News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

zsvq1p

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

OK.. Now looks like all the ERX gaps filled.. Time to get back into ERY..

Gap filled.. Lets see how it goes.. ERX has some gaps to fill.. might be a good time to get out.. reload when ERX gap fills..

Kinda a bounce early.. I got stopped out of ERY..But did well on it.. .. I do agree with you on ERX.. ERX has some gaps to fill too.. One thing I know 100%.. Energy stocks will recover. Just predicting when!!! lol..

I do believe the gap above is $35 is going to fill..

Oil Drillers' Credit Lines to Shrink as Banks Revalue Assets

by Asjylyn Loder

September 23, 2015 — 10:09 AM EDT

Total Cuts Oil Output Target as Prices Expected to Stay Low little line above headline

a U.S. Crude Oil Inventories Fall 1.92 Million Barrels little line above headline

Oil producers in the U.S. are about to see their credit lines shrink, just when they need the money most.

The latest round of twice-yearly reevaluations is under way, and almost 80 percent of oil and natural gas producers will see a reduction in the maximum amount they can borrow, according to a survey by Haynes and Boone LLP, a law firm with offices in Houston, New York and other cities. Companies’ credit lines will be cut by an average of 39 percent, the survey showed.

"There’s going to be a reduction to the majority of these credit lines," said Neal Dingmann, an analyst at SunTrust Robinson Humphrey Inc. "It’ll make a lot of these companies reduce a bit more on spending."

In many cases, banks have first claim on assets in a bankruptcy, and the size of a loan is tied to how much an oil producer’s acreage is worth. To reduce their risk, lenders reduce credit lines when prices fall. That’s helped keep loans backed by oil and gas properties some of the safest bets around, even amid the worst oil crash in almost 30 years.

Reserves, Price

At bottom, the math is pretty simple. The amount banks are willing to lend is based on two things: the size of a company’s reserves, and the price of crude. Multiply the number of barrels by the price, and that’s the value of a company’s oil prospects.

In practice, it’s not that easy. Counting barrels trapped thousands of feet below the ground is by nature an uncertain business. And prices are always moving. Crude has declined 51 percent in the past year, and slipped 3.1 percent Wednesday to $44.94 a barrel.

To protect themselves, banks underestimate both reserves and prices. First, they attribute very little value to wells that haven’t been drilled yet, unlike equity investors who see undeveloped properties as growth potential. Banks also don’t lend against every barrel credited to producing wells. And lastly, they assume oil will sell for less than market prices.

During the boom, credit lines went up along with prices. With the oil and gas assets securing the loans, banks were able to extend low-interest credit to junk-rated companies that consistently spent more money than they made. The frenzied pace of drilling fueled the expansion of reserves, meaning more collateral for even bigger loans.

Lower Prices

Now the situation is reversed. Lenders are using $48 a barrel to value assets in the third quarter, down from $77 at the end of last year, according to a quarterly bank survey from Macquarie Group Ltd. And reserve growth has slowed because companies are spending less on drilling. The redetermination, which takes place around April and October, comes as investor appetite for energy company debt is fading.

Whiting Petroleum Corp. may see the maximum amount it can charge on its credit line lowered to $3.75 billion from $4.5 billion, James Volker, the Denver-based company’s president and chief executive officer, said in a Sept. 9 presentation.

The banks also have regulators looking over their shoulders to make sure they’re not taking undue risks. The Office of the Comptroller of the Currency, which oversees 1,620 financial institutions, has been examining oil lending standards since April as part of its annual review into shared loans. Banks received the results in mid-June, and a report is scheduled to be released as early as this month.

Producers that defaulted on their debt from 1995 to 2012 still repaid every cent of their $1.27 billion in reserves-backed loans, according to a 2013 report from Standard & Poor’s.

The biggest risk is to borrowers that have already tapped their credit lines. If the borrowing base is cut to less than it already owes, the company will find itself abruptly facing a large repayment.

"The banks always have a second way out," said Tom Watters, head of S&P’s U.S. energy team. "The first way is to get paid back. The second way is to have the collateral."

Hard to pass up a 8% gain in a couple days..

PERF chart

http://stockcharts.com/freecharts/perf.php?$RIENG,erx

Mod it and see it was 3 x's the index... at any time.. look at 2 days..

select the bar and see..

This ETF leverages the index to achieve 3 x(daily) the index... which are companies in the energy area.. not oil. Many oil companies are in trouble because of low oil prices.

The market was down yesterday and sure people sell those energy stocks too.. Its jitters..

Fact sheet: http://www.direxioninvestments.com/wp-content/uploads/2014/02/ERXERY-Fact-Sheet.pdf

Russell 1000® Energy Index ("Energy Index").

S&P Energy Select Sector Index

The index is provided by Standard & Poor’s and includes domestic companies from the energy industry. It is developed and maintained in accordance with the following criteria:

Each of the component securities in the Index is a constituent company of the S&P 500 Index

Each stock in the S&P 500 Index is allocated to one and only one of the Select Sector Indexes

The Index is calculated by using a modified “market capitalization” methodology, which is a hybrid between equal weighting and conventional capitalization weighting with the weighting capped for the largest stocks included in the Index.

This design ensures that each of the component stocks within a Select Sector Index is represented in a proportion consistent with its percentage with respect to the total market capitalization of such Select Sector Index. One cannot directly invest in an index.

Index Sector Weightings (%)

Oil, Gas & Consumable Fuels 81.49

Energy & Equipment Services 18.51

Data as of 6/30/2015 is subject to change at any time.

Top Ten Holdings %

Exxon Mobil Corp 15.77

Chevron Corp 12.44

Schlumberger LTD 7.67

Kinder Morgan Inc 4.47

EOG Resources Inc 3.94

ConocoPhillips 3.76

The Williams Cos Inc 3.67

Occidental Petroleum Corp 3.50

Pioneer Natural Resources Co 3.15

Anadarko Petroleum Corp 3.10

Why do you think it is not trading as it should?

If we go fill that gap I'm going to sell and buy erx,.. That head and shoulders would form...

I agree this explains today. I'm going to play that gap on the short then out.. We'll see.

Period?? LOL

I'm not so sure.

Why Saudi Arabia won't cut oil production

Nine months after OPEC decided to leave its production target unchanged and pursue market share instead of trying to prop up prices, the group is facing a set of complex problems and decisions going forward.

At first blush, the collapse of oil prices and the resiliency of U.S. shale appears to hand OPEC, and its most powerful member in Saudi Arabia, a stinging defeat. U.S. oil production has leveled off but has not dramatically declined. The revenues of OPEC members have fallen precipitously along with the price of crude.

Saudi Arabia is under tremendous pressure. The Saudi government is considering slashing spending by a staggering 10% as it seeks to stop the budget deficit from growing any bigger. The IMF predicts that Saudi Arabia could run a budget deficit that amounts to about 20% of GDP.

The pain is manifesting itself in different ways. Not only will the Kingdom have to cut spending, but it has also turned to the bond markets in a big way. Low oil prices have forced Saudi Arabia to issue bonds with maturities over 12 months for the first time in eight years, raising 35 billion riyals (around $10 billion) so far in 2015.

At the same time, the currency is coming under increasing pressure. Saudi Arabia pegs the riyal to the dollar at a rate of about 3.75:1, but speculation is rising that the currency may need to be devalued, given that the oil producer won't be able to defend that ratio indefinitely. On one-year forward markets, the riyal has already weakened to 3.79, according to the FT. That forced the government to issue a statement, saying that the Saudi Arabian Monetary Agency "is committed to the policy of pegging the Saudi riyal with the American dollar." But if oil prices do not rebound, the government will have to continue to draw down on its foreign exchange in order to keep the currency steady.

All the damage inflicted upon Saudi Arabia has the world looking back towards Riyadh, especially after oil prices crashed on "Meltdown Monday." The markets are trying to figure out if Saudi Arabia may switch tactics in order to stop the crash from worsening.

Pressure is actually the greatest within the oil cartel. Algeria's oil minister wrote a letter to OPEC's secretariat requesting action, although the letter stopped short of a call for a production cut. Months earlier, before OPEC's last meeting in June, Venezuelan officials pressed for a change in strategy to shore up oil prices. Venezuela is arguably the worst off member, as its economic and financial crisis worsens by the day.

More recently, Iran's oil minister said that his country would increase oil production "at any cost," but also supported an emergency OPEC meeting before the scheduled summit in December in order to discuss the group's strategy. More and more members are clamoring for a cutback in the cartel's production.

If Saudi Arabia's strategy of pursuing market share has not worked, and even its colleagues inside OPEC want a policy change, perhaps Riyadh would reconsider and now decide to restrict production in order to boost prices?

Related: Why oil prices could since to $15 a barrel

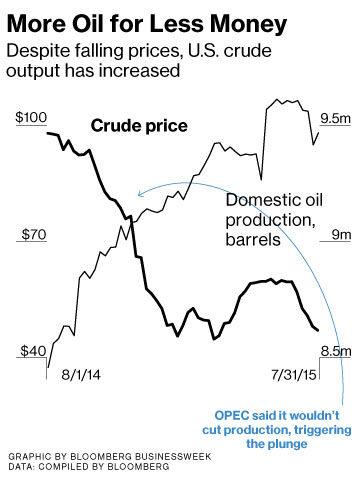

That is more wishful thinking than a likely possibility. There is little chance that Riyadh would retreat now just as the worst pain is really beginning to set in for rival producers. Sure, Saudi Arabia is suffering from low prices, but its competitors are hurting worse. U.S. oil production, after years of blistering growth, has not only ground to a halt, but has started to decline. Output peaked in March at 9.69 million barrels per day (mb/d), dropping to 9.51 mb/d in May (the latest month for which accurate data is available). In all likelihood, the decline has picked up pace in the intervening months.

And more to the point, U.S. oil production will continue to decline the longer Saudi Arabia holds out. Several companies have already gone bankrupt, and more are no doubt coming down the pike. That will allow Saudi Arabia to achieve its goal of holding onto market share, and letting prices adjust on the back of rival producers.

To highlight this point, Saudi Arabia's decision to cut its budget should be seen not as evidence that it is buckling under crushing weight of low prices, but that it is in the game for the long haul. It is shrinking its budget to fit a world of depressed oil prices, positioning itself to ride the wave as far as it goes. Cutting spending is actually a signal of the government's resolve in regards to its current oil strategy, not a sign of wavering.

Going to play this gap... Oil is still under pressure to go lower... Gap fill At 35.55

I think you re-enter at some point...

What a beat down today..

Wow.. What a mistake to sell.. Should be happy.. gap that will fill.

OK.. I sold after looking at erx... well see

I'm up now over 25%.. wondering on a big pop today I should sell at close and re-enter later.. hum

Any way to find out?

Is this a shell?

Well that gap filled now I think we go back up.

That gap might fill at 24.63

August 6, 2015 — 3:15 PM EDT

Not long ago the oil industry looked like it had dodged a bullet. After the worst bust in a generation cut crude prices from $100 a barrel last summer to $43 in March, the oil market rallied. By June, prices were up 40 percent, passing $60 for the first time since December. Oil companies that had cut costs began planning to deploy more rigs and drill more wells. “We didn’t think we’d be quite this good,” Stephen Chazen, chief executive officer of Occidental Petroleum, told analysts in May.

The runup was short-lived. Fears over weak demand from China, along with rising production in the U.S., Saudi Arabia, and Iraq pushed prices back below $50. In July, even as the summer driving season boosted U.S. gasoline demand close to record highs, oil posted its biggest monthly drop since October 2008. “The much feared double-dip is here,” Francisco Blanch, head of global commodity research at Bank of America, wrote in a July 28 report.

è

The largest oil companies are reporting their worst results in years. ExxonMobil’s second-quarter net income fell 52 percent; Chevron’s fell 90 percent. ConocoPhillips lost $180 million. Billions of dollars in capital spending have been cut, and more layoffs are likely. Part of the problem facing the majors is that they’re producing in some of the most expensive places on earth: deep water and the Arctic.

With their healthy cash reserves the majors can hold out for higher prices, even if they’re years away. The same can’t be said for many of the smaller companies drilling in the U.S. shale patch. Shale producers had bought themselves time by cutting costs, locking in higher prices with oil derivatives, and raising billions from big banks and investors. Many cut drilling costs by as much as 30 percent, fired thousands of workers, and renegotiated contracts with oilfield service companies. “That postponed the day of reckoning,” says Carl Tricoli, co-founder of private equity firm Denham Capital Management.

But it’s not clear what’s left to cut. The futures contracts and other swaps and options they bought last year as insurance against falling prices are beginning to expire. During the first quarter, U.S. producers earned $3.7 billion from these hedges, crucial revenue for companies that often outspend their cash flow. “A year ago, you could hedge at $85 to $90, and now it’s in the low $60s,” says Chris Lang, a senior vice president with Asset Risk Management, a hedging adviser for oil companies. “Next year it’s really going to come to a head.”

Over the first half of 2015, U.S. shale producers were able to raise about $44 billion in debt and equity, according to UBS. As oil prices keep falling, investors are losing their appetite for risky shale debt. Bonds have become more expensive and are laden with more onerous terms, including liens against drillers’ oil and gas assets. More than $24 billion of the $235 billion in debt owed by 62 North American independent oil companies is trading at distressed levels, meaning their yields are more than 10 percentage points above U.S. Treasuries.

“For the weaker companies, it could be very, very painful. Some of them are essentially running on fumes.” —Jimmy Vallee, Paul Hastings

Regulators have warned of the risks of lending to U.S. shale drillers, threatening a cash crunch in an industry that’s more dependent than ever on other people’s money. In October, as they do twice every year, banks will reevaulate drillers’ lines of credit, which are often based on the value of reserves. If prices stay where they are, many companies could be cut off from crucial funding. “For the weaker companies, it could be very, very painful,” says Jimmy Vallee, a partner in the energy mergers and acquisitions practice at law firm Paul Hastings in Houston. “Some of them are essentially running on fumes.”

Over the past year, shale producers have lowered their costs so much that the average break-even price for a barrel of U.S. crude is now in the upper $40s, down from $60, according to research from IHS Energy. That’s allowed them to keep producing, feeding the glut that continues to weigh down prices. At some point, though, they may have to pull back.

The bottom line: The renewed decline in oil prices has made it hard for shale producers to issue stock or sell bonds.

Rig count is down but supply is strong on what is active...

OPEC is going to beat the shit out of frackers..

OPEC oil exporters have no plans for an emergency meeting to discuss the drop in oil prices before a next scheduled gathering in December, two OPEC delegates said on Monday.

Algerian Energy Minister Salah Khebri said discussions about potentially holding such a meeting were ongoing, state news agency APS reported on Monday as oil prices fell towards $48 a barrel, their lowest since January.

Algeria is one of the Organization of the Petroleum Exporting Countries members which had misgivings about its 2014 shift in policy to defend market share rather than prop up prices, and has been seeking supply cuts.

Saudi Arabia and the Gulf members which drove the change of tack have shown no sign of softening their stance.

While OPEC countries are in touch with each other to discuss developments in the market, "there is no proposal for an emergency meeting," one of the OPEC delegates said. Another said there was no suggestion of a meeting before the Dec. 4 gathering.

OPEC kept output policy unchanged at its last meeting held in June, despite lobbying by Khebri for a production cut. Oil's collapse from over $100 in June 2014 is more painful for African OPEC countries like Algeria than for Gulf members.

"Consultations are ongoing to take a decision," APS cited Khebri as saying, when asked about a possible OPEC extraordinary meeting. He did not give further details.

Despite the drop in prices since the last OPEC meeting, officials including Secretary-General Abdullah al-Badri have downplayed the prospect of the group cutting output and said they expect rising demand to support prices.

Algeria, heavily dependent on oil income, has foreign exchange reserves as a cushion against any economic fallout, but the central bank director has warned those reserves may swiftly diminish if oil remains low for a long period.

Its foreign exchange reserves dropped by $19.02 billion to $159.9 billion in the first quarter of 2015 due to the collapse in global crude oil prices.

(Reporting by Lamine Chikhi in Algiers and Alex Lawler in London, writing by Rania El Gamal, editing by William Hardy)

Still pressure on stocks this is a good one...

JV.. ERX is energy stocks... Exxon, BP, riggers, etc.. Following the index..

Most investors think Iran is going to dump on the market.. thus lower profits in this sector. Timing is everything..

In time we know energy will fly.. when? if we guess right.. we can gain great returns...

Investment consultant.. $10-$20 oil

http://finance.yahoo.com/video/iran-supply-pushes-oil-10-115300946.html

This gap could fill...

did you make $3/share?

Almost hit a 52 week low today. I had some limit buys. These oil companies have really cut back and it is going to turn... Just when?

Thinking a good time to start consider longer...

• Saudi Arabia’s move to abandon its role as the balancing force in world oil markets has successfully pressured U.S. shale players and put the brakes on America’s energy boom, Royal Dutch Shell (RDS.A, RDS.B) CEO Ben van Beurden tells Financial Times

Only a matter of time..

I do think oil is going back up soon..

Oil Markets Could Be in for a Shock From China Soon

Nick Cunningham

June 21, 2015

Oil analysts and commodity traders watch the price of crude swing down and up, and are trying to figure out when and to what extent the OPEC “price war” will force supply reductions from U.S. shale. Any insight into this development can clarify the trajectory of oil prices.

But, of course, oil market dynamics are complex and fluid. U.S. shale supply is hugely important for oil prices, but one of the more underreported factors influencing the price of oil is the pace of demand growth coming from China.

Consumption of oil in China has climbed rapidly and consistently since it took off in 1990, accelerating into overdrive in the 2000s. The inexorable surge in demand caused oil markets to tighten in the lead up to the financial crisis, and then again in subsequent years as the global economy recovered.

The rise in U.S. shale production managed to finally halt the climb in prices, adding enough supply to send prices downwards. Much of the analysis since last year’s bust has been focused on what is going on in Texas and North Dakota, as well as on key decisions made in Vienna every six months.

But the story in China has been overlooked. When it comes to demand, China is arguably the most important country to watch.

And despite accounting for much of the world’s growth in demand in the 21st century, China’s oil imports have been all over the map in recent months. In April, China imported 7.4 million barrels per day, a record high and enough to make it the world’s largest oil importer. But a month later, imports plummeted to just 5.5 million barrels per day. Much of that had to do with Chinese refineries going offline for maintenance, suggesting that the slowdown may have been just a slight detour from China’s seemingly ceaseless climb in import demand.

On the other hand, China’s exceptionally high levels of imports could be temporary. China is in the midst of filling up its strategic petroleum reserve, a project aimed at stockpiling 100 days’ supply in a reserve by 2020. China has seized the opportunity of low oil prices to fill up its strategic reserve as quickly as it can, buying up crude while it is cheap. This elevated level of imports has soaked up some of the glut, diverting several hundred thousand barrels per day of global supplies to China.

But what happens when China stops buying extra oil for its stockpile?

“We need to understand the dilemma of hidden demand in China, where you have two types of demand – normal demand and strategic stockpiling. The latter won’t last forever,” Jamie Webster of IHS Energy told Reuters in an interview. That could send prices down because once China stops vacuuming up a lot of the excess supply floating around for its strategic reserve, that additional oil will stay on the market.

But the bigger question is over how much oil China is actually burning – as opposed to stockpiling – and the magnitude of its rate of growth. In 2014, China’s growth in demand slowed to just 3% compared to the year before, adding just 300,000 barrels per day. In previous years the growth rate was often twice as high. The deceleration in oil demand growth can be attributed to a slowing economy – China’s GDP is growing at its lowest rate in a quarter century.

Demand is indeed inching up in the U.S. because of low oil prices, but maybe not enough to really move the needle on oil prices. Efficiency efforts in the U.S. and Europe are keeping demand largely stagnant.

The developing world, led by China, represent the most important demand-side factor when it comes to affecting the trajectory of oil prices. But after years of solid growth, China is now raising a lot of questions for the oil markets.

http://www.cheatsheet.com/business/oil-markets-could-be-in-for-a-shock-from-china-soon.html/?ref=YF&tpl=op

If it's an IRA, no issues.

I cannot believe those tax companies could not figure it out??? It's just another form and you pay on earnings even when you have not sold the ETF.

If you treat it as a 1099 the my bet is they never catch it...

http://www.irs.gov/pub/irs-pdf/i1120ssk.pdf

Well that gap filled quick..