I use the risk indicators to determine the appropriate maximum level of cash held in reserve. When max'd out I then use a combination of selling and vealies to contain the cash at that max level. If risk goes up, I follow AIM's selling guides to let the cash level rise. If risk goes down, I use more vealies to hold cash steady in dollars but let the percentage fall off to the new lower risk level.

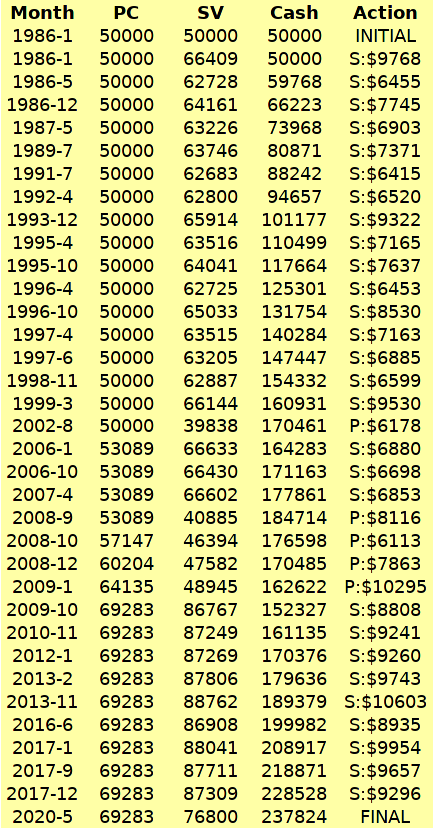

Classic AIM, 50% initial cash, with 10% of Stock Value for both SAFE and Minimum Trade size. Applied to the Dow since 1986, price only (dividends excluded), ignoring cash interest, monthly reviews.

Fundamentally you might opine that cash interest should be included, as then both share price and cash interest might broadly offset inflation, however there are three forms of gains, price appreciation, income and volatility capture (trading), and AIM is in part a volatility capture tool/mechanism such that we can rely upon AIM trading to in part help offset inflation, enabling cash interest to be ignored (spent, alongside spending dividends).

With monthly reviews AIM's trades were ...

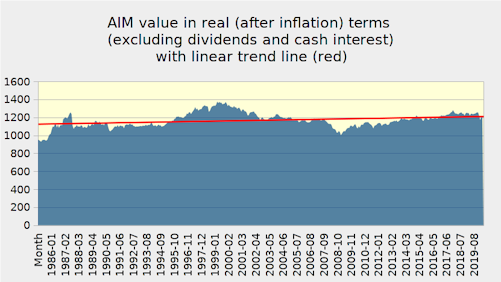

Resulting in a US$/inflation based AIM portfolio value of ...

So great, AIM without dividends or cash interest broadly offset inflation in a relatively consistent manner, leaving us free to spend dividends/cash interest.

However AIM expanded % cash, reduced # shares over time. For the above data it ended with 75% in cash, averaged 69% cash overall. Compared to 50/50 yearly rebalanced stock/cash that achieved a 6.9% annualised real (after inflation) gain, AIM achieved 6.4%. Had yearly rebalanced (that averaged 50% cash) been levelled to the same 69% average cash that AIM averaged then the results had AIM a little ahead, 6.4% compared to 6.2% for constant weighted (yearly rebalanced). [These are all real (after inflation) results, out of total returns - including all price appreciation, dividend/interest and trading gains, excluding costs/taxes]

However, when running with a portfolio massively heavy in cash, light on stock/shares that can be revised to 'correct' that issue. But when? If revised by not trading (selling shares) when AIM indicates to sell, but to instead just revise PC upwards, then that's like having virtually sold and then immediately repurchased shares, at a price level where AIM was indicating to sell/reduce (potentially a relatively high price). Better is to let cash accumulate, and then when AIM is indicating a Buy trade (potentially relatively low price), to only then 'correct' the AIM/portfolio (deploy surplus cash into stock/shares, and increase PC by the amount of stock value added).

In the above Dow AIM trades the first Buy trade that occurred in 2002-08 (end of August) at that time had around 80% in cash. Deploying some of that cash back into stock at that time (reducing AIM back to 50% cash) would have seen subsequent relatively good (above average) gains. The same for had the AIM been 'corrected' during the next period of when AIM was buying in 2008/9.

Can/does aligning to risk indicators better overall outcome compared to selective lumping cash back into stock at opportune moments when AIM is indicating to add/buy? My observations/test indicate not. Yes there is missed gains in more often having to wait longer before deploying surplus cash, but the overall benefits of deploying larger amounts when AIM was buying anyway is better than deploying smaller amounts earlier at times when AIM was indicating it to be appropriate to be reducing stock.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.