News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

mas

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

I think Merrifield is a $4-$5 cost die. It will be sold for more than that initially of course but eventually when Broxton is released that's what it will be selling for. How many of the ARMy's soldiers will it take out at that price ? This is the bigger longer picture Ashraf is totally missing in his attempt to paint it as a stillborn failure.

Because Intel mobile products are late and ARM's products have been more aggressive than anyone expected this is a lot closer now to trench warfare rather than a blitzkrieg many had envisaged on the Intel side. In time that will change as Intel gets more aggressive with its designs on more advanced processes while the ARMy slows down hindered by being maxed out on both its design headroom and process costs. Until then this is reality in 2014 and Merrifield has a crucial future part to play in flushing the opponent's trenches out in hand to hand combat.

Why do we need an often inaccurate low-level test when there are application tests that show clearly Cyclone is nothing special and does indeed fit in the Silvermont/A15 class ?

http://www.anandtech.com/show/7335/the-iphone-5s-review/5

http://www.anandtech.com/show/7460/apple-ipad-air-review/3

The truly ironic thing here is you have often used these other benchmarks in your articles to show how strong Silvermont is  .

.

Logical consistency is missing from your grand picture.

Apple's Cyclone cores are *extremely* powerful - far beyond Silvermont/Krait 400/A15 class.

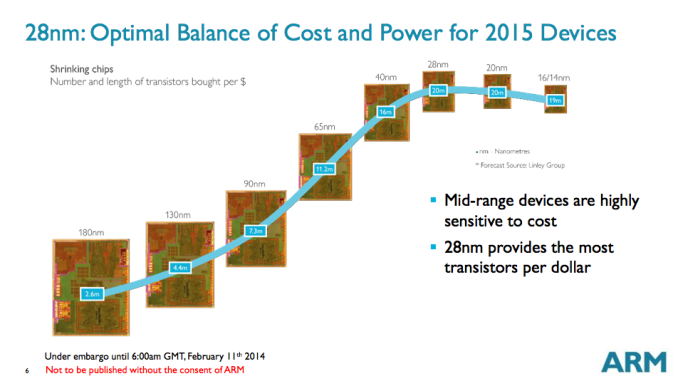

Thanks, interesting slide by ARM which confirms 28nm is the foundry transistor price sweet spot.

p.s. I don't expect the A17 to match A15 in everything so it will not be Silvermont's equal.

Any public links ?

What is A17 anyway, just that rejigged more efficient A15 that Nvidia are using in K1 but renamed ?

I'm not sure why you think that. Intel showed off BYT-T running a 64-bit Android kernel and seemed to be really proud of that.

For market differentiation. Moorefield will undoubtedly have a superior gpu to Bay Trail so make that the premium 64-bit part and get the Android profit on that.

This is why Merrifield won't be able to compete.

Will an octo-core Big.Little and dual-core Merrifield really be competing for the same sockets ? Moorefield with 7260 will be that chip's competitor and that octo-core is still 32-bit so it will never go past 4GB in memory.

It's the repetitiveness of the commentary that grates not the content. We get it, you think Merrifield is a dud but unless you have new information as to why it is and or is not a dud there is no need to repeat this basic theme ad-nauseum.

I suspect Intel will divide the 22nm Silvermonts up in Android with Bay Trail being 32-bit and Merrifield/Moorefield being 64-bit.

It's about the same die size as Medfield yet 2-5 times as fast. Of course according to AE there's no market for such a chip and it should be aborted at birth .

Why release Cherry Trail for tablets?

It will be a smaller faster cheaper Bay Trial that addresses its main competitive flaw (gpu). It will also do considerable more damage to AMD's Kabinis in the Windows space than Bay Trail already has and will debut a full year before Broxton which is really its 14nm architectural successor (tock). Basically the 14nm tick for phones has been cancelled due to time to market reasons and Intel will be going straight from 22nm tick/tock (Silvermont) to 14nm tock (Broxton).

I liked Merrifield until I learned a lot more about when it's actually supposed to be in the market, what modem it was supposed to be paired with, and got some clues as to what kind of design win traction it garnered

So relaunch it as a tablet chip then. Bet it will be cheaper to make (smaller die) and have fewer BOM issues than Bay Trail. A dual-core 22nm Silvermont is worth doing as that is the natural smallest unit of the design and in time I believe will sell more than the native 22nm quad-cores. Consider it a smaller faster updated CLT+ and that chip is ending up everywhere these days. Again look at the possible positives and you will be getting your quad-core Moorefield not long after when XMM 7260 is actually available to take advantage of it. A sku foundation of x86 mobile chips has to be built and it's better that the dual-core is native for cost reasons rather then harvested quad-cores.

No.

How do you know it has not shipped already to OEMs ? What if it is waiting for the 64-bit software which coincidentally will be a bonus to what was originally planned ? Also when you take the clockspeed of Silvermont into account it is in the same league as those other dual-cores. I am not sugar-coating anything, just writing with the sober realism that a few more decades observing this industry has given me.

Merrifield has not been officially released yet, you will have to wait for those sweeties until MWC.

and it has the very real potential to do exactly what A7 did.

What, prove that a dual-core mobile chip like A7 and Merrifield and Nvidia's Denver still have a mobile future ? Frankly you are displaying all the petulance of a child who has not had a recent sugar fix and your posts are embarrassing to read in their trivializing simplicity. You are no real analyst.

for a nice Exynos?

Ah yes the big little octo power hog CLT+ and Merrifield are far better suited for mobile products in real day to day usage.

Samsung is not the target, it's the fab-less device-less ARM licensees Intel is gunning for as a merchant chip provider. Samsung is a partner (like Apple) and has already shown a willingness to use Intel mobile products if the price is right. Qualcomm is a special case as the comms leader and will take more time to take down or at least degrade.

If anything, X86 = RISC, ARM (via Samsung/Qualcomm/Apple) = X86 in this analogy.

No it isn't. Intel did not release the best performing products in servers for many years and I would argue even now the Power series is still the King in specialized enterprise server applications. What it did do, as it is doing now in mobile first in 32nm and then in 22nm, is build the most compelling performance/price products year after year until the competition was eventually suffocated. None are so blind as those who will not see and I'm afraid you are only interested in quick clean kills to see the bigger picture and the x86 foundation that is being slowly but surely laid in mobile.

Performance/power/price and it is selling in many volume products.

Your mobile expectations were always unrealistic to those of us who saw how slowly but steadily the server battle was won.

Clovertrail+ is a successful competent product and finding itself in more and more sockets but of course only the glamor sockets matter to you.

Do you think Merrifield will be tied to XMM 7160 forever ? I am telling you now, you will look back on all these Merrifield slurs in years to come and be embarrassed.

unfortunately the rest of the world

This part of 'the rest of the world' is not where the volume in phones currently is.

If Moorefield is in the Nexus 8, is 64-bit and has a great gpu you will be the first one drooling over it. It's not spin just Intel reacting to recent competitive events and regrouping and highlighting the advantages their products do have.

You can't sell a dual core A15 class chip into modern large phones in 2014 and expect to make money.

You still don't get it even now, Merrifield's strength will be its ability to be in the slimmest and lightest of phones not the largest yet still be fast and frugal on battery consumption.

Reading between all the lines it appears to me that there will not be any 32-bit Android 22nm Atom products only 64-bit ones. One way to overcome your legacy 32-bit issues .

Apple probably got the best of the ex-DEC team that was at AMD and a few ex-DEC from Intel too. Building an ARM Alpha was not that difficult for them . Notice AMD could not have come straight out and said we sacked Meyer because our current brand new design 32nm flagship product is no faster and sometimes slower than our old 45nm flagship product but that was the inference I drew especially when no new mobile designs appeared to justify the stated reason.

Meyer as the processor chief had over 10 years to find a decent architectural successor to K7 because K8 and K10 were really just derivatives and he failed abysmally and he should not have had considering his pedigree. There were a couple of K9s it seems which were canines and never got released. I really don't understand it but oh well, Intel's gain.

re: Tri-cores, they did to a certain extent later on as they did appear eventually but just not as a separate die only harvested ones. Notice also that AMD's most highest asp successful products of recent times were the native 45nm 6-core K10 Stars skus so I was obviously on the right lines with my native multiples of 3. From K10 they should have copied Intel once again in their lives and went wider issue and added SMT rather than go off on their own bizarre cluster-based tangent to a Bulldozed dead-end which by default left Intel unopposed in the x86 high-end. On such subtle technical choices are companies made or broken and Moore, Glew and ultimately Meyer as the highest technical lead sure broke AMD. This is the real reason he lost his job IMO as AMD's mobility strategy, the excuse given, has not changed really since he left.

A lot of ifs there . Now remove all the contra-revenue in 2015 and how are we looking ? The contra-revenue is masking a margin improvement this year. What about the further margin improvement Broadwell will bring, Cherry Trail ?

I agree that Ashraf's sole emphasis on smartphones as indicative of whether INTC has a future as a good stock or not is too one-dimensional and blinkered and too long term to really matter for now. What really matters in the short to medium term is what Intel does in the combined PC and Tablet market and I don't see much wrong there apart from still having to fix some netbook orientated legacy issues with Bay Trail.

Broadwell-Y, Cherry Trail, they matter much more this year as new products than Merrifield or Moorefield.

You make good points but sometimes companies read public/private constructive criticism of their actions and then act on it. When I was an AMD investor I had many strategic/tactical e-mail conversations with Hector Ruiz (I think I might have been responsible for a sku or two from his comments and a presentation theme they once gave) although he and Richards never fully realized the ELE event I was trying to point out that Core 2 was and the unconventional architectural steps they needed to take to counter it. In the end Dork Mayer got his way and Bulldozed the company and I moved on.

Another CEO (of ASTC) basically arranged a phone conversation with me after I publicly berated him on several points (the major one being balancing the need to control expenses while developing new revenue streams to still allow profitable quarters to occur from time to time with his fixed core business while not engendering future developments) all of which he later implemented in time and his stock price has since recovered.

I know what you are trying to say about basically lumping it or leaving but no company's people have a monopoly on good ideas and a smart pro-active investor can influence the direction his company takes. Ashraf is probably too abusive and sarcastic with his comments (the young internet generation) which blunts the message but he still makes valid observations occasionally and the deal for him is to stop stewing about it after he has noted the flaws and try and think of bright ideas to then offer to the company he still wants to be invested in and he has the perfect journalistic platforms to do so.

... as chipguy has been predicting for years. eom

re:Vend, for a company that has never made a profit, has negative tangible assets, only has $2m quarterly revenue and has a going concern note in its last 10-Q a $123m market cap (double ASTC's) is some achievement of hope and inflation

http://biz.yahoo.com/e/131120/vend10-q.html

http://www.sec.gov/Archives/edgar/data/1526689/000155724013000404/vend_10q-sept2013.htm

p.s. ascending chart does look good for the moment though with support at 2-3 although how long that will last when heavy dumping occurs is anyone's guess. Seems a grossly inflated stock to me but hey if no-one's complaining .

It is to the author's credit that he allowed Intel to interject a few cold hard facts in there before Feldman went on his big fairy tale telling that had very little to do with anything truthful on Planet Earth either past, present or future.

I don't think you fully appreciate the significance of this event, it fully validates the spectrometer technology

Huckleberry Investments now own 2,178,521 shares (11% of company)

http://secfilings.nasdaq.com/filingFrameset.asp?FileName=0001062993-14-000476.txt&FilePath=\2014\02\04\&CoName=ASTROTECH+CORP+\WA\&FormType=SC+13G&RcvdDate=2%2F4%2F2014&pdf=

http://secfilings.nasdaq.com/filingFrameset.asp?FileName=0001062993-14-000472.txt&FilePath=\2014\02\04\&CoName=ASTROTECH+CORP+\WA\&FormType=SC+13G%2FA&RcvdDate=2%2F4%2F2014&pdf=