News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

SFSecurity

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Hi Toofuzzy,

If you use AIM, you do not need to concern yourself with predicting market direction and stuff like this.

Thanks Is7550! Got Newport working now all I need to do is figure out how to use it.  (Is there a list of acceptable emoticons? I've tried a couple that didn't work?)

(Is there a list of acceptable emoticons? I've tried a couple that didn't work?)

Is there any way to run each stock position separately or, alternatively, run multiple instances of Newport like I do for Netstock? I need to keep at least four accounts separate - my own, my IRA, and two trust accounts. Or am I better off handling that part via the spreadsheet using separate tabs?

Another sort of crazy question, how do you change the % cash and the initial Portfolio Control (PC)? Since I am migrating already held positions into AIM, the cash element has no relationship to reality and I want to use a single cash pool for all positions.

As to PC, I recall one post that said a PC of 54-58% gave better results and I'd like to see if that is true for me. I guess I could try this using the spreadsheet, but I hesitate to do that because I'm not quite sure exactly how to do this. Some of the formulas are a bit opaque to me and I'm not quite sure which one to fiddle with. Clues for either approach?

Warmest Regards,

Allen

Hi Bowler Bob,

With your bad knees and my bad feet we make a great pair to go dancing. What shall it be? Square dance, ballet or just plain old Charlie Chaplin prat falls?

ROTFLMGO!

Allen

Like backtesting? Beat this!

October 21st, 2014 by Meb Faber

(snip) We’ve done testing going back 100 years or so (so has AQR in their paper) and I was delighted to see a new book out by the crew at ISAM (up a whopping 28% this year) that has a 800 year backtest! Looking forward to reading it.

Most Excellent, Is7550, but where can I get a legit copy of Newport? I have a couple of machines that I can run Puppy Linux on. I haven't run it or Damn Small Linux in a while but it would not be all that hard to get up to speed again. I also run NetBSD and OpenBSD. Alas, I can't move to them completely yet. Quite possibly it could run on one of those as well.

BTW, your comments on mid-caps for the most part matches the AAII portfolio. Price to book ratio <0.8, market capitalization between $30 and $300 million, positive earnings and several more criteria. Since 1993 17.8%/year versus Vanguard 500 Index (VFINX) at 9.3% and Vanguard Small Cap Index (NAESX) of 10.6%. The dollar amounts (starting at $10K) are $345,501, $69,156 and $88,063. I think these figures prove your point.

Warmest Regards,

Allen

On another note entirely, I was reading my American Association of Individual Investor's (AAII) mag last night and saw an interesting comment by James Cloonan (AAII founder) where he mentions a weird cycle that goes back over 100 years that years that end in 5 do better than average and that the 3rd year in a presidential term is also better than average.

"The Mystery Cycle

The election cycle indicates an above average return in the prior to the U.S. national election, this has been widely discussed and will be in the

news as we approach 2015. Twenty years ago, I came across another cycle for which I can find no rationale but that has been pervasive for the last 100 years. It is the positive impact on the market of years ending in 5. This cycle is particularly important in years when it coincides

with the election cycle. This combination occurs only every 20 years, and the year 2015 is one of those years. I have always been suspicious of data

like this that indicates a possible anomaly when I can’t find a rationale for the behavior. In the election cycle we have the rationale that government spending and talk of government spending prior to the election boosts expectations, but I cannot think of any cycle for years ending

in 5, or any 10 year cycle, to explain this rather dramatic impact. While it could be coincidence, it is also possible that I simply can’t find the explanation. Note that although the data covers a large number of years, the actual sample size is small.

I must admit that in 1995, I was extra bullish and was rewarded. I will be a little extra bullish in 2015, although I hesitate to suggest that anyone else should do the same. But here are the numbers.

Average annual returns since 1935:

11.0% = S&P 500 index

20.7% = year 3 of the election cycle

28.4% = years ending in 5

42.4% = year 3 + years ending in 5

0 = number of times year 3 was negative

Just an observation."

Also, look at http://www.seasonalcharts.com/zyklen_wahl_dowjones4j.html - Dow Jones Election Cycle, 4 Year Period 1897-2011 - and note that this year is roughly no real gain as it is the third year in the election cycle.

An appropriate bit of weirdness for Guy Fawkes Day.

Warmest Regards,

Allen

P.S. Bowler Bob (I can imagine you doing a soft shoe dance with cane and a bowler hat sort of like a cross between Charlie Chaplin and Gene Kelly) I just ordered "The Ivory Portfolio" fro Alibris.

Thanks Bowler Bob. I'm sure you did post this most useful link, I can only say, in mitigation, is it got lost in my notes. Sometimes I note something as I'm on my way somewhere else and it gets lost in the shuffle. Sorry.

Warmest Regards

Allen

Hi Tom, Thanks for the link. Maybe I should stop complaining/worrying about my current positions as I'm getting a bit over 11% return in dividends. There are a couple that I think I should shed as they are small positions and lower rate of return, but not all that much as a $ %age of the total package.

Going back to your very helpful post about a pyramid with a solid base, this is where I think I am deficient. This is tough because I don't love anything in particular to the point of wanting to hold it long term.

It seems that there is almost always something fundamental that concerns me. For example, take Apple.

A long time ago I was building a special desk to do a variety of things on and was using a solid core door for the top. Since I was going to use a sewing machine on occasion on it I was concerned about vibration. I called my dad, a civil engineer, and asked him about using a 1 3/8" inch door. His response was to use the 1 3/4" door because it would be a bit over 4 times as resistant to vibration. The iPhone has used Gorilla Glass with a thickness of 0.020" thick and they break rather easily, as I know from my daughter's experience. Why don't they use 0.025" thick glass, or even wildly more, say 0.040"? This would be about 30 times stronger but then there wouldn't be as many iPhones that need repair or replacing. Do I want to hold a position in a company (or an ETF with a position in Apple) that has shown so little concern for its consumers?

Another example is Nestle. Just think a bit about two things they are known for, resisting any effort to reduce sugar consumption to help with the current obesity problem among US kids, the other being the push in the developing world to substitute formula for breast feeding and creating a generation with reduced immunity. Again, do I want to hold a position in a company that is not very concerned about the health of its consumers.

Then there is Union Carbide (now wholly owned by Dow Chemical) and Bhopal and the lack of cleaning up after itself. Accidents will happen, no question, but most of us clean up after ourselves.

I could go on and on but I'll spare you.

Acccck!!! What should I do, hold my nose, avert my eyes and ignore the the failings of most large businesses when it comes to being good citizens?

I know that it is not possible to live totally isolated from the world around me, no more than a fish can avoid the water it swims in. I just don't like swimming in a sewer.

Warmest Regards,

Allen

Thanks Tom, most illuminating and helpful. I had not thought of it in terms of a (food) pyramid.

Warmest Regards,

Allen

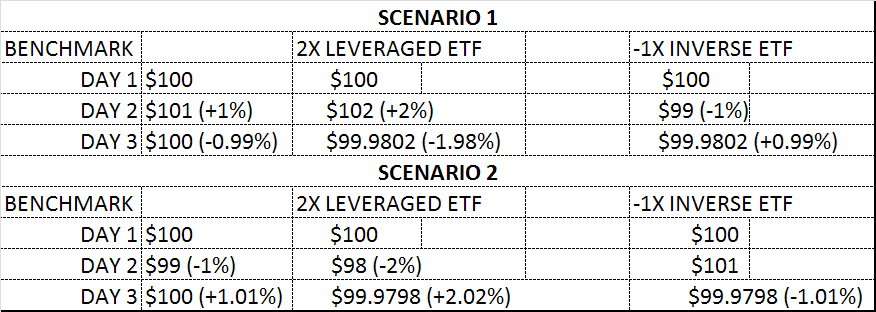

Hi Gang, Here is the best explanation of leveraged and inverse ETFs and how they work I've seen. In a way it confirms my concern about leveraged ETFs as a series of whipsaws can lose you a pot of money.

Thomas Preston

EDITOR’S NOTE: This article first appeared in the Spring 2014 issue of thinkMoney. (TDAmeritrade's house mag.)

Inverse and leveraged ETFs have become some of the most actively traded financial products. And why not? These instruments can offer opportunities to take interesting positions. For example, an ETF that tracks the Russell 2000 moves three times the amount of the underlying index. Another, a leveraged inverse ETF that tracks the Standard & Poor’s 500 index, moves inversely from the U.S. equity benchmark by a factor of two. Because it goes up when the S&P 500 goes down, it can be a way to hold a bearish position where you’d otherwise be prohibited from shorting stock. Still, you can get tripped up if you don’t understand how these work.

Less Than Zero?

Stocks, bonds, indexes, and ETFs can’t have negative prices. So, imagine an inverse ETF whose price moves in the opposite direction point for point from its benchmark price—when the benchmark moves up one point, the inverse ETF moves down one point. But what happens if the index moves up more points than the inverse ETF is worth? For example, if the benchmark is $50 and the inverse ETF is $50, the inverse ETF would have a negative value if the benchmark moved up 51 points to $101. This is also a consideration with leveraged ETFs.

The creators of inverse and leveraged ETFs solved this problem by basing the price change for the inverse and leveraged ETFs on the daily percentage change of the benchmark. If the benchmark moves up 1% in one day, the inverse ETF moves down the same amount. But what happens if the benchmark keeps going up, day after day? The inverse ETF keeps moving down in price, but never below $0. That’s because when inverse ETF’s price is lower, the percent change equates to a smaller change in points.

For example, say a benchmark is at $100 and the 1x inverse ETF is $100. If the price of the benchmark moves up $2 to $102 in a day, that’s 2%, meaning the ETF moves down 2% of $100, to $98. If the benchmark on the following day moves up another 2% ($2.04, to $104.04), the ETF moves down 2% of $98 ($1.96, to $96.04). The inverse ETF had a smaller price change on the second 2% drop than it did on the first because its starting price was lower. Thus, the inverse ETF can never go below $0. Very clever—but that also creates another problem.

The leveraged, inverse ETFs track the daily percentage price change of the benchmark. Those ETFs can sometimes move in ways that are counterintuitive because the prices of the leveraged and inverse are path-dependent. If the benchmark moves up $1 today and down $1 tomorrow, that has a different impact on the ETF than down $1 today and up $1 tomorrow. Huh?

Connective Financial Tissue

Let’s look at two scenarios for a leveraged ETF that moves 2x the percent change of the benchmark, and an inverse ETF that moves –1x the percent change of the benchmark. Let’s assume that the benchmark and the leveraged or inverse ETFs each start at $100.

In Scenario 1, the benchmark starts at $100 and moves up 1% on day 2 to $101. The leveraged ETF starts at $100 and moves up 2% to $102, and the inverse ETF moves down 1% to $99. When the benchmark drops $1 to $100 on day 3, that’s not quite 1%. It’s 0.99%. The price of the leveraged drops 2x 0.99% (1.98% of $102) to $99.9802. The inverse rises 0.99%, from $99 to $99.9802. Both the leveraged and inverse ETFs are a little lower than where they started ($100), while the benchmark didn’t change at all (see figure 1).

FIGURE 1: PULLING LEVERS. The leveraged ETF in this example would effectively allow you to double down on the underlying benchmark. But remember, it works both ways, whether the price goes up or down.For illustrative purposes only. Past performance does not guarantee future results.

In Scenario 2, the benchmark drops $1 on day 2, and the leveraged ETF drops 1% x2, to $98. When the benchmark rises $1 back to $100 on day 3, that’s a 1.01% increase. The leveraged rises 1.01% x 2 to $99.9798. It doesn’t rise $2 back up to $100.

The inverse ETF exhibits similar behavior. That’s the nature of percentage price changes: 1% on a higher price is a bigger change than 1% on a lower price. In both scenarios, the benchmark started at $100 and ended at $100, but the leveraged and inverse ETFs neither ended at $100, nor had the same ending value in the two scenarios. Their prices depend on the specific price path of the benchmark.

Track Your Expectations

Take note: These are simplified scenarios involving only three price changes. Imagine the difference that could accumulate over some 260 trading days through the year. Although the benchmark didn’t have a net change—it started at $100 and ended at $100—in the three-price-change examples above, the leveraged and inverse ETFs both lost value to different degrees, depending on the path of the benchmark’s price changes.

That doesn’t necessarily mean there’s something wrong with the leveraged and inverse ETFs. It’s just how they work. Because the leveraged and inverse ETFs track the daily percent changes of the benchmark, the performance of those ETFs can be quite different from the percent changes in the benchmark over longer periods. That’s what many investors can find confusing. It looks like the leveraged and inverse ETFs should have done one thing, but they actually did another.

What does that mean? Should you avoid trading leveraged and inverse ETFs long-term, if at all? That’s for you to decide. All trading products present risk. But some have nuances that can surprise you if you don’t understand them. In the case of leveraged and inverse ETFs, their particular nuance is that the daily, percentage price changes create discrepancies compared to the benchmark’s longer-term performance. So, if you’re looking for an exact leveraged or inverse replica of the benchmark, you might not get that. Go in with an educated expectation, though, and the leveraged and inverse ETFs might provide opportunity.

Hi Tom, Back in the far, far distant past you said:

I was in the process of updating the list about a month ago and got sidetracked. I now have finished it (mutual fund report) as a separate AIM page. ( execpc.com )

The intent of the list was to have a good source of names that fit well with AIM for very long term holdings.

Hi Gang, Poking around can be dangerous to perceptions.

Way back in 2/8/1998 on Silicon Investor a gentleman was chatting with Tom about PBEGX, a mutual fund. So I got curious to see what had happened to it since then. Well, imagine my surprise when I found:

Company: Pilgrim Baxter

Ticker Symbol: NASD: PBHGX, PBEGX, PBHG, PBHLX PBHEX, PBFVX

Class Period: November 13, 1998 through November 13, 2003

Court: Eastern District, PA

Date Filed: Nov-14-03

Lead Plaintiff Deadline: Jan-13-04

Hi Gang, This is confusing, lots of comments about sticking to ETFs but the pointers are to finding and rating individual stocks. Pointing to what worked in the past, but is advised against today doesn't seem to make a lot of sense. So what should I do to select something for the warehouse? The 1x ETFs don't seem to have all that much volatility so don't seem to fit AIM very well. The 2x and 3x scare the pants off me.

I've already been a bit burned by one 2x that was suggested by my now ex-broker/dealer. The return is good but the price has not gone down enough to capture new stocks, nor has it gone up at all so there could be a bit of a sell. The return is almost 20%/year which is fine for the trust for my brother but it is hovering around 12-14% loss for the last while. So, net net, only a real gain of 6-8% a year. Not bad but in reality only about 3-4% over real inflation, and after taxes somewhat less than 3%.

The area of migrating from what my mother was in to what it should be now is painful and while I'm doing well overall - ~10% income/year - there is more risk than I like this late in the normal business cycle. At this point it seems that I need to wait it out and close a potentially risky position when it is in modest positive territory but then what do I do with the cash? Do I just sit on it for the next 18-36 months?

Where are the tools or methods to analyze the ETFs/ETNs?

Thanks,

Allen

Hi Tom, In poking around just now I found:

Three things are usually considered the basics of investment goals:

1) Price Appreciation over Time

2) Dividend Capture over Time

3) Profitable Volatility Capture over Time

AIM is a method for implementing successfully #3. It works fine with either #1 or #2, but those shouldn't be ignored. Note the inclusion of the word "profitable" in the Volatility Capture item.

Hi Tom, I think may have used the wrong name for the spreadsheet I was playing with. What I was looking for was one that had a place to download data for a stock symbol and had a currency table that was used in the calculations.

BTW, I've been looking at the old stuff at Silicon Investor and it is interesting so see various methods for finding signals for the market like the vWave and other ways of setting up AIM besides Vealies.

And, I agree with jamil about having more suggestions for things to look at for possible positions. Lots of negative, "...don't buy individual stocks...." stuff but not a lot of what to buy for the warehouse.

Thanks,

Allen

Hi Tom,

So, Grabber said we made 27%, but he didn't indicate in what time frame. That's because AIM 'reacts' to market price change, it doesn't time it or predict it. If the old horse carries us to town and that is our goal, then we can't criticize the old horse for not being as fast as a young horse. If we accomplish our goal, then we don't have to worry about time.

Hi Grabber,

I haven't found anyone who will accept %'s as legal tender.

Thanks jamil, not what I was expecting but most excellent to study as there are some explanations of different thinking than I have not considered.

BTW, yeah, Excel can be shit but for those of us who are not programmers it is a great crutch and, done right, prevents some stupidity caused by brain drain and distractions.

Best,

Allen

Help! I seem to have corrupted my LD-AIM spreadsheet (fat fingers and tiredness) and have misplaced the link for getting a fresh start. Pointer, please?

Thanks,

Allen

Hi Gang,

The Return Rate is 210 / 770 = 0.273 or 27.3%

Hi Tom, The AIMBARES.XLS spreadsheet is set up that for a fixed number of stocks although one can change that number as you go along. However the online calculator is always a percentage of the stock held.

Is there any advantage to using a percentage of stocks as opposed to a fixed percentage of the original purchase number?

BTW, thanks for the comments on the old AIM users material. It sort of seems that sometimes minor tweaks are needed to handle major changes in the market.

Best,

Allen

Thanks for the link, Tom, to the old aim-users stuff.

The answer where you say:

I have also used a reduced SAFE on both the sell side and the buy side for those stocks where I have 1000 shares or less. Say I have 500 shares of a $20 stock. If I'm going to trade 100 shares lots then 10% safe is probably too much. I then reduce the buy and sell SAFE values equally to get the trading range to about what the 52 week highs and lows have been. That way I will get more trading activity and make more money.

Hi karw, How far back do you start a no-down machine? Also, I've played a bit with this and I'm not coming up with a 6% buy. How are you arriving at this?

Thanks,

Allen

Hi Toofuzzy, In general good advice, but the problem with Simple Moving Average (SMA)is that it take time to react and weights older events the same as current events. I suspect that using an Exponential Moving Average (EMA) for at least the 13 day average might provide a better signal for buying/selling as it would be closer to the change in direction for a volatile position that does well with AIM.

I have not tested this approach but others might and their input is requested.

Warmest Regards,

Allen

Speaking of hedge funds, WSJ says that "Market Swoon Bruises Some Hedge Funds Losses Amplified by Funds’ Tendency to Buy, Sell Same Stocks."

Also John Paulson's hedge fund, Paulson & Co., has gotten hammered and now "Hedge fund regulatory adviser FrontLine Compliance reports that the SEC has been exerting its force with the registered investment adviser community this year."

See some examples at: http://www.hedgeco.net/news/10/2014/sec-takes-a-closer-look-at-hedge-fund-investment-advisers.html

So an approach, legal or not, does not work forever in our changing world.

Best,

Allen

Thanks, karw. I guess I'll have to look closer at GNAT, and, perhaps run a no-down machine as well.

It's waiting to get to the point of actually buying into a position that is a bit tough. Acck! What do I do with my idle money while I wait?

BTW, thanks for sharing what is happening in your portfolio. It helps a lot to see how others are managing their money so that one can create what one wants to do.

Best,

Allen

Hi Not Always Toofuzzy, Alas, irony is very difficult on the net. I thought that my comment about being able to stand the ride would convey that idea. Clearly not, at least with some.

As to the various stocks you mention, including some that no longer exist, yes, some went to zero and anyone would have been burned had they been in them. But that needs to be taken with at least a small grain of salt.

One of the key ideas that Lichello pushes, at least indirectly, is to get your emotions out of the way. You are going to make mistakes and have losses. Look at hedge funds, almost all of them do well for a while and then die, or mutual funds that do well for a while and then less than the S&P, as examples of approaches that seem to be great ideas but prove, over the long haul, not so perfect.

ETFs/ETNs might be in the same boat when the wizards (not) of Wall Street attempt to make them work slightly differently to meet their own greedy desires. Face it, we are living on the scraps that they allow to fall off the table or that they can not prevent from falling off the table. In fact one of the significant trading patterns, Sam Seiden's approach, is premised on the idea that you can catch a ride on the tail coats of the big institutions to make money. If we are careful we will be well fed, but there might not be enough to go around. Hard to tell in real time, we can only see after the fact what the results are going to be. We might make a wild guess that proves to be true. Great. But don't count on it.

Did the Greeks, during the Periclian democracy period, foresee its end? Did the Romans foresee the end of the Empire? Did the Romanovs foresee the end of the Russian Empire? In the same way it is unlikely we will see a sea change in the markets, such as happened around 1981, except in retrospect. If you are not aware of this, look at the various market chart stats prior to 1980 and those after 1982. Try overlaying one on the other and it is astonishing how vastly different and the downturns tend to be after 1982.

Given all this, I think Lichello was right to tell us to get out emotions out of the equation. Design a rule set to follow, refine it as needed to meet changing conditions, but not too fast, and accept that you will not always get it right in our lifetimes. After all, there an end point for us, either we need the money in our dotage, or we die. Either way we will be out of the Wall Street rat race with whatever success or failure that results from our choices.

It is the choices we make that are key and this is where the wisdom of crowds, this AIM users forum, helps us to make fewer, but not zero, mistakes.

As to HZNP, there are four possible outcomes that I see over the near to longer term, (but not 100 years). It will go out of business and the stock go to zero, it will limp along as a volatile stock, never hitting zero but never growing significantly, it will hit it big with a blockbuster drug and jump sky high, or it will be a little fish that is eaten by a bigger one. Of the four, three might prove profitable, only might. I'm guessing that a small bet that it will be one of those might be worth it. The key is knowing you might lose it all and judge your risk/reward ratio and trade or not depending on how risk adverse you are and how much you are willing to lose.

I can certainly see good reason, like you do, to not invest directly in stocks, or REITs, but if an ETF/ETN is made up of the wrong mix it will wind up limping badly at times and may even almost disappear by becoming so marginalized that you are never able to recoup your losses in your investing lifetime. Maybe your kids will do okay, but even that is a wild ass guess.

Warmest regards,

Allen

Hi karw, Isn't GNAT a bit thinly traded? Seems like only 5-25k a day average.

What does everyone think about thinly traded stocks? I was always told that they can be very hazardous and are often targets of pump and dump schemes because even a small amount of activity can change the price significantly.

On another point, what do you mean, "2 no-down machines"?

Best,

Allen

Need a shot of volatility? Try HZNP! Great AIM stock if you can stand the roller coaster ride.

Best,

Allen

Thanks, Toofuzzy, for the perspective. I hadn't looked at it from that viewpoint so it is with great appreciation I read your information.

Best,

Allen

Re:

Return of capital is more important than return on capital.

The 14% dividend will not do you much good when the dividend is cut and the stock price is cut in half.

Thanks Tofuzzy, very clear reasoning and metrics. My question about interest rates is that the Fed keeps punting raising the rates down the road. In the meantime my cash is getting almost nothing in interest so it seems that the payout that MORL has a much better return on cash, especially if I get only a small position and add to it as it declines - which I'm sure it will - and am planning on holding it then it might make sense.

It is this transition phase from what my mother had done to what I need to do while I manage the trusts. I can't let them sit in the positions they are in now as my mother was trading income for stock depreciation which made some sense at 92 but not for me or my younger brother. So finding reasonable things to do to improve things is what I'm up to at the moment and any suggestions are most welcome.

Thanks,

Allen

Hi Art, Yes, I did back test it and it seemed good. Good volatility and the underlying stocks/ETFs/REITs, what few I've back tested so far seem reasonable. But I need to do more due diligence which is why I ask what others think. I know that while I'm fairly sharp I'm not always the sharpest knife in the draw and it is easy to miss a key point of two given the "positive spin" that we are all exposed to 24/7/366 (in a leap year).

Thanks,

Allen

Hi Tom, you got what I was thinking in one. I'm going to have to study it in more depth. We all tend to write quite condensed explanations of what we are talking about because we don't want to work our finger to the bone.

It is clearer that there are a number of different ways of using AIM that might enhance its results. Clearly I'm going to need to dig deeper into Good 'til Cancelled Limit Orders. I understand the GTC part but am a bit unclear about how to add the limit part as well as a good way to select a limit price to use when buying into a position for the first time.

Best,

Allen

Talk about fat fingering and typos, well I was backtesting SCCO, looking to see if I wanted to buy it, and accidentally typed 355 for minimum shares (MS) instead of the 35 I had intended and got a huge jump in return. I was like, wow, how did that happen? So I played around and looked at the prices and noticed that it avoided earlier sales. I then tried boosting the MS to 400 and got an even bigger jump. Finally with a bit more tuning got it to sell at the peak.

This set me to thinking about the ValueLine expected price and the 52 week range. It might be wise to have two next buy/sell MS figures, one at the 5-10% level and the other calculated to be nearer the top of the ValueLine/52 week range.

The logic is that the overall business cycle has broader up cycles and, although typically shorter, down cycles. While we don't know when a cycle starts or turns around, we can guess after we are in one or the other which we are in. With this guess we can sit on the sidelines for a while and wait until we get close to the calculated higher buy/sell price and then take action.

The way to do this, using a spreadsheet, is to make two copies, one with a 5-10% (or whatever amount you chose) MS and a second copy with the calculated MS. With SCCO the calculated MS turned out to be about 60% of the shares held. I would not select anything that high in practice but 30-40% or so might be reasonable in an up market and 20-25% in a down market. Those %ages are less than the typical up and down major moves in the recent past. Plus, if the past is any predictor of the future, the cycle tops and bottoms have gotten more extreme over the last 30 or so years therefor it might well be the same going forward.

However, it still is a judgement call. SCCO, for example has not gone up since December 2010, while the market has gone up quite a bit since then, so it could be risky.

Not exactly predicting the future but guessing that a series of past behaviors is likely to repeat, just like one can "predict" the next night's behavior of the town drunk. Yeah, he might stay sober, but the odds aren't good. The only real question is how drunk he will be, and that depends on how much money he has in his pocket and we can't know that because we don't have x-ray vision.

Best,

Allen

Hi jamil,

I've also been stocking SLW for and entry, along with FCX.

What does everyone think of MORL, an LETN that in less than a month dropped 12.66%? It pays a bit over 17% and pays monthly. It trades rather thinly, mostly under ~400k share per day and since it was created has been up to 31.86 and down to 16.88 from a creation price of ~25.88 back on 10/17/2012.

Thanks,

Allen

Hi lostcowboy, I don't find the other spreadsheets when I click your link.

In the header at the bottom is a link to the rest of the spreadsheets.

Most Excellent, Clive. Now I get the reasoning.

Warmest Regards,

Allen

My apologies if this is a duplicate, I don't recall where I got this link, but the discussion of LETFs brought it to mind.

http://leveragedetfs.net/Home.html

Quite a list of 2 and 3x ETFs of a variety of types and sectors.

Which leads to the question I have. Clive said:

I also hold some riskier 'bonds' that yield in excess of 8% that if cash reserves did get down that low I'd rather not sell, so the easier option is simply to switch from using 2x to using a 3x version of the LETF.