Sunday, December 21, 2014 7:33:02 AM

This Could Be Your Best Chance to Make a Fortune in the Commodities Market

Saturday, December 20, 2014

The recent selloff in high-yield bonds is something Stansberry Research has been warning about for months.

In short, high-yield bonds (aka "junk bonds") are the riskiest of corporate credits... And until recently, they were trading at record-high prices. Yet investors continued to leverage up and buy record amounts of junk.

In addition, energy companies have become larger and larger issuers of junk bonds. So when oil began its selloff recently, it was partly responsible for sparking the trouble in the high-yield market.

Earlier this week, Bloomberg published an interview with billionaire activist investor Carl Icahn – one of the best investors alive today. (He holds a $5 billion-plus stake in Apple in his hedge fund.) Like us, Icahn is still concerned with high yield. When asked what investors' biggest risk is today, he replied...

There's still risk in the financial markets, even though the economy looks pretty good. The one area I think is getting to be a bubble is the high-yield market. These bonds are still at way too low an interest rate. In other words, you can borrow money too cheaply if you're a risky company.

There are arguments that there's a lot of cash flow to cover the interest payments on the bonds. But some of that cash flow is ephemeral – it's not likely to last. It's a bubble that's going to burst in the next couple of years.

Icahn also agreed the selloff in oil is proof of the risk in the high-yield market... Prices have plunged in the face of a single economic shock. Icahn believes the energy sector will offer huge upside... just not today...

Oil will be a great opportunity, but not now. The energy sector is probably in for more problems. Oil prices will probably go down more, and these energy companies, especially oil-service companies, are going to be hurt. But then I think there will be a tremendous opportunity.

Oil prices will eventually recover, because worldwide demand will continue to grow and supply will diminish, due to depletion. Additionally, the cost of finding oil is growing. We are not coming up with enough alternative energy that quickly.

We don't agree with Icahn's belief that oil supplies will diminish. We don't buy into the "Peak Oil" argument. We're long human ingenuity. But he's right that the cost of finding oil is growing.

Steve Schwarzman – cofounder and CEO of private-equity giant Blackstone Group – is also looking for good deals in energy.

Blackstone is nearly finished raising a new fund for energy investments, which should be larger than $4 billion. As he recently noted at the DealBook economic conference in Manhattan...

I think this is going to be a wonderful, wonderful opportunity for us. It's going to be one of the best opportunities we've had in many, many years... This is a wonderful, wonderful time. This is a commodity. It's not patent-protected. Commodities go into undersupply and oversupply.

Oil is down to around $57 a barrel today, down nearly 50% from its highs in June. As Icahn and Schwarzman suggest, low prices will crush some producers. Supply will come offline. As supply dwindles (and demand potentially increases), prices will start to rise again. It's the definition of a commodities cycle.

We aren't predicting an oil recovery around the corner. But we do believe natural gas prices should bottom soon...

In the December 3 Growth Stock Wire, titled "How to Profit From Oil's Price Collapse," Stansberry Resource Report research analyst Brian Weepie explained how to profit from oil's price collapse. Like oil, natural gas prices had also gotten crushed. But Brian said natural gas was close to a rebound.

He also shared a chart of five natural gas producers that had been crushed this year. (Note that we've updated it as the price of oil has continued to fall since that essay was published.)

Company Mkt Cap Production % Nat Gas) Decline Since June

Chesapeake Energy (CHK) $12.4B 71% -34%

Encana (ECA) $9.9B 84% -42%

Southwestern Energy (SWN) $10.8B 100% -33%

Talisman Energy (TLM) $8.1B 63% -24%

Range Resources (RRC) $9.7B 67% -37%

Source: Capital IQ

Shares of Talisman Energy – one of the most beaten-down natural gas companies on the list – jumped nearly 20% on Monday on word that the Canada Pension Plan Investment Board was considering buying the company. That's on top of an 18% jump the previous Friday after news broke that Spanish energy company Repsol was considering buying Talisman.

While we're not going to waste our time speculating on the specific price movements of oil and natural gas, we are certain we'll see more deals like this...

Institutional investors with plenty of cash (like Blackstone) are scouring the beaten-down energy sector in search of great assets at low prices.

But one sector of commodity stocks is actually outperforming the market: royalty companies. Royalty companies have one of our favorite business models, particularly when it comes to oil and gold.

Stansberry Resource Report editor Matt Badiali explained the gold-royalty business model in a Growth Stock Wire essay last year...

Royalty companies don't actually operate mines. Instead, they own a percentage of a mine's production. Typically, a mining company sells a royalty to raise cash to build the mine. Once the mine is built, the royalty becomes a revenue stream. After the royalty company makes its first payment, the cost of that revenue is practically zero.

That business model allows royalty companies to generate enormous profit margins of 80% to 90%... a heck of a lot better than the average mining stock.

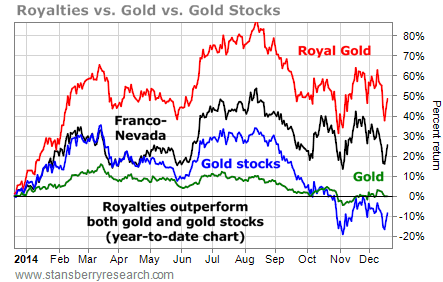

As you can see, gold royalty firms Franco-Nevada (FNV) and Royal Gold (RGLD) consistently outperform gold and the Market Vectors Gold Miners Fund (GDX), which holds a basket of major gold stocks...

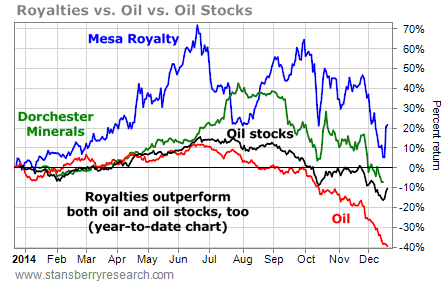

The strength in royalties isn't limited to gold. The chart below shows oil royalties Mesa Royalty Trust (MTR) and Dorchester Minerals (DMLP) plotted against West Texas Intermediate crude oil (the domestic benchmark) and the Energy Select Sector SPDR Fund (XLE), which holds a basket of major oil stocks...

As we've long said, royalty companies are some of the best you can own. And their recent strength versus the rest of the commodity market only further proves that.

Dan Ferris just recommended a brand-new royalty company to his Extreme Value portfolio. This company owns a rare 7% gross royalty. Over the past five years, it has earned an average of nearly $110 million per year in royalty payments.

This company has also received nearly $90 million in dividends off its equity since the fourth quarter of 2013. And it earns millions of dollars in commission through all of the production, sales, and shipping of its commodity.

As Dan summed up in the December issue...

Mining is a terrible business. But owning royalties can be an excellent one.

In an internal e-mail this week, Dan told us why "right now is a golden moment for any capital provider in the mining space today, including royalty companies, private-equity firms, and other deep-value investors." As he explained...

There's a whole slew of high-quality, small-cap mining companies that will need capital to survive the downturn and take advantage of new opportunities. Some of our favorite resource stocks hold shares in tiny natural-resources companies across the entire energy and commodity spectrum, including oil and gas, coal, uranium, potash, farming, cattle, iron-ore, copper, zinc, gold... you name it.

Right now, these companies' share prices are getting clobbered as the cyclical commodity market continues to pull back. But people are also rushing to the exits to sell so that they can report tax-deductible losses for 2014...

Personally, I'm doing the opposite of the tax-loss sellers. I'm buying small-cap natural resource companies. I've been buying almost every day since Thanksgiving. I even sold out of some of my best equity investments to raise cash for this opportunity. All of that fresh cash is now earmarked to buy small-cap resource stocks. Share prices were down again earlier this week, just like we expected them to be... and once again, I was buying.

As Dan continued to explain, if small-cap mining stocks are your thing – and we realize they aren't for everyone – now is the time to start buying...

If you can't be a deep contrarian in natural resources and buy when everyone is selling – you should avoid ever putting a penny into those stocks. If you are a natural-resources contrarian, this is the contrarian moment. In Extreme Value, we've recommended a small portfolio of some of the best contrarian natural-resource stocks around.

The tax-loss selling that happens this time of year is adding more pressure to beaten-up commodities.

And while Dan isn't a fan of trying to time the market, the tax-loss selling and pullback in commodities has created a terrific opportunity to pick up high-quality stocks at massive discounts. As he explained in the November issue of Extreme Value, "I've been preparing for this moment for 20 years." To get all the details about this huge opportunity – and receive all of Dan's extensive research – click here.

Regards,

Sean Goldsmith

Editor's note: Extreme Value editor Dan Ferris says that between now and the end of 2014, you have a unique opportunity in the commodities market to set yourself up for the biggest gains of your lifetime – but you must act BEFORE December 31...

And right now, you can take advantage of this opportunity by signing up for a risk-free trial subscription to Extreme Value (which includes Dan's special reports... past issues... and three brand-new issues).

http://www.growthstockwire.com/

Saturday, December 20, 2014

The recent selloff in high-yield bonds is something Stansberry Research has been warning about for months.

In short, high-yield bonds (aka "junk bonds") are the riskiest of corporate credits... And until recently, they were trading at record-high prices. Yet investors continued to leverage up and buy record amounts of junk.

In addition, energy companies have become larger and larger issuers of junk bonds. So when oil began its selloff recently, it was partly responsible for sparking the trouble in the high-yield market.

Earlier this week, Bloomberg published an interview with billionaire activist investor Carl Icahn – one of the best investors alive today. (He holds a $5 billion-plus stake in Apple in his hedge fund.) Like us, Icahn is still concerned with high yield. When asked what investors' biggest risk is today, he replied...

There's still risk in the financial markets, even though the economy looks pretty good. The one area I think is getting to be a bubble is the high-yield market. These bonds are still at way too low an interest rate. In other words, you can borrow money too cheaply if you're a risky company.

There are arguments that there's a lot of cash flow to cover the interest payments on the bonds. But some of that cash flow is ephemeral – it's not likely to last. It's a bubble that's going to burst in the next couple of years.

Icahn also agreed the selloff in oil is proof of the risk in the high-yield market... Prices have plunged in the face of a single economic shock. Icahn believes the energy sector will offer huge upside... just not today...

Oil will be a great opportunity, but not now. The energy sector is probably in for more problems. Oil prices will probably go down more, and these energy companies, especially oil-service companies, are going to be hurt. But then I think there will be a tremendous opportunity.

Oil prices will eventually recover, because worldwide demand will continue to grow and supply will diminish, due to depletion. Additionally, the cost of finding oil is growing. We are not coming up with enough alternative energy that quickly.

We don't agree with Icahn's belief that oil supplies will diminish. We don't buy into the "Peak Oil" argument. We're long human ingenuity. But he's right that the cost of finding oil is growing.

Steve Schwarzman – cofounder and CEO of private-equity giant Blackstone Group – is also looking for good deals in energy.

Blackstone is nearly finished raising a new fund for energy investments, which should be larger than $4 billion. As he recently noted at the DealBook economic conference in Manhattan...

I think this is going to be a wonderful, wonderful opportunity for us. It's going to be one of the best opportunities we've had in many, many years... This is a wonderful, wonderful time. This is a commodity. It's not patent-protected. Commodities go into undersupply and oversupply.

Oil is down to around $57 a barrel today, down nearly 50% from its highs in June. As Icahn and Schwarzman suggest, low prices will crush some producers. Supply will come offline. As supply dwindles (and demand potentially increases), prices will start to rise again. It's the definition of a commodities cycle.

We aren't predicting an oil recovery around the corner. But we do believe natural gas prices should bottom soon...

In the December 3 Growth Stock Wire, titled "How to Profit From Oil's Price Collapse," Stansberry Resource Report research analyst Brian Weepie explained how to profit from oil's price collapse. Like oil, natural gas prices had also gotten crushed. But Brian said natural gas was close to a rebound.

He also shared a chart of five natural gas producers that had been crushed this year. (Note that we've updated it as the price of oil has continued to fall since that essay was published.)

Company Mkt Cap Production % Nat Gas) Decline Since June

Chesapeake Energy (CHK) $12.4B 71% -34%

Encana (ECA) $9.9B 84% -42%

Southwestern Energy (SWN) $10.8B 100% -33%

Talisman Energy (TLM) $8.1B 63% -24%

Range Resources (RRC) $9.7B 67% -37%

Source: Capital IQ

Shares of Talisman Energy – one of the most beaten-down natural gas companies on the list – jumped nearly 20% on Monday on word that the Canada Pension Plan Investment Board was considering buying the company. That's on top of an 18% jump the previous Friday after news broke that Spanish energy company Repsol was considering buying Talisman.

While we're not going to waste our time speculating on the specific price movements of oil and natural gas, we are certain we'll see more deals like this...

Institutional investors with plenty of cash (like Blackstone) are scouring the beaten-down energy sector in search of great assets at low prices.

But one sector of commodity stocks is actually outperforming the market: royalty companies. Royalty companies have one of our favorite business models, particularly when it comes to oil and gold.

Stansberry Resource Report editor Matt Badiali explained the gold-royalty business model in a Growth Stock Wire essay last year...

Royalty companies don't actually operate mines. Instead, they own a percentage of a mine's production. Typically, a mining company sells a royalty to raise cash to build the mine. Once the mine is built, the royalty becomes a revenue stream. After the royalty company makes its first payment, the cost of that revenue is practically zero.

That business model allows royalty companies to generate enormous profit margins of 80% to 90%... a heck of a lot better than the average mining stock.

As you can see, gold royalty firms Franco-Nevada (FNV) and Royal Gold (RGLD) consistently outperform gold and the Market Vectors Gold Miners Fund (GDX), which holds a basket of major gold stocks...

The strength in royalties isn't limited to gold. The chart below shows oil royalties Mesa Royalty Trust (MTR) and Dorchester Minerals (DMLP) plotted against West Texas Intermediate crude oil (the domestic benchmark) and the Energy Select Sector SPDR Fund (XLE), which holds a basket of major oil stocks...

As we've long said, royalty companies are some of the best you can own. And their recent strength versus the rest of the commodity market only further proves that.

Dan Ferris just recommended a brand-new royalty company to his Extreme Value portfolio. This company owns a rare 7% gross royalty. Over the past five years, it has earned an average of nearly $110 million per year in royalty payments.

This company has also received nearly $90 million in dividends off its equity since the fourth quarter of 2013. And it earns millions of dollars in commission through all of the production, sales, and shipping of its commodity.

As Dan summed up in the December issue...

Mining is a terrible business. But owning royalties can be an excellent one.

In an internal e-mail this week, Dan told us why "right now is a golden moment for any capital provider in the mining space today, including royalty companies, private-equity firms, and other deep-value investors." As he explained...

There's a whole slew of high-quality, small-cap mining companies that will need capital to survive the downturn and take advantage of new opportunities. Some of our favorite resource stocks hold shares in tiny natural-resources companies across the entire energy and commodity spectrum, including oil and gas, coal, uranium, potash, farming, cattle, iron-ore, copper, zinc, gold... you name it.

Right now, these companies' share prices are getting clobbered as the cyclical commodity market continues to pull back. But people are also rushing to the exits to sell so that they can report tax-deductible losses for 2014...

Personally, I'm doing the opposite of the tax-loss sellers. I'm buying small-cap natural resource companies. I've been buying almost every day since Thanksgiving. I even sold out of some of my best equity investments to raise cash for this opportunity. All of that fresh cash is now earmarked to buy small-cap resource stocks. Share prices were down again earlier this week, just like we expected them to be... and once again, I was buying.

As Dan continued to explain, if small-cap mining stocks are your thing – and we realize they aren't for everyone – now is the time to start buying...

If you can't be a deep contrarian in natural resources and buy when everyone is selling – you should avoid ever putting a penny into those stocks. If you are a natural-resources contrarian, this is the contrarian moment. In Extreme Value, we've recommended a small portfolio of some of the best contrarian natural-resource stocks around.

The tax-loss selling that happens this time of year is adding more pressure to beaten-up commodities.

And while Dan isn't a fan of trying to time the market, the tax-loss selling and pullback in commodities has created a terrific opportunity to pick up high-quality stocks at massive discounts. As he explained in the November issue of Extreme Value, "I've been preparing for this moment for 20 years." To get all the details about this huge opportunity – and receive all of Dan's extensive research – click here.

Regards,

Sean Goldsmith

Editor's note: Extreme Value editor Dan Ferris says that between now and the end of 2014, you have a unique opportunity in the commodities market to set yourself up for the biggest gains of your lifetime – but you must act BEFORE December 31...

And right now, you can take advantage of this opportunity by signing up for a risk-free trial subscription to Extreme Value (which includes Dan's special reports... past issues... and three brand-new issues).

http://www.growthstockwire.com/

Join the InvestorsHub Community

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.