News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

zsvq1p

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

broke out of that channel!

About time for a beat down. Fill that lower gap.

About time for a beat down. Fill that lower gap.

About time for a beat down. Fill that lower gap.

Oil prices dip on persistent fuel supply overhang

By Sabina Zawadzki | LONDON 11/11/16

Oil prices dipped on Friday as the market refocused on a persistent fuel supply overhang that is not expected to abate unless OPEC and other producers cut their output significantly.

International Brent crude futures LCOc1 traded at $45.70 per barrel at 0445 ET, down 14 cents from their last close.

U.S. West Texas Intermediate (WTI) crude futures CLc1 were trading 29 cents lower at $44.37 per barrel, weighed down by weakening U.S. demand.

"This week, both U.S. gasoline and diesel demand decelerated on a four-week rolling average basis to minus 2.1 percent year-on-year and plus 0.9 percent, respectively," U.S. investment bank Jefferies said on Friday.

Traders said a crude and refined product glut that has dogged markets for over two years was dragging on prices.

The supply overhang could run into a third year in 2017 without an output cut from the Organization of the Petroleum Exporting Countries, while escalating production from other exporters could lead to relentless supply growth, the International Energy Agency (IEA) said on Thursday.

"Oil markets are increasingly reflecting growing consensus that the persistent oversupply seen throughout 2016 will carry on into 2017," analysts at JBC Energy wrote.

"We would actually go a step further, as while 2016 has seen a significant improvement from 2015 with easing oversupplies, 2017 will be worse again barring massive outages or OPEC action."

In its monthly oil market report, the IEA said global supply rose by 800,000 barrels per day (bpd) in October to 97.8 million bpd, led by record OPEC output and rising production from non-OPEC members such as Russia, Brazil, Canada and Kazakhstan.

Nigeria is working out new oil and gas policies to attract more private investors and boost crude production by 500,000 bpd by 2020, state firm NNPC said on Thursday.

The IEA kept its demand growth forecast for 2016 at 1.2 million bpd and expects consumption to increase at the same pace next year, having slowed from a five-year peak of 1.8 million bpd in 2015.

Beyond oversupply, a surging dollar .DXY following the initial shock of Donald Trump's U.S. presidential election win also put pressure on prices, traders said. The dollar was on course on Friday for its best week in a year.

Because oil and refined products are traded in dollars, their import costs rise for countries using other currencies, potentially crimping demand.

(Reporting by Sabina Zawadzki; Additional reporting by Henning Gloystein in Singapore; Editing by Dale Hudson)

Playing the Gaps.. Time to sell and buy ERY.

Playing the Gaps..

we gapped up today meaning will fill fill down..

"I wouldn't be surprised if by the end of the week or beginning of next week, we'll get to $42 or $41 a barrel, as very few believe OPEC will make cuts that matter."

Keeping some dry powder ready..

http://www.reuters.com/article/us-global-oil-idUSKBN12X02E?il=0

Well this triggered a buy.. We'll see

http://finviz.com/quote.ashx?t=erx

Buy the rumor sell the fact. Next big day? Nov. 30

October 19, 2016

Many nations are willing to join OPEC in cutting production to secure a continued improvement in oil prices, said Saudi Arabia’s Minister of Energy and Industry Khalid Al-Falih.

The minister didn’t name any countries in his speech at the Oil & Money conference in London Wednesday, saying only that negotiations will continue until the scheduled Nov. 30 meeting of the Organization of Petroleum Exporting Countries in Vienna. So far, only Russia has said it’s considering an output freeze or a reduction, while other non-OPEC producers that cooperated with past supply curbs, including Mexico and Norway, said they won’t cut.

“We are going to work with our colleagues and the decision I think will be fair and equitable to all countries,” Al-Falih said in an interview after his speech. Saudi Arabia will not decide alone how much production it should cut because “this is a collective decision that we have to make.”

Al-Falih painted an upbeat picture, telling a packed audience that included the chief executive officers of Exxon Mobil Corp., Chevron Corp. and Total SA that the oil market is "clearly rebalancing," bringing the industry to the end of a "considerable downturn." U.S. crude inventories are declining and supply and demand are coming back into line, he said.

Oil has fluctuated near $50 a barrel amid uncertainty about whether OPEC will be able to implement an accord to reduce supply at an official meeting in November. A committee will meet later this month to try to resolve differences in the group over how much individual countries should pump. There’s no possibility that Russia will pull out of its agreement to cooperate, OPEC Secretary-General Mohammed Barkindo said Tuesday.

Oil producing countries can secure a "healthy" price increase with a small percentage output cut, Al-Falih said. Crude futures extended gains after the minister’s comments, with West Texas Intermediate advancing 1.3 percent to $50.95 at 7:08 a.m. on the New York Mercantile exchange.

The consensus among executives, traders and officials gathered at the annual Oil & Money conference was that the world should get used to oil prices between $50 and $60. Falling costs in America’s shale fields will counteract OPEC’s renewed commitment to supply management, keeping a lid on prices, they said.

http://www.bloomberg.com/news/articles/2016-10-19/saudi-arabia-says-many-nations-back-opec-move-to-boost-oil-price

I hope you didn't jump ship..

Not sure when the bull ends but the ride has been good since $15...

Who did this?

Accumulate and sell at gaps

Channel trade...

Gaps have always seemed to fill...

This ETF is based on stocks.. leveraged.

The key is stock prices of energy companies..

Tread lightly..

"Bernstein Research estimates that by 2019 we’ll see more than $70 billion in defaults amid more than $400 billion in high-yield energy debt — that would indicate that we’re only halfway through the bankruptcies."

http://www.forbes.com/sites/christopherhelman/2016/05/09/the-15-biggest-oil-bankruptcies-so-far/#3728bb0f739b

Supply and demand

Frank,

I think this group did you wrong. The Greed and selfishness demonstrated by these men for the "love of money" is on display. They are a bunch of young men (kids) who have yet to discover what is most important in life.

I do wish you well.

David

PS.. NEVER trust a lawyer.

Saudi Arabia Burns Through Foreign Reserves As Oil Prices Tank

You have to hand it to Saudi Arabia. The Kingdom ruled global oil markets for nearly 40 years, increasing or decreasing production as it willed, playing the role of global oil markets swing producer. The OPEC de facto leader, and the second largest global oil producer now after Russia, has simply lost its footing.

The Reason? The U.S. shale oil and gas boom. The problem for the Saudis is that they have been caught in a snare of their own making. When global oil markets first became oversupplied in 2014 due to increased U.S. oil production, the Saudis in their now infamous November 2014 decision, decided to not pull back production to support plunging prices.

The Saudis have taken a step further, actually increasing production in the past two years. The effects have been cataclysmic for the global oil industry. Prices, which topped off at $114 during the summer of 2014 are now trading in the low to mid $40s level, after dipping into the $20s mark earlier this year – a pricing scenario unthinkable just a few years ago.

Massive oil industry lay-offs, bankruptcies and a general downturn in the sector has ensued, with little respite on the horizon. Now, the Saudis are having to contend with Iran, post sanctions on Tehran’s energy sector, for market share in both Europe and Asia. Unfortunately, for the Saudis, Iran is willing to cut prices to the bone in order to reach a pre-sanction production level of 4 million barrels per day.

Saudi Arabia is also losing market share in Asia to Russia, including China’s vast oil market, which could soon surpass the U.S. as the word’s largest oil importer.

Tim Daiss , CONTRIBUTOR

Journalist, author and geopolitical analyst based in Vietnam.

Opinions expressed by Forbes Contributors are their own.

TWEET THIS

The Saudis are also running budget deficits attributed to the prolonged oil price down turn.

Saudi investors monitor stocks at the newly opened exchange market department at the National Commercial Bank (NCB) in Riyadh on November 12, 2014. The Saudi stock market rebounded last week as markets in the rest of the region fell. However, the real problem for Saudi Arabia is the more than two year free-fall in global oil prices and a massive loss of revenue. (Photo FAYEZ NURELDINE/AFP/Getty Images)

You have to hand it to Saudi Arabia. The Kingdom ruled global oil markets for nearly 40 years, increasing or decreasing production as it willed, playing the role of global oil markets swing producer. The OPEC de facto leader, and the second largest global oil producer now after Russia, has simply lost its footing.

The Reason? The U.S. shale oil and gas boom. The problem for the Saudis is that they have been caught in a snare of their own making. When global oil markets first became over supplied in 2014 due to increased U.S. oil production, the Saudis in their now infamous November 2014 decision, decided to not pull back production to support plunging prices.

The Saudis have take a step further, actually increasing production in the past two years. The effects have been cataclysmic for the global oil industry. Prices, which topped off at $114 during the summer of 2014 are now trading in the low to mid $40s level, after dipping into the $20s mark earlier this year – a pricing scenario unthinkable just a few years ago.

ADVERTISING

inRead invented by Teads

Massive oil industry lay-offs, bankruptcies and a general downturn in the sector has ensued, with little respite on the horizon. Now, the Saudis are having to contend with Iran, post sanctions on Tehran’s energy sector, for market share in both Europe and Asia. Unfortunately, for the Saudis, Iran is willing to cut prices to the bone in order to reach a pre-sanction production level of 4 million barrels per day.

Saudi Arabia is also losing market share in Asia to Russia, including China’s vast oil market, which could soon surpass the U.S. as the word’s largest oil importer.

Recommended by Forbes

Move Over Saudi Arabia, Russia Is Selling More Oil To China Than You

Saudis And Iranians Battle For Asian Oil Market Share

OracleVoice: 3 Ways Healthcare Providers Can Take Advantage Of Social Media Disruption

Iran Defies, Then Keeps OPEC Guessing

Why Islamic State's (ISIS) Oil Revenue Is Plunging

MOST POPULAR Photos: The World's Highest-Paid Models 2016

The DEA Is Placing Kratom And Mitragynine On Schedule I

MOST POPULAR Photos: The Most Expensive Home Listing in Every State 2016

MOST POPULAR What We Know About The Apple iPhone 7

Saudis need cash to offset historic budget deficits

Now, news has broken that the Saudis, amid this ongoing oil industry dilemma, is burning through foreign reserve holdings. Media reported on Monday that the Kingdom’s foreign reserve holdings, likely in U.S. dollars, dropped 16%, from the same period in 2015, to $555 billion. This marks a drop of $6 billion from July, and their lowest level since February 2012. Holdings peaked in August 2014 at $737 billion before prices tanked in July that year.

The Saudis are also running budget deficits attributed to the prolonged oil price down turn. The Saudi budget deficit hit a record $98 billion last year, but Riyadh expects this figure to drop to $87 billion this year. The government has been borrowing domestically and abroad to help reduce the deficit.

Slowdown in Oil Finds Raises Alarm Over Supply Gap Ahead

Zacks

Zacks Equity Research

August 30, 2016Comment

The Oil and Gas sector continues to remain in troubled waters with a new report mentioning that in 2015 explorers had managed to discover only about 10% of the average level of oil found annually since 1960 and the level is expected to decline even further. This has raised apprehensions that the amount of oil discovered might be too less to meet future demand.

Oil prices have more than halved since the commodity prices started tumbling two years ago. As a result, drillers have cut their exploration budgets enormously, which in turn, has resulted in discovery of just 2.7 billion barrels of new supply. Per the figures from Edinburgh-based consulting firm Wood Mackenzie Ltd., this is the lowest level since 1947. As of the end of last month, drillers found just 736 million barrels of conventional crude.

Per the U.S. Energy Information Administration, global oil demand is expected to grow to 105.3 million barrels in 2026 from 94.8 million barrels a day in 2016. However, the slowdown in the discoveries has raised questions regarding the ability to meet this increasing demand. Though the U.S. shale boom has the potential to make up for the difference, prices locked below $50 a barrel undermine the possibility of growth in the area.

Wood Mackenzie reported that global spending on exploration – seismic studies to actual drilling – has been lowered to $40 billion in 2016 from about $100 billion in 2014. The spending level is expected to remain flat through 2018. Moreover, through August this year only 209 wells were drilled as against 680 in 2015 and 1,167 in 2014. This compares unfavorably with an annual average of 1,500 in data from 1960.

The low exploration data indicates that production might be obstructed few years down the line, which in turn, would push up the oil prices. Currently, oil prices are hovering around $50 a barrel that is less than half their 2014 peak. In a Saudi Arabia-led strategy to augment market share, the Organization of Petroleum Exporting Countries (OPEC) decided to continue pumping without limits. This pushed down the U.S. production to a two-year low.

According to the CEO of Royal Dutch Shell plc RDS.A, oil companies will need to invest about $1 trillion a year to continue to meet demand. The CEO expects demands to rise by 1 million to 1.5 million barrels a day, with about 5% of supply lost to natural declines every year.

The persistent weakness in prices has forced explorers to find new resources that are less risky as well as cheap. As a result, these companies are focusing more on appraisal wells on already-discovered fields and less on frontier areas such as the Arctic. Companies that have abandoned exploration in Alaska last year include Statoil ASA STO and Royal Dutch Shell.

ExxonMobil Corporation (XOM) has also decided against investing further in the proposed Alaska LNG facility. The other stake owners in the project are BP plc BP and ConocoPhillips COP holding 20% each. These companies too have indicated their possibility of withdrawing from the project.

This Will Be the Last Time Down for Oil

By DANIEL DICKER Follow | AUG 25, 2016 | 1:27 PM EDT

Stock quotes in this article: EOG, XEC, CLR, HES

We've tried to work inside a very long-term and a relatively short-term strategy when it comes to investing in the oil space: Inside the long term, we've been identifying the winners from the losers in the coming fresh oil boom, which I believe will send prices above $100 by the end of 2017. In the short term, we've noticed the vagaries of the financially and rumor-driven oil price that has prematurely inflated many of those stocks, and we've taken a break from investing in those companies until a better value price can be found.

Now that a good part of the rumor mill has quieted down and the speculative trade has as well, we're starting to see oil move again toward the mid to low $40s.

This, however, will be the last time down for oil -- and your last opportunity to target some great oil companies.

It's one thing to have a long-term strategy and invest accordingly, but quite another to time those trades effectively. Since a terrible year ended in 2015, I've been having increasingly better success this year in timing entry and exit points, and much of my experience and analysis tell me the coming mini-crash in oil and oil stocks will be the last one we ever see. I've lightened up in virtually all of my best independent U.S. E&P positions, but readying myself again to deploy into them as prices on oil drop (I hope) again toward $40.

All of the hopes of a September production freeze from OPEC and non-OPEC members are correctly fading. The dollar, which has stabilized in the last few sessions, looks ready to rebound higher again.

Speculative oil buyers have increased their positions far ahead of the fundamentals, indicating that they're a bit early to the party. Stockpiles increased by 2.5 million barrels last week, and production is not yet falling off fast enough to clear the market of continuing huge gluts -- at least not until another chokehold of $40 oil puts some of those producers back onto the sidelines. When oil again begins approaching $40, we'll again hear the wrong chorus of oil never seeing $70 and of oil companies fit to survive sub-$50 prices. Just like the last time in the spring of this year, that will be the time to add to positions again.

And I think it's the last opportunity like that we'll ever see.

I want to create new targets on independent E&Ps where I can again increase positions. I want to see EOG Resources (EOG) get close to $85 before adding again, Cimarex Resources (XEC) nearer to $125, Continental Resources (CLR) to $40 and Hess (HES) to $53. I'd rather miss these targets than overpay for oil companies that have reached stock prices that correspond to oil in the $60s rather than nearer to $50.

Patience in the short term will lead to the better returns we're looking for in the long term.

Thank you to those who've expressed interest in my interactive webcast, beginning this fall. More info will be coming after Labor Day. And if you might have interest in this service but have not yet submitted your email, please do: dan.dicker@thestreet.com

Game of Chicken Continues Among Oil Producers

By DANIEL DICKER Follow | AUG 11, 2016 | 12:33 PM EDT

Pardon me for using more charts, and less words, this week to try and fathom where we are in the crude cycle.

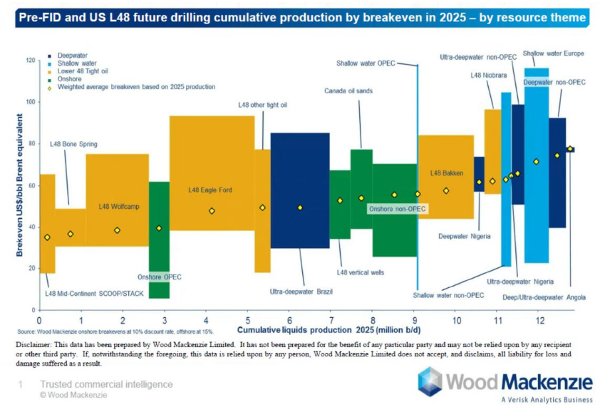

I enjoy seeing most of the mainstream oil analysts come to conclusions on the unsustainability of oil prices that I came to more than a year and a half ago. It started with the fantastic Wood Mackenzie report on break evens that appeared (and I commented on) more than two weeks ago:

No need to go into this chart again -- but don't be fooled: Just because a certain shale area is yielding a weighted average breakeven price of, say, $40 a barrel -- as the chart says for the Wolfcamp area of the Permian -- it doesn't mean it's economically smart to run all the acreage, or that it's even profitable to do so.

If you have wells that break even at $35 and wells that break even at $45, and oil prices are at $40, are you going to run the more expensive ones? Theoretically, no. And yet, they are all running -- as oil companies continue to compete on production goals and market share.

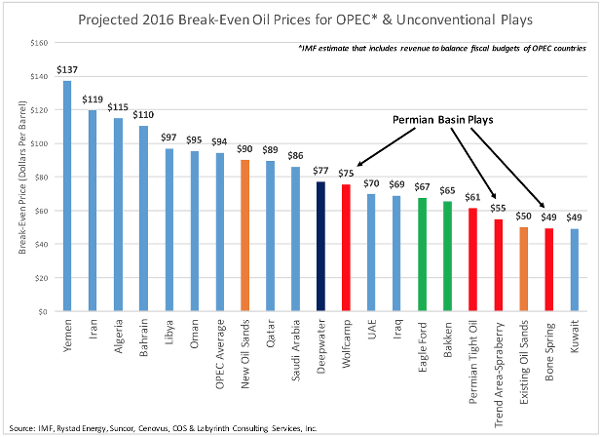

Here is a chart from Arthur Berman (an oil guy who doesn't write much, but is definitely worth following) about real breakeven prices, as his analysis (with consultancy Rystad Energy) shows:

Berman's claim is that the Wood Mackenzie analysis just counts exploration, drilling and completion costs -- but doesn't include administrative, interest or tax costs. Adding those in, in my view, gives much truer breakeven numbers. Notice that Wolfcamp now appears to have a $75 breakeven price, even with all the efficiency gains that have been seen in the last two years.

If you like, you can also consider Berman's analysis on OPEC oil states. I don't want to take much time with those figures, but Berman is trying to put a price on oil where the sovereign budgets for these nations near a breakeven point. They are a lot higher than most people thought -- and equally unsustainable.

But social budgets can be cut with a lot more ease than bondholders can be lured into lending money to losing operations. Berman may be a bit pessimistic, but I believe only a bit. And we come to the same conclusion as we have held for the last year and a half: Oil prices under $75 a barrel will ultimately bankrupt everyone -- oil company and oil country, alike.

It has been my mistake trying to gauge how long both OPEC and energy CEOs would be able to dance around cash-flow-negative operations without doing what seems so obvious -- either cutting back on production severely, or just going bust. But with the current increases coming out of Saudi Arabia, Iraq and Iran, and the current promises of increases out of the majors from recent second-quarter conference calls, it has become clear that this dance is going to extend further than I originally thought.

I was early, and loaded on oil stocks when it was clear that unsustainable prices would lead to a necessary rally in independent oil companies with core acreage and balance sheets that assured their survival. Now, it seems that the market has caught up to me, with many of my core long-term holdings -- EOG Resources (EOG) , Cimarex Energy (XEC) , Continental Energy (CLR) and Hess (HES) -- having run much further than the current oil price would seem to imply. Most of these now have prices last seen when oil was above $60 a barrel, not $40.

It's at this point that I'm cutting back on all of these holdings.

What? Haven't I just proved that oil prices are absolutely destined to rebound three-fold from where they are trading now? Have I lost confidence in my thesis of triple-digit oil by the end of 2017? No.

But the suicide watch on oil producers has gone on far longer than I originally suspected. And I will back away from oil stocks that I think are now way ahead of themselves for this point in the recovery cycle.

I wanted to be first, or close to first, in getting in to these great oil winners.

Now, I want to be first, or close to it, to get out with some amazing profits -- and look for a better time to add again.

That's now.

Oil prices heading toward $40. Here’s when: Analyst

Tom DiChristopher,CNBC 18 hours ago Comments Like Reblog on Tumblr Share Tweet Email

0:16 / 1:55 6/10/16

China's 'insane' oil stockpiles could send crude to $40: ...

Oil prices are likely to fall toward $40 a barrel as China's crude imports hit an inevitable ceiling, according to Matt Smith, director of commodity research at ClipperData.

Oil futures have rallied more than 90 percent to about $50 a barrel since their winter lows, but Smith said Friday the market is missing something in China.

"China is importing so much crude, it's absolutely insane. They're importing about a million barrels a day more than they are actually consuming," he told CNBC's "Squawk Box."

China put about 787,000 barrels of oil per day into storage in the first quarter, Oilprice.com reported, citing Bloomberg data.

By Smith's count, China has stockpiled about 135 million barrels of oil. The trouble is the most optimistic estimates put China's storage capacity at 155 million barrels, he said.

In theory, China could hit capacity in 20 to 30 days, at which point imports will "drop off a cliff," he said.

Meanwhile, Saudi Arabia, Iran and Iraq are ramping up production, and higher prices appear to be eliciting a supply response from U.S. drillers, he said. On Wednesday, weekly data indicated U.S. output ticked up for the first time in three months.

Those factors could send crude prices spiraling down toward $40 a barrel, and perhaps even into the $30s, Smith said.

Smith made the call one day after Continental Resources (CLR) Chairman and CEO Harold Hamm told "Squawk Box" he expects oil prices to end the year between $69 and $72 a barrel.

Channel

Hit a resistant yesterday so we could see a slight pull back for opportunities to buy. A chance to let the gap fill.

Gaps

They have worked in the past and might fill.

Buy monthly, set at gaps, sell at highs when short gaps appear to be needing filled.. It has worked so far.

American oil's 'sleeping giant' is about to spring to life

Irina Slav, Business Insider Tue, Jun 7 10:00 PM PDT

A pumpjack brings oil to the surface in the Monterey Shale, California, April 29, 2013. REUTERS/Lucy Nicholson Thomson Reuters

A pumpjack brings oil to the surface in the Monterey Shale

Last week saw the first significant increase in the number of active drilling rigs in the U.S. since the start of this year, suggesting that optimism is returning, albeit cautiously, to the shale plays, and nowhere did things look better than Texas' prolific Permian Basin-long regarded as America's 'sleeping giant'.

Operators in the Permian added five rigs to their active count during the week, in the latest demonstration that the basin is perhaps the most viable across the shale patch, with its low production costs and abundant reserves.

The Permian is enjoying a lot of attention from the energy industry and from private equity alike. Those with a presence in the basin are upbeat about the future, and those without are trying to step into it in order to share in the riches.

One of the biggest operators in the Permian, Pioneer Natural Resources, just recently indicated its optimism for the short term. Speaking at an industry conference, Pioneer's executive VP Joey Hall said the company is planning to allocate $1.8 billion-about 90 percent of its total budget-to operations in the Permian. What's more, the company is ready to ramp up its rig count in its two Permian fields - Spraberry and Wolfcamp - and hasrevised up its overall production growth projections to 12 percent. A bold move in a still oversaturated oil market that has just seen the re-entry of Iran.

Another of the majors, Occidental Petroleum, is also planning a production increase in the Permian, of 4-6 percent, to be fuelled by capex of some $3 billion. The company is consistently working on lowering its production costs, which last year averaged around $40 a barrel, to ensure its profitability even if prices start sliding again.

Occidental Petroleum recently became the object of media speculation that had it buying smaller rival Apache Corporation. Although the report proved unfounded and was denied by Occidental, Apache's stock shot up immediately, suggesting investors would favor some consolidation in the Permian, where Occidental has acreage of 5.4 million gross, and Apache has over 3.3 million acres.

Pioneer, by the way, was also suggested as a suitable takeover target for Occidental, reinforcing an impression that Permian operators should take advantage of the situation and consolidate to maximize the benefits low production costs and a stable oil price offer them at the moment. Tying up with a peer could indeed bring in synergies that will enhance profitability and resilience in the face of future price slumps. After all, it's unclear how long this will last, especially after OPEC's recent meeting ended with no change of the organization's production policy: members can still pump as much as they can.

For now, however, both Occidental and Pioneer seem to prefer to go it alone, as do other players in the Permian, and they all sound relatively optimistic. A recent survey among Permian operators by the local Midland Reporter-Telegram found that there is a general consensus that oil prices will continue to be volatile in the short-term and that the drive to improve efficiency and reduce costs is the surest way to stay profitable in the lower-price environment. The general mood was positive.

Whether or not consolidation will rear its head in the Permian anytime soon, operators there have two things going for them that are unique for the play: the easier accessibility (hence low production costs) of the crude and its prodigious volume. Making the best of these while they last is the only reasonable course of action at the moment.

Read the original article on OilPrice.com. Copyright 2016.http://www.businessinsider.com/sleeping-giant-of-oil-is-about-to-wake-up-2016-6

Dollar vs oil

Crude oil’s negative correlation with the US Dollar Index between September 2007 and April 2013 clearly implies that crude oil had an inverse relationship with the US Dollar Index. However, since April 2013 to date, the one-month correlation has been more bidirectional. In the last three years, the one-month correlation fluctuated between -64% and 43%. This fluctuation could indicate that fundamental drivers like Saudi Arabia’s decision not to cut production, US shale oil producers’ cost and production dynamics, US inventory data, and other fundamental news had a greater impact on crude oil compared to the dollar.

Al-Falih said. “We see supply and demand converging.”

OPEC’s executive director Abdalla El-Badri lost his job Thursday. Don’t feel bad for him. The 76 year old Libyan was supposed to be replaced in 2012 at the end of his maximum second term, but the cartel members couldn’t agree on a replacement. They finally did this week, unanimously appointing Nigeria’s Mohammed Barkindo to the gig.

It was just the start of the Vienna lovefest. “There’s been too much emphasis on the divisions within the OPEC body,” Nigeria’s Minister Emmanuel Ibe Kachikwu reportedly said. “We’d like to finish this meeting feeling that we’re cohesive.”

New Saudi Oil Minister Kahlid Al-Falih sounded as if he was on a charm offensive as well, reassuring oil markets that the Kingdom wants stability. “We will be very gentle in our approach and make sure we don’t shock the market in any way,” Falih reportedly said Thursday.

Falih promised that the Kingdom would not add more barrels to an already flush market. “There is no reason to expect that Saudi Arabia is going to go on a flooding campaign,” he said.

There had been some concern about that. At the April meeting of OPEC+Russia, the Saudis said they would only agree to freeze their output if the Iranians did too. Iran has no intention of doing so; Minister Bijan Zanganeh said there was no reason why Iran shouldn’t be able to increase production from 3.8 million bpd now to 4.7 million.

But now it’s looking increasingly like the Saudis and Iranians can smoke the peace pipe, at least when it comes to divvying up market share. Al-Falih appeared ready to declare victory in the battle for market share that the Saudis initiated in late 2014. By holding their own output steady, OPEC has brought a halt to the shale boom and has also potentially scared off a whole generation of exploration into the deepwater and arctic. “I believe that the strategy that OPEC adopted in 2014 has indeed succeeded,” Al-Falih said. “We see supply and demand converging.”

Recommended by Forbes

MOST POPULAR Photos: The Most Expensive Home Listing in Every State 2016

TRENDING ON LINKEDIN Hard Work Won't Make You Successful -- But Doing This Will

Charles SchwabVoice: 3 Ways To Help Increase Portfolio Income

It helps that oil prices are up nearly 100% since late January. “We are satisfied with the price movement over the last few months and think it will continue to gently edge up without much intervention, assuming that more or less OPEC production stays where it is,” said Al-Falih. Maybe $50 a barrel really will be the new $100.

“The long-awaited rebalancing of the global oil markets is at hand,” wrote SocGen’s oil analyst Michael Wittner in a big report yesterday. His team predicts that global oil stockdraws will begin in the second half. And could go on for awhile.

Of course the U.S. will be the locus of much of this rebalancing. Having peaked at 9.6 million bpd a year ago, U.S. output is now down to around 8.8 million, according to government estimates. It will continue to fall, given that 75% of America’s drilling rigs are in mothballs and fracking crews tossed to the wind. The worst blowdown has been in the Eagle Ford, down from 1.7 million bpd to 1.3 million. The Bakken is off from 1.2 million to about 1 million. SocGen figures on a further 600,000 bpd in U.S. declines this year, and a 100,000 bpd reduction in 2017, with supplies from America’s shales to bottom out in late 2017.

And yet what’s interesting is that it’s not really the declines from American shales that are stabilizing the market. Fires in Canada, chaos in Libya, and attacks in Nigeria caused about 3.7 million bpd of outages in May, and “have in effect brought forward the rebalancing,” says SocGen. The Canadian barrels should come back soon, but Nigeria and Venezuela have deeper issues.

Venezuelan production has fallen from about 2.7 million bpd in 2014 to 2.5 million bpd this year. Power outages have hampered operations there, and oil service companies are having a hard time getting paid. Schlumberger SLB +0.24% and Halliburton HAL +1.71% said last month they were pulling back. Argus Media reported yesterday that 83 tankers were backed up at Venezuelan ports, with BP in particular holding back deliveries of light, sweet American crude that the Venezuelans like to blend with heavier grades.

According to WoodMackenzie, the consultancy, oil companies have deferred nearly $400 billion of capital spending all over the world, projects that would have provided about 3 million barrels per day of oil supply in the next decade. Furthermore, Rystad, another consultancy, said in a report this week that the average natural decline rate for mature oilfields around the world has climbed from 2% in 2012 to more than 6%. That’s about 5 million bpd lopped off of global supply every year.

No wonder those OPEC ministers are happy. Their plan worked. They responded to interlopers by refusing to cut output. The resulting low prices have mostly eliminated the market oversupply and permanently impaired rivals’ capital. With prices still too low to incentivize renewed interest in places like the deepwater, Arctic or lesser shale plays, Iran and Iraq are now free to add to their market share. Contrary to rumors, it looks like OPEC didn’t die after all.

Ahead of Meeting, OPEC Seems Close to Riding out Price Slump

By GEORGE JAHN, ASSOCIATED PRESS VIENNA — Jun 1, 2016, 6:14 AM ET

3

SHARES

Email

OPEC is not yet in safe harbor. But ahead of a top-level meeting, the 13-nation oil cartel appears close to weathering the storm of slumping crude prices that threatened to bankrupt some members and called into question its relevance.

After touching a 13-year low early this year, the price of oil has moved steadily upward to their present level of around $50 a barrel.

While that's still only half of what crude fetched as late as two years ago, it's a gain of almost 90 percent since January. That is easing some of the pain for poorer members such as Algeria, Venezuela and Nigeria that depend on crude as their main income. And there are promises of further increases.

U.S. shale production is in decline as it needs higher prices to be economical. At the same time, the world economy is showing signs of some improvement, meaning that the appetite for petroleum may increase.

Oil ministers of the Organization of the Petroleum Exporting Countries convening in Vienna Thursday will thus likely opt for the status quo. Total production is now well over 32 million barrels a day, and in a note ahead of the meeting, analysts at Commerzbank Commodity Research said expectations are for the "meeting to end without reaching any agreement on production targets or production caps."

Ironically, part of the credit for OPEC's improving fortunes is due to its inability to act in unity in recent years. Instead, many individual members produced what they could, driving down prices to the point where shale producers are increasingly unable to compete. Some have gone out of business, reducing the glut of global supply.

At the height of its power decades ago, OPEC essentially was able to set world prices and supplies. Although it is still responsible for more than a third of world production, that clout has eroded since the 1980s, as outside output increased and members looking to maximize income increasingly ignored OPEC production ceilings.

The final statement at the last OPEC meeting in December didn't even mention an output target. That effectively left it up to individual members how much crude to pump and was a strong signal of the cartel's eroding ability to act as a group in efforts to influence supply, demand — and prices.

But it took top OPEC producer Saudi Arabia to turn overproduction into market strategy.

Since deciding in 2014 to squeeze out outside competition by flooding the market to drive down prices, it has pumped close to or above 10 million barrels a day — close to a third of the organization's total production. That, plus resurgent output from Iraq and post-sanctions Iran, helped push down prices, with the desired effect of making shale production increasingly uneconomical.

Turmoil in OPEC members Libya and Nigeria has also helped tighten supplies. Even with the upturn in prices, though, OPEC is unlikely to regain its past glory — although some members would like to see that happen.

"We need to revindicate the role of OPEC ... in defense of oil producing countries," said Venezuelan oil minister Eulogio Del Pino to reporters. "It has been a historical role for more than 60 years."

But some poorer members will be tempted to continue ignoring any attempt at setting joint policies and sell as much as they can. And Middle East politics will continue to play a role as the Saudis and Iran fight out their rivalry within the cartel.

Qatar's Ministry of Energy and Industry said in a statement that the upward price trend "was largely due to a rise in demand and the slowing down or outage of many production stations around the world, let alone the retreat in investments in the sector."

But the days of oil at $100 a barrel appear to be history. No one can say exactly what price shale producers need to become profitable and pump more, pushing the market back down, but it appears to be well below the $100 level. And production by OPEC members is expected to remain rampant.

With prices at long last appearing to be heading upward, some of the past edginess marking the most recent meetings should be missing Thursday.

"Market forces have made it easier to get along," says Phil Flynn of the Price Futures group.

For now, he says, "I think the price war is over."

————

Andras Adam Zagoni-Bogsch in Vienna and Adam Schreck in Dubai contributed to this report.

Saudi Oil Gambit Moves to Phase Two

Apr 10, 2016 3:00 AM EDT

There's an oil supply crunch looming and Saudi Arabia and its local allies are positioning themselves to take advantage.In what would be the second phase of the kingdom's strategy to defend its market share against rival producers (most visibly U.S. shale), Gulf states are planning to raise output capacity to fill the hole left by the lack of investment in new projects elsewhere.

It may seem odd talking about an oil shortage when the world seems awash with the stuff and storage tanks are brimming, but listed oil companies are slashing spending for the second year running, leading the International Energy Agency's Neil Atkinson to warn of possible oil-security surprises in the “not too distant” future.

There are too few new projects being sanctioned by non-state oil companies to offset the inevitable decline in output from existing fields and to meet additional demand. This is expected to increase by 1.2 million barrels a day each year for the rest of the decade. New fields due to start producing this year and next are the result of investment decisions taken when oil was about $100 and expected to stay there.

The collapse in company spending is illustrated perfectly by the level of drilling activity. After all, if you don't drill, you can't get the oil out of the ground.

Drilling Collapse

In March, the worldwide rig count hit its lowest level since September 1999

http://www.bloomberg.com/gadfly/articles/2016-04-10/saudi-arabia-oil-gambit-moves-to-phase-two

Yep... It will gap open.. might get some profit selling later to fill the open gap.. but this one still looks strong for awhile..

The rally in crude oil? Shale will cap it, says Citi

Huileng Tan,CNBC 2 hours 36 minutes ago Like Reblog on Tumblr Tweet

Despite a jump in crude oil prices this week, gains may be capped by a quick ramp up in shale oil production, said an analyst Friday.

Oil prices have jumped over 20 percent since hitting 12-year lows last week and are around $34 a barrel in Asian hours on the back of reports that OPEC and producers from outside the cartel would meet to discuss production cuts.

Speaking to CNBC's Capital Connection on Friday, Citigroup's Head of Asia Commodity Research, Ivan Szpakowski said that the shutdown of shale wells and the subsequent support in oil prices as envisioned by Saudi Arabia is a "questionable victory" because unlike traditional oil and gas production, shale production can be ramped up fast.

"This production can be switched on within a matter of months; so if prices start moving higher later this year, you'll see shale production in the U.S. starting to increase again," he said.

"It really caps the rally," he added without giving a price forecast.

Despite a 70 percent decline in crude oil prices since the summer of 2014 when the extended decline started, OPEC has refused to cut the group's production ceiling as Saudi Arabia sticks to its strategy of pumping more oil to squeeze out higher-cost energy producers such as shale companies.

The plan however is taking far longer than Saudi envisioned, said analysts, and prices hit fresh 12-year lows last week due to the lifting of international sanctions against Iran.

Szpakowski said the house is expecting Iran to export another 300,000 barrels of oil a day in the coming months—short of the country's own forecast of half to one million barrels a day in the first year after sanctions.

"We don't think that's actually achievable more from a technical standpoint. The major constraint there will be how fast they can actually reopen the wells, get the oil pumping. And there's also an issue of insurance; who's going to insure all of these tankers going out to the rest of the world?"

Believe these guys ?

Iran says low oil prices will not last long

Reuters 20 hours ago Comments Like Reblog on Tumblr Share Tweet Email

PARIS (Reuters) - Iranian President Hassan Rouhani said on Thursday that oil prices would not stay low for long as producers restore market balance.

"The price of oil is at a low level ... I don't think it will last in the long term ... The pressure on oil-producing nations means balance will be restored in the short term," Rouhani, whose country is the third-largest producer in OPEC, said at the French Institute of International Relations.

Pragmatist Rouhani arrived in France on Wednesday on the second leg of a state visit to Europe after three days in Italy. Iran is pushing to boost oil exports now that international sanctions against it have been lifted.

Reiterating Iran's official stance, Rouhani blamed Shi'ite Iran's Sunni regional rival Saudi Arabia for the drop in oil prices, which have halved since last May as global supply outstrips demand.

Oil futures surged on Wednesday after non-OPEC member Russia indicated there was a possibility of cooperation with the Organization of the Petroleum Exporting Countries to curb output and thus raise the crude price, currently near $33 a barrel.

Nikolai Tokarev, head of Russia's oil pipeline monopoly Transneft, said on Wednesday Russian officials had decided they should talk to Saudi Arabia and other OPEC countries about output cuts aimed at bolstering crude prices.

But Iranian Oil Minister Bijan Zanganeh said Tehran had not been contacted by Moscow over oil output cuts.

"I have not received anything," Zanganeh said at a Franco-Iranian summit in Paris, adding that Iran would sign an agreement with French oil major Total (TOTF.PA).

"We will sign an agreement with Total (this) afternoon," he said, without elaborating. Total declined to comment.

that 22 will fill imo.. not sure when?

I've got some small shares of ERX.. Flipping ERY, a strategy started in December to buy each month to average in... I think oil does go to 20 so I might skip Feb and double up in March.

These gaps have been filling so I do believe it will just when?

How can you not think oil will go bull in the coming year?

Well... that gap just filled... what's the thoughts?