| Followers | 689 |

| Posts | 143817 |

| Boards Moderated | 35 |

| Alias Born | 03/10/2004 |

Monday, November 23, 2020 7:51:16 AM

Taxpayers Face $435 Billion in Student-Loan Losses, Already Baked in: Leaked Education-Department Study

By: Wolf Richter | November 22, 2020

• Most of the losses come from established income-based repayment programs that include debt forgiveness at the end. No one has ever put a number to it until now.

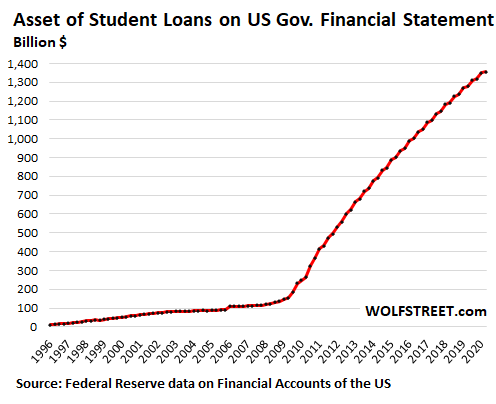

In 2009, the US government entered the business of reckless, no-matter-what lending to students, even to older students with subprime credit ratings and to students at iffy for-profit colleges with dubious degree programs. And then tuition soared, and student housing went upscale and became a global asset class with its own commercial mortgage-backed securities (CMBS) that are now experiencing record delinquency rates. And Apple and textbook publishers and everyone began feeding at the big trough, with students just being the conduit for this money. Student-loan balances on the government’s financial statement skyrocketed from $147 billion in 2009 to $1.37 trillion at the beginning of 2020, despite the 11% decline in student enrollment since 2011.

Taxpayers face a loss of $435 billion on the $1.37 trillion in student loans on the government’s financial statement at the beginning of this year, even if no additional loans are issued going forward, according to an internal study by the Department of Education, reported by the Wall Street Journal which reviewed the documents. Most of the losses would come from the already established income-based repayment programs and the debt forgiveness at the end of their term.

The expected loss of $435 billion is far larger than the rosy estimates released previously, including the Congressional Budget Office’s estimate in May 2019 of a loss of $31 billion, including administrative costs.

The student loan balances in the chart above do not include student loans carried by private lenders that are guaranteed by the US government and that will produce additional losses for taxpayers.

The Department of Education, fearing that government staff had underestimated the losses on student loans, brought in FI Consulting to build a computer model for a much more detailed analysis. And it brought in Deloitte to review the model.

The study found that most of the losses are already baked into the cake through the income-based repayment and loan-forgiveness plans, which see to it that effectively many loans do not get paid back in full before the remainder is forgiven.

Only a small number of borrowers owe a gigantic part of the student loans: 7% of all federal student-loan borrowers, mostly those that went to graduate school, piled up $500 billion of student loans – meaning these 7% of borrowers owe 37% of the federal student debt, according to a report by Moody’s dated January 2020. Each of them owes more than $100,000.

But a majority of borrowers don’t owe all that much: At the end of 2017, the “median” amount owed by the 45 million federal student-loan borrowers was around $17,500, according to the Moody’s report. “Median” means half owe more and half owe less. It means that there were 22.5 million borrowers who owed less than $17,500 – about the price of the cheapest new car available in the US.

And these 50% of borrowers combined owed only $200 billion of the total federal student loan debt.

Student loans are a top-heavy affair, with the vast majority of borrowers owing manageable amounts, and with a small number of borrowers, mostly with graduate degrees, owing very large amounts. This distribution skews the “average” student debt (total debt divided by total number of borrowers) that is often cited in the media as being over $30,000, compared to the median student debt of $17,500, with half of the borrowers owing less than $17,500.

But student-loan forgiveness is already the rule through income-based repayment plans, which allow borrowers to make monthly payments of only 10% of a special income measure composed of gross income minus 150% of the federal poverty limit. And the remaining balances are then forgiven after 10, 20, or 25 years, depending on the program.

Borrowers in income-based repayment programs will repay only 51% of their balances on average, while borrowers in other plans will repay 80% of their balances, according to the analysis by the Department of Education.

The idea – particularly for borrowers with huge debts, such as former graduate students – is to drag repayment out as far as possible, and make it as slow as possible, and to pay the least amount possible, and then have the rest forgiven. Students with smaller balances too use this strategy to avoid default and minimize payments.

This is in part responsible for the surge in student loan balances, according to Moody’s; as new loans are being added, old loans are simply not being repaid.

And these income-based repayment programs and the debt forgiveness that comes with them are a major component in the projected $435 billion loss to taxpayers on the loan balance of $1.37 trillion, according to the analysis by the Department of Education.

At this point, federal student loans are not easily discharged in bankruptcy court, but they’re forgiven at the end of the income-based repayment programs. And this is already baked into the cake. And taxpayers are on the hook for these losses.

The fact that student loans began surging only a few years ago means that this tsunami of losses stemming from loan forgiveness at the end of the income-based repayment programs is still in the future, but can be estimated.

But who ultimately got this money, since students were just the conduit? The educational-financial-industrial complex, of course, the entities that have lined up to clean out the taxpayer via these student loans. Billionaires have been printed in the process, enabled and encouraged by the government since 2009. Any solution to the student-loan crisis needs to include measures that shut down that money-transfer and return the government’s role in student loans to where it had been before 2009.

Read Full Story »»»

DiscoverGold

DiscoverGold

By: Wolf Richter | November 22, 2020

• Most of the losses come from established income-based repayment programs that include debt forgiveness at the end. No one has ever put a number to it until now.

In 2009, the US government entered the business of reckless, no-matter-what lending to students, even to older students with subprime credit ratings and to students at iffy for-profit colleges with dubious degree programs. And then tuition soared, and student housing went upscale and became a global asset class with its own commercial mortgage-backed securities (CMBS) that are now experiencing record delinquency rates. And Apple and textbook publishers and everyone began feeding at the big trough, with students just being the conduit for this money. Student-loan balances on the government’s financial statement skyrocketed from $147 billion in 2009 to $1.37 trillion at the beginning of 2020, despite the 11% decline in student enrollment since 2011.

Taxpayers face a loss of $435 billion on the $1.37 trillion in student loans on the government’s financial statement at the beginning of this year, even if no additional loans are issued going forward, according to an internal study by the Department of Education, reported by the Wall Street Journal which reviewed the documents. Most of the losses would come from the already established income-based repayment programs and the debt forgiveness at the end of their term.

The expected loss of $435 billion is far larger than the rosy estimates released previously, including the Congressional Budget Office’s estimate in May 2019 of a loss of $31 billion, including administrative costs.

The student loan balances in the chart above do not include student loans carried by private lenders that are guaranteed by the US government and that will produce additional losses for taxpayers.

The Department of Education, fearing that government staff had underestimated the losses on student loans, brought in FI Consulting to build a computer model for a much more detailed analysis. And it brought in Deloitte to review the model.

The study found that most of the losses are already baked into the cake through the income-based repayment and loan-forgiveness plans, which see to it that effectively many loans do not get paid back in full before the remainder is forgiven.

Only a small number of borrowers owe a gigantic part of the student loans: 7% of all federal student-loan borrowers, mostly those that went to graduate school, piled up $500 billion of student loans – meaning these 7% of borrowers owe 37% of the federal student debt, according to a report by Moody’s dated January 2020. Each of them owes more than $100,000.

But a majority of borrowers don’t owe all that much: At the end of 2017, the “median” amount owed by the 45 million federal student-loan borrowers was around $17,500, according to the Moody’s report. “Median” means half owe more and half owe less. It means that there were 22.5 million borrowers who owed less than $17,500 – about the price of the cheapest new car available in the US.

And these 50% of borrowers combined owed only $200 billion of the total federal student loan debt.

Student loans are a top-heavy affair, with the vast majority of borrowers owing manageable amounts, and with a small number of borrowers, mostly with graduate degrees, owing very large amounts. This distribution skews the “average” student debt (total debt divided by total number of borrowers) that is often cited in the media as being over $30,000, compared to the median student debt of $17,500, with half of the borrowers owing less than $17,500.

But student-loan forgiveness is already the rule through income-based repayment plans, which allow borrowers to make monthly payments of only 10% of a special income measure composed of gross income minus 150% of the federal poverty limit. And the remaining balances are then forgiven after 10, 20, or 25 years, depending on the program.

Borrowers in income-based repayment programs will repay only 51% of their balances on average, while borrowers in other plans will repay 80% of their balances, according to the analysis by the Department of Education.

The idea – particularly for borrowers with huge debts, such as former graduate students – is to drag repayment out as far as possible, and make it as slow as possible, and to pay the least amount possible, and then have the rest forgiven. Students with smaller balances too use this strategy to avoid default and minimize payments.

This is in part responsible for the surge in student loan balances, according to Moody’s; as new loans are being added, old loans are simply not being repaid.

And these income-based repayment programs and the debt forgiveness that comes with them are a major component in the projected $435 billion loss to taxpayers on the loan balance of $1.37 trillion, according to the analysis by the Department of Education.

At this point, federal student loans are not easily discharged in bankruptcy court, but they’re forgiven at the end of the income-based repayment programs. And this is already baked into the cake. And taxpayers are on the hook for these losses.

The fact that student loans began surging only a few years ago means that this tsunami of losses stemming from loan forgiveness at the end of the income-based repayment programs is still in the future, but can be estimated.

But who ultimately got this money, since students were just the conduit? The educational-financial-industrial complex, of course, the entities that have lined up to clean out the taxpayer via these student loans. Billionaires have been printed in the process, enabled and encouraged by the government since 2009. Any solution to the student-loan crisis needs to include measures that shut down that money-transfer and return the government’s role in student loans to where it had been before 2009.

Read Full Story »»»

DiscoverGold

DiscoverGold

Information posted to this board is not meant to suggest any specific action, but to point out the technical signs that can help our readers make their own specific decisions. Caveat emptor!

• DiscoverGold

Join the InvestorsHub Community

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.