| Followers | 130 |

| Posts | 18112 |

| Boards Moderated | 0 |

| Alias Born | 01/16/2007 |

Thursday, December 28, 2017 12:31:39 PM

*** NOTE: NOT Verbatim, several lines omitted ***

Saturday, December 23, 2017

Where we have been... Where we are now... and Where we are going at HHSE...

Greetings HHSE Friends & Followers:

As we reflect back on 2017, HHSE Management is taking a few days to look at our past, present and future activities to help guide sage decisions. 2017 has been a momentous year for the company - due in large part to the attempted (but terminated) merger with Crimson Forest, and the subsequent re-focus of the company's primary activities and revenue streams.

Looking much further back - five, six, seven years and more - and looking forward in time for an equal time-frame, we can see trends and opportunities for HHSE and our shareholders.

First of all, we'd like to point out that Hannover House is unlike most any other "OTC Pinksheet" listed company. We have been operating continuously since 1993 (24-years) and have been reporting to the OTC Markets since Dec. 2009 (8-years). Statistically, most OTC listed equities are flashes-in-the-pan time wise... lots of Stock Hype / I.R. Promotions, insider share dumps, and quick closures. That's definitely not HHSE.

So, let's take a few minutes to take a high-altitude look at the Company and where we are going.

WHAT IS OUR PLAN FOR GROWTH IN 2018 AND BEYOND?

* We believe that HHSE is "one film away" from being a major independent studio. All it takes is any one of the many titles in our current release queue to become a surprise box officer performer such as "Lady Bird" or "Get Out" and we are suddenly a $100-MM company.

* We have an impressive slate of titles for 2018 and 2019 - and two terrific distribution partners for North America (Cinedigm Entertainment and Sony Pictures Home Entertainment) - as well as our direct relationships with all of the major theatre exhibition chains. Our "lower-end" titles are much higher profile than in past years... and our higher-end titles are now genuine theatrical caliber contenders. We are positioned for the proverbial lucky break that happens when the right film is released at the right time...

* Our recently re-focused Theatrical Release model is delivering huge benefits to our ancillary revenues... and our new partnerships with indie labels is providing access for the VODWIZ streaming venture, which truly could become "the tail that wagged the dog" for HHSE shareholders.

What else is worth noting for this long, holiday weekend? Here are a few observations:

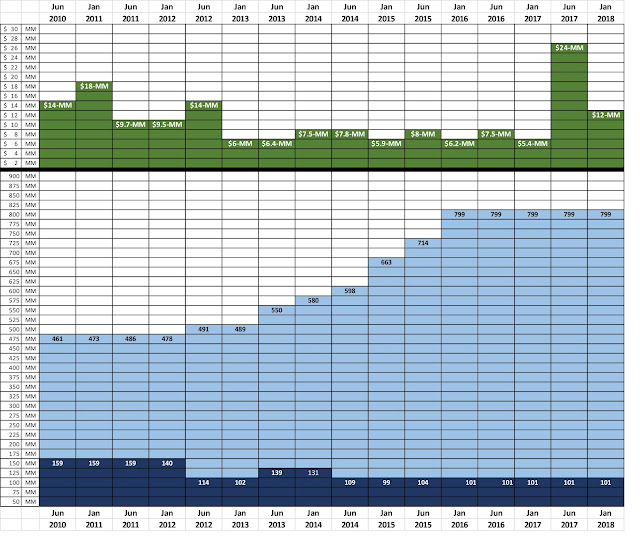

1). Hannover House has Not Issued any Shares in 2.5-years. See the chart below. For the company's first two years as a public equity, the stock structure was quite stable. For the past 2-1/2 years, the stock structure has also been stable. But in 2013 and 2014, the company got involved in some ugly predatory lender situations, most notably TCA Global and JSJ, which precipitated a rapid growth in share issuances. The business model for both TCA and JSJ - as exercised against HHSE and many other borrowers - is to make repayment with cash as difficult as possible, in order to force a "conversion of the debt" into freely trading shares of the issueer at a dramatic discount-to-market. Such returns grossly exceed the legal usury law limitations in all states, and this general business practice is operating in a legally dubious space. JSJ, for instance, refused to accept repayment from HHSE via a bank wire transfer (including all applicable, legal interest per the note), preferring instead to file a lawsuit (in Texas?!), in order to try to force repayment via shares at 200% or more interest. These predatory lenders generally prey on companies that are unable to defend themselves, and therefore are forced to allow the lenders to squeeze out profits far in excess of lending laws through toxic-conversions; most of the time, these small borrowers are ultimately forced out of business. However, this was not the case with Hannover House - as the company has a operating business that is unaffected by fluctuations of our stock price and not dependent on the issuance of shares for capital. These toxic dilutions from 2013 and 2014 definitely hurt our shareholders, and hurt our "market cap," as demonstrated in the charts. So, the Board voted to cease such forms of borrowing, and as a result, HHSE has not issued any new shares in 2.5-years. Anyone predicting on a chat board or anywhere else that a "big dilution is coming" is mistaken.

2). It Doesn't Take Much to Double or Triple the HHSE Share Price - Look at the market-cap spike for HHSE stock earlier this year (seen as June, 2017). This increase in PPS was due to shareholder excitement about the prospect that a merger with Crimson Forest would provide HHSE with high-profile films to distribute. The growth in PPS was not based on any increase in revenues (in fact, the time-distraction of the Crimson merger caused many 2017 releases to be delayed). The PPS spike was driven solely by enthusiasm.

3). Does HHSE Need a Merger Partner? - If the right opportunity came along that would provide HHSE with a reliable source of high-end theatrical titles, we would be responsive to consider such opportunities. However, the programing philosphy ultimately revealed by Crimson Forest did not conform to North American market conditions, in HHSE's opinion. When the promised operating funding didn't materialize, the promised high-end productions turned into low-end films, and the promised "big" releases all turned out to be Mandarin-language releases, we knew that the partnership would not deliver what HHSE wanted for our step-up to major independent status.

4). What's in Store for the first half of 2018?

a). Release Activities: January will see the theatrical release of "BLOODFEAST" - delayed since July due to MPAA re-cut needs. February will see a massive placement of DVDs and BluRays for "BATTLECREEK" (street date Feb. 6). That same week, on Friday (Feb. 9), HHSE will commence the initla theatrical launch of "DEATH HOUSE" to theatres. In April, three titles will be released via Sony Pictures Home Entertainment (including "DAISY WINTERS"); in May, HHSE will release "THE RIOT ACT" to theatres and Cinedigm will release DVD's and BluRays of "THE LENNON PROJECT" for the Company. Other titles in queue for theatrical and / or home video during the first half of 2018 include "MUSE", "INSOMNIUM", "IDENTITY CRISIS", "SLEEPER CELL", "DINOSAURS OF THE JURASSIC" and "SACRED HEARTS" (all but the last title were planned for 2017, but delayed during the Crimson merger pursuit).

b). Corporate Governance: HHSE will be re-filing a Form 10 Registration with two full years of audits (2016 and 2017) early this coming year, during the first few weeks; the CPA review is already underway and much of the documentation and procedural steps for the audit were already assembled during 2017 while planning for the Crimson merger. We feel that a registration of the shares and the subsequent uplist to OTC:QB will attract more investors and some institutional funds... resulting in a higher anticipated daily trading volume, and a predicted much higher HHSE stock price (based on business results, industry fundamentals and the proven power of Shareholder Enthusiasm).

c). New Ventures - With Sony and Cinedigm handling selected HHSE releases, our management time can be redirected towards theatrical releases, higher-end acquisitions (including productions) and our VODWIZ streaming venture. As will be seen in our 2017 filings, theatrical release activities are the engine that is now driving HHSE revenues in all other arenas. Theatrical titles get more shelf space and priority placement when released to home video; theatrical titles get larger license fees from Netflix and Television licensors; and theatrical titles provide two direct revenue streams for HHSE in the form of both servicing fees and revenue participations. The current mass merchant and key video retail support for "BATTLECREEK" evidences the sales boost that a targeted, limited theatrical release can deliver for the subsequent home video release.

5). Thoughts on the HHSE Stock Chart - The chart below is divided into two sections. The top section shows the "approximate market cap" at six-month intervals beginning in June 2010 and continuing through to this week. The Market Cap was calculated by the total of all shares in issue, multiplied by the closing price of the stock during a one-week period during the stated month. The bottom section of the chart shows the total SHARES IN ISSUE for the company during this same time frame. The dark-blue shares represent those that are "restricted" from sale, and the light-blue shares represent the total share count of restricted plus unrestricted shares for that time period.

Perhaps the most visible trends to see on this chart are that the company did very little in share issuances for the first two years... and none for the past 2.5-years - as seen by the flat-line of total shares in issue.

The next interesting item of note is the tremendous PPS Spike that occurred earlier this year, at which time the Market Cap jumped from $5.4-MM to $24-MM in just a few month's time. What's interesting about this result is that the company was functionally frozen from new releases during that time, so the sudden shareholder enthusiasm cannot be attributed to improved revenues... it can only be viewed as a reaction to the prospective merger with Crimson. The current Market Cap of $12.4-MM has been stable for quite a few months now.

A third observation can be seen during the "heavy dilution" time-frames of 2013 to the end of 2015, when TCA (via MAGNA) and JSJ were flooding the market with toxic-conversion shares. What is interesting about this? Well, the market cap stayed surprisingly stable during this dilution... meaning that the average PPS went DOWN while the total float went UP, but the overall Market Cap remained steady. HHSE Management believes that the Market Cap remained relatively steady during these dilution times due to Investor Relations / Stock Promotions. As the toxic-lenders dumped their HHSE shares onto the market, some effort was being expended (by them or third parties) to create an investor market for their share dumps... which is another reason why HHSE management hates the concept of these toxic-conversion notes. It also answers the question that some shareholders have posted to HHSE management over the past few years about "why aren't you doing IR / Stock PR now?" The answer is that we are are focused on building the fundamentals of the business rather than on creating a momentary spike in PPS interest while some third party lender dumps out shares. We are not philosophically opposed to I.R. and new investor outreach. We just feel that the cost of such promotions would be best utilized after our Registration and other major events in the works.

There are more thoughts and developments to share... watch this blog over the holidays, and watch for news releases occuring between Christmas and New Years, as well as during the first week of January. Happy Holidays / Merry Christmas / Happy New Year and Best Wishes to all our HHSE shareholders!

http://hannoverhousemovies.blogspot.com/2017/12/where-we-have-been-where-we-are-now-and.html

HHSE

Recent HHSE News

- Form 8-K - Current report • Edgar (US Regulatory) • 01/05/2024 07:17:02 PM

Kona Gold Beverage, Inc. Updates Multi-Million Dollar Merger and Posts Over $1.2 Million in Q3 Revenues • KGKG • Nov 15, 2024 10:36 AM

HealthLynked Corp. Announces Third Quarter and Year-to-Date 2024 Results with Strategic Restructuring, Third-Party Debt Repayment, and Core Technology Focus • HLYK • Nov 15, 2024 8:00 AM

Alliance Creative Group (ACGX) Releases Q3 2024 Financial and Disclosure Report with an increase of over 100% in Net Income for 1st 9 months of 2024 vs 2023 • ACGX • Nov 14, 2024 8:30 AM

Unitronix Corp. Publishes Its Cryptocurrency Portfolio Strategy • UTRX • Nov 14, 2024 8:05 AM

Avant Technologies and Ainnova Tech Form Joint Venture to Advance Early Disease Detection Using Artificial Intelligence • AVAI • Nov 12, 2024 9:00 AM

Swifty Global Announces Launch of Swifty Sports IE, Expanding Sports Betting and Casino Services in the Irish Market • DRCR • Nov 12, 2024 9:00 AM