ceased its bond-purchase program. Overnight- indexed swaps continued to price in four rate hikes by the central bank this year. The Kiwi also advanced, in part on purchases against Aussie post RBA. Japan’s bonds extended a decline to a fourth day amid growing speculation that the central bank will step in to slow a rise in yields. The yen gained for third day.

Crypto markets were varied in which Bitcoin traded sideways around 38.5k and Ethereum gained over 2%.

In commodities, crude futures fade a sharp drop. WTI finds support near $87 before recovering back on to a $88-handle. Brent trades flat near $89.20. Most base metals trade in the green; LME nickel rises 1.3%, outperforming peers, LME lead and tin lags. Spot gold rises roughly $10 to trade near $1,807/oz

U.S. economic data slate includes January Markit manufacturing PMI (9:45am), ISM manufacturing, December construction spending and JOLTS job openings (10am); while AMD, Alphabet, Electronic Arts, Exxon, General Motors, Gilead, PayPal, Stanley Black & Decker, Starbucks and UPS are among companies reporting results.

Market Snapshot

S&P 500 futures down 0.3% to 4,490.00

STOXX Europe 600 up 0.8% to 472.72

MXAP up 0.4% to 185.38

MXAPJ up 0.3% to 606.58

Nikkei up 0.3% to 27,078.48

Topix little changed at 1,896.06

Hang Seng Index up 1.1% to 23,802.26

Shanghai Composite down 1.0% to 3,361.44

Sensex up 1.3% to 58,793.71

Australia S&P/ASX 200 up 0.5% to 7,006.04

Kospi up 1.9% to 2,663.34

Brent Futures down 0.9% to $88.45/bbl

Gold spot up 0.5% to $1,805.93

U.S. Dollar Index down 0.16% to 96.38

German 10Y yield little changed at -0.01%

Euro up 0.2% to $1.1258

Brent Futures down 0.9% to $88.45/bbl

Top Overnight News from Bloomberg

Money markets are wagering on the BOE raising rates five times by 25 basis points and a move of that magnitude from the ECB by December. That spurred a renewed selloff in bonds across the continent on Monday, and challenges ECB policy makers including President Christine Lagarde who have pushed back against the idea of raising borrowing costs this year

Euro-area manufacturers are taking a more aggressive approach to price setting -- another signal that inflation won’t slow quickly after stronger- than-expected readings from the region’s biggest economies. Output prices rose at the second-fastest rate on record in January, according to a survey of purchasing managers by IHS Markit released Tuesday. While there were some signs of supply- chain problems easing, robust demand allowed firms to pass on higher costs to customers

German joblessness fell at a much faster pace than anticipated in January as the economy comes to terms with coronavirus curbs to contain surging infections. Unemployment in Europe’s largest economy declined by 48,000, pushing the jobless rate down to 5.1%. Economists had forecast a drop of just 6,000

A more detailed look at global markets courtesy of Newsquawk

Asian stocks were positive but with upside limited amid mass holiday closures for the Lunar New Year. ASX 200 (+0.5%) rose above 7,000 with the index further underpinned as the RBA stuck to a dovish tone. Nikkei 225 (+0.3%) was kept afloat after lower unemployment although retraced gains as JPY strengthened. Nifty 50 (+1.4%) outperformed as focus in India centred on earnings and the budget announcement.

Top Asian News

Europe Is Losing Nuclear Power Just When It Really Needs Energy

Winners and Losers in India’s Budget Aiming to Bolster Growth

Widespread Bullying, Harassment Detailed in Rio Tinto Report

India Plans Record Borrowing to Fund Modi’s Growth Ambitions

European bourses are firmer taking impetus from the holiday-thinned APAC handover and Monday's US close; albeit, benchmarks are off best levels, Euro Stoxx 50 +1.0%. Sectors are all in the green though Telecom lags while Basic Resources, Banks and Tech do well amid base metals, UBS (+7.0%) earnings and the NQ/NXPI read-across respectively. Stateside, US futures are relatively contained but have moved directionally with European peers, the NQ remains the current modest outperformer.

Top European News

U.K. Mortgage Approvals Rise to 71k in Dec. Vs. Est. 66k

Slovenia Mulls Law on Swiss-Franc Loans Slammed by Lenders, ECB

Europe Is Losing Nuclear Power Just When It Really Needs Energy

Putin Meets Orban Amid Diplomatic Flurry: Ukraine Update

In FX, DXY sheds more Fed rate hike premium and month end rebalancing momentum. Franc rebounds firmly as yields recede and SNB President Jordan sets sights on keeping track of inflation. Sterling underpinned by risk appetite and firm UK macro releases. Kiwi turns table on Aussie after encouraging NZ trade data and RBA pledges patience on tightening after confirming removal of QE. Rouble on front foot ahead of call between Russia’s Foreign Minister Lavrov and US Secretary of State Blinken, but Lira lurching after Turkey’s manufacturing PMI slows to the brink of stagnation. BoJ is under less pressure to shift yield target than market thinks, sources cited by Reuters say. Sources say the central bank has many tools to combat rising yields; BoJ currently prefers market operations.

In commodities, WTI and Brent are pivoting the mid-point of ~USD 1.50/bbl ranges that have seen a test of yesterday's trough for Brent at worst thus far. Total OPEC+ production was lower by 824k/BPD than the required production in December, via JTC cited by Energy Intel's Bakr; overall compliance in December was 122%. Goldman Sachs, on OPEC+, sees growing potential for a faster ramp-up, given the pace of the recent rally and likely pressures from importing nations. Spot gold/silver are firmer picking up from the pressure seen in recent sessions. Though, gold remains near the USD 1800/oz mark and as such the 200-, 100- & 50-DMAs.

US Event Calendar

9:45am: Jan. Markit US Manufacturing PMI, est. 55.0, prior 55.0

10am: Dec. JOLTs Job Openings, est. 10.3m, prior 10.6m

10am: Dec. Construction Spending MoM, est. 0.6%, prior 0.4%

10am: Jan. ISM Manufacturing, est. 57.5, prior 58.7, revised 58.8

10am: Jan. ISM Employment, est. 53.0, prior 54.2, revised 53.9

10am: Jan. ISM New Orders, est. 58.0, prior 60.4, revised 61.0

10am: Jan. ISM Prices Paid, est. 67.0, prior 68.2

.............

Have a Great Day

Weird-looking cat Wilfred goes viral with Michael Rapaport voiceover

.

.

.

.

.

.

.

.

.

.

.

. . . .

Join the InvestorsHub Community

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.