| Followers | 2571 |

| Posts | 307030 |

| Boards Moderated | 29 |

| Alias Born | 04/12/2001 |

Monday, December 10, 2018 1:48:43 PM

The OLIEphant in the Room

Janice Shell

It's been a big week for formerly narcoleptic Olie Inc. (OLIE). On Monday 16 December it moved out of the triple zeros to close at $0.0022. The next day it soared above a penny, closing at $0.014 on astonishing volume of 180 million shares. On Thursday, profit-taking hit after an intraday high of $0.02 was reached; Friday's performance was lackluster. But many believe the fun isn't over.

The cause of all the excitement was evidently known to some on Monday, and to everyone else on Tuesday, when OLIE's CEO Robert Gardner issued a press release announcing that the company's subsidiary, Settlement Management Series 1, LLC, had “just completed an assignment for $20,000,000 MTN [Medium Term Note] USD, credit linked to a Triple A US Treasury Strip ("MTN"). This MTN matures in ten years and upon maturity pays out Settlement Management's clients, the principal, and the 5% interest premium. Settlement Management has no liens or debts, and accordingly there should be no depreciation in the inherent value held in the MTN which therefore would accrue to the benefit of the Company's consolidated financial statements. This assignment is in addition to the $5,000,000 five year, 5% US Treasury Strip already owned by Settlement Management and announced by the Company on November 19th, 2013.” On the same day, OLIE filed a Form 8-K containing a great deal more information, none of which makes much sense.

The 19 November news had gone practically unnoticed, causing only a small and short-lived blip in OLIE's stock price. The company reported then that it had acquired Settlement Management, a Delaware LLC that owned the Treasury strip referenced above, which supposedly matures in five years “and upon maturity pays out Settlement Management the principal and the 5% interest premium.” That is not how Treasury strips work, as will be explained moving ahead. CEO Robert Gardner noted that the acquisition was in keeping with the “Three Step Corporate Plan” announced a few weeks earlier, when the company declared that it intended to “use its Convertible Preferred Securities as currency.” Presumably the acquisition was paid for with a chunk of that convertible preferred. No amount was specified, but the Forward Acquisition Agreement between the parties, attached as an exhibit to the 8-K filed on 17 December, stated that the managing partner of Settlement Management, D. A. Pearman, was given 2 million Series B “Anti Dilutive Preferred Shares priced at @ $2.50,” and 4.9% of OLIE's total issued and outstanding stock.

In the body of the 8-K, however, it was specified that the stock was actually issued to “ten United States resident NexPhase shareholders in reliance on Section 4(2) and Regulation D of the United States Securities Act of 1933.” “NexPhase” is not identified, but as it turns out, it is a Florida company specializing in LED lighting. In February 2011 it was acquired by InfoSpi, Inc., a public company. In the share exchange agreement struck between the two, ten NexPhase shareholders—its only shareholders—are named. They must be the people who received 2 million shares of OLIE's Series B convertible preferred. D. A. Pearman is not among them. Subsequently, InfoSpi changed its name to Onteco Corp., and then to Inelco Corp. The name changes didn't help: it's a Pink Limited Information stock trading at $0.0001 by $0.0002, though an SEC filer.

No explanation of the distribution of the OLIE convertible preferred to the ten NexPhase shareholders is offered. What is their relation to Settlement Management? Were they the owners of the Treasury strip?

Two pumps are better than one

OLIE was not alone in its run; it had a companion, Hi Score Corp. (HSCO). Though it scarcely seems possible, HSCO was even deader than OLIE, stuck at $0.0001 by $0.0002, trading no volume at all some days. Its sorry performance was in considerable part due to a 1:2000 reverse split inflicted on shareholders in July. But it rose from $0.0002 on 18 December to an intraday high of $0.0012 on the 19th. Though it fell back to close at $0.0006, it was still up 133% for the day, on volume of 526 million shares. There was a lot of buying, and a lot of selling.

HSCO rose in tandem with OLIE because on the 18th, new CEO William White announced that the company would be acquired by OLIE. Gardner issued a similar press release on behalf of OLIE. The acquisition would be paid for with—you guessed it—convertible preferred stock, this time Series D. The amount was not disclosed because the transaction will not be consummated until HSCO completes an audit. To accomplish that last task, they've hired MaloneBailey, LLP. MaloneBailey has already been paid.

White added: “We have on our balance sheet, a $5,000,000 USD MTN, credit linked to a AAA US Treasury Strip, and we have moved a considerable amount of affiliate and non-affiliate debt off our balance sheet.”

Another Treasury strip, or the same one?

HSCO is purportedly in the LED lighting business. So is NexPhase. Both are located in Florida. It might seem reasonable to imagine that there's some connection, but NexPhase is never mentioned in HSCO's OTCMarkets filings. That theory must be eliminated. The ten NexPhase shareholders who now own OLIE convertible preferred are apparently not associated with HSCO in any way.

One Treasury strip, two, or none at all?

In an attempt to arrive at an answer to that question, it's best to consider the events of the recent past chronologically. The story is complicated, and in some ways tedious, but it is very important.

On 14 November, Hi Score announced that it had acquired a company called Sequoia Management Series 1, LLC, “a company that owns a $5,000,000, five year, 5% US Treasury Strip, without liabilities on its own financial statements.” It did not publish or explain the terms of the acquisition. Since it, like OLIE, has proclaimed that convertible preferred stock is “currency,” very likely that's what Sequoia received. Or what we are meant to think Sequoia received.

On 19 November, OLIE announced its own acquisition of Settlement Management Series 1, LLC, which, like the company just acquired by HSCO, happened to own a $5 million, five year, 5% Treasury strip, and was willing to sell it in exchange for convertible preferred stock. We know that stock went to the NexPhase shareholders.

Both Sequoia Management and Settlement Management are Delaware companies. Sequoia was formed on 15 November 2013, one day after it was acquired by HSCO.

Settlement Management, bought by OLIE, was formed on 18 November 2013, one day before Gardner announced the deal.

Obviously they were created for the sole purpose of being acquired by a couple of penny stock companies. But why should they have happened to hold identical—and identically described, in the relative press releases—Treasury strips?

Strips is the acronym for Separate Trading of Registered Interest and Principal of Securities. When a Treasury not or bond is “stripped,” the principal payment becomes a zero-coupon security. Holders of strips are not paid both principal and interest. This is well-known; most people understand what a zero-coupon bond is. Oddly, though, it seems our CEOs do not: Gardner insisted that “upon maturity [the strip] pays out Settlement Management the principal and the 5% interest premium.”

And what 5% interest are Gardner and White fantasizing about? Since 2009, no Treasury notes or bonds have had yields anywhere near 5%.

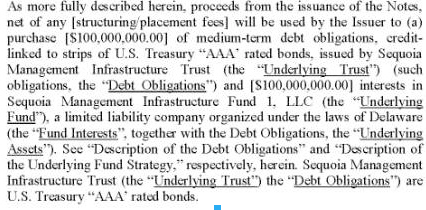

There are several exhibits attached to the OLIE 8-K reporting the acquisition of Settlement Management. The Forward Acquisition Agreement between OLIE and Settlement Management has already been discussed. Another is a private placement memorandum in which Sequoia Management Infrastructure Series 1, LLC offers $200 million medium term notes at 5.5% interest. Gardner referenced these notes in his OLIE press release of 17 December, saying Settlement Management—newly acquired by OLIE—had just completed an assignment for them. Yet he got the interest rate and the dollar amount wrong: he said 5% instead of 5.5%, and $20 million instead of $200 million.

The private placement memorandum is a curious document. Unusually, it's in .pdf format. The SEC does not permit documents of this kind to be submitted in formats that are not searchable. And in fact it never was filed with the SEC. The securities are senior, unsecured corporate notes with a maturity date in December 2023.

Treasury strips are mentioned only once in the lengthy document:

Clearly Sequoia Infrastructure doesn't plan to buy strips; it plans to buy securities credit-linked to strips.

The document lacks clarity in parts, and is inconsistent. The type on some pages is justified; on others it is not. That, of course, suggests a careless cut-and-paste job. Perhaps the author never expected anyone to read it from start to finish.

The memorandum is dated 15 November 2013, and is signed by J. R. Blackwell, managing member of Sequoia Infrastructure. Which is interesting, given that the LLC wasn't formed in Delaware until 22 November.

There is also a Partial Deed of Assignment between Sequoia Management Infrastructure Series 1 and Sequoia Management Series 1, LLC, executed “on or about December 10,” but dated 16 November. In it, Sequoia Infrastructure assigns the full $200,000,000 worth of the notes offered in the prospectus—which was signed only the day before—to Sequoia Management Series I, the company acquired by HSCO on 14 November. The signatory for Sequoia Infrastructure is Sherrie A. Jenkins. Like D. A. Pearman, she does not turn up on any internet searches. Neither one has as much as a Linked In page. They would not be the first nonexistent company officers to turn up in connection with a penny stock.

The Deed of Assignment states that the agreement was made “as collateral for the equity investment as described in the Capitalization Acquisition Agreement dated on or about December 10, 2013...” That document is not one of the exhibits.

What was the point of composing a prospectus if the plan all along was to sell the notes to Sequoia Management, HSCO's company? But according to Gardner, the notes were assigned to OLIE's Settlement Management. It may be wondered whether he even read the relevant documents. In the Forward Acquisition Agreement, Settlement Management makes it clear that the Treasury strip is its only asset.

Obviously all these Delaware companies were created at the same time for the same purpose: to do deals—or what appear to be deals—with OLIE and HSCO. Is there really a Treasury strip worth $5 million that someone was willing to exchange for convertible preferred that may never be worth a dime?

Probably not. In the private placement memorandum, two securities firms were named as underwriters: Fordham Financial Management and Centaurus Financial. An early morning call to Fordham proved fruitful. Phyllis Henderson, Chief Compliance Officer, was very surprised indeed to learn of her company's supposed participation in the purported offering. She stated unequivocally that Fordham had never heard of Sequoia Management Infrastructure Series 1, LLC, much less agreed to underwrite anything for it.

This explains why the documentation is inconsistent, and why Gardner and White reported their contents inaccurately. The whole “bond” story is an invention. And it is brazen fraud.

Javan King and the Syndicate Trust

Anyone familiar with the Citadel Eft (CDFT) comedy will already have detected Javan King's hand in OLIE and HSCO's insistence that convertible preferred stock can be used as “currency.” No doubt its judicious use can help a company restructure debt in the short term, but moving debt around does not make it disappear. Convertible preferred shares are a hybrid security, with the characteristics of both debt and equity.

Robert Gardner is an Englishman, a barrister proud to be a Queen's Counsel. He emigrated to Canada decades ago, and settled in Vancouver, where he opened a successful law practice. Along the way, he became interested in the financial markets. He once defended notorious Vancouver promoter Murray Pezim. He became a promoter himself, and has served as an officer or director of many companies, most of them listed in Canada. In recent years he's extended his reach into the States. Gardner is a colorful character. As a young man, he served in Britain's famous SAS, a highly-trained special forces unit. He's tried his hand at movie making, run for political office, and spent a good deal of time sailing the Pacific. He's been involved in considerable controversy over the years, and has made quite a few enemies, but has never been subjected to any disciplinary actions by the Canadian or U.S. regulators.

Gardner took over as sole officer and director of OLIE on 30 November 2012, replacing Avraham Morgenstern and Itai Freed; the change in control was not announced until 7 January. He and a group of associates planned to acquire a battery company called EnCanSol Capital Corporation, and evidently intended to pursue that line of business. In connection with the acquisition, Gardner sought to raise $10 million. Negotiations dragged on for several months. Presumably because fundraising had been more difficult than anticipated, the transaction was terminated on 10 May.

Perhaps Gardner had already seen the writing on the wall, and was looking around for something else to do with the OLIE shell. It appears that he became acquainted with Javan (“Jay”) King, or at least with some members of King's circle, as early as February. On the 27th, someone from “BenjaminFunds” tweeted:

BenjaminFunds doesn't identify its management—always a bad sign—but they claim to do PIPEs, IPOs and secondary offerings, mergers and acquisitions and more. They are definitely friends of King; it seems likely that his buddy Richard (“Ricky”) De Sousa is one of the Benjamin boys. Benjamin sold CDFT its not-so-successful vacation villa in the Dominican Republic. They also worked up a business plan for OLIE before the EnCanSol deal fell through. By early April, OLIE was featured on the “news” page of King's Syndicate Trust website.

King, like Gardner, lives in Vancouver. Before he created the Trust in 2012, he was one of the managers at Qualico Capital, which became known for pushing scams. With the Trust, he built on some of the ideas he'd developed at Qualico. He preaches the wonders of “anti-dilutive” convertible preferred stock, beguiling debt ridden penny CEOs with explanations of the ease with which they can “remove debt from the balance sheet.” He may even buy into his own story, as he's willing to accept convertible preferred in exchange for his services. It seems likely he also takes consulting fees, though that cannot be confirmed, as he's always careful to keep his name and the name of the Syndicate Trust out of SEC or OTCMarkets filings.

He preaches that companies can't have enough convertible preferred—one company he's advised, ARNH, literally has a class for every letter in the alphabet—because they can use it not only to restructure debt, but also to acquire assets. Those assets will accomplish two things: they'll contribute to the bottom line, and they'll increase the company's worth so impressively that an uplist to a national exchange will be easy and quick. His favorite exchange, evidently, is the NYSE MKT (formerly know as the Amex); he recommends it to all his clients. CDFT's CEO Gary DeRoos even paid a hopeful visit to New York to have a tour and engage in a preliminary chat with an official.

King counsels “his” CEOs to issue a dividend of a special class of convertible preferred to ordinary investors. With CDFT, shareholders received between 1 and 3 shares of preferred depending on how much they'd invested. The distribution was not pro rata. Neither was it run by FINRA; King seems to have a poor understanding of SEC and FINRA rules and regulations. The next item on the agenda was a reverse split so large it reduced the outstanding to a little less than 15,000 shares. The idea was to control the size of the “reconstituted” float, which would make it easier to maintain a higher price than before. The price proposed was $2.50 a share. At the same time, shareholders were encouraged to convert some of their preferred to restricted common. Since CDFT is an SEC filer, they were obliged to hold it for six months. DeRoos was supposed to file a Form S-1 to register that stock, but it never happened. And now everyone's stuck with penny stock certs very few brokers, if any, will accept for deposit.

For CDFT shareholders, the plan has gone badly wrong.

King also does his best to arrange the desired asset purchases. The people he introduces to CEOs are not always the most reputable. Most people are uninterested in exchanging something valuable for something potentially worthless, like convertible preferred stock in a penny issue. He first set CDFT up with Dennis Radcliffe, assuring DeRoos that the Radcliffe family's collection of sports memorabilia was worth more than $10 million. Earlier, two of the Radcliffes had been sued by the SEC for fraud in connection with that collection. When CDFT had it appraised, the $10 million number was revised down to a mere $2.9 million, and probably that overstates its resale value. King then sold DeRoos his Benjamin Funds associates' villa in the Dominican Republic, which is worth a whopping $230,000. And finally, either he or Dennis Radcliffe got DeRoos involve with Joe Riad, a poseur who claims to be worth $43.8 billion. Or more, considering that he owns bonds—yes, bonds again—that he says are worth $2.2 billion apiece. He has 732 of them. Naturally they're fakes; examples of one version of the notorious 1934 “Morgenthau bonds”.

DeRoos fell for the story, and purchased five of them for CDFT with stock. They were valued at a total of $700 million. The auditor, who happens to be MaloneBailey, recently hired by HSCO, refused to accept the valuation. DeRoos fired the firm. There followed an embarrassing series of amended 8-Ks. MaloneBailey finally said flatly that the bonds had not been issued by the U.S. government, and were not backed by its full faith and credit. A few weeks later, DeRoos abruptly announced the termination of the purchase agreement.

Prospects for OLIE and HSCO

Obviously King is pushing his scheme on Olie and Hi Score. Both have announced an upcoming dividend in convertible preferred stock. HSCO properly submitted a corporate action request to FINRA, as did OLIE. They've recently been processed. The two companies have been doing their best to reduce their debt, and have also been looking for assets to buy. They have very little cash on hand—OLIE had only $127 at the end of the last quarter—and need ways to generate revenues.

Some of the King gang has made its presence felt. Ken Radcliffe, Dennis's brother, was installed for awhile as OLIE's investor relations representative. OLIE has also purchased King's NanoCap Magazine. The other Syndicate Trust publications were deep-sixed a few months ago, and last week the Trust's site began serving up 404 error messages. Incredibly, Gardner recently appointed Iman Khatam and Michael Zoyes to its Audit Committee and Advisory Board, without, apparently, making them directors. Just as well. Iman Khatam works for King; one of his jobs has been to act as site admin for the Trust. Zoyes is the former CEO of HSCO; he's detested by long-term shareholders for driving the company into the ground. It may legitimately be wondered what qualifications either has to sit on an audit committee.

In the end, it seems likely that both OLIE and HSCO will have replaced an excessive number of common shares with an even more excessive number of convertible preferred shares. When the latter are converted and hit the street—and it will happen—they'll be back where they started.

One of the people who must be happy about HSCO's run is Eddy Marin. His Green Streak Group holds $167,188 in notes, along with accrued interest. In January 2013, he converted 312 million shares in exchange for $312 of debt; it's obvious that any further conversions will be extremely dilutive.

Marin is best known as the “king of spam,” has criminal convictions for cocaine dealing and money laundering. More recently he pled guilty in the high profile Rothstein “hidden diamond” case, in which he helped fraudster Scott Rothstein's wife hide a valuable yellow diamond from the Feds.

He'll be sentenced on 3 February, but perhaps he can live it up till then.

Marin isn't the only one facing trouble. Securities fraud as been committed by at least some of the players in the drama, and the consequences may be serious.

North Bay Resources Commences Operations at Bishop Gold Mill, Inyo County, California; Engages Sabean Group Management Consulting • NBRI • Sep 25, 2024 9:15 AM

CEO David B. Dorwart Anticipates a Bright Future at Good Gaming Inc. Through His Most Recent Shareholder Update • GMER • Sep 25, 2024 8:30 AM

Cannabix Technologies and Omega Laboratories Inc. Advance Marijuana Breathalyzer Technology - Dr. Bruce Goldberger to Present at Society of Forensic Toxicologists Conference • BLOZF • Sep 24, 2024 8:50 AM

Integrated Ventures, Inc Announces Strategic Partnership For GLP-1 (Semaglutide) Procurement Through MedWell USA, LLC. • INTV • Sep 24, 2024 8:45 AM

Avant Technologies Accelerates Creation of AI-Powered Platform to Revolutionize Patient Care • AVAI • Sep 24, 2024 8:00 AM

VHAI - Vocodia Partners with Leading Political Super PACs to Revolutionize Fundraising Efforts • VHAI • Sep 19, 2024 11:48 AM