| Followers | 679 |

| Posts | 140848 |

| Boards Moderated | 36 |

| Alias Born | 03/10/2004 |

Monday, October 14, 2019 9:27:50 AM

The Maximum Pain for SPY Option Buyers This Week

By: Schaeffer's Investment Research | October 14, 2019

• The 14 level could come into play for the VIX in the near term

• The low bar set for earnings, plus elevated short interest, could be a boon for bulls

"Since late April, when the SPX touched 2,950 after going pretty much straight up since the December low, the action can best be described as ‘messy,’ with a range mostly between 2,850 and 3,000…Expect more of the same in the coming weeks – ‘messy action’ in equity benchmarks. A plethora of uncertainties has been thrown at market participants, ranging from how the Fed will deal with slowing world growth and China-U.S. trade tensions, to the instability in Hong Kong and the Middle East, a potential presidential impeachment, Brexit, and others."

-- Monday Morning Outlook, October 7, 2019

The action last week can best be described as messy, with the S&P 500 Index (SPX - 2,970.27) beginning the week below 2,950, and quickly gapping down to the round 2,900 century mark on Tuesday morning. The gap was spurred by headlines that the Trump administration was threatening to block pension companies from investing in publicly traded Chinese companies, in addition to blacklisting several big Chinese tech firms from doing business with U.S. companies, and restricting visas for some Chinese officials based on human rights violations.

The actions were perceived as threatening to progress on the trade negotiations, which were slated to begin later in the week. But as trade negotiations neared, intraday fluctuations were abundant and driven by headlines, rumors, tweets, and even various Fed governors talking, including Fed Chair Jerome Powell. The swings resulted in zero net direction from Monday’s close into Thursday’s close.

A trendline connecting higher lows since June was the site of Tuesday’s low. In Friday’s pre-market trading, S&P futures were back above the key 2,950 level on the heels of headlines suggesting talks were going well and a partial trade deal was imminent. The move through 2,950 was progress from a technical perspective, given it has acted as both intermediate-term and short-term resistance on numerous occasions since October 2018, as noted in last week’s commentary.

S&P futures were also boosted by hints that the U.K. could strike a deal with the European Union ahead of the Oct. 31 Brexit deadline. Finally, and perhaps viewed as a "trifecta" for bulls, the Federal Reserve gave details on boosting its balance sheet via Treasury bill purchases into the second quarter of 2020, to address concerns about strains in bank funding rates that suddenly popped up last month.

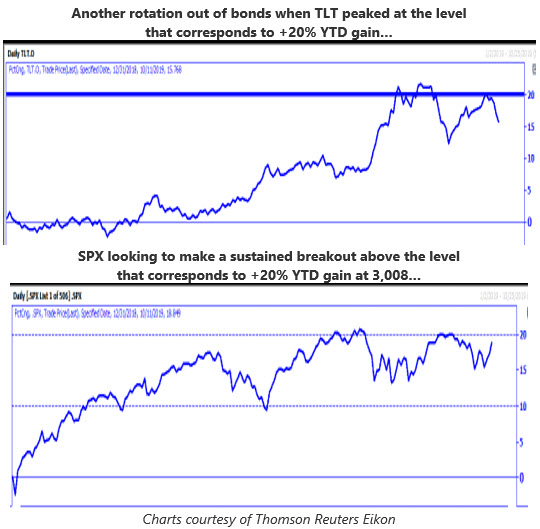

"... SPX, iShares 20+ Year Treasury Bond ETF (TLT - 145.99), and SPDR Gold Shares (GLD - 141.90) – as rallies have been capped around levels that represent their respective plus-20% zones."

-- Monday Morning Outlook, October 7, 2019

Traders bid stocks higher for the second consecutive Friday, with the move through 2,950 coincidental with a positive backdrop on trade, Brexit, and the Federal Reserve. That said, the SPX enters options expiration week just below another layer of historical resistance: the round 3,000 millennium mark, which is just below the SPX’s 20% year-to-date (YTD) gain at 3,008. Bonds, as represented by the iShares 20+ Year Treasury Bond ETF (TLT - 140.44), experienced a sharp retreat from the round 20% YTD level last week, amid a rotation out of bonds into stocks.

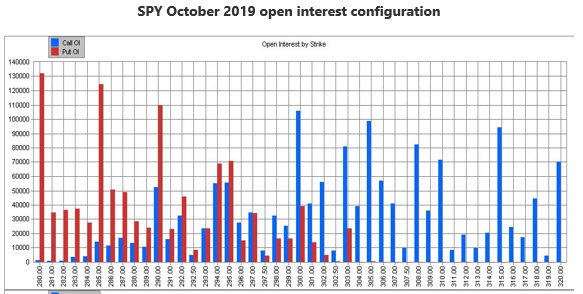

The choppy action with little net direction during the past six months is welcomed by option premium sellers, looking to pocket the option premium they sold in anticipation of support and resistance levels holding. Speaking of which, as we enter October standard expiration week, the maximum pain for SPDR S&P 500 ETF Trust (SPY - 296.28) option buyers -- which is the level at which the largest number of puts and calls expire worthless -- is at the 293 strike, per the open interest configuration graph below.

It would take a decline below the put-heavy 290 strike to put delta-hedge selling in play. Meanwhile, big call open interest resides at the 300 strike, equivalent to SPX 3,000, and premium sellers will work to defend a move above this level. This was evident late Friday, as the SPX sold off in the last 15 minutes of trading after sniffing the 3,000 area. Most of this open interest was bought to open at the 300 strike, setting up the potential for delta-hedge buying that pushes the SPY to $305, or SPX to 3,050, if sellers are unable to defend the SPY 300 strike successfully.

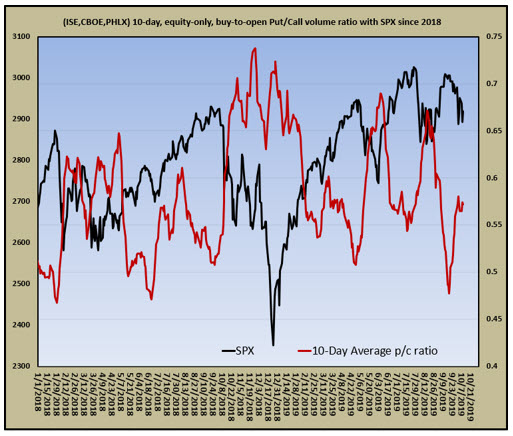

"It was just a few weeks ago when I cautioned that the increasing optimism among equity option buyers made stocks vulnerable in the short term ... The risk to bulls, if the SPX is below 2,950, is the ratio continuing to rise since it is not yet at level that has typically marked short-term bottoms that occur when speculative pessimism is widespread."

-- Monday Morning Outlook, October 7, 2019

With some clarity emerging last week on a few uncertainties overhanging the market, the sentiment among short-term traders is neither one that suggests excessive optimism nor pessimism when looking into the actions of equity option buyers. That said, there was a build in pessimism relative to few weeks ago, when short-term traders turned very optimistic just ahead of a pullback in stocks. I would not be surprised to see the ratio of equity put buying to call buying turn lower in the days ahead, but given it could turn lower from relative-low level, there may not be as much buying power relative to when this ratio turns lower from a higher level.

"With less than a week to go before earnings season kicks off in earnest with results from major banks, analysts estimate companies in the S&P 500 will report a 4.5% drop in profits from the year-earlier period, according to FactSet."

-- The Wall Street Journal (subscription required), October 11, 2019

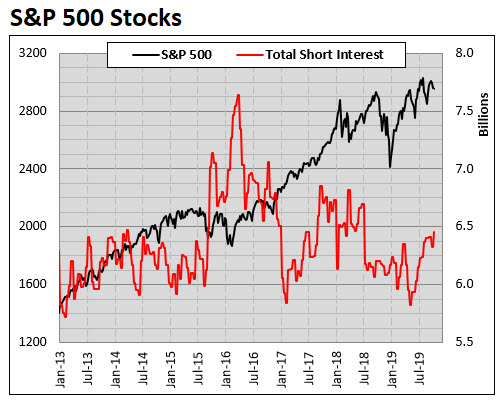

A couple of factors that could be supportive of stocks in the weeks ahead is the contrarian implications of low earnings expectations as we move into earnings season. And, since late April, when the SPX was trading around 2,950, short interest on SPX component stocks is up nearly 11%.

In other words, stocks have held their own amid a plethora of shorting activity that has pushed total short interest on SPX components to the highest level since June 2018. With a relatively low bar set with respect to earnings, and more clarity on China-U.S. trade, an unwinding of the six-month build in short interest could be what is needed to push the SPX above the top of its range.

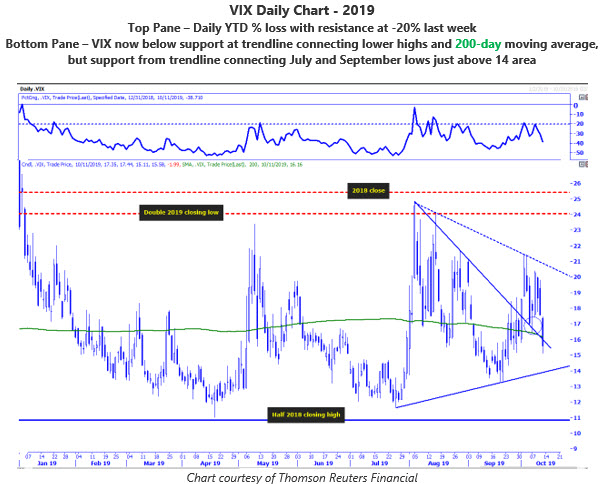

"The VIX peak at the round 20 area was interesting, as not only is this a round number, but it also marks an area roughly 20% below its 2018 close. The VIX's negative-20% year-to-date (YTD) level has marked several peaks in 2019 ... By Friday, the VIX was meandering around the 18 area and in between two trendlines that I have drawn connecting various highs since its early August peak in the 24 area, which is double its 2019 closing low. An ‘all clear’ for a continued decline in volatility would be a close below the lower trendline, which is also in the vicinity of the VIX's 200-day moving average. A close above 20 would enhance the odds of volatility spike into the 24 area."

-- Monday Morning Outlook, October 7, 2019

After another "mini-spike" in the Cboe Volatility Index (VIX - 15.58) early last week, the VIX retreated substantially as headlines on trade showed progress being made. In fact, as you can see in the chart below (top pane), for the second time in as many weeks, the VIX peaked at the round 20 level, which coincides with the round negative-20% year-to-date return.

The "all-clear" signal for a near-term decline in volatility triggered as of Friday’s close, as the VIX closed below its 200-day moving average and a trendline connecting lower highs since the early-August peak. The question is: "How much room is there for a volatility decline?” -- the VIX is in a triangle formation when considering the July and September lows. Therefore, the 14 area could come into play as a potential floor in the days and weeks ahead, coincident with an SPX rally into potential resistance in the 3,000 to 3,010 area.

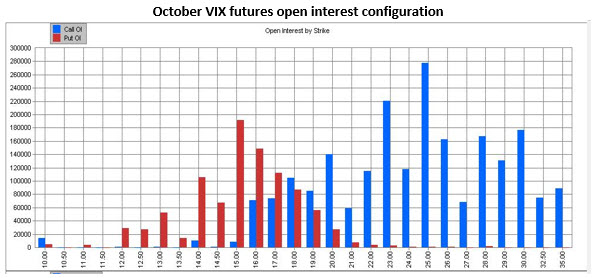

Moreover, October VIX futures options expire on Wednesday, and for at least the next couple of days, there will be an effort to keep the VIX above peak put open interest at the 15 strike into mid-week. That said, it is interesting that the VIX never really got above the 20 strike, which is where the big call open interest build-up begins in the October series.

A risk to bulls is that volatility pops usually occur after a huge number of calls expire worthless, as those short volatility futures (and there are many of them) may no longer be hedged after October VIX expiration, and are thus more susceptible to cover short volatility futures positions if a headline emerges that could send volatility expectations higher.

Read Full Story »»»

DiscoverGold

DiscoverGold

By: Schaeffer's Investment Research | October 14, 2019

• The 14 level could come into play for the VIX in the near term

• The low bar set for earnings, plus elevated short interest, could be a boon for bulls

"Since late April, when the SPX touched 2,950 after going pretty much straight up since the December low, the action can best be described as ‘messy,’ with a range mostly between 2,850 and 3,000…Expect more of the same in the coming weeks – ‘messy action’ in equity benchmarks. A plethora of uncertainties has been thrown at market participants, ranging from how the Fed will deal with slowing world growth and China-U.S. trade tensions, to the instability in Hong Kong and the Middle East, a potential presidential impeachment, Brexit, and others."

-- Monday Morning Outlook, October 7, 2019

The action last week can best be described as messy, with the S&P 500 Index (SPX - 2,970.27) beginning the week below 2,950, and quickly gapping down to the round 2,900 century mark on Tuesday morning. The gap was spurred by headlines that the Trump administration was threatening to block pension companies from investing in publicly traded Chinese companies, in addition to blacklisting several big Chinese tech firms from doing business with U.S. companies, and restricting visas for some Chinese officials based on human rights violations.

The actions were perceived as threatening to progress on the trade negotiations, which were slated to begin later in the week. But as trade negotiations neared, intraday fluctuations were abundant and driven by headlines, rumors, tweets, and even various Fed governors talking, including Fed Chair Jerome Powell. The swings resulted in zero net direction from Monday’s close into Thursday’s close.

A trendline connecting higher lows since June was the site of Tuesday’s low. In Friday’s pre-market trading, S&P futures were back above the key 2,950 level on the heels of headlines suggesting talks were going well and a partial trade deal was imminent. The move through 2,950 was progress from a technical perspective, given it has acted as both intermediate-term and short-term resistance on numerous occasions since October 2018, as noted in last week’s commentary.

S&P futures were also boosted by hints that the U.K. could strike a deal with the European Union ahead of the Oct. 31 Brexit deadline. Finally, and perhaps viewed as a "trifecta" for bulls, the Federal Reserve gave details on boosting its balance sheet via Treasury bill purchases into the second quarter of 2020, to address concerns about strains in bank funding rates that suddenly popped up last month.

"... SPX, iShares 20+ Year Treasury Bond ETF (TLT - 145.99), and SPDR Gold Shares (GLD - 141.90) – as rallies have been capped around levels that represent their respective plus-20% zones."

-- Monday Morning Outlook, October 7, 2019

Traders bid stocks higher for the second consecutive Friday, with the move through 2,950 coincidental with a positive backdrop on trade, Brexit, and the Federal Reserve. That said, the SPX enters options expiration week just below another layer of historical resistance: the round 3,000 millennium mark, which is just below the SPX’s 20% year-to-date (YTD) gain at 3,008. Bonds, as represented by the iShares 20+ Year Treasury Bond ETF (TLT - 140.44), experienced a sharp retreat from the round 20% YTD level last week, amid a rotation out of bonds into stocks.

The choppy action with little net direction during the past six months is welcomed by option premium sellers, looking to pocket the option premium they sold in anticipation of support and resistance levels holding. Speaking of which, as we enter October standard expiration week, the maximum pain for SPDR S&P 500 ETF Trust (SPY - 296.28) option buyers -- which is the level at which the largest number of puts and calls expire worthless -- is at the 293 strike, per the open interest configuration graph below.

It would take a decline below the put-heavy 290 strike to put delta-hedge selling in play. Meanwhile, big call open interest resides at the 300 strike, equivalent to SPX 3,000, and premium sellers will work to defend a move above this level. This was evident late Friday, as the SPX sold off in the last 15 minutes of trading after sniffing the 3,000 area. Most of this open interest was bought to open at the 300 strike, setting up the potential for delta-hedge buying that pushes the SPY to $305, or SPX to 3,050, if sellers are unable to defend the SPY 300 strike successfully.

"It was just a few weeks ago when I cautioned that the increasing optimism among equity option buyers made stocks vulnerable in the short term ... The risk to bulls, if the SPX is below 2,950, is the ratio continuing to rise since it is not yet at level that has typically marked short-term bottoms that occur when speculative pessimism is widespread."

-- Monday Morning Outlook, October 7, 2019

With some clarity emerging last week on a few uncertainties overhanging the market, the sentiment among short-term traders is neither one that suggests excessive optimism nor pessimism when looking into the actions of equity option buyers. That said, there was a build in pessimism relative to few weeks ago, when short-term traders turned very optimistic just ahead of a pullback in stocks. I would not be surprised to see the ratio of equity put buying to call buying turn lower in the days ahead, but given it could turn lower from relative-low level, there may not be as much buying power relative to when this ratio turns lower from a higher level.

"With less than a week to go before earnings season kicks off in earnest with results from major banks, analysts estimate companies in the S&P 500 will report a 4.5% drop in profits from the year-earlier period, according to FactSet."

-- The Wall Street Journal (subscription required), October 11, 2019

A couple of factors that could be supportive of stocks in the weeks ahead is the contrarian implications of low earnings expectations as we move into earnings season. And, since late April, when the SPX was trading around 2,950, short interest on SPX component stocks is up nearly 11%.

In other words, stocks have held their own amid a plethora of shorting activity that has pushed total short interest on SPX components to the highest level since June 2018. With a relatively low bar set with respect to earnings, and more clarity on China-U.S. trade, an unwinding of the six-month build in short interest could be what is needed to push the SPX above the top of its range.

"The VIX peak at the round 20 area was interesting, as not only is this a round number, but it also marks an area roughly 20% below its 2018 close. The VIX's negative-20% year-to-date (YTD) level has marked several peaks in 2019 ... By Friday, the VIX was meandering around the 18 area and in between two trendlines that I have drawn connecting various highs since its early August peak in the 24 area, which is double its 2019 closing low. An ‘all clear’ for a continued decline in volatility would be a close below the lower trendline, which is also in the vicinity of the VIX's 200-day moving average. A close above 20 would enhance the odds of volatility spike into the 24 area."

-- Monday Morning Outlook, October 7, 2019

After another "mini-spike" in the Cboe Volatility Index (VIX - 15.58) early last week, the VIX retreated substantially as headlines on trade showed progress being made. In fact, as you can see in the chart below (top pane), for the second time in as many weeks, the VIX peaked at the round 20 level, which coincides with the round negative-20% year-to-date return.

The "all-clear" signal for a near-term decline in volatility triggered as of Friday’s close, as the VIX closed below its 200-day moving average and a trendline connecting lower highs since the early-August peak. The question is: "How much room is there for a volatility decline?” -- the VIX is in a triangle formation when considering the July and September lows. Therefore, the 14 area could come into play as a potential floor in the days and weeks ahead, coincident with an SPX rally into potential resistance in the 3,000 to 3,010 area.

Moreover, October VIX futures options expire on Wednesday, and for at least the next couple of days, there will be an effort to keep the VIX above peak put open interest at the 15 strike into mid-week. That said, it is interesting that the VIX never really got above the 20 strike, which is where the big call open interest build-up begins in the October series.

A risk to bulls is that volatility pops usually occur after a huge number of calls expire worthless, as those short volatility futures (and there are many of them) may no longer be hedged after October VIX expiration, and are thus more susceptible to cover short volatility futures positions if a headline emerges that could send volatility expectations higher.

Read Full Story »»»

DiscoverGold

DiscoverGold

Information posted to this board is not meant to suggest any specific action, but to point out the technical signs that can help our readers make their own specific decisions. Your Due Dilegence is a must!

• DiscoverGold

Join the InvestorsHub Community

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.