News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

cjgaddy

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

I don't ever remember hearing GILEAD mentioned, nor can I find anything on them on my PC or via Google. I agree, a great customer to add.

Customer Splits for FY20 (4-30-20) from pg.39/10K:

Latest 10K 4-30-20 iss. 6-20-20 https://tinyurl.com/yak25nco (Cash 4-30-20=$36.3mm)

Period Halozyme Gilead Acumen IGM Coherus ADC-Ther. Others

FYE 4-30-14 91% 8%

FYE 4-30-15 79% 9%

FYE 4-30-16 69% 26% 5%

FYE 4-30-17 58% 16% 26% 16%

FYE 4-30-18 55% 22% 9% 14%

FYE 4-30-19 30% <10% <10% 13% 21% 36%

FYE 4-30-20 28% 24% 11% 11% 10% <10% --

Link to CC (4:30ET, 1:30PT): https://edge.media-server.com/mmc/p/bt2399kr

6-30-20: Avid Bioservices Reports Financial Results for 4th Quarter FYE April 30, 2020, and Recent Developments

https://www.globenewswire.com/news-release/2020/06/30/2055808/0/en/Avid-Bioservices-Reports-Financial-Results-for-Fourth-Quarter-and-Fiscal-Year-Ended-April-30-2020-and-Recent-Developments.html

-- Appointed Nicholas Green as President and CEO

-- Recorded Fourth Quarter Revenue of $12.6M and Annual Revenue of $59.7M

-- Signed $23M in Business Orders and Achieved Record Backlog of $65M During Q4

-- Project Fiscal 2021 Revenue of $76-$81M

Nick Green 2014 Interview. I LIKE this guy. Seems very down to earth and genuine, with a leadership style based on team power. I assume he’ll be on tomorrow’s CC, though he becomes Avid's CEO eff. 7-30-20.

March 2014: CMO Leadership Awards 2014 - Therapure Biopharma

= = = = = = = = =

Nicholas Green (ex-Therapure Biopharma) becomes President/CEO of Avid Bioservices (eff. 7-30-2020) https://tinyurl.com/yczapcc7

After awhile, you just know who to never look at EB.

6-23-20: Avid Bioservices Names New CEO: Nicholas Green (eff. 7-30-2020)

Avid Bioservices Names Nicholas Green as President and Chief Executive Officer

http://ir.avidbio.com/news-releases/news-release-details/avid-bioservices-names-nicholas-green-president-and-chief

Seasoned Executive Brings More than 30 Years of Pharmaceutical and Healthcare Services Industry Experience to Lead Avid Through Next Phase of Growth and Expansion

TUSTIN, June 23, 2020: Avid Bioservices, Inc. (NASDAQ:CDMO/CMDOP), a dedicated biologics contract development and manufacturing organization (CDMO) working to improve patient lives by providing high quality development and manufacturing services to biotechnology and pharmaceutical companies, today announced that Nicholas Green has been appointed President and CEO, as well as a member of the company’s board of directors, effective July 30, 2020. He will succeed Rick Hancock who has served as interim president and CEO since May 2019. Mr. Hancock will continue to serve on Avid’s board of directors.

Mr. Green has more than 30 years of experience in the global pharmaceutical and healthcare services industry with significant expertise in the contract manufacturing of novel pharmaceutical products. His global pharmaceutical experience spans four continents, having run 31 facilities in nine countries spanning North America, South America, Europe, and Asia. Throughout his career, Mr. Green has held a number of senior management roles for several contract manufacturing organizations and life science companies, where he is credited with successfully building and expanding those businesses and delivering significant value for customers, patients, employees, and other stakeholders.

Joseph Carleone, Ph.D., chairman of the Avid board of directors, said, “On behalf of the Avid board, I’d like to welcome Nick as our new president and CEO. His appointment is the result of a deliberate and comprehensive search for an industry executive capable of leading Avid to achieve its full potential. Nick’s lengthy and impressive career in the pharmaceutical contract development and manufacturing sector, which has included senior leadership roles at several successful companies, positions him perfectly to oversee Avid’s ongoing efforts aimed at customer base expansion and revenue growth. The board and I look forward to the positive impact that Nick will make on the company’s business over both the near and long-term.”

“I am excited to join the Avid team and contribute my industry experience to helping the company continue its impressive growth trajectory,” said Mr. Green. “Today, there is significant and growing demand for companies at the leading edge of contract development and manufacturing services for biologics. With its high-quality offerings in the areas of process development, analytical services, and CGMP manufacturing, combined with its more than 25 years of experience in manufacturing complex biologics, Avid is among the best positioned companies to seize this opportunity.”

“I thoroughly enjoyed my role as the interim president and CEO of Avid and am proud of what the company has achieved during that time in diversifying our client base and increasing revenues,” said Rick Hancock. “I believe that Avid is well positioned to execute successfully on its growth strategy moving forward and the addition of a leader such as Nick will only serve to strengthen the company’s prospects. The appointment of someone of Nick’s caliber, combined with the strength and talents of the entire Avid team, make it easy for me to step aside and transition back into the sole role of board member at this time. I would like to express deep gratitude to all Avid team members for their commitment and hard work during my tenure.”

Mr. Green most recently served as president and CEO of Therapure Biopharma [ https://www.therapurebio.com/ ], a Canada-based biopharmaceutical company which includes Therapure Biomanufacturing. In this role, he oversaw the growth of the company’s CDMO business, while also leading the creation of Therapure’s proprietary plasma protein business, named Evolve. Prior to Therapure, he held a number of senior management roles, most notably managing director of Nipa Laboratories Ltd., head of the life science division of Clariant International Ltd. in the USA, president and CEO of Rhodia Pharma Solutions Ltd. and president of Codexis, Inc.’s pharma division. Mr. Green holds a bachelor’s degree in chemistry from Queen Mary College in London and an MBA from the University of Huddersfield.

= = = = = = = =

6-23-20/OCBJ: Avid Bioservices Names New CEO: Nicholas Green

Tustin-based Avid Bioservices Inc. (Nasdaq: CDMO) appointed Nicholas Green as its new CEO effective, July 30th.

Green will succeed Rick Hancock who served as interim CEO since May 2019; Hancock will remain on the board of directors following the change of leadership.

"I thoroughly enjoyed my role as the interim president and CEO of Avid and am proud of what the company has achieved," Hancock said in a press release.

Green recently served as President & CEO of Canada-based Therapure Biopharma. Prior to that, he was managing director of Nipa Laboratories Ltd., and headed the life science division of Clariant International Ltd. in the USA as well as served as President & CEO of Rhodia Pharma Solutions Ltd.

Avid is a dedicated CDMO specializing in biopharmaceuticals. The company had a $311M market cap at press time and was trading at $5.62/sh.

https://www.ocbj.com/news/2020/jun/23/avid-bioservices-names-new-ceo/

I think EarningsWhispers is complete and utter nonsense on earnings dates. I never remember them being anything close to right.

May19/5pm: “At least 63 public-companies have returned PPP-Loans worth about $510 million as of Tuesday afternoon.”

https://www.morningstar.com/news/marketwatch/20200519575/as-deadline-passes-for-returning-small-business-loans-public-companies-have-given-back-500-million-and-kept-900-million

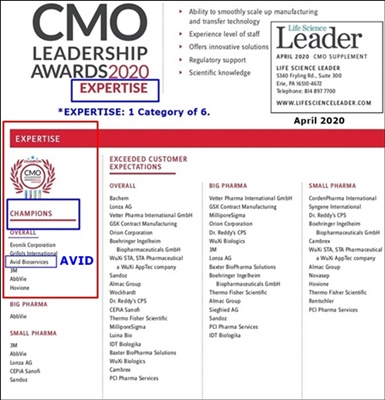

Well, they’ve got The EXPERTISE...

5-18-20: Avid Listed In Top CMO Awards Article https://tinyurl.com/yb5cnh6m

11 TOP CMO’s LISTED (with short descriptions):

3M, Abbvie, Boehringer’s Ingelheim, Grifols, Lonza, Millipore Sigma, Vetter, Wuxi Biologics, Avid Bioservices, Fujifilm Diosynth Biotechnologies, Samsung Biologics

...The 1st 8 rec. All 6 Awards; the last 3 (Avid/Diosynth/Samsung) rec. 5 of 6 Awards.

AVID BIOSERVICES

Avid Bioservices received recognition in 5 CMO Leadership Awards categories, including 2 Champion designations in both Expertise & Service. The contract manufacturer is critical in the supply chain for the pharmaceutical industry and it is maintaining a high level of safety and quality to continue development and providing manufacturing services to its customers during the COVID-19 pandemic.

5-18-20: Avid Listed In Top CMO Awards Article

5-18-20: Top Awarded Biopharmaceutical Companies Responding to COVID-19

By: Healthcare Business Today Team

Since 2011, Life Science Leader & Outsourced Pharma have been recognizing the leaders of top contract manufacturing organizations (CMOs) through individual customer feedback. The resulting CMO Leadership Awards represent the highest level of achievement as evaluated and determined by actual customers. Only those customers that have worked with the CMO on an outsourced project for at least 18 months are able to provide an evaluation…

...With the recent COVID-19 outbreak, the biotechnology industry is feeling the pressure to create and manufacture effective treatments and vaccines to combat the virus.

The 2020 CMO Leadership Awards evaluated more than 125 contract manufacturers on 23 different performance metrics. The awards were given at an interesting time this year as biopharma and CMOs step up their efforts to combat the COVID-19 crisis.

Below, we look at the biopharmaceutical companies that came out on top in the 2020 CMO Leadership Awards, and how they are rising to face the challenge of fighting COVID-19.

11 Companies were listed, incl AVID.

The 1st 8 rec. All 6 Awards.

The last 3 (Avid/Diosynth/Samsung) rec. 5 of 6 Awards.

I don’t know if this is truly the Top 11 of all 125 CMO’s evaluated or if we paid to make this top list in this article. If the former, very good industry recognition.

TOP CMO’s LISTED (with short descriptions):

3M, Abbvie, Boehringer’s Ingelheim, Grifols, Lonza, Millipore Sigma, Vetter, Wuxi Biologics, Avid Bioservices, Fujifilm Diosynth Biotechnologies, Samsung Biologics,

AVID BIOSERVICES

Avid Bioservices received recognition in 5 CMO Leadership Awards categories, including 2 Champion designations in both Expertise & Service. The contract manufacturer is critical in the supply chain for the pharmaceutical industry and it is maintaining a high level of safety and quality to continue development and providing manufacturing services to its customers during the COVID-19 pandemic.

The CMO Leadership Awards are the most meaningful in the drug development and manufacturing outsourcing industry. The organizations on this list are only a handful of those who received awards. In addition, these are just a few of the companies tackling the COVID-19 crisis. With many opportunities on the horizon, it is only a matter of time that the combined efforts produce positive results for our world health.

https://www.healthcarebusinesstoday.com/top-awarded-biopharmaceutical-companies-responding-to-covid-19/

= = = = =

Here is a 55pg. PDF of All the 2020 CMO Leadership Awards:

https://www.qgdigitalpublishing.com/publication/?i=652719

The EXPERTISE CATEGORY (1 of 6 categories).

...Avid makes the overall champions list with 5 other CMO’s:

3-10-20 Qtly CC-Transcript, PR(Q3FY20/qe1-31-20), Avid Revs History Table

*Revs Guidance (FY’20 fye 4-30-20): $55-59M. 10-31-19 Backlog=$58M

*Cash: 1-31-20: $30.7M

*As of 11-30-19: 56,338,143 shares o/s.

*10Q/1-31-20 iss. 3-10-20: https://tinyurl.com/vkocrsg

*Avid Total Revs May03-Jan20: $396.1M

*Avid’s website: https://avidbio.com (A/o 4-30-19, 211 full-time & 4 part-time emps)

This large post has 4 sections:

I. 3-10-20 Qtly. Earnings Conf. Call TRANSCRIPT (FY20/Q3 q/e 1-31-20)

II. 3-10-20 CDMO Press Release: Q3/FY20 Earnings & Developments

IV. Updated Table of Avid Revenues By Quarter (May’06-Current)

III. Updated O/S Shares History Table – 2006-curr.

…Recall: Avid’s FY runs May-Apr, so FY’20 = May’19-Apr’20.

GO HERE (I messed up the Stickies – sorry)...

https://investorshub.advfn.com/boards/read_msg.aspx?message_id=154286734

Total INST.+LARGE Holdings now 36,882,771 65.3% (3-31-20)

Down from 40,237,198 71.4% at 12-31-19 (assuming 2.6M Ronin shares sold – see below).

28,296,779 50.1% INSTITUTIONS (a/o 3-31-20)

https://www.nasdaq.com/symbol/cdmo/institutional-holdings

+ 8,585,992 15.2% LARGE SHAREHOLDERS via Forms13/14 (EasternCap/Dart, Tappan) – ie, not in Nasdaq Inst. List.

------------

= 36,882,771 65.3%

1. I’m not sure about Eastern Cap(K.Dart): no updates since 12-2017, assume NO CHG.

2. Also assuming that a/o 3-20-2020, Ronin(Stafford/Farley) has no ownership (they owned 2,638,450 4.7% a/o 4-17-18 13D https://tinyurl.com/ycf7d2uk ): 3-20-20 https://www.pionline.com/trading/ronin-capital-assets-auctioned (“CME Group auctioned off Ronin’s portfolios in March”. Maybe whoever bought Ronin’s portfolio still owns the 2,638,450 shares of CDMO? See RONIN NOTE AT BOTTOM. So strange.)

Note: Ownership %’s based on 56,482,154 common O/S at 3-2-20 (10Q: https://tinyurl.com/vkocrsg )

11 LARGEST SHAREHOLDERS:

1. IsZo Capital Mgt. (Brian Sheehy): 5,645,701 10.0% (+1,425,553 a/o 3-31-20 Nasdaq Inst.)

2. Eastern Capital (Kenneth Dart): 4,300,992 7.6% (a/o 12-7-17 14A: https://tinyurl.com/y7qprpg9 acq. 10-2015)

3. Tappan Street (Prasad Phatak): 4,285,000 7.6% (a/o 12-31-19 13G: https://tinyurl.com/wlcwnnv )

4. Blackrock Inc. (Larry Fink): 3,881,521 6.9% (-52,910 a/o 3-31-20 Nasdaq Inst.)

5. Vanguard Group 2,638,045 4.7% (+57,499 q/e 3-31-20 Nasdaq Inst.)

6. Snyder Capital 2,280,905 4.0% (+98,519 a/o 3-31-20 Nasdaq Inst.)

7. Altravue Capital 1,950,355 3.5% (-261,087 a/o 3-31-20 Nasdaq Inst.)

8. Sargent Invest. Grp. 1,165,997 2.1% (+204,415 a/o 3-31-20 Nasdaq Inst.)

9. State Street 1,038,673 1.8% (-21,871 a/o 3-31-20 Nasdaq Inst.)

10. Geode Capital 740,689 1.3% 42,493 (+42,493 a/o 3-31-20 Nasdaq Inst.)

11. Silvercrest Asset Mgt. 736,143 1.3% (+173,411 a/o 3-31-20 Nasdaq Inst.)

BIGGEST DROPS q/e 3-31-20:

Millennium -330,454 to 700,169

Two Sigma Investments -269,192 Sold Out

Oxford Asset Mgt. -264,077 Sold Out

Altravue Capital -261,087 to 1,950,355

= = = = = = = = = = = =

Shares O/S as of 3-2-20=56,482,154 - history since 4-2006: https://tinyurl.com/s9cmzmf

...A/O 1-31-20: 2,941,000 stock options outstanding at a wgt.avg. exercise price of $6.45 (pg.15 10Q).

3-10-20: Qtly. Conf. Call (Hancock/Hart/Compton) PR & Transcript https://tinyurl.com/s9cmzmf

4-30-20: “Ronin’s Collapse: The Mysterious Disappearance of a Chicago Trading Giant - Puzzling Losses, a Closely Guarded Auction and Possible Redemption”

By Costas Mourselas @CostasMourselas

More than a month after Ronin Capital’s portfolios were seized and sold off by clearing houses, much about the affair remains unknown, including the source of the firm’s losses and the results of the auction at CME. It’s not just observers that are in the dark. Risk.net understands Ronin’s management team is still waiting to find out what happened in the auction – information that could ultimately help determine whether the famed Chicago prop trader has some kind of future.

https://www.risk.net/risk-management/7535981/the-mysterious-disappearance-of-a-chicago-trading-giant

No problem EB. A lot quotes & news services have mixed up “Avid Systems” and “Avid Technologies” with us at various times over the years. Very frustrating when it happens.

ArchieK, you posted Wainwright 11=>9 back on March 12th, right after the 3-10-2020/Q3 Earnings/CC.

https://investorshub.advfn.com/boards/read_msg.aspx?message_id=154307711

I wonder if this one got mixed-up w/Avid?

3-12-20: Stifel Initiates Coverage on Avadel Pharmaceuticals (AVDL) with Buy, $14 Price Target. The 14 target sounds way out of range for new coverage of CDMO to me.

Is it still there, Eb0783?

3-10-20 Qtly CC-Transcript, PR(Q3FY20/qe1-31-20), Avid Revs History Table

*Revs Guidance (FY’20 fye 4-30-20): $55-59M. 10-31-19 Backlog=$58M

*Cash: 1-31-20: $30.7M

*As of 11-30-19: 56,338,143 shares o/s.

*10Q/1-31-20 iss. 3-10-20: https://tinyurl.com/vkocrsg

*Avid Total Revs May03-Jan20: $396.1M

*Avid’s website: https://avidbio.com (A/o 4-30-19, 211 full-time & 4 part-time emps)

This large post has 4 sections:

I. 3-10-20 Qtly. Earnings Conf. Call TRANSCRIPT (FY20/Q3 q/e 1-31-20)

II. 3-10-20 CDMO Press Release: Q3/FY20 Earnings & Developments

IV. Updated Table of Avid Revenues By Quarter (May’06-Current)

III. Updated O/S Shares History Table – 2006-curr.

…Recall: Avid’s FY runs May-Apr, so FY’20 = May’19-Apr’20.

TRANSCRIPT 3-10-20 FY20/Q3 Earnings Conf. Call (q/e 1-31-20):

Rick Hancock(Interim CEO), Daniel Hart(CFO), Tim Compton(CCO)

Q&A Analysts:

Matt Hewitt - Craig-Hallum Capital

Jacob Johnson - Stephens

Paul Knight - Janney Montgomery Scott

Joe Munda - First Analysis

READ the CC Transcript here:

https://www.fool.com/earnings/call-transcripts/2020/03/10/avid-bioservices-inc-cdmo-q3-2020-earnings-call-tr.aspx

Link to webcast replay: http://ir.avidbio.com/events-and-presentations => https://edge.media-server.com/mmc/p/vvmbx7ze

= = = = = = = = = = = = = = = = = = = = = = = = = = = = = == = = =

3-10-20: Avid Bioservices Reports Financial Results for 3rd Quarter FY 2020 (1-31-20) and Recent Developments

http://ir.avidbio.com/news-releases/news-release-details/avid-bioservices-reports-financial-results-third-quarter-1

-- Recorded Third Quarter Revenue of $13.6 Million

-- Signed New Customer and Project Expansion Orders with Current Customers for $20 Million

-- Adjusting Fiscal 2020 Projected Revenue to $55-59 Million

TUSTIN, March 10, 2020: Avid Bioservices, Inc. (NASDAQ:CDMO/:CDMOP), a dedicated biologics contract development and manufacturing organization (CDMO) working to improve patient lives by providing high quality development and manufacturing services to biotechnology and pharmaceutical companies, today announced financial results for the third quarter and first nine months of fiscal 2020 ended January 31, 2020.

HIGHLIGHTS SINCE OCTOBER 31, 2019

“During the third quarter of 2020, Avid strengthened both its project pipeline and backlog, and the fundamentals of the business remained strong,” said Rick Hancock, interim President and CEO of Avid. “However, the company faced production challenges during the period related to a problem with a specific piece of equipment which resulted in the termination of in-process manufacturing runs, and the postponement of several other manufacturing runs scheduled to commence during the third quarter. Though we are now implementing the necessary corrections, the temporary production interruption resulted in lower revenue and profits for the third quarter, and we expect it to also impact revenues and profits for the fourth quarter of fiscal 2020. For this reason, we are adjusting our revenue guidance for fiscal 2020 to $55-59 million vs. our prior guidance of $64-$67 million. It is our expectation that this problem will be behind us soon, and as such, we anticipate that the impact will be contained to fiscal 2020. While we are disappointed that this temporary operational setback will negatively impact our fiscal 2020 results, we anticipate that we will be able to recover those revenues in fiscal 2021. We remain optimistic about Avid’s growth potential. Critical to achieving this growth is the continued expansion of Avid’s customer and project base. To lead this effort, we recently welcomed Timothy Compton to the Avid team as our chief commercial officer. During the third quarter, Tim launched the first phase of an aggressive business development campaign. As a result, we signed agreements to add one new customer and multiple additional manufacturing campaigns with existing customers during the period. With respect to operations, we continue to make progress on projects to optimize our existing Myford facility while finalizing plans for its future expansion. We will continue to update you moving forward as these plans progress.”

FINANCIAL HIGHLIGHTS AND GUIDANCE

* The company is adjusting revenue guidance for the full fiscal year 2020 to $55-59 million from prior full fiscal year 2020 guidance of $64-67 million.

* Revenue was $13.6 million for the third quarter of fiscal 2020, consistent with $13.8 million for the third quarter of last fiscal year. For the nine months ended January 31, 2020, revenues were $47.2 million, a 29% increase as compared to revenues of $36.5 million during the same prior year period. The slight decrease during the third quarter of fiscal 2020 can primarily be attributed to a decrease in process development revenue, combined with the impact of the production interruption described above, which were largely offset by an increase in the number of in-process and completed manufacturing runs conducted during the quarter compared to the same prior year quarter. Likewise, the increase during the first nine months of fiscal 2020 was primarily due to an increase in the number of in-process and completed manufacturing runs, a result of growing demand from a more diverse client base, partially offset by a decrease in process development revenue and the third quarter production interruption.

* As of January 31, 2020, revenue backlog was approximately $58 million, an increase of 12% compared to the second quarter of fiscal 2020. The company expects to recognize the majority of this backlog within the next 12 months.

* Gross margin for the third quarter of fiscal 2020 was 6%, a decrease compared to the 15% gross margin for the third quarter of fiscal 2019. The decrease in gross margin for the quarter was primarily attributed to the costs associated with the aforementioned production interruption, an increase in depreciation expense from the acquisition of new equipment, and a net decrease in revenues. Gross margin for the nine months ended January 31, 2020 was 11%, up slightly compared to 10% in the prior year period. This increase was primarily due to an increase in manufacturing runs, partially offset by costs associated with payroll and related costs, higher facility and equipment related costs primarily associated with the production interruption described above, increased depreciation expense from the acquisition of new equipment, and general equipment repairs and maintenance costs.

* Selling, general and administrative expenses (“SG&A”) for the third quarter of fiscal 2020 were $3.0 million, a decrease of 8% compared to $3.2 million for the third quarter of fiscal 2019. This decrease was primarily due to a decrease in accrued bonuses for fiscal 2020, partially offset by an increase in employee separation costs. For the first nine months of fiscal 2020, SG&A expenses were $11.0 million, an 19% increase compared to $9.3 million for the first nine months of fiscal 2019. The increase in SG&A was primarily attributed to employee separation-related expenses and increased stock-based compensation. When excluding the separation-related expenses, SG&A increased by 10% during the first nine months of fiscal 2020 as compared to the prior year.

* For the third quarter of fiscal 2020, the company recorded a consolidated net loss attributable to common stockholders of $3.5 million or $.06 per share, compared to a consolidated net loss attributable to common stockholders of $2.6 million or $.05 per share, for the third quarter of fiscal 2019. For the first nine months of fiscal 2020, the company recorded a consolidated net loss attributable to common stockholders of $9.3 million or $.17 per share, compared to a consolidated net loss attributable to common stockholders of $8.2 million or $.15 per share, for the first nine months of fiscal 2019.

* Avid reported $30.7 million in cash and cash equivalents as of January 31, 2020, compared to $32.4 million on April 30, 2019.

More detailed financial information and analysis may be found in Avid Bioservices’ Quarterly Report on Form 10-Q, which will be filed with the SEC today. [ https://tinyurl.com/vkocrsg ]

RECENT CORPORATE DEVELOPMENTS

* Appointed Timothy (Tim) Compton as chief commercial officer. Mr. Compton has extensive experience in commercial operations, including sales team management, business development, marketing and corporate development. In his new role, he will be responsible for driving the continued growth of Avid’s CDMO business, including the ongoing expansion of the company’s commercial and clinical client base.

* Expanded our customer base with the addition of one new customer and executed multiple project expansion orders with existing customers representing additional revenue backlog of $20 million during the third quarter.

* Advanced planning and design to both enhance our Myford facility, and support its future expansion. These near-term improvements include installing a pharmaceutical grade water system, and upgrading key IT systems and general infrastructure. We expect the installation and validation of the water system to take place in late calendar year 2020 and the IT system enhancements and general infrastructure upgrades to be complete by the end of fiscal 2021.

CONFERENCE CALL

Avid will host a conference call and webcast this afternoon, March 10, 2020, at 4:30 PM EDT (1:30 PM PDT). To listen to the conference call, please dial (877) 312-5443 or (253) 237-1126 and request the Avid Bioservices conference call. To listen to the live webcast, or access the archived webcast, please visit: http://ir.avidbio.com/events.cfm .

ABOUT AVID BIOSERVICES, INC.

Avid Bioservices is a dedicated contract development and manufacturing organization (CDMO) focused on development and CGMP manufacturing of biopharmaceutical products derived from mammalian cell culture. The company provides a comprehensive range of process development, high quality CGMP clinical and commercial manufacturing services for the biotechnology and biopharmaceutical industries. With 25 years of experience producing monoclonal antibodies and recombinant proteins in batch, fed-batch and perfusion modes, Avid's services include CGMP clinical and commercial product manufacturing, purification, bulk packaging, stability testing and regulatory strategy, submission and support. The company also provides a variety of process development activities, including cell line development and optimization, cell culture and feed optimization, analytical methods development and product characterization. https://www.avidbio.com

Forward-Looking *snip*

AVID BIOSERVICES, INC.

?CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS AND COMPREHENSIVE LOSS

(Unaudited)(In thousands, except per share information)

Three Months Ended

January 31,

Nine Months Ended

January 31,

2020 2019 2020 2019

Revenues $ 13,585 $ 13,781 $ 47,152 $ 36,548

Cost of revenues 12,800 11,731 41,921 32,972

Gross profit 785 2,050 5,231 3,576

Operating expenses:

Selling, general and administrative 2,996 3,242 10,989 9,273

Loss on lease termination — — 355 —

Total operating expenses 2,996 3,242 11,344 9,273

Operating loss (2,211 ) (1,192 ) (6,113 ) (5,697 )

Interest and other income, net 107 9 415 190

Loss from continuing operations before income taxes (2,104 ) (1,183 ) (5,698 ) (5,507 )

Income tax benefit — 44 — 217

Loss from continuing operations, net of tax (2,104 ) (1,139 ) (5,698 ) (5,290 )

Income from discontinued operations, net of tax — — — 739

Net loss $ (2,104 ) $ (1,139 ) $ (5,698 ) $ (4,551 )

Comprehensive loss $ (2,104 ) $ (1,139 ) $ (5,698 ) $ (4,551 )

Series E preferred stock accumulated dividends (1,442 ) (1,442 ) (3,604 ) (3,604 )

Net loss attributable to common stockholders $ (3,546 ) $ (2,581 ) $ (9,302 ) $ (8,155 )

Basic and diluted net (loss) income per common share attributable to common stockholders:

Continuing operations $ (0.06 ) $ (0.05 ) $ (0.17 ) $ (0.16 )

Discontinued operations — — — 0.01

Net loss per share attributable to common stockholders $ (0.06 ) $ (0.05 ) $ (0.17 ) $ (0.15 )

Weighted average basic and diluted shares outstanding 56,404 56,069 56,275 55,949

AVID BIOSERVICES, INC.

CONDENSED CONSOLIDATED BALANCE SHEETS

(Unaudited)(In thousands, except par value)

January 31,

2020 April 30,

2019

ASSETS

Current assets:

Cash and cash equivalents $ 30,687 $ 32,351

Accounts receivable 10,151 7,374

Contract assets 6,111 4,327

Inventory 9,565 6,557

Prepaid expenses and other current assets 763 709

Total current assets 57,277 51,318

Property and equipment, net 26,850 25,625

Operating lease right-of-use assets 20,437 —

Restricted cash 350 1,150

Other assets 302 302

Total assets $ 105,216 $ 78,395

LIABILITIES AND STOCKHOLDERS’ EQUITY

Current liabilities:

Accounts payable $ 5,332 $ 4,352

Accrued payroll and related costs 2,985 3,540

Contract liabilities 26,355 14,651

Operating lease liabilities 1,172 —

Other current liabilities 710 619

Total current liabilities 36,554 23,162

Operating lease liabilities, less current portion 21,584 —

Deferred rent, less current portion — 2,072

Other long-term liabilities — 93

Total liabilities 58,138 25,327

Commitments and contingencies

Stockholders’ equity:

Preferred stock, $0.001 par value; 5,000 shares authorized;

1,648 shares issued and outstanding at January 31, 2020 and April 30, 2019, respectively 2 2

Common stock, $0.001 par value; 150,000 shares authorized;

56,479 and 56,136 shares issued and outstanding at January 31, 2020 and April 30, 2019, respectively 56 56

Additional paid-in capital 613,323 613,615

Accumulated deficit (566,303 ) (560,605 )

Total stockholders’ equity 47,078 53,068

Total liabilities and stockholders’ equity $ 105,216 $ 78,395

CONTACTS:

• Stephanie Diaz (Investors) Vida Strategic Partners 415-675-7401 sdiaz@vidasp.com

• Tim Brons (Media) Vida Strategic Partners 415-675-7402 tbrons@vidasp.com

- - - - - - - -

From 10-Q header: “As of Mar 2, 2020, there were 56,482,154 shares outstanding.”

- - - - - - - - - - - - - - - - -

Latest 10K 4-30-19 iss. 6-27-19 http://tinyurl.com/yxukx6t4 (Cash 4-30-19=$32.4mm)

Latest 10Q 1-31-20 iss. 3-10-20 https://tinyurl.com/vkocrsg (Cash 1-31-20=$30.7mm)

ALL SEC filings for PPHM: http://tinyurl.com/6d4jw8

10-K: “As of 4-30-19, we employed 211 full-time & 4 part-time emps.” (2018: 185/1)

= = = = = = = = = = = = = = = = = = = = = = = = = = = =

Updated PPHM REVS-BY-QTR TABLE, now thru FY20Q3(qe 1-31-20), per the 10Q issued 3-10-20.

• Total Avid Revs since May’03: $396.1M

• 3-10-20: FY'20 (May'19-Apr'20) Avid revs guidance $55-59M (committed B/L=$58 at 1-31-20).

• Inventories at 1-31-20 total $9.6M, UP from $7.8M at 1-31-20.

Avid’s website: http://www.avidbio.com

AVID GROSS PROFITABILITY BY QTR: CONTRACT

QTR (1000’s) Rev$ COGS$ Prof$ GP% INVEN$ LIABILITIES*

FY13Q1 7-31-12 4,135 2,024 2,111 51% 5,744 16,280

FY13Q2 10-31-12 6,061 3,703 2,358 39% 5,426 14,721

FY13Q3 1-31-13 6,961 3,651 3,310 47% 4,635 11,790

FY13Q4 4-30-13 4,176 3,217 959 23% 4,339 12,230

FY14Q1 7-31-13 4,581 2,670 1,911 42% 5,679 12,692

FY14Q2 10-31-13 7,354 4,195 3,159 43% 4,033 11,126

FY14Q3 1-31-14 3,885 2,416 1,469 38% 5,224 12,975

FY14Q4 4-30-14 6,474 3,829 2,645 41% 5,530 11,001

FY15Q1 7-31-14 5,496 3,583 1,913 35% 5,998 10,896

FY15Q2 10-31-14 6,263 4,139 2,124 34% 5,379 11,161

FY15Q3 1-31-15 5,677 3,113 2,564 45% 6,148 14,063

FY15Q4 4-30-15 9,308 4,758 4,550 49% 7,354 17,993

FY16Q1 7-31-15 9,379 4,608 4,771 51% 10,457 17,890

FY16Q2 10-31-15 9,523 4,741 4,782 50% 12,554 24,623

FY16Q3 1-31-16 6,672 3,896 2,776 42% 15,189 37,851

FY16Q4 4-30-16 18,783 9,721 9,062 48% 15,189 39,630

FY17Q1 7-31-16 5,609 3,062 2,547 45% 25,274 43,262

FY17Q2 10-31-16 23,370 15,441 7,929 34% 25,924 44,908

FY17Q3 1-31-17 10,747 7,974 2,773 26% 33,829 52,577

FY17Q4 4-30-17 17,904 11,782 6,122 34% 33,099 45,517

FY18Q1 7-31-17 27,077 20,448 6,629 24% 24,235 27,755

FY18Q2 10-31-17 12,782 16,242 -3,460 -27% 16,518 20,611

FY18Q3 1-31-18 6,819 10,951 -4,132 -61% 14,218 24,235

FY18Q4 4-30-18 6,943 8,904 -1,961 -28% 16,129 27,935

FY19Q1 7-31-18 12,589 11,397 1,192 9% 9,168 17,994

FY19Q2 10-31-18 10,178 9,844 334 3% 9,736 17,307

FY19Q3 1-31-19 13,781 11,731 2,050 15% 8,660 14,620

FY19Q4 4-30-19 17,055 13,407 3,648 21% 6,557 14,651

FY20Q1 7-31-19 15,254 14,168 1,086 7% 8,031 18,104

FY20Q2 10-31-19 18,313 14,953 3,360 18% 7,809 22,199

FY20Q2 1-31-20 13,585 12,800 785 6% 9,565 26,355

*7-31-18 10Q: “prior-yr amts related to (deferred revenue

+ cust deposits) now reclass’d as contract liabilities.”

FY13 TOTAL: 21,333 12,595 8,738 41%*

FY14 TOTAL: 22,294 13,110 9,184 41%*

FY15 TOTAL: 26,744 15,393 11,151 42%*

FY16 TOTAL: 44,357 22,966 21,391 48%*

FY17 TOTAL: 57,630 38,259 19,371 34%*

FY18 TOTAL: 53,621 56,545 -2,924 -5%*

FY19 TOTAL: 53,603 46,379 7,224 13%*

*Avid Net-Profit(Selling/G&A) not split out from PPHM-Corp. in the fin’s.

AVID TOTAL REV’s BY YEAR):

FY04 4-30-04 3,039 (Avid-Revs didn’t incl. Avid’s Gov’t work)

FY05 4-30-05 4,684

FY06 4-30-06 3,005

FY07 4-30-07 3,492

FY08 4-30-08 5,897

FY09 4-30-09 12,963

FY10 4-30-10 13,204

FY11 4-30-11 8,502

FY12 4-30-12 14,783

FY13 4-30-13 21,333

FY14 4-30-14 22,294

FY15 4-30-15 26,744

FY16 4-30-16 44,357

FY17 4-30-17 57,630

FY18 4-30-18 53,621

FY19 4-30-19 53,603

FY20 4-30-20 47,152 <=thru Q3 1-31-20

**TOTAL: 396,121 (5/1/2003–1/31/20)

.

QTLY. NET PROFIT/LOSS BY QTR:

(“attributable to common stockholders”; ie, incl. PREF Div’s**)

**2-11-14: PPHM Raises $16.2M, 700k Pref. Shares w/10.5% DIV.

FY16Q1 7-31-15 -15,101,000

FY16Q2 10-31-15 -14,578,000

FY16Q3 1-31-16 -18,227,000

FY16Q4 4-30-16 -13,264,000

FY17Q1 7-31-16 -12,437,000

FY17Q2 10-31-16 -4,498,000

FY17Q3 1-31-17 -9,216,000

FY17Q4 4-30-17 -6,714,000

FY18Q1 7-31-17 -2,647,000

FY18Q2 10-31-17 -14,066,000

FY18Q3 1-31-18 -12,446,000

FY18Q4 4-30-18 +1,578,000 <=includes $9,154,000 income from disc. operations.

FY19Q1 7-31-18 -3,403,000

FY19Q2 10-31-18 -2,893,000

FY19Q3 1-31-19 -2,581,000

FY19Q4 4-30-19 -1,106,000

FY20Q1 7-31-19 -4,606,000

FY20Q2 10-31-19 -1,872,000

FY20Q3 1-31-20 -3,546,000

Period Halozyme ADC-Therap. Coherus-BioSci. Other-Custs

FYE 4-30-14 91% 8%

FYE 4-30-15 79% 9%

FYE 4-30-16 69% 26% 5%

FYE 4-30-17 58% 26% 16%

FYE 4-30-18 55% 9% 22% 14%

FYE 4-30-19 30% 21% 13% 36%

...(cust. splits not given in 7-31-18+ 10Q’s)

Total INST.+LARGE Holdings now 40,237,198 71.4% (12-31-19)

Up from 37,448,204 66.6% at 9-30-19.

29,012,756 51.5% INSTITUTIONS (a/o 12-31-19)

https://www.nasdaq.com/symbol/cdmo/institutional-holdings

+ 11,224,442 19.9% LARGE SHAREHOLDERS via Forms13/14 (Tappan, EasternCap/Dart, Ronin/Stafford) – ie, not in Nasdaq Inst. List.

I’m not sure about Eastern Cap(K.Dart) and Ronin(Stafford/Farley) - no updates since 12-2017 & 4-2018 respectively. I’m assuming that means NO CHG.

------------

= 40,237,198 71.4%

Note: Ownership %’s based on 56,338,143 common O/S at 11-30-19 (10Q: https://tinyurl.com/v37mgjk )

11 LARGEST SHAREHOLDERS:

1. Eastern Capital (Kenneth Dart): 4,300,992 7.6% (a/o 12-7-17 14A: https://tinyurl.com/y7qprpg9 acq. 10-2015)

2. Tappan Street (Prasad Phatak): 4,285,000 7.6% (-569,100 a/o 12-31-19 13G: https://tinyurl.com/wlcwnnv )

3. IsZo Capital Mgt. (Brian Sheehy): 4,220,148 7.5% (-314,546 a/o 2-31-19 Nasdaq Inst.)

4. Blackrock Inc. (Larry Fink): 3,934,431 7.0% (+8,905 a/o 12-31-19 Nasdaq Inst.)

5. Ronin Trading (John Stafford III+Roger Farley): 2,638,450 4.7% (a/o 4-17-18 13D: https://tinyurl.com/ycf7d2uk )

6. Vanguard Group 2,580,546 4.6% (-98,873 q/e 12-31-19 Nasdaq Inst.)

7. Altravue Capital 2,211,442 3.9% (-11,940 a/o 12-31-19 Nasdaq Inst.)

8. Snyder Capital 2,182,386 3.9% (-69,667 a/o 12-31-19 Nasdaq Inst.)

9. State Street 1,060,544 1.9% (+32,716 a/o 12-31-19 Nasdaq Inst.)

10. Millennium Mgt. 1,030,623 1.8% (+203,339 a/o 12-31-19 Nasdaq Inst.)

11. Sargent Invest. Grp. 961,582 1.7% (+324,471 a/o 12-31-19 Nasdaq Inst.)

BIGGEST DROPS q/e 12-31-19:

IsZo Capital Mgt. -314,546 to 4,220,148

Vanguard Group -98,873 to 2,580,546

= = = = = = = = = = = =

Shares O/S as of 11-30-19=56,338,143 - history since 4-2006: https://tinyurl.com/tfewuzc

...A/O 10-31-19: 3,552,000 stock options outstanding at a wgt.avg. exercise price of $7.57 (pg.14 10Q).

12-9-19: Qtly. Conf. Call (Hancock/Hart/Kinjerski) PR & Transcript https://tinyurl.com/tfewuzc

Tappen+IsZO 13G’s: Both dropped a little a/o 12-31-19 quarter...

9 LARGEST SHAREHOLDERS:

1. Tappan Street (Prasad Phatak): 4,285,000 7.6% (-569,100 a/o 12-31-19 13G: https://tinyurl.com/wlcwnnv )

2. IsZo Capital Mgt. (Brian Sheehy): 4,220,148 7.4% (-314,546 a/o 12-31-19 13G: https://tinyurl.com/wfnhv7h )

Blackrock 13G a/o 12-31-19: 3,934,431(7.0%), up slightly (+8,905) from 9-30-19 Nasdaq Inst. figure:

2-4-2020/13G BlackRock (Larry Fink): https://tinyurl.com/uukaedp

A/o 12-31-19: Aggregate amt. beneficially owned: 3,934,431

%Class: 7.0%

= = = = = =

9-31-19 Nasdaq INST/BLACKROCK INC: 3,925,526

https://www.nasdaq.com/market-activity/stocks/cdmo/institutional-holdings

9 LARGEST SHAREHOLDERS a/o 9-30-19:

1. Tappan Street (Prasad Phatak): 4,854,100 8.6% (+337,993 a/o 12-31-18 13G: http://tinyurl.com/yxrpla3b )

2. IsZo Capital Mgt. (Brian Sheehy): 4,534,694 8.1% (-243,429 a/o 9-30-19 Nasdaq Inst.)

3. Eastern Capital (Kenneth Dart): 4,300,992 7.6% (a/o 12-7-17 14A: https://tinyurl.com/y7qprpg9 acq. 10-2015)

4. Blackrock Inc. (Larry Fink): 3,925,526 7.0% (+135,240 q/e 9-30-19 Nasdaq Inst.)

5. Ronin Trading (John Stafford III+Roger Farley): 2,638,450 4.8% (a/o 4-17-18 13D: https://tinyurl.com/ycf7d2uk )

6. Vanguard Group 2,676,002 4.8% (+3,417 q/e 9-30-19 Nasdaq Inst.)

7. Snyder Capital 2,252,053 4.0% (+9,761 a/o 9-30-19 Nasdaq Inst.)

8. Altravue Capital 2,223,382 4.0% (+114,570 a/o 9-30-19 Nasdaq Inst.)

9. State Street 1,027,828 1.8% (+87,955 a/o 9-30-19 Nasdaq Inst.)

Inst. Holdings (Nasdaq) - updated 45-days after each qtr-end: http://www.nasdaq.com/symbol/cdmo/institutional-holdings

Shares O/S as of 11-30-19=56,338,143 - history since 4-2006:

https://tinyurl.com/tfewuzc

...A/O 10-31-19: 3,552,000 stock options outstanding at a wgt.avg. exercise price of $7.57 (pg.14 10Q).

12-9-19 Qtly CC-Transcript, PR(Q2FY20/qe10-31-19), Avid Revs History Table

*Revs Guidance (FY’20 fye 4-30-20): $64-67M. 10-31-19 Backlog=$52M

*Cash: 10-31-19: $34.0M

*As of 11-30-19: 56,338,143 shares o/s.

*10Q/10-31-19 iss. 12-9-19: https://tinyurl.com/v37mgjk

*Avid Total Revs May03-Jul19: $382.5M

*Avid’s website: https://avidbio.com (A/o 4-30-19, 211 full-time & 4 part-time emps)

This large post has 4 sections:

I. 12-9-19 Qtly. Earnings Conf. Call TRANSCRIPT (FY20/Q2 q/e 10-31-19)

II. 12-9-19 CDMO Press Release: Q2/FY20 Earnings & Developments

IV. Updated Table of Avid Revenues By Quarter (May’06-Current)

III. Updated O/S Shares History Table – 2006-curr.

…Recall: Avid’s FY runs May-Apr, so FY’20 = May’19-Apr’20.

((( Orig. transcript from SeekingAlpha.com [https://tinyurl.com/rd75k59 ] with numerous corrections made. )))

Link to webcast replay: http://ir.avidbio.com/events-and-presentations => https://edge.media-server.com/mmc/p/kgzqm8c5

TRANSCRIPT 12-9-19 FY20/Q2 Earnings Conf. Call (q/e 10-31-19) (Hancock/Hart/Kinjerski)

RICK HANCOCK (INTERIM CEO) – OPENING COMMENTS:

Thank you to everyone who has dialed in, and to those who are participating today via webcast. During Q2, increased productivity and efficiency drove positive results across the organization, and I am happy to provide an overview of the progress made during the period. I’ll begin by stating that revenue for Q2 of 2020 was the highest that Avid has recorded in the last two years. In addition, our backlog and other financial metrics were strong during the quarter and Dan will provide more details regarding our financial results in a moment. On the business development front, we continue to have a strong presence in the market with the goal of attracting new business and we’re advancing multiple discussions to expand our scope of work with several current customers. Tracy will provide an update on these activities. We also achieved several important milestones operationally during the quarter that we believe will enhance our services, offerings, and contribute to the continued growth of our business. I'll provide more details on these accomplishments following an overview of our second quarter financial results. With that, I’ll turn the call over to Dan.

DANIEL HART (CFO) – OPENING COMMENTS:

Before I begin, I'd like to recommend that everyone participating on today's call refer to our 10-Q filing with the SEC which we filed today for additional details https://tinyurl.com/v37mgjk . I'll now discuss our financial results for continuing operations for Q2 and the first six months of FY2020 ended October 31, 2019. I'll first address our second quarter results. Revenue for the quarter was considerably better than market estimates at $18.3M, an increase of 80% as compared to $10.2M for the same period of the prior year. This significant increase was primarily the result of an increase in the number of in-process and completed manufacturing runs during the quarter, primarily for our largest customer. Gross margin for Q2 of 2020 was 18%, a significant increase as compared to the 3% gross margin in the prior-year period. The increase in gross margin for the quarter was primarily attributed to revenue from an increased number of manufacturing runs, which was more than enough to offset the unexpected costs incurred at the beginning of our fiscal year. I’ll now address operating expenses. Total SG&A expenses for Q2 of FY2020 were 3.5M compared to 2.8M for Q2 of FY2019. This increase was primarily due to increases in both payroll-related expenses and stock-based compensation. Also during the quarter, we entered into a lease amendment to terminate an operating lease for one of our non-manufacturing facilities that was primarily utilized as warehouse space. As part of our continuing efforts to reduce costs and increase efficiencies, this quarter we successfully consolidated our available warehouse space thereby moving supplies and materials closer to manufacturing, which allowed for the termination of this lease. In connection with the lease termination, we recognized a one-time charge of $355,000. As a result, our future lease and related payments have been reduced by approximately $1.3M over the next four years and the termination freed up $250,000 of restricted cash that was pledged as collateral under a letter of credit required by the lease. The lease termination of this redundant warehouse space has no impact on our future expansion plans as we still have 42,000 square feet available within our Myford facility.

For Q2 of FY2020, the company recorded a consolidated net loss attributable to common stockholders of 1.9M or $.03 a share. This outcome was an improvement compared to a consolidated net loss attributable to common stockholders of 2.9M or $0.05 a share for Q2 of FY2019 exceeding consensus estimates. Our backlog at the end of Q2 of 2020 was $52M, a decrease of 16% compared to the $61M at the end of Q1 2020 and an increase of 13% compared to the 46M at the end of last fiscal year. This quarter-over-quarter decrease resulted from efficiencies that allowed us to increase manufacturing activity by initiating several runs in Q2 that were originally scheduled for a later period and was partially offset by current period bookings. Despite accelerating our production schedule, we continue to maintain a strong backlog, much of which we expect to recognize in FY2020. I’ll now provide an overview of our results for the first six months of FY2020. For the first six months ended October 31, 2019, revenues were 33.6M, a 47% increase as compared to revenues of 22.8M during the prior year period. As is the case with the quarter, the significant increase was primarily the result of continued growth in the number and scope of customer projects. Gross margin for the six months ended October 31, 2019 was 13%, up significantly compared to the 7% in the prior-year period. This increase was primarily due to an increase in manufacturing the customer projects, which was more than enough to offset the step-up in personnel costs required to accommodate growth and production demand, and the realignment of company’s compensation structure to secure our existing workforce that occurred at the beginning of our fiscal year as well as equipment repairs and maintenance costs. For the first six months of FY2020, SG&A expenses were $8M, a 33% increase compared to $6M for the first six months of FY2019. The increase in SG&A was primarily attributable to employee separation-related expenses and increased stock-based compensation. When excluding the separation-related expenses, SG&A increased 19% during the first six months of FY2020 as compared to the prior year. Also included within the first half of FY2020 was the lease termination charge of 355,000 that I mentioned earlier. For the six months of FY2020, the company recorded a consolidated net loss attributable to common stockholders of 6.1M or $.11 per share compared to a consolidated net loss attributable to common stockholders of 5.9M or $.11 per share for the first six months of FY2019. Our cash and cash equivalents at October 31, 2019 were $34M as compared to $32.4M as of the prior fiscal year ended April 30, 2019. Given the strength of our backlog and the visibility we have into current customer projections, we are reaffirming our revenue guidance for FY2020 of $64M to $67M. We are pleased with our financial performance during the quarter. The company continues to approach our near-term milestone of operational breakeven, which we believe will position the company to achieve both industry standard margins and sustainable profitability. This concludes my financial overview. I will now turn the call over to Tracy for an update on business development activities and achievements for the quarter.

TRACY KINJERSKI (VP, BUSINESS OPERATIONS) - OPENING COMMENTS:

As Rick mentioned, during the quarter we continued our efforts in attracting new customers and advancing new business with our existing customers. We continue to focus on increasing the awareness of our services and our strength as an industry leader through technical presentations, webinars and conference participation. During Q2, Avid’s business team continued to execute an aggressive visibility campaign with participation at industry events, including the Bioprocessing Summit in August, Biotech Week in contract pharma in September and World ADC in outsourced pharma in October as well as local industry events. We recently hosted a technical seminar in Cambridge along with industry colleagues. Each of these events gives us access to potential new customers, provides an excellent platform to promote Avid's latest enhancements and accomplishments and the opportunity to provide insight into advancing molecules from concept to market from a CDMO perspective. This quarter we hosted a number of potential new client visits at Avid for technical due-diligence business as well as quality audits, both critical gaining items in the outsourcing process. The feedback we received from customer audits is universally positive. We also continue to prospect for new opportunities across the industry by meeting with potential new clients at their facilities.

I will now address the opportunities represented by the new client prospects mentioned above. First, these new projects are diverse ranging from customers interested in Avid’s development and early phase manufacturing experience to interest in our late phase and commercial experience, including access to the space we have for expansions to meet their future commercial demand. I'm also pleased to announce the forward movement and execution of new business opportunities with our existing clients. We are currently expanding work that will result in the advancement of existing projects to the next phase of manufacturer, progressing molecules from smaller scale manufacturers to our larger 2,000-liter scale in Myford and increasing batch numbers. In an earlier earnings call we announced supporting other clients with their process validation activities. Recent completion of these activities will enable certain clients to submit their biologics license application filings which will trigger the scheduling of future pre-approval inspections estimated to occur within the next two years related to the anticipated approval of these particular molecules. For those products approved during – using processes validated at Avid, the commercial manufacturing will be conducted at Avid. As we have stated previously for this reason we see each process validation completed today as an opportunity to build commercial business in the future. Also during the quarter, we completed multiple other batch manufacturers for earlier phase client molecules. As we announced in early July, Avid signed two new contract manufacturing service agreements to support the development of novel drug candidates. The onboarding of these projects has been completed and they are progressing towards manufacture. The agreements include the addition of one of the world's leading pharmaceutical companies to Avid’s list of customers as well as the expansion of the relationship with one of the company's existing biotechnology customers. All of these opportunities are a result of Avid’s commitment to quality, reliability and collaboration to ensure the success of our clients. It also demonstrates a path to continued growth in our backlog and revenue. I'm pleased with the activity ongoing at Avid with respect to enhancing biopharmaceutical industry's awareness of Avid and our capabilities, including our available 2,000-liter capacity, room for expansion and growth of our pipeline of activity projects and partnership opportunities with new and existing clients. This concludes my business overview.

RICK HANCOCK (CEO) – Q4/FY19 OPERATIONAL & COMMERCIAL UPDATE:

Thank you, Tracy. First, I’d like to welcome Rich Richieri back to the Avid team. As we announced in October, Rich previously spent 15 years with Avid Bioservices and its former parent company Peregrine Pharmaceuticals in the role of Senior VP of Manufacturing. During that time, Rich was instrumental in establishing and growing Avid’s CDMO business and helping the company diversify its production capabilities. He spent the past five years serving as an advisor and acting head of biologics production for Syngene International, a global discovery, development and manufacturing organization serving the pharmaceutical industry. Richard rejoins Avid as Chief Operations Officer with responsibility for overseeing process development, clinical and commercial manufacturing, technical support and facilities. In this role, Rich will be focused on streamlining operations, building internal efficiencies and strategic planning for future growth. In addition, Rich will work with our business development team to optimize every aspect of our customer experience. Given his global CDMO experience combined with his Avid specific expertise, we're very happy to have Rich in this important leadership role. In other leadership matters, we continue our search for a permanent CEO for the company. We are actively screening highly qualified candidates and we look forward to providing an update soon. In the meantime, we continue to grow the business and advance all core objectives. Our team has the expertise required to execute all the company's strategic goals and no projects or programs are being delayed pending the arrival of a new CEO. As a case in point, we were pleased to report that during Q2 we officially launched our expanded process development facility in services at an Open House event attended by customers, prospective customers, vendors and community leaders. This purpose-built state-of-the-art facility which houses Avid's expanded upstream and downstream process development capabilities represents an important new opportunity for the company. It allows us to expand our existing relationships and attract new business by offering support to customers that seek to outsource their PD work. Equally important, this PD capability allows us to expand our scope of services beyond biologics into the diagnostics and general biologics research and development sectors. We are very pleased to officially launch this new lab in service and we believe it will make great contributions to Avid’s continued growth. In other operations news, we have entered into the final design stage for the construction of a new pharmaceutical grade water system in the Myford facility. Installation of this system, which will supply water to multiple manufacturing systems, is a critical step in creating the manufacturing efficiencies required to increase our output and strengthen our margins. As with the rest of our Myford facility, this system will be state-of-the-art and we anticipate installation in calendar 2020. Lastly, during Q2, Avid conducted its annual maintenance overhaul. During these overhauls, certain of our facilities maybe partially or completely shut down so that we can conduct a comprehensive evaluation of our facilities and equipment. Last year, both facilities were down for more than 3 weeks. However, due to the significant amount of work that was done during last year's evaluation, the process with shorter this year with Franklin down for less than two weeks and only a partial shutdown at Myford affecting only the exterior of the building. In light of this shutdown, we are particularly proud of the increase in both revenue and margins during the quarter which we believe reflect an organizational resilience that is rare with larger CDMOs. In closing, I'd like to highlight a few takeaways. Our business development effort continues to be wide reaching and robust. Our reputation in the industry for quality products and regulatory success continues to grow, allowing us to engage with a growing pool of potential new customers. It also allows us to expand our relationships with existing customers providing us with an opportunity to pitch new projects and services. Operationally, we continue to improve and enhance our equipment, facilities and systems. The opening of the new process development lab, the successful completion of our annual maintenance overhaul, and upcoming installation of a new pharmaceutical grade water system, all reflect the dedication we have to maintaining the highest standards possible. Financially, revenues for the quarter were the highest since Avid transitioned to a pure-play CDMO. We also achieved an 18% gross margin which represents a significant increase year-over-year as well as quarter-over-quarter. Expenses remained in line with expectations and our backlog continues to be strong. Importantly, during the quarter, we nearly achieved breakeven income from operations despite the deferral of revenue during the first half of FY2020 caused by unplanned equipment repairs in Q1 and our annual maintenance overhaul in Q2. Productivity and efficiency contributed significantly to Avid’s strong second quarter results, and we expect our financial performance will continue to track positively with these factors. We believe that Avid has turned an important corner, creating a stronger platform from which to achieve increased revenues, improved margins and sustainable profitability. This concludes my prepared remarks for today.

Q&A: [beg. 19:44]

1. Joseph Pantginis - H.C. Wainwright

JP: ”Hi, guys. Good afternoon. Thanks for taking the question. Wanted to ask a couple related questions. First, with regard to Myford and for example the new water system that you’re putting in, is this to be considered sort of a course of normal business with regard to the costs or how should we view that with regard to costs going forward?”

Rick Hancock: The Myford, water-for-injection system is an enhancement to the overall systems in the utilities within our Myford facility. We do have the structure of a water-for-injection system within our Franklin facility. It's just time for us to add as we continue to look at expansion into our Myford facility, which will also help with increasing our margins. As far as the overall operational costs, I would imagine all-in for one of these complicated type systems would be somewhere in the realm of about $2M to $3M.

JP: ”Got it. That's very helpful. Thank you for that. And then with regard to your commentary with regard to scope of work, obviously when you talk about the backlog number, you've always stated that you don't include future potential work that you have projected, but that might not be signed as an example. How do you view the scope of work with regard to when you might look to open up new facilities that you have capacity for?”

Rick Hancock:

Right. So, I believe you're referring to that 42,000 square feet of space in the Myford facility which is located right next to the facilities that are built out already. So, we're preparing contingency plans to build that out as soon as the demand is solid. It will probably be based on continuing to increase the use of the existing facility. We saw some room for revenue growth in Myford. Franklin is pretty busy, but there's room for growth in Myford. And then based on discussions that we have, long-term projections for some of the commercial products, we have plans to build that out, and we're just waiting for some of that capacity to have clear visibility of the usage of some of that future capacity, and then we’ll pull the trigger.

JP: Got it. And again, thanks. That’s very helpful. And then lastly with regard to your overall corporate strategy, Halozyme recently, for example, one of your biggest clients, they had some corporate update/volatility. How are you prepared to sort of weather any volatility with regard to your biggest clients, even though it appears that there was no impact to you guys from Halozyme?”

Rick Hancock: Right. That's a great question. We've obviously had significant discussions with Halozyme. As we understand it, we won't have any negative impact for the discontinuation of one of their products. Halozyme, as they have stated, will be very, very focused on their ENHANZE platform and the materials that we produce here at Avid supports that ENHANZE platform. So, no negative impact can be anticipated there. And in fact, they are probably more focused on expanding efforts in that area. In terms of our other major clients, as Tracy noted, we've had a number of them go through the scale up for their commercial production and just waiting to see how those timelines develop, but that's all very positive for us in terms of future commercial work. So the trends are very positive right now in the biotech industry in general, and we're very, very fortunate that the number of our clients are expanding their programs and are very, very healthy at this point.

2. Mike XXXX (in for Paul Knight) – Janney Capital

MX: ”Good afternoon, guys. It's Mike [??] in for Paul. And thanks for the time. We were modeling down sequentially given the planned shutdowns you guys mentioned in Q1. Can you just talk a little bit more about the dynamics that you mentioned earlier in the call that led to the increase and then kind of the weakness in the backlog in Q2 as compared to Q1? Thanks.”

Dan Hart: Sure, Mike. Pleasure to speak with you. Thanks for the questions. I guess how I would phrase the increase in revenues for Q2 was truly based on us being able to find some efficiencies in the overall capacity of our facilities to bring in some of the manufacturing projects that were scheduled to start later on in the quarter or even the next quarter. So we had the ability and the opportunity to pull in some of those projects. Because for the most part, the shutdown in our Franklin facility and the shutdown we had in our Myford facility went extremely well. It went ahead of schedule and we're able to open back up and schedule production quicker than we had originally anticipated. As far as the backlog, our backlog will ebb and flow quarter-over-quarter and it just all depends on how much revenue we recognized during the period and how much we sign. And given our business, we don't necessarily sign change orders and contracts for new molecules every week, every month, every quarter. So, it depends on the timing of those major programs and when they come in. So we will see some volatility in our backlog, but in general it should remain fairly strong on a trend towards growth.

MX: ”Great. Thanks. And then with the three process validation campaigns complete, do you have any visibility from your communications with clients on when they expect to either file or hear a decision from the regulatory agencies? And then those three potentially commercial products, how does that compare to how many commercial projects you support now? Thanks.”

Rick Hancock: Sure. So, obviously, we are in very, very active discussions with our clients about their future plans. They have certain things that they can control in terms of when they complete their submissions, and then once it goes to the agency, it moves a little bit beyond their control. There's certain waiting periods, and then depending on what the agency comes back with, they may request additional information or things like that. So, we planned capacity for the earliest date that they may require production, but beyond that, it's just very frequent updates and we don't have tremendous visibility when they will get approval. But just having a number of those, and I would say the odds of them getting approval, my opinion is very high based on what the projects are, what the molecules are, but having the existing commercial production that we do, three different molecules and then a number of others going into commercial in the future is very gratifying. I think as a CDMO, having a substantial amount of our capacity taken out by commercial products and holding that steady while we bring in earlier stage programs as well, there's a lot of benefits. One is that we can look at the calendar early in the year and have a very good idea of capacity utilization.

3. Matt Hewitt - Craig-Hallum Capital

MH: ”Maybe if you could help us a little bit. Given the efficiencies that you're able to find on the manufacturing side in Q2 that allowed you to either start some projects early from later in the quarter or even pulling from Q3, are those efficiencies expected to continue? Meaning will you be continuing to kind of pull forward some of that backlog from Q3 and Q4 earlier into the year?”

Rick Hancock: Well, Matt, that's a great question. I think you're spot on. The reality is, as we continue to fill the pipe and to look at the remainder of the year, it's not necessarily all the backlog shifted forward. We had the opportunity to move some of those projects forward. But as far as looking for the rest of the year, like we stated in the prepared comments, we're still looking at 64M-67M for the year, and our backlog’s at 52M which a majority of that typically winds out within 12 months, and we looked at most of that coming into our FY2020 year. We’re still in plenty of active discussions with our clients in increasing our overall backlog and look to continue to move towards that growth.

MH: ”Okay. All right. And then shifting gears to gross margin, very strong quarter. Some of that was being able to get the facilities back up and running faster than expected. But as we look at the next few quarters for this year and I guess looking out a little bit further, how should we be thinking about gross margin? Where do you see that kind of exiting the year? And then I've got a follow up to that as well.”

Dan Hart: Well, Matt, I'm not going to guide towards what the overall margin is going to look like, but I will say that our incremental margins going forward – since we're a largely fixed cost business, our incremental margins going forward will be somewhere between the 50% and 70% range, so most of that will be dropping to the bottom line. So I would anticipate that our margins will be stronger than where we ended last year on a fiscal year of 13%. We should continue to beat those margins.

MH: ”That's great. And then I guess a follow up is regarding the new water treatment capabilities, you mentioned that that would also help margins. What kind of a pop or boost would you expect that to give to gross margin?”

Rick Hancock: Not terribly significant to gross margin. Where it will make a greater contribution is in efficiencies, moving projects through the Myford facility at a slightly accelerated rate. It's something that our customers will be happy to see. Right now we purchased the water for injection that we used in 200-liter drums and it's a little bit of a logistical challenge moving those throughout the supply chain. So this will just contribute to the overall productivity of that facility.

4. Jacob Johnson - Stephens Inc.

JJ: ”Hi. Thanks. Congrats on the strong quarter. Just one question on guidance. It implies for a slowdown in the second half of the year outside of the benefit from pulling forward some of the revenues in Q2. Are there any other puts and takes when you just think about for the back half of your FY2020?”

Dan Hart: No. Jacob, how’s it going and thanks for calling in and thanks for the question. Looking at the remainder of the fiscal year, there's no seasonality per se or facility shutdown per se that we're anticipating for the rest of the year. And we will continue to produce within the manufacturing capacity for the remainder of the second half.

JJ: ”Got it. And then in October you opened the expanded process development lab. Obviously, it's going to generate its own revenue stream. But is that important to your business development efforts, including building out your manufacturing pipeline?”

Rick Hancock: It really is. In the past we were slightly constrained in terms of process development. So we're focused on bringing on projects that were more mature where the bulk of the process development work has already been completed, and they could transition pretty rapidly to our clinical manufacturing. This rounds us out and allows us to take on very, very early stage projects. And also it allows us to do additional process development work on projects that we're completing already, whether it's a scale up or looking for more efficiencies in either upstream or downstream process. It also opens us up to doing standalone process development projects. And typically PD has a pretty healthy margin associated with it. So by being able to do purely process development projects, we can start working with a new customer doing very specific activities in PD and get the relationship going and then progress to additional work.

JJ: ”Got it. Thanks for that, Rick. And then, Dan, just one quick point of certification. The 2M to 3M for the new water system, will that be a capital expenditure in terms of accounting for it or will that flow through the OpEx line?”

Dan Hart: It will absolutely be a capital item that's going to the balance sheet.

RICK HANCOCK (CEO) – CLOSING COMMENTS:

The progress made during Q2 has placed us in a strong position for growth and we look forward to updating you on our future advancements. Thank you, again, for participating today and for your continued support of Avid Bioservices.

= = = = = = = = = = = = = = = = = = = = = = = = = = = = = == = = =

12-9-19: Avid Bioservices Reports Financial Results for 2nd Quarter FY 2020 (10-31-19) and Recent Developments

http://ir.avidbio.com/news-releases/news-release-details/avid-bioservices-reports-financial-results-second-quarter-0

-- Achieved Strong Second Quarter Revenue of $18.3 Million and Gross Margin of 18% --

-- Fiscal 2020 Projected Revenue of $64 to $67 Million Reaffirmed --

-- Launched Expanded Process Development Facility and Services --

TUSTIN, Dec. 9, 2019: Avid Bioservices, Inc. (NASDAQ:CDMO/CDMOP), a dedicated biologics contract development and manufacturing organization (CDMO) working to improve patient lives by providing high quality development and manufacturing services to biotechnology and pharmaceutical companies, today announced financial results for Q2 of fiscal 2020 ended October 31, 2019.

HIGHLIGHTS SINCE JULY 31, 2019

“During Q2 of 2020, we strengthened multiple core areas of our business,” said Rick Hancock, interim president and chief executive officer of Avid. “Our business development effort continues to be wide reaching and robust. Our reputation in the industry for quality and regulatory success continues to grow allowing us to engage with a broadening pool of potential new customers and expand our relationships with existing customers.

“Operationally, we continue to improve and enhance our equipment, facilities and systems. The opening of our new process development lab, the successful completion of our annual maintenance overhaul, and the planned installation of a new pharmaceutical grade water system in calendar 2020 all reflect the dedication we have to maintaining the highest standards possible.

“The revenues for this quarter were the highest since Avid transitioned to a pure-play CDMO in January 2018, and we achieved 18% gross margin, which represents a significant increase year-over-year as well as quarter-over-quarter. Expenses remained in line with expectations and our backlog continues to be strong. Also important, during the quarter we approached breakeven income from operations.

“Productivity and efficiency contributed significantly to Avid’s strong second quarter results, and we expect that our financial performance will continue to track positively with these factors. We believe that Avid has turned an important corner, creating a stronger platform from which to achieve sustainable profitability.”

Financial Highlights and Guidance

* The company is confirming prior revenue guidance for the full fiscal year 2020 of $64-67 million.

* Revenue was $18.3 million for Q2 of fiscal 2020, an increase of 80% as compared to $10.2 million for Q2 of last fiscal year. For the six months ended October 31, 2019, revenues were $33.6 million, a 47% increase as compared to revenues of $22.8 million during the prior period. Increases during both current-year periods were primarily due to an increase in the number of in-process and completed manufacturing runs as a result of growing demand from a more diversified client base.

* As of October 31, 2019, revenue backlog was approximately $52 million, a decrease of 16% as compared to the first quarter of fiscal 2020. The company expects to recognize the majority of this backlog within the next 12 months.

* Gross margin for Q2 of fiscal 2020 of 18% was up significantly compared to a gross margin of 3% in the prior period. Gross margin for the six months ended October 31, 2019 was 13%, up significantly compared to 7% in the prior period. These increases were primarily attributed to the increased number of manufacturing runs, partially offset by costs associated with the hiring of personnel to accommodate growth in production demand, increases in other compensation expenses, and equipment repairs.

* Selling, general and administrative expenses (“SG&A”) for Q2 of fiscal 2020 were $3.5 million compared to $2.8 million for Q2 of last year. The increase was primarily attributed to payroll and related costs, and stock-based compensation. For the first six months of fiscal 2020, SG&A expenses were $8.0 million compared to $6.0 million for the first six months of fiscal 2019. The increases in SG&A during the six-month period were primarily attributed to payroll and related costs, including one-time employee separation-related expenses, and increased stock-based compensation.

* In September 2019, the company recognized a one-time loss of $.4 million in connection with the termination of a non-manufacturing facility lease, which reduces our future lease and related payments by approximately $1.3 million over the next four years. Additionally, the lease termination released $.3 million of restricted cash that was pledged as collateral under a letter of credit required by the terminated lease back to the company. The lease termination of this redundant warehouse space has no impact on our future expansion plans, as the company continues to have 42,000 square feet available within our Myford facility.

* For Q2 of fiscal 2020, the company recorded a consolidated net loss attributable to common stockholders of $1.9 million or $0.03 per share, compared to a consolidated net loss attributable to common stockholders of $2.9 million or $0.05 per share, for the prior year period. For the first six months of fiscal 2020, the company recorded a consolidated net loss attributable to common stockholders of $6.1 million or $0.11 per share, compared to a consolidated net loss attributable to common stockholders of $5.9 million or $0.11 per share, for the prior year period.

* Avid reported $34.0 million in cash and cash equivalents as of October 31, 2019, compared to $32.4 million on April 30, 2019.

More detailed financial information and analysis may be found in Avid Bioservices’ Quarterly Report on Form 10-Q, which will be filed with the SEC today. https://tinyurl.com/v37mgjk

RECENT CORPORATE DEVELOPMENTS

* Launched expanded process development (PD) facility and services. This purpose-built state-of-the-art facility, which houses Avid’s expanded upstream and downstream process development capabilities, represents an important new opportunity for the company by allowing us to expand our existing relationships and attract new business by offering support to customers that seek to outsource their PD work.

* Expanded scope of work with multiple existing customers to increase the number of manufacturing batches and/or scale of production.

* Appointed Richard (Rich) Richieri as chief operations officer. Mr. Richieri will oversee Process Development, Clinical and Commercial Manufacturing, Technical Support and Facilities. In this role, Mr. Richieri will be focused on streamlining operations, building internal efficiencies and strategic planning for future growth. Mr. Richieri has over 25 years of biopharmaceutical industry experience spanning the areas of drug discovery, CGMP operations, contract manufacturing and process development. Mr. Richieri previously spent 15 years with Avid Bioservices and its former parent company, Peregrine Pharmaceuticals, including the role of senior vice president of manufacturing. During that time, he was instrumental in launching, building and growing Avid’s CDMO business and helping the company diversify its production capabilities.

* Initiated final design stage for the construction of a new pharmaceutical grade water system in the Myford facility. Installation of this system will supply water to multiple manufacturing systems, a critical step in creating the manufacturing efficiencies required to increase output and strengthen margins. The company expects the system to be installed in calendar 2020.

Conference Call

Avid will host a conference call and webcast this afternoon, December 9, 2019, at 4:30 PM ET (1:30 PM PT). To listen to the conference call, please dial (877) 312-5443 or (253) 237-1126 and request the Avid Bioservices conference call. To listen to the live webcast, or access the archived webcast, please visit: http://ir.avidbio.com/events.cfm .

About Avid Bioservices, Inc.

Avid Bioservices is a dedicated contract development and manufacturing organization (CDMO) focused on development and CGMP manufacturing of biopharmaceutical products derived from mammalian cell culture. The company provides a comprehensive range of process development, high quality CGMP clinical and commercial manufacturing services for the biotechnology and biopharmaceutical industries. With 25 years of experience producing monoclonal antibodies and recombinant proteins in batch, fed-batch and perfusion modes, Avid's services include CGMP clinical and commercial product manufacturing, purification, bulk packaging, stability testing and regulatory strategy, submission and support. The company also provides a variety of process development activities, including cell line development and optimization, cell culture and feed optimization, analytical methods development and product characterization. http://www.avidbio.com

AVID BIOSERVICES, INC.

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS AND COMPREHENSIVE LOSS

(Unaudited) (In thousands, except per share information)

Three Months Ended

October 31, Six Months Ended

October 31,

2019 2018

2019 2018

Revenues $ 18,313 $ 10,178 $ 33,567 $ 22,767