| Followers | 687 |

| Posts | 142844 |

| Boards Moderated | 35 |

| Alias Born | 03/10/2004 |

Saturday, October 26, 2019 9:52:58 AM

Subprime Auto Loans Blow Up, 60-Day Delinquencies Shoot Past Financial Crisis Peak

By: Wolf Richter | October 26, 2019

Santander Consumer USA is on the forefront of souring subprime-auto-loan backed securities.

Santander Consumer USA, one of the largest subprime auto lenders and the largest securitizer of subprime auto loans, is not alone. But it’s on the forefront. It had $26.3 billion of subprime auto loans as of June 30 that it either owned and carried on its books or that it had packaged into subprime-auto-loan backed securities and sold to investors; in terms of the loans that it collects payments on, 14.5% of the borrowers were delinquent, according to S&P Global Ratings, cited by Bloomberg.

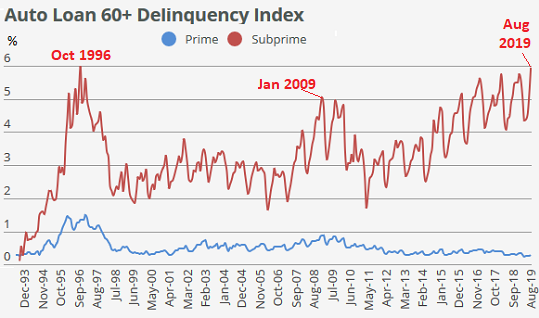

In the industry overall, subprime auto loans that have been packaged into asset-backed securities (ABS) are experiencing the highest delinquency rates in two decades, according to Fitch, which rates these securities. The 60-day delinquency rate surged to 5.93% in August, substantially higher than during the peak of the Financial Crisis at 5.04% in January 2009 (orange line, chart via Fitch):

But “prime” auto loans are holding up very well (blue line in the chart above): Their 60-day delinquency rate is hovering around a historically low 0.28%.

Santander’s loans include a surprising number that defaulted within the first few months, according to Moody’s Investors Service. These early-payment defaults (EPDs) are a hallmark of loosey-goosey underwriting standards that accomplish three things:

• Initially, they boost revenues from fees and high interest rates, and thus paper profits.

• They get weaker borrowers into loans with punitively high interest rates and payments so high that many borrowers will have to default.

• They enable or even encourage fraudulent loan applications.

Concerning the link between fraud and early-payment defaults, Frank McKenna, chief fraud strategist at PointPredictive, told Bloomberg: “We found that depending on the company, between 30% to 70% of auto loans that default in the first six months have some misrepresentation in the original loan file or application.”

OK. But Santander is not trying very hard to prevent fraud. In September, Moody’s pointed out that Santander had verified income on less than 3% of the subprime loans it packaged into over $1 billion of ABS that it was marketing to investors at the time. Income verification is not the only measure, but it’s an important measure of good underwriting practices. In these structured securities, where the highest-rated tranches carried a credit rating of Aaa, the lowest-rated tranches take the first losses, and the top-rated tranches could come out unscathed.

Moody’s said that it expected losses of 24% on this deal, far higher than 17% in losses that Moody’s expected on all of Santander’s ABS.

By comparison, Moody’s cited GM Financial, which also packages subprime auto loans into ABS: In a subprime-loan deal issued in June, it had verified income on 68% of the loans; and Moody’s expected losses of about 10%.

Even though Santander has sold these subprime-auto-loan-backed securities to investors, it is not entirely off the hook, especially when borrowers fail to make the first few payments – the infamous EPDs. It is then obligated to buy back those loans and eat the potential losses itself. According to a Bloomberg analysis, Santander was obligated to buy back 3% of the loans, which according to Moody’s, is a higher rate than Santander’s faced in its earlier securitizations.

But in a deal that it sold to investors last year, Santander has been obligated so far to buy back 6.7% of the loans mostly due to due EPDs, according to a Bloomberg analysis.

So these losses due to early-payment defaults were shifted from ABS holders back to Santander. Moody’s analyst Matt Scully put it this way: “The situation is somewhat perverse in that bondholders are actually benefiting from high early-payment defaults through the repurchases.”

Subprime-auto-loan-backed securities have other protections for bondholders, such as loss-absorbing buffers in form of additional auto loans beyond the face value of the securities.

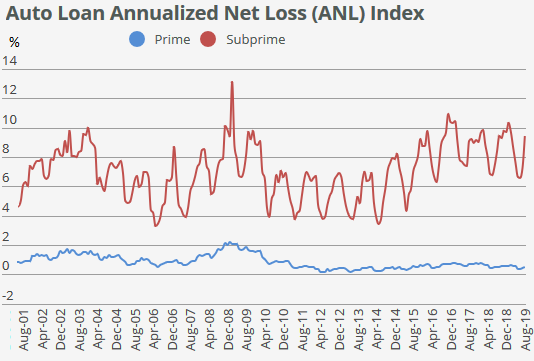

Nevertheless, the remaining losses are being eaten by the lower-rated tranches of the ABS. And the losses are piling up. According to Fitch, the subprime auto-loan Annualized Loss Ratio rose to 9.4% in August, up from 8.3% in August last year. During the peak of the Financial Crisis in February 2009, the ANL had spiked to 13.1%:

In terms of the overall auto-lending industry and the banking system, how much of a problem are we talking about?

Total auto loans and leases outstanding have soared to $1.3 trillion at the end of the second quarter. Typically, between 20% and 25% of the new loans and leases being originated each quarter are subprime rated. In the first half of this year, about 21% were subprime.

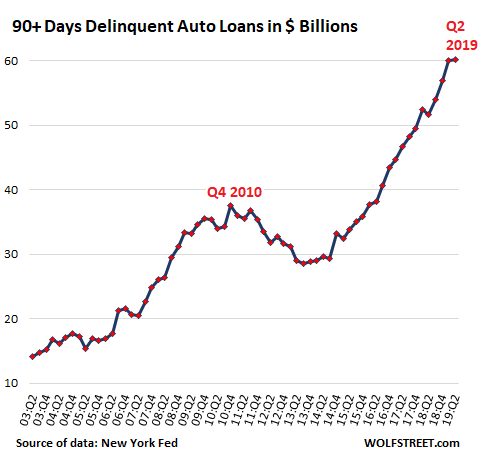

At the end of the second quarter, according to Federal Reserve data, 4.6% of those $1.3 trillion in auto loans and leases – subprime and prime combined – were 90+ days delinquent. This is where delinquencies were in Q3 2009 but below the Financial Crisis peak of 5.3%. In dollar terms, the 90+ delinquencies – most of them by subprime rated customers – amounted to $60 billion:

While delinquencies have skyrocketed, losses are just a small fraction of what subprime mortgages had generated during the Financial Crisis. Subprime auto loans, being about one-tenth the magnitude of subprime mortgages, are not going to take down the big banks. But smaller specialized non-bank lenders could collapse, and some of them have already collapsed.

Given the risks and losses, why is the industry engaging in subprime lending? And why are investors lapping up the subprime-auto-loan backed securities? Follow the money.

Subprime loans are immensely profitable. The dealer gets to sell a car and make a fatter profit on the car itself and on arranging the loan because subprime borrowers know they’re having trouble getting loans, and there is often no negotiation on price, interest rates, or payments. Subprime customers are sitting ducks.

Subprime loans are also high-risk, and lenders want to earn higher rates of return – and charge higher interest rates – to be compensated for the risk. So, until the loans sour, lenders make more money on subprime loans.

At first, everyone is happy. The dealer made lots of money. The lender made lots of money. Investors earn a higher yield on their ABS. And the customer, who is paying out of the nose for all this, is driving a nice car.

But a customer that is struggling and already has some credit problems – which is why the credit score is below “prime” – may have trouble making the payments on a car loan with a 21% interest rate financing not only the car but also the fat profits of the dealer.

It’s quick these days to repo a car and sell it at a wholesale auction. The used-vehicle market is liquid, and transactions are fast, unlike the housing market. So a lender will take some loss on a defaulted car loan, perhaps 30% or 40% of loan value. But given the profits made on the loan before it defaulted and on the loans that do not default, subprime lending, when greed isn’t allowed to run wild, remains a profitable business overall. And it allows customers with subprime credit to buy a car despite the risks for lenders.

Read Full Story »»»

DiscoverGold

DiscoverGold

By: Wolf Richter | October 26, 2019

Santander Consumer USA is on the forefront of souring subprime-auto-loan backed securities.

Santander Consumer USA, one of the largest subprime auto lenders and the largest securitizer of subprime auto loans, is not alone. But it’s on the forefront. It had $26.3 billion of subprime auto loans as of June 30 that it either owned and carried on its books or that it had packaged into subprime-auto-loan backed securities and sold to investors; in terms of the loans that it collects payments on, 14.5% of the borrowers were delinquent, according to S&P Global Ratings, cited by Bloomberg.

In the industry overall, subprime auto loans that have been packaged into asset-backed securities (ABS) are experiencing the highest delinquency rates in two decades, according to Fitch, which rates these securities. The 60-day delinquency rate surged to 5.93% in August, substantially higher than during the peak of the Financial Crisis at 5.04% in January 2009 (orange line, chart via Fitch):

But “prime” auto loans are holding up very well (blue line in the chart above): Their 60-day delinquency rate is hovering around a historically low 0.28%.

Santander’s loans include a surprising number that defaulted within the first few months, according to Moody’s Investors Service. These early-payment defaults (EPDs) are a hallmark of loosey-goosey underwriting standards that accomplish three things:

• Initially, they boost revenues from fees and high interest rates, and thus paper profits.

• They get weaker borrowers into loans with punitively high interest rates and payments so high that many borrowers will have to default.

• They enable or even encourage fraudulent loan applications.

Concerning the link between fraud and early-payment defaults, Frank McKenna, chief fraud strategist at PointPredictive, told Bloomberg: “We found that depending on the company, between 30% to 70% of auto loans that default in the first six months have some misrepresentation in the original loan file or application.”

OK. But Santander is not trying very hard to prevent fraud. In September, Moody’s pointed out that Santander had verified income on less than 3% of the subprime loans it packaged into over $1 billion of ABS that it was marketing to investors at the time. Income verification is not the only measure, but it’s an important measure of good underwriting practices. In these structured securities, where the highest-rated tranches carried a credit rating of Aaa, the lowest-rated tranches take the first losses, and the top-rated tranches could come out unscathed.

Moody’s said that it expected losses of 24% on this deal, far higher than 17% in losses that Moody’s expected on all of Santander’s ABS.

By comparison, Moody’s cited GM Financial, which also packages subprime auto loans into ABS: In a subprime-loan deal issued in June, it had verified income on 68% of the loans; and Moody’s expected losses of about 10%.

Even though Santander has sold these subprime-auto-loan-backed securities to investors, it is not entirely off the hook, especially when borrowers fail to make the first few payments – the infamous EPDs. It is then obligated to buy back those loans and eat the potential losses itself. According to a Bloomberg analysis, Santander was obligated to buy back 3% of the loans, which according to Moody’s, is a higher rate than Santander’s faced in its earlier securitizations.

But in a deal that it sold to investors last year, Santander has been obligated so far to buy back 6.7% of the loans mostly due to due EPDs, according to a Bloomberg analysis.

So these losses due to early-payment defaults were shifted from ABS holders back to Santander. Moody’s analyst Matt Scully put it this way: “The situation is somewhat perverse in that bondholders are actually benefiting from high early-payment defaults through the repurchases.”

Subprime-auto-loan-backed securities have other protections for bondholders, such as loss-absorbing buffers in form of additional auto loans beyond the face value of the securities.

Nevertheless, the remaining losses are being eaten by the lower-rated tranches of the ABS. And the losses are piling up. According to Fitch, the subprime auto-loan Annualized Loss Ratio rose to 9.4% in August, up from 8.3% in August last year. During the peak of the Financial Crisis in February 2009, the ANL had spiked to 13.1%:

In terms of the overall auto-lending industry and the banking system, how much of a problem are we talking about?

Total auto loans and leases outstanding have soared to $1.3 trillion at the end of the second quarter. Typically, between 20% and 25% of the new loans and leases being originated each quarter are subprime rated. In the first half of this year, about 21% were subprime.

At the end of the second quarter, according to Federal Reserve data, 4.6% of those $1.3 trillion in auto loans and leases – subprime and prime combined – were 90+ days delinquent. This is where delinquencies were in Q3 2009 but below the Financial Crisis peak of 5.3%. In dollar terms, the 90+ delinquencies – most of them by subprime rated customers – amounted to $60 billion:

While delinquencies have skyrocketed, losses are just a small fraction of what subprime mortgages had generated during the Financial Crisis. Subprime auto loans, being about one-tenth the magnitude of subprime mortgages, are not going to take down the big banks. But smaller specialized non-bank lenders could collapse, and some of them have already collapsed.

Given the risks and losses, why is the industry engaging in subprime lending? And why are investors lapping up the subprime-auto-loan backed securities? Follow the money.

Subprime loans are immensely profitable. The dealer gets to sell a car and make a fatter profit on the car itself and on arranging the loan because subprime borrowers know they’re having trouble getting loans, and there is often no negotiation on price, interest rates, or payments. Subprime customers are sitting ducks.

Subprime loans are also high-risk, and lenders want to earn higher rates of return – and charge higher interest rates – to be compensated for the risk. So, until the loans sour, lenders make more money on subprime loans.

At first, everyone is happy. The dealer made lots of money. The lender made lots of money. Investors earn a higher yield on their ABS. And the customer, who is paying out of the nose for all this, is driving a nice car.

But a customer that is struggling and already has some credit problems – which is why the credit score is below “prime” – may have trouble making the payments on a car loan with a 21% interest rate financing not only the car but also the fat profits of the dealer.

It’s quick these days to repo a car and sell it at a wholesale auction. The used-vehicle market is liquid, and transactions are fast, unlike the housing market. So a lender will take some loss on a defaulted car loan, perhaps 30% or 40% of loan value. But given the profits made on the loan before it defaulted and on the loans that do not default, subprime lending, when greed isn’t allowed to run wild, remains a profitable business overall. And it allows customers with subprime credit to buy a car despite the risks for lenders.

Read Full Story »»»

DiscoverGold

DiscoverGold

Information posted to this board is not meant to suggest any specific action, but to point out the technical signs that can help our readers make their own specific decisions. Your Due Dilegence is a must!

• DiscoverGold

Join the InvestorsHub Community

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.