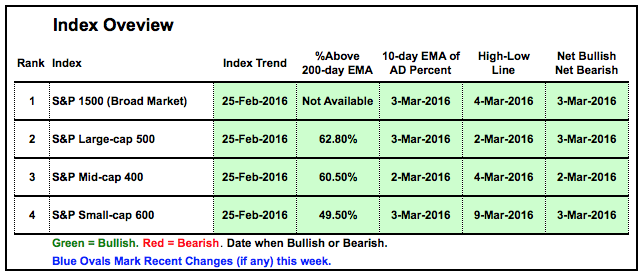

There is no change in the index table and only one change in the sector table. The bulk of the evidence remains bullish for the market. Small-caps continue to lag overall as the Small-Cap %Above 200-day EMA (!GT200SML) dipped below 50%. Note that Mid-Cap %Above 200-day EMA (!GT200MID) and S&P 500 %Above 200-day EMA (!GT200SPX) are both above 60%. Small-caps may be weighing, but the weight of mid-caps plus large-caps is more than that of small-caps. BY ART HILL

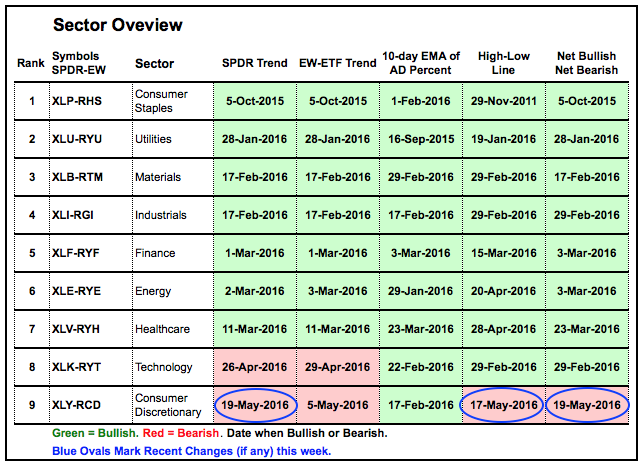

The consumer discretionary sector got a downgrade because the Consumer Discretionary HiLo Line ($XLYHLP) moved below its 20-day EMA and XLY broke below its April low. This means the indicators are net bearish for XLY and it remains the weakest sector. Amazon is the big dog in XLY, but there appear to be too many dog dogs in the sector right now (blame retailers). Despite weakness in technology and consumer discretionary, the other seven sectors remain bullish and this is net bullish for the broader market. At worst, pockets of weakness may impede the bulls and result in a grinding advance for the broad market indexes.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

News

News  Market Data

Market Data  Discover

Discover