News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

investor15

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

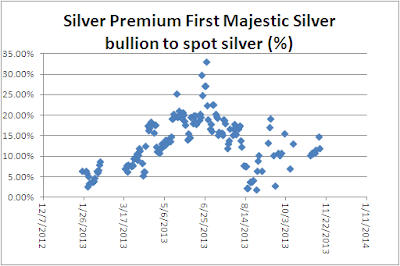

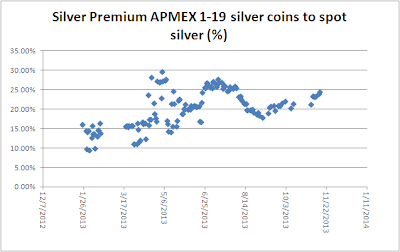

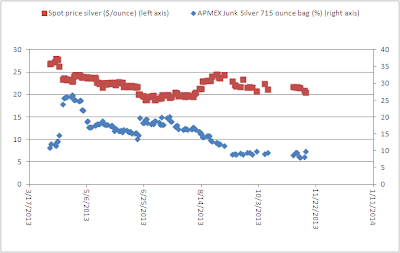

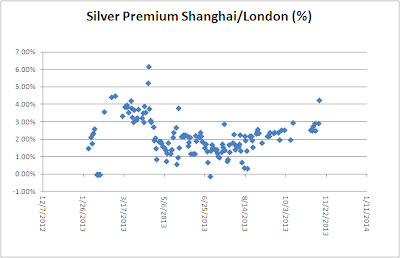

Silver Premiums Going Through The Roof

Nov. 13, 2013

Katchum's Macro-Economic Blog

Just an update on something very interesting in the silver market. We already know the U.S. Mint is selling a lot of silver, but this is also visible in the premiums.

It occurred to me that we are seeing rising premiums again in some miners.

And we see the same thing at some bullion dealers, we are approaching new highs.

Not so much in junk silver.

But take a look at this. I first thought it was a miscalculation, but I checked it thoroughly. It was reality. In Shanghai

we saw a major jump in silver premiums.

It will be interesting to see what the future will bring.

Geplaatst door Albert Sung op 19:22

http://katchum.blogspot.com/

Silver Premiums Going Through The Roof

Nov. 13, 2013

Katchum's Macro-Economic Blog

Just an update on something very interesting in the silver market. We already know the U.S. Mint is selling a lot of silver, but this is also visible in the premiums.

It occurred to me that we are seeing rising premiums again in some miners.

And we see the same thing at some bullion dealers, we are approaching new highs.

Not so much in junk silver.

But take a look at this. I first thought it was a miscalculation, but I checked it thoroughly. It was reality. In Shanghai

we saw a major jump in silver premiums.

It will be interesting to see what the future will bring.

Geplaatst door Albert Sung op 19:22

http://katchum.blogspot.com/

Bill Written by Citibank Lobbyists Gets Banksters Back in High-Risk Derivatives Business – American Taxpayer to Pay for Losses

By Kurt Nimmo

Global Research, November 13, 2013

In late October, the House passed a “bipartisan tweak” to the Dodd-Frank bill Congress earlier passed off as “reform” after the banksters nearly crashed the financial system in 2008.

H.R. 992, the Swaps Regulatory Improvement Act, authored primarily by Citibank lobbyists, will allow predatory Wall Street financial institutions to once again engage in high-risk derivatives trading. Losses will be socialized and paid for by the American taxpayer through the Federal Deposit Insurance Corporation or FDIC.

“Citigroup’s recommendations were reflected in more than 70 lines of the House committee’s 85-line bill,” Eric Lipton and Ben Protess wrote for the New York Times. “Two crucial paragraphs, prepared by Citigroup in conjunction with other Wall Street banks, were copied nearly word for word.”

Co-sponsors of the bill are on the Citibank payroll. They received nearly 17 times more money from the bank than have members of the House who have not signed on as co-sponsors, according to Forbes. “Citigroup has given $503,150 to current members of the House of Representatives,” writes Tom Groenfeldt. “Representative Jim Himes, D-Conn., has received $66,450 from Citigroup, more than any other member of the House of Representatives. Himes is a co-sponsor of the bill.”

Wall Street lobbyists targeted House Democrats. 70 of them came out in support of the bill. Only two Republicans voted thumbs down. They were washed away by overwhelming support for bankster criminality.

According to the chairman of the House Financial Services Committee, Representative Jeb Hensarling, a Republican from Texas, the Dodd-Frank bill revamp will fix the economy. “America’s economy remains stuck in the slowest, weakest nonrecovery recovery of all times,” he said on October 30. “Those who create jobs for America are drowning in a sea of red tape preventing them.”

Hensarling didn’t explain how allowing large banks to play high-stakes blackjack and then force a beleaguered American taxpayer pick up billions in losses will create jobs.

Left to their own devices, banksters will create new “unusual or exigent circumstances” Frank-Dodd was supposedly passed to address. Bank lobbyists have successfully rolled back sections of Frank-Dodd and are now working feverishly to institute a return of the heyday of unencumbered derivatives criminality.

Congress is a wholly owned subsidiary of the bankers and the global elite. The so-called Dodd–Frank Wall Street Reform and Consumer Protection Act signed into law by Obama in 2010 was largely devised as a propaganda device to placate Americans outraged by the “too big to fail” bail-out swindle.

Not surprisingly, Dodd-Frank has been left to twist in the wind. As of June, 175 of 279 passed Dodd-Frank deadlines have been missed. Government regulators have neglected 70.1 percent of rulemaking deadlines and 99.6 percent of 280 rules with specified deadlines, according to Bank Credit News.

Frank-Dodd was never a serious attempt to “reform” bankster financial institutions. Citibank and the money mobsters have paid off Congress. In turn Congress has given the Mafia dens up and down Wall Street a wink and a nod. No significant reform will be forthcoming.

http://www.globalresearch.ca/bill-written-by-citibank-lobbyists-gets-banksters-back-in-high-risk-derivatives-business-american-taxpayer-to-pay-for-losses/5357973

Bankrupting America When Leverage Fails - The Policies of Insolvency Stock-Markets

Nov 13, 2013 - 01:36 PM GMT

By: Ty_Andros

Rarely, if ever, have I seen this level of INSANITY UNFOLDING in over 30 years watching and analyzing GLOBAL macroeconomics, politics and markets. To say it is frightening is to understate the combustible nature of the world economy and its ability to generate future growth and prosperity.

It can't and won't grow without massive reform of governments and their policies, which contrary to public opinion are deepening this MAN-MADE disaster. Conversely, times of great danger and risk offer the most outstanding investment opportunities if you can SEE IT and prepare yourself properly.

"There are two requirements for success in Wall Street. One, you have to think correctly; and secondly, you have to think independently." ~ Ben Graham

The battle lines are clear; on one side of the BATTLE are the most powerful people and elites in the world, led by the Federal Reserve (Bernanke, Yellen and Co.), Bank of England (Mark Carney), and ECB (Mario Draghi). Combined with their partners in the public sectors in the capitals of the developed world: Washington DC (Barack Obama and congress), London (David Cameron and the city), Brussells (European commission) and let's not leave out Beijing, Tokyo and Germany. On the other side of the fight are Mother Nature and Darwin: the apostles of history.

In the long run, Mama Nature and Darwin have never lost this war ever, but in the short run men can appear to be IN CHARGE. In charge of the titanic that is. It is quite clear that the powers that be think they can EXTRACT any amount of blood, treasure and toil and the world will continue to grow. Nothing could be further from the truth and we await the societal & economic collapse for which they are laying the foundations.

Foundations which will be extremely hard to remove and undo as they are embedded in law and the people who must undo them are the same people that CREATED them. Only a crushing blow will roll back the insanity and the future that is coming at us like a freight train.

The socialists in disguise in the developed world's capitals have put their constituents on a modern version of the RACK and are turning the wheels VIGOROUSLY. These elites are Blind ideologues and will INFLICT any AMOUNT of MISERY on their constituents at the point of their regulatory and tax guns to achieve their ambitions of control over others.

A lot of ink has been spilled on the Healthcare.gov failures but the impact that is unfolding is far DEEPER for the future of the world's greatest economy and its private sector. The affordable care act (ACA) is the antithesis of its title: it is wholesale destruction of the healthcare industry and the lives of those who rely upon it. It is everything that socialism is: misery spread widely and less HEALTH care for (crony capitalism) much more money, it is very large doses of poison into people's lives and futures.

You must understand that control of people's lives through control of their healthcare has been a progressive goal (both from the left and the right) for many, many decades. Our system of checks and balances between the various branches of governments and congress has prohibited this dream from being realized.

UNTIL the 2008 election that is, when in a stroke of coincidence gave veto proof majority's and progressives captured complete and total power of the US government. The acceleration of central planned economies and theft of private property through printing press and RUNAWAY regulation was multiplied EXPONENTIALLY, now those balls which began rolling then are hitting the economy like a tip of an iceberg.

"A crisis is a terrible thing to waste" ~ Rahm Emanuel

They didn't let it go to waste as they justified their legislative and executive branch actions as necessary to SAVE you. Unfortunately for us, all they inserted political solutions which served their lust for power over others, the money and themselves rather than practical solutions which serve all the public at large.

The moral and fiscal INSOLVENCY of the financial system was on plain display at that time. Now we are seeing the moral and fiscal insolvency of the system that allowed it to unfold.

As thinly disguised Socialists and Marxists ascended to unbridled power, the total remaking of our institutions was PUT in PLACE. Illinois is one of the epicenters of democratic/socialist corruption and it is on plain display to its residents and onlookers from around the nation, and they rose to power on a national scale 2008. That political corruption took the driver's seat of the national government at that time.

In Illinois, laws are routinely ignored and political foes are destroyed from the misuse of government power. Crony capitalists are generally the only groups which are allowed to thrive and POLITICIANS GUIDE IT ALL as divided government has gone the way of the DO DO bird (extinct), thus corruption is unrestrained. The results are predictable: an economy in free fall with those in charge PREYING upon those who aren't, at the point of a government gun. California and New York are in the SAME BOAT.

These are the places which will be at the vanguard of economic failure in the United States. It is why I recently left Chicago for Florida: to escape the unfolding destruction of my families' future. Most every country in the OECD is in secular decline as centrally planned socialist economies FAIL under their redistributionist policies.

No matter where you look, socialist states are in various stages succumbing to their moral and fiscal insolvency. Argentina, Brazil, Italy, Greece, Portugal, France, Spain each have implemented the same policies, some are further down the path to their demise/chaos and others a just a few steps behind in the SAME process.

Some still have the ability to print money and other don't. It is why the EURO is doomed as those countries which can't print must regain the ability to do so or, quite simply, the elites will be destroyed. Above all else, the euro is a device to transfer power from local governments to Brussels in exchange for the printing press which they NEVER REACH. Sooner or later, the local socialists will break away, recover seignoriege or experience an "off with their head" moment.

We all live in something for nothing societies where the majority of the people think they can live at the expense of the PRODUCTIVE minority and they have firm grips on our elected offices. The governments of the developed world are good reflections of the MAJORITY of their constituents: lazy, thieving, dumbed down, non-self-reliant, unproductive, unable to produce more than they consume, unable to do critical thinking and ignorant of history. USEFUL idiots as Lenin called them. But very dangerous as they are ripe for manipulation and can VOTE!

"A Nation of sheep breeds a government of wolves!" ~ Anonymous

"Any man who thinks he can be happy and prosperous by letting the government take care of him had better take a closer look at the American Indian." ~ Henry Ford

As government dependency caroms exponentially higher, the productive minority is ground under the demands of the majority. They believe they are ENTITLED to the fruits of others labor and VOTE to extract it under the point of a government gun.

They normally NEVER feel the cost of their impossible beliefs that they can live at the expense of others, but this time is DIFFERENT. The affordable care act is hitting them right where it hurts: their incomes and well-being. It now sets up the mother of all showdowns as the victim to victor ratio is enormous.

What is the victim to victor ratio you ask? There are probably ten people who are badly damaged by the law compared to one person whose life is improved. The victims are the very people the President got to vote for him to support the ACA.

Quoting Peggy Noonan -

"They said if you liked your insurance you could keep your insurance - but that's not true. It was never true! They said if you liked your doctor you could keep your doctor - but that's not true. It was never true! They said they would cover everyone who needed it, and instead people who had coverage are losing it - millions of them! They said they would make insurance less expensive - but it's more expensive! Premium shock, deductible shock.

They said don't worry, your health information will be secure, but instead the whole setup looks like a hacker's holiday. Bad guys are apparently already going for your private information. And now there are reports the insurance companies are taking advantage of the chaos of the program, and its many dislocations, to hike premiums. Meaning the law was written in such a way that insurance companies profit on it."

Now the president and progressives in congress are saying to everyone: who do you believe? Me or you're lying eyes. He is going to have a hard time pulling that over on the 4.6 million people who have received insurance pinks slips with millions more to come. Do you really think it is a coincidence that millions are being forced out and into the ACA? The very insurance companies who canceled them await them inside the exchanges with huge premium increases and deductibles. This is intentional folks...

It is clear that as we learn what was in the ACA the more monstrous and pernicious it becomes. It is a regulatory and freedom destructive morass of Washington progressive and special interest WEASEL words. It can be interpreted any way the Washington bureaucrats wish. Regulations and sales of business to crony capitalists who wait in line to buy them through K street lobbyists. Look at the volume of goods sold:

The ACA - whose intent is nothing what it has been presented as. In something for nothing societies, the true impact of policies can never DIRECTLY impact the useful idiots who supported it or the truth becomes SELF apparent. They can only touch them indirectly, so they cannot pin the tails of the donkeys who are preying on them: their leaders.

Now let's cover recent history and put an impact statement for you to consider concerning the national debt and paying for the something for nothing society we inhabit.

Less than 1 month ago (distant memory now) a debt ceiling showdown and government shutdown (God forbid the something for nothings may have had to do something to supplement themselves) was in full bloom and the world was on the brink of disaster (those on the dole cut off from their benefactors within the beltway, and the government unable to print money thru QE), which when resolved supposedly everything was FINE. Quoting the commander in chief:

"Now, this debt ceiling -- I just want to remind people in case you haven't been keeping up -- raising the debt ceiling, which has been done over a hundred times, does not increase our debt; it does not somehow promote profligacy. All it does is it says you got to pay the bills that you've already racked up, Congress. It's a basic function of making sure that the full faith and credit of the United States is preserved." ~ Barrack Obama

Actually, the trouble was obscured from the public who is mostly dependents of government through a variety of programs too numerous to mention. On the day of the debt ceiling resolution, the US debt mushroomed by approximately $329 billion dollars (329,000 million) or $1,061 dollars for every man woman and child in the U.S. The administration has racked up $8 trillion dollars of debt since his inauguration not counting UNFUNDED entitlements.

For your information that is $25,806 dollars for every man woman and child in the U.S. That goes with the $25,000+ dollars borrowed before the current administration in was elected and must be added to obligations which are off balance sheet of 5 times more (approximately $300,000 for every man woman and child in the country). Do the math.

Not one media source informed the public of this insidious fact. Do you think 90 days of big government is worth this price to the public? Why weren't they informed? Main stream Media blackout of the facts? Say it ain't so...

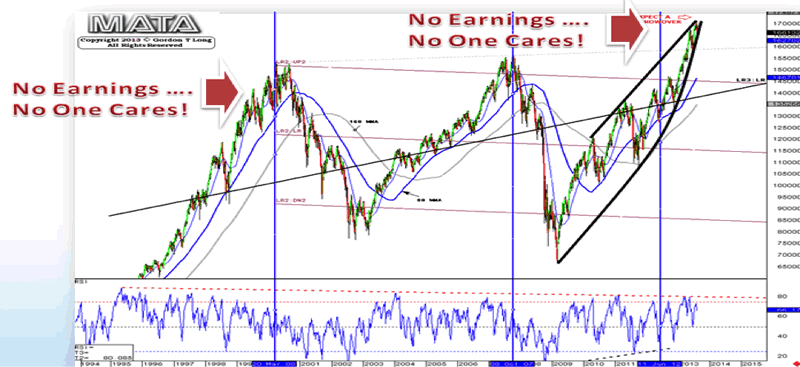

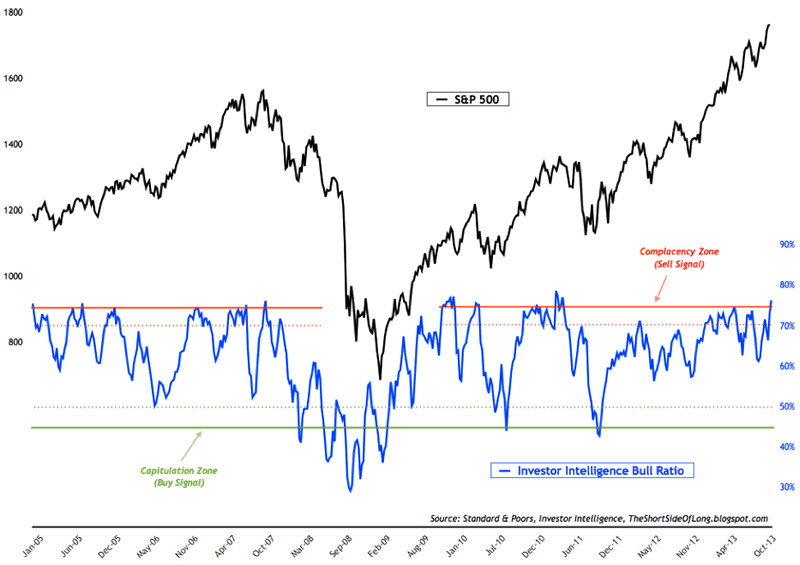

Now on to the stock market where it's become a party like 1999. Insanity is the norm as it was then. Tech companies with valuations in the tens of BILLIONS of dollars on companies with NO EARNINGS. Nothing for sale but hot air, hype and the HOPE of monetizing future growth.

The public and huge money managers are piling in with no fear, with record inflows happening as we speak. Today's Twitter IPO is valuing the company at roughly $30+ Billion dollars, more than the market value of over 337 S&P 500 companies, worth more than GM, John Deere and many more.

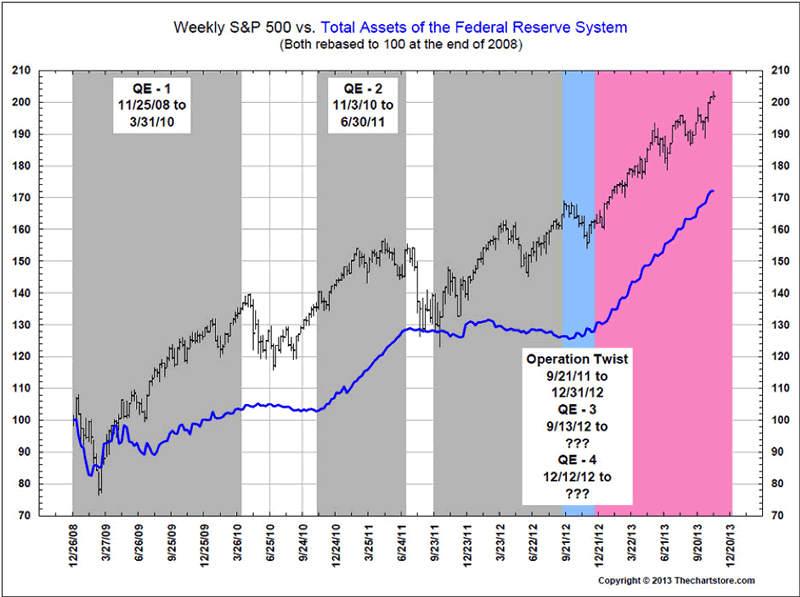

Stocks are floating higher with a direct correlation to the Federal Reserve's EXPLODING balance sheet and the debasement of the currency the S&P is denominated in. It doesn't take a genius to buy this chart until it doesn't work. Take a look at the world's most ugly and widely known chart courtesy of the chart store and Ron Griess;

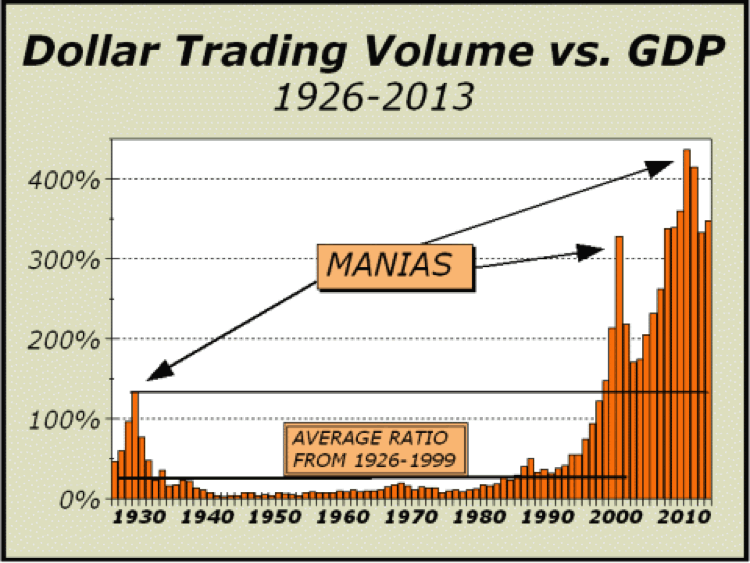

Do you think today's stock markets are moving higher on fundamentals? The ONLY fundamental driving this chart is $4.1 billion dollars and yen ($4,100 million) printed out of thin air on a daily basis and nothing else. And a mania is in full swing (chart courtesy of www.cross-currents.net). Too many dollars chasing too few destinations.

Dollar Trading Volue vs. GDP

Margin use is at record highs which have preceded every market crash in the past 15 years (courtesy www.cross-currents.net):

And bullish newsletter sentiment is at extremes seen at previous market tops:

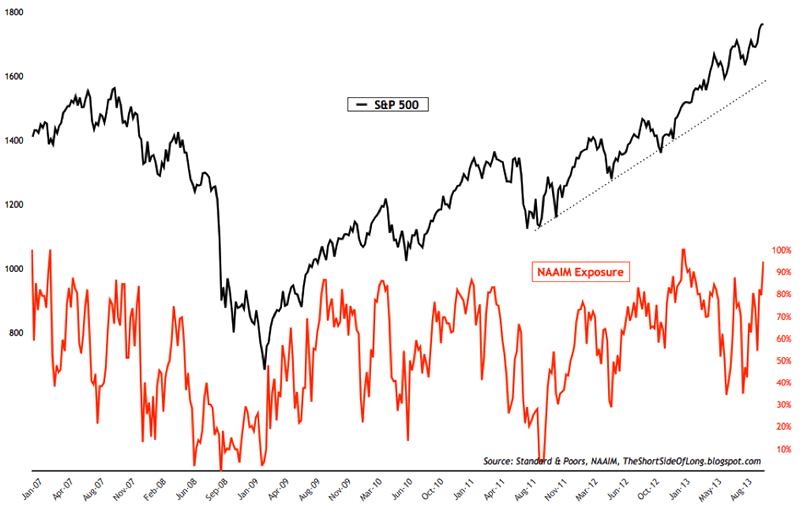

And professional managers are holding extreme levels of long exposure:

People have short memories, and today's troubles obscure the recent past and why REAL economic growth CANNOT RESUME under current government policies IMPLEMENTED since the global financial crisis exploded at that time. And the public is piling in, in a manner not seen since 2007:

[img]www.marketoracle.co.uk/images/2013/Nov/image9.1.png

[/img]

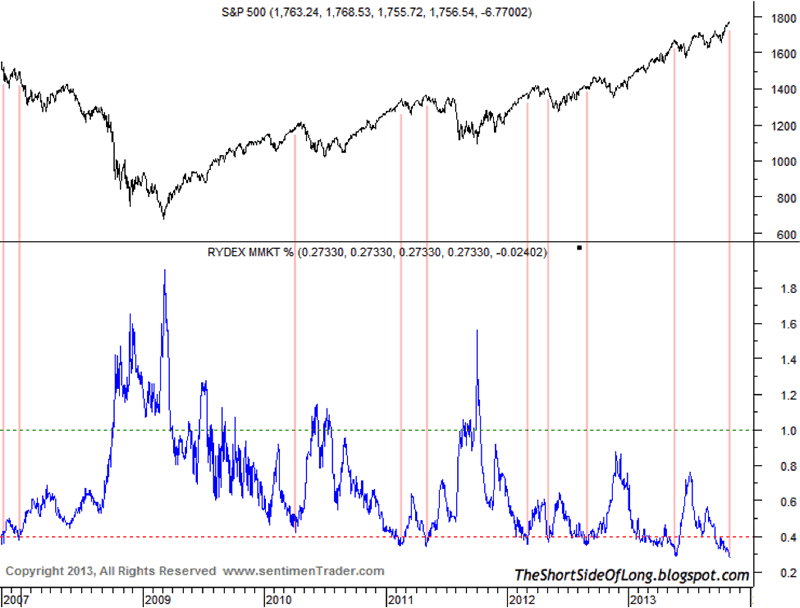

And the retail investor cash levels are now at extreme lows so buying power is now a Fed affair:

With hedge funds approaching record net longs in the tech sector:

[img]www.marketoracle.co.uk/images/2013/Nov/image11.1.png

[/img]

Of course the main stream media tells the public "this time it's different". HA HA... All I can say is someday soon it will be BOMBS away. For these maniacal daredevils, the operative words at this point is "Don't FIGHT the FED" and pray they keep it up. Make no mistake: there will never be a taper, just ask Janet.

In conclusion, as I said several weeks ago: the smell of napalm is in the air. The only thing preventing an explosion is FIREHOSES of NEW money being poured on the fires of insolvency to keep them under control. The purpose of this commentary is not doom and gloom, it is a fire alarm. So you can better prepare yourself to avoid the fires and prepare yourself to benefit from them.

Authors Note: In my opinion, this is NOT Doom and GLOOM, it is one of the greatest opportunities in HISTORY. Invest properly for this outcome and Prosper, invest looking in the REARVIEW mirror and your wealth will be irreparably DAMAGED. Volatility is opportunity for the prepared investor. As it is priced in and markets ZOOM higher or LOWER to price in collapsing economies and money printing huge opportunities are created. Is your portfolio structured to thrive? For a personal consultation with me CLICK HERE!

The crises are now never ending and broad credit growth to the private sector flat to down. But, as I said, this is Mother Nature and Darwin versus the most powerful people on the planet. This is a battle royal to see who determines the face of reality. The Keynesian illusionists or Mother Nature.

Don't miss the next edition of Tedbits, subscriptions are free: CLICK HERE

Tedbits subscribers also get video roundtables with Gordon T. Long, Charles Hugh Smith, John Rubino of www.Dollarcollapse.com, Catherine Austin Fitts, Bert Dohmen and many more, keeping you right in front of breaking news and global macroeconomic analysis.

You do not want to miss the next edition of TedBits. Why not subscribe? Subscriptions are free!

CLICK HERE.

By Ty Andros

TraderView

Copyright © 2013 Ty Andros

http://www.marketoracle.co.uk/Article43099.html

Society is ripe for collapse!” Vanessa Collette interviews Greg McCoach at the 11th Annual Silver Summit

Vanessa Collette | November 12, 2013 - 1:36am

Ronald Reagan Predicted The Obamacare Disaster Back In 1961

Steve Hayward

11/5/2013

Forbes

Ronald Reagan had an uncanny way of predicting the future and offering ideas that were way ahead of their time. In the 1960s he proposed privatizing the Tennessee Valley Authority, an idea the Obama Administration now embraces. In the 1970s he discussed private retirement accounts as an alternative to Social Security, a reform idea that has become popular today. And of course he predicted the end of the Soviet Union, which seemed laughable to liberals when he said it in 1982, but came true just a few years later.

Reagan also predicted the disaster of Obamacare, and for the specific reasons we see unfolding right now. But if Reagan’s analysis is correct, the worst is still to come.

In his famous speech for Barry Goldwater in 1964, Reagan observed that “the doctor’s fight against socialized medicine is your fight. We can’t socialize the doctors without socializing the patients.”

The second half of this is rapidly coming true, in the form of the millions who are having their health insurance policies canceled despite Obama’s false promise that if you like your health insurance you can keep your health insurance. It is necessary to the redistributionist logic of Obamacare that millions be required to cross-subsidize the health insurance of others. Hence, free choice between consumers and insurers has to be regulated out of existence.

But patients are already finding that they aren’t just losing their current health insurance; many are losing their doctors, too. And predictably Obamacare’s desperate defenders are openly embracing government coercion to solve this problem. In other words, we’re going to socialize the doctors, too. This problem is not brand new. Many doctors and medical practice groups have limited the number of Medicaid and Medicare patients they will treat because low (and slow) government reimbursement rates make them unprofitable. This problem is likely to grow worse under Obamacare.

A Democratic candidate for the Virginia state legislature in this week’s election advocates making it mandatory for doctors and medical practices to accept all Medicare and Medicaid patients, despite what this might do to the financial health of the doctors and their practice groups. This is only a short step from wholesale regulation of the way medicine is practiced, which will also prove necessary to fulfill the redistributionist design of Obamacare.

Reagan was on to this in his famous 1961 recording criticizing the original Medicare scheme:

Today, the relationship between patient and doctor in this country is something to be envied any place. The privacy, the care that is given to a person, the right to choose a doctor, the right to go from one doctor to the other.

But let’s also look from the other side, at the freedom the doctor loses. A doctor would be reluctant to say this. Well, like you, I am only a patient, so I can say it in his behalf. The doctor begins to lose freedoms; it’s like telling a lie, and one leads to another. First you decide that the doctor can have so many patients. They are equally divided among the various doctors by the government. But then the doctors aren’t equally divided geographically, so a doctor decides he wants to practice in one town and the government has to say to him you can’t live in that town, they already have enough doctors. You have to go someplace else. And from here it is only a short step to dictating where he will go.

One of the reasons Hillarycare collapsed back in 1994 was its proposal to regulate the number, kind, and location of medical specialities throughout the entire country. When people realized that Hillarycare meant that they might not be able to choose their doctor or specialist, public support for Hillrycare, initially very strong, collapsed. This was the reason Obama felt it necessary to offer the promise that we could keep our insurance and doctors if we liked them. But it was never going to work out this way, as Obama’s technocrats knew early on. Even when you begin only by targeting the uninsured, socialized medicine, as Reagan understood, requires “indefinite expansion in every direction until it includes the entire population.”

And as Reagan said in 1961, one lie leads to another. In modern times we’re supposed to be cynical about government deceptions, but Obama’s promise is arguably the greatest single lie in the history of American politics. Reagan also said at the time, “Well, we can’t say we haven’t been warned.”

http://www.forbes.com/sites/stevenhayward/2013/11/05/ronald-reagan-predicted-the-obamacare-disaster-back-in-1961/

What A Confidential 1974 Memo To Paul Volcker Reveals About America's True Views On Gold, Reserve Currency And "PetroGold"

Tyler Durden on 11/11/2013 22:09 -0500

Zero Hedge

Just over four years ago, we highlighted a recently declassified top secret 1968 telegram to the Secretary of State from the American Embassy in Paris, in which the big picture thinking behind the creation of the IMF's Special Drawing Right (rolled out shortly thereafter in 1969), or SDRs, was laid out. In that memo it was revealed that despite what some may think, the fundamental driver behind the promotion of a supranational reserve paper currency had one goal in mind: allowing the US to "remain masters of gold."

Specifically, this is among the top secret paragraphs said on a cold night in March 1968:

If we want to have a chance to remain the masters of gold an international agreement on the rules of the game as outlined above seems to be a matter of urgency. We would fool ourselves in thinking that we have time enough to wait and see how the S.D.R.'s will develop. In fact, the challenge really seems to be to achieve by international agreement within a very short period of time what otherwise could only have been the outcome of a gradual development of many years.

This then puts into question just what the true purpose of the IMF is. Because while its stated role of preserving the stability in developing, and increasingly more so, developed, countries is a noble one, what appears to have been the real motive behind the monetary fund's creation, was to promote and encourage the development of a substitute reserve currency, the SDR, and to ultimately use it as the de facto buffer and intermediary, for conversion of all the outstanding "barbarous relic" hard currency, namely gold, into the fiat of the future: the soon to be newly created SDR. All the while, and increasingly more so as more countries converted their gold into SDR, such remaining hard currency would be almost exclusively under the control of the United States.

Well, in the intervening 44 years, the SDR never managed to take off, the reason being that the dollar's reserve currency status was exponentially cemented courtesy of both the great moderation of the 1980s and the derivative explosion of the 1990s and post Glass Steagall repeal 2000s, when the world was literally flooded with roughly $1 quadrillion in USD-denominated derivatives, inextricably tying the fate of the world to that of the dollar.

However, back in 1974, shortly after Nixon ended the Bretton Woods system, and cemented the dollar's fate as a fiat currency, no longer convertible into gold, the future of the SDR was still bright, especially at a time when the US seemed set to suffer a very unpleasant date with inflationary reality following the 1973 oil crisis, leading to a potential loss of faith in the US dollar.

Which brings us to the topic of today's article: the international monetary system, reserve currency status, SDRs, and, of course, gold... again.

Below is a memo written in 1974 by Sidney Weintraub, Deputy Assistant Secretary of State for International Finance and Development, to Paul Volcker, when he was still just Under Secretary of the Treasury for Monetary Affairs and not yet head of the Federal Reserve. The source of the memo was found in the National Archives, RG 56, Office of the Under Secretary of the Treasury, Files of Under Secretary Volcker, 1969–1974, Accession 56–79–15, Box 1, Gold—8/15/71–2/9/72. No classification marking. A stamped notation on the note reads: "Noted by Mr. Volcker." Another notation, dated March 8, indicates that copies were sent to Bennett and Cross. It currently resides in declassified form in Document 61, Foreign Relations Of The United States, 1973–1976, Volume XXXI Foreign Economic Policy, and is found at the Office of the Historian website.

The memo is a continuation of the US thinking on the issue of the then brand new SDR, the fate of paper currencies, and the preservation of US control over reserve currency status. Most importantly, it addresses several approaches to dominating gold as well as the US' interest of banning gold from monetary system and capping the free market price, contrasted by the opposing demands of various European deficit countries (sound familiar?) on what the fate of gold should be at a time when the common European currency did not exist, and some European countries were willing to fund their deficits with gold: something the US naturally was not happy about.

While we urge readers to read the full memo on their own, here the two punchlines.

First, here is what the S intentions vis-a-vis gold truly are when stripped away of all rhetoric:

U.S. objectives for world monetary system—a durable, stable system, with the SDR [ZH: or USD] as a strong reserve asset at its center — are incompatible with a continued important role for gold as a reserve asset.... It is the U.S. concern that any substantial increase now in the price at which official gold transactions are made would strengthen the position of gold in the system, and cripple the SDR [ZH: or USD].

In other words: gold can not be allowed to dominated a "durable, stable system", and a rising gold price would cripple the reserve currency du jour: well known by most, but always better to see it admitted in official Top Secret correspondence.

We continue:

To encourage and facilitate the eventual demonetization of gold, our position is to keep the present gold price, maintain the present Bretton Woods agreement ban against official gold purchases at above the official price and encourage the gradual disposition of monetary gold through sales in the private market. An alternative route to demonetization could involve a substitution of SDRs for gold with the IMF, with the latter selling the gold gradually on the private market, and allocating the profits on such sales either to the original gold holders, or by other agreement.... Any redefinition of the role of gold must be based on the principle stated above: that SDR must become the center of the system and that there can be no question of introducing a new form of gold– paper and gold–metal bimetallism, in which the SDR and gold would be in competition.

And there, in three sentences, you have all the deep thinking behind the IMF's SDR: simply to use it as a vehicle through which a select few can accumulate gold (namely those who can create fiat SDRs d novo), while handing out paper "profits" to the happy sellers.

And just in case it was not quite clear, here it is again, point blank:

Option 3: Complete short-term demonetization of gold through an IMF substitution facility. Countries could give up their gold holdings to the IMF in exchange for SDRs. The gold could then be sold gradually, over time, by the IMF to the private market. Profits from the gold sales could be distributed in part to the original holders of the gold, allowing them to realize at least part of the capital gains, while part of the profits could be utilized for other purposes, such as aid to LDCs. Advantages: This would achieve our goal of demonetization and relieve the problem of gold immobility, since the SDRs received in exchange could be used for settlement with no fear of foregoing capital gains. Disadvantages: This might be a more rapid demonetization than several countries would accept. There would be no benefit from the viewpoint of financing oil imports with gold sales to Arabs (although it is not necessarily incompatible with such an arrangement).

One wonders just who in the "private market" would be stupid enough to convert their invaluable paper money into worthless, barbaric relics?

And finally, was there the tiniest hint of a proposed alternative system to the PetroDollar. Namely, PetroGold?

There is a belief among certain Europeans that a higher price of gold for settlement purposes would facilitate financing of oil imports... Although mobilization of gold for intra-EC settlement would help in the financing of imbalances among EC countries, it would not, of itself, provide resources for the financing of the anticipated deficit with the oil producers. For this purpose, it would be useful if the oil producers would invest some of their excess revenues in gold purchases from deficit EC countries at close to a market price. This would be an attractive proposal for European countries, and for the U.S., in that it would not involve future interest burdens and would avoid immediate problems arising from increased Arab ownership of European and American industry. (The Arabs could both sell the gold and use the proceeds for direct investment, so that the industry ownership problem would not be completely solved.) From the Arab point of view such an asset would have the advantages of being protected from exchange-rate changes and inflation, and subject to absolute national control.

One wonders if the price of gold is "high enough" now for Arab purposes, and just where the Arabs are now in their thinking of converting oil into gold... or alternatively into a gold-backed renminbi. And if not now, soon, once the pent up inflation in the Fed's $4 trillion, and rising, balance sheet inevitably start to leak out?

The full Volcker memo can be found here.

h/t Koos Jansen

http://www.zerohedge.com/news/2013-11-11/what-confidential-1974-memo-paul-volcker-reveals-about-americas-true-views-gold-rese

What A Confidential 1974 Memo To Paul Volcker Reveals About America's True Views On Gold, Reserve Currency And "PetroGold"

Tyler Durden on 11/11/2013 22:09 -0500

Zero Hedge

Just over four years ago, we highlighted a recently declassified top secret 1968 telegram to the Secretary of State from the American Embassy in Paris, in which the big picture thinking behind the creation of the IMF's Special Drawing Right (rolled out shortly thereafter in 1969), or SDRs, was laid out. In that memo it was revealed that despite what some may think, the fundamental driver behind the promotion of a supranational reserve paper currency had one goal in mind: allowing the US to "remain masters of gold."

Specifically, this is among the top secret paragraphs said on a cold night in March 1968:

If we want to have a chance to remain the masters of gold an international agreement on the rules of the game as outlined above seems to be a matter of urgency. We would fool ourselves in thinking that we have time enough to wait and see how the S.D.R.'s will develop. In fact, the challenge really seems to be to achieve by international agreement within a very short period of time what otherwise could only have been the outcome of a gradual development of many years.

This then puts into question just what the true purpose of the IMF is. Because while its stated role of preserving the stability in developing, and increasingly more so, developed, countries is a noble one, what appears to have been the real motive behind the monetary fund's creation, was to promote and encourage the development of a substitute reserve currency, the SDR, and to ultimately use it as the de facto buffer and intermediary, for conversion of all the outstanding "barbarous relic" hard currency, namely gold, into the fiat of the future: the soon to be newly created SDR. All the while, and increasingly more so as more countries converted their gold into SDR, such remaining hard currency would be almost exclusively under the control of the United States.

Well, in the intervening 44 years, the SDR never managed to take off, the reason being that the dollar's reserve currency status was exponentially cemented courtesy of both the great moderation of the 1980s and the derivative explosion of the 1990s and post Glass Steagall repeal 2000s, when the world was literally flooded with roughly $1 quadrillion in USD-denominated derivatives, inextricably tying the fate of the world to that of the dollar.

However, back in 1974, shortly after Nixon ended the Bretton Woods system, and cemented the dollar's fate as a fiat currency, no longer convertible into gold, the future of the SDR was still bright, especially at a time when the US seemed set to suffer a very unpleasant date with inflationary reality following the 1973 oil crisis, leading to a potential loss of faith in the US dollar.

Which brings us to the topic of today's article: the international monetary system, reserve currency status, SDRs, and, of course, gold... again.

Below is a memo written in 1974 by Sidney Weintraub, Deputy Assistant Secretary of State for International Finance and Development, to Paul Volcker, when he was still just Under Secretary of the Treasury for Monetary Affairs and not yet head of the Federal Reserve. The source of the memo was found in the National Archives, RG 56, Office of the Under Secretary of the Treasury, Files of Under Secretary Volcker, 1969–1974, Accession 56–79–15, Box 1, Gold—8/15/71–2/9/72. No classification marking. A stamped notation on the note reads: "Noted by Mr. Volcker." Another notation, dated March 8, indicates that copies were sent to Bennett and Cross. It currently resides in declassified form in Document 61, Foreign Relations Of The United States, 1973–1976, Volume XXXI Foreign Economic Policy, and is found at the Office of the Historian website.

The memo is a continuation of the US thinking on the issue of the then brand new SDR, the fate of paper currencies, and the preservation of US control over reserve currency status. Most importantly, it addresses several approaches to dominating gold as well as the US' interest of banning gold from monetary system and capping the free market price, contrasted by the opposing demands of various European deficit countries (sound familiar?) on what the fate of gold should be at a time when the common European currency did not exist, and some European countries were willing to fund their deficits with gold: something the US naturally was not happy about.

While we urge readers to read the full memo on their own, here the two punchlines.

First, here is what the S intentions vis-a-vis gold truly are when stripped away of all rhetoric:

U.S. objectives for world monetary system—a durable, stable system, with the SDR [ZH: or USD] as a strong reserve asset at its center — are incompatible with a continued important role for gold as a reserve asset.... It is the U.S. concern that any substantial increase now in the price at which official gold transactions are made would strengthen the position of gold in the system, and cripple the SDR [ZH: or USD].

In other words: gold can not be allowed to dominated a "durable, stable system", and a rising gold price would cripple the reserve currency du jour: well known by most, but always better to see it admitted in official Top Secret correspondence.

We continue:

To encourage and facilitate the eventual demonetization of gold, our position is to keep the present gold price, maintain the present Bretton Woods agreement ban against official gold purchases at above the official price and encourage the gradual disposition of monetary gold through sales in the private market. An alternative route to demonetization could involve a substitution of SDRs for gold with the IMF, with the latter selling the gold gradually on the private market, and allocating the profits on such sales either to the original gold holders, or by other agreement.... Any redefinition of the role of gold must be based on the principle stated above: that SDR must become the center of the system and that there can be no question of introducing a new form of gold– paper and gold–metal bimetallism, in which the SDR and gold would be in competition.

And there, in three sentences, you have all the deep thinking behind the IMF's SDR: simply to use it as a vehicle through which a select few can accumulate gold (namely those who can create fiat SDRs d novo), while handing out paper "profits" to the happy sellers.

And just in case it was not quite clear, here it is again, point blank:

Option 3: Complete short-term demonetization of gold through an IMF substitution facility. Countries could give up their gold holdings to the IMF in exchange for SDRs. The gold could then be sold gradually, over time, by the IMF to the private market. Profits from the gold sales could be distributed in part to the original holders of the gold, allowing them to realize at least part of the capital gains, while part of the profits could be utilized for other purposes, such as aid to LDCs. Advantages: This would achieve our goal of demonetization and relieve the problem of gold immobility, since the SDRs received in exchange could be used for settlement with no fear of foregoing capital gains. Disadvantages: This might be a more rapid demonetization than several countries would accept. There would be no benefit from the viewpoint of financing oil imports with gold sales to Arabs (although it is not necessarily incompatible with such an arrangement).

One wonders just who in the "private market" would be stupid enough to convert their invaluable paper money into worthless, barbaric relics?

And finally, was there the tiniest hint of a proposed alternative system to the PetroDollar. Namely, PetroGold?

There is a belief among certain Europeans that a higher price of gold for settlement purposes would facilitate financing of oil imports... Although mobilization of gold for intra-EC settlement would help in the financing of imbalances among EC countries, it would not, of itself, provide resources for the financing of the anticipated deficit with the oil producers. For this purpose, it would be useful if the oil producers would invest some of their excess revenues in gold purchases from deficit EC countries at close to a market price. This would be an attractive proposal for European countries, and for the U.S., in that it would not involve future interest burdens and would avoid immediate problems arising from increased Arab ownership of European and American industry. (The Arabs could both sell the gold and use the proceeds for direct investment, so that the industry ownership problem would not be completely solved.) From the Arab point of view such an asset would have the advantages of being protected from exchange-rate changes and inflation, and subject to absolute national control.

One wonders if the price of gold is "high enough" now for Arab purposes, and just where the Arabs are now in their thinking of converting oil into gold... or alternatively into a gold-backed renminbi. And if not now, soon, once the pent up inflation in the Fed's $4 trillion, and rising, balance sheet inevitably start to leak out?

The full Volcker memo can be found here.

h/t Koos Jansen

http://www.zerohedge.com/news/2013-11-11/what-confidential-1974-memo-paul-volcker-reveals-about-americas-true-views-gold-rese

Shadow banks reap Fed rate reward

Published: Monday, 11 Nov 2013 | 3:06 PM ET

By: Sam Fleming

Financial Times

Jasper James | Stone | Getty Images

Loosely regulated non-bank lenders have emerged as among the biggest beneficiaries of the Federal Reserve's ultra-low interest rates with three specialist categories increasing their assets by almost 60 percent since the height of the financial crisis.

Such lenders, widely considered part of the "shadow banking" system, have expanded rapidly on the back of investors who are clamoring for the higher returns on offer from financing riskier types of lending.

Shadow banking has been steadily climbing the regulatory agenda, with the Financial Stability Board this summer proposing a package of measures aimed at curbing excessive risk-taking in the sector. The regulators' concern is that many of these lenders could over-borrow or make increasingly dicey loans as they rush to take advantage of historically low rates, exuberant markets and the retreat of traditional banks from certain businesses in response to tougher regulation.

"Think of it like a pipeline," says Dan Zwirn, managing partner of Arena Investors, a hedge fund focused on lending to companies that most banks will not lend to. "When you can connect the pipe between a type of asset and yield-hungry investors, then what happens is that issuance grows."

(Read More: Ronald Coase and the nature of shadow banking)

The amount of assets held by US business development companies (BDCs), specialist finance companies and real estate investment trusts (Reits) has jumped from $779 billion in 2008 to $1.22 trillion in the second quarter of 2013, according to data compiled by SNL Financial for the Financial Times.

The rapid growth of Reits, which borrow in the short term financial markets to make tax-favorable investments in longer-term assets like mortgage bonds, has drawn the attention of US regulators.

The New York Fed probed US banks' exposure to the investment vehicles earlier this year, amid concern that a rapid rise in rates could trigger a sell-off that would affect larger banking institutions. Last week, researchers at the Richmond Fed said that while Reits had "mushroomed" since the crisis, it remained unclear what risk they might pose to the financial system.

Regulators are attempting to strengthen oversight of the lightly-regulated sector while avoiding measures that would stifle its ability to contribute to the recovery.

Last month, Mark Carney, the FSB's chair and Bank of England governor, floated the option of opening up access to the BoE's liquidity facilities to non-banks, while adding that this would mean extending the reach of regulation.

Paul Tucker, the former Bank of England deputy governor, warned the same month that regulators need to "up their game" in overseeing hedge funds and shadow banks. He said it would be "disastrous" if the fragility of mainstream banks gets recreated beyond the mainstream banking sector, calling for securities regulators to improve the quality of data they are collecting on non-banks.

BDCs provide capital and loans for middle-market companies, using a tax-favorable structure that is similar to Reits. While the leverage of BDCs is capped under law, they too have experienced rapid growth in recent years, leading to heightened competition.

"Underwriting standards go lower, interest rate risk goes higher," said Mr Zwirn, adding that many BDCs have sought to boost returns by purchasing the riskiest pieces of collateralized loan obligations or the equity of specialist finance companies that are allowed higher leverage rates than BDCs.

Some such companies which proliferated before the financial crisis are still reducing the troubled assets they collected before 2008, while others have been expanding in fields such as lending to people with flawed credit histories to fill a gap left by retreating banks.

Springleaf, the former subprime consumer lending arm of the bailed-out mega-insurer AIG, has been able to take advantage of a turnaround in securitization markets to repackage its loans into asset-backed securities and expand its business.

"The combination of increased capital requirements and regulatory focus will make it harder for banks to serve non-prime customers," said Steven Moffitt, who leads the consumer structured finance team at Goldman Sachs.

He estimates that 25 to 40 per cent of bank customers will need to source credit from non-bank entities, potentially leading to further growth for specialty lenders.

http://www.cnbc.com/id/101188282

Obamashock! Hits Employees of Sodexo, "World's Largest Quality of Life" Service Company

Nov. 10, 2013

Mish's Global Ecnomic TrendAnalysis

Some employees of Sodexo, the "World's largest quality of life services company" have been hit with a massive case of "Obamashock!" because of the way Obamacare identifies part-time employment.

An email from reader "Mark" will explain.

Hello Mish

I thought you would be interested in another new angle regarding fallout from the ACA.

Yesterday we received a notice of cancellation of our eligibility in the large group health plan through my wife's employer. They state that this is due to the Affordable Care Act.

My wife has worked for Sodexo, USA for about 3 years.Sodexo is a contract food service provider at literally thousands of institutions around the world. Her job is at a small private college in Iowa.

The notice we received states that, "Sodexo has aligned how we define full-time employees eligible for benefits with the Affordable Care Act". As such, she no longer qualifies as a full time employee, and can no longer be part of the benefit plan, as of January 1, 2014.

The new definition is that a full time employee must average 30 hours a week over the past 12 months. The cafeteria at a private college is not open 12 months of the year, and does not operate an average of 30 hours per week over 12 months. It is impossible to attain this number of hours when they are not available.

I am self employed. We will not qualify for any 'exchange subsidies'. She worked this just over minimum wage job solely for access to the health plan.

Now our options seem to be either to pay $19,600.52 per year for the COBRA plan, or $12,636 for an individual family plan with a deductible that is 3 times our current plan.

We are definitely in Obamashock!

Mike "Mish" Shedlock

http://globaleconomicanalysis.blogspot.com

Read more at http://globaleconomicanalysis.blogspot.com/2013/11/obamashock-hits-employees-of-sodexo.html#tBtm6vQdDwawjzwe.99

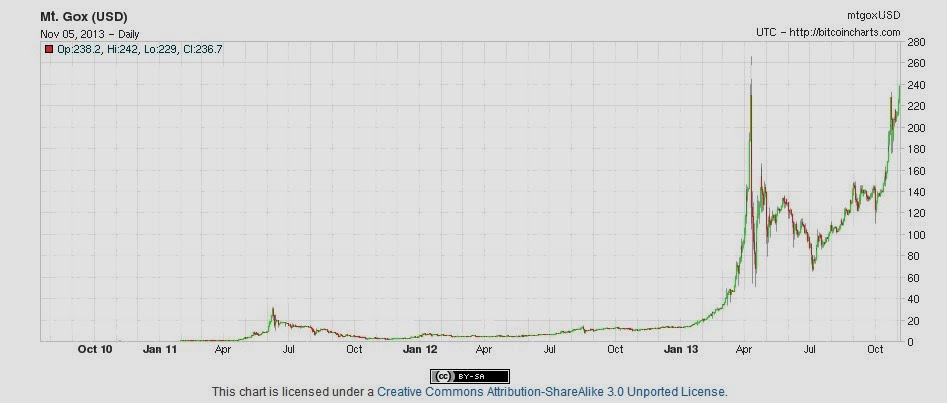

Federal Reserve Economist On Bitcoin: 'Small Phenomenon But Growing'

11/7/2013

Kashmir Hill

Forbes

The price of Bitcoin reaches a new high this week, nearing and passing $300 on major exchanges

(image via Zero Block)

It’s a big moment for Bitcoin. The digital currency has gotten an official nod from the overseer of U.S. currency in the form of a primer out of the Federal Reserve Bank of Chicago. Senior economist François R. Velde wrote an elegant critique of the four-year-old currency, explaining its mechanics, limitations, and prospects for success, ultimately deeming it a “remarkable conceptual and technical achievement, which may well be used by existing financial institutions.” If this were Economic Mean Girls, this is the part of the movie where Lindsay ‘Bitcoin’ Lohan gets friended by the powerful, popular crowd.

Velde starts out by laying out the numbers. Producing a bitcoin “at current levels of difficulty requires a machine worth about $3,000 and about a dollar’s worth of electricity per day,” meaning the cost of producing one bitcoin, taking into account the machine’s depreciation over five years, is about $2.50. While the estimate seems to discount the steadily rising cost of higher-powered machines that are necessary for more complex hashing — and the pools of machines necessary for mining — with Bitcoins currently valued at 100 times that, you can see why companies offering ‘mining’ equipment are doing such good business.

Velde points out that there is $1,200 billion circulating in U.S. currency compared to $1 billion in Bitcoin (when he authored the December 2013 paper). Thanks to a recent price surge to over $250, the market cap for the nearly 12 million Bitcoin in existence is now well over $3 billion, but even given that, Bitcoin is a “relatively small phenomenon,” as Velde puts it. “But it has been growing,” he writes. “[T]he value of a bitcoin has increased tenfold since early 2013.”

To further put it into the context of the larger economy, he writes that “there are on average about 30 bitcoin transactions per minute” vs. 200,000 Visa transactions per minute, and that the average bitcoin transaction size is “about 16, i.e., on the order of $2,000? while “the average Visa transaction is about $80.” At that level of spending, it’s fairly obvious that most of the activity happening in Bitcoin is not actually buying things (as I did in May), but rather trading. (Of course, every once in a while someone might drop a cool mil on mining gear.)

“So far, the uses of bitcoin as a medium of exchange appear limited, particularly if one excludes illegal activities,” notes Velde. “It has been used as a means to transfer funds outside of traditional and regulated channels and, presumably, as a speculative investment opportunity.”

(And occasionally to circumvent trade sanctions for a pair of Persian sneaks.)

For those who have pondered what bitcoin actually is — currency vs. stock vs. money — Velde has an answer. It’s a fiduciary currency, he writes, explaining it has no intrinsic value meaning it’s “inherently fragile,” deriving value only from “exchange either from government fiat or from the belief that they may be accepted by someone else.” That’s much like the no-longer-gold-backed U.S. dollar, say many Bitcoin believers.

So is it viable as a currency people would actually want to use for anything beyond Silk Road 2.0, asks Velde. While Bitcoin attempts to act like cash online, there are “costs.”

“One prominent cost is the loss of anonymity,” he writes. One of the biggest myths around bitcoin is that it is “anonymous.” While it is has been useful for getting your fix online because a purchase with it entails far less personal information than using a credit card or Paypal account, the currency’s security is predicated on the fact that everything is traceable. So you only remain anonymous if you never tie a purchase to your identity.

“Possession of the virtual currency must be linked to the unique identifier of the wallet,” writes Velde. “Admittedly, there is no limit on the number of wallets one can own and there are ways to make the wallet hard to trace back to its owner, but these require additional efforts.”

The other cost is speed. While small transactions with Bitcoin are usually processed immediately, larger ones take longer because they must be confirmed by miners and that only happens when the transactions are included in the block chain which happens about every ten minutes. “For large amounts it is customary to wait for six blocks, or one hour,” writes Velde. That is long but for those of us who have had Paypal freeze a transaction for five days (as it did when I tried to send a large amount to a new person as a security deposit on my apartment) or when a bank refuses to send a wire transfer at all, it does not seem like that long a delay.

“Why this delay to complete bitcoin transactions?” writes Velde. “It is rooted in the decentralized nature of the bitcoin network (and its reliance on a sort of majority voting), which is both its most ambitious feature and its main vulnerability.”

Chicago Fed senior economist François Velde, a specialist in monetary history and monetary theory, tackles Bitcoin

Velde is most critical of the governance structure of Bitcoin. The code is deployed by a group of five core developers — who are loosely empowered with the responsibility for deciding when Bitcoin is “broken” — with a larger body of Bitcoin users and miners deciding on changes to be made.

“Although some of the enthusiasm for bitcoin is driven by a distrust of state-issued currency,” writes Velde, “it is hard to imagine a world where the main currency is based on an extremely complex code understood by only a few and controlled by even fewer, without accountability, arbitration, or recourse.”

It works for the governance of the Internet — Hi, ICANN! — so perhaps it can work for Bitcoin too.

Velde also dispels the notion that Bitcoin fulfills the Hayekian concept of denationalization of money. While Bitcoin is indeed stateless, it “is not issued by a private enterprise operating in a competitive environment, disciplined by the market to maintain the stable value of its currency,” as economist Friedrich Hayek imagined, but is instead issued automatically at a predictable rate. Austrian economists everywhere will surely collectively issue a sigh of relief at having that straightened out.

“Some of bitcoin’s features make it less convenient than existing currencies and payment systems, particularly for those who have no strong desire to avoid them in the first place,” writes Velde.

In other words, if you’re not trying to evade trade sanctions or the DEA and you’re not a philosophical convert, what’s the point?

If it does catch on, Velde predicts it’s unlikely to remain free of government intervention, “if only because the governance of the bitcoin code and network is opaque and vulnerable.” Beyond the Fed, Bitcoin is already getting scrutiny from lawmakers and regulators with some, like New York’s state financial regulator hinting at intervention plans. The Senate Homeland Security Committee, meanwhile, plans on holding hearings on Bitcoin within the month, according to Time.

Velde ultimately gives Bitcoin a thumbs up: “[I]t represents a remarkable conceptual and technical achievement, which may well be used by existing financial institutions (which could issue their own bitcoins) or even by governments themselves.”

No ‘burn book‘ for Bitcoin.

Bitcoin: A primer [Chicago Fed Reserve]

Disclosure: Author owns Bitcoin that remain from her week of living on them

http://www.forbes.com/sites/kashmirhill/2013/11/07/federal-reserve-economist-on-bitcoin-small-phenomenon-but-growing/

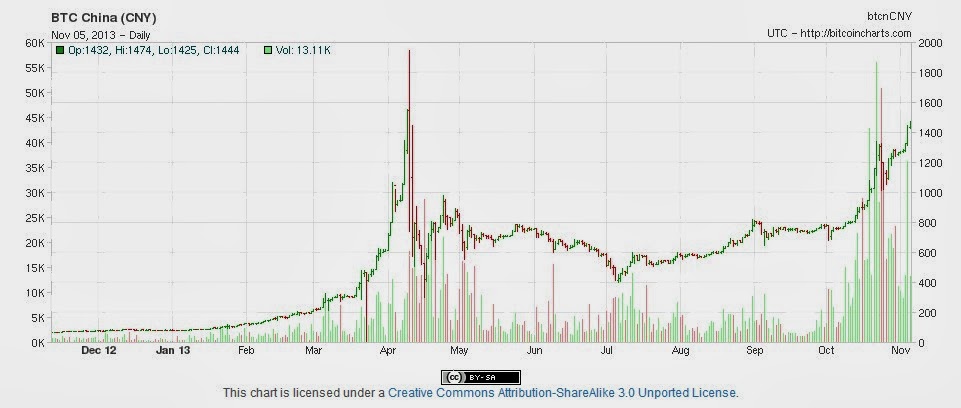

As BitCoin Touches $400 The Senate Starts Seeking Answers... As Does The Fed

by Tyler Durden on 11/09/2013 12:38 -0500

Zerohedge

Moments ago BitCoin hit $395, and will likely cross $400 in the immediate future (the chart looks a little less scary in log scale).

So as more and more pile into the electronic currency, some due to ideological reasons, some simply to chase momentum, some out of disappointment with the manipulated gold price looking to park their savings in an alternative, non-fiat based currency, which a year ago traded 40 times lower, the attention of the government is finally starting to shift to what has been the best performing asset class in the past year, outperforming even the infamous Caracas stock market.

Which means one thing: Congressional hearings.

From Bloomberg:

The U.S. Senate Committee on Homeland Security and Governmental Affairs will meet on Nov. 18 “to explore potential promises and risks related to virtual currency for the federal government and society at large,” it said in a statement today.

The hearing, titled “Beyond Silk Road: Potential Risks, Threats, and Promises of Virtual Currencies,” will invite witnesses to testify about the challenges facing law enforcement and regulatory agencies, and include views from “non-governmental entities who can discuss the promises of virtual currency for the American and global economies.”

“Bitcoin is obviously getting a lot of attention from the federal

government on the regulatory side,” Nicholas Colas, an analyst at ConvergEx Group, said in an interview. “Given the involvement of the currency in illegal activities, that is entirely warranted. I expect these hearings to be largely informational, which is good for Bitcoin.”

“The architecture of the system is elegant from a computer-science perspective, but hard for a non-tech person to understand,” Colas said. “Getting industry professionals to close this gap will be very helpful.”

Or not. Because the only thing the government does when its interest is piqued by something, anything, especially things that have to be looked in log-scale, is to promptly regulate it and then tax it, not necessarily in that order. Just how it will achieve this with Bitcoin remains unclear but one thing is certain: it will try.

Especially, now that even the Fed is looking at BitCoin when a few days ago the Chicago Fed issued 'Bitcoin: A primer" in which the Fed states quite simply:

So far, the uses of bitcoin as a medium of exchange appear limited, particularly if one excludes illegal activities. It has been used as a means to transfer funds outside of traditional and regulated channels and, presumably, as a speculative investment opportunity. People bet on bitcoin because it may develop into a full-fledged currency. Some of bitcoin’s features make it less convenient than existing currencies and payment systems, particularly for those who have no strong desire to avoid them in the first place. Nor does it truly embody what Hayek and others in the “Austrian School of Economics” proposed. Should bitcoin become widely accepted, it is unlikely that it will remain free of government intervention, if only because the governance of the bitcoin code and network is opaque and vulnerable.

Finally, while the Fed may be late to the game, the ECB has already made its feelings on BitCoin well-known long ago: recall from over a year ago: "The ECB Explains What A Ponzi Scheme Is; Awkward Silence Follows" in which the European central banks didn't mince its words: BitCoin is nothing but a ponzi scheme to the central bank tasked with preserving the viability of an entire insolvent continent, and a a currency which unlike BitCoin would never survive absent regulatory intervention.

So while the electronic currency is soaring exponentially as it goes through its appreciation golden age, will the one thing that can finally end the dream of BitCoin holders arrive soon: when the government, and existing monetary authorities, start taking it seriously.

Full Chicago Fed paper on BitCoin

http://www.zerohedge.com/news/2013-11-09/bitcoin-touches-400-senate-starts-asking-questions-does-fed

ICE's takeover of NYSE to close on November 13

BY JOHN MCCRANK

Fri Nov 8, 2013 6:23pm EST

Specialist traders work at the booth that trades the stock for

IntercontinentalExchange, on the floor at the New York Stock Exchange, May 1, 2013. REUTERS/Brendan McDermid

(Reuters) - IntercontinentalExchange Inc (ICE.N) said its takeover of NYSE Euronext (NYX.N) would close on November 13, after clearing final regulatory hurdles on Friday.

The derivatives exchange and clearing house operator said in December it would buy the owner of the New York Stock Exchange in a deal that also gives ICE control of Liffe, Europe's No. 2 derivatives market.

The transaction had been expected to close on Monday, November 4, but ICE said on Wednesday that while there were no substantive issues remaining, certain European regulators needed more time to review the takeover.

The deal, which consists of around 75 percent shares and 25 percent cash, was worth 10.9 billion as of November 1.

Shares of ICE and NYSE will cease to trade after Tuesday, November 12, and the shares of the merged company will begin trading the next day under the ticker symbol "ICE" on the New York Stock Exchange.

ICE Chief Executive Jeff Sprecher, who helped start the company in 2000 and built it up through a series of deals, said on a call with analysts on Tuesday that ICE would move quickly to integrate the parts of NYSE it plans to keep, while unloading other parts of the business.

Sprecher has had a history of eliminating the trading floors of the exchanges his company has bought, but has vowed to keep open the floor of the New York Stock Exchange, which traces its origins back to an agreement signed under a buttonwood tree on Wall Street in 1792.

ICE said in December it expects to cut the majority of $450 million of run-rate expenses from the combined company by the second full year after the deal closes.

NYSE's website says the company has 2,993 employees, while ICE had 1,121 employees as of September 30, according to a recent regulatory filing.

ICE also plans to spin off Euronext, which includes the Paris, Amsterdam, Brussels and Lisbon stock exchanges, in an IPO likely some time next year.

(Reporting by John McCrank and Anil D'Silva; editing by G Crosse

http://www.reuters.com/article/2013/11/08/us-nyse-ice-idUSBRE9A712420131108

Second Canadian Telecom Evaluating Valdor Splitter

November 6, 2013 - Hayward, California

Valdor Technology International Inc. ("Valdor") (TSX: VTI-V) is pleased to report that Valdor’s operating subsidiary, Valdor Fiber Optics, Inc., has delivered a Valdor harsh environment fibre optic splitter to a second Canadian telecom company. This sample device will be evaluated by this telecom to determine if it is a solution for their on-going splitter problems.

Mr. Ron Boyce, VP Sales & Marketing/Director, states: "Our confidence in our technology is now beginning to bear fruit with a second Canadian telecom now evaluating our harsh environment splitters. Reliability and quality are the most important pre-requisites for the Canadian telecoms and Valdor’s harsh environment products have proven that they can meet and exceed their technical requirements."

There are ten regional and national telecoms in Canada; ranging from the government owned SaskTel to the national and publically owned Bell Canada. Currently, the telecom FTTx market accounts for about 80% of global fibre optic expenditures. In North America fibre-to-the-home is at only 5% penetration. For the vendor, the telecom market is a difficult one to penetrate due to its extensive requirements for high quality products and services. It is estimated that the telecom market for passive and active FTTx products, for Canada only, will be in excess of $300 million/year, for at least the next five years. The telecom FTTx market is much larger in the USA.

For medical reasons, Mr. Ralph Kettell has resigned as a Director and Officer of Valdor. The Valdor Board and Management thank him for his many years of support and assistance and wish him the best of health in the near future. He will continue to provide services and support.

About the Fiber Optics Industry

Fiber optics is the future of communications. The signal transmission business is in the early stages of a fiber optics bull market. All signal transmission, in their many and various forms, are being converted from electrical to fiber optics. A comprehensive global report on the fiber optics components market projects that it will reach US$42 billion by the year 2017.

About Valdor Technology International Inc. (www.valdortech.com)

Valdor is a high technology fiber optic components company specializing in the design and manufacture of fiber optic connectors, laser pigtails, splitters, and other optical and optoelectronic components, including some that use the Valdor proprietary and patented Impact Mount™ technology. Valdor's Impact Mount™ technology is all-mechanical with no epoxy or matching gel. Valdor specializes in harsh environment products and in particular splitters and connectors.

On Behalf Of the Board of Directors of

VALDOR TECHNOLOGY INTERNATIONAL INC.

Operations Office: 3116 Diablo Avenue, Hayward CA U.S.A. 94545 ph. (510) 293-1212

Corporate Office: Suite 480 - 789 West Pender Street, Vancouver B.C. Canada V6C 1H2 ph. (604) 682-3117

Disclaimer:

The TSX-Venture Exchange has not reviewed and does not accept responsibility for the adequacy or accuracy of this release. This news release may contain certain "Forward-Looking Statements" within the meaning of Section 21E of the United States Securities Exchange Act of 1934, as amended. All statements, other than statements of historical fact, included herein are forward-looking statements that involve various risks and uncertainties. There can be no assurance that such statements will prove to be accurate, and actual results and future events could differ materially from those anticipated in such statements. Important factors that could cause actual results to differ materially from the Company's expectations are disclosed in the Company's documents filed from time to time with the TSX-Venture Exchange, the British Columbia Securities Commission and the US Securities and Exchange Commission.

http://www.valdor.com/media/releases/valdor-news-release.php?year=2013&seq=6&sign=0

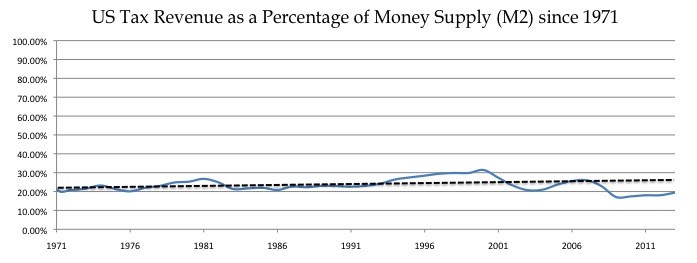

This one chart shows you who’s really in control

November 7, 2013

Simon Black

Bangkok, Thailand

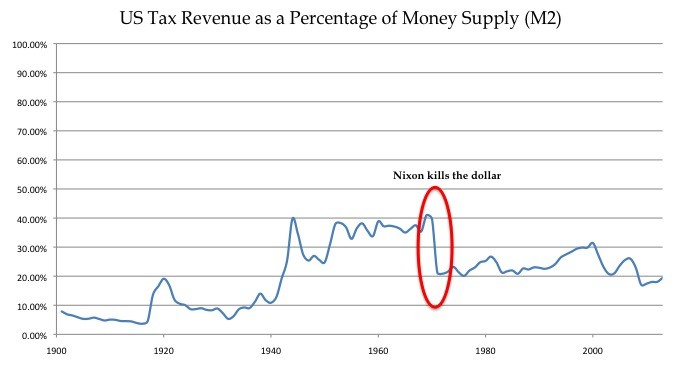

Check out this chart below. It’s a graph of total US tax revenue as a percentage of the money supply, since 1900.

For example, in 1928, at the peak of the Roaring 20s, US money supply (M2) was $46.4 billion. That same year, the US government took in $3.9 billion in tax revenue.

So in 1928, tax revenue was 8.4% of the money supply.

In contrast, at the height of World War II in 1944, US tax revenue had increased to $42.4 billion. But money supply had also grown substantially, to $106.8 billion.

So in 1944, tax revenue was 39.74% of money supply.

You can see from this chart that over the last 113 years, tax revenue as a percentage of the nation’s money supply has swung wildly, from as little as 3.65% to over 40%.

But something interesting happened in the 1970s.

1971 was a bifurcation point, and this model went from chaotic to stable. Since 1971, in fact, US tax revenue as a percentage of money supply has been almost a constant, steady 20%.

You can see this graphically below as we zoom in on the period from 1971 through 2013– the trend line is very flat.

What does this mean? Remember– 1971 was the year that Richard Nixon severed the dollar’s convertibility to gold once and for all.

And in doing so, he handed unchecked, unrestrained, total control of the money supply to the Federal Reserve.

That’s what makes this data so interesting.

Prior to 1971, there was ZERO correlation between US tax revenue and money supply. Yet almost immediately after they handed the last bit of monetary control to the Federal Reserve, suddenly a very tight correlation emerged.

Furthermore, since 1971, marginal tax rates and tax brackets have been all over the board.

In the 70s, for example, the highest marginal tax was a whopping 70%. In the 80s it dropped to 28%.

And yet, the entire time, total US tax revenue has remained very tightly correlated to the money supply.

The conclusion is simple: People think they’re living in some kind of democratic republic. But the politicians they elect have zero control.

It doesn’t matter who you elect, what the politicians do, or how high/low they set tax rates. They could tax the rich. They could destroy the middle class. It doesn’t matter.

The fiscal revenues in the Land of the Free rest exclusively in the hands of a tiny banking elite. Everything else is just an illusion to conceal the truth… and make people think that they’re in control.

by Simon Black

Simon Black is an international investor, entrepreneur, permanent traveler, free man, and founder of Sovereign Man. His free daily e-letter and crash course is about using the experiences from his life and travels to help you achieve more freedom.

http://www.sovereignman.com/expat/this-one-chart-shows-you-whos-really-in-control-13119/

Confusion in Beijing's gold shops on price manipulation

Tom Chatham

Nov. 8, 2013

I received an email from someone who is Chinese with investments in Australia giving a view from the average person in China:

"Gold community in China is much different from western world. The customers are mostly old people (not discribed Chinese Dama [Bron - means middle aged married women]). Their only purpose is to preserve their savings (to against inflation) which earned by hard working of their whole life. When we go to Beijing's biggest gold shop and see some old couples sitting there, looking at gold price chart monitor with hopeless eyes (someone even have heart attack), we are filled with anger. Those good natured and hard working people, they don't chase equities or any kind of riskier investment, they buy gold for safety only. But now, the community is mostly hurted.

As for me, I only have a little gold less than 1% of my assets, but my very old father have a lot. He exchanged 25% of his savings to gold. When every week he met and ask me about gold's "cliff drop" and "volatility" and depressed several months, I can't explain to him exactly what happened. Chinese mainstream media are full of copies of wall streets comments and suggestions, I can't explain to my father clearly what is bullion bank's manipulation and I don't know how to make him happier. Such cases are numerous in China.

Bullion banks are not only making people suffer loss, but also destroying good faith and human logic. CMEgroup says Bullion banks' participation in gold/silver market is to "provide liquidity", but most of end buyers don't need such "liquidity" in the market. Bullion bank's trading is only for their own profit. Those "value-add" profit should belong to customer, miners and even you and your mint.

The problem come from huge naked short in thin time with no news in mid night electronic trading session or London fix, but sadly mid-night electronic session is afternoon in China, that triggers heard attack and depression of old people.

SGE already delivered 1782.997 metric ton in 2013 till October 25, about 15-20 times than Comex, we can't imagine why world price is controlled by a few of US banks."

Unfortnately it seems the average Chinese is no better informed than the average Westerner that we operate in a FIRE economy these days. That is why SGE's larger physical deliveries don't matter, as the ZIRP free money drives leveraged speculation in all markets, gold included. Simply the weight of this money in the gold market overwhelms the non-leverage money from the "good natured and hard working" just looking for safety.

So even if you got rid of fractional reserve banking, futures markets and manipulative trading tatics (which would help), you would still have this volatility as large investors could still borrow money at little cost and leverage up the little bit of their own money to buy a lot more gold. The consequence of that leverage is that it only takes a small change in price to threaten to wipe their capital out, resulting in quick and rushed liquidations back out.

And don't think that "China" is somehow not part of the problem. The same FIRE dynamic is in play in China as well, see this article or this on arbitrages using gold.

There was a great article out a few months ago called On the Phenomenon of Bullshit Jobs where he asks why predictions of a 15-hour work week never eventuated even though productivity increases could allow for it. He proposes that "rather than allowing a massive reduction of working hours to free the world’s population to pursue their own projects, pleasures, visions, and ideas, we have seen the ballooning" of bullshit jobs "as if someone were out there making up pointless jobs just for the sake of keeping us all working".

I propose a related phenonenom - that we are in a bullshit economy.

I am not confident that this is sustainable, which is why I have some gold insurance in my retirement savings account. All I can say to investors is to realise the bullshit FIRE dynamic that drives markets these days, be aware that this will result in large price swings, don't get all excited if we have a quick price rise as it could just be hot money that will flow out again, and remember gold is insurance to protect your wealth, not grow it.

I started reading commentary on the net about precious metals in 1998, when the The Perth Mint transferred me from Sydney to Perth to take up the position of Depository Administrator. In that time I have seen some intelligent writing but also a lot of stuff that could be described as emotional, misinformed, misguided, driven by hidden agendas or all of the above, and a fair bit by people who have never worked in the industry.