Friday, September 06, 2019 3:39:46 PM

RAIT Financial Trust: Senior-Notes Holders Should Be Safe In Bankruptcy; Equity Likely Cancelled

Sep. 6, 2019 8:54 AM ET Paolo Gorgo

"Summary

RAIT Financial Trust filed for bankruptcy. Holders of Senior Notes should receive their payment in full, and equity will likely be cancelled.

Preferred holders are also at risk of receiving no recovery at all, according to the company’s first bankruptcy dockets.

However, recent documents highlight that an Ad Hoc Committee of Holders of Preferred and Common Equity has been formed - a potential positive presence supporting preferred holders’ position.

Last Friday, RAIT Financial Trust (OTCQB:RASF) (RASFQ) filed for Chapter 11 - just ahead of a long weekend, and on the exact day its 7.125% Notes (OTCQB:RFTA) were due for redemption.

The company plans to sell its assets to a buyer affiliated with Fortress Investment Group LLC for $174.4 million through a court approved sale process under Section 363 of the United States Bankruptcy Code, which allows for higher or better offers.

Background

Since early 2018, in an effort to increase liquidity and better position the company to meet its financial obligations, RAIT made changes to its business operations, which included the suspension of new investment opportunities and its loan origination business, and the sale of a portion of its owned real estate and loan portfolio.

In simpler words, as Petition summarized it, RAIT has "been in a state of perpetual restructuring AND marketing going as far back as Q3 '17".

After filing its Annual Report for the fiscal year ended December 31, 2018, RAIT stopped producing its quarterly reports as the company was completing an evaluation of whether its investments in preferred equity interests should be accounted for as loans or as equity method investments, a decision that included, later on, requesting "accounting guidance from the SEC's Office of the Chief Accountant".

From an investor's viewpoint, the company stopped providing updated financial information, leaving all credit and equity holders in the dark, exactly when it started shopping its assets:

Source: Docket n. 7, pg. 20 - You may find RAIT's court filings and other documents related to the bankruptcy proceedings here.

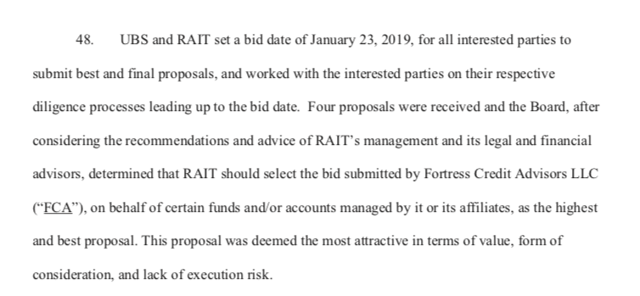

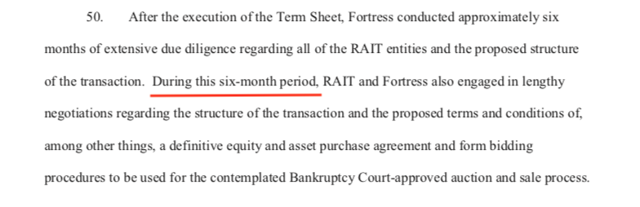

Six months of extensive due diligence were necessary to close a deal, which will be subject to a court supervised sale process:

RAIT Fortress six months negotiationsSource: docket n. 7, pg. 20; emphasis added.

There are several tickers linked to RAIT's equity and debt instruments; however, before we try to help investors tracking them properly after the bankruptcy filing, we should note that the company's failure to pay the principal amount of its 7.125% Notes (RFTA) by their maturity date on August 30, 2019, created a strange situation for the holders of those notes that have not been tradable for a few days. A new ticker, RFTZQ, has been added on September 5th to allow owners of these securities to sell them, if they prefer.

Here is an updated list of RAIT's listed equity and debt instruments, with their new tickers as of September 4th:

How to trade RAIT's bankruptcy?

Investors should always be very careful when dealing with bankruptcy companies - especially in complex situations like RAIT. As we already noticed, the company has not filed updated financial data, and the last official document available relates to the company's fiscal year ended December 31, 2018.

For example, RAIT's cash and cash equivalents balance as of December 31, 2018, was $42.5 million and, as of March 15, 2019, it was $40.2 million, while restricted cash available as of December 31, 2018, was $63 million (link, pg. 4).

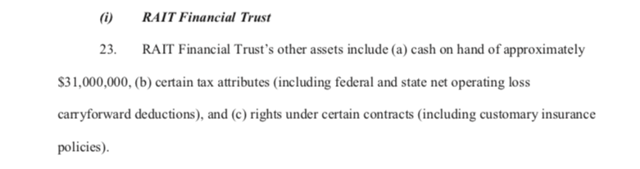

From the bankruptcy filing, we now learn that the company has $31 million of cash available, which is good news as it will not need to look for a (usually very expensive and super-priority) DIP financing, but certainly bad news compared to the $42.5 million available less than six months ago:

Source: Docket n. 7, pg. 10

To quickly summarize the few information available as we write, RAIT has $31 million of cash available, and the sale of its assets should bring at least $174.4 million, for a total of roughly $205 million.

According to RAIT, this amount of money will be sufficient to repay in full "holders of the 7.125% Senior Notes, holders of the 7.625% Senior Notes, and all administrative, priority and general unsecured claims".

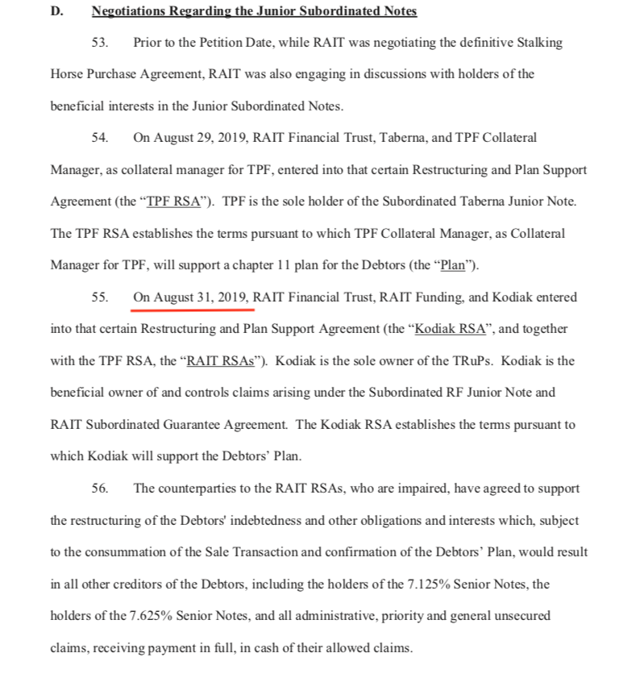

Source: Docket n. 7, pg. 22; emphasis added on the date of Kodiak agreement, subsequent to the Chapter 11 filing

Holders of the beneficial interests in the Junior Subordinated Notes are described as "impaired" - in other words, pursuant to the RSAs, each of the RSA counterparties has agreed, subject to certain conditions, to accept less than the total unpaid amounts due under the 2035 Note and the 2037 Note.

There are obviously several pieces of the puzzle still missing, but the fact that holders of the Junior Subordinated Notes are said to accept a partial recovery shouldn't bring good news to preferred and equity holders.

In particular, given the presence of roughly $290 million, in value, of preferred shares, senior to equity, we do not expect any recovery for shareholders. (RASFQ).

At the moment, we see preferred holders at risk of receiving little or no recovery at all, unless there is a bidding war for the assets or better-than-expected news on the liability side, which will include bankruptcy costs.

We noticed, however, that an Ad Hoc Committee of Holders of Preferred and Common Equity has been formed, which could bode well at least for preferred holders, as they could have a voice heard during the bankruptcy proceeding.

A controversial area that could be investigated by the Ad Hoc Committee of Holders of Preferred and Common Equity is the redemption of RAIT's Series D preferred shares in June 2018, and the company's black out in communication with debt and equity holders since filing RAIT's 2018 report.

The Purchase Agreement, the Kodiak RSA and the Taberna RSA are key missing pieces to get a better understanding of the whole picture. According to RAIT latest filing, they should "be filed as exhibits to RAIT's Quarterly Report on Form 10-Q for the quarterly period ending September 30, 2019".

Investors with some appetite for risk might consider buying the 7.625% Notes (OTCQB:RFTT), now (RFTTQ).

On September 3rd, the notes traded at about $22, on an unusual high volume of over 120,000 shares.

In roughly six months (the expected time to close the bankruptcy sale), they might approach their full $25 value - unless the whole deal collapses, obviously..."

https://seekingalpha.com/article/4290126-rait-financial-trust-senior-notes-holders-safe-bankruptcy-equity-likely-cancelled

Sep. 6, 2019 8:54 AM ET Paolo Gorgo

"Summary

RAIT Financial Trust filed for bankruptcy. Holders of Senior Notes should receive their payment in full, and equity will likely be cancelled.

Preferred holders are also at risk of receiving no recovery at all, according to the company’s first bankruptcy dockets.

However, recent documents highlight that an Ad Hoc Committee of Holders of Preferred and Common Equity has been formed - a potential positive presence supporting preferred holders’ position.

Last Friday, RAIT Financial Trust (OTCQB:RASF) (RASFQ) filed for Chapter 11 - just ahead of a long weekend, and on the exact day its 7.125% Notes (OTCQB:RFTA) were due for redemption.

The company plans to sell its assets to a buyer affiliated with Fortress Investment Group LLC for $174.4 million through a court approved sale process under Section 363 of the United States Bankruptcy Code, which allows for higher or better offers.

Background

Since early 2018, in an effort to increase liquidity and better position the company to meet its financial obligations, RAIT made changes to its business operations, which included the suspension of new investment opportunities and its loan origination business, and the sale of a portion of its owned real estate and loan portfolio.

In simpler words, as Petition summarized it, RAIT has "been in a state of perpetual restructuring AND marketing going as far back as Q3 '17".

After filing its Annual Report for the fiscal year ended December 31, 2018, RAIT stopped producing its quarterly reports as the company was completing an evaluation of whether its investments in preferred equity interests should be accounted for as loans or as equity method investments, a decision that included, later on, requesting "accounting guidance from the SEC's Office of the Chief Accountant".

From an investor's viewpoint, the company stopped providing updated financial information, leaving all credit and equity holders in the dark, exactly when it started shopping its assets:

Source: Docket n. 7, pg. 20 - You may find RAIT's court filings and other documents related to the bankruptcy proceedings here.

Six months of extensive due diligence were necessary to close a deal, which will be subject to a court supervised sale process:

RAIT Fortress six months negotiationsSource: docket n. 7, pg. 20; emphasis added.

There are several tickers linked to RAIT's equity and debt instruments; however, before we try to help investors tracking them properly after the bankruptcy filing, we should note that the company's failure to pay the principal amount of its 7.125% Notes (RFTA) by their maturity date on August 30, 2019, created a strange situation for the holders of those notes that have not been tradable for a few days. A new ticker, RFTZQ, has been added on September 5th to allow owners of these securities to sell them, if they prefer.

Here is an updated list of RAIT's listed equity and debt instruments, with their new tickers as of September 4th:

How to trade RAIT's bankruptcy?

Investors should always be very careful when dealing with bankruptcy companies - especially in complex situations like RAIT. As we already noticed, the company has not filed updated financial data, and the last official document available relates to the company's fiscal year ended December 31, 2018.

For example, RAIT's cash and cash equivalents balance as of December 31, 2018, was $42.5 million and, as of March 15, 2019, it was $40.2 million, while restricted cash available as of December 31, 2018, was $63 million (link, pg. 4).

From the bankruptcy filing, we now learn that the company has $31 million of cash available, which is good news as it will not need to look for a (usually very expensive and super-priority) DIP financing, but certainly bad news compared to the $42.5 million available less than six months ago:

Source: Docket n. 7, pg. 10

To quickly summarize the few information available as we write, RAIT has $31 million of cash available, and the sale of its assets should bring at least $174.4 million, for a total of roughly $205 million.

According to RAIT, this amount of money will be sufficient to repay in full "holders of the 7.125% Senior Notes, holders of the 7.625% Senior Notes, and all administrative, priority and general unsecured claims".

Source: Docket n. 7, pg. 22; emphasis added on the date of Kodiak agreement, subsequent to the Chapter 11 filing

Holders of the beneficial interests in the Junior Subordinated Notes are described as "impaired" - in other words, pursuant to the RSAs, each of the RSA counterparties has agreed, subject to certain conditions, to accept less than the total unpaid amounts due under the 2035 Note and the 2037 Note.

There are obviously several pieces of the puzzle still missing, but the fact that holders of the Junior Subordinated Notes are said to accept a partial recovery shouldn't bring good news to preferred and equity holders.

In particular, given the presence of roughly $290 million, in value, of preferred shares, senior to equity, we do not expect any recovery for shareholders. (RASFQ).

At the moment, we see preferred holders at risk of receiving little or no recovery at all, unless there is a bidding war for the assets or better-than-expected news on the liability side, which will include bankruptcy costs.

We noticed, however, that an Ad Hoc Committee of Holders of Preferred and Common Equity has been formed, which could bode well at least for preferred holders, as they could have a voice heard during the bankruptcy proceeding.

A controversial area that could be investigated by the Ad Hoc Committee of Holders of Preferred and Common Equity is the redemption of RAIT's Series D preferred shares in June 2018, and the company's black out in communication with debt and equity holders since filing RAIT's 2018 report.

The Purchase Agreement, the Kodiak RSA and the Taberna RSA are key missing pieces to get a better understanding of the whole picture. According to RAIT latest filing, they should "be filed as exhibits to RAIT's Quarterly Report on Form 10-Q for the quarterly period ending September 30, 2019".

Investors with some appetite for risk might consider buying the 7.625% Notes (OTCQB:RFTT), now (RFTTQ).

On September 3rd, the notes traded at about $22, on an unusual high volume of over 120,000 shares.

In roughly six months (the expected time to close the bankruptcy sale), they might approach their full $25 value - unless the whole deal collapses, obviously..."

https://seekingalpha.com/article/4290126-rait-financial-trust-senior-notes-holders-safe-bankruptcy-equity-likely-cancelled

The only breaks you get in life...are those you give yourself!!!

Join the InvestorsHub Community

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.