News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

10452km2

![]()

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

PSUN called it yesterday up another .06

Wow up big in pre market... Something must be going on.

Company is buying $1mil worth of stock at $2

ASSET SALES

After the quarter ended, EMMS closed or will soon close 3 transactions that combined should generate $169 million of after tax and fees proceeds that will be used to repay debt.

1) ESPN transaction which has already closed and generated $75 million of cash proceeds.

2) KISS transaction which should generate $10 million of cash proceeds when it closes this summer.

3) Grupo Radio Centro Put/call which should generate $84 million of cash proceeds when it closes this summer.

For more details on these sales, see the earnings call transcript and SEC filings.

WOW MUST READ ON EMMS...INSIDERS KNOW SOMETHING.

Below is a reader submitted investment idea for Emmis Communications (EMMS), drawing attention to important events that have occurred subsequent to the end of the most recent financial statements.

Disclosure: No position (Frank)

******

OVERVIEW

On an LTM basis, Emmis Communications Corp. (“EMMS”) appears to be an overvalued, overlevered company. However, after the quarter ended, the company closed (or is in the process of closing) several transactions that are significantly accretive and massively deleveraging. Pro forma for these transactions (and an unannounced but inevitable refinancing of debt, including 12.25% and 23.0% debt), EMMS is trading at only 5.9x equity cap/LTM free cash flow. The valuation drops to 4.8x equity cap/free cash flow if EMMS wins a lawsuit regarding its outstanding preferred stock. This is a complicated (and somewhat illiquid) situation that for a variety of reasons has not appeared on many investors’ radar screens. However, insiders believe the stock is undervalued and instituted a 10b5 plan to buy up to 1million shares at prices up to $2.00 per share (up 33% from current levels). In an unusual situation, the 10b5 was abruptly terminated after only two days due to an error by the broker, and could not be reinstated due to blackout issues. We believe that had this termination not occurred, EMMS’ stock price would be significantly higher today.

Emms operates the 8th largest publicly traded radio portfolio in the United States based on total listeners. Emmis owns 18 FM and two AM radio stations in New York, Los Angeles, St. Louis, Austin, Indianapolis and Terre Haute, IN.

DEBT AS OF LATEST 10-Q

At Feb. 29, 2012, the company had the following debt ($mm):

OPCO:

Revolver $6.0

Term @ L+4: $87.9

Term @ 12.25%: $110.0

Total OPCO debt: $203.8

Holdco:

Notes @ 23.0%: $33.9

Consolidated:

Total Debt $237.7

For the LTM ended Feb. 29, 2012, EMMS generated reported EBITDA of $26.3 mm (or $23.4mm as per Bloomberg and Yahoo), which implies a Debt to Ebitda of 9.0x. However, this reported EBITDA figure includes certain non-recurring items and, as illustrated by the company’s analysis (http://www.emmis.com/investors/quarterly-earnings.aspx then under Quarter 4 click Non-GAAP Leverage Disclosure, 2.29.12 ), a more appropriate LTM EBITDA is $30.8 mm, which implies a still high leverage ratio of 7.7x. However, this ratio comes down significantly when the below asset sales are considered.

ASSET SALES

After the quarter ended, EMMS closed or will soon close 3 transactions that combined should generate $169 million of after tax and fees proceeds that will be used to repay debt.

1) ESPN transaction which has already closed and generated $75 million of cash proceeds.

2) KISS transaction which should generate $10 million of cash proceeds when it closes this summer.

3) Grupo Radio Centro Put/call which should generate $84 million of cash proceeds when it closes this summer.

For more details on these sales, see the earnings call transcript and SEC filings.

REFINANCING OPPORTUNITY

After closing the above asset sales, the company will be much less levered, so the company can refi its debt at significantly lower rates. All of the company’s debt is prepayable with the following caveats. The 12.25% debt is subject to a 6% prepayment fee and due to a make whole provision, its not economically feasible to repay the 23% debt until next May, although we imagine the company could negotiate a prepayment.

A refinancing post-closing of all the asset sales might look like:

Sources:

Asset Sale Proceeds 169.0

New Debt at 6.5% 88.3

Total Sources 257.3

Uses:

Repay Revolver 6.0

Repay Term 87.9

Prepayment fee on 12.25% 6.6

Repay 12.25% Term 110.0

Repay 23% Holdco 41.6 (assumes 1 year of accretion from current balance)

Other Fees 5.0

Total Uses 257.3

Note: on May 30 the company refinanced over $70 million of its debt with a new 4.1% facility, but this isn’t reflected in our analysis.

VALUATION

Pro forma this refinancing, EMMS would have Debt/EBITDA of 3.7x (down significantly from the current levels). Importantly, the company has large NOLs, so it pays no cash taxes and thus delevers more quickly than the debt/ebitda ratio may suggest.

We are assuming the new debt can be obtained at 6.5%.

So, pro forma the refinancing the company will have LTM free cash flow of:

23.8 – Adjusted EBITDA (as per May 10 eps call)

(5.7) -6.5% interest on new debt

(0.0) -Cash taxes (~100mm NOL)

(5.4) – Capex

(2.9) – Preferred dividends

9.7 Free cash flow

Stock Price $1.50

Shares outstanding 38.2

Equity cap 57.3

Equity Cap/Free cash flow 5.9x

But it may be even cheaper than that.

PREFERRED STOCK

On its balance sheet, EMMS has 6.5% preferred stock with a liquidation value of $47 million. In a complicated and controversial transaction, the company repurchased (for ~ $17 per preferred share compared to its $50 per share liquidation value) significant amounts of preferred and is now attempting to strip the remaining preferred stock of its dividends and essentially force each preferred to convert into 2.4 shares of common. There is currently a lawsuit regarding this matter and the next court date is later this summer. We believe EMMS has a good chance of prevailing. However, in order to be conservative, our analysis assumes EMMS loses this issue. However, if EMMS wins, and the preferred convert into 2.3 million common shares and there will be no more dividend payments, the pro forma equity cap would be increase to $60.7 million, pro forma free cash flow would be $12.7 mm (9.7+2.9) and the equity cap/fcf multiple would be 4.8x. The preferred are publicly listed (EMMSP) and last traded at $15 (much less than the $50 liquidation value), but on very light volume.

INSIDER BUYING / 10B5-1

When the window was briefly open after the last earnings release, insiders bought stock. Perhaps most interesting was the activity by Herb Simon (of Simon Property Group). After some earlier purchases at lower prices, on May 16 he bought 98k shares at $1.50. The following day he formed a “partnership” with EMMS’ Chairman/CEO and that entity entered into a 10b5-1 plan that would enable it to buy up to 1.0 million shares at no more than $2.00 per share. On May 17 the partnership bought 98k shares at $1.48 and on May 22nd it bought 106k shares at $1.70 (15% above current price). On May 23 the 10b5 plan was terminated because the broker apparently screwed up by not buying any shares. We believe that since the company was in a blackout period, the 10b5 plan could not be reinitiated. However, the company reports earnings in mid-July at which time the insider buying window would reopen and the 10b5 could be restarted. We believe the $2.00 limit and $1.70 last purchase price give a good sense for what insiders think EMMS is worth. We also believe that had the 10b5 plan not been terminated, EMMS’ stock price would currently be significantly higher not only because of buying by the plan, but also because the frequent insider buying filings would put this (complicated) idea on more investors’ radar screen.

Since the 10b5 plan situation is unusual, below is the announcement from the original 13d.

HSJS, LLC has entered into a Rule 10b5-1 Purchase Plan with Stifel, Nicolaus & Company, Incorporated (“Stifel”) which provides for the purchase of up to 1,000,000 shares of Class A Common Stock, including shares of Class A Common Stock purchased on or after May 17, 2012 by HSJS, LLC. Under the plan, Stifel is not permitted to purchase any shares of Class A Common Stock at a price greater than $2.00 per share. The plan can be terminated at any time subject to the Issuer’s insider trading policy and pre-clearance by the Issuer.

Below is the disclosure in a later 13d announcing the termination of the plan.

Although the Rule 10b5-1 Purchase Plan entered into by HSJS, LLC provided for daily purchases of the Issuer’s Class A Common Stock, subject to certain conditions and limitations, the broker implementing the Purchase Plan failed to purchase any Class A Common Stock on May 23, 2012. The decision not to purchase shares was made without the approval or knowledge of the Reporting Persons. Because the Purchase Plan had been deviated from, HSJS, LLC terminated the Purchase Plan on May 24, 2012.

OTHER

1) This idea has several moving parts so we suggest you read the transcript of the last earning call and view SEC filings and the financial information on the Investors section of the website.

2) While the company does not give guidance, comments from the earning call seem to indicate that this quarter (which will be announced in July) is doing well.

3) Reported results are very deceiving because they do not reflect the asset sales mentioned above. As discussed in the earning call, pro forma these transactions, the business is doing much better than the “reported” results may indicate.

4) Management essentially controls the company thru a dual class of stock and in the past has attempted to take it private. On the last earnings call they indicated they will not try to take it private again.

About the author:

Visit Frank Voisin's Website

Yea I agree, maybe just maybe it's a good thing they are doing it this fast and not waiting it out... The PPS was at a 52 week low not to long ago.. I will be watching ti closely because if phase 3 will be successful then this stock will make for a great buyout target. IMPORTANT news is that they have positive results from there testing.. that is important.

Nice movement going on here. 52 week high and some nice insider buys!

SMULYAN JEFFREY H member of 10% 13(d) group 2012-07-17 Buy 268,100 $1.87 9.09 view

SIMON HERBERT Member of 10% owner 13d group 2012-07-16 Buy 173,600 $1.88 8.51 view

Walsh Patrick M Executive VP, COO/CFO 2012-07-16 Buy 1,630 $1.79 13.97 view

HSJS, LLC Member of 10% owner 13d group 2012-07-16 Buy 173,600 $1.88 8.51 view

*****EMMS Insiders think the stock is undervalued...MUST READ. KEEP IT ON THE RADAR.

ASSET SALES

After the quarter ended, EMMS closed or will soon close 3 transactions that combined should generate $169 million of after tax and fees proceeds that will be used to repay debt.

1) ESPN transaction which has already closed and generated $75 million of cash proceeds.

2) KISS transaction which should generate $10 million of cash proceeds when it closes this summer.

3) Grupo Radio Centro Put/call which should generate $84 million of cash proceeds when it closes this summer.

For more details on these sales, see the earnings call transcript and SEC filings.

Nice insider buys, stock up nice today.

SMULYAN JEFFREY H member of 10% 13(d) group 2012-07-17 Buy 268,100 $1.87 9.09 view

SIMON HERBERT Member of 10% owner 13d group 2012-07-16 Buy 173,600 $1.88 8.51 view

Walsh Patrick M Executive VP, COO/CFO 2012-07-16 Buy 1,630 $1.79 13.97 view

HSJS, LLC Member of 10% owner 13d group 2012-07-16 Buy 173,600 $1.88 8.51 view

http://www.gurufocus.com/news/180109/emmis-communications-important-subsequent-events

Insiders believe the stock is undervalued and instituted a 10b5 plan to buy up to 1million shares at prices up to $2.00 per share (up 33% from current levels). In an unusual situation, the 10b5 was abruptly terminated after only two days due to an error by the broker, and could not be reinstated due to blackout issues. We believe that had this termination not occurred, EMMS’ stock price would be significantly higher today.

But dont forget most of the research has probably been going on during those times when they are burning thru this much cash. Positive news came out just a few days ago and now they are moving along to phase 3 which will require more cash, I think this move was very expected but maybe not this soon.

OPK

CEO been on a buying spree the last few weeks. Frost is known to get bio company's off the ground then flip them for nice $$

FROST PHILLIP MD ET AL , Director, 10% Owner 2012-07-17 Buy 85,000 $4.58 0.87 view

FROST PHILLIP MD ET AL , Director, 10% Owner 2012-07-13 Buy 45,000 $4.61 0.22 view

FROST PHILLIP MD ET AL , Director, 10% Owner 2012-07-12 Buy 30,000 $4.6 0.43 view

FROST PHILLIP MD ET AL , Director, 10% Owner 2012-07-11 Buy 92,500 $4.56 1.32 view

FROST PHILLIP MD ET AL , Director, 10% Owner 2012-07-10 Buy 90,000 $4.61 0.22 view

FROST PHILLIP MD ET AL , Director, 10% Owner 2012-07-09 Buy 45,000 $4.64 -0.43 view

FROST PHILLIP MD ET AL , Director, 10% Owner 2012-07-06 Buy 90,000 $4.7 -1.7 view

FROST PHILLIP MD ET AL , Director, 10% Owner 2012-07-05 Buy 50,000 $4.76 -2.94 view

FROST PHILLIP MD ET AL , Director, 10% Owner 2012-07-03 Buy 45,000 $4.72 -2.12 view

FROST PHILLIP MD ET AL , Director, 10% Owner 2012-07-02 Buy 50,000 $4.65 -0.65 view

Well with the news we received the other day, I think today's news is pretty expected because they will need cash for the next phase and we all know if they can be successful in that phase this stock will rebound big time. I am going to keep a look out for any more insider buys or any more big buys by institutional guys.

I dont see it on my level 2 that it went that low.. But if it did I hope it drops then so we can have another run.

This is great news for us, let the stock reset and it will run again... Great buy at if it reaches $1 or lower.

It's not at a $1, never touched $1... It's at $1.12

It will trade for at least another 3 months

They still have the news from how the conference went this past weekend. Still holding pretty strong here. up still almost 100% from last weeks low.

GALE Back in at $2.02

PSUN looking good lately, Management back on track to turn this company around. Some nice insider buys lately...

Gartner Christine Lee Sr. VP & GMM, Women's 2012-07-06 Buy 27,400 $1.82 49.9 6.59 Link

BREWER BRETT Director 2012-06-25 Buy 30,000 $1.5 45 29.33 Link

STARRETT PETER Director 2012-06-15 Sell 25,000 $1.55 38.8 25.16 Link

Schoenfeld Gary President and CEO

(Click for the stocks that their CEOs have bought) 2012-05-30 Buy 150,000 $1.47 220.5 31.97 Link

MRKONIC GEORGE R JR Director 2012-05-29 Buy 100,000 $1.48 148 31.08 Link

MURNANE THOMAS M Director 2012-06-01 Buy 50,000 $1.55 77.5 25.16 Link

MURNANE THOMAS M Director 2011-06-07 Buy 25,000 $3.19 79.8 -39.18 Link

MURNANE THOMAS M Director 2011-05-31 Buy 31,348 $3.19 100 -39.18 Lin

PSUN Check it out. Some nice insider buys not to long ago.

This is a future that they will be able to licence to other VOIP.

Vonage Holdings Corp. (NYSE: VG), a leading provider of communication services connecting individuals through cloud-connected devices worldwide, today announced the grant of U.S. Pat. No. 8,223,720 titled "Systems and Methods for Handoff of Mobile Telephone Call in a VoIP Environment." This invention allows a mobile handset user who is on a voice-over-IP call to seamlessly move between multiple wireless data connections without dropping the call. The '720 patent was granted approximately 7 months after filing under the U.S. Patent and Trademark Office's new Prioritized Examination Procedure.

Wow that may have just saved the company. Huge news!

I might take a AH position. This is good news.

Was just on the loacl news. Approved!

I agree, I was going to jump in and 1st think I check our insiders buying or selling, because news like this is pretty dam good! But for an insider to dump 2mil shares something smells. Better to hold off and see how it trades tomorrow. If it's going to run we can still chase it a little and get in and out make our $.

Some even dumped as much as 2,000,000 for a loss!

Float dont matter, What I want to know is why most senior guys in the company all sold out 2 weeks before this news hit.. That is the strange part.

Alcatel is getting killed in the handset market. ZTE and Hauwei are killing it. Seeing it this low is very interesting. I am going to take a start position tomorrow and see where this goes.

Can you explain that to me a little better. I dont understand.

Extended Hours 0.55

Last Trade 0.29 (+111.54%)

After Hours Change

826,299

Volume 6:42:09 PM EDT

Good volume but I still dont understand why insiders sold 2 weeks ago for .30...Anyhow I dont pay to much attention to AH right now. Lets see how it does in the AM.

Wow insiders got burned? They sold not to long ago for cheap

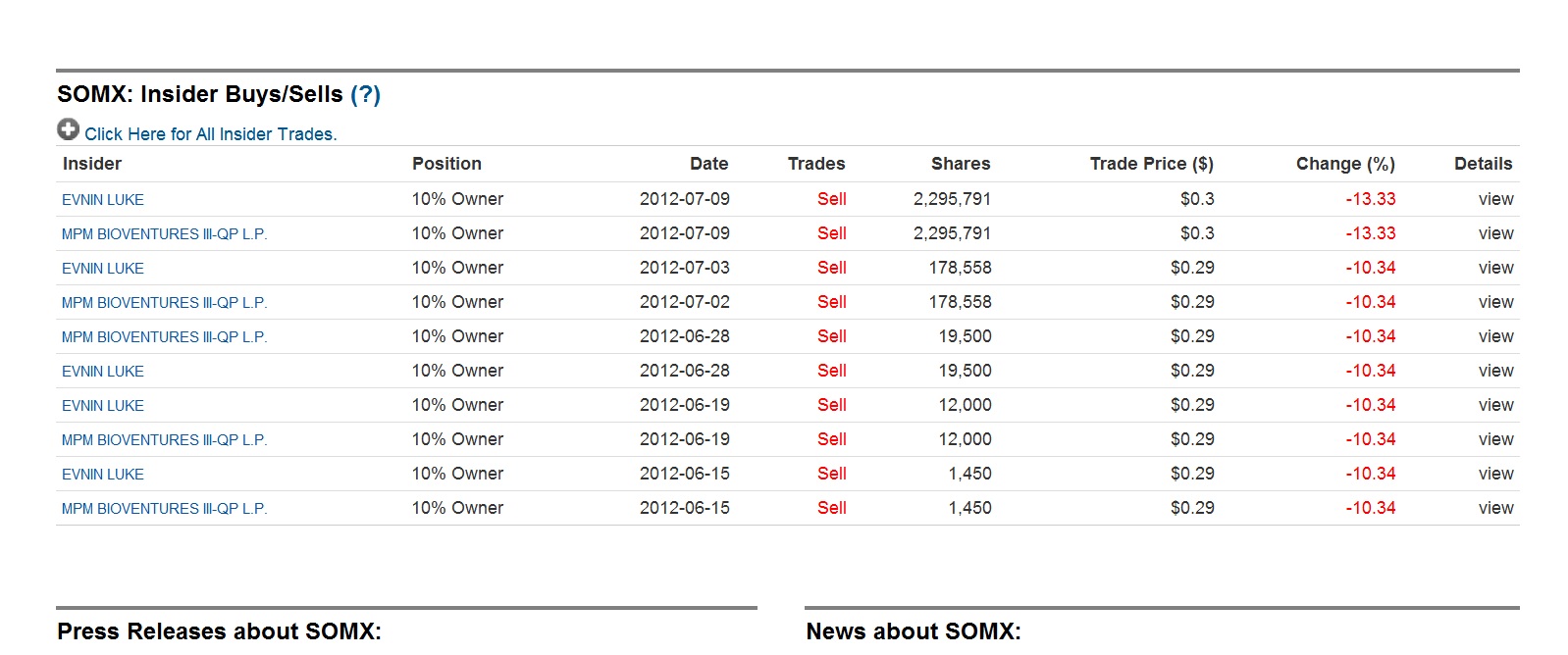

Insider Position Date Trades Shares Trade Price ($) Change (%) Details

EVNIN LUKE 10% Owner 2012-07-09 Sell 2,295,791 $0.3 -13.33 view

MPM BIOVENTURES III-QP L.P. 10% Owner 2012-07-09 Sell 2,295,791 $0.3 -13.33 view

EVNIN LUKE 10% Owner 2012-07-03 Sell 178,558 $0.29 -10.34 view

MPM BIOVENTURES III-QP L.P. 10% Owner 2012-07-02 Sell 178,558 $0.29 -10.34 view

MPM BIOVENTURES III-QP L.P. 10% Owner 2012-06-28 Sell 19,500 $0.29 -10.34 view

EVNIN LUKE 10% Owner 2012-06-28 Sell 19,500 $0.29 -10.34 view

EVNIN LUKE 10% Owner 2012-06-19 Sell 12,000 $0.29 -10.34 view

MPM BIOVENTURES III-QP L.P. 10% Owner 2012-06-19 Sell 12,000 $0.29 -10.34 view

EVNIN LUKE 10% Owner 2012-06-15 Sell 1,450 $0.29 -10.34 view

MPM BIOVENTURES III-QP L.P. 10% Owner 2012-06-15 Sell 1,450 $0.29 -10.34 view

Wow huge news but yet so strange why a ton of insiders sold?

Insider Position Date Trades Shares Trade Price ($) Change (%) Details

EVNIN LUKE 10% Owner 2012-07-09 Sell 2,295,791 $0.3 -13.33 view

MPM BIOVENTURES III-QP L.P. 10% Owner 2012-07-09 Sell 2,295,791 $0.3 -13.33 view

EVNIN LUKE 10% Owner 2012-07-03 Sell 178,558 $0.29 -10.34 view

MPM BIOVENTURES III-QP L.P. 10% Owner 2012-07-02 Sell 178,558 $0.29 -10.34 view

MPM BIOVENTURES III-QP L.P. 10% Owner 2012-06-28 Sell 19,500 $0.29 -10.34 view

EVNIN LUKE 10% Owner 2012-06-28 Sell 19,500 $0.29 -10.34 view

EVNIN LUKE 10% Owner 2012-06-19 Sell 12,000 $0.29 -10.34 view

MPM BIOVENTURES III-QP L.P. 10% Owner 2012-06-19 Sell 12,000 $0.29 -10.34 view

EVNIN LUKE 10% Owner 2012-06-15 Sell 1,450 $0.29 -10.34 view

MPM BIOVENTURES III-QP L.P. 10% Owner 2012-06-15 Sell 1,450 $0.29 -10.34 view

Strong day here, not a bad close at all.

Good call! Sprint is solid and IMO undervalued. Nextel merger really killed it's cash and now they are back to focusing in on building back up there CDMA network. They spent so much time and money on building the iDEN network that they forgot CDMA was much more superior.

I sold yesterday after my trigger hit at $1.10. I went to rebuy and at $1.03 and said wait for $1 then it took off... Made some nice money, but this stock will go back to $2 at some point. The news yesterday was very encouraging news.

Man this in unreal.

ZBB needs some action it loves .35

holding up not to bad. ask still getting pounded.

Let's see how it handles with the dumping now.

lol by that time this stock will be trading at $10+ just like all other stocks when they get FDA approval.

Insiders have been selling for some reason

Hagan Joseph P Chief Business Officer 2012-07-13 Sell 30,000 $6.77

NARACHI MICHAEL President and CEO 2012-07-13 Sell 150,000 $6.7

NARACHI MICHAEL President and CEO 2012-06-29 Sell 225,000 $5.89

Hagan Joseph P Chief Business Officer 2012-06-29 Sell 108,000 $5.53

Booth Mark D Chief Commercial Officer 2012-06-28 Sell 103,309

When Dr. Frost is buyen he knows something is up.

Hes been loading the boat!