News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

chico237

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

The Recent News & Timing is "Interesting"..... If you follow the context of Responses shared from Niocorp Management. I remain Hopeful our team will complete the F.S. & Finance in 2023!

Sharing Jims Response to past & recent questions & given (HOW) the recent "SEVEN FIGURE CLOSED $$$$..... ) Has my attention!

Niocorp's "PRIMARY financing focus has been on Private Sector Sources!"However the possibility of a U.S. govt. loan guarantee remains.... See trail below:

U.S. Senate Committee on Energy and Natural Resources

January 27, 2021 Hearing

ENR QFR Template (senate.gov)

Secretary Grantholm's Answer 7: Critical Mineral projects are eligible for loan guarantees under the Title XVII Innovative Technologies Loan Guarantee Program and the Advanced Technology Vehicles Manufacturing Program. If confirmed as Secretary, I will encourage applications from potential projects that meet the applicable statutory and regulatory criteria involving the production, manufacture, recycling, processing, recovery, or reuse of Critical Minerals and other minerals to advance clean energy and advanced vehicle manufacturing technologies.

Please see Jim's responses 6/2021-

(Jim...Private funding methods have been the primary target however, ... can you offer any comment to the following questions.)

a) Does/Can Niocorp qualify for a U.S. govt. (DOE/DOD) Loan, or Loan Guarantee as described above or similar ?

Quite possibly, and we are in discussions with them on this now. However, the ability of this program to fund critical minerals projects will depend upon what the Democratic leadership in Congress enacts in its appropriations bills, as new funding is required to cover the credit subsidy cost of these loans. In recent years, the Congressional appropriations process has been a very politically contentious with little bipartisan agreement on much of anything. Some opposition in the Congress has already quietly developed to the Administration’s proposal to expand this program’s traditional funding focus to include critical minerals mines, which it has not funded in the past. Regardless, it is not likely that funding levels for the credit subsidies used by these programs will be finalized until late this year, or into next year.

I will add that our team is very familiar with the DOE Loan Guarantee program, as we navigated this process some years ago. It is a very slow process and requires more than a year (for some projects) to complete. It also costs a great deal of money and resources in which to engage in this process – those costs can easily grow into the 7 figures. We continue to examine the possibilities here, however.

"This funding was placed in the FY24 DoD Appropriations bill at the request of Nebraska Senator Deb Fischer, a member of the Senate Appropriations Committee, for the purpose of helping to fund NioCorp's effort to establish domestic commercial production of AlSc master alloy. There is always a process within the DoD to select appropriate projects with funding provided to it by Congress. In this case, however, the House and Senate Armed Services Committees provided additional guidance to DoD on this topic in their respective National Defense Authorization bills, including prioritizing domestic production of such materials."

"Latent markets for scandium oxide and aluminum-scandium master alloy – both commercial and military -- are quite large, and we are working with a number of potential scandium consumers and related technology companies interested in scandium. We will make announcements in this area as developments require. In general, we don’t comment on detailed commercial business strategies except in the course of necessary announcements and/or public filings. "

"There are multiple such engagements ongoing now for each product in our planned product offering. In general, we don’t comment on commercial business strategies except in the course of necessary announcements and/or public filings. "

"YES"

Thanks Crit! Waiting with many…

Chico

I’m with you Jeunke! My back of the napkin numbers look really good to me! (I’ve posted $220million plus just for REE’s)

Scott Honan stated Niocorp intends to produce at least 750 Tons of REE oxides per year (there is a video I posted a while back that will confirm such).

“I still think Niocorp could push that number to 1,000 Tons/yr.) given the metrics”

Jeunke - as you have stated that’s $600 M +\_.

Plus the New improved Niobium & Titanium oxides…

Entities are interested per recent Niocorp responses to my questions posted. I do agree the current share price sucks after that Deal!

Yet fundamentally nothing has changed imho….

Yep I’m Waiting with many!….

Chico

Stellantis, Ford, GM, VW and more could also be moving towards ScAl frames, battery boxes & more to lightweight the industry & compete with Tesla innovations.

Remembering the addition of less than 1% of scandium allows tremendous “weld-ability”!

Niocorp stands ready to deliver 100 tons per year in addition to upgraded Titanium & Niobium oxides & REE’s.

I have shared my responses from Jim/management on direct relevant questions on the aforementioned critical minerals.

Folks seeing all the recent news releases, and responses can form their own opinions as always.

Imho- nothing fundamentally has changed. Niocorp has only two goals left.

1) Announce independently verified 2023 F.S. (With all the updated goodies & CAPEX/Opex)

2) Announce Project FINANCE-via any combination of ALL the methods being hinted as being in play by management.

EXIM,DoE/LPO, DoD, Stellantis or other Entities T.B.D. Even that major U.S. Steel manufacturer is still on the line!

Waiting with many….

With my PPE on! :)

Chico

I agree NorCal- Entities have got to be running their own numbers & closely watching (NDA’s).

Several options are still in play per responses shared (August 14th)! Anything can happen…. We could wake up to a DoE announcement, EXIM commitment letter, Stellantis Anchor investor, DoD offtake or any combo….

Waiting still with many

Hey NorCal! I believe that is the fifth or sixth time I asked Jim a variation of that exact question & have shared & posted the entire series & line of questions & responses.

Each time Jim has answered has been “YES”.

For clarity-

In this instance I did take the liberty of adding the “!” …, but the answer is still “YES”.

( Other entities which may include those mentions and more… but do not allow comment are interested & May be in play.)

So for the fifth or sixth time asked - Niocorp has responded “YES”.

Form your own opinions & conclusions above:

Imho- the share price sucks! But nothing fundamentally has changed. The critical minerals the Elk Creek Mine will produce appears to be generating & forming (behind the scenes) -

Supply Chain inputs & outputs with some “Serious Players” (DoE,DoD, EXIM, Stellantis … even the major U.S. steel manufacturer & other entities??? -“YES”

Waiting with many…

Chico

Hey GE & NorCal! All is well… busy lately.

Looking for “PROOF” from Niocorp now a completed 2023 F.S. & “Finance!” With many here.

We may get “Proof” of Aliens or Skunk-Works stuff first??? Who knows lol!!

Either way… I’m sure they both could utilize some of the critical minerals Niocorp will provide.

Waiting… still here… with many!

Yada… Yada… indeed!

Chico

PM, Grunt, PC- Thank you all for sharing your responses! Still here waiting with many…

Chico

When You Play the Game OF Mines~ "You Win... Or You DIE!"

"I HOPE NIOCORP HAS SOME DRAGONS??" cause even I have to admit this SHARE PRICE is a DISMAL Performance since listing on the NASDAQ after the GXII DEAL!!!!!!

PLAY TO WIN TEAM NIOCORP!!! LETS GO!!!!!!

Chico

JULY 12th 2023 - American Lithium Intersects Highest Grade Lithium and Cesium Samples Encountered to Date at Falchani - Up to 5,645 ppm Lithium and up to 12610 ppm Cesium

https://mailchi.mp/americanlithiumcorp/surgeinvestmentclose-8224263?e=1f0e41ab3d

American Lithium Intersects Highest Grade Lithium and Cesium Samples Encountered to Date at Falchani - Up to 5,645 ppm Lithium and up to 12610 ppm Cesium

VANCOUVER, BRITISH COLUMBIA, July 12, 2023 – American Lithium Corp. (“American Lithium” or the “Company”) (TSX-V:LI | NASDAQ:AMLI | Frankfurt:5LA1) is pleased to provide details of assay results from three diamond drill holes recently drilled at the Falchani Lithium project in Puno, southeastern Peru (“Falchani”). These 3 holes were drilled under the ten-hole Environmental Impact Assessment (“EIA”) hydrology drilling program launched at Falchani last fall as part of the EIA hydrology study designed by EDASI SAC and SRK Peru with field work overseen by EDASI. This program has successfully demonstrated that there are no water table issues within proposed development areas across Falchani and the program has also enabled the drilling and analysis of core down to a depth of 120 metres (“m”). Once full results from this program are complete all data and assays will be incorporated into an updated resource report on Falchani to be prepared by Stantec Consulting, Inc (“Stantec”).

Core logging and assay results from these three diamond holes intersected intervals of typical Falchani volcanic tuff as well as large sections of breccias with highlights including Lithium up to 5,645 ppm and Cesium up to 1.22%, the highest grades of both metals encountered to date from 1 m drill core interval samples at Falchani. These holes were drilled in key areas both within and outside the current Falchani resource footprint and will add additional information to the planned mineral resource estimate update with a focus on expanding the overall resource and reclassifying the existing resource. Full details of the results from these three holes are set out below:

EIA Drill Program and Initial Results

Link to: Figure 1 – Falchani EIA Hydrology and Previous Drill Hole Location Map (also see below)

EIA diamond drill hole Pz04-TV (vertical) intersected lithium mineralization over the entire vertical drill hole; 0-120 m averaged 2,186 ppm Lithium (Li); 841 ppm Cesium (Cs); 1,215 ppm Rubidium (Rb); and 2.62% Potassium (K) - (see Table 1 – Drill Hole Pz04-TV results, below):

Several substantial sub-intervals of +3,000 ppm Li intersected;

Maximum Li of 5,645 ppm Li over 1 m at 54 m downhole; and

This drill hole is the westernmost drill hole reported at Falchani and extends the drilled mineralization approximately 250 m further west. Mineralization remains open at depth (>120 m).

EIA diamond drill hole Pz03-TV (vertical) intersected the strongest Cesium mineralization to date with associated moderate lithium mineralization over the upper 63 m downhole averaging 1,428 ppm Li; 4,770 ppm Cs; 1,188 ppm Rb; and 2.67 %K (see Table 2 – Drill Hole Pz03-TV results, below):

The upper interval (0-23 m) is richer in Li with the lower interval (23-63 m) much richer in Cs, including the highest 1 m Cs interval sample encountered at Falchani of 12,160 ppm Cs (1.2% Cs);

Cs mineralization is associated with more intense brecciation and hydrothermal overprint observed in this hole, drilled from within the natural valley separating the east and western parts of the Falchani resource. This hole establishes the deposit thickness/bottom within the valley.

EIA diamond drill hole Pz06-TV (vertical) intersected typical Falchani tuff over the entire 86 m drilled and analyzed to date averaging 2,739 ppm Li; 338 ppm Cs; 1,292 ppm Rb; and 2.87% K (see Table 3 – Drill Hole Pz06-TV results, below); drilling at this location continues in Li mineralization.

Ground water has yet to be encountered in any holes within the 120 m reporting drill depth, so EDASI and the Company is requesting permission from ANA, the National Water Authority, to drill deeper:

10 diamond drill holes were approved for EIA drilling, including installation of downhole piezometers to monitor water table and local groundwater parameters where water is encountered;

Every 5m EDASI collects drill hole wall-rock measurements of moisture content, water, etc. resulting in very slow drill advancement, but essential data and information for feasibility study;

Drill core chemical analysis is required under the EIA, and reporting mineralization is allowed; and

EIA Program is close to completion and additional results will be reported when available.

Simon Clarke, CEO of American Lithium states, “We are excited to have intersected thick, high grade lithium mineralization west of the current Falchani resource footprint, which should allow for resource expansion. The strong cesium and lithium mineralization encountered in the central valley bisecting Falchani is also very interesting from a strategic perspective with higher than previously recorded cesium grades. The entire EIA program will provide valuable additional data to the existing drill results from Falchani.

We are also very pleased to be back working constructively and successfully in Peru. We received the first new permits for the new Quelcaya targets several weeks ago and have also launched a new drill program on some of our best targets across the Macusani Plateau. We anticipate receiving our next drill permits for additional infill and expansion drilling at both the Falchani Deposit and the Macusani Uranium Project shortly. Expanding and reclassifying the resource is a key piece of the updated PEA we are targeting for the end of Q3.

News continues with additional charts....

Form your own opinions & conclusions above!

FALCHANI & TLC PROJECTS ARE GAINING TRACTION - (I think production 2027/2028 is in the cards... keep adding, trading as each investor sees fit!) IMHO

STELLANTIS, FORD,VW & OTHER AUTOMAKERS NEED LITHIUM AS THEY BUILD OUT BATTERY MANUFACTURING SUPPLY CHAINS! AMERICAN LITHIUMS TWO PROJECTS ARE WELL ADVANCED & MY GUESS 3- YEARS OUT @ 2027 timeframe. LOOK FORWARD TO PEA's, then F.S. & Finance & OFF-Take agreements or a BUY-OUT FROM larger Lithium producer...

Chico

Thanks for Posting HETFIELD!!!! eom

Great article & read! Thank-you for sharing Dakota! Knowing what the Niobium, Scandium, Titanium & Rare Earths can do…

& the need for a stable , secure domestic supply.

Niocorp’s Elk Creek ESG/GHG driven generational mine will be built!

Chico

Nice find GE! Thanks for sharing... you may also like this one... Fernada Fenga should be happy!

https://www.msn.com/en-us/money/markets/the-world-bank-is-betting-on-this-company-to-green-the-16-trillion-steel-industry-take-a-look-inside/ar-AA1c9hOF

JUNE 12, 2023~A new discovery could lead to a mining resurgence in the West~

https://www.boisestatepublicradio.org/show/idaho-matters/2023-06-12/rare-earth-mineral-mining-in-the-west

THIS DEPOSIT IS WORLD CLASS & about 7 -10 YEARS out! KEEP this on your watch list!

Chico

June 11, 2023~ How the U.S. let EV battery tech born here wind up in the hands of China

Startup A123's failure haunts the U.S. — and reveals our flawed approach to innovation

https://www.autoblog.com/2023/06/11/how-the-u-s-let-ev-battery-tech-born-here-wind-up-in-the-hands-of-china/

On a 3-mile stretch of farmland in southwest Michigan, Ford Motor Co. is building a battery factory. The technology Ford needs to make cheap, stable batteries to power electric vehicles will come from China’s Contemporary Amperex Technology Co. Ltd., better known as CATL, the world’s biggest battery manufacturer. By most measures, Ford’s deal with the Chinese giant is a coup for the state — it’s getting a $3.5 billion investment in a 2.5-million-square-foot factory, thousands of new jobs and the ability to produce enough batteries annually to power 400,000 electric vehicles when the plant opens in 2026. But for anyone who’s been paying attention, it’s a devastating moment of irony for the U.S.: The deal could have been the other way around.

A niobium anode allows this type of battery to sidestep the intercalation problem that stops most other batteries from charging up at a fast rate. In a lithium ion battery, intercalation is the process of moving the lithium ion from the cathode and inserting it into the graphite anode. It’s the reversible process of storing molecules or ions within layered structures. There’s only so fast this process can happen. Niobium’s structure allows for extremely fast changing and discharging, which means that a niobium battery functions more like a capacitor than a traditional battery. It’s actually not that far off from the SuperBattery, a supercapacitor/battery hybrid, which is produced by Skeleton Technologies in Estonia and Germany.

Across the pond, Battery Streak is currently trying to commercialize this technology from its California headquarters. Its battery can achieve an 80% charge in only 10 minutes. That’s C-rate of about 6C! This speed also doesn’t sacrifice much energy density, as these batteries can pack about 140 Wh/kg (with the goal of 180), and last a strong 3,000 cycles. But Battery Streak has tested them at up to 9,000 charge cycles.23 24 25

Niobium batteries can also stay very cool, unlike most other batteries. While a standard battery’s temperature gradient is about 27 C, a niobium battery’s temperature gradient is significantly lower at 8 C.24 So, where’s the downside? Just like any other battery we’ve talked about with a very high charge rate, it’s an infrastructure problem. Even if you put this into an EV, there’s nothing available right now that could charge it at full capacity. Both Battery Streak and CBMM, a Brazilian company specializing in niobium products, are hopeful that commercialization can begin this year or in 2024.

Our 3rd generation XNO® anode material is available world-wide at the multi-tonne scale today, and will be available at the 2000 t/year scale from 2024.

We typically supply samples up to 1 tonne scale under a simple Material Transfer Agreement, and have the ability to enter multi-year supply agreements for larger quantities guaranteeing outstanding quality, support, and supply security to our customers.

LCP- Here are the "PLANT" pictures you requested:

PLEASE SEE 2018 PLANT

DOH- they've been DELAYED again 2 years later 2020 Please see picture of "2020 The PLANT"!

DOH- they've been DELAYED again ..... 2023...... Still waiting. LCP What are they doing there exactly????? NIOCORP has posted & completed A LOT in 2023, Yet when I look here- "Not so much!"

https://www.sunriseem.com/investors/asx-announcements/

They appear to be waiting for Finance too.... "Imagine that! & they priced Scandium much lower too!"

Fully understand if this gets removed but.... it is kinda relevant? =).....

Chico

American Lithium Reaches Definitive Agreement to Spin Out

Macusani Uranium Deposit into an Independent Public Company

https://mailchi.mp/americanlithiumcorp/macusanispinout?e=1f0e41ab3d

RIDING THIS INTO PRODUCTION!

TLC -LITHIUM

FACHANI-LITHIUM

Not yet sure what URANIUM Company this will turn into or how it all pans out? But they are SPINNING it out into a new entity.

Under $2 is undervalued. One good OFF-take agreement and a F.S. away from $$$

all IMHO

Chico

Thanks for sharing, Richard! Someone on another board posted this =) a while back. I did take a peek & although I am just a lil construction dude. The report really points out the obvious facts & flaws that the U.S. has allowed to happen on (All Watches!)....

A) MP Materials produces a mixed CONCENTRATE!!!!!

B) That currently all Rare Earth Separation is done in CHINA & all OXIDES ARE CREATED IN CHINA & shipped back to the U.S. for OEMS & End-User Industries

C) In late 2024 MP materials & partner GM are (With U.S. Govt. LOAN over $150Million) Building out a U.S. Based Separation facility here in the U.S. (TEXAS).

D) MP Materials produces "VERY LITTLE" Terbium & Dysprosium (Negligible)

E) The U.S. DoD & Defense Contractors & Private Industries rely heavily on MAGNETS, METAL ALLOYS & MATERIALS currently sourced from China, or derivatives thereof; & much more!

Currently there is a move to DE-GLOBALIZE & RE-SHORE many such industries back to the U.S. & Allies (Or those countries that share similar values) Niocorp is very well postitioned right now to take full advantage of the current situation.

Please see Jim's responses to questions posed for comment-3/17/2022.

~A) Could you comment on what the production of higher purity Niobium & Titanium could be utilized for once realized?

RESPONSE:

"If the higher purity niobium and titanium intermediates that L3 was able to produce at bench-scale are replicated and proven at demonstration scale, this would put us in a position to more easily move to other products beyond those outlined in our 2019 Feasibility Study. Niobium oxide for use in Li-Ion batteries is one possible example, although the production of that product would require additional processing steps beyond the higher-purity niobium intermediate that we discussed in last week’s news release. The company is not yet in a position to make a determination on whether or not, and when, to possibly expand our Niobium product offering. Higher grade TiO2 could expose us to additional markets where higher margins could be obtained. But, again, we are not in a position to speak to those possibilities in any detail yet. "

"No, the processes we recently discussed occur in the earlier stages of the flowsheet, prior to any SX processing. We look forward to unveiling those details once these processes are verified at the demonstration plant level and once all associated work needed to complete an updated Feasibility Study is completed. "

"We have made an internal estimate of the benefits of our planned products at a Scope 3 emissions level. However, the definition and applicability of Scope 3 emissions must eventually be determined by government regulators, and the SEC is examining many aspects of this issue now. At present and in general, carbon credits are created by mitigation measures taken at the Scope 1 emissions level, although there are several different approaches being examined across the U.S. As to DOE programs, I am not allowed to comment on that at this time."

"Yes. "

"Yes, multiple federal agencies, elected officials in the Congress, and the WH. "

Grunt & I both posted are back of the napkin numbers -All speculation of course! Everyone can run there own & play with the results but no matter which way you hit the NIOCORP values they land pretty solid at $600 + IMHO

Just look at what MP materials makes in a year for those casting doubts.... NIOCORP will match or exceed (all imho)

Should be an interesting 2023 F.S. for sure "Third times a charm!" lol

Chico

Advocate- I have shared along with many of your frustrations! I have agreed with you on several occasions & I have vented at times as well on the board! "AS MANY HAVE DONE!"

They appear to be doing exactly what they stated during the 2020 AGM presentation, & it has indeed taken a lot more time than many expected.

Fundamentally nothing has changed with the project.

IN FACT- the project has become more robust than ever before in light of recent DEMO Plant results announced! Compared to all the other U.S. Projects (Of which I have followed & posted relevant information.) Niocorp still stands on top of all it's pier U.S. Competitors with the exception of MP Materials (Aligned with GM) for which CHINA still holds power over until late 2024 when their U.S. Separation comes online.

Niocorp team appears to have (D, E, F & G.... etc... IN MOTION or in PLAY.....) (SEVERAL FEDERAL AGENCIES , CONGRESS & THE WHITEHOUSE, EXIM BANK & OTHER ENTITES as well as private potential Anchor Investors.

I am staying tuned with many here, & yes 2024 start is looking very good.

Note "I always thought 2025... then with covid 2026.... but I guess I can wait a bit longer too! lol!

I THINK

&

PENDING THAT DARN DEBT/EQUITY STUFF!!

Oh & I appreciate your common point of views very much!!!! Thank you!

Chico

Wagner- MP materials produces very LITTLE Terbium or Dysprosium! It is not present in their ore bodies geology in any great measurable content for production!

See post #76063 From November of 2021.

THE OUTPUT & ECONOMICS OF THESE PROJECTS HAVE NOT CHANGED- TO-Date!! ("BUT NIOCORPS ENTIRE INTENDED PRODUCTION OF NIOBIUM, SCANDIUM, TITANIUM & VIABLE RARE EARTHS HAS & IS BEING INCORPORATED INTO A NEW 2023 F.S.

BEAR LODGE RESOURCE WYOMING (REEMF): Plans to generate @$330 Million/year from REE production

https://www.rareelementresources.com/docs/default-source/pdfs/rer-corporate-presentation_june-2021.pdf?sfvrsn=2

http://www.rareelementresources.com/App_Themes/NI43-101PreFeasibilityStudyReport/HTML/files/assets/basic-html/index.html#562

Table 25.2 - Bear Lodge Financial Summary

(US$ Million)Pre-tax / After-tax NPV @ 10%

Discount Rate $426 /$330

Pre-tax / After-tax IRR 32.7% / 28.6%

Project Payback After Start-up (years)2.9

Assumed Discounted RE basket price/kg$24.60

Estimated Annual Cash Operating Cost,LOM (US$ millions)$102.6

Bear Lodge- "Pilot plant testing/needs permits, gaining fast"

Owner: Rare Element Resources (REEMF:OTC) and General Atomics

Deposit Type: Carbonatite with Bastnäsite

Resource (1.5% TREO c/o): 16.2 Million mt (M & Ind)*

In-place TREO Grade: 8.0%

In-place TREO: 1.3 Million mt

Annual TREO Production: 20,000 mt

Annual Pr Oxide Output: 1,200 mt ( 7.5% of 2025 US demand)

Annual Nd Oxide Output: 4,500 mt (11.3% of 2025 US demand)

Annual Tb Oxide Output: 30 mt ( 4.9% of 2025 US demand)

Annual Dy Oxide Output: 90 mt ( 3.2% of 2025 US demand)

Comments: - Additional inferred resource of 41 Million mt

- An advanced, partnered project located in Wyoming, U.S.

- Entering pilot plant phase with major partner General Atomic

Round Top Project, Texas (TMRC)-

http://tmrcorp.com/_resources/presentations/corporate_presentation-20201112.pdf

NPV (10% Pre-Tax)(based upon current spot Mineral pricing)=$1.56 billion

IRR (Pre-Tax) 70%

Payback Period 1.4 years

Initial Life of Mine 20 years*

Average Annual Revenue $396 million-(***NOTE @$113 MILLION is generated from REE production alone!)

Round Top -"Is Shovel Ready looking to start production 2023/4"

Owner: Texas Mineral Resources w/ USA Rare Earths Earn-In (OTCQB:TMRC)

Deposit Type: Tertiary peralkaline rhyolite intrusion

Resource: 364 Million mt (M & I)*

In-place Pr Grade: 10.3 ppm (crustal abundance 7.1 ppm)

In-place Nd Grade: 27.9 ppm (crustal abundance 26.0 ppm)

In-place Tb Grade: 3.5 ppm (crustal abundance 0.06 ppm)

In-place Dy Grade: 33.3 ppm (crustal abundance 3.5 ppm)

Annual Mine Production: 7.3 Million mt TPY (20,000 TPD leach feed)

Annual Pr Oxide Output: 70 mt (0.4% of 2025 US demand)

Annual Nd Oxide Output: 182 mt (0.4% of 2025 US demand)

Annual Tb Oxide Output: 24 mt (4.0% of 2025 US demand)

Annual Dy Oxide Output: 207 mt (7.4% of 2025 US demand)

- Advanced Project located in Texas, U.S. has low REE grades in abundance

~Partnered with USA Rare Earth going public via SPAC later this year owning 80% stake & pursuing mine to magnet strategy

- Projected as a multi-industrial minerals/metals and commodity

chemicals manufacturer, with REEs as by-products

- PEA (2019) claims project will produce 20 products:

Y, Pr, Nd, Sm, Tb, Dy, Lu, Sc and Ga Oxides; Be Hydroxide; U3O8

,Li Carbonate; Al, Fe, Mg, Mn and K Sulfates

UCORE

https://ucore.com/docs/PEA.pdf

Bokan Mountain -(years away IMHO)

Owner: Ucore Rare Metals (TSX-V: UCU, OTCQX:UURAF, FSE: U9U)

Deposit Type: Alkaline Igneous Intrusion

Resource (at 0.04 % TREO c/o): 5.8 Million mt (M & I)*

In-place TREO Grade: 0.60%

In-place TREO: 28,000 mt

Recoverable TREO: 22,500 mt

Annual TREO Production: 1,875 mt (1,500 TPD mill feed)

Annual Pr Oxide Output: 71 mt (1.2% of 2025 US demand)

Annual Nd Oxide Output: 274 mt (1.8% of 2025 US demand)

Annual Tb Oxide Output: 12 mt (5.5% of 2025 US demand)

Annual Dy Oxide Output: 83 mt (7.9% of 2025 US demand)

Comments: - Small resource; Dotson Zone geologically constrained

- Adjacent to EPA Superfund site (Uranium) located in Alaska, U.S.

- Alaska AIEDA commitment of $145 M (but only with a positive

Feasibility Study – the least advanced project)

- 2019 PR claims it will produce the REE “basket” plus Nb, Zr,

Be, Hf, TiO2

***Note: U-Core is pursuing it's Alaskan "Separation Plant" utilizing it's proprietary Rapid SX tech.

MP Materials-California

Expects to generate additonal @$250Million/year from Nd/Pr production once in operation 2023/4! (see attached) CURRENTLY SENDA ALL PRODUCTION TO CHINA FOR PROCESSING!

https://s25.q4cdn.com/570172628/files/doc_presentations/2021/MP-Feb_2021_Sust_ESG_Deck-02.24.21-FINAL.pdf

Mountain Pass - Currently one of the only Producers of REE materials with Chinese "Interests!":

Owner: MP Materials - JHL Capital Group, QVT Financial LP,

Shenghe Resources Holding Co. Ltd.(9.9%)

Deposit Type: Carbonatite with 10-15% Bastnäsite

Resource (5.0% TREO C/O): 16.7 Million mt (P & P)*

In-place TREO Grade: 8.0% (Highest grade in U.S.)

In-place TREO: 1.3 Million mt (83% La and Ce)

Annual Pr Oxide Output: 927 mt (15.4% of 2025 US demand)

Annual Nd Oxide Output: 2,511 mt (16.7% of 2025 US demand)

Annual Tb Oxide Output: Very small production in past

Annual Dy Oxide Output: Very small production in past

Comments: - Currently produces only REE concentrates

- Resource is likely much, much larger than current “reserves”

- Currently produces only REE concentrates which are all

exported to China for processing to metal; plans to have U.S. based pilot plant & production in @2024

Form your own opinions & conclusions above:

Chico

AWESOME thanks for posting Element41! eom

PM & ALL- I think you will find the response to this question posed in June of 2021, & Given ALL the Material News Events leading up to present June 2023 -

"Interesting!"

JUNE 17, 2021:

a) Does/Can Niocorp qualify for a U.S. govt. (DOE/DOD) Loan, or Loan Guarantee as described above or similar ?

"Quite possibly, and we are in discussions with them on this now. However, the ability of this program to fund critical minerals projects will depend upon what the Democratic leadership in Congress enacts in its appropriations bills, as new funding is required to cover the credit subsidy cost of these loans. In recent years, the Congressional appropriations process has been a very politically contentious with little bipartisan agreement on much of anything. Some opposition in the Congress has already quietly developed to the Administration’s proposal to expand this program’s traditional funding focus to include critical minerals mines, which it has not funded in the past. Regardless, it is not likely that funding levels for the credit subsidies used by these programs will be finalized until late this year, or into next year.

I will add that our team is very familiar with the DOE Loan Guarantee program, as we navigated this process some years ago. It is a very slow process and requires more than a year (for some projects) to complete. It also costs a great deal of money and resources in which to engage in this process – those costs can easily grow into the 7 figures. We continue to examine the possibilities here, however."

Elk Creek gets built before Sunrise! Place your bets!

I’m betting on the Elk Creek mine! & team Niocorp.

Chico

Thanks Hetfield! One Application has been officially announced! ARE THERE OTHERS???

MAY 2023 ~DoE/LPO MONTHLY APPLICATION ACTIVITY REPORT Loan Programs Office~

MONTHLY APPLICATION ACTIVITY REPORT | Department of Energy

APRIL 2023 SHOWN FOR COMPARISON

NOTE:

Each month, the LPO Monthly Application Activity report updates:

The total number of current active applications that have been formally submitted to LPO (150)

The cumulative dollar amount of LPO financing requested in these active applications ($127.7 billion)

The 24-week rolling average of new applications per week as of the close of the previous month (1.7)

Technology sectors represented by applications

Proposed project locations represented by applications

6. Status of where applications stand in the review process: Of the 150 active applications, approximately 45% of applications are under initial review, approximately 40% are under advanced review, and roughly 15% are in due diligence

NEBRASKA & the (PLAINS AREA ) HAVE 28 ACTIVE APPLICATIONS or at 40% = 11 UNDER ADVANCED REVIEW! (WHAT ARE THE CHANCES NEBRASKA HAS ONE OR TWO???)

FORM YOUR OWN OPINIONS & CONCLUSIONS ABOVE:

Very Happy to see the announcement of a Formal APPLICATION TO THE EXIM BANK!

IMHO - There could be multiple applications in play given everything I have shared & posted D.D.

Waiting with many!

Chico

Thanks Nebraskan! You have brought up an excellent subject. There was a deadline in place (2024) rings a bell but unable to check Right right now…

I agree Richard! There are thing going on behind the scenes for some time now! If a person were to look at some of Niocorp’s News releases with L3 they do state something along the lines of-[/quote]”working with L3 & other entities..” [/quote]

Niocorp was questioned on this topic several times over several years & I posted that info here. (There are other entities doing stuff?.. what exactly ??? T.B.D.)

I wonder if the folks from the Sunrise project would answer that too… still waiting! Lol

Chico

They did produce AlSc alloy materials with both IBC & Ames Lab. When asked if they intended to patent the materials then Niocorp stated they wanted to keep it simple & just prove they could do it.

Now with all updated recoveries, economics proven at Demo Scale for production.

Niocorp is collaborating with NanoScale on “PATENTABLE” AlSc alloys/powders should they prove out. Allowing three years +/- to develop and scale out. Not only that but Niocorp is working with other entities in the background with Scandium. ( I can think of several entities for that)

Then you must consider what entities want the new Niobium & Titanium oxides and Chlorides chief! ( Knowing what they can do… & the need for a stable U.S. strategic supply. I would think future collaboration/off take agreements will be in play.)

Of course all pending that elusive finance. But hey …. EXIM BANK IS INTERESTED..& I think/speculate other entities are as well)

I can wait a little longer. Heck even the Sunrise project is treading water still imagine that!)

Chico

I’m TICKLED PINK -Grunt. Niocorp just released a Niobium update.. The last 25% of production was never placed under an enforceable contract since 2020. Now with improved recoveries you’re looking at about 30% more Niobium at a HIGHER PRICE POINT!

Then Titanium, Scandium and viable rare earths.

Your numbers and mine own funky speculations look darn good to me & in the ballpark.

Standing bye my 600/700$ million /year before Opex opinion.

Pending the 2023 F.S. & that darn elusive debt/equity finance that will allow us to sign the EPC contractors and build the project (T.B.D.)

Waiting to go “Fly a Kite ?? with many!

Chico

Hey Doug! I understood Niocorp/NanoScale are collaborating on AlSc master alloys with a Scandium ratio "up to 5%". Typically 1-2% are used but there are many cases where higher ratios are used for both Defense, Aerospace & Private Industries, although less common. (NOTE: Higher Ratios EXIST! High Entropy Alloys with %20 to %30 Scandium!)

Aluminum scandium alloys

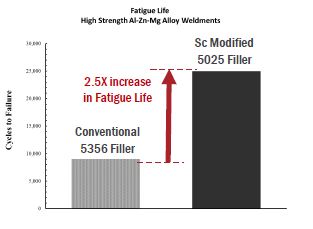

Advantages on different areas when scandium is added in aluminum alloys. This is shown if the graph below.

Due to its fine grain refinement Scandium alloys reduces hot cracking in welds, increased strength in the welds and deliver better fatigue behavior. Welding filler/ thread with scandium has great potential for aluminum.

A NICE "WHITE-PAPER" On SCANDIUM & AlSc Alloys from a competitor is always worth a view!:

https://scandiummining.com/site/assets/files/5740/scandium-white-paperemc-website-june-2014-.pdf

Current Market Opportunities for Scandium

Two robust growth markets await a reliable and expanded supply of scandium. These are defined as markets that would be able to utilize 2-5 times their current consumption, if only the supply sources were there to offer scandium at prices that could be absorbed into the product. In each case, the end product is a game-changer, and the cost of the new material comes with performance offsets that pay for the higher expense.

These two markets are:

1. Solid Oxide Fuel Cells (SOFC’s), and

2. Scandium-alloyed Aluminum alloys (Al-Sc alloys)

Aluminum-Scandium Alloys (Al-Sc)

In general, it is possible to modify and improve aluminum or titanium base materials by alloying them with scandium, typically by additions of up to 2% scandium (by weight). When scandium and aluminum metal are combined in a molten state, these two elements can be made to solidify in a number of different intermetallic phases, depending on the cooling temperature selected, and the Al-Sc ratio present. The most desirable of those phases (dispersoids) is as Al3Sc, which holds scandium in thermodynamic equilibrium with aluminum, and is the form that exhibits the most dramatic effects on

the microstructure and properties of the resultant aluminum alloy material, which we will refer to as Al-Scalloy.

The key changes are

? Grain Refinement – Scandium promotes (during so called heterogeneous nucleation) the

formation of small, evenly shaped (equiaxed) grains in the alloy melt, which is a desirable

characteristic. As a molten alloy metal mixture cools and solidifies, smaller evenly shaped grains are able to better fill the cavities created by the shrinking solidified metal. This creates increased strength by avoiding shrinkage porosity, and also reduces the tendency for hot cracking, which shows up in high temperature environments or as a result of welding. This grain refinement markedly improves both weldability and weld strength.

? Superplasticity – This characteristic is defined as a substance’s ability to bend under stresses that would normally cause a fracture, and is typically achieved at half of the absolute melting point. Fine grained aluminum base material structure and stabilization of that grain boundary structure by the Al3Sc dispersoids is believed to cause this trait, which is highly useful in a manufacturing context. This allows alloy material to be heated and formed under high stress into more complex shapes without creating a narrowing or pinching which would otherwise lead to early fracture.

? Precipitation Hardening –This is somewhat the opposite of the superplasticity characteristic, in that very fine and evenly distributed coherent Al3Sc phases, can give significant hardness increases to the alloy. These phases can be precipitated from a so- called supersaturated Al matrix by moderate heat treatments of 250-350° C. All high performance (aerospace) aluminum alloys which display a strength value higher than 300 MPa (43 ksi) rely on precipitation hardening. This characteristic is particularly useful because the addition of scandium to certain Al-alloys (like 5XXX Al-Mg), that are otherwise not heat treatable, makes them respond to this beneficial annealing technique. Compared to other alloying elements, scandium is the most efficient precipitation hardener for aluminum base materials.Beyond these micro-structure changes that occur when scandium alloys with aluminum, there are two other important and very practical application characteristics that emerge:

? Corrosion Resistance - The addition of scandium to aluminum alloys makes them highly corrosion resistant. Aluminum resists corrosion by rapidly forming a thin oxidized layer which tends to haltfurther degradation, but salty environments can attack and destroy aluminum quickly. Typical aluminum alloying and hardening techniques tend to further reduce corrosion resistance. Scandium’s dramatic positive effect on corrosion resistance, in concert with increasing strength, is highly unusual and useful.

? Weldability - Aluminum is weldable, as are many aluminum alloys, depending on their alloying components, and use of advanced welding technologies. With alloys however, the heat- affected zone at the weld site, particularly the frontier zone of the weld itself, tends to be weaker than the alloy base material---often by 50% or more. Some of this loss in strength can be regained by subsequent heat treatments, depending on the alloy specifics. Certain Al-Sc alloys weld with no appreciable loss in strength. This characteristic is extremely valuable, due to the flow-on effects of lower cost manufacturing options in designing and assembling aluminum alloy parts and

structures. There are several steps to the manufacture of Al-Sc alloys. First, the scandium oxide needs to be procured, which is the most significant problem today. The oxide grade is important but not critical: grades of 95% or better are suitable. Al-Sc master alloy typically has 2% Sc content, considerably above the first eutectic state, so most of the scandium is actually not fully dissolved in its inter-metallic form of Al3Sc, as it is in the final product. The 2% master alloy is then used to precisely dose larger batches of molten aluminum, along with other desired alloying metals, to produce various aluminum alloys. Master

alloy producers are typically smaller specialist companies who market a variety of master alloy products to the major aluminum smelters.

The science of advanced aluminum alloy manufacture is highly technical, and beyond the limits of this discussion. However, a couple more points are important to register, in terms of scandium’s potential to deliver a new, valued, high performance aluminum alloy to market:

A little bit of scandium makes a big difference. It doesn’t take much scandium mixed with

aluminum to generate significant material improvements; as little as 0.10 - 0.15 wt-% Sc has

dramatic effects, but more scandium tends to generate additional benefits, depending on the

alloy processing route selected.

? Higher scandium contents deliver more benefits. Scandium’s natural solubility in aluminum is about 0.4% (known as the first eutectic state), but the introduction of other alloy materials in combination with scandium, along with rapid-solidification techniques (like melt-spinning, powder atomization, and permanent mold casting technologies), can hold considerably higher concentrations of scandium properly in solid solution, enabling additional precipitation hardening by nano-sized Al3Sc dispersoids.

? The technology of raising scandium content in alloys is advancing. The achievable amount of scandium in solid solution depends directly on the rapid solidification technology: the faster the solidification can be made to happen, the more scandium is taken up in the aluminum crystallattice structure. As a general rule, 0.1 wt-% of Sc will provide about 50 MPa (8.5 ksi) of strength gain. Therefore 1.0 wt-% Sc can generate an additional 500 MPa (72.5 ksi) of tensile strength, and theoretically 2.0 wt-% could deliver an incredible 1,000 MPa (145 ksi) improvement. This strength level for an aluminum alloy would match that of a very high strength steel!

? Al-Sc alloys also exhibit much higher heat working tolerances. Scandium raises the working heat range (due to micro structure stability) of aluminum by a factor of two, suggesting Al-Sc alloys could be employed in temperature environments of 350 -400°C, which is appreciably higher than possible with other aluminum alloys.

Ultimately it is these strength improvements that engineers are seeking with the addition of scandium to aluminum alloys. Certain alloys show major strength improvement with solution heat treatment or other forms of hot or cold rolling, while others are not treatable in this manner. It is interesting to note that scandium’s strengthening improvement tends to be much larger (percentage-speaking) in the non-heat treatable alloys. Alloys that respond to strengthening procedures do also show further improvement by scandium additions, but those improvements are somewhat less dramatic.

The four strongest aluminum alloy families today are the 2XXX, 5XXX, 7XXX, and Al-Li configurations, with the 2XXX and 7XXX families used today in commercial aircraft structural components, and the AlCu,Mg-Litype reserved more for military, aerospace and extreme duty applications. The 5XXX group is used in auto and marine products, and is has been certified for certain aircraft applications.

? The 2XXX alloy group is heat-treatable and is mainly alloyed with Cu & Mg. This is a medium strength alloy, with good toughness and a tensile strength ranging from 350 – 500 MPa.

? The 7XXX alloy group is also heat treatable and is mainly alloyed with Zn, Mg & Cu. This is a very high strength alloy with tensile strength up to 700 MPa, but lower toughness (notch strength). Extruded profiles can reach or exceed 800 Mpa.

? Both the 2XXX and 7XXX alloy groups are prone to corrosion and have densities ~2.8 g/cm³ or higher.

? The 5XXX alloy group is not heat treatable, and is mainly alloyed with Mg. This is generally a lower strength alloy, showing a tensile strength of 120 Mpa. Here, the addition of scandium to the alloy mix enables a strong strength push, making the material stronger than the 2XXX alloy, while retaining good corrosion resistance, and showing a lower density of about 2.65 g/cm.

? The Al-Li group does show improvement with scandium additions but they are not particularly significant. Principal research work has been conducted worldwide on aluminum alloys over the last 3 decades, at various laboratory and research institute levels. At the industry level, the EADS Group (Airbus Industries, Eurocopter, ASTRIUM, etc.) in particular is pushing the boundary for Al-Sc alloys, developing new alloy applications for future air transportation requirements and challenges. EADS has patents utilizing rapid solidification methods (melt-spinning or selective laser melting), that can hold scandium in an alloy in

concentrations that exceed 1.0 wt-% Sc. Their Scalmalloy® material concept enables different products (“profiles”) with up to 1.4% scandium content (plus Al-Mg-Zr). These are really ultra-high performance 5XXX alloys, currently achieving tensile strength scores as high as 700 Mpa. Because of the weldability factor, ScalmalloyRP® is also suitable for use in state-of-the-art additive layer manufacturing (ALM) systems. ALM is a new manufacturing technique which generates, or “prints” a 3-D digital CAD model shape, layer by layer, directly into a fully built-up metallic part. This metal application technique offers the ability to produce precise and complex metal shapes with absolute minimum material losses, efficiently minimizing completed part costs with relatively high cost materials.

Form your own opinion s & conclusions above:

IMHO- NIOCORP has gotten all the mine details done & is finally concentrating on formulating Patented AlSc alloys with collaborating partnerships to form a domestic U.S. Supply Chain for Scandium Aluminum moving forward. The NanoScale partnership MAY NOT BE THE ONLY ONE IN PLAY HERE! Nor are they the only Interested entities imho. AS OEM End users may be seeking off-take agreements etc.. for not only Scandium, but Niobium, Titanium & viable Rare Earths. THINK THOOSE BATTERY BOXES, OEMS, FUEL CELLS, DEFENSE, BOEING, AEROSPACE, HYDROGEN.... & more!!!!! OH MY!

Chico

PM/All- Niocorps Carbon Capture methods caught my eye early on! Niocorp could at the very least qualify for some future Tax/Carbon Credits or assistance from the DoE/LPO (Like the video you posted discusses!) Niocorp has stated several times that they are indeed in discussions with "SEVERAL FEDERAL AGENCIES!" Please see a repost of all relevant D.D. & responses from our Niocorp Team!

ON 6/29/2022 - Jim:

1) Could the Elk Creek mine "Separation Process" now under development be utilized as a method for "In situ carbon mineralization/carbon capture"?

RESPONSE:

Not ‘in situ,’ as that implies injecting chemicals underground to perform the desired reaction. The carbonization process we are testing MAY result in some carbon sequestration, depending upon whether and how we end up making more byproducts from the magnesium and calcium we remove from the ore. That is all still TBD.

The reagent recycling tied to the Calcium and Magnesium removal, which we recently announced as part of our demonstration plant operations, is effectively a carbon sink and is expected to reduce the carbon footprint of the eventual operation.

We hold the rights to any intellectual property developed and related to the Elk Creek process by virtue of our contractual relationships with L3 and other entities involved in the work. While our focus remains on using proven commercial technologies in the public domain, we will act to protect the parts of our process that may be novel.

"I think it’s important to keep in mind that while we are segregating and capturing carbon, we are generating carbon emissions in the process of doing so. We take ore that contains iron, magnesium and calcium carbonate and heat it up to about 850 degrees with natural gas. The carbonate minerals break down at this temperature, giving us iron, magnesium and calcium oxides along with CO2 gas. We then leach what comes out of the calciner with ammonium chloride, which selectively removes calcium and magnesium from the calcined solids. We treat the dissolved calcium and magnesium with the off-gas from the calciner, which contains CO2 from the burning of natural gas as well as CO2 from carbonate mineral breakdown. The CO2 reacts with the solution, causing the calcium and magnesium to precipitate as solid calcium and magnesium carbonate and regenerating the ammonium chloride so it can be used again. The carbon sink here is the creation of new calcium and magnesium carbonate, but the overall process is a net generator of CO2 emissions. Because we capture some of the CO2 as calcium and magnesium carbonate, the process generates less CO2 than it otherwise would.

We’ll certainly evaluate the calcium and magnesium carbonate as a potential product, as it comes out of the process pretty clean. However, if we want to claim revenue (especially in a public context), we would have to do two things – (1) find someone who wants to buy it and (2) go through the exercise of adding those two elements to our formal resource and reserve. "

"As noted above, we are generating less CO2 than we would with approaches to these initial process steps that don’t involving recycling CO2 and regenerating the ammonium chloride reagent. However, the fundamental mass balance means that the process will always generate more CO2 than it consumes. It’s an exciting process development, but we need to be cautious here – we would not be able to use the process to capture and segregate someone other entity’s CO2 emissions. The best we could do is make the whole thing carbon neutral, and we could do that if we heated the calciner with electricity generated from wind and solar and made the ammonium chloride recycling step 100% efficient. Unfortunately, neither of these is practical or cost effective. "

There are three groups or ‘SCOPES’ of emissions as defined by the Greenhouse Gas (GHG) Protocol Corporate Standard****A company’s supply chain emissions (included in Scope 3) are on average 5.5 times more than its direct operations (Scope 1 and Scope 2) *****

"We have made an internal estimate of the benefits of our planned products at a Scope 3 emissions level. However, the definition and applicability of Scope 3 emissions must eventually be determined by government regulators, and the SEC is examining many aspects of this issue now. At present and in general, carbon credits are created by mitigation measures taken at the Scope 1 emissions level, although there are several different approaches being examined across the U.S. As to DOE programs, I am not allowed to comment on that at this time.

"Yes. "

"Yes, multiple federal agencies, elected officials in the Congress, and the WH. "

NIOCORP mentioned in article June 1, 2023

The United States Needs a Shift in Perspective on Mining

https://www.csis.org/analysis/united-states-needs-shift-perspective-mining

The energy transition involves more than a move away from high-carbon fuels to low- and zero-carbon fuels. It also entails the fundamental reorganization of the global economy around so-called critical minerals—the metals and other raw materials needed to build electric cars, solar panels, power lines, and other technologies that cut carbon emissions.

At the risk of stating the obvious, mines are needed to produce critical minerals, and right now, United States doesn’t have enough mines meet the demands of the energy transition—not even close.

While the United States also has to work closely with allies to secure the supply chains for these materials, something has to change at home, too.

Like many other U.S. industries, mining was largely outsourced to other parts of the world during the late twentieth century. As a result, global markets for most in-demand minerals are now dominated by the Chinese Communist Party. In fact, of the 50 critical minerals listed by the U.S. government, China is the top producer of 30 of them.

“For most critical minerals, the United States is heavily reliant on foreign sources for its consumption requirements,” a U.S. Geological Survey report said. It further reported that domestic metals production fell 6 percent in 2022.

Simply stated, the United States needs to build new mines and expand existing mines in the United States. Rather than stop digging, the United States needs to start.

To be sure, it will not be easy. Before the passage of landmark environmental laws in the 1970s, including the National Environmental Policy Act and Clean Water Act, the U.S. mining sector was known for polluting practices and indifference to the concerns of neighboring communities. Public anger and distrust proved to be a major factor in the offshoring of U.S. mining after the 1970s. This was understandable, but there were unintended consequences.

An “out of sight, out of mind” approach to metals and other mineral commodities took hold, giving tacit approval to toxic waste dumping, the use of child labor, and other reprehensible mining practices abroad.

Today, there is an opportunity to write a new chapter for the U.S. mining sector, in which the some of the raw materials for advanced energy technologies are produced here, under close scrutiny, subject to the most protective standards in the world and—above all—with strong public support.

The complicated history of mineral extraction in this country must be addressed fully and forthrightly, but it cannot be used as an excuse to keep saying no. At this point there doesn’t seem to be a mine on federal land that is not facing opposition, delays, or rejection.

Fortunately, there are already some promising examples of this new approach to mining in the United States.

A Sense of Patriotism

In southeast Nebraska, for example, the developers of a mine that will produce materials for electric-vehicle batteries have built a strong base of support in the local community. As reported by the New York Times, the mine has secured all the permits it needs to start digging and the developer—Colorado-based NioCorp—is now working with the U.S. Export–Import bank to complete financing for the billion-dollar project.

The planned Elk Creek mine will produce niobium, scandium, titanium, and a series of magnetic rare earth minerals. The global market for these minerals is dominated by other countries, including China, Russia, and Brazil.

These critical minerals can be used to build the components for electric vehicle batteries, fuel cells and wind turbines. But in conservative southeast Nebraska, NioCorp has found ways to connect with people who are less concerned with the energy transition and more worried about economic issues and national security.

The minerals produced at Elk Creek will also be used to make lighter and stronger steel products for the automotive, construction, and oil and natural gas industries, and to build fighter jet engines, among other military applications.

“NioCorp is being very thoughtful in how they’re communicating with Southeast Nebraskans,” Senator Julie Slama (R-NE), who represents the Elk Creek area, said. “In Nebraska, we have a sense of patriotism and desire to serve our country.”

While the proposed mine still has its detractors, the broad-based appeal of the project has helped maintain a sufficient mass of support, also known within industry circles as the “social license to operate.”

MY 2023 F.S. PREDICTION of Average Annual Gross Revenue Before OPEX

(ALL SPECULATION & GUESSING ON MY PART)

Sc2O3 - $355,368,421

Nb - $226,458,000 -(An 8% increase)

The pricing for Titanium Dioxide varies greatly. Given Niocorp only quoted .99 (2022 F.S.) I am using a price point of $200/mt of the quoted pricing below:

800,000,000kg / 2,204kg = 362,976 mt x $200 = $72,595,281

Titanium Concentrate (TiO2≥46%) price historical Data

https://www.metal.com/Titanium/202007280003

Titanium Concentrate(TiO2≥46%) (USD/mt) $288.870 - Jun 01, 2023

What Niocorp intends to produce "TRICKLE" SPONGE GRADE & maybe other grades as well has a price point of @$1,100/mt +/- (Very interesting indeed) 362,976 mt x $1,000 = $362,976,000 Oh my! ....

But I'll Use:

(TiO2≥46%) - $72,595,281

Viable Rare Earths T.B.D.

My guess will produce the following when compared to MP materials & 3 other U.S. projects (& This could be low!) :

600 tons per year Ny/Pr = 600,000kg x $173 = $103,800,000 (not far off Grunt's estimate!)

24 tons per year of Tr = 24,000kg x $2,383 = $57,320,000

120 tons per year of Dy = 120,000kg x $495 = $59,400,000

Total REE annual value prior to OPEX = $220,392,000 Million

~ & I THINK Niocorp's numbers for Dy & Tr might be a touch more! 30mt & 170mt respectively???~

Viable Rare Earths T.B.D. = $220,392,000

Average Annual Gross Revenue

Sc2O3 - $355,368,421 or 41%

Nb - $226,458,000 or 26%

TiO2≥46% - $72,595,281 or 8%

Viable Rare Earths - $220,392,000 or 25%

Total Average Annual Gross Revenue = $874,813,702

IF YOU TAKE AWAY ALL THE SCANDIUM = $519,445,281

IF YOU ONLY PRICE THE SCANDIUM Half Value = $697,129,492

PLUS YOU HAVE BYPRODUCTS CaCO3 & MgCO3 - If you do some D.D. you might do a happy dance as these are not too shabby either & they will have ALOT OF IT! Probably close to TITANIUM Tonnage? (All Speculation & GUESSING ABOVE on my part of course!)

HENCE I STILL STAND BY MY CALL OF Niocorp "Could" now push earnings to $600 to $700Million/year

FORM YOUR OWN OPINIONS & CONCLUSIONS ABOVE:

:format(jpeg):mode_rgb():quality(40)/discogs-images/R-245441-1289401433.jpeg.jpg)

Chico

PM - IMHO NIOCORP has all results from DEMO operations in hand for production at SCALE for (Niobium, Scandium, Titanium & viable REE's, Plus CaCO3 & MgCO3)

All of which will be incorporated into a NEW 2023 F.S. (With all Capex/Opex & Project Economics updated.

I am of the belief with this recent announcement & (responses to Scandium questions posted below) shows Niocorp is well on the way to establishing Several MINE TO OEM & END USER Collaborations. Once The Elk Creek Mine is in full production. (2026/27? pending Finance T.B.D.)

NanoScale Powders, IBC, Jabil, Ames Lab & several others just for Scandium alone.

GIVEN: Just this recent announcement for Scandium. It is very reasonable to believe that the NEW TITANIUM & NIOBIUM Oxide/Chloride Products, REE's & New Byproducts will also be in play and can now all be further developed. OFF-Take agreements, Future Patents, new Materials etc..

Remember the last 25% of NIOBIUM production is still in LIMBO since 2020! TITANIUM is now a true "Sleeper". As quoted pricing from $1 to well over $1,200 /TON is achievable!

The Collaboration with NanoScale could just be the start. In addition to contracts for 75% of the Niobium & 10% of the Scandium already in place.

MAY 26, 2023 NioCorp Launches Phased Approach to Commercial Production of Made-in-America Aluminum-Scandium Master Alloy

https://www.niocorp.com/niocorp-launches-phased-approach-to-commercial-production-of-made-in-america-aluminum-scandium-master-alloy/

NioCorp Partnering with Nanoscale Powders LLC to Explore the Possibility of Establishing the First US-Based Mine-to-Master-Alloy Vertically Integrated Production of the High-Performance Material

NioCorp’s Potential Commercial Production of Al-Sc Master Alloy Could Launch Prior to the Company’s Planned Production of >100 Tonnes/Year of Scandium Oxide at its Proposed Elk Creek Critical Minerals Project in Nebraska and Would Use Scandium Produced at the Elk Creek Facility as well as From Other Sources

China Now Dominates the Scandium World, but North America is Now Positioned to Emerge as a “Leading Scandium Producer,” says NioCorp CEO

Many applications in aerospace, energy, and industrial markets require the production of refractory metals and alloys. Conventional production techniques involve casting ingots of the starting metals, working these ingots to produce the correct form factor of each metal, followed frequently by further steps to shape the final product with significant yield loss. Alloying involves the added complexity of combining via high temperature melting the alloy components, prior to final product shaping and machining. These production techniques are lengthy, capital and energy intensive, and typically operate at low overall yield to final product.

With our patented technology, we offer a direct route to metals and alloys through one-step production of powders with the desired chemical composition, followed by densification of the powder to a finished rough shape. Lead times can be dramatically shortened, batch sizes substantially reduced, energy intensity reduced, and waste from machining minimized.

NANOSCALE POWDERS PATENTS: (They have been working on this track since early 2015!)

https://uspto.report/patent/app/20220008993

1) DATE FILED 2022-01-13 Methods for Producing Metal Powders

U.S. patent application number 17/485596 was filed with the patent office on 2022-01-13 for methods for producing metal powders. The applicant listed for this patent is Nanoscale Powders LLC. Invention is credited to Donald Finnerty, David Henderson, John W. Koenitzer, Andrew Matheson, Richard Van Lieshout.

2) Date of Patent: September 28, 2021 Methods for producing metal powders

BACKGROUND OF THE INVENTION

Metal powders can be used for advanced metallurgical processes, such as near net shape powder pressing, and additive manufacturing, including laser metal deposition (LMD), direct metal laser sintering (DMLS), selective laser sintering (SLS), and selective laser melting (SLM). The end products find applications in a wide variety of industries, including aerospace, medical, and electronics. Other applications include the production of wire bar stock for rolling into medical alloys (e.g., superconducting wires for MRI machines), sputtering targets in electronics manufacturing for thin film metal deposition in displays, use in semiconductors and data storage devices, superalloy production, intermetallic powders for the manufacture of jet engine components, and photovoltaic cells. Metal powders can also be pressed into dense objects using conventional pressing techniques.

Preferably, metal powders are highly pure and have consistent flow properties. However, processes for achieving metal powders having such characteristics require further development. Accordingly, there is a need in the art for methods of making pure metal powders that have adequate flow properties such that the powders can be used for advanced manufacturing applications.

It is a different process that will be utilized.

Yes and yes. But we do not discuss the details of intellectual property matters except as required by law

We are focusing on our partnership with Nanoscale on the production of AlSc master alloy, but we engaged with a number of parties on various elements of our scandium-aluminum master alloy business development. We are not working with IBC on niobium or titanium product development efforts.

The client (whose name is being withheld at its request) is an advanced materials company in the United States. For clarity, this client is unrelated to the global aerospace OEM client for which the Company continues the qualification process to become an approved supplier.

Additionally, this new client has placed a provisional order for a further six tonnes (or 6,000 kilograms), contingent upon the client determining, at its discretion, the appropriate demand for additional powders.

In 2022, one company recovered ilmenite and rutile concentrates from its surface mining operations near Nahunta, GA, and Starke, FL. A second company processed existing mine tailings to recover a mixed heavy-mineral concentrate in California. Based on reported data through September, the estimated value of titanium mineral and synthetic concentrates imported into the United States in 2022 was $780 million. Abrasive sands, monazite, and zircon were coproducts of domestic titanium minerals mining operations. More than 95% of titanium mineral concentrates were consumed by domestic TiO2 pigment producers. The remainder was used in welding-rod coatings and for manufacturing carbides, chemicals, and titanium metal.

1.43 BILLION TONNES ~HUGE! LARGEST U.S. Rare EARTH RESOURCE POTENTIAL June 2, 2023 ~American Rare Earths Reports Positive Metallurgical Test Results~

https://www.investorsobserver.com/news/qm-pr/7786960789984847

PHOENIX, June 02, 2023 (GLOBE NEWSWIRE) -- American Rare Earths ( ASX: ARR | OTCQB: ARRNF | FSE:1BHA ) ( ARR or the Company ) is pleased to report on the latest in a series of metallurgical tests on ore from its Halleck Creek project in Wyoming. With a JORC Resource of 1.43 billion tonnes the Halleck Creek project is potentially the largest rare earth project in the United States. The metallurgy test work continues to pave the way for low-cost processing using conventional technology.

Highlights

The latest test work supports previous results showing a simple process flow sheet to produce a rare earth concentrate and maximize the recovery of magnet metals Neodymium and Praseodymium (NdPr).

Bulk rougher/scavenger (primary) Wet High Intensity Magnetic Separation (WHIMS) produced 72% recovery and rejected 77% of feed mass, an upgrade ratio of 3.1.

Further testing will commence in the coming weeks to generate the final concentrate for refinery testing.

Current internal studies focus on annualized ore processing rates of 10, 15 and 20 million tonnes per annum feed rate to the concentrator to establish optimal project economics.

This equates to a modelled production of 3,800 tonnes, 5,700 tonnes and 7,600 tonnes, respectively of the highly valuable NdPr oxides contained in Mixed Rare Earth Carbonate (MREC) as a saleable product to be processed within the USA.

Recent tests rejected a highly encouraging 77% of waste material in the early processing stages prior to the flotation circuit, demonstrating potential opportunities to reduce the project's operating and capital costs. This is a 5% improvement from preliminary test work results announced in December 2022. These promising results are further enhanced by the low levels of penalty elements thorium and uranium, which remain well below regulatory standards.

CEO and Managing Director, Mr. Chris Gibbs, commented:

“Rare earth projects typically have complex metallurgy. Under the technical leadership of Wood PLC, these outstanding test results provide confidence for a simple process flow sheet. Halleck Creek ore continues to pass all the key tests from a processing perspective: good recovery using conventional processing methods, low radioactive penalty elements and the ability to produce a mixed rare earth concentrate product.”

“In short, Halleck Creek has the right rare earths (NdPr) and low penalty elements. This means a valuable product, simple metallurgy, and lower costs. Most importantly, the project is in the heart of the USA, the largest economy in the world.”

“As an exploration company I’m also excited to advance our exploration activities at Halleck Creek. to support the economic and feasibility studies currently underway.”

“With less than 25% of the area drilled, the deposit remains open at depth and with significant upside potential. To further enhance the project economics, we are keen to test the depth of the deposit, seek to upgrade resources and explore potential higher-grade zones within the project footprint.”

This market announcement has been authorized for release to the market by the Board of American Rare Earths Limited.

Mr. Chris Gibbs

CEO & Managing Director

https://cdn-api.markitdigital.com/apiman-gateway/ASX/asx-research/1.0/file/2924-02649178-2A1440486?access_token=83ff96335c2d45a094df02a206a39ff4

Thanks Nebraskan... ! During the 2020 AGM Scott stated the Hydrological work would take @ 6 months to complete, & shaft freezing If needed would take an additional 5-6 months.

(Could conditions have changed since 2020- "Yes" I am thinking Team Niocorp is on a faster trajectory..... we shall see.) I would like to see them break ground in July/August 2023 for a late 2026 production, But 2024- 2027 Production works too! lol

Power-Lines, Gas Lines & Water as well as long lead time components are all critical path.... Go well with New Roads too...

& Very Telling IF they are announced!

Chico

Hey- how's that Sunrise project going chief?

https://wcsecure.weblink.com.au/pdf/SRL/02636487.pdf

(Looks like they are still waiting for $$$$ too!)

IMHO Niocorp appears to have the 2023 NDA in play here MINE TO PROCESSING TO END USER or MINE to MAGNET, or MINE to METAL in hand & set to come into play as the mine comes into production. (Let's say late 2026/27). I would imagine there are indeed OFFTAKE agreements behind the scenes taking shape. As the NanoScale Deal was but one of several pans in the fire...

NIOCORP RESPONDED TO RECENT SCANDIUM QUESTIONS share on board MAY 29th 2023~

Jim/NIOCORP respond to question on recent Scandium News Release above:

What comes to mind right off the bat is:

A)"How is this Scandium AlSc master Alloy different than what Niocorp produced with IBC & AMES laboratory???"

Response:

It is a different process that will be utilized.

Yes and yes. But we do not discuss the details of intellectual property matters except as required by law

We are focusing on our partnership with Nanoscale on the production of AlSc master alloy, but we engaged with a number of parties on various elements of our scandium-aluminum master alloy business development. We are not working with IBC on niobium or titanium product development efforts.

Appreciated BM! Hydrological work is "Critical Path work! I see FINAL "BoP" Engineering happening now! This is HUGE imho as it does appear & "SIGNAL TO ME" that NIOCORP has all of the DEMO-Information well in hand! (PERHAPS other Entities do as well!??)

IMHO they have proved out that "Improved Flowsheet/ P&ID's" that was shown last year! Costing out the latest newest equipment & components at today's prices to all be incorporated into the 2023 F.S. While incorporating & updating all project economics & Capex/Opex adjustments etc.. (This is ongoing now....)

Nothing like seeing a Power-Block go in BM! =) (Pending Finance of course T.B.D.)

For Consideration I am posting the following for CONTEXT ONLY, AS THINGS MAY HAVE CHANGED!:

"IF" Scott & the Team are still following the 2020 AGM presentation trajectory this Hydromet work may take 6 months to complete. (**** THIS TIMEFRAME COULD HAVE ALL CHANGED!!!****)

(***NOTE: THIS VIDEO NO LONGER EXISTS BUT I HAVE ATTACHED MY DD NOTES!)

"The money may come in tranches; some of them may be bigger & some of them may be smaller. It will likely be some kind of a mix between Debt & Equity.

The first 8-9 months are really an engineering effort. We need to advance detailed engineering to get to the point where we can start constructing things on the ground. "I think the point I want to make here is that… when we think about execution planning. We really are adaptable to the ultimate financing mix & when the financing arrives! So… for instance we might get an initial offering of modest size. We might get the land we need; so instead of getting the land in month five we get it at the beginning!!!

"We would probably prioritize the work we need on permitting & the utilities we need to run the operation. We certainly want to spend some money on advancing the detailed engineering; & we want to keep a little money aside to cover our operating expenses!!! While we pursue subsequent tranches of funding! "

Once The Finance Debt/Equity is locked & EPC Contractors are signed. Hydrology & Shafts are "Critical Path". ~Note the time needed!~)

Scott details the shaft freezing methods to be utilized. Up-Front the "Drilling"-Hydrology, including Geo Tech. work takes approx. 6-7 months & the ground Freezing itself 5-6 months!

My point in all of this is that the geotech work was not done because we are getting ready to revise an FS. It was done because we are getting ready to do final detailed design work on the processing plant.

Grunt! "SPOT ON!" We are all waiting for that 2023 F.S. now with all the updated goodies. Niocorps increased recoveries for Niobium & Titanium plus the improved oxides are phenomenal! (The END-USE APPLICATIONS... "Oh My!")

The pricing for Titanium Dioxide varies greatly. Given Niocorp only quoted .99 (2022 F.S.) I am using the following pricing when I called for $70 Million per year at $100/mt about 1/3 of this quoted pricing below:

Titanium Concentrate(TiO2≥46%) price historical Data

https://www.metal.com/Titanium/202007280003

Titanium Concentrate(TiO2≥46%) (USD/mt) $288.870 - Jun 01, 2023

What Niocorp intends to produce "TRICKLE" SPONGE GRADE & maybe other grades as well has a price point of @$1,100/mt +/- (Very interesting indeed)

Given L3 Already has a PATENTED PROCESS for TITANIUM SEPARATION & UPGRADING (Plus for other Minerals too)

I do NOT know where the final numbers will fall (because we can only SPECULATE out loud!) but I think we are both darn close my friend & the UPSIDE is TREMENDOUS FOR NIOCORPS (NIOBIUM, SCANDIUM, TITANIUM & VIABLE REE's

Given the U.S. Govt. Calls Out ALL OF THE ABOVE in the 2023 NDA (as posted here prior) For Mining to Processing to END-USE here on U.S. soil! & GIVEN what NIOCORPS Critical Minerals Can do...

Waiting with many here...

Chico

NioCorp Completes Geotechnical Drilling Campaign