News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

ls7550

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Hi Tom

The Buffett indicator is up at 148%

https://www.gurufocus.com/stock-market-valuations.php

He is talking about what you would normally do after a stock sale Or purchase. You need to adjust the parameters for the sale

Then I'd increase my investment control to 8333 to re-start the program. I'd also increase my cash balance to reflect the 833 sale, so now my cash balance is 3,333 and my next minimum transaction is 1/3 of that making it 1100. This re-starting is not mentioned by Mr. Lichello, but I've found that it is useful to track my portfolio upwards.( I've been dismayed to have been using A.I.M. for AAPL for instance only to build up a large cash account, but see the price of AAPL continue to soar leaving me with too few shares to really feel good about it.)

about restarting AIM after a sell

If you use the individual AIM's cash figure and pulled a Vealie, then that ensures you keep it more aligned to your target weighting in that asset. If you used the wider total cash pot reserve level then its a means to in effect pull in cash from elsewhere to add to that asset (increase its relative weighting).

No right or wrong answer. Similar to do you reinvest dividends into the stock or add them to cash, and also add cash interest to cash .... or not.

A interesting variant for instance is to consider dividends and cash interest as the inflationary offset (which tend to be more linear compared to stock price increases offsetting inflation), and count stock gains as your (more irregular) 'income'. In which case your AIM might totally exclude dividends and cash interest when recording the AIM values, but used to add stocks over time (deploying accumulated combined cash interest and dividend payments recorded separately into AIM stock and cash in the proportions of the AIM's stock/cash weightings at the time). And accumulate AIM sells ... into a collective "disposable income" pot.

Based on accumulated stock price (SPY dividends used to buy more SPY shares; VFISX dividends/interest used to buy more VFISX (cash)).

AIM X-HI (90)

Buffett proposes cost averaging into stocks over a decade or so. He also advocates 90/10. He in effect bought a 'index' of stocks by buying relatively down at the time individual holdings.

When you look at the range of returns investors achieve there is massive volatility. Buy at the peak, end at a trough and you might barely see a break even in total returns after inflation, costs and taxes. Buy at the trough, end at a peak and the rewards can be out-of-this-world.

Makes you wonder if Lichello's AIM-HI should perhaps been 90/10 with Vealies at 10% than his 80/20 choice. Repeated cost averaging in and out that 10% cash across a 30% or 40% range, along with selective purchases (Value) and timing is more inclined to broadly average not having bought and locked into the worst possible time.

Hi Toofuzzy

With the new tax law it may make sense to swap houses with your neighbor and rent each others houses. Deduct 100% interest, taxes, maintainence, but also take depreciation. Then you can take losses in the early years against other income and also take full standard deduction.

If a house is a large chunk of your wealth then yes, too little disposable income, in effect you're spending all your "wage" on rent.

Compare house prices + gross imputed rent to stock + dividends and they can be broadly similar. If I sell a home and invest in stocks the share price appreciation would ideally match house price increases and the net of tax dividends would ideally cover the gross rent of a similar sized/location home. Even if that were the case however there's the loss of liability matching. If stocks and in particular dividends decline, my rent likely wont.

Depends on geopolitics, but here in the UK generally its better to liability match (own) than not. But not to the extreme, where you're all-in on that alone and illiquid home value rich, cash/income poor. Our taxes are lower as well, of the order $2800 on $1.7M

Hi Toofuzzy

During the years you were pulling cash out of your accounts to live on wasn't almost impossible to build up too much cash?

Hi UT. Good to see you're keeping well.

in 99% of the tests he ran, Buy and Hold beat AIM.

22% 2MCL (2x FT250 UK midcaps (UK has a tendency to have above average dividend yield (Value) and our midcaps market cap sizes are comparable to US small caps ... so I see FT250 as being a form of Small Cap Value type holding). 33% BRK-B, 44% Gold. That lot approximates to a third each in SCV/BRK/Gold and spans GBP, US$ and global currency i.e. I'm tending towards neutrality this year (US$ could swing either way, possibly a sizable move, so could be stocks up/gold down or gold up/stocks down. As could GBP be volatile (Pound up, SCV down or vice-versa)).

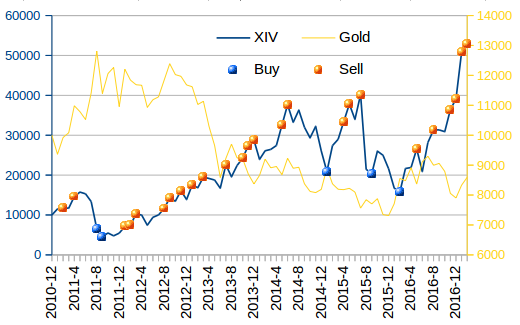

Buy/hold for the calendar year (slow AIM) - not rebalancing leveraged ETF's often has the tendency to attenuate declines, amplify upside. XIV has had a great couple of years (benefits when volatility is relatively low), I'm guessing that will change this year (bad year for XIV, higher volatility than the last couple of years).

Moderately defensive without giving up on upside potential ... having a character something like https://tinyurl.com/ybmqq7cv

The situation is not totally clear yet, some brokers still allow you to buy US ETFs, other brokers have implemented a buy lock on those ETFs.

We have to see how it will develop. Indeed a position in BRK is now more attractive; BRK is not a packaged product like an ETF according to the rules.

I assume the blue line is the XIV+ portfolio and the red line is a general index?

re-balanced once or twice a year?

2017 has been a very generous year for most investors

Hi Neko

Kevin McDevitt's your man.

30 original stocks, just bought and held since 1935. Now down to the low 20's (large chunk in BRK-A holdings and even larger in XOM (around a third of the portfolio value combined)).

the only way that new stocks could enter the portfolio would be through spin-offs or mergers and acquisitions. On the other hand, a company would only be sold if it suspended its dividend or was in danger of being delisted or going bankrupt.

Hi Tom

Oracle of Omaha warns equity investors are "Playing with Fire" due to his key overvaluation metric nearing an all time high:

"Buffett indicator is the total market capitalization of all U.S. stocks relative to the country’s gross domestic product. When it’s in the 70% to 80% range, it’s go time. When it moves well above 100%, it’s time to tap the brakes. The metric sits at almost 139% at the moment, which is getting awfully close to the record 145% it hit during the peak of the dot-com bubble in 2000, the only other time the number has been this high"

Hi SFSecurity

... article that argues that 2X ETFs are a better deal than 3X.

http://ddnum.com/articles/leveragedETFs.php

I'll have to re-read it to see...

This article has not proved that the optimal leverage is about 2. It has just demonstrated that 2 has been good in the past. The future may be different.

Free to access TooFuzzy. You do have to open up noscript to see all of the charts however.

RE: LETF's

I buy and hold 'em, and have done so for a number of years now with a substantial part of my total 'stock' portfolio.

When compared in equal capital amounts invested in a 3x and 1x, picture it as not a expectancy of providing 3x the return over the mid to longer term, but rather more broadly like the same return, but 3x the volatility along the way.

The manner in which I use them is to drop a third into the 3x of the amount I otherwise would have invested in the 1x. Primarily for taxation benefits.

For the remainder two-thirds 'bonds/cash' I prefer a barbell of two extremes, stocks and gold 50/50.

With 2x you can get away with rebalancing back to target weightings once each year or so. With 3x you should rebalance more frequently, 6 monthly is fine with me

See here

Thru, threw, through ?

Don't make me spell corectly, it makes my head hurt!

That is why I worked with numbers.

Hi Toofuzzy

I was only a tax preparer for 16 years

You need to have LOTS of cash available for the drops in price

Leveraged ETF's scale up volatility.

Whilst they 2x or 3x scale (whatever the choice of leverage) the daily price move, over time they tend to realign to similar overall reward as 1x (non leveraged), but with much higher volatility along the way.

link

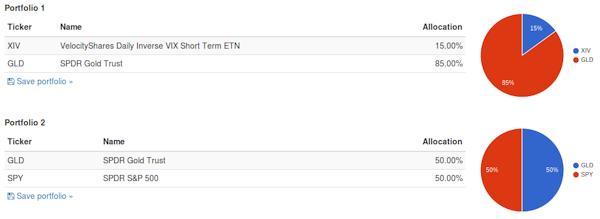

Note that 15% XIV and 85% gold is a proxy for 50/50 stock/gold (XIV acts similar to a 5x long stock, stock/gold 50/50 acts like a volatile bond). The above used quarterly rebalancing

AIM likes volatility. For AIM settings of 15% stock (XIV), 85% cash (gold), monthly reviews, 5% minimum trade size, 10% SAFE. 85% Sell Vealie, 85% Buy Vealie ...

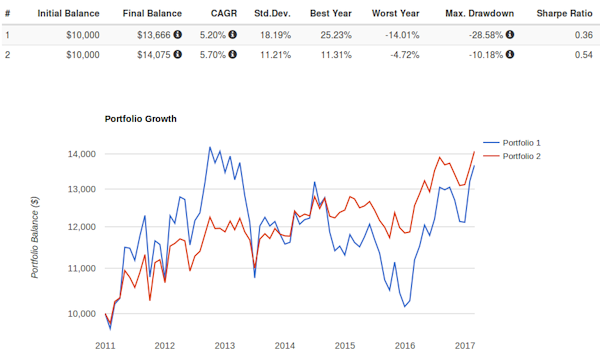

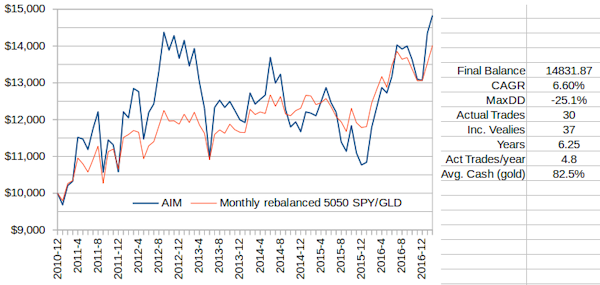

AIM over that period bettered each of monthly, quarterly, semi-annual, annual and band based rebalancing.

Hi Tom.

Both AIM and Modified Duration based total rewards broadly compared to 100% buy and hold (when using gold as 'cash'), both averaged similar amounts of average cash reserves, but arrived at those averages via distinctly different routes (AIM was the more aggressive in its weightings)

Both bettered the rewards from constant weighted (50/50) i.e. found the more appropriate overall weightings compared to trying to pre-guess that in advance as per constant weighting.

Of the two modified duration had the better r-squared (tracked the broader trend line more closely).

Both are more recently indicating 50% (MD) to 53% (AIM) cash reserves as being appropriate for the current start of year weighting level.

Modified duration obviously more closely reflects yields

That longer term chart provides a indication of just how historically exceptional the big declines of the 1970's/80's due to massively rising yields (declining prices) were, resulting in the subsequent 1980's onwards relatively good benefits of declining yields (lower yields, higher prices).

Both MD and AIM have you tending to add-low/sell-high (which constant weighting also has a tendency to do), and avoid the tendency to profit chase (greed/buy-high), capitulate (fear/sell-low) ... which is a significant failing of many investors (some don't even achieve inflation pacing total returns and would have been better just buying T-bills). Both tend to provide better overall risk-adjusted reward (similar reward with less than 100% stock exposure volatility/risk). AIM however has the edge in just using price as its input and as such is less prone to distortions due to yield/bond interest rates - that can be distorted by the likes of taxation or policy (QE/Central Bank manipulation). For instance past policy in the US I believe was to tax dividends higher - resulting in lower dividends being paid, more being retained.

Its nice to see multiple measures derived different ways acting as confirmation of each other. Most seem to be suggesting moderate/average risk, neither particularly expensive, certainly not cheap, confirming that taking some of past profits off the table to build up cash reserves has been/is a reasonable recent stance.

Regards.

Clive.

PS - One thing I still struggle with is despite AIM's more aggressive approach, for instance tending to deploy all of reserves at times (constant weighting and MD are much less prone to exhausting all of reserves), and at apparent lows, the overall rewards don't seem to reflect that aggression (risk).

Allen, another valuation measure is to use Modified Duration, which for stocks can be approximated as price / dividend

With Bonds when interest rates are high you want to shift up towards longer dated holdings as the price is relatively cheap/yields are relatively high. When interest rates are low shift to shorter dated. Modified duration for stocks is similar. If dividend yields are down at 1% then prices are high. If dividend yields are 10% then prices are low.

You can use Shillers yearly data for price and dividend value to identify a yearly price / dividend figure (you have to limit between 0 min and 100 max as some values will fall outside of that). And then use that as a guide as to the amount of 'cash' to hold (rebalance to once/year).

Hi Allen

I cheat and use Robert Shillers historic data. The third link on this web site provides monthly data http://www.econ.yale.edu/~shiller/data.htm (Data worksheet, column H for real values). They change each month as its rebased to the most recent data values.

Drop that into my spreadsheet (extending the number of rows as required) http://tinyurl.com/qygn3bm

... and you'll have a copy of what I use.

Thanks for the alternative suggestions.

The most recent inflation rate is a bit of guesswork involved if you want to bring it right up to date. Mostly I use that as a overall vWave type alternative guide. For instance if instead of 'cash' (bonds) you hold 50/50 stock/gold barbell as a bond proxy, then halve the AIM indicated cash % = gold %.

Use that as a guide for once yearly AIM indicated cash % to rebalance to at the start of each year (stock and gold % weightings where gold % = half the AIM indicated cash % figure) and since 1896 (using US stock total return for 'stock', and total portfolio value currency converted to GB Pounds (my local currency)) yielded yearly averaged figures of

Buy and Hold

Avg 12.1

stdev 20.1

min -32.6

max 65.8

CAGR 10.3

AIM timed

11.4

16.5

-26.4

65.8

10.2

Constant 75/25 (i.e. if 50/50 stock/gold is considered as being 'bond' then that's a 50/50 stock/bond type holding)

10.6%

15.4%

-24.3%

51.7%

9.5%

Which is indicative that AIM timed produced near the same overall annualised total return/reward to 100% stock buy and hold, had lower downs (min), similar up's (max) and did so with lower volatility (stdev). (Lower yearly average (mean), lower stdev, yielded comparable annualised compounded growth rate (CAGR))

Averaged 20% gold over the total period i.e. AIM steered to that naturally, compared to a default 75/25 constant weighting that yielded a lower 9.5% annualised reward. (Note AIM initial settings where 50/50 stock/cash which = 75/25 stock/gold (MTS and SAFE were both 10%)).

The charts I posted earlier in http://investorshub.advfn.com/boards/read_msg.aspx?message_id=128821849 provides a indication of the overall amount of gold being held over time i.e. half the cash % amount of weighting. So broadly ranged between 0% and 35% extremes. Reposting that zoomed-in chart I posted earlier

you can for instance see how at the late 1990's peak 70% cash (hence 35% gold) was being indicated. As of the start of 2017 year 53% cash (26.5% gold) was being indicated (contrasted for instance with 36% cash (18% gold) being indicated at the start of 2010).

Total overall nominal return comparison for that once yearly rebalance approach looked like

In short, AIM timed produced near-as the same reward as 100% stock buy and hold, but holding a average 20% gold and did so with less risk (volatility) i.e. better risk-adjusted reward. Since legal tender gold coins in the UK are tax exempt in net terms it would also have been more tax efficient (not so in the US however as (I believe) 1. at times it was illegal to hold gold and 2. the US applies relatively high taxes to gold).

Clive.

Whoops. Just seen your posting Allen

If you are using an inflation adjusted S&P 500, why then do you say that dividends and cash offset inflation? Why is it not one or the other, not both?

RE: Signalpoint

Guess it is a country block as the States side guys seem OK whereas us the other side of the pond are being blocked

Tried turning uBlock Origin and NoScript off, but still the same

Is anyone else hitting a error when visiting http://www.signalpointinvest.com ?

Gold is like a cross between undated zero coupon inflation bond and long volatility (stocks are like being short volatility)

Takes a bit of thought to get your head around this group of comparisons to see that though https://tinyurl.com/jyjhdsm

From a casual glance the more recent situation looks like it was gold up because long dated TIPS were up ??? (chicken and eggs (perhaps the other way around))

50/50 stock/gold is a short and long volatility barbell ... which is like a volatile bond bullet. Instead of 50/50 stock/bonds for instance 75/25 stock/gold might be used as a more volatile but perhaps more tax efficient substitute https://tinyurl.com/z2sah75

One final pair the first shows how stocks are like short volatility http://tinyurl.com/z44wc5c ZIV sells 5 month VIX futures and acts similar to being a 3x stock. This second http://tinyurl.com/jcd65fh uses XIV that shorts 30 day VIX futures and is more like a 5x long stock. If instead of allocating 20% 5x, 80% bonds in order to track 100% 1x long stock, you substitute in 50/50 stock/gold as the 'bonds' then if the choice of stock held pays no dividends nor does XIV nor does gold ... then you have a no dividend type long stock position - handy if otherwise dividends might be taxed relatively more than capital gains.

The growth charts in the above links are best viewed when the log scale box is ticked/checked.

Clive.

If the wealthy aren't spend all that much perhaps they've been advice that the bull market is getting long in the tooth

Re: v-Wave getting nervously high

Belated best wishes to all for the New Year.

I don't frequent here much nowadays ... find the layout (excessive ads) displeasing ... but you and yours remain in my thoughts.

Clive

Hi Neko

Lexcx is a mutual fund that has had zero turnover since its inception. In strategizing over its use . In a taxable account I assume there would be no capital gains . Since nothing is ever sold except for redemption of shares as a person sells out their position. The dividends I assume are taxable .

I have come to the conclusion that I don't want to beat the market as much as I don't want to be beaten by the market.

Chase has a fund of funds. They are always selling and buying . It is their conservative allocation fund. It is a fund of funds. Do they make money by constantly buying and selling mutual funds.

My friend had shares in it. He saw little advancement over its value.

Bogle recommends the ultimate in buy-and-hold investing: a completely static portfolio. He would buy the 50 largest companies in the S&P 500 and then never buy another.

The next-to-the-top line is the original Dow 30, using a price-weighted index, just like the current Dow 30 uses. The only changes in the next 80 years are companies getting bought or dying. That "Original 30" gives us an annual return of 9.6%. Just 0.7% a year, so you might think, not much difference. But if you start with $100 and compound it for 80 years, that 0.7% becomes a quite large differential. With the Dow 30, your $100 would have grown to $96,993 as of December 2008, but the Original 30 would have grown to $161,603.

And there is an even bigger differential if you simply equal-weight the components rather than use a price-weighting methodology. Your $100 grows at a 10.4% clip and becomes $272,554, or almost three times the actual Dow 30.

I suggested that long dated treasury's were a good buy ages ago. Some suggested otherwise :) With the EU printing 1 trillion/Euro's year with no end in sight (80B/month) ... money is very cheap. So much so that some even pay to lend to treasuries (why would a counterfeiter borrow money when they can just print some off themselves to spend).

In the context of legal counterfeiting ... the printer gets to spend the money they print at the expense of all other money in circulation being devalued a little. They're not going to go broke, so in lending to them you're certain to get your money back, albeit that money has less purchase power when it is returned to you including interest payments (negative real yields).

With other assets the risks are much higher. A rise in interest rates would have investors re-valuing assets at much lower prices. "Fixed" income held to maturity have a definite outcome - known at the time of purchase.

Certain groups are obligated to hold treasury's - no choice and have to continue buying no matter what the price.

If the world were comprised of two islands, EU and US, and EU is printing money like crazy to spend, then US will suffer and see its currency appreciate relative to the EU. To counter the US has to print at a equal rate ... which negates the otherwise benefit to the EU. Brexit has helped the UK as otherwise the Pound was strengthening considerably against the Euro, resulting in more (cheaper) imports, fewer (expensive) exports. Realigning has negated that 'cost'. IIRC the new President will have a handful come the end of the first quarter 2017 as that's when I believe the US emergency measures come to a end and the debt ceiling will again come to the forefront. Remember last time when Fed workers were potentially not going to be paid, concerns about a default ....etc that ran right up to the wire. Well 2017 and the new President will again have to 'address' that. Many of the current big-names in the EU will also be gone come the third quarter of 2017 (elections), replaced by current unknowns who will have their hands full in addressing issues. I just hope not too many extremists rise to fame.

Pre 2008 and banks took risks on a heads win, tails win basis. Speculate and win and pay themselves massive bonuses. Speculate and lose and taxpayers bail them out. The same has been scaled up, but instead of banks its now states. Who will bail out the states that are printing to buy things (at relatively high prices), if/when the avalanche of a rush for the exit (sell) occurs. It only takes one state to decide enough is enough for such a avalanche to potentially occur (earlier to the door, the less the negative impact). UK printing to spend was spent on buying up older higher cost debt it had issued, and replaced it with more lower cost debt. Responsible central banking. Others such as the EU are irresponsibly borrowing to spend, buying corporate (speculative) assets.

Buying TIPS that promise to return your money in inflation adjusted terms at some fixed future date, less some costs (negative real yields), even at 2% yearly cost is potentially a good asset if all else is crashing and burning.

That all said and its been a good year for long dated UK treasury bonds, up over +30%, so relatively speaking not the best of times to be buying (that was last year). I suspect next 12 months will see a good year for stocks, relatively poor year for Treasury's ... at least from a UK perspective. But with the likes of the first quarter of 2017 US debt ceiling issues providing some buying opportunities along the way.

Subject to the usual unknowns of course. Remember that when Germany was in difficulties the Greeks amongst others helped bail them out. More recently Germany has irresponsibly lent to the Greeks who have irresponsibly borrowed to buy German goods. Since that has peaked, instead of writing off debt as the Greeks did for the Germans the Germans have two fingered the Greeks. Neither side is fully to blame, neither side is clean. The Greeks for instance had made paying tax voluntary, and introduced the likes of retiring at age 50, along with 3 months of summer vacation periods...etc.

Helicopter money looks to be a good choice. To date most of technological advances such as robotics working 24/7, replacing millions of menial work, hasn't been for the benefit of the collective, rather to the benefit of very few. That wealth needs to be redistributed. 1% billionaires, 99% in declining living standards/overcapacity has to be addressed. Otherwise we'll continue along the lines of the likes of where China supply steel at below cost, simply on the grounds of over-capacity/low demand where selling at any cost is better than not selling at all. Increasing demand to match/exceed supply is the way forward, which can be induced by sharing money around more fairly that generates demand when otherwise demand would have remained low.

1980's to noughties had the benefit of tail wind, interest rates declining from 15% down to more recent near 0% levels. Either there will be a soft landing where interest rates remain near 0% for a prolonged period of time, or there will be some crisis like the 1970's that sees inflation/interest rates soar into double digits and we start the 1980's/noughties type cycle all over again. We're not on a gold standard/peg, so none of the 1933/34 years when gold was pegged and compulsory purchased at around $20 levels to a year later ramp the peg price up closer to $40. That sort of thing/trick had been used in the past - Henry VIII was known as Copper Nose as the prior silver coinage that he continued to mint but with copper mixed in, with wear had his image of his face on the coin showing the copper through.

We still have gold coins as legal tender in the UK, a gold sovereign has a legal tender value of one pound, not that you'll get any in your loose change as the metallic value is worth much more. A few years ago when copper prices soared the public had to be reminded that it is illegal to destroy/melt legal tender i.e. when copper pennies copper value was worth more than the penny legal tender value. As a guide the Pound dates back to the 700's when a Pound was a Saxon Pound weight of silver. The Pound nowadays buys nowhere near the same amount of silver.

Some wise individuals across time have suggested diversification is the key. Own some land, a business, keep some cash safely and some gold/precious. Diversification isn't just different stocks. CISCO for instance list on both the Mexican and New York stock exchanges, buying some of each appears to be more diverse than one alone, but is the exact same in reality. Open up that more widely and what might appear more diversified can amount to being no different.

Instead diversify ... and exploit the volatility in the differences in a positive manner ... take from those that trade the same assets in a negative manner. Or as Tom puts it, buy from the scared, sell to the greedy.

Communal

Remember that I'm fond of leveraged holdings, so at 100% long stock I can be sitting on 67% cash in hand with a 3x (80% cash in hand with a 5x).

in one of your posts you reference "ETF/ETP/ETN". What is ETP?

interesting charts and argues strongly for delayed AIM buys as the market heads down

There's always the option to borrow cash

40% 1x, 20% 2x, 40% cash is no different to 80/20 stock/cash. Shifting that to being 40% 2x, 60% cash is the exact same (near-as) :)

Comparison

Hi Toofuzzy

I take issue with your love of 80/20 Aim