| Followers | 243 |

| Posts | 2993 |

| Boards Moderated | 0 |

| Alias Born | 06/16/2015 |

Sunday, March 18, 2018 11:40:31 PM

ONCI - Fresh Start DD

Downward pressure on the pps from the 3(a)(10) selling is all but over.

With the 3(a)(10) stock sales 99.9% completed on 3/15 (maybe now 100% complete after Friday), the O/S was increased by only 12.4% - AWESOME!

With only 12.4% added to the O/S from the 3(a)(10) transaction, the proportional reduction in the benchmark pps value of ONCI - the pre-3(a)(10) share price of ~0.014 in early October - gives a pps of 0.0124. PPS is now ~0.003. Correction to 0.0124 represents a gain of 313%.

So let's see, what was that? The O/S was increased by only 12.4%, but the pps was pushed down from ~0.0140 to ~0.003, which is a nearly 80% drop in price. There's a correction looking for a direction. Gee, where's Waldo when you need him. I know he could tell me which way the price will correct.

The correction to 0.0124 based on the benchmark price is just a starting point - it's the initial price correction. What has the company done since the 3(a)(10) selling began putting downward pressure on the pps?

Quite a bit, actually - but for starters, it reported about $1,725,000 revenue, as well as about $780,000 net income. Yes, NET INCOME - 42% operating margin!

What else has changed since the 3(a)(10) selling began putting downward pressure on the pps (AND moreso from traders flipping down and flipping the low channel)?

- if you think the CEO may be fraudulent - and risking prison time - you should just run away now.

- if you're not comfortable with reading or analyzing income statements or balance sheets or cash flow statements… you're just gambling, anyway; otherwise, know that this is where the opportunity lies for out-sized gains.

- I'm very happy to see SB doing what he's doing and keeping as much focus as possible on launching the product(s), improving production/cost in tandem, and building the distribution as fast as possible… and improving/extending & customizing the product, as well. I have enough experience on my own to know that this is exactly what he should be doing - as top priority. I really don't give a crap about audited reports right now - that can come later. Why?

- Because: cost goes up substantially - in terms of $ AND management resources - when climbing each higher rung of reporting status: Pink, unaudited; Pink, audited; QB, audited (new listing, only recently made available); Pink, SEC reporting; Pink, audited, SEC reporting; QB, audited, SEC reporting

- I've bought and held - and made very good gains and $$ - with many stocks that were pink/unaudited, well into the pennies. One of them went over 0.25 recently (RXM$ - went over a nickel long before auditing fins). Yes, I prefer audited, SEC reporting. After that, I want them to uplist ultimately to the big boards. Lack of audited fins is NOT going to hold the stock down in the subs. Sure, for a short time it can be "used" while certain traders flip the channel and other traders and investors buy up the bottom prices.

(click on image or open in new tab to view full size)

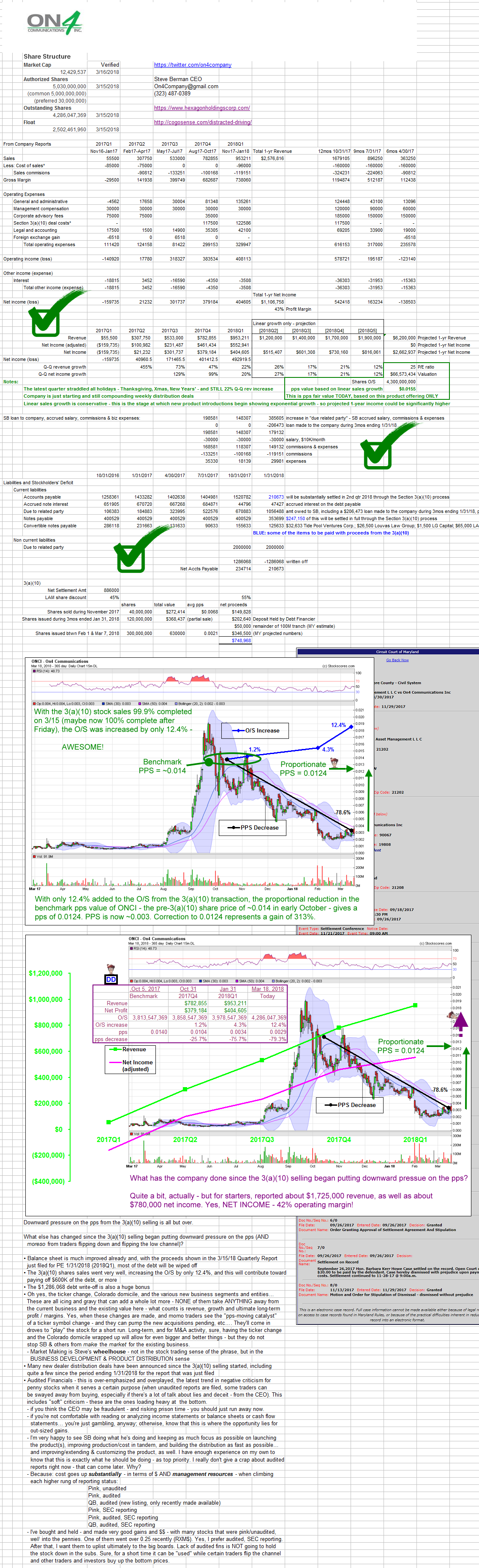

Downward pressure on the pps from the 3(a)(10) selling is all but over.

With the 3(a)(10) stock sales 99.9% completed on 3/15 (maybe now 100% complete after Friday), the O/S was increased by only 12.4% - AWESOME!

With only 12.4% added to the O/S from the 3(a)(10) transaction, the proportional reduction in the benchmark pps value of ONCI - the pre-3(a)(10) share price of ~0.014 in early October - gives a pps of 0.0124. PPS is now ~0.003. Correction to 0.0124 represents a gain of 313%.

So let's see, what was that? The O/S was increased by only 12.4%, but the pps was pushed down from ~0.0140 to ~0.003, which is a nearly 80% drop in price. There's a correction looking for a direction. Gee, where's Waldo when you need him. I know he could tell me which way the price will correct.

The correction to 0.0124 based on the benchmark price is just a starting point - it's the initial price correction. What has the company done since the 3(a)(10) selling began putting downward pressure on the pps?

Quite a bit, actually - but for starters, it reported about $1,725,000 revenue, as well as about $780,000 net income. Yes, NET INCOME - 42% operating margin!

What else has changed since the 3(a)(10) selling began putting downward pressure on the pps (AND moreso from traders flipping down and flipping the low channel)?

- Balance sheet is much improved already and, with the proceeds shown in the 3/15/18 Quarterly Report just filed for PE 1/31/2018 (2018Q1), most of the debt will be wiped off;

- The 3(a)(10) shares sales went very well, increasing the O/S by only 12.4%, and this will contribute toward paying off $600K of the debt, or more;

- The $1,286,068 debt write-off is also a huge bonus;

- Oh yes, the ticker change, Colorado domicile, and the various new business segments and entities… these are all icing and gravy that can add a whole lot more - NONE of them take ANYTHING away from the current business and the existing value here - what counts is revenue, growth and ultimate long-term profit / margins. Yes, when these changes are made, and momo traders see the "pps-moving catalyst" of a ticker symbol change - and they can pump the new acquisitions pending, etc… they'll come in droves to "play" the stock for a short run. Long-term, and for M&A activity, sure, having the ticker change and the Colorado domicile wrapped up will allow for even bigger and better things - but they do not stop SB & others from make the market for the existing business.

- Market Making is Steve's wheelhouse - not in the stock trading sense of the phrase, but in the BUSINESS DEVELOPMENT & PRODUCT DISTRIBUTION sense;

- Many new dealer distribution deals have been announced since the 3(a)(10) selling started, including quite a few since the period ending 1/31/2018 for the report that was just filed;

- Audited Financials - this is over-emphasized and overplayed, the latest trend in negative criticism for penny stocks when it serves a certain purpose (when unaudited reports are filed, some traders can be swayed away from buying, especially if there's a lot of talk about lies and deceit - from the CEO). This includes "soft" criticism - these are the ones loading heavy at the bottom.

- if you think the CEO may be fraudulent - and risking prison time - you should just run away now.

- if you're not comfortable with reading or analyzing income statements or balance sheets or cash flow statements… you're just gambling, anyway; otherwise, know that this is where the opportunity lies for out-sized gains.

- I'm very happy to see SB doing what he's doing and keeping as much focus as possible on launching the product(s), improving production/cost in tandem, and building the distribution as fast as possible… and improving/extending & customizing the product, as well. I have enough experience on my own to know that this is exactly what he should be doing - as top priority. I really don't give a crap about audited reports right now - that can come later. Why?

- Because: cost goes up substantially - in terms of $ AND management resources - when climbing each higher rung of reporting status: Pink, unaudited; Pink, audited; QB, audited (new listing, only recently made available); Pink, SEC reporting; Pink, audited, SEC reporting; QB, audited, SEC reporting

- I've bought and held - and made very good gains and $$ - with many stocks that were pink/unaudited, well into the pennies. One of them went over 0.25 recently (RXM$ - went over a nickel long before auditing fins). Yes, I prefer audited, SEC reporting. After that, I want them to uplist ultimately to the big boards. Lack of audited fins is NOT going to hold the stock down in the subs. Sure, for a short time it can be "used" while certain traders flip the channel and other traders and investors buy up the bottom prices.

(click on image or open in new tab to view full size)