Wednesday, January 19, 2022 7:57:23 AM

Amtrak Snow-mo Collision on "Morning Markets"

Morning Markets

.

.

.

.

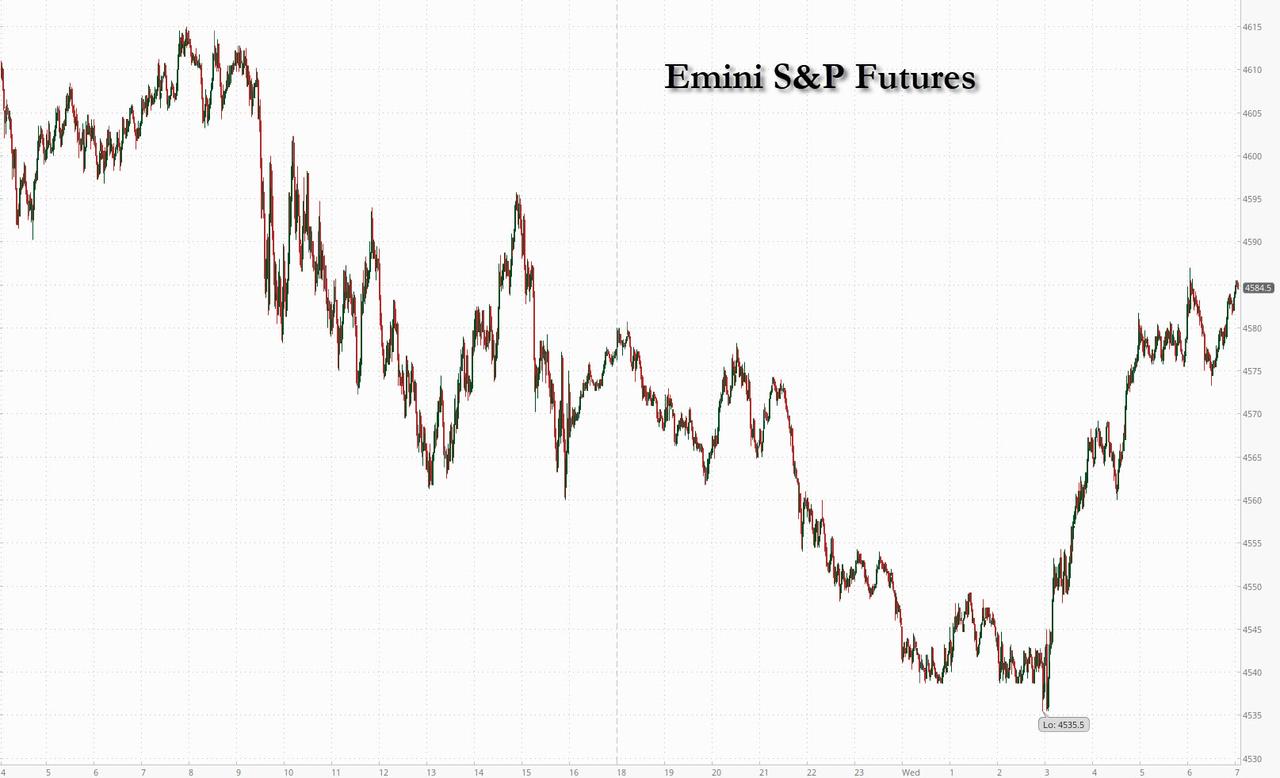

Futures Rebound Strongly From Overnight Rout As Yields Stabilize

Wednesday, Jan 19, 2022 - 07:34 AM

After what earlier looked like another assured overnight rout, especially after 10Y yields hit 1.90% and Brent rose as high as $89/bbl, US equity futures reversed earlier losses to trade higher as earnings optimism outweighed concerns over soaring bond yields and a 50bps March rate hike. As of 7:00am ET, emini S&P futures were up 14 points ot 0.3% to 4,585, Nasdaq futures were up 65 points or 0.44% and Dow futures were also in the green by 89 points or 0.25%. The dollar slumped after several days of sharp gains, the 10Y yield traded at 1.8826%, down from the session's highest levels, and Brent was at $88.23.

The prospect of accelerated policy tightening as well as concerns over the omicron variant and inflation hurting companies’ profits have whipsawed equities this year. The surge in Treasury yields has fueled a rotation out of expensive technology and growth shares and into cheaper parts of the market. Meanwhile, the 10Y yield has continued its aggressive push higher overnight, and hit a fresh 2 year high, rising just above 1.90% for the first time since Jan 2020, before retracing some of the move. Britain’s inflation rate surged unexpectedly to the highest since 1992 and Germany’s 10-year yield turned positive for the first time since 2019.

The surge in yields has routed high duration tech names - the Nasdaq 100 plunged 2.6% yesterday to the lowest level since mid-October. “The 2-year Treasury has moved too aggressively in pricing in Fed tightening, in our view, and we expect the yield curve to steepen,” said Mark Haefele, chief investment officer at UBS Global Wealth Management. “This steepening should further improve the positive backdrop for financial services companies,” he said.

SoFi Technologies, the financial firm led by former Twitter executive Anthony Noto, extended its gains in U.S. premarket session after the Office of the Comptroller of the Currency granted it a U.S. banking charter.

“We are in late stage of the cycle, where equities will post lower returns due to weaker growth and higher rates, but we expect the ongoing correction to be short,” Luca Paolini, chief strategist at Pictet Asset Management, said by email. He’s forecasting the S&P 500 index and U.S. 10-year yields at 2% by the end of the year.

Most European equities are in the green, recovering after a soggy start. Euro Stoxx 50 is up 0.5%, rallying ~1% from opening levels. Consumer products and services and retail names are the best performers after Richemont and Burberry Group Plc beat expectations; utilities and insurance names are the weakest. Shares in Switzerland's Richemont are leading the STOXX 600 and up a whopping 7% after the world's second-largest luxury group reported string demand for jewellery and watches.That had a positive effect across the sector and France's heavyweights, LVMH, Kering and Hermes are up and lifting the Paris CAC 40 benchmark above the floatation mark.The UK's Burberry is another strong performer, rising close to 5% as the luxury brand said annual profit would beat market expectations. The retail sector was also on a roll, rising over 2% with Spain's Inditex leading the pack after Goldman Sachs upgraded the stock due to resilient earnings and cashflow. Marks & Spencer, Zalando and Kingfisher were all rising over 2%.

Earlier in the session, risk aversion deepened in stock markets across Asia on Wednesday as bond yields remained elevated, with investors trying to gauge the timing and scope of the Federal Reserve’s anticipated interest-rate hikes. The MSCI Asia Pacific Index slid as much as 1.5%, heading for a five-day slump, as tech and consumer-discretionary stocks furthered recent declines. Sony Group and Toyota Motor were among the biggest drags on the gauge. Energy shares climbed, even as the oil rally eased in Asia. Quantitative tightening may exert capital-outflows pressure on Asia, “which may theoretically lead to compression in asset valuations,” Nomura strategists including Chetan Seth wrote in a note. Given that valuations are currently modest, Asian stocks will not face as significant a de-rating as they did when the Fed tightened in 2017-2018, they added. Higher yields have damped investor appetite for global equities, particularly hitting richly valued tech shares. Asian firms are also weighed down by concerns over China’s economy. Still, the yield spike isn’t all bad for stocks, as “the sum total of expected rate hikes remains low,” BlackRock Investment Institute strategists wrote in a note. Japan’s stock benchmarks were the worst performers in Asia on Wednesday, with the Topix a whisker away from technical correction as Tokyo and other parts of the nation prepare to come under a state of quasi-emergency for three weeks starting Friday. Hong Kong-listed tech stocks capitulated ahead of a Reuters report in the late afternoon about China slapping new curbs on investment deals for the industry’s largest firms. Equity losses were relatively limited in mainland China, where the central bank pledged to use more monetary-policy tools.

Japanese equities fell and the yen strengthened amid extended global risk-off trading on concerns over expected Federal Reserve monetary tightening. Electronics and auto makers were the biggest drags on the Topix, which was down 3% as of 2:37 p.m. in Tokyo, with all 33 industry groups in the red. Tokyo Electron Ltd was the largest contributor to a 3% loss in the Nikkei 225 Stock Average. Sony Group Corp. dropped more than 12% after rival Microsoft Corp. announced it will acquire Activision Blizzard Inc. The Japanese currency gained 0.3% against the dollar. After initial enthusiasm following the Bank of Japan’s decision to maintain policy, Japanese stocks swung to a loss Tuesday amid regional concerns after U.S. Treasury yields spiked. U.S. stocks dropped overnight as speculation grew that central banks will have to boost interest rates sooner than earlier anticipated. “There’s market jitters over the possibility of a U.S. rate hike taking place earlier than March,” said Mitsushige Akino, a senior executive officer at Ichiyoshi Asset Management Co. “The level of market uncertainty is high and share price swings are likely to continue into March, until there’s clarity on the Fed’s monetary policy steps.” Meanwhile, the greater Tokyo region and other parts of Japan are set to come under a state of quasi-emergency for three weeks starting Friday as the government tries to rein in a surge in Covid-19. Tokyo will seek to have bars and restaurants close early, national broadcaster NHK said.

In Australia, the S&P/ASX 200 index fell 1% to 7,332.50, closing at its lowest level since Dec. 20. Global stocks dropped as Treasury yields soared on bets that central banks will have to boost interest rates earlier than expected. Yields in Australia and New Zealand also climbed. READ: Kiwi Dollar, Yields Jump on ANZ Rate View: Inside Australia/NZ Megaport was the worst performer on Australia’s benchmark after it reported 2Q sales results. Harvey Norman was among the top performers after it was upgraded at Credit Suisse. In New Zealand, the S&P/NZX 50 index fell 1.6% to 12,612.31, marking its worst session in almost a year

In rates, Treasury yields remained cheaper on the day despite futures rebounding sharply from session lows. Yields higher by 1bp-2bp across the curve and most spreads within a basis point of Tuesday’s close; 10-year 1.885% after topping 1.90% for first time since January 2020, while in Europe, bund yields climbed above zero for the first time since before the pandemic. Treasury coupon sales resume with $20b 20-year bond reopening. $20b 20-year bond reopening at 1pm ET follows small tails for last week’s 10- and 30-year auctions; a $16b 10-year TIPS new issue is slated for Thursday. German 2s10s steepen ~2bps with 10y bund yields turning slightly positive. Gilts bear-flatten, cheapening as much as 8bps across the curve after a hot inflation print; OIS rates price ~24bps of tightening for the Feb. BOE meeting. Cash USTs bear-flatten slightly.

In FX, Bloomberg dollar spot drops 0.25%, slightly extending Asia’s weakness, and the dollar was steady-to-weaker against all of its Group-of-10 peers. The Norwegian krone and Canadian dollar rallied as oil prices continued to rise while New Zealand’s dollar gained and the nation’s short-end yields climbed after ANZ economists said they now expect the RBNZ’s official cash rate to peak at 3% by April 2023, up from a prior projection of 2% in 2H 2022. The pound inched up amid broad dollar weakening while the yield on 10-year Gilts soared through 1.30% following a report showing that Britain’s inflation rate surged unexpectedly to the highest since 1992. The euro inched up following yesterday’s deep loss versus the dollar; the rate on 10-year Bunds rose four basis points to 0.02%, crossing above zero for the first time since May 2019. The yen pared an advance as European stocks rebounded from opening losses. Commodity currencies lead broad gains against the dollar in G-10. ZAR leads in EMFX after Dec. inflation data nears the top of SARB’s target range.

In commodities, crude futures drift back up toward session highs after an early dip. WTI is up over 1% after finding support near $86, Brent regains $88. Spot gold pushes slightly higher, adding $3 near $1,817/oz. LME copper outperforms in a broadly positive base metals complex; tin lags.

Looking at the day ahead, data releases include the UK and Canada’s CPI reading for December, along with US housing start and building permits for December. Central bank speakers include BoE Governor Bailey, Deputy Governor Cunliffe and the ECB’s Holzmann. Finally, earnings releases include UnitedHealth Group, Bank of America, Procter & Gamble, Morgan Stanley, Charles Schwab, US Bancorp and United Airlines.

Market Snapshot

S&P 500 futures down 0.1% to 4,565.50

STOXX Europe 600 little changed at 479.76

MXAP down 1.3% to 191.05

MXAPJ down 0.5% to 628.97

Nikkei down 2.8% to 27,467.23

Topix down 3.0% to 1,919.72

Hang Seng Index little changed at 24,127.85

Shanghai Composite down 0.3% to 3,558.18

Sensex down 1.0% to 60,142.26

Australia S&P/ASX 200 down 1.0% to 7,332.50

Kospi down 0.8% to 2,842.28

Brent Futures up 1.1% to $88.45/bbl

Gold spot up 0.2% to $1,817.04

U.S. Dollar Index down 0.13% to 95.61

German 10Y yield little changed at 0.01%

Euro up 0.2% to $1.1343

Brent Futures up 1.1% to $88.44/bbl

Top Overnight News from Bloomberg

China’s central bank pledged to use more monetary policy tools to spur the economy and drive credit expansion, sending its clearest signal yet of an easing bias to boost market confidence

The European Central Bank’s inflation forecasts aren’t a “blind certitude” and the institution will take action if the price surge proves more persistent, Bank of France Governor Francois Villeroy de Galhau said

A group of rookie Tory MPs gathered on Tuesday to discuss whether there was any appetite to move together against the prime minister, several lawmakers said

Oil held gains above the highest close since 2014 as the International Energy Agency said the market looked tighter than previously thought, with demand proving resilient to omicron. Some in the market now think it’s now a question of when -- not if -- oil hits triple digits

The Cyberspace Administration of China is drafting new guidelines that will require any company with more than 100 million users or over 10 billion yuan ($1.6 billion) in revenue to seek the watchdog’s approval before such deals, Reuters reported. Any internet firm in sectors named on a “negative list” issued last year will also require approval, the news agency said

A more detailed look at global markets courtesy of Newqsuawk

Asian stocks followed suit to the losses on Wall St where all major indices declined led by tech and growth as US yields climbed to two-year highs and with financials also hit following earning releases in which Goldman Sachs and Charles Schwab both missed on their bottom lines. ASX 200 (-1.0%) traded lower in which tech mirrored the underperformance of the sector stateside as Nasdaq 100 futures dipped into correction territory after shedding 10% from its November peak and with BHP failing to benefit from an increase in its quarterly iron ore and petroleum output as the mining giant also reported a decline in coal production and warned of short-term disruptions from next month’s proposed easing of Western Australia border restrictions. However, the energy sector was buoyed by continued advances in oil prices due to the geopolitical risk premium and after an explosion in Turkey forced the shutdown of the Iraq-Turkey crude oil pipeline which is Iraq’s largest crude oil export line. Nikkei 225 (-2.8%) was heavily pressured by recent currency strength and with Japan set for tighter COVID-19 restrictions in key areas including Tokyo, while Toyota and Sony were the notable laggards after the automaker flagged a miss to its output targets due to chip shortages and with Sony impacted by news that rival Microsoft is to acquire video game publisher Activision. Hang Seng (U/C) and Shanghai Comp. (-0.4%) were choppy and initially fared better than their regional peers after the PBoC continued with its liquidity efforts and recently hinted of more easing, but with upside restricted amid reports of further scrutiny by the US on Chinese businesses including an examination into Alibaba's cloud unit to determine if it poses a risk to US national security. Finally, 10yr JGBs were kept afloat amid the broad risk aversion in Tokyo although gains in JGBs were gradual as T-note futures remained pressured by a further rise in yields and following slightly weaker demand at the enhanced liquidity auction for 2yr-20yr JGBs.

Top Asian News

Sunac China Dollar Bonds’ Record Surge Approaches 20 Cents

Hamsters, Wings, Shrimp Ensnared by China’s Covid Zero Zeal

China’s Sinopec Floods LNG Spot Market with Cargoes for 2022

Tokyo to Press Bars to Close Early as Covid Cases Hit Record

Major bourses in Europe are now mostly in positive territory (Euro Stoxx 50 +0.5%; Stoxx 600 +0.3%) as the region recovered from the losses seen at the cash open – which saw the Euro Stoxx 50 and DAX 40 open lower by 0.5% and 0.8% respectively. US equity futures have also nursed earlier losses and now reside in positive territory, with the NQ recuperating from losses of over 1.0% at one stage as the US 10yr cash yield eclipsed 1.90% and the German 10yr yield turned positive for the first time in over three years. Back to cash equities, the CAC (+0.6%) and IBEX (+0.6%) outperform amid their large retail exposure, with the sector bolstered after stellar updates from Richemont (+9.1%) and Burberry (+6.0%) coupled with a broker upgrade for Inditex (+3.5%) at Goldman Sachs; in turn lifting the likes of LVMH (+3.0%) and Kering (+3.3%). Delving deeper into the sectors, the earlier defensive bias has evolved into a more cyclical one, with Basic Resources, Travel & Leisure and Retail at the top of the bunch, whilst Healthcare and Food & Beverages make their way down the ranks. Tech has recovered from its earlier yield-induced underperformance with the aid of a post-earnings ASML (+1.1%) which missed on net sales expectations, but the group announced a 100% Y/Y increase in its dividend, whilst the CEO suggests their production capacity cannot accommodate higher demand. For reference, ASML accounts for around 7.5% of the Euro Stoxx 50. In terms of other individual movers, Leoni (-14.0%) slumped as Co. sites were searched by the German Federal Cartel Office as part of an investigation into various cable manufacturers and other industry-related companies.

Top European News

Richemont, Burberry Signal That Luxury Market Is Thriving

Airbus Gears Up for Growth With Plans to Add 6,000 New Staff

5G Rollout Disrupts Flights Into U.S. From Across the World

Hamsters, Wings, Shrimp Ensnared by China’s Covid Zero Zeal

In FX, sterling remains somewhat caught between stalls after stronger than forecast UK CPI readings that add more weight to expectations and pricing for further BoE policy normalisation, but cautious about carrying too much rate hike premium given the growing prospect of change at the highest level in Government and the rising rebellion against Tory Party leader Boris Johnson. Hence, the post-data pop above 1.3600 in Cable was relatively limited and short-lived, while Eur/Gbp only dipped marginally within a tight 0.8342-23 range before stabilising. However, the Pound is holding off Tuesday’s lows vs the Dollar by virtue of the fact that the Greenback has faded generally and topped a key Fib retracement level at 1.3610 as the index slips back a bit further towards 95.500 having reached 95.832 at best yesterday and consolidating between 95.792-549 ahead of US housing data and the 20 year auction.

NZD/AUD - In contrast to Sterling, the Kiwi has no political inhibitions on the domestic front inhibitions and is outperforming amidst hawkish RBNZ calls from ANZ Bank, as Nzd/Usd bounces from overnight lows towards the psychological 0.6800 mark and the Aud/Nzd cross retreats through 1.0600 again. To recap, ANZ expects a 25 bp hike at every meeting from February to April 2023 that would push the OCR up to 3% from the current 75 bp. Meanwhile, the Aussie is lagging in wake of a fall in Westpac consumer sentiment and in advance of more pivotal jobs data tomorrow, albeit with Aud/Usd also off worst levels within a 0.7177-0.7214 band following a strong rise in iron ore prices.

CAD/CHF/EUR/JPY - All recouping some lost ground against the Buck, and the Loonie still getting a lift from crude as WTI extends its heady rise to probe Usd 87/brl, while the Franc is approaching 0.9150 from sub-0.9175 and remains above 1.0400 vs the Euro even though Eur/Usd has regained enough poise to retest offers/resistance into 1.1350, including the 21 DMA that comes in at 1.1347 today (and incidentally matches Tuesday’s 55 DMA). Elsewhere, the Yen is rather betwixt and between on respective UST/JGB yield and broad risk grounds, as Usd/Jpy pivots 114.50 before Japanese inflation on Thursday. Back to Usd/Cad, Canadian CPI looms and could either compound BoC tightening perceptions or undermine, while the near term technical backdrop is basically flanked by resistance around 1.2550 and support circa 1.2450 beyond the current 1.2525-1.2472 bounds.

In commodities, WTI and Brent front month futures remain elevated following an initial blip lower in early European hours – which at the time emanated from reports that the Iraq-Turkey pipeline will resume oil flows after an explosion yesterday - said to have been an accident as opposed to an attack, which had been feared. The explosion was the cited driver behind yesterday’s rise in crude, with WTI Feb reaching a USD 86.41/bbl high and Brent March a peak of USD 89.05/bbl before waning off best levels. Nonetheless, prices see tailwinds in European trade as equities recovered off lows and following the IEA Monthly Oil Market report which raised its global demand growth forecast and suggested Omicron has had less of an impact than initially expected. Furthermore, the report suggested that OPEC+ effective spare capacity will be just 2.6mln BPD in H2-2022, "held primarily by Saudi Arabia and the UAE." Saudi Arabia has usually kept more than 1.5-2mln BPD of spare capacity on hand for market management, according to the EIA. Elsewhere, spot gold has been driving higher as the Dollar remains near lows, with the yellow metal finding some support around USD 1,810/oz. LME copper meanwhile is on the front-foot and prices have extended on their APAC gains as stocks trim earlier losses, whilst mining giant Antofagasta sees the demand picture for the red metal continuing. Elsewhere, Indonesia has not issued any export permits for tin for 2022, according to a commodity exchange official.

US Event Calendar

7am: Jan. MBA Mortgage Applications, prior 1.4%

8:30am: Dec. Building Permits MoM, est. -0.8%, prior 3.6%, revised 3.9%

8:30am: Dec. Housing Starts MoM, est. -1.7%, prior 11.8%

8:30am: Dec. Building Permits, est. 1.7m, prior 1.71m, revised 1.72m

8:30am: Dec. Housing Starts, est. 1.65m, prior 1.68m

..............................

Have a Blast today

and stay warm...

Amtrak Snow-mo Collision

.

.

.

.

.

. . . .

Join the InvestorsHub Community

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.