Tuesday, June 25, 2019 4:22:20 PM

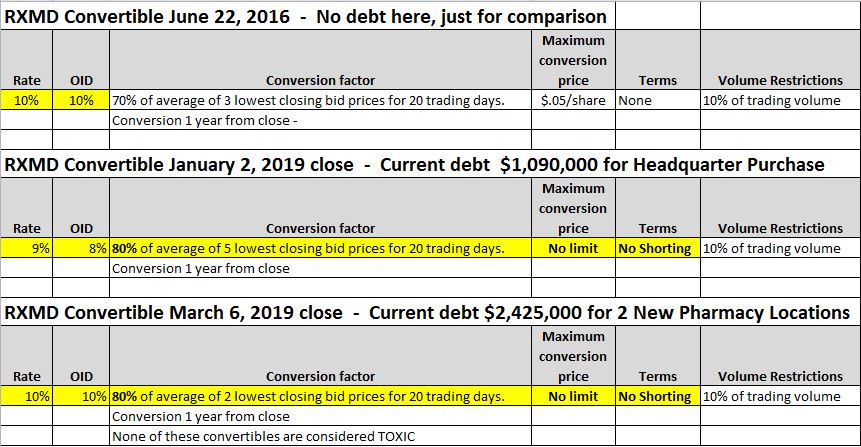

The current convertible debt funding agreement balance is $3,515,000. This is comprised of two tranche’s that have been drawn which consist of the following:

1. On January 2, 2019, the Company entered into a securities purchase agreement with Chicago Venture in the amount of $2,710,000 which included $200,000 Original Interest Discount (“OID”) and $10,000 in debt issuance costs for the transaction. The notes are convertible into common shares of the Company. On January 2, 2019, the Company drew down the first tranche against the Chicago Venture note in the amount of $1,090,000, which included $80,000 of the OID and the $10,000 debt issuance costs.

2. On March 6, 2019, the Company entered into a securities purchase agreement with Iliad Research and Trading, L.P. in the amount of $3,310,000, which included $300,000 Original Interest Discount (“OID”) and $10,000 in debt issuance costs for the transaction. The notes are convertible into common shares of the Company. On March 11, 2019, the Company drew down the initial tranche against the Iliad Research and Trading note in the amount of $2,300,000, which included $115,000 of the OID with the remainder of the OID to be applied at closing on the acquisition of Family Physicians. Tranche was $2,425,000.

As I have stated previously, there is no certain guarantee that states any of the remaining balances will be withdrawn. Is it likely some will? Possibly, but not guaranteed. The first note some 2 1/2 years ago was for $2,000,000 and they only borrowed $830,000 and it is completely paid-off and superseded by current funding agreements.

****Let’s not forget, using this approach leaves the door open to complete more pharmacy location acquisitions this year with a total of $2.2 million ($1.5 million plus $700K) in cash funding still available to them yet****

Yes, it’s likely shares will be converted starting January 2, 2020 to cover the $1,090,000 funding and then March 6, 2020 for the two new location acquisitions and $2,435,000 funding that added another $18 million in revenue and the new company headquarters that will remedy a $230k a year lease expense.

Well prior to that, come this June, we will experience a doubling of revenues, doubling of scripts and then SEC Registration soon after that. I think shareholders have done the DD and know all to well what is in store for RXMD, and it's called share price increases and eventual NASDAQ listing.

Background

Why did we take funding? For Acquisitions!!

Nearly everyone has to take out loans for acquisitions, it's the assets you get that matter. That's why some fail to mention the huge assets that are obtained that outweigh the funding and are substantial to ProgressiveCare's continued success.

Here is an example calculation that can occur that I provided a few days ago. Remember this conversion can't take place until 1 year after the 2019 agreement dates below, and they can only obtain a small portion of shares and then sell 10% of weekly share volume max at a time, its a brilliant leak-out clause. Also, the company can pay back in cash at anytime as well instead of issuing shares. Hope this makes sense.

Calculation

Current A/S is 500 million shares

Current O/S is: 441 Million shares (431 million + 10 million for $700K FSRX seller Conversion)

We all know reservation of shares is not an indication in any way to the number of shares that will be issued. When conversion time comes around, the share price could be in the $.50 or better range, that conversion factor for the present outstanding funding amounts ($3.515 million as noted below) calculates to approximately 7 million shares.

Let's say it is $.25, that's 14.1 million shares.

Let's say it is $.10, that's 35.2 million shares.

Let's say it is $.07, that's 50.2 million shares.

What if the convertible ends up being $6,000,000 total to fund the two purchases and additional acquisitions. This is the amount that could be borrowed on the 2 agreements.

Let's say it is $.50, that's 12 million shares.

Let's say it is $.25, that's 24 million shares.

Let's say it is $.10, that's 60 million shares.

Let's say it is $.07, that's 85.7 million shares.

So as you can see, the current A/S count very well could be enough to cover any potential conversions with the exception of a few unlikely scenarios. This is if the company even chooses to convert to shares instead of paying a portion of the funding back with cash.

IMPROVED FUNDING AGREEMENTS FOR ACQUISITIONS and NEW PROGRAMS

"To Give Anything Less Than Your Best, Is To Sacrifice the Gift." - Steve Prefontaine

Recent RXMD News

- Form 8-K - Current report • Edgar (US Regulatory) • 08/14/2024 03:51:39 PM

- Form DEF 14A - Other definitive proxy statements • Edgar (US Regulatory) • 08/06/2024 08:54:58 PM

- Form 10-Q - Quarterly report [Sections 13 or 15(d)] • Edgar (US Regulatory) • 05/15/2024 07:54:25 PM

- Form 8-K - Current report • Edgar (US Regulatory) • 05/15/2024 04:38:35 PM

- Form 8-K - Current report • Edgar (US Regulatory) • 11/14/2023 04:16:29 PM

- Form 4 - Statement of changes in beneficial ownership of securities • Edgar (US Regulatory) • 10/23/2023 01:40:42 PM

- Form 4 - Statement of changes in beneficial ownership of securities • Edgar (US Regulatory) • 10/23/2023 01:34:02 PM

- Form 3 - Initial statement of beneficial ownership of securities • Edgar (US Regulatory) • 10/23/2023 01:20:59 PM

- Form 4 - Statement of changes in beneficial ownership of securities • Edgar (US Regulatory) • 10/20/2023 04:05:24 PM

- Form 4 - Statement of changes in beneficial ownership of securities • Edgar (US Regulatory) • 10/20/2023 04:04:51 PM

FEATURED Element79 Gold Corp. Appoints Kevin Arias as Advisor to the Board of Directors, Strengthening Strategic Leadership • Sep 18, 2024 10:29 AM

Mawson Finland Limited Further Expands the Known Mineralized Zones at Rajapalot: Palokas step-out drills 7 metres @ 9.1 g/t gold & 706 ppm cobalt • MFL • Sep 17, 2024 9:02 AM

PickleJar Announces Integration With OptCulture to Deliver Holistic Fan Experiences at Venue Point of Sale • PKLE • Sep 17, 2024 8:00 AM

North Bay Resources Announces Mt. Vernon Gold Mine Bulk Sample, Sierra County, California • NBRI • Sep 11, 2024 9:15 AM

One World Products Issues Shareholder Update Letter • OWPC • Sep 11, 2024 7:27 AM

Kona Gold Beverage Inc. Reports $1.225 Million in Revenue and $133,000 Net Profit for the Quarter • KGKG • Sep 10, 2024 1:30 PM