News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

mas

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

some 33-50% of the TSA order will ship end of May to end of June.

I heard 10 months starting from the end of May.

Probably but if you are getting 50+% margin on that and the TSA comes back for many repeat orders up to the value of the $162m IDIQ what difference does it make in the long run ? Even Intel gives 50% discount to large OEMS like Amazon, HP, Dell etc and it is unrealistic to think that a list price for a single B220 that was published years ago is still relevant now for a large bulk order.

The TSA order will completely fill the first 3 quarters of FY2016 meaning revenue of over $10m in each (with other orders added) which will probably be profitable or close enough. That should bring new shareholders into the fold interested in value stocks rather than just the story investors you have now.

Of course a buyout of DMRJ's debt is the ideal option but DMRJ just maybe the reason McGann is CEO now rather than Bolduc. So it may just have to be a multi-year grind of good results to burn through all that dilution. FY2016Q1 is reported mid-November and that's when the trading volume should pick up and if any of you are thinking of doubling down it would be best before then and probably before the 10-K in September to be on the safe side.

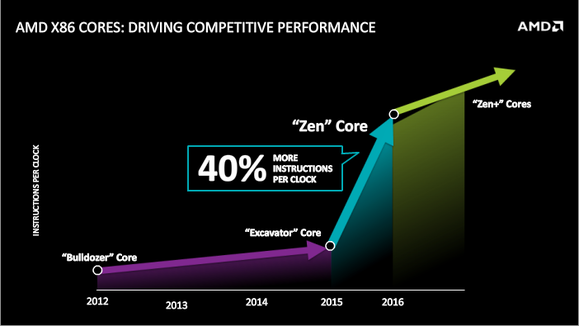

Do you have any public links or are you just extrapolating from the 40% ipc increase remark ?

If it was AMD would be making billions  .

.

Vladimir Vladimirovich Putin, modern day Czar of Russia, can ensure local compliance and homegrown cpu uptake regardless of performance

If preliminary benchmarks are excellent this stock may yet see double figures again.

Back to the future with ZEN x86 and K12 ARM

http://www.pcworld.com/article/2919601/amd-pivots-back-to-high-performance-computing.html

After years of jerking around AMD finally remembers what made it in the first place !

None unless sales have suddenly spiked up.

I have been suggesting for some time that if the company supports the moving averages that contain the high volume LMT sale day (and older) the stock will support itself and so it has proved. The 221-241 SMA is 2.87 and that has provided support several times in the last month. That's 22 days of moving average support at greater than 200 days and the moving averages around that are only a cent or two lower providing further back-up. If enough people are not under water they just won't sell and will wait. Stock trading at its most basic.

Out of three NGCD MSID competitors only Chemring have had a further development option activated in 2015

https://www.fpds.gov/ezsearch/fpdsportal?s=FPDSNG.COM&q=+msid+ngcd+PIID%3A%22W911SR14C0038%22&indexName=awardfull&y=13&x=18&templateName=1.4.4

click View to see ...

Reason For Modification: Exercise an Option

Description Of Requirement: NCD MSID Brassboard Prototype

All development contracts so far can be see at ...

https://www.fpds.gov/ezsearch/fpdsportal?indexName=awardfull&templateName=1.4.4&s=FPDSNG.COM&q=+msid+ngcd&x=18&y=13

Battelle(/ASTC) and Bruker remain on one.

Bodes well for the 14nm Sofias that will have to compete on price.

Actually my history here is more akin to accurate forecasting of future events and stock price action. Some of you just don't like hearing the truth but the truth is getting better for you guys so what I say lately should be more appealing to hardcore Longs.

We can get on nasdaq pretty easily if we clean up debt situation.

You will need net positive book value i.e. no debt after assets taken into account and a $2+ stock price. When is the last time IMSC saw and held $2 for any length of time ?

Qualcomm is already shipping the 820, it's just that it is not in demand as it runs too hot.

If you use the Intel’s per drawn micron metric, TSMC 16FF+ has ~10% more drive current than Intel 14nm (all other things being equal including leakage and voltage).

Well I suppose when your Finfet transistor is over 50% bigger than Intel's you have got to look for any upsides . TSMC has a bigger problem than Intel in that Samsung's 14nm is denser than its 16FF and already in production at over 70% yield apparently and already taking away Finfet business from it before TSMC has even started Finfet production. I also suspect foundry customers are more interested in price than performance and that depends on smaller and higher yielding die sizes i.e. density where TSMC is last. Still 16FF+ sounds a nice upgrade for TSMC 28nm users for those who wish to stay with TSMC.

I think this was the article that was referred by your post but only oblique references were made to TSMC in it but I suppose it does not take much to set Nenni, the TSMC publicist/advocate, off.

http://www.fool.com/investing/general/2015/04/28/intel-corporation-a-look-at-the-new-xeon-d-process.aspx

I am not saying it's in the works, just that it maybe a by-product of someone taking all your debt away for equity. Conversely they could just swap their own debt for DMRJ's or just do a conventional buy-out. It depends who the new creditor could be, could even be someone like L3 (LLL) who has no ETD at the moment. No sense in ignoring all the possibilities, that kind of hopeful thinking ignored all the downside of DMRJ convertible debt in the first place. Reverse splits are not bad per se anyway especially if you can then get on NASDAQ/NYSE afterwards.

10/1 so the minimum bid price is comfortably met for exchange listing. Or you can hope the price goes to $2+ under its own steam and stay on OTC until then but I suspect anyone offering you $60m+ for shares will have other ideas on that.

Reading the tea leaves it's looking like a debt for equity restructure with someone coming in to pay off DMRJ/BAM and receive cheap discount shares for their effort but which will obviously still be higher than 8c. If this company has no debt it can then go on to Nasdaq/NYSE, after a reverse split, and benefit from the much greater liquidity there.

Obviously it is going to be painful in the short to medium term for the share price as DMRJ unload but in the long run this company will have a chance then to breathe like other companies without major debt do on leading exchanges and as profit eventually should come with McGann's focus on execution rather than the previous Blowduc hot air you can eventually start getting a stock price with nice earnings multiples. There is very little chance of the stock price appreciating or at least holding on to appreciation with the DMRJ 8c sell machine in place but without it you could have a more normal future like other stocks do.

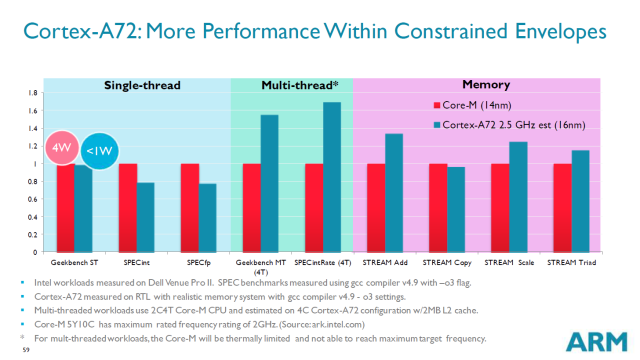

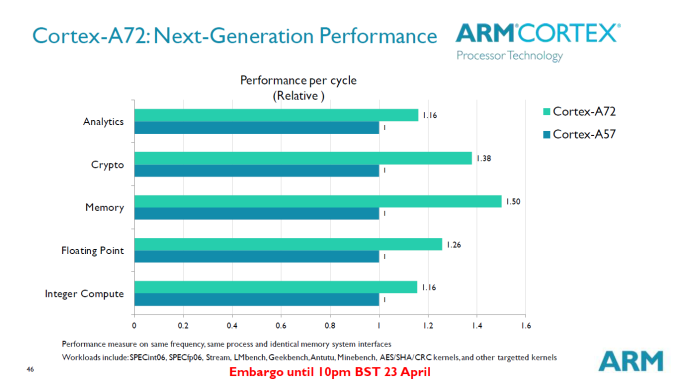

The Core-M is a dual-core within a 4W TDP implying each core has a 2W TDP vs the 1W ARM are claiming for an A72 core. Also 2.5 GHz A72 would only be 55% of the performance of the top-bin 2.9 GHz 5Y71 Core-M which also has the same 4W TDP as the 2 GHz they tested. So the A72 might have slightly better performance/watt than Broadwell Core-M which is not bad finally considering all the bragging ARM has done for years about their performance/watt and yet they still have not produced a server sku of their mobile cpus that match a Xeon LV in sustained performance/watt. Skylake Core-M will also be the competition for A72 and its performance/watt should be greater than the Broadwell Core-M.

http://ark.intel.com/products/family/83613/Intel-Core-M-Processors#@Mobile

http://www.anandtech.com/show/9184/arm-reveals-cortex-a72-architecture-details

They are comparing a top bin 2.5 GHz A72 against a lower bin 2 GHz Core-M and Core-M does clock higher than that, the 2.6 GHz SY70. Skylake will also be the Core-M cpu by 2016 too, not Broadwell.

A72 is only an incremental increase over A57 at the same clock and process size.

Asustek looking to ship 30 million ZenFone smartphones in 2015

http://www.digitimes.com/news/a20150423PD200.html

Asustek Computer has reportedly raised its internal shipment forecast for its ZenFone-series smartphones for 2015 from 25 million units originally to 30 million, according to sources from the upstream supply chain.

Shipments of Asustek's new ZenFone 2-series smartphones will reach two million units in May after their launch in March, indicated the sources, adding that the monthly shipments will rise to 2.5-3 million units in June.

Since Asustek has been increasing its orders to the upstream supply chain recently, it is able to acquire rather competitive prices for needed parts and components, said the sources.

In addition to using chipset solutions from Intel, Asustek has now expanded the chipset sources to include Qualcomm for its ZenFone products, added the sources.

However, whether Asustek is able to achieve its shipment goal for smartphones will still depend on its sales in China, commented the sources.

Meanwhile, Asustek is expected to ship 300,000-500,000 units of its ZenWatch- and VivoWatch-series smartwatches in 2015, the sources estimated.

Intel to launch quad-core SoFIA-LTE chips in 4Q15, say Taiwan makers

http://www.digitimes.com/news/a20150422PD205.html

Intel will move ahead the launch of its 4G chip, the SoFIA LTE, to the fourth quarter of 2015 and the SoFIA LTE 2 in the second quarter of 2016, according to industry sources in Taiwan.

The SoFIA LTE, which integrates a 4G baseband and quad-core Atom CPU, comes after Intel and its partner Rockchip Electronics jointly released a 3G solution, the SoFIA 3G-R, recently.

To help mobile device makers shorten time to market, Intel will have its China-based ODM partner Wanlida and Taiwan's Elitegroup Computer Systems (ECS) offer corresponding reference designs for 6-inch models, the sources indicated.

Based on Intel's roadmap, the chip giant also plans to launch the 14nm quad-core SoFIA LTE 2 in the second quarter of 2016, supporting both Windows and Android OS. Furthermore, Intel also plans to release its 8-core solution, the SoFIA MID T3, in August 2016, the sources noted.

Samsung 14nm is not equivalent to Intel 14nm.

This can be quantified.

TSMC 16FF has 90nm gate pitch, 64nm minimum metal pitch.

Samsung 14FF has 78nm gate pitch, 64nm minimum metal pitch.

Intel 14nm has 70nm gate pitch, 52nm minimum metal pitch.

If transistor area can be compared by the ratio of (gate pitch * minimum metal pitch) you get the following relative transistor area sizes

TSMC 16FF - 1.58

Samsung 14FF - 1.37

Intel 14nm - 1.00

It's obvious that the foundries initial Finfet processes are roughly a half-node larger than Intel's 14nm in density.

Samsung Busts TSMC's 'Monopoly,' Analysts Say

http://www.eetimes.com/document.asp?doc_id=1326409&;

“TSMC's monopoly on leading edge has been broken thanks to Samsung's successful ramp of 14nm with current yields exceeding 70%,” said Mehdi Hosseini, an analyst with Susquehanna International Group. “Samsung has effectively become as good as TSMC at 14nm while offering a much lower ASP per wafer.”

Besides Apple, TSMC’s other anchor client — Qualcomm — is likely to shift orders to Samsung, starting with the Snapdragon 820, Ng said. With TSMC’s dominance in the advanced foundry space at risk, the company may need to cut its wafer pricing premium, he added ....

.... Smartphone slowdown

A slowdown in the market growth of smartphones, the largest business driver for TSMC, has also raised analyst concerns.

“Global smartphone unit growth will be only 14% this year, down from 23% in 2014,” market research firm GFK said in a February 2015 report. “The slowdown forecast for 2015 is due to developed markets reaching saturation.”

TSMC’s revenue from its top-seven customers grew approximately 27-32% annually during the period from 2012 through 2014, representing about 38-44% of TSMC’s total revenue, HSBC analyst Stephen Pelayo said. This was the period when TSMC “caught the smartphone wave” while the global market grew about 30-45% annually, he added.

Pelayo’s analysis of TSMC’s top-seven customers — Qualcomm, Apple, Broadcom, MediaTek, Nvidia, Altera and Xilinx — shows “flattish revenue growth” this year.

Previous big gifts to the Silver Surfer, destroyer of (shareholders) worlds

http://www.secform4.com/insider-trading/1310519.htm

http://www.secform4.com/filings/1001907/0001181431-08-044044.htm

http://www.secform4.com/filings/1001907/0001209191-09-042732.htm

2008-07-18

Option Award 1,100,000 $0.45

2009-08-19

Option Award 750,000 $0.00

and about 412K more up to 2012 and now another free 660K in 2015. So 11% of the company gifted to him by his fellow pig trough directors just up to 2012. He buys another 9% (1,783,746) at only $0.90 in 2012 and now another 3% gift in 2015.

All this shareholder value he has acquired has come purely from the Astrotech business he inherited, absolutely none from his Spacetech efforts over 9 years and also LMT came looking for ASTC to buy ASO not the other way round. Nice 'work' if you can get it.

Insiders have basically given themselves a third of this company (dilution of an extra half of original sharecount) for bumbling along not doing much at all for 8 years until someone came knocking to take the legacy business off them.

The shackles on corporate greed are too little as basically these guys sit on the boards of their companies and give each other big awards. Incestuous circle of greed. The last employee renumeration plan with all these free stock grants should have been rejected but share votes held by brokers are not counted so these excessive greed plans are easily passed.

http://www.gsmarena.com/asus_launches_zenfone_2_in_europe-news-11727.php

It will be even better with this new phone o/s

http://lumiaconversations.microsoft.com/2015/04/01/microsoft-launches-ms-dos-mobile/

Usual buyout numbers, current price +(30-50)%. This rumor makes the rounds every year though so don't believe it until it actually happens .

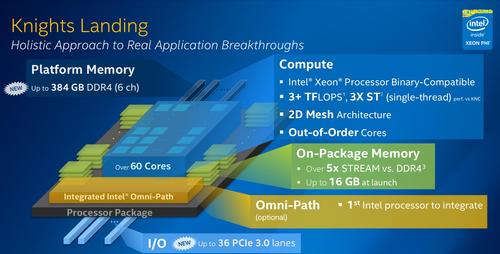

Intel's Xeon Phi to House 72 Cores, System-in-package sports 16-Gbytes

http://www.eetimes.com/document.asp?doc_id=1326121&;

http://wccftech.com/amd-allegedly-merge-samsung/

Samsung is the only semi company that can duke it out with Intel on near equal terms.

Lots of support in the 2.80s

Indeed and it did not need the company to support it this time either. The peak of this support is at 2.85 (currently 202-210 MAs) and there is a lot of volume tied up in these and older moving averages (LMT sale high volume day and the initial run-up to 4) and as long as this support is not broken the stock will always have the ability to bounce back up to 4 easily again. The long-term support is strengthening.

What is your take on the recent acquisition

I have an open mind, show us the money .

Death Cross : A bearish signal generated when the 50-day (short-term) moving average (currently 33.52) crosses below the 200-day (long-term) moving average (currently 33.53).

I an not sure if it really means that much when INTC is so below both averages as the bearish bit has already happened . It's a trailing indicator in this case and not really indicative of what will happen in the future. Obviously earnings will decide where the stock goes next but when the stock price meets the 50 MA will also be important, i.e. will the 50 MA become support or remain resistance. If it becomes support that will arrest the decline.

If it gets to 2% by then it will be a minor miracle.

There will be only one ARM server chip worth keeping an eye out for, Broadcom Vulcan, and that's only because it is a direct copy of its own successful quad-issue quad-threaded XLPII MIPS network chip. Even then it will have to offer some extra accelerator IP to really take some hold as it's not going to beat Xeon in single-thread.

PR Mistake rectified and good selection of words in the PR striking the right balance.

I didn't know IMSC has a twitter account :). Anyway if the PR is still to come then that should spark more buying interest but my general point about PRs still stands as McGann is not big on talking whereas Bolduc was too big on it. There is a happy medium and it should be found for the benefit of shareholders.

This company made a PR mistake in not advertising the fact in a PR that the Morpho complaint was dismissed as only those who follow stock boards and GAO dockets know, after all they put out one when it was raised why not when it is dismissed ? The general market still does not know but this is a mistake that can be rectified next week if they wanted to. Is this the new McGann regime in action, from fluff PRs to no PRs ? I get he is a technologist but this function can be delegated and should be in this case.