| Followers | 689 |

| Posts | 143817 |

| Boards Moderated | 35 |

| Alias Born | 03/10/2004 |

Friday, December 24, 2021 6:56:09 PM

By: Simply Wall Street | December 23, 2021

QUALCOMM Incorporated (NASDAQ:QCOM) is a wireless chipmaker, currently focused on the 5G landscape. The company is highly appealing based on the fundamentals, which is what we are evaluating today.

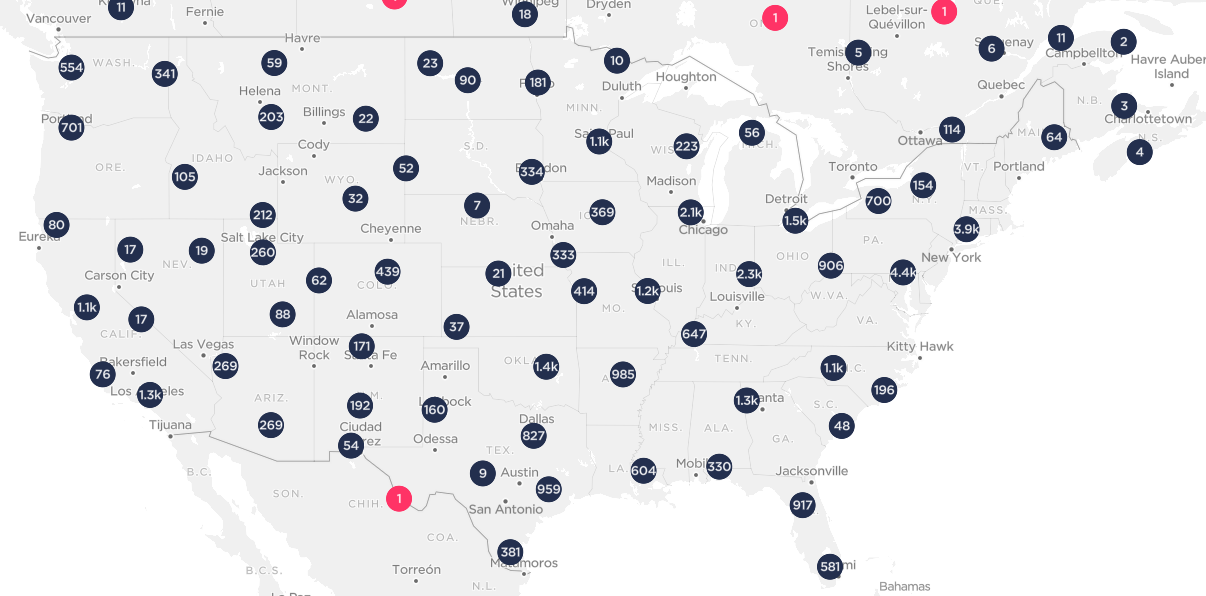

5G is coming at a quicker pace than some analysts have predicted, and many companies are tied to the development of this technology, including Qualcomm. This map of commercially available 5G locations shows the scale of the expansion:

Considering this, we want to see to what extent can Qualcomm gauge this growth, and how profitable will this endeavor be.

Fundamentals

QUALCOMM reported US$34b in revenue, a growth of 43% vs the year before - roughly in line with analyst forecasts. Earnings per share (EPS) of US$7.87 beat expectations, being 7.3% higher than what the analysts expected.

The chart below shows that the company has grown and is also expected to continue that growth in the future. We can also see that Qualcomm has a 27% profit margin and is Free Cash Flow positive with US$8.6b in FCF.

Taking into account the latest results, the current consensus from QUALCOMM's 25 analysts is for revenues of US$39.5b in 2022, which would reflect a solid 18% increase on its sales over the past 12 months. Per-share earnings are expected to ascend 15% to US$9.29.

Stock price growth is deemed to closely follow per share earnings growth, which is why analysts are usually focused on this metric. This is even more reliable when we have a stable company like Qualcomm. In our case, the estimated EPS growth of 15% resembles a potential upside for the stock, but be careful because markets start pricing this in, on the earnings report date - which was Nov.5.2021 for Qualcomm.

The price target average is US$200, and we estimate the company to have an intrinsic value of US$186 per share. Looking at the spread of price target estimates, we see that the most bullish analyst values QUALCOMM at US$225 per share, while the most bearish prices it at US$163. A wide spread like this implies some volatility, but industry trends suggest a steady growth in earnings and revenue.

Qualcomm also pays a small but stable 1.5% dividend yield. This may start increasing as the company optimizes for cash flow generation and investors can slowly start considering the Qualcomm as an income stock.

Conclusion

Qualcomm is a growing company in a developing industry and delivering positive cash flows for investors. The stock seems to be trading around intrinsic value, so there isn't much concern of it being overvalued.

The price may fluctuate, but the growth direction is positive, and the company seems to be optimizing for cash flows for investors.

Considering this, Qualcomm may still be a good stock for investors that want to enter the 5G landscape.

Even so, be aware that QUALCOMM is showing 2 warning signs in our investment analysis , you should know about...

Read Full Story »»»

DiscoverGold

DiscoverGold

Information posted to this board is not meant to suggest any specific action, but to point out the technical signs that can help our readers make their own specific decisions. Caveat emptor!

• DiscoverGold

Recent QCOM News

- AIG names new CFO; Progyny Drops 24% After Losing Key 2025 Contract; Exicure Jumps 190% With Nasdaq Extension • IH Market News • 09/19/2024 10:26:48 AM

- Form 4 - Statement of changes in beneficial ownership of securities • Edgar (US Regulatory) • 09/06/2024 08:13:55 PM

- Broadcom Down 10% Post-Earnings, UiPath Up 8%; Qualcomm Eyes Intel Assets; Salesforce Acquires Own Company • IH Market News • 09/06/2024 11:59:00 AM

- Form 144 - Report of proposed sale of securities • Edgar (US Regulatory) • 09/05/2024 08:02:04 PM

- Qualcomm Develops Mixed Reality Glasses; Verizon to Boost Dividend, Eyes Acquisition; Samsonite Plans US Dual Listing • IH Market News • 09/05/2024 10:11:35 AM

- Form 4 - Statement of changes in beneficial ownership of securities • Edgar (US Regulatory) • 09/04/2024 08:07:03 PM

- Form 4 - Statement of changes in beneficial ownership of securities • Edgar (US Regulatory) • 09/04/2024 08:06:45 PM

- Form 144 - Report of proposed sale of securities • Edgar (US Regulatory) • 09/03/2024 09:18:30 PM

- Form 144 - Report of proposed sale of securities • Edgar (US Regulatory) • 09/03/2024 08:08:35 PM

- Form 4 - Statement of changes in beneficial ownership of securities • Edgar (US Regulatory) • 08/21/2024 08:22:15 PM

- FuboTV Soars 12% After Venu Sports Block, Goldman Sachs Lowers U.S. Recession Odds, BHP Ends Chile Strike • IH Market News • 08/19/2024 09:28:19 AM

- Deutsche Bank Faces Shareholder Backlash, Bank of America Sponsors 2026 World Cup, Quanterix CEO Buys More Shares • IH Market News • 08/16/2024 10:03:21 AM

- Google Mandated to Modify Play Store, Apple Innovates, Victoria’s Secret Hires CEO, Mars Buys Kellanova • IH Market News • 08/15/2024 10:05:46 AM

- Google Forced to Modify Play Store, Apple Innovates, Victoria’s Secret Hires CEO, Mars Buys Kellanova • IH Market News • 08/15/2024 10:05:46 AM

- Form 8-K - Current report • Edgar (US Regulatory) • 08/09/2024 08:05:49 PM

- Form 4 - Statement of changes in beneficial ownership of securities • Edgar (US Regulatory) • 08/09/2024 08:05:43 PM

- Form 4 - Statement of changes in beneficial ownership of securities • Edgar (US Regulatory) • 08/09/2024 08:05:27 PM

- Form 144 - Report of proposed sale of securities • Edgar (US Regulatory) • 08/08/2024 09:01:47 PM

- Form 4 - Statement of changes in beneficial ownership of securities • Edgar (US Regulatory) • 08/05/2024 09:03:28 PM

- Form 144 - Report of proposed sale of securities • Edgar (US Regulatory) • 08/02/2024 08:01:38 PM

- Qualcomm Gewinnmitteilung auf der Investor Relations Website des Unternehmens verfügbar • Business Wire • 07/31/2024 10:50:00 PM

- Publication des résultats de Qualcomm disponible sur le site web de la société consacré aux relations avec les investisseurs • Business Wire • 07/31/2024 10:50:00 PM

- Form 10-Q - Quarterly report [Sections 13 or 15(d)] • Edgar (US Regulatory) • 07/31/2024 08:02:08 PM

- Form 8-K - Current report • Edgar (US Regulatory) • 07/31/2024 08:01:12 PM

- Qualcomm Earnings Release Available on Company’s Investor Relations Website • Business Wire • 07/31/2024 08:00:00 PM

VHAI - Vocodia Partners with Leading Political Super PACs to Revolutionize Fundraising Efforts • VHAI • Sep 19, 2024 11:48 AM

Dear Cashmere Group Holding Co. AKA Swifty Global Signs Binding Letter of Intent to be Acquired by Signing Day Sports • DRCR • Sep 19, 2024 10:26 AM

HealthLynked Launches Virtual Urgent Care Through Partnership with Lyric Health. • HLYK • Sep 19, 2024 8:00 AM

Element79 Gold Corp. Appoints Kevin Arias as Advisor to the Board of Directors, Strengthening Strategic Leadership • ELMGF • Sep 18, 2024 10:29 AM

Mawson Finland Limited Further Expands the Known Mineralized Zones at Rajapalot: Palokas step-out drills 7 metres @ 9.1 g/t gold & 706 ppm cobalt • MFL • Sep 17, 2024 9:02 AM

PickleJar Announces Integration With OptCulture to Deliver Holistic Fan Experiences at Venue Point of Sale • PKLE • Sep 17, 2024 8:00 AM