News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

active long

navycmdr

![]()

active long

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

active long

$Boooom ! over 1 Mil volume 1st 15 mins + $Freddie closing the Gap

now $0.16 from the 20's .... ..

$KBW UPGRADE ! .

Raising our Price Targets $2.00 FNMA $2.50 FMCC ! ..

[/color]KBW upgrade $FNMA $FMCC on election upside pic.twitter.com/ABzafeKm5l

— Retail Investor (@Retail_Investin) February 26, 2024

...

...

...

...

$Freddie closing up on the gap - now $0.16

Pershing Sq. annual slides on Fannie Mae, Freddie Mac

"We do not expect litigation will be the catalyst to end conservatorship"

"Presidential election in Nov 2024 may be a catalyst ... ?

Share price rally since 2022 reflects optimism around a Trump / GOP win"

Pershing Sq. annual slides on Fannie Mae, Freddie Mac

— Librarian Capital (@LibrarianCap) February 25, 2024

"We do not expect litigation will be the catalyst to end conservatorship"

"Presidential election in Nov 2024 may be a catalyst ... Share price rally since 2022 reflects optimism around a Trump / GOP win"$PSH $FNMA $FMCC pic.twitter.com/5BwviNvcI0

$Booom ! $Monday Rally 200,000 shares $Fannie & 300,000 Freddie

The housing market will take off in a 2024 renaissance

as construction, demand are set to surge,

National Association of Home Builders CEO says

The housing market will take off in a 2024 renaissance as construction, demand are set to surge, National Association of Home Builders CEO ... https://t.co/Ks4BizHEIp

— Cmdr Ron Luhmann (@usnavycmdr) February 26, 2024

More of a threshold, or evergreen, question: If Fannie and Freddie have been so profitable for over a decade, why are they in conservatorship?

— David Fiderer (@Ny1david) February 24, 2024

Well 2012-2019 the government acted in bad faith according to a jury to take all their profits for itself. Absent that outright theft, they would have exited long ago — but their guarantee fees were doubled and capital requirements increased too. Making them impenetrable

— Fanniegate Hero (@DoNotLose) February 24, 2024

America's housing affordability crisis makes a comeback

Updated Feb 21, 2024 - Economy

Spiking mortgage rates and high home prices — a dreadful combination that brought America's housing market to a standstill in recent years — is making a comeback after a brief respite.

Why it matters: Financial markets no longer see near-term interest rate cuts after a run of hotter-than-expected inflation data. Those dimmed expectations have consequences for would-be homebuyers waiting for cheaper borrowing costs.

What's new: The average rate for a 30-year mortgage spiked above 7% last week, the Mortgage Bankers Association said Wednesday morning. It was the biggest weekly jump — by almost 0.2% — since last fall.

--- The result is plummeting interest in applying for a new mortgage, with MBA's measure of new applications dropping more than 10% in a week.

--- "Potential homebuyers are quite sensitive to these rate changes, as affordability is strained with both higher rates and higher home values in this supply-constrained market," MBA chief economist Mike Fratantoni said in a statement.

Where it stands: Mortgage rates remain below their most recent peak of 8% seen in October. But they remain well above that seen before the Fed's aggressive rate-hiking cycle took off.

--- This same time in 2022, for instance, mortgage rates hovered around 3%.

The intrigue: America's housing affordability shock is a side effect of the Fed's tightening campaign. After all, higher mortgage rates are one of the most salient ways that Fed moves ripple through the economy.

--- The opposite is the case, too: Signals of possible Fed easing have been reflected in falling mortgage rates, which nudged some would-be homebuyers into the market.

What they're saying: "A lot of my customers are paying close attention to what the Federal Reserve says," Redfin real estate agent Hal Bennett said in a release.

--- "Buyers and sellers came off the sidelines in December when the Fed signaled it would lower interest rates three times in the next year, but now some are getting cold feet because the Fed indicated that rate cuts may come later than expected."

By the numbers: The lack of available supply, partly triggered by stay-in-place owners unwilling to give up low-rate mortgages, means home prices have remained high.

--- The median home sale price climbed 5% from the same time a year ago to $402,343, Redfin said — the biggest annual jump since 2022. (On a monthly basis, prices were little changed, though Redfin cautions that data is not adjusted for seasonality.)

What to watch: Executives at The Home Depot, which has a good pulse of the state of the homebuying market, expect the housing market to coast along this year — with no clear signs of further deterioration or a sharp rebound.

--- "We don't think there's incremental pressure, nor do we think that we're quite ready for a hockey stick recovery," Home Depot CEO Ted Decker told analysts yesterday.

--- One reason: Decker said executives as the retailer have been "talking for some time" about the "Fed's stance for higher for longer."

--- "I think we now we have an appreciation that 'longer' is going to go through the first half of this year," Decker said.

nothing on Judge Lamberth's Calendar today -

jus maybe we get a REPLY to request for "prompt approval " ?

..........

..........

nothing on Judge Lamberth's Calendar today -

jus maybe we get a REPLY to request for "prompt approval " ?

..........

$Freddie $Vol 275,865 is 10X Fannie Vol 27,252 ??

DaJester Re: navycmdr post# 786601

Wednesday, February 21, 2024 4:29:56 PM Post# 786605 of 786605

"a private party’s debts owed to the government do not justify the Government’s taking for public use of more than what is due to it. As the Supreme Court explained, under the Fifth Amendment, “[t]he taxpayer must render unto Caesar what is Caesar’s, but no more.”

That's it in a nutshell. Whatever backstop Treasury provided has been paid, and does NOT necessitate the taking of the future profits for public benefit. Takings are allowed by statute but not without just compensation.

requesting "prompt approval" on 2/12/2024 ...

Greystone Provides $39 Million in Freddie Mac Permanent Financing Towards

New Affordable Housing Development in Tysons Corner, Virginia

265 Units To Be Constructed utilizing 4% Low-Income Tax Credits with Additional

Financing Partners Bank of America , Amazon, Virginia Department of Housing

and Community Development , and Fairfax County Redevelopment and Housing Authority

NEW YORK , Feb. 21, 2024 (GLOBE NEWSWIRE) -- Greystone, a leading national commercial

real estate finance company, has provided $39,000,000 in Freddie Mac Tax-Exempt Loan (TEL)

Unfunded Forward financing towards the construction of 265- units of a 516 unit affordable housing

property in Tysons, Virginia .

The financing was originated by Pharrah Jackson , Vice President at Greystone, on behalf of

non-profit housing developer Arlington Partnership for Affordable Housing (APAH).

Located at 1592 Spring Hill Road within the Washington DC MSA, the multifamily project is a

part of a larger development known as The Exchange at Spring Hill Station and will be the first

100% affordable housing property in Tysons. The completed building will be developed on two

acres and will consist of two, 20-story residential condominiums (Dominion North, the Subject, and

Dominion South) and a community center condominium owned and managed by Fairfax County

Government. Planned residential project amenities also include community rooms, a business center,

landscaped courtyard, resident support services, resident lounge, and laundry facilities.

The unit mix for Dominion North consists of 55 one-bedroom units, 146 two-bedroom units, and

64 three-bedroom units, with 100% of the units at varying affordability restrictions (40 units at

30% area median income (AMI), 77 units at 50% AMI, 87 units at 60% AMI and 61 units at 70% AMI).

In addition, Fairfax County Redevelopment and Housing Authority (FCRHA) has approved and

awarded APAH 40 project-based vouchers for Dominion North. The units are required to be leased

to households at or below 50% AMI. APAH elected to lease those 40 units at 30% of AMI in the

following mix: 9 one- bedrooms, 22 two-bedrooms, and 9 three-bedrooms.

The Freddie Mac Forward commitment financing includes a 48-month construction period with a

17-year permanent loan term. Bank of America, the equity investor for this transaction, will be

providing capital contributions in excess of $ 60 million in tax-credit equity during the course of

the construction timeline. Other debt sources for Dominion North include: Amazon Housing Equity

Fund ( $29,000,000 ); Virginia Housing Trust Fund ( $700,000 ); Virginia Department of Housing

and Community Development (VADHCD) Energy Efficiency (HIEE) ( $2,000,000 ); and FCRHA

Blueprint & Move to Work -- HCV Reserve Loan Funds ( $18,986,897 ).

"The Exchange at Spring Hill Station marks a significant step forward in our commitment to

providing affordable housing options at-scale in an area of incredible opportunity," said APAH

President and CEO Carmen Romero . "Having partners like Greystone is fundamental to securing

the critical financing needed to make a project of this magnitude possible. As a result, the residents

who will call The Exchange home will have access to a vibrant and rapidly growing community full

of opportunity and resources. More than just what you build, and where, but who you build for

is what matters most."

"It's so gratifying to see a 100% affordable development plan come to fruition, and when you realize

how many partners and contributors it takes to make it happen, you really appreciate both the need

and impact of affordable housing in our country," said Ms. Jackson . "We are thrilled to play a role

as the permanent lender with Freddie Mac's Forward TEL program, which has been truly transformative

in the affordable housing construction space. We congratulate all of the parties involved and are looking

forward to the ribbon cutting in 2027."

Fannie Mae held $30.73 billion of MBS as of the end of 2023, up 43.7% from the end of the third quarter. The GSE said the increase in MBS holdings was tied to lender-liquidity activity. https://t.co/k6oQLU5n2Z

— InMortgageFinance (@IMFpubs) February 20, 2024

What could go wrong? https://t.co/vxXOs0TfCe

— Mark Calabria (@MarkCalabria) February 20, 2024

So that’s where @FannieMae and @FreddieMac’s money is ending during your fraudulent conservatorship?

— José E Burgos Lugo, PA (@TheBurgosGrp) February 20, 2024

The corruption on this country is so apparent they’re not even afraid to hide it.

Release the GSEs now!$FNMA $FMCC https://t.co/bEj6Nj1zbv

What could go wrong? https://t.co/vxXOs0TfCe

— Mark Calabria (@MarkCalabria) February 20, 2024

Release, Re-list NYSE, Repay Shareholders ASAP…….!

— d.l. (@outerspace987) February 21, 2024

$FMCC $FNMA "Fannie Mae and Freddie Mac were placed into conservatorship in September 2008. They remain under conservatorship, which Lockhart said there’s no reason for, despite the fact he was the one who made the call years ago." https://t.co/KZtR2aF3wN

— Patrick (@InvestIt3) February 21, 2024

some FREDDIE FOMO takin' effect - but need MORE VOLUME !

just HOW LONG will LAMBERTH DRAG this NEVER ENDING STORY OUT ?

"prompt APPROVAL was REQUESTED 8 DAYS AGO on 2/12/2024

Bruce Berkowitz video - Fannie / Freddie comments begin 1:01 mark

Whalen on GSEs - enjoying a progressive LSD trip c/o Biden

Why? Because NY bank is buying a lot of whole loans. The GSEs @FannieMae and @FreddieMac are enjoying a progressive LSD trip c/o @JoeBiden . Cash window might as well be closed. Don't even ask about release of GSE from @USTreasury

— Richard Christopher Whalen (@rcwhalen) February 20, 2024

Bethany McLean Video - GSEs at the 28min mark !

$Boooom ! _ 80,084 pre-mkt $FNMA HOD = $1.31 _ last $1.27 ...

$Boooom ! _ 80,084 pre-mkt $FNMA HOD = $1.31 _ last $1.27 ...

Strength in home prices helped boost Fannie, Freddie 2023 profits https://t.co/xazEdoMNTf

— Cmdr Ron Luhmann (@usnavycmdr) February 17, 2024

Support, Risk & Stop-loss for Fannie Mae stock

On the downside, the stock finds support just below the level from accumulated volume

at $1.14 and $1.10. There is a natural risk involved when a stock is testing a support level,

since if this is broken, the stock then may fall to the next support level. In this case,

Fannie Mae finds support just below today's level at $1.14. If this is broken, then the next

support from accumulated volume will be at $1.10 and $1.07.

This stock has average movements during the day and with good trading volume, the risk

is considered to be medium. During the last day, the stock moved $0.0450 between high

and low, or 3.60%. For the last week, the stock has had daily average volatility of 5.05%.

Our recommended stop-loss: $1.21 (-4.74%) (This stock has medium daily movements

and this gives medium risk. There is a sell signal from a pivot top found 17 days ago.)

Trading Expectations (FNMA) For The Upcoming Trading Day Of Tuesday 20th

For the upcoming trading day on Tuesday, 20th we expect FNMA to open at $1.27, and

during the day (based on 14 day Average True Range), to move between $1.18 and $1.36,

which gives a possible trading interval of +/-$0.0900 (+/-7.09%) up or down from last

closing price. If Federal National Mortgage Association takes out the full calculated

possible swing range there will be an estimated 14.18% move between the lowest and

the highest trading price during the day.

Since the stock is closer to the resistance from accumulated volume at $1.35 (6.30%)

than the support at $1.14 (10.24%), our systems don't find the trading risk/reward intra-day

attractive and any bets should be held until the stock is closer to the support level.

Support, Risk & Stop-loss for FMCC stock

Federal Home Loan Mortgage Corp finds support from accumulated volume at $1.05

and this level may hold a buying opportunity as an upwards reaction can be expected

when the support is being tested.

This stock has average movements during the day, but be aware of low or falling volume

as this increases the risk. During the last day, the stock moved $0.0400 between high

and low, or 3.81%. For the last week the stock has had daily average volatility of 5.24%.

Our recommended stop-loss: $1.01 (-4.73%) (This stock has medium daily movements

and this gives medium risk. There is a sell signal from a pivot top found 17 days ago.)

Trading Expectations (FMCC) For The Upcoming Trading Day Of Tuesday 20th

For the upcoming trading day on Tuesday, 20th we expect FMCC to open at $1.07, and

during the day (based on 14 day Average True Range), to move between $0.99 and $1.13,

which gives a possible trading interval of +/-$0.0705 (+/-6.65%) up or down from last

closing price. If Federal Home Loan Mortgage Corp takes out the full calculated possible

swing range there will be an estimated 13.30% move between the lowest and the highest

trading price during the day.

Since the stock is closer to the support from accumulated volume at $1.05 (0.94%) than the

resistance at $1.09 (2.83%), our systems sees the trading risk/reward intra-day as attractive

and believe profit can be made before the stock reaches first resistance..

Support, Risk & Stop-loss for FMCC stock

Federal Home Loan Mortgage Corp finds support from accumulated volume at $1.05

and this level may hold a buying opportunity as an upwards reaction can be expected

when the support is being tested.

This stock has average movements during the day, but be aware of low or falling volume

as this increases the risk. During the last day, the stock moved $0.0400 between high

and low, or 3.81%. For the last week the stock has had daily average volatility of 5.24%.

Our recommended stop-loss: $1.01 (-4.73%) (This stock has medium daily movements

and this gives medium risk. There is a sell signal from a pivot top found 17 days ago.)

Trading Expectations (FMCC) For The Upcoming Trading Day Of Tuesday 20th

For the upcoming trading day on Tuesday, 20th we expect FMCC to open at $1.07, and

during the day (based on 14 day Average True Range), to move between $0.99 and $1.13,

which gives a possible trading interval of +/-$0.0705 (+/-6.65%) up or down from last

closing price. If Federal Home Loan Mortgage Corp takes out the full calculated possible

swing range there will be an estimated 13.30% move between the lowest and the highest

trading price during the day.

Since the stock is closer to the support from accumulated volume at $1.05 (0.94%) than the

resistance at $1.09 (2.83%), our systems sees the trading risk/reward intra-day as attractive

and believe profit can be made before the stock reaches first resistance..

Support, Risk & Stop-loss for Fannie Mae stock

On the downside, the stock finds support just below today's level from accumulated volume

at $1.14 and $1.10. There is a natural risk involved when a stock is testing a support level,

since if this is broken, the stock then may fall to the next support level. In this case,

Fannie Mae finds support just below today's level at $1.14. If this is broken, then the next

support from accumulated volume will be at $1.10 and $1.07.

This stock has average movements during the day and with good trading volume, the risk

is considered to be medium. During the last day, the stock moved $0.0450 between high

and low, or 3.60%. For the last week, the stock has had daily average volatility of 5.05%.

Our recommended stop-loss: $1.21 (-4.74%) (This stock has medium daily movements

and this gives medium risk. There is a sell signal from a pivot top found 17 days ago.)

Trading Expectations (FNMA) For The Upcoming Trading Day Of Tuesday 20th

For the upcoming trading day on Tuesday, 20th we expect FNMA to open at $1.27, and

during the day (based on 14 day Average True Range), to move between $1.18 and $1.36,

which gives a possible trading interval of +/-$0.0900 (+/-7.09%) up or down from last

closing price. If Federal National Mortgage Association takes out the full calculated

possible swing range there will be an estimated 14.18% move between the lowest and

the highest trading price during the day.

Since the stock is closer to the resistance from accumulated volume at $1.35 (6.30%)

than the support at $1.14 (10.24%), our systems don't find the trading risk/reward intra-day

attractive and any bets should be held until the stock is closer to the support level.

BAC has 8 Billion shares outstanding

so 4X Fannie+Freddie shares = $120/sh

Number of shares outstanding as of February 2024 : 8,017,100,000.

Bank of America (BAC) - basic shares outstanding

Jarndyce Jarndyce ...

https://t.co/0O0xwj7nuh$FNMAS $FNMA pic.twitter.com/d0RAVjs15k

— Jarndyce Jarndyce (@JarndyceJ) February 17, 2024

Strength in home prices helped boost Fannie, Freddie 2023 profits

With a combined net worth of $125B after earnings this week, the mortgage giants

remain on a path that could lead to eventual release from government conservatorship

if political winds shift

BY MATT CARTER - February 16, 2024

https://www.inman.com/2024/02/16/strength-in-home-prices-helped-boost-fannie-freddie-2023-profits/

Rising interest rates hindered mortgage giants Fannie Mae and Freddie Mac from

growing their portfolios last year, but strength in home prices helped both companies

post double-digit growth in profits and net worth.

At $17.4 billion, Fannie Mae’s net income was up 35 percent from a year ago, while

Freddie Mac boosted net income by 13 percent, to $10.5 billion, the companies

reported this week in quarterly and full-year earnings calls.

“The strength in home prices throughout the year had a direct impact on our earnings,

largely due to the release of credit reserves that reflected higher actual and forecasted

home prices,” Fannie Mae CEO Priscilla Almodovar said on an earnings call Wednesday.

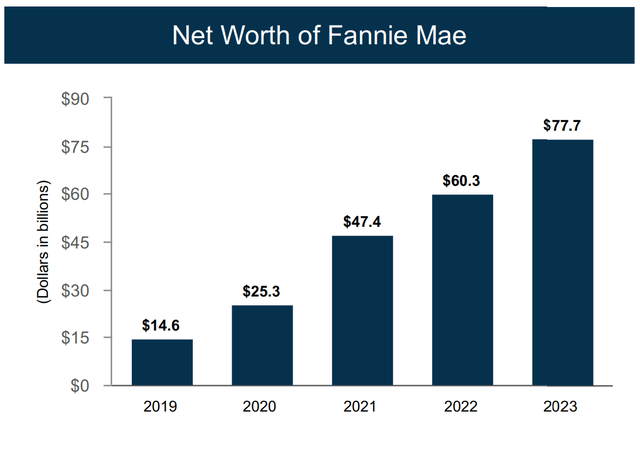

Fannie and Freddie profits, 2018-2023

Source: Fannie Mae and Freddie Mac annual earnings reports.

Freddie Mac Chief Financial Officer Chris Lown also said the company’s growth in 2023 net income was driven primarily by rising home prices, which allowed the company to release $872 million in credit reserves in the single-family business. In 2022, deteriorating housing market conditions prompted the company to boost provisions for losses by $1.8 billion.

The mortgage giants’ bottom lines were also boosted by controversial changes to upfront fees, known as loan level price adjustments (LLPAs), implemented last spring. Fannie and Freddie’s federal regulator, which also eliminated upfront fees for first-time homebuyers of limited means, said the price adjustments were aimed at helping the companies improve their capital positions.

Fannie Mae Chief Financial Officer Chryssa Halley said 2023 revenues were helped by “healthy guaranty fee income” and higher yields on investments.

“While our base guaranty fee income grew slightly in 2023, higher interest rates during the year drove a decline in deferred guaranty fee income due to lower refinance activity,” Halley said. “This was offset by an increase in income due to higher yields on securities in our corporate liquidity portfolio, also driven by the higher interest rate environment.”

Source: Fannie Mae and Freddie Mac annual earnings reports.

Since hitting a pandemic peak of $881 billion in 2021, Fannie Mae and Freddie Mac have seen their new purchase loan business decline for two years in a row in the face of rising mortgage rates, elevated home prices, and for-sale inventory shortages.

Fannie and Freddie's fees going up Monday despite lender objections

Regulator rescinds new Fannie, Freddie fee for riskier borrowers

Priscilla Almodovar

“We continue to modernize the home valuation process by using models and analytics that allow us to offer less costly appraisal waivers and alternatives,” Almodovar said. “Through these options, low- to moderate-income borrowers saved an estimated $52 million in up-front costs in 2023. We’re also giving lenders the option to use an attorney opinion letter instead of a traditional lender’s title insurance policy on some transactions.”

Lown also emphasized that about half of the 800,000 home purchases Freddie Mac financed in 2023 were for first-time homebuyers.

“That is the highest percentage of first-time homebuyers since Freddie Mac started tracking that statistic three decades ago,” Lown said.

Halley said the $316 billion in single-family mortgages Fannie Mae acquired or guaranteed last year represented a 50 percent drop from 2022, and was the lowest volume of new business since 2000.

Advertisement

With higher mortgage rates taking away the incentive for most homeowners to refinance, purchase mortgages represented 86 percent of Fannie Mae’s new business last year, Halley said.

Fannie Mae acquired or guaranteed $273 billion in purchase mortgages, a 28 percent drop from 2022. Freddie Mac’s purchase loan business declined less severely, falling 22 percent to $265 billion.

That helped narrow the gap between Fannie Mae and Freddie Mac’s purchase loan business to just $8 billion, compared to $86 billion in 2020.

Single-family guarantee portfolio hits $6.64 trillion

Source: Fannie Mae and Freddie Mac annual earnings reports.

Advertisement

Together, Fannie Mae and Freddie Mac were guaranteeing payments on $6.64 trillion in single-family mortgages as of Dec. 31, 2023.

At the end of last year, Freddie Mac was guaranteeing payments to investors on a portfolio of $3.04 trillion in single-family mortgages, up 2 percent from the year before.

Fannie Mae’s portfolio of single-family mortgages stayed flat in 2023 at $3.6 trillion, as homeowners in the portfolio paid down their mortgage balances as fast as the mortgage giant added new loans.

While Fannie Mae faced stiff competition from Freddie Mac last year, its single-family mortgage guarantee portfolio exceeds its smaller rival’s by $561 billion. But as recently as 2020, the gap was nearly twice that, at $1 trillion.

Combined net worth hits $125 billion

Source: Fannie Mae and Freddie Mac annual earnings reports.

Advertisement

Fannie and Freddie each grew their net worths by 29 percent in 2023, to a combined total of $125 billion, keeping them on a path that could eventually allow them to be released from government conservatorship if political winds shift.

Fannie Mae grew its net worth to $77.7 billion, up $17.4 billion from a year ago. Freddie Mac added $10.7 billion to its net worth, which totalled $47.7 billion as of Dec. 31.

“This increase bolsters our financial stability and enables us to continue being a reliable source of mortgage credit for America’s homeowners and renters,” Almodovar said.

Nevertheless, Halley said the company remains “significantly undercapitalized,” needing an additional $243 billion to be considered fully capitalized.

Fannie and Freddie were placed into government conservatorship in 2008 as potential losses from the subprime mortgage meltdown threatened to put them out of business. But the move was intended to be a temporary one, and the mortgage giants long ago repaid the $191 billion taxpayer bailout, plus interest.

How much net worth Fannie and Freddie would need to exit conservatorship “is a matter of great debate,” former Freddie Mac CEO Donald Layton wrote last fall in an opinion piece for the NYU Furman Center blog. Under current regulations, Fannie and Freddie would still need about three times as much capital to exit conservatorship, Furman wrote.

Advertisement

But those regulations are controversial, and based on his own research into government-mandated annual stress test results, Layton had previously estimated that Fannie and Freddie could be considered recapitalized when their net worth hits $150 billion — “and the requirement could potentially be even modestly lower.”

If lawmakers could agree on a plan for the mortgage giants to go public again, Layton wrote in September, more capital could be raised by issuing new common equity. While their was talk of privatizing the “GSEs” (government-sponsored enterprises) during the Trump administration, Congress has shown little interest lately.

“It is broadly agreed, as best as I can determine, that there is no appetite in Congress, either at this time or in the foreseeable future, for devoting the considerable time and resources required to attempt full-scale GSE reform,” Furman wrote.

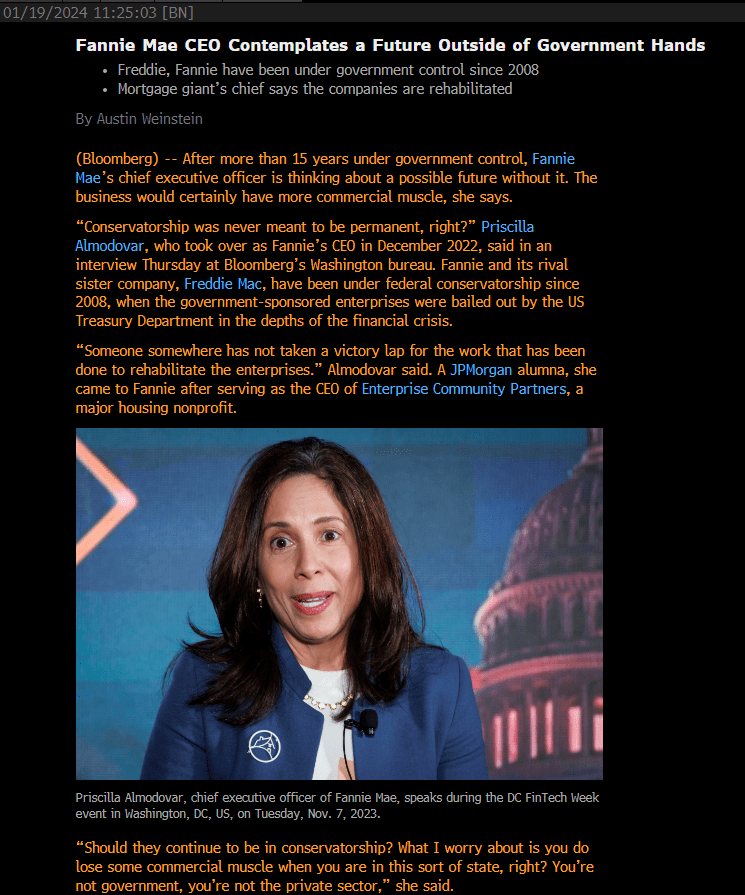

That isn’t stopping Almodovar from planning for an eventual exit from conservatorship, and contemplating how Fannie Mae might benefit, Bloomberg reported last month.

“Conservatorship was never meant to be permanent, right?” Almodovar told Bloomberg.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

a whole pile of wishful thinking not supported by ANY ACTION AT ALL ...

Inflation, Housing Crisis, And GSE Conservatorship: A Path Forward[/color]

Feb. 17, 2024 12:47 AM ET - Glen Bradford

...... Summary .....

--- Rising home prices, inflation concerns, and housing shortages highlight the urgency

for GSE reform, aligning with proposed solutions from Democratic housing experts.

--- White House signals, including statements from key officials like Brian Deese and

Lael Brainard, indicate a growing focus on housing policy, potentially paving the way

for GSE recapitalization and release.

--- Fannie Mae and Freddie Mac remain in conservatorship since 2019, with recent

efforts focused on their responsible exit. Legal battles and political shifts suggest a

potential path toward release.[/color]

Fannie Mae (OTCQB:FNMA) and Freddie Mac (OTCQB:FMCC) are two companies in conservatorship retaining their earnings since September 2019 on their path out of conservatorship. Combined they now have over $125B in net worth which is an all-time record high. Since the companies have begun retaining earnings, the FHFA has been diligently preparing them to responsibly exit conservatorship. Over the years, numerous lawsuits have challenged the government's actions during conservatorship. In August of last year, a jury decided that the government acted in bad faith when arranging the net worth sweep. Since then, prior Democratic White House housing officials have come out separately saying that the conservatorship should end as well as how they would allocate $90B to solve the nation's affordable housing crisis. In fact, the CEO of Fannie Mae came out associating ending the conservatorship with a victory lap.

Investment Thesis

The litigation so far and the pending litigation has not and probably will not result in the legal system forcing the government to release Fannie Mae and Freddie Mac from conservatorship. The Trump administration came up 6 months to a year too short from being able to restructure and effectuate an equity offering. While I believe that it is true that if Trump becomes president again, releasing Fannie and Freddie from conservatorship is a sure thing, I think that the politics are concurrently heating up to drive Biden admin action. Further, I believe the steps the Biden administration has taken to prepare the companies to exit conservatorship points to where things are headed despite the administration not explicitly prioritizing resolving the conservatorships.

For the Biden administration to move forward with recapitalizing and releasing Fannie and Freddie from conservatorship, housing needs to gain steam as a political issue. With there being a housing supply shortage and inflation running high, this sets the stage for a victory lap where the government's equity stake is restructured and the proceeds go to increasing housing supply and thus combating inflation. In any restructuring via recap and release where the government is able to monetize its equity position, junior preferred would be made whole and common would potentially have upside if the government decides to write down their SPSPA liquidation preference or if the equity markets value reformed GSEs with higher than historical valuations. Junior preferred shares currently trade at ~15% of face value.

Fannie Mae FY 2023 Earnings Highlights

The CEO of Fannie Mae Priscilla Almodovar pointed out that the companies have been profitable on a quarterly basis for 24 quarters in a row:

The fourth quarter capped another successful year. Fannie Mae reported $3.9 billion in net income, marking our twenty-fourth consecutive quarter of positive earnings

Since they have been able to retain all their earnings, their net worth has exploded higher since 2019, not bad for a company in conservatorship:

Fannie Mae Net Worth

Fannie Mae has been retaining tens of billions of dollars a year. The earnings press release also points out increasing home prices:

--- Home prices grew 7.1% on a national basis in 2023 according to the Fannie Mae Home Price Index

This factors into higher inflation and affordability as the CEO pointed out:

It was a challenging year for housing, with higher mortgage rates, limited homes for sale, and high home prices weighing on affordability.

Should the Biden administration take action to increase housing supply and decrease mortgage rates through administrative recap and release, more Americans could find their way into home ownership.

Freddie Mac FY 2023 Earnings Highlights

The third bullet point in Freddie Mac's 2023 earnings report summary indicates the continued benefit to Freddie Mac's earnings of rising home prices.

--- Net income of $2.9 billion, an increase of 65% year-over-year, primarily driven by higher net revenues and a credit reserve release in Single-Family in the fourth quarter of 2023 compared to a credit reserve build in Single-Family in the fourth quarter of 2022.

--- Net revenues of $5.4 billion, an increase of 11% year-over-year, driven by higher net interest income and non-interest income.

--- Benefit for credit losses of $0.5 billion, primarily driven by a credit reserve release in Single-Family due to improvements in house prices.

While Freddie Mac and Fannie Mae benefit from rising home prices, home prices are a large factor driving inflation. Thus, it would be a political victory to allocate money to increasing housing supply and all the more reason to believe the Biden admin would at least want to take action. Freddie Mac now has a net worth of $47.7B and has been profitable for many years and should no longer be held in conservatorship.

Fannie Mae CEO: Exiting Conservatorship = A Victory Lap

The CEO of Fannie Mae on January 19 equated the end of conservatorship with a Victory Lap.

Prior FHFA director James Lockhart had previously told Inside Mortgage Finance that this was precisely the sort of public commentary the CEOs should be engaging in:

This was precisely the sort of public commentary that former Federal Housing Finance Agency Director James Lockhart recently told Inside Mortgage Finance the GSEs should be engaging in. He said that, despite the edict against lobbying by the GSEs, as long as they don't ask for specific votes, it's fine for them to educate Congress and the public about issues like the conservatorship.

Prior Democrat Admin Officials

James Parrott and David H Stevens are two prior Democratic leaders of housing finance reform issues.

James Parrott

James Parrott served as a senior advisor at the National Economic Council (NEC) in the Obama White House. He led the team of advisers charged with counseling the cabinet and president on housing issues during one of the most tumultuous times in the history of housing policy, helping them navigate through the collapse of the housing market and the early days of GSE reform. On February 12, he has written with Mark Zandi on how to solve the nation's affordable housing crisis. He estimates that his plan would put millions of families into homes:

Taken together, these moves would trigger a dramatic increase in the supply and affordability of entry-level homes and put millions of families into position to take advantage of it.

He estimates the ultimate cost to be $90B:

This would be an aggressive effort, costing as much as roughly $90 billion over the next decade, according to our budget analysis, depending on how aggressive Congress wants to be.

Note that this $90B cost would seem to be covered by the CBO's estimate of what the government's warrants would be worth $100B. As such, it would seem there is a potential solution here being advocated by influential Democratic housing experts that costs about the same amount that the government would reap from ending the conservatorships.

David H Stevens

David H Stevens was the former assistant secretary of Housing and FHA commissioner under President Obama. In December, he wrote in favor of ending the conservatorships:

HERA explicitly provided guidelines for FHFA to take the GSEs out of conservatorship.

...

But ultimately FHFA has the authority - even a duty - under HERA to take the GSEs out of conservatorship, working with the Treasury which holds its preferred stock.

...

FHFA and the Treasury should release the GSEs from conservatorship as soon as possible.

David H Stevens has been advocating for the end of the conservatorships since the Supreme Court ruled that FHFA is a political agency in June 2021. My last correspondence with him before he passed last month was a message from him, "Well done" with reference to my most recent article that he contributed to. I wish we still had his voice to push this forward. Regardless of personal opinions on his message, he held a unique ability to captivate listeners. Reluctantly, I must acknowledge his prophetic accuracy, making his absence felt even more deeply.

Janet Yellen Hearing Testimony

On February 6, Treasury's Janet Yellen attended a House Financial Services committee where she answered some questions on Fannie and Freddie:

Mr. FitzGerald: When Fannie Mae and Freddie Mac were taken into conservatorship in 2008, Treasury received warrants that give it the right to buy common stock in each of the GSEs equal to 80% of the total outstanding shares and those warrants expire in September 7 of 2028. In August of 2020 the Congressional Budget Office issued a report that estimated Treasury could receive the $190B for its Senior Preferred shares in addition to $110 billion from exercising its warrants in the GSEs. FHFA Director Thompson in the hearing last May said that the two of you have not discussed these warrants. The conservatorship has gone on for -- I think you could agree -- probably too long now. I am concerned that the conservatorship of the GSEs and the warrants could be used to further politicize the entities. Have you or your staff given any consideration to the monetization of Treasury's warrants in the GSEs?

Janet Yellen: This is not a matter that I'm up to speed on. I'm not knowledgeable about this. I have a staff that spends a great deal of time thinking about it but I've not had a discussion with them about this. I would appreciate it if I could get back to you on this matter.

What we can see from this is that there are staff at Treasury who spend a great deal of time thinking about what to do with Treasury's equity stake in Fannie and Freddie. Also, it is my view that Treasury is not in the driver's seat of administrative reform. Direction would come from the White House. Who is to say why Janet Yellen's staff has been spending all this time looking at the valuation of Treasury's equity position. It is hard to imagine it being relevant unless there is interest from the White House.

White House National Economic Council Observations

In my view, there have been indications from within the White House that support the path of the Biden administration moving recap and release.

Prior Biden WH NEC Director Brian Deese

Brian Deese posted on twitter late last year that we need to take action on housing now.

We need more active fiscal policy on housing. We need to incentivize the building of affordable housing. We should do that now, and not admire the problem in 2025/26/27.

To provide context around the gravitas of Brian Deese and James Parrott, they both originally worked on the third amendment net worth sweep.

Bowler testified that prior to finalizing the Third Amendment, "as Treasury Staff negotiated with FHFA staff, the Treasury staff . . . would propose the National Economic Council as to developments and the two people that we proposed would be Brian Deese and Jim Parrott.

It would appear that the two leading White House officials who orchestrated the net worth sweep to keep the companies in conservatorship may be setting the stage for their exit.

WH NEC Director Lael Brainard

Lael Brainard for the first time in the Biden administration publicly addressed housing in December of last year. That's notable in its own right. She spoke about fully utilizing their administrative authorities to address the challenge of housing affordability:

Our first major priority is increasing the supply of affordably priced homes in order to lower housing costs. We are using every lever at our disposal - legislative proposals, our administrative authorities, our convening power, and our bully pulpit - to do so.

But we cannot wait for Congress to act. Through our Housing Supply Action Plan, we are reducing barriers to housing and offering new and improved financing for affordable housing development.

In August, Daniel Hornung was promoted within the NEC as the housing guy. Further, the White House CEA director Jared Bernstein previously wrote about how to structure recap and release:

The key, then, is to a) put private capital in a "first loss" position ahead of the government, and b) set a price for the government insurance that accurately reflects and offsets the expected taxpayer costs of the backstop, something the GSEs decidedly did not do.

The White House definitely has definitely been spending more time on housing the past year. This past week Lael Brainard came out saying that they are still struggling to convince the American public that they are winning the battle against inflation and that

Americans are "fed up" with high prices for everyday purchases such as many food products and housing, and said the Biden administration would seek to push them down

The administration has the political lever through its controlling interest in Fannie and Freddie to increase housing supply and task Fannie and Freddie to buy down mortgage rates to fight inflation and increase affordability.

Recent Legal Developments

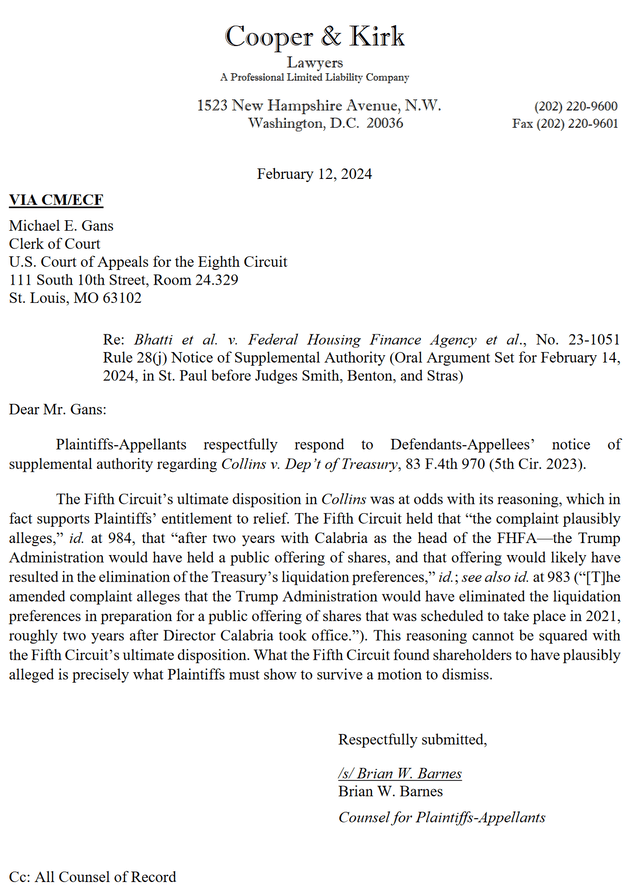

Bhatti v. FHFA had oral arguments February 14 before the Eighth Circuit that you can listen to here. If you are interested in the summary of what is going on there --- they are basically disputing the Collins ruling. There is a letter that summarizes their argument below:

Eighth Circuit Court Letter

So far the legal system has not been impressed with this line of reasoning in the fifth circuit. It will be interesting to see if the Eighth circuit court agrees with plaintiffs.

Timing & Catalysts

Tim Pagliara, an activist shareholder, is optimistic the Biden administration will start politicizing housing affordability and inflation and that this will bring GSE recap and release to the table as an actionable solution and that the State of the Union address by Biden will be revealing:

Bloomberg reports the recapitalization and release of the GSE's as a "Trump" trade. I believe it is the Biden trade. March 7, SOTU is one of the latest ever scheduled. Watch Housing and the shortage of single family homes become a major theme. Biden will call for a recommitment to the American Dream of home ownership. Recap, release, monetization of the warrants will be part of the solution.

Two days before the SOTU address, Super Tuesday will likely determine Trump officially wins the Republican party's nomination. Fannie and Freddie junior preferred shares still trade at a significant discount to his election probabilities. In theory this gap should close or there until there is less money to be arbitraged out of Shorting Trump election odds and going long Fannie and Freddie junior preferred. For those skeptical that Trump would move forward with recap and release he did write a letter saying he would have but he ran out of time:

Trump letter to Rand Paul

In another Trump administration, with 5+ years of retained earnings and FHFA as a political appointee, recap and release in my view is a sure thing. This doesn't even take into account that Fannie Mae is expected to hit statutory minimum capital on a preferred stock adjusted basis in the next year and a half. How do you keep a company like that in conservatorship?

Treasury FY 2023 Budget

The government published its updated FY 2023 valuation of its senior preferred stock in both companies on February 15:

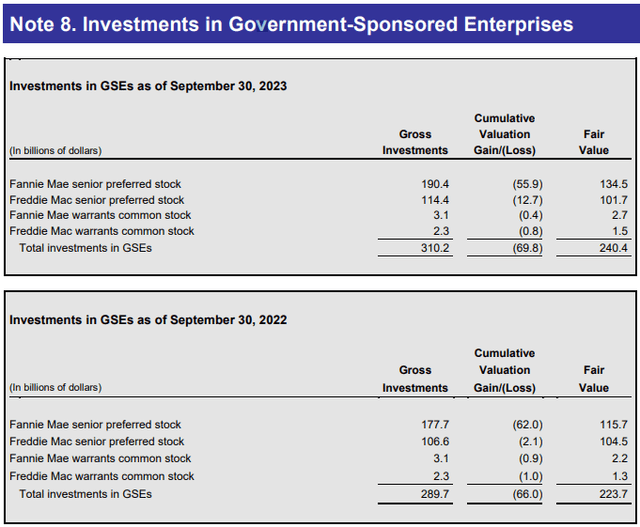

The government increased the FV of its senior preferred stock due to higher projected cash flows:

The FV of the senior preferred stock-as measured by unobservable and observable inputs-increased as of September 30, 2023, when compared to September 30, 2022. Fannie Mae's senior preferred stock drove this increase primarily due to higher projected cash flows and a decrease in credit-related expenses.

The Treasury report continues:

To date, Congress has not passed legislation nor has FHFA taken action to end the GSEs' conservatorships.

It looks like Treasury is blaming FHFA as the party responsible for needing to take action while FHFA is saying it needs someone at Treasury to help restructure the SPSPA agreement. Seeing as how both federal agencies are controlled by the White House, this seems more like a pending policy decision while both federal agencies wait for the green light.

Summary & Conclusion

Administrative action with respect to Fannie Mae and Freddie Mac has been a long time coming ever since Mark Calabria worked with Steven Mnuchin to begin the retention of earnings in 2019. Inflation is a real problem with rising home prices and this also exacerbates the affordable housing crisis:

One of the most important issues in the President's economic agenda - lowering costs and increasing access to housing for Americans.

...

Our first major priority is increasing the supply of affordably priced homes in order to lower housing costs.

It would seem to me that they should want to monetize their equity position to solve the funding problem. Treasury staff seem to be actively engaged in valuing Treasury's equity position. The companies may have $125B of net worth (All-time record high), but the government still has not officially let them go and raise capital and exit conservatorship. When they do, shareholders stand to benefit and the CBO report suggests junior preferred specifically can expect face value. The only step left to really kickstarting administrative action is raising awareness. Here's to helping make affordable housing and fighting inflation more visible political priorities so that the government can take the victory lap.

a whole pile of wishful thinking not supported by ANY ACTION AT ALL ...

Inflation, Housing Crisis, And GSE Conservatorship: A Path Forward[/color]

Feb. 17, 2024 12:47 AM ET - Glen Bradford

...... Summary .....

--- Rising home prices, inflation concerns, and housing shortages highlight the urgency

for GSE reform, aligning with proposed solutions from Democratic housing experts.

--- White House signals, including statements from key officials like Brian Deese and

Lael Brainard, indicate a growing focus on housing policy, potentially paving the way

for GSE recapitalization and release.

--- Fannie Mae and Freddie Mac remain in conservatorship since 2019, with recent

efforts focused on their responsible exit. Legal battles and political shifts suggest a

potential path toward release.

Fannie Mae (OTCQB:FNMA) and Freddie Mac (OTCQB:FMCC) are two companies in conservatorship retaining their earnings since September 2019 on their path out of conservatorship. Combined they now have over $125B in net worth which is an all-time record high. Since the companies have begun retaining earnings, the FHFA has been diligently preparing them to responsibly exit conservatorship. Over the years, numerous lawsuits have challenged the government's actions during conservatorship. In August of last year, a jury decided that the government acted in bad faith when arranging the net worth sweep. Since then, prior Democratic White House housing officials have come out separately saying that the conservatorship should end as well as how they would allocate $90B to solve the nation's affordable housing crisis. In fact, the CEO of Fannie Mae came out associating ending the conservatorship with a victory lap.

Investment Thesis

The litigation so far and the pending litigation has not and probably will not result in the legal system forcing the government to release Fannie Mae and Freddie Mac from conservatorship. The Trump administration came up 6 months to a year too short from being able to restructure and effectuate an equity offering. While I believe that it is true that if Trump becomes president again, releasing Fannie and Freddie from conservatorship is a sure thing, I think that the politics are concurrently heating up to drive Biden admin action. Further, I believe the steps the Biden administration has taken to prepare the companies to exit conservatorship points to where things are headed despite the administration not explicitly prioritizing resolving the conservatorships.

For the Biden administration to move forward with recapitalizing and releasing Fannie and Freddie from conservatorship, housing needs to gain steam as a political issue. With there being a housing supply shortage and inflation running high, this sets the stage for a victory lap where the government's equity stake is restructured and the proceeds go to increasing housing supply and thus combating inflation. In any restructuring via recap and release where the government is able to monetize its equity position, junior preferred would be made whole and common would potentially have upside if the government decides to write down their SPSPA liquidation preference or if the equity markets value reformed GSEs with higher than historical valuations. Junior preferred shares currently trade at ~15% of face value.

Fannie Mae FY 2023 Earnings Highlights

The CEO of Fannie Mae Priscilla Almodovar pointed out that the companies have been profitable on a quarterly basis for 24 quarters in a row:

The fourth quarter capped another successful year. Fannie Mae reported $3.9 billion in net income, marking our twenty-fourth consecutive quarter of positive earnings

Since they have been able to retain all their earnings, their net worth has exploded higher since 2019, not bad for a company in conservatorship:

Fannie Mae Net Worth

Fannie Mae has been retaining tens of billions of dollars a year. The earnings press release also points out increasing home prices:

--- Home prices grew 7.1% on a national basis in 2023 according to the Fannie Mae Home Price Index

This factors into higher inflation and affordability as the CEO pointed out:

It was a challenging year for housing, with higher mortgage rates, limited homes for sale, and high home prices weighing on affordability.

Should the Biden administration take action to increase housing supply and decrease mortgage rates through administrative recap and release, more Americans could find their way into home ownership.

Freddie Mac FY 2023 Earnings Highlights

The third bullet point in Freddie Mac's 2023 earnings report summary indicates the continued benefit to Freddie Mac's earnings of rising home prices.

--- Net income of $2.9 billion, an increase of 65% year-over-year, primarily driven by higher net revenues and a credit reserve release in Single-Family in the fourth quarter of 2023 compared to a credit reserve build in Single-Family in the fourth quarter of 2022.

--- Net revenues of $5.4 billion, an increase of 11% year-over-year, driven by higher net interest income and non-interest income.

--- Benefit for credit losses of $0.5 billion, primarily driven by a credit reserve release in Single-Family due to improvements in house prices.

While Freddie Mac and Fannie Mae benefit from rising home prices, home prices are a large factor driving inflation. Thus, it would be a political victory to allocate money to increasing housing supply and all the more reason to believe the Biden admin would at least want to take action. Freddie Mac now has a net worth of $47.7B and has been profitable for many years and should no longer be held in conservatorship.

Fannie Mae CEO: Exiting Conservatorship = A Victory Lap

The CEO of Fannie Mae on January 19 equated the end of conservatorship with a Victory Lap.

Prior FHFA director James Lockhart had previously told Inside Mortgage Finance that this was precisely the sort of public commentary the CEOs should be engaging in:

This was precisely the sort of public commentary that former Federal Housing Finance Agency Director James Lockhart recently told Inside Mortgage Finance the GSEs should be engaging in. He said that, despite the edict against lobbying by the GSEs, as long as they don't ask for specific votes, it's fine for them to educate Congress and the public about issues like the conservatorship.

Prior Democrat Admin Officials

James Parrott and David H Stevens are two prior Democratic leaders of housing finance reform issues.

James Parrott

James Parrott served as a senior advisor at the National Economic Council (NEC) in the Obama White House. He led the team of advisers charged with counseling the cabinet and president on housing issues during one of the most tumultuous times in the history of housing policy, helping them navigate through the collapse of the housing market and the early days of GSE reform. On February 12, he has written with Mark Zandi on how to solve the nation's affordable housing crisis. He estimates that his plan would put millions of families into homes:

Taken together, these moves would trigger a dramatic increase in the supply and affordability of entry-level homes and put millions of families into position to take advantage of it.

He estimates the ultimate cost to be $90B:

This would be an aggressive effort, costing as much as roughly $90 billion over the next decade, according to our budget analysis, depending on how aggressive Congress wants to be.

Note that this $90B cost would seem to be covered by the CBO's estimate of what the government's warrants would be worth $100B. As such, it would seem there is a potential solution here being advocated by influential Democratic housing experts that costs about the same amount that the government would reap from ending the conservatorships.

David H Stevens

David H Stevens was the former assistant secretary of Housing and FHA commissioner under President Obama. In December, he wrote in favor of ending the conservatorships:

HERA explicitly provided guidelines for FHFA to take the GSEs out of conservatorship.

...

But ultimately FHFA has the authority - even a duty - under HERA to take the GSEs out of conservatorship, working with the Treasury which holds its preferred stock.

...

FHFA and the Treasury should release the GSEs from conservatorship as soon as possible.

David H Stevens has been advocating for the end of the conservatorships since the Supreme Court ruled that FHFA is a political agency in June 2021. My last correspondence with him before he passed last month was a message from him, "Well done" with reference to my most recent article that he contributed to. I wish we still had his voice to push this forward. Regardless of personal opinions on his message, he held a unique ability to captivate listeners. Reluctantly, I must acknowledge his prophetic accuracy, making his absence felt even more deeply.

Janet Yellen Hearing Testimony

On February 6, Treasury's Janet Yellen attended a House Financial Services committee where she answered some questions on Fannie and Freddie:

Mr. FitzGerald: When Fannie Mae and Freddie Mac were taken into conservatorship in 2008, Treasury received warrants that give it the right to buy common stock in each of the GSEs equal to 80% of the total outstanding shares and those warrants expire in September 7 of 2028. In August of 2020 the Congressional Budget Office issued a report that estimated Treasury could receive the $190B for its Senior Preferred shares in addition to $110 billion from exercising its warrants in the GSEs. FHFA Director Thompson in the hearing last May said that the two of you have not discussed these warrants. The conservatorship has gone on for -- I think you could agree -- probably too long now. I am concerned that the conservatorship of the GSEs and the warrants could be used to further politicize the entities. Have you or your staff given any consideration to the monetization of Treasury's warrants in the GSEs?

Janet Yellen: This is not a matter that I'm up to speed on. I'm not knowledgeable about this. I have a staff that spends a great deal of time thinking about it but I've not had a discussion with them about this. I would appreciate it if I could get back to you on this matter.

What we can see from this is that there are staff at Treasury who spend a great deal of time thinking about what to do with Treasury's equity stake in Fannie and Freddie. Also, it is my view that Treasury is not in the driver's seat of administrative reform. Direction would come from the White House. Who is to say why Janet Yellen's staff has been spending all this time looking at the valuation of Treasury's equity position. It is hard to imagine it being relevant unless there is interest from the White House.

White House National Economic Council Observations

In my view, there have been indications from within the White House that support the path of the Biden administration moving recap and release.

Prior Biden WH NEC Director Brian Deese

Brian Deese posted on twitter late last year that we need to take action on housing now.

We need more active fiscal policy on housing. We need to incentivize the building of affordable housing. We should do that now, and not admire the problem in 2025/26/27.

To provide context around the gravitas of Brian Deese and James Parrott, they both originally worked on the third amendment net worth sweep.

Bowler testified that prior to finalizing the Third Amendment, "as Treasury Staff negotiated with FHFA staff, the Treasury staff . . . would propose the National Economic Council as to developments and the two people that we proposed would be Brian Deese and Jim Parrott.

It would appear that the two leading White House officials who orchestrated the net worth sweep to keep the companies in conservatorship may be setting the stage for their exit.

WH NEC Director Lael Brainard

Lael Brainard for the first time in the Biden administration publicly addressed housing in December of last year. That's notable in its own right. She spoke about fully utilizing their administrative authorities to address the challenge of housing affordability:

Our first major priority is increasing the supply of affordably priced homes in order to lower housing costs. We are using every lever at our disposal - legislative proposals, our administrative authorities, our convening power, and our bully pulpit - to do so.

But we cannot wait for Congress to act. Through our Housing Supply Action Plan, we are reducing barriers to housing and offering new and improved financing for affordable housing development.

In August, Daniel Hornung was promoted within the NEC as the housing guy. Further, the White House CEA director Jared Bernstein previously wrote about how to structure recap and release:

The key, then, is to a) put private capital in a "first loss" position ahead of the government, and b) set a price for the government insurance that accurately reflects and offsets the expected taxpayer costs of the backstop, something the GSEs decidedly did not do.

The White House definitely has definitely been spending more time on housing the past year. This past week Lael Brainard came out saying that they are still struggling to convince the American public that they are winning the battle against inflation and that

Americans are "fed up" with high prices for everyday purchases such as many food products and housing, and said the Biden administration would seek to push them down

The administration has the political lever through its controlling interest in Fannie and Freddie to increase housing supply and task Fannie and Freddie to buy down mortgage rates to fight inflation and increase affordability.

Recent Legal Developments

Bhatti v. FHFA had oral arguments February 14 before the Eighth Circuit that you can listen to here. If you are interested in the summary of what is going on there --- they are basically disputing the Collins ruling. There is a letter that summarizes their argument below:

Eighth Circuit Court Letter

So far the legal system has not been impressed with this line of reasoning in the fifth circuit. It will be interesting to see if the Eighth circuit court agrees with plaintiffs.

Timing & Catalysts

Tim Pagliara, an activist shareholder, is optimistic the Biden administration will start politicizing housing affordability and inflation and that this will bring GSE recap and release to the table as an actionable solution and that the State of the Union address by Biden will be revealing:

Bloomberg reports the recapitalization and release of the GSE's as a "Trump" trade. I believe it is the Biden trade. March 7, SOTU is one of the latest ever scheduled. Watch Housing and the shortage of single family homes become a major theme. Biden will call for a recommitment to the American Dream of home ownership. Recap, release, monetization of the warrants will be part of the solution.

Two days before the SOTU address, Super Tuesday will likely determine Trump officially wins the Republican party's nomination. Fannie and Freddie junior preferred shares still trade at a significant discount to his election probabilities. In theory this gap should close or there until there is less money to be arbitraged out of Shorting Trump election odds and going long Fannie and Freddie junior preferred. For those skeptical that Trump would move forward with recap and release he did write a letter saying he would have but he ran out of time:

Trump letter to Rand Paul

In another Trump administration, with 5+ years of retained earnings and FHFA as a political appointee, recap and release in my view is a sure thing. This doesn't even take into account that Fannie Mae is expected to hit statutory minimum capital on a preferred stock adjusted basis in the next year and a half. How do you keep a company like that in conservatorship?

Treasury FY 2023 Budget

The government published its updated FY 2023 valuation of its senior preferred stock in both companies on February 15:

The government increased the FV of its senior preferred stock due to higher projected cash flows:

The FV of the senior preferred stock-as measured by unobservable and observable inputs-increased as of September 30, 2023, when compared to September 30, 2022. Fannie Mae's senior preferred stock drove this increase primarily due to higher projected cash flows and a decrease in credit-related expenses.

The Treasury report continues:

To date, Congress has not passed legislation nor has FHFA taken action to end the GSEs' conservatorships.

It looks like Treasury is blaming FHFA as the party responsible for needing to take action while FHFA is saying it needs someone at Treasury to help restructure the SPSPA agreement. Seeing as how both federal agencies are controlled by the White House, this seems more like a pending policy decision while both federal agencies wait for the green light.

Summary & Conclusion

Administrative action with respect to Fannie Mae and Freddie Mac has been a long time coming ever since Mark Calabria worked with Steven Mnuchin to begin the retention of earnings in 2019. Inflation is a real problem with rising home prices and this also exacerbates the affordable housing crisis:

One of the most important issues in the President's economic agenda - lowering costs and increasing access to housing for Americans.

...

Our first major priority is increasing the supply of affordably priced homes in order to lower housing costs.

It would seem to me that they should want to monetize their equity position to solve the funding problem. Treasury staff seem to be actively engaged in valuing Treasury's equity position. The companies may have $125B of net worth (All-time record high), but the government still has not officially let them go and raise capital and exit conservatorship. When they do, shareholders stand to benefit and the CBO report suggests junior preferred specifically can expect face value. The only step left to really kickstarting administrative action is raising awareness. Here's to helping make affordable housing and fighting inflation more visible political priorities so that the government can take the victory lap.

Freddie Mac 150 & 300 share ... pre-mkt Form T MM rip off @ $1.13

It seems filing is about Exbit A

https://storage.courtlistener.com/recap/gov.uscourts.dcd.163155/gov.uscourts.dcd.163155.417.1.pdf

Boooom ! Something Filed Today on Pacer !

https://www.courtlistener.com/docket/4212341/in-re-fannie-maefreddie-mac-senior-preferred-stock-purchase-agreement/?order_by=desc

https://www.courtlistener.com/docket/4212077/fairholme-funds-inc-v-federal-housing-finance-agency/?order_by=desc

267,000 on FMCC BID before the close

$FNMA $FMCC 👇👇👇👇👇 pic.twitter.com/uglAi4RF21

— Patrick (@InvestIt3) February 15, 2024

now 267,407 Shares on the Freddie Bid !! -