News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

investor15

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Precious Metals Intervention In The Extreme

GOLD AND METALS DESK, SPECIAL GUEST QUARTERS

DAVE KRANZLER | JANUARY 7, 2014 2:13 PM

A nuclear currency war rooted in the historical intervention of the gold market by the Federal Reserve and the U.S. Treasury.

Anyone who calls what is happening a “flash crash” or hedges on their assertion of “possible” direct intervention is either completely ignorant of the facts or they write their commentary in fear of public ridicule and doubt from other intellectual hedgers. It is what it is: a nuclear currency war rooted in the historical intervention of the gold market by the Federal Reserve and the U.S. Treasury.

Forget the “flash crash” story being widely promoted. The “flash crash” story that says that technical and algo trading caused the plunge. Really? In the absence of a big dose of intervention, the flash crash never happens. Therefore, the only attributable cause by anyone who is being intellectually honest – not just with their readers but with themselves – is that INTERVENTION was culprit

In the last two days, 26+ tonnes was delivered on the Shanghai Gold Exchange. The enormous physical off-take in China is a freight train w/out brakes. From Standard Bank:

“In the physical market we are witnessing strong demand. Since the start of 2014, the SGE premium has jumped higher, reaching $18/oz this morning. The buying frenzy in especially China comes on the back of the seasonal demand pick-up ahead of the country’s New Year, which starts on 31 January…More broadly we have also noted an improvement in Asia demand for gold since mid-December. This is evident in the pickup of our Standard Bank Gold Physical Flow Index”

The manipulation in the gold (NYSEARCA:GLD) market is getting worse by the day as the demand for physical gold from the eastern hemisphere begins to accelerate. It looks like the western Central Banks and their bullion bank market agents are going to work on silver with more focus. SLV (NYSEARCA:SLV) is starting to see physical drawdowns, as is the Comex. The capping in silver is beyond blatant. Turkey imported a record amount of silver last year, as did India.. India’s demand for silver is the substitution of the gold that was cut off by the U.S. Government-induced Indian import controls.

Make no mistake about it. In the face of China’s moves to move away from the U.S. dollar (NYSEARCA:UUP) and bolster their own currency with an historically epochal program of systemic physical gold accumulation, the U.S Government and the Fed are waging a nuclear currency war with a war on the physical gold market at its nexus. Anyone who asserts that it is any less than that is a complete coward.

Contributed by Dave Kranzler, The Golden Truth

http://wallstreetsectorselector.com/2014/01/precious-metals-intervention-extreme/

23 Reasons to Be Bullish on Gold

Laurynas Vegys,

Research Analyst

Casey Research

January 8, 2014 4:23am

(hattip to Seminole Red & basserdan)

It's been one of the worst years for gold in a generation. A flood of outflows from gold ETFs, endless tax increases on gold imports in India, and the mirage (albeit a convincing one in the eyes of many) of a supposedly improving economy in the US have all contributed to the constant hammering gold took in 2013.

Perhaps worse has been the onslaught of negative press our favorite metal has suffered. It's felt overwhelming at times and has pushed even some die-hard goldbugs to question their beliefs… not a bad thing, by the way.

To me, a lot of it felt like piling on, especially as the negative rhetoric ratcheted up. Last year's winner was probably Goldman Sachs, calling gold a "slam-dunk sale" for 2014 (this, of course, after it's already fallen by nearly a third over a period of more than two and a half years—how daring they are).

This is why it's important to balance the one-sided message typically heard in the mainstream media with other views. Here are some of those contrarian voices, all of which have put their money where their mouth is…

• Marc Faber is quick to stand up to the gold bears. "We have a lot of bearish sentiment, [and] a lot of bearish commentaries about gold, but the fact is that some countries are actually accumulating gold, notably China. They will buy this year at a rate of something like 2,600 tons, which is more than the annual production of gold. So I think that prices are probably in the process of bottoming out here, and that we will see again higher prices in the future."

• Brent Johnson, CEO of Santiago Capital, told CNBC viewers to "buy gold if they believe in math… Longer term, I think gold goes to $5,000 over a number of years. If they continue to print money at the current rate, I think it could be multiples of that. I see a slow steady rise punctuated with some sharp upward moves."

• Jim Rogers, billionaire and cofounder of the Soros Quantum Fund, publicly stated in November that he has never sold any gold and can't imagine ever selling gold in his life because he sees it as an insurance policy. "With all this staggering amount of currency debasement, gold has got to be a good place to be down the road once we get through this correction."

• George Soros seems to be getting back into the gold miners: he recently acquired a substantial stake in the large-cap Market Vectors Gold Miners ETF (GDX) and kept his calls on Barrick Gold (ABX).

• Don Coxe, a highly respected global commodities strategist, says we can expect gold to rise with an improving economy, the opposite of what many in the mainstream expect. "You need gold for insurance, but this time the payoff will come when the economy improves. In the past when everything was falling all around you, commodity prices were soaring out of sight. We had three recessions in the 1970s and gold went from $35 an ounce to $850. But this time, gold is going to appreciate when we start getting 3% GDP growth."

• Jeffrey Gundlach, bond guru and not historically known for being a big fan of gold, came out with a candid endorsement of the yellow metal: "Now, I kind of like gold. It's definitely very non-correlated to other assets you may have in your portfolio, and it does seem sort of cheap. I also like the GDX."

• Steve Forbes, publishing magnate and chief executive officer of Forbes magazine, publicly predicted an impending return to the gold standard in a speech in Las Vegas. "A new gold standard is crucial. The disasters that the Federal Reserve and other central banks are inflicting on us with their funny-money policies are enormous and underappreciated."

• Rob McEwen, CEO of McEwen Mining and founder of Goldcorp, reiterated his bullish call for gold to someday top $5,000. "We now have governments willing to seize their citizens' assets. We now have currency controls on the table, which we haven't seen since the late 1960s/early '70s. We have continued debasement of currencies. And the economies of the Western world remain stagnant despite enormous monetary stimulation. All these facts to me are bullish for gold and make me believe the price will bounce back relatively soon."

• Doug Casey says that while gold is not the giveaway it was at $250 back in 2001, it is nonetheless a bargain at current prices. "I've been buying gold for years and I continue to buy it because it is the way you save. I'm very happy to be able to buy gold at this price. All the so-called quantitative easing—money printing—by governments around the world has created a glut of freshly printed money. This glut has yet to work its way through the global economic system. As it does, it will create a bubble in gold and a super-bubble in gold stocks."

And then there's the people who should know most about how sound the world's various types of paper money are: central banks. As a group, they have added tonnes of bullion to their reserves last year…

• Turkey added 13 tonnes (417,959 troy ounces) of gold in November 2013. Overall, it has added 143.6 tonnes (4,616,847 troy ounces) so far this year, up 22.5% from a year ago, in part thanks to the adoption of a new policy to accept gold in its reserve requirements from commercial banks.

• Russia bought 19.1 tonnes (614,079 troy ounces) in July and August alone. With the year-to-date addition of 57.37 tonnes—second only to Turkey—Russia's gold reserves now total 1,015 tonnes. It now holds the eighth-largest national stash in the world.

• South Korea added a whopping 20 tonnes (643,014 troy ounces) of gold in February, and now carries 23.7% more gold on its balance sheet than at the end of 2012." Gold is a real safe asset that can help (us) respond to tail risks from global financial situations effectively and boosts the reliability of our foreign reserves holdings," said central bank officials.

• Kazakhstan has been buying gold every month, at an average of 2.4 tonnes (77,161 troy ounces) through October. As a result, the country's reserves have seen a 21% increase to 139.5 tonnes from a year ago.

• Azerbaijan has taken advantage of a slump in gold prices and has gone from having virtually no gold to 16 tonnes (514,411 ounces).

• Sri Lanka and Ukraine added 5.5 (176,829 troy ounces) and 6.22 tonnes (199,977 troy ounces) respectively over the past year.

• China, of course, is the 800-pound gorilla that mainstream analysts seem determined to ignore. Though nothing official has been announced by China's central bank, the chart below provides some perspective into the country's consumer buying habits.

China ended 2013 officially as the largest gold consumer in the world. Chinese sentiment towards gold is well echoed in a statement made by Liu Zhongbo of the Agricultural Bank of China: "Because gold has capabilities to absorb external economic shocks, growth of its use in the international monetary system will be imminent."

And those commercial banks that have been verbally slamming gold—it turns out many are not as negative as it might seem…

• Goldman Sachs proved itself to be one of the biggest hypocrites: while advising clients to sell gold and buy Treasuries in Q2 2013, it bought a stunning (and record) 3.7 million shares of GLD. And when Venezuela decided to raise cash by pawning its gold, guess who jumped in to handle the transaction? Yes, they claim the price will fall this year, but with such a slippery track record, it's important to watch what they do and not what they say.

• Société Générale Strategist Albert Edwards says gold will top $10,000 per ounce (with the S&P 500 Index tumbling to 450 and Treasuries yielding less than 1%).

• JPMorgan Chase went on record in August recommending clients "position for a short-term bounce in gold." Gold's price resistance to Paulson & Co. cutting its gold exposure, along with growing physical gold demand in Asia, were cited among the main reasons.

• ScotiaMocatta's Sunil Kashyap said that despite the selloff, there's still significant physical demand for gold, especially from India and China, which "supports prices."

• Commerzbank calls for the gold price to enter a boom period this year. Based on investment demand from Asian countries—China and India in particular—the bank predicted the yellow metal will rise to $1,400 by the end of 2014.

• Bank of America Merrill Lynch, in spite of lower price forecasts for gold this year, reiterated they remain "longer-term bulls."

• Citibank's top technical analyst Tom Fitzpatrick stated gold could head to $3,500. "We believe we are back into that track where gold is the hard currency of choice, and we expect for this trend to accelerate going forward."

None of these parties thinks the gold bull market is over. What they care about is safety in this uncertain environment, as well as what they see as enormous potential upside.

In the end, the much ridiculed goldbugs will have had the last laugh.

http://www.caseyresearch.com/articles/23-reasons-to-be-bullish-on-gold

Reasons Why The U.S. Government Is Destroying The Dollar

Jan 08, 2014 - 10:21 AM GMT

By: Dan_Amerman

Overview

The United States government has six interrelated motivations for destroying the value of the dollar:

1. Creating money out of thin air on a massive basis is all that stands between the current state of hidden depression, and overt depression with unemployment levels potentially rivaling those seen in the Great Depression of the 1930s.

2. It is the most effective way to not just pay down current crushing debt levels using devalued dollars, but also to deal with the rapidly approaching massive generational crisis of paying for Boomer retirement promises.

- It creates a lucratively profitable $500 billion a year hidden tax for the benefit of the US government - a tax which is not understood by voters or debated in elections.

- It creates a second and quite different form of hidden taxation by way of generating artificial market highs, which while non-existent in inflation-adjusted terms, do create artificial investment profits that are fully taxable and highly profitable for the US government.

- It is the weapon of choice being used to wage currency war and reboot US economic growth; and

- It is an essential component of political survival and enhanced power for incumbent politicians.

In this article we take a holistic approach to understanding how individual short, medium and long-term pressures all come together to leave the government with effectively no choice but to create a significant rate of inflation that will steadily destroy the value of the dollar over time.

If you have savings, if you rely on a pension, if you are a retiree or Boomer with retirement accounts - any one of these six fundamental motivations is by itself a grave peril to your future standard of living. However, it is only when we put all six together and see how the motivations reinforce each other, that we can most effectively seek personal solutions.

Reason One: The Political Interests Of Self-Serving Politicians

Even after the major tax increases of about $400 billion a year that took effect at the end of 2012, almost 5% of the US economy is still currently funded by deficit spending. From a political perspective, this approximately $750 billion a year in borrowed money is "free money" that politicians often get to disburse on a political district and favored special interest group basis. In other words, roughly $650 per month per above-poverty line American household can be used to reward friends - and can be withheld from enemies - with personal credit being taken by the benevolent politicians for this never-ending largess.

In past decades, politicians were restricted to spending perhaps $200 or $300 per month per household over and above what the government was collecting in taxes, with the difference being borrowed in the bond market. Anything above that would require the unpleasantness of raising taxes, which might put individual politicians in danger of actually losing their position and privileged lifestyle if he or she weren't in a "safe" district. However, in the current climate all limitations are gone, the pork is rolling out on a historically unprecedented basis, and the politicians are wielding unprecedented power.

So why do the limitations usually exist on at least some level, and why are they gone now? Historically, the US government had directly created money out of thin air on a massive basis to fund deficit spending during the Civil War, and also during the Revolutionary War. There is a very good reason such governmental actions are so rare: the value of the US dollar was rapidly destroyed in both instances. So, this spending without limit would not ordinarily be a sensible path. Unless, from the government's perspective, there were other dangers that were considered a greater threat, and that could be addressed only through destroying the value of the dollar.

Reason Two: To Hide A Depression

(I have written numerous articles about various aspects of Reasons Two through Six for some years now, and my long-term readers and subscribers have been well aware of the building pressures. While the emphasis of this article is on the interweaving of the short, medium and long-term relationships between the six reasons, we will first set the stage by taking a few paragraphs each to briefly review the individual government motivation, with a link to a full length article that covers the problem in more depth.)

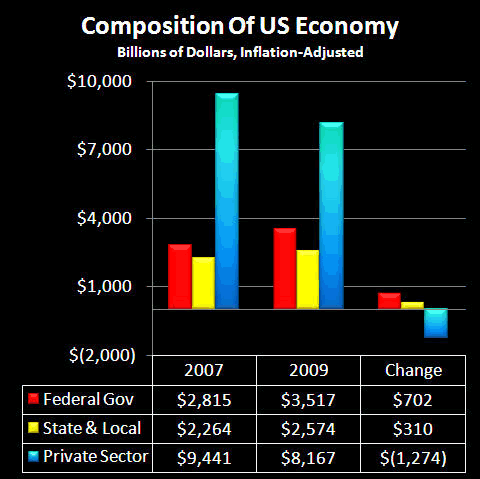

While you wouldn't know it from government press releases or media headlines, there has been a gaping hole in the US economy since 2008, as illustrated below:

Composition of US Economy

During the first round of the Financial Crisis in 2008 and 2009, the US private sector nearly collapsed, threatening to send the US economy straight into deep depression. We're talking about a $1.3 trillion private sector collapse that was contained only by the government fantastically increasing the money it spent, even while tax revenues were falling. Indeed, the creation of huge government deficits has been all that has maintained even a facade of semi-normalcy. Remove that mechanism, and it is straight to official Great Depression-level unemployment in months.

Even as the true gravity of the situation is hidden from the general public, so too is the true cost of the grossly irresponsible short-term "band-aid" that is being used to cover the hole in the US economy. The destruction of the value of savings in general, as well as the impoverishment of Boomers and retirees in particular, is explained in my article linked below, "Hiding A Depression: How The US Government Does It."

Article Link

Reason Three: A Desperate Attempt To Escape Depression By Waging Currency War

The US government has been waging currency war since September of 2010. Simply put, the US would have great difficulty emerging from depression so long as the US dollar were "strong", because a strong dollar translates to "expensive" US workers who have difficulty competing for market share even in the US economy, let alone abroad. So one reason for a nation intentionally slashing the value of its currency is that its workers become relatively cheaper, enabling them to not only better defend their domestic market share, but to begin to take market share in foreign economies as well. However, when a major player goes on the currency offensive, many trading partners will counterattack in the attempt to defend their own economies, not by making their own currencies stronger, but by weakening them- so that their domestic workers remain relatively inexpensive and will be better able to compete for market share.

To successfully maintain and increase the power of this currency offensive while negating attempted counterattacks, the Federal Reserve chose a radical weapon in the form of QE3 - which began with the public announcement that it would be directly creating money on a massive scale equal to 6% of the US economy indefinitely, with the proceeds going to purchase US government debt and mortgage-backed securities in the secondary markets. Ultimately, the only protections for a symbolic currency such as the US dollar are the policies deployed by the Central Bank to maintain that value. And when the nation's chief central banker directly threatens to use his power to destroy the symbol, rather than preserve it - the threat is extraordinarily effective.

QE3 has been highly successful in reducing the value of US currency relative to both Europe and China. However, Japan has counterattacked with the new Abenomics, a particularly potent form of quantitative easing which has been quite successfully pushing down the value of the yen versus the rest of the world, thereby ratcheting up Japanese export profits.

There is no free lunch, however. While the US government is insisting to the world-at-large that it is not engaged in currency warfare, in order to maintain the plausible deniability that is essential to diplomatic doublespeak, it is also hiding the heavy cost from its own citizens. The US standard of living since the late 1990s has been based on having a "strong" dollar and huge trade deficits - meaning we haven't actually been able to pay for what we consume for a long time. Therefore, even as jobs and the real economy grow, there is a drop in the overall standard of living, which is not evenly weighted, but is disproportionately borne by savers, Boomers and retirees.

A deeper exploration of how this works, including the specific ways that older citizens are - and will continue to be - the primary victims, can be found in my article linked below, "Bullets In The Back: How Boomers & Retirees Will Become Stimulus, Bailout & Currency War Casualties".

Article Link

These second and third components of hiding a depression and waging currency war are tightly interwoven, and could even be called "killing two birds with one stone". The money doesn't exist to keep the US from openly plunging into depression, it simply isn't there for a fiscally responsible government. And covering the economic hole by creating money out of thin air at a rate equal to 6% of the total US economy is so fiscally irresponsible, that few nations dare a counterattack of such magnitude. So for now, massive monetary creation allows the US to not only cover over the current hidden depression, but also to wage all-out currency war to try to emerge from that depression.

While boosting employment is an important motive behind currency warfare, to better understand the agenda of the US government, we'll next explore the greatest financial problem of all, and how destroying the value of the dollar is the intended solution.

Reason Four: Dodging National Bankruptcy

Sometimes households reach the unfortunate point where when they add up the credit cards, mortgage payments, and second mortgage payments - they realize that they will never be able to pay their bills. They know they are bankrupt and there is no way of dodging it. But instead of reducing their spending - they may actually ratchet it up, until all the lines of credit are maxed out, and the bills are all in arrears. Because once bankruptcy is inevitable anyway, why slash your standard of living before you absolutely have to? Partying it up for another few months won't change the destination, so why not?

Fortunately, relatively few ordinary people are so irresponsible as to think that way. There is ample evidence, however, that a good number of politicians hold that mindset when it comes to budget deficits that appear impossible to repay, at least in the conventional manner.

There is a pervasive myth that is being frequently repeated, which is that our children and grandchildren will be slaving away for decades to pay back the money that we've been borrowing to fund this reckless deficit spending. The assumption behind the myth is that were it not for the current spending, the nation would be fine, and therefore increased taxes will be needed to pay back these borrowings over the decades to come.

Except that the nation wouldn't be fine. For like most other major developed nations in the world, the United States has been effectively bankrupt for quite some time, with a day of reckoning that is approaching fast - with or without the current outrageous level of deficit spending.

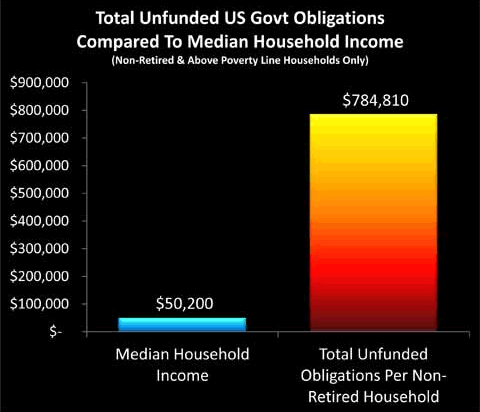

The graph below is from my article, "Six Layers Of Deficit Impossibilities Mean Retirement Catastrophe".

Total Unfunded US Govt Obligations compared to Median Household Income

As developed step by step in "Six Layers", when we add up current and future federal deficits, as well as unfunded Social Security, Medicare and other unfunded government promises, the total comes to over $785,000 per non-retired household over the coming years that has an above-poverty line income. And this actually isn't even the total cost - it is the excess cost over and above current estimated tax receipts, with those estimated receipts being based on the assumption of a healthy and growing economy. When we drop the assumption of an economy growing at the same rates of the last 50 years, then the shortfall goes far higher - perhaps to over $200 trillion for Social Security and Medicare alone by some recent estimates. That would raise the total shortfall to over $2 million per non-retired and above-poverty-line household.

If taxes can't pay (and it's ludicrous to think they can), and the US doesn't declare bankruptcy, then just how do we cover the gap?

Short answer: pay in full, but make the dollar worth five cents. This drops the per household cost for everything from almost $800,000 down to about $40,000. Painful, but manageable over a period of 20-30 years.

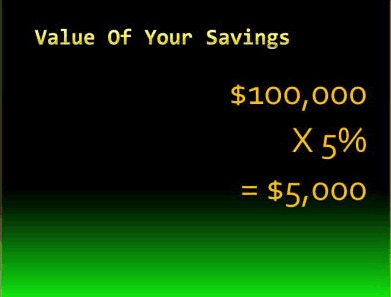

Value of your Savings

Merely make a dollar worth five cents, and those seemingly impossible government promises become quite payable. The problem with this "solution", however, is that it also requires making most people's life savings worth five cents on the dollar.

Reason Five: Create A Massive Hidden Tax

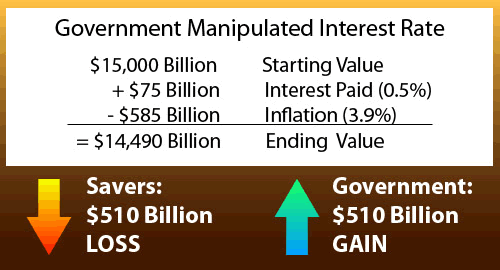

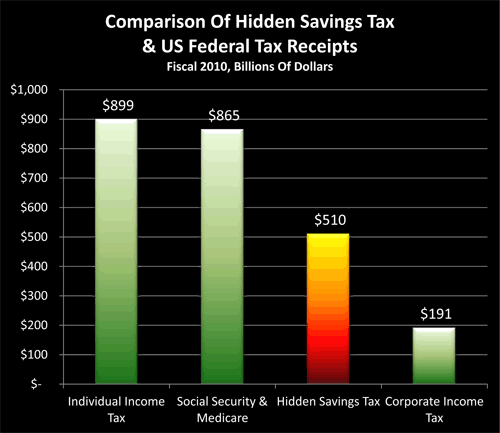

The Federal Reserve effectively controls short, medium and long-term interest rates in the United States, and this means that it controls the borrowing costs of the United States government. As developed in my article linked below, "Hiding A $500 Billion Tax On Savings: How The Government Deceives Millions", by forcing interest rates below the rate of inflation, the Federal Reserve creates about a half trillion dollar per year "windfall" gain for the federal government.

Government Manipulated Interest Rate

This is not "free money", far from it - for every dollar that the government takes in from interest rate manipulations comes directly out of the pockets of savers. That is, for the government to come out ahead by $500 billion per year requires savers and pension funds to come up short by $500 billion per year. This makes it a tax - in all but name. It is also essential to note that two elements have to come together to make this hidden tax work: 1) there have to be low interest rates, and 2) there also has to a substantive real rate of inflation (which can be quite different from the official rate).

Comparison of Hidden Savings Tax & US Federal Tax Receipts

From a politician's perspective, this massive tax - almost three times the size of federal corporate taxation - is a "dream tax". Half a trillion dollars a year is available to spend without overtly raising taxes or increasing deficits! Sure, there is a cost, which is the entirely deliberate destruction of retirement dreams and promises for tens of millions of US workers and retirees - particularly Boomers - as well as pushing forward the insolvency of state and local government pension funds around the country. But the deliberate bankrupting of a generation is a long-term problem with no clear accountability and almost no voter understanding, which means it is more or less irrelevant for how political decisions are made today.

Reason Six: Taxing Inflation As Income

Let's consider three market scenarios when viewed from a governmental tax collection perspective.

1) Falling Markets. If investment markets such as the stock market are falling - then on average, rather than generating taxes for the government, they result in tax deductions, as investors write off their losses. Falling asset values are disastrous for government budgets, because falling investment markets act to reduce government tax collections.

2) Level Markets. If markets are on average neither rising nor falling but going sideways - then while tax deductions are not being generated on a net basis, neither are total tax collections. While this is a better scenario for the government than falling markets, it is still quite problematic for tax collection in general, because one of the primary sources of tax revenues - particularly from the more affluent portion of the population - ceases to exist.

3) Rising Markets. There is nothing like a good bull market to rapidly increase government tax collections. Investors all across the country are ratcheting up their tax payments, and rising markets also tend to generate frequent short-term trading, which means that many of those tax collections will be at the lucrative (for the government) short-term bracket level. It is no coincidence that the only US government surpluses in recent decades occurred at the height of the tech stock bubble, with the often frenetic short-term trading (at short-term tax rates) that was a part of it.

If governments didn't have a means for turning level or falling markets into rising markets - this three-part relationship could be a huge problem, particularly with a struggling economy.

Fortunately for the government - and very unfortunately for investors - there is a very powerful weapon which can turn falling or level markets into rising markets, while radically increasing investment tax revenues. This weapon is inflation, the destruction of the value of the dollar, and it has generated enormous hidden tax revenues for the US government ever since the United States went off the gold standard in 1933.

While these hidden inflation taxes are very well understood by governments and economists, the average voter and investor is not even aware of their existence. To help address this knowledge gap, I have prepared two resources, linked below.

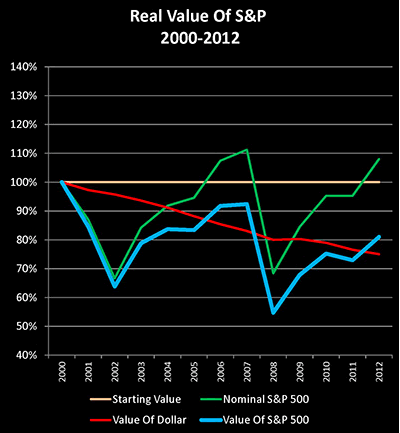

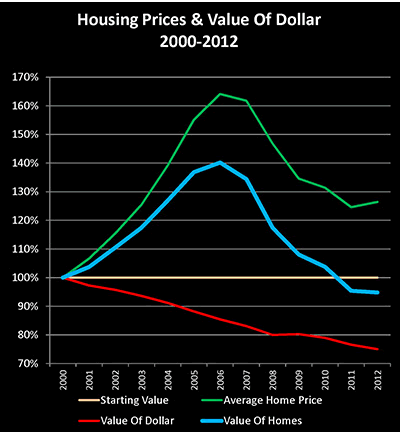

" Could Misleading Theory And Jargon Threaten Your Net Worth?" is an easy to follow, illustrated tutorial which shows how the destruction of the value of money can be used to cover over the destruction of the value of assets - even while generating substantial false "income", which is fully taxable even though it doesn't exist in after-inflation form.

Real Value of S&P 2000-2012

Housing Prices& Value of Dollar 2000-2012

[img][/img]

[img][/img]

Article Link

As developed in the article, when it comes to the largest components of household net worth for American households, for the 22 out of 40 years analyzed - the destruction of the purchasing power of assets was being (successfully) hidden from the public.

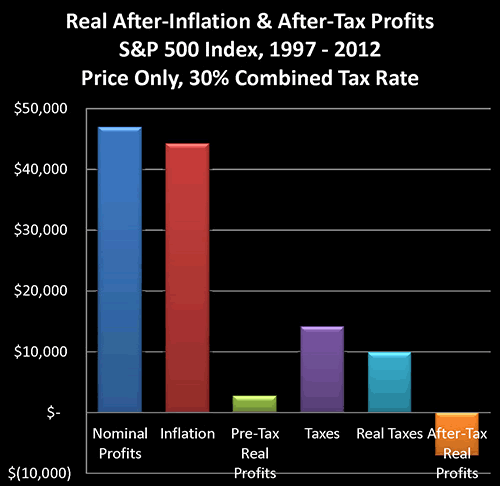

Real After-Inflation & After-Tax Profits, S&P 500 Index, 1997-2012

As shown in the graph above, and developed in my article, " Stealth Taxes Consume Stock Gains & Retirement Plans", about 94% of taxes paid on stock price gains held between 1997 and 2012 weren't actually paid on real income - but rather on inflation. That is, for every $1 of taxes on "real" or after-inflation income, the government was collecting $17 in taxes on phantom income - which had been created by the rate of inflation.

It is difficult to overstate the importance of inflation to the government when it comes to both the level and the reliability of investment tax collections. With no inflation in the mix, it all comes down to the economy and the luck of the markets. And in any given year, falling markets could generate increased tax deductions that could cripple government revenues.

Even a moderate annual rate of inflation, then (whether included in official government inflation estimates or not), is enough to skew investment tax returns strongly in the government's favor. And of course the higher the rate of inflation, the more powerful the financial advantages to the government of this long-standing tax, which as the US government knows quite well from eight decades of experience - most voters don't understand.

The Convergence Of The Six Overwhelming Governmental Motivations

The second half of this article takes a look at the intertwined relationships between the six reasons over the short, medium and long term, and how the six-way motivation to create inflation is far stronger than with any one reason in isolation.

Continue Reading The Article

Daniel R. Amerman, CFA

Website: http://danielamerman.com/

E-mail: mail@the-great-retirement-experiment.com

Daniel R. Amerman, Chartered Financial Analyst with MBA and BSBA degrees in finance, is a former investment banker who developed sophisticated new financial products for institutional investors (in the 1980s), and was the author of McGraw-Hill's lead reference book on mortgage derivatives in the mid-1990s. An outspoken critic of the conventional wisdom about long-term investing and retirement planning, Mr. Amerman has spent more than a decade creating a radically different set of individual investor solutions designed to prosper in an environment of economic turmoil, broken government promises, repressive government taxation and collapsing conventional retirement portfolios

http://www.marketoracle.co.uk/Article43874.html

Ron Paul on ObamaCare: ‘It’s all a tax’

Video first released on 1/2/13

marketsanity.com

“The only way it’s going to disappear quickly is if it totally self-destructs, which is conceivable,” Paul said of Obamacare. “Everybody just quits because they’re getting nowhere with it, and they just opt out.”

There’ll be excuses made, and the politicians will spin it a certain way.”

A Freebie from Uncle Ted

By Turd Ferguson | Friday, January 3, 2014 at 3:32 pm

Ted Butler's "New Year" newsletter was released to subscriber's on Wednesday. He's made it public today through the SilverSeek site.

Here's the link to the full report at SilverSeek:

www.silverseek.com/commentary/2013-–-year-jpmorgan-12815

You should be sure to read the entire report but I want to C&P and highlight two paragraphs below. As regular know, I've been tracking JPM's hoarding of Comex gold and silver deliveries since July of last year. Ted has, too, and these two paragraphs get to the crux of the matter:

"Here’s something new I’ve been meaning to mention. The CME Group (owner-operator of the COMEX) lists a spot month position limit and monthly limit on actual deliveries of 7.5 million silver oz and 300,000 gold ounces by any one trader. Yet the CME is reporting that JPMorgan in its house account took delivery of more than double the amount of gold allowed in any one month. Since JPMorgan held the 6254 gold contracts from first delivery day forward, it also means that JPM was in violation of CME rules limiting spot month holdings in gold futures of 3000 contracts for the entire month. The violations in silver were less egregious but were violations nonetheless.

I’m sure if pressed the CME could come up with some cockamamie excuse why JPMorgan was allowed to hold and take delivery of so many gold and silver contracts in one month, but the real reason is that JPMorgan is above all rules and law. The CFTC backed down on policing JPMorgan and it would be foolish to think the CME would restrict its most important client in any way. Far from a band of brothers, this is a brotherhood of criminals. Besides, rules are for the little people, not JPMorgan."

If you're looking for something to do this weekend, perhaps you should C&P these two paragraphs yourself and send them off to the CFTC for an answer...

mwetjen@cftc.gov

Again, to subscribe to Ted's excellent service, simply click here: www.butlerresearch.com/subscribe.asp

TF

http://www.tfmetalsreport.com/blog/5361/freebie-uncle-ted

A Year of Infamy

Posted Sunday, 29 December 2013

By Andrew Hoffman

(special thanks to the cork)

In my view, 2013 was a key inflection point in modern history; surpassed only by 2008 in terms of irreversible economic damage, but NONE as pertains to unabashed usage of overt (and covert) money printing, market manipulation, and propaganda in a last-gasp attempt to “kick the can” that last, pitiful mile. At least – or more appropriately, as Rizzo said in Grease, the very least – the “pre-QE” efforts of 2008-11 had the semblance of (misguided) officialdom actually believing they were “saving” the world.

Unfortunately, since the current crisis commenced in late 2011 – yielding QE3 and QE4 in the U.S., “whatever it takes” market support in Europe, and “quantitative-qualitative easing” in Japan, TPTB’s intentions have clearly taken on a more malignant tone. In other words, whilst the inflationary after-effects of TARP and other post-2008 money printing schemes were simply considered collateral damage, today’s collapsing currencies, rising political tensions, emerging militarism, and burgeoning financial repression are considered “weapons” to quell the nasty, acrid smell of “the 99%” daring to desire “the 1%’s” blood money.

The year started with Congress selling out America’s interests with the vile “fiscal cliff deal”; in fact, nearly to the minute, given that it was passed in a rare New Year’s Eve session. Ironically, the eleventh hour deal that dramatically reduced the “sequester” cuts created by the paradoxically named “Budget Control Act of 2011” – which itself, was a diluted replacement of what the “Super Committee” failed to achieve – was deemed the “American Taxpayers Relief Act of 2012.” I’m still having trouble understanding that name, given the payroll tax exemption was eliminated for all Americans, whilst top earners received a significant tax increase. But then again, no budget was created by the aforementioned Budget Control Act; whilst essentially all the “sequester cuts” it earmarked for 2013 were cancelled by the October 2013 “Continuing Appropriations Act.” Better yet, said act claimed $20 billion of annual budget savings on a $1.012 trillion budget; when in fact, that “budget” represented just a quarter of the government’s nearly $4 trillion spending plans (let alone, that such budget savings are, as always, “back-end loaded”). Last week, I discussed this very issue in “the truth of the so-called budget deal”; yet, no one seems to care that the deal excludes the $2.8 billion of annual spending considered “essential” – and thus, not subject to negotiation.

As for the national debt, it was $14.2 trillion when Standard & Poor’s stripped America’s triple-AAA rating in August 2011. Today – barely two years later – it stands at $17.3 trillion today; excluding, of course, $5+ trillion of “off balance sheet” debt, and perhaps $200 trillion of “unfunded liabilities.” At the time, S&P’s reasoning was the following…

The downgrade reflects our opinion that the fiscal consolidation plan Congress and the Administration recently agreed to falls short of what, in our view, would be necessary to stabilize the government’s medium-term debt dynamics.

More broadly, the downgrade reflects our view that the effectiveness, stability, and predictability of American policymaking and political institutions have weakened at a time of ongoing fiscal and economic challenges to a degree more than we envisioned when we assigned a negative outlook to the rating on April 18, 2011.”

The outlook on the long-term rating is negative, “. We could lower the long-term rating to ‘AA’ within the next two years if we see that less reduction in spending than agreed to, higher interest rates, or new fiscal pressures during the period result in a higher general government debt trajectory than we currently assume in our base case. -Standard and Poors, August 5, 2011

No sane person, including the most rabid government sympathizer, could opine that, according to S&P’s own criteria, the U.S. credit rating should still be rated AA+ – or even investment grade, for that matter. However, as S&P’s CEO was “forced to resign” immediately following that decision, and S&P itself subsequently sued by the U.S. government, the so-called leading rating agency not only didn’t follow up on its own advice, but raised its outlook in June 2013 – per what I wrote in “S&P hits a new all-time low.” Then again, as Matt Taibbi described earlier this year – as if we didn’t already know – the ratings business is as corrupt as the Wall Street criminals that fund it.

As for the supposed “debt ceiling,” it was “delayed” by the even more inappropriately named “No Budget, No Pay” act of February 2013; thus, allowing it to grow unabated until the arbitrary date of May 18th, 2013. Of course, no budget was created during that time, so “Citigroup Jack” Lew simply stole from U.S. pensioners and along with other accounting chicanery (cumulatively deemed “extraordinary measures”), pushed the debt ceiling breach into October 2013. At that point, the aforementioned “Continuing Appropriations Act of 2014” again delayed the debt ceiling – this time, until the equally arbitrary date of February 7th, 2014”; enabling said “extraordinary measures” to immediately be counted as debt (to the tune of $300+ billion), and starting the clock on a second round of “extraordinary measures” – which this time, will only last until March.

Amazingly, “Tough Talk” Boehner actually allowed the Democrats to insert fine print into the October law, enabling the President to veto any future attempts to cap the national debt. Only a 2/3rds majority of both the House and Senate can stop the President now; which I think we all know can never happen. And thus, when a new “deal” is hashed out on February 6th – likely, with another, even more egregious misnomer of a name – there will be absolutely ZERO consternation about the debt ceiling; which, frankly, may be overtly eliminated in the same manner as it just was in Australia.

“Tapering” and all – which last week, I proved is but a mirage, the Fed now owns one-third of all U.S. Treasury bonds, and one half of all mortgage-backed securities. Overt QE amounted to more than $1 trillion this year – and likely, with covert spending was closer to $1.4 trillion. Moreover, in 2014, the current plan is to spend another $900 billion (taking Treasury and MBS holdings to 50% and 75% of their respective, outstanding totals); whilst government spending rises by 5%, excluding “off balance sheet” items, of course. Thus, I have ZERO doubt that the published national debt will be well above $18 trillion by year-end; and perhaps, if interest rates continue to rise, considerably more. Remember, each 1% increase in interest rates raises annual debt service by nearly $200 billion; and that’s just on the Federal level. The nation as a whole has never been more addicted to ultra-low interest rates; and sadly, the coming wave of adjustable rate resets could make the 2006-08 “subprime” wave look like a mere ripple. Worse yet, in recent years, the Federal government has refinanced most of its debt to short-term maturities and thus is heavily sensitive to even microscopic rate changes.

Of course, I have barely scratched the surface of the infamy that 2013 was; as even the government’s economic crimes and policy errors have been barely touched. Increased financial repression – across the board – has characterized a nation on the verge of a police state. Between FATCA; FBAR; the banning of certain nations from the SWIFT international wiring system; heightened attacks on offshore accounts and telling Germany it must wait until 2020 to receive a measly 300 tonnes of gold, the U.S. government has shown the entire world its lack of respect for investors, both domestic and foreign. It’s no wonder Europe’s largest PM storage operator – ViaMat – has kicked out American investors; which, by the way, is NOT an issue with Miles Franklin’s Brink’s Montreal vault.

Moreover, the economic damage caused by the U.S. government is not all of the direct kind. As discussed in the “Most important article I’ve ever written,” the inflation exported by the Fed’s expanding QE program has caused the average global currency to plunge 20% over the past two years, with the majority occurring in the last nine months or so. Trust me it’s no coincidence that social unrest has erupted in the “Fragile Five” nations of India, Indonesia, Brazil, Turkey, and South Africa, where 25% of the world’s population resides; or, for that matter, many other areas. The “Final Currency War” has officially begun; and now that the Fed is committed to hyper-inflating the dollar for the sake of its Wall Street masters, all other nations are being forced to follow suit. Such is the Ponzi scheme nature of fiat currency; and no nation is a better poster child for such mutually assured destruction tactics than the “Land of the Setting Sun” itself; i.e., Japan.

Internally, both Presidential and Congressional approval ratings have reached all-time lows; in the latter case, below 10%, as each day it becomes increasingly clear how little our elected “representatives” care for America’s best interests. Between the IRS and NSA spying scandals; the Russian-squelched attempt to attack Syria; and the oppressive, inept Obamacare launch, it’s hard to believe there are any remaining believers in the efficacy of America’s government. Heck, when combining the failures of the Bush and Obama regimes, it’s difficult to find a single redeeming moment!

And then, of course, you have the political and economic carnage in the world’s largest population block – Europe. Draghi officially declared the ECB’s intention to create an unelected continental government when he stated he’d do “whatever it takes” to save the Euro in July 2012. And sadly, since then, the European economy has plummeted from hell to something worse. Like the U.S., both overt and covert market manipulation has temporarily masked the horror of economic reality.

However, with European unemployment at an all-time high – in sync with the U.S. Labor Participation rate at a 35-year low – it’s only a matter of time before reality once again steps to the fore. The people’s voices will be heard decisively in the EU Parliamentary election in May 2014; and I assure you, it won’t be pretty. Here at the Miles Franklin Blog, we continue to rate the PIIGS – or more appropriately, the PIFIGS due to France’s cascading economic issues – as the most likely to catalyze the next, irreversible, global financial crisis. And oh yeah, I forget to mention the Cyprus “bail-in”; which, since it shocked the world in March, has been accepted as a global template for future financial crisis. Nope, nothing to worry about here!

Of course, when speaking of potential “crisis catalysts,” I’d be remiss if I didn’t mention India; where, also in May, major national elections could replace the ruling, Wall Street friendly leaders with more traditional, pro-gold factions. The current Indian regime is perhaps the world’s most incompetent; and this year’s suicidal attempt to slow Precious Metals buying is already collapsing upon itself. Silver imports will set an all-time high this year; and as for gold, smuggling has become so prevalent, it has overtaken narcotics as the nation’s top illegal industry after just four months’ time. PHYSICAL premiums have surged to all-time highs above 25% – thus, making a mockery of the fraudulent PAPER markets; and with the Rupee on the cusp of plunging anew, there’s no telling what might happen in 2014. Remember, the Indian government made an insane promise earlier this year to provide heavily subsidized rice to roughly three quarters of the population; and thus, even a modest increase in rice prices could cause the nation’s finances to implode. Sort of like the U.S. national debt’s sensitivity to interest rate changes, to drive the point home.

In the interest of brevity, I’ve left out a whole bunch of things; sort of like Rodney Dangerfield in this hilarious clip from my all-time favorite comedy, Back to School. However, I of course must mention the most egregious – ultimately, self-destructive acts of Precious Metal suppression of our lifetimes. In November’s “(End of the) Manipulation Timeline,” I listed the incredible list of PM-positive headlines since “dollar-priced gold” achieved its all-time high in August 2011; and particularly, throughout 2013’s heinous Cartel attacks, as exemplified by the April 12th-15th “Alternative Currencies Destruction.”

Fortunately, those holding PHYSICAL gold and silver are none for the worse; aside, of course, from the anger, frustration, and helplessness of living through such blatant attacks on their net worth – whilst overvalued assets like stocks, bonds and real estate were supported by the very same entities putting the hammer to gold and silver. Personally, I increased my “stack” by between five and ten percent – in terms of ounces owned; and thus, have turned this year’s lemons into lemonade. Undoubtedly, it was the most mental strain I have ever dealt with – which is saying a lot, given the Cartel hell that was 2008. However, in the end game, both Miles Franklin and I have never been better positioned.

Moreover, if anything, TPTB have only accelerated the end game of fiat currency collapse, by stepping up the money printing whilst causing the tiny, remaining inventories of PHYSICAL gold and silver to be rapidly drained. I mean, seriously, record 2012 Chinese gold demand more than doubled in 2013; whilst even the U.S. Mint set a record high for Silver Eagle sales! Furthermore, with PM prices having been pushed well below the cost of production, the Cartel has inadvertently created what will unquestionably be years, if not decades, of reduced gold and silver production, just when it will be needed most. Frankly, when prices do finally take off – and consequently, permanently break the Cartel’s bonds; I expect government nationalizations and windfall profit taxes to cause further, even more deleterious production declines.

When the ball reaches Times Square at midnight on Tuesday, no one will be happier to put 2013 behind us. It was indeed a “year of infamy”; but fortunately, one that clearly set up better times for 2014 and beyond. Of course, I say “better times” tongue-in-cheek”; as whilst higher gold and silver prices will make PM holders “richer,” such events will likely coincide with a far scarier, more difficult world. The good news is the ultimate, inevitable financial crash will set the stage for a better world in the future; based on honest money, of course. However, getting from “here” to “there” will likely be an extremely dark chapter in human history. Hopefully, you are one of the few taking actions to PROTECT assets amidst what will likely be history’s largest-ever wealth transfer; and equally importantly, preparing for the difficult times ahead.

As always, Miles Franklin is here to help, as it has for the past 24 years. Give us a call, and we’ll be happy to answer your questions any time. All we ask is the opportunity to earn your business; which via premium customer service and the industry’s broadest, most intensive education platform, is our ultimate goal. We consider our clients to be “partners” in the quest to preserve wealth; and thus, are always available.

http://blog.milesfranklin.com/

http://news.goldseek.com/GoldSeek/1388348390.php

The End of Pretend

James Howard Kunstler

December 30, 2013

(special thanks to basserdan)

If being wealthy was the same as pretending to be wealthy then people who care about reality would have a little less to complain about. But pretending is a poor way for a society to negotiate its way through history. It makes for accumulating distortions which eventually undermine the society’s ability to function, especially when the pretending is about money, which is society’s operating system.

The distortion that even simple people care about is that the gap between the rich and the poor is as plain, vast, and grotesque as at any time in our history — except perhaps during slavery times in Dixieland, when many of the poor did not even own their existence. We’ve had plenty of reminders of that in pop culture the last couple of years, including Quentin Tarantino’s fiercely stupid movie Django Unchained and the more recent melodrama 12 Years a Slave. But you have to wonder what young adults weighed down by unpayable college debt think when they go to see them, because without a rebellion that millennial generation will not own their own lives either. They must know it, but they must not know what to do about it.

The pretense and distortions start at the top of American life with a President who broadcasts the message that some kind of “recovery” has occurred in the economic affairs of the country. Either he just wants the public feel better, or he is misled by the people and agencies in his own government, or perhaps he just lies to keep the lid on. To truly recover from the dislocations of 2008, we would have to make a consensual decision to start behaving differently in the process of adapting to the new circumstances that the arc of history is presenting to us. We’d have to decide to leave behind the economy of financialization, suburban sprawl, car dependency, Wal-Mart consumerism, and prepare for a different way of inhabiting North America.

The dislocations of 2008 when the banking system nearly imploded were Nature’s way of telling us that dishonesty has consequences. The immediate dishonesty of that day was the racket in securitizing worthless mortgages — promises to pay large sums of money over long periods of time. The promises were false and the collateral was janky. It got so bad and ran so far and deep that it essentially destroyed the mechanism of credit creation as it had been known until then, and it has not been repaired.

Since then, we have pretended to repair the operations of credit by falsely substituting bank bailouts and Federal Reserve “quantitative easing” (QE) or digital money-printing for plain dealing in borrowed money between honest brokers at the local level. The unfortunate consequence is that in the process we have distorted — and possibly destroyed — the value of our money and the various things denominated in it, especially securities, bonds, stocks and other money-like paper.

The crash of the mortgage racket occurred not just because of swindling and fraud among bankers; in fact, that was only a nasty symptom of something larger: peak oil. I know that many people have come to disbelieve in the idea of peak oil, but that is only another mode of playing pretend. Peak oil, which essentially arrived in 2006, undermined the basic conditions of credit creation in an advanced techno-industrial society dependent on increasing supplies of fossil fuels. Most people, including practically all credentialed economists, fail to understand this. There is a fundamental relationship between ever-increasing energy supplies > economic growth > and credit-based money (or “money,” if you will). When the energy inputs flatten out or decrease, growth stops, wealth is no longer generated, old loans can’t be repaid, and new loans can’t be generated honestly, i.e. with the expectation of repayment. That has been our predicament since 2008 and nothing has changed. We are pretending to compensate by issuing new unpayable debt to pay the interest on our old accumulated debt. This pretense can only go on so long before our economic relations reflect the basic dishonesty of it. Reality is a harsh mistress.

In the meantime, we amuse ourselves with fairy tales about “the shale oil revolution” and “the manufacturing renaissance.” 2014 could be the year that the forces of Nature compel our attention and give us a reason to stop all this pretending. I’ll address this question in next week’s annual yearly forecast.

http://kunstler.com/clusterfuck-nation/the-end-of-pretend/

Look What Big Banks Are Hiding from You Now

Dec 30th, 2013

By Shah Gilani

WallStreetInsightsandIndictments.com

Remember the outrage last July when we found out owners of giant metal storage warehouses, folks like Goldman Sachs and JPMorgan Chase, were delaying delivery of stocks of aluminum so that they could collect more rent on them?

We learned that, since Goldman took over some industrial warehouses in Detroit, the delivery time for aluminum went from six weeks to 16 months.

That got a lot of people mad because, in case you can’t add two and two, raising metal storage costs increases the prices producers who use the stuff pay for it. And of course, they pass those price increases along to consumers.

The CFTC began an investigation. The Justice Department is looking into it too. But not wanting to wait, the London Metal Exchange (LME) acted right away.

The LME is the world’s largest metal exchange. And they oversee the 778 privately owned warehouses (75% of which are owned by just five companies) that stockpile metals traded on the LME. So they got a lot of bad publicity from the fiasco. The LME threatened warehouse owners with a slap in the face if they don’t cut back delayed delivery times to only 50 days, starting April 1, 2014.

Too bad they were a day late and a few million tonnes of metal balls short.

The warehouse owners, it turns out, were already fixing the problem themselves – and have been for three years. Not because they were hell bent on getting ahead of LME rule changes and applying a market solution to a regulatory problem…

But because there’s more money in smarter manipulation.

Since 2010, warehouse owners have been building huge warehouses that aren’t governed by LME rules. According to a Wall Street Journal article from Friday, they’re storing hundreds of millions of tons of metals – like aluminum, copper, nickel, and zinc – in these “shadow warehouses,” as opposed to in LME-sanctioned warehouses.

Let’s use aluminum as an example. Analysts estimate that while there’s about 5.5 million tons of aluminum in authorized, LME-approved warehouses, there’s even more in shadow warehouses – probably between seven and 10 million tons.

Now, here’s the part where I tell you why they’re really doing this, so you don’t get fooled by what you read anywhere else.

Some analysts will postulate that storing millions of tons of metals in “off-exchange” shadow warehouses – while the world looks to spot and future prices posted at the LME as indicative of “real world” prices – will cause price collapses if huge stockpiles of warehoused metals flood the market.

Oh the fear of deflation! I’m shivering in my boots.

Don’t worry. The chance of that happening is exactly between slim and none.

It doesn’t mean metals prices won’t go down. They sure could. It means don’t expect them to go down and stay down, because that ain’t gonna happen unless we get another 2008 meltdown.

Here’s the real reason shadow warehouses are stockpiling metals…

By keeping the true levels of stockpiles from the public metals miners, financiers of metal stockpiles and warehouse owners (of course I’m talking about some giant banks and behemoth metals mining and trading corporations, like Glencore Xstrata Plc., that run this monster game) can profit from information others don’t have.

By casting stockpiles into the shadows and reducing transparency, manipulators can increase volatility, which of course is the essence of trading profitability.

How? Two ways.

First of all, if metals are taken out of the market, removed from the numbers that are counted that determine prices in a supposedly free market price discovery exchange, prices will go up. Now, if you own warehouses full of the stuff, that’s a good thing, right?

Second, there’s a futures market. That’s what they trade at the LME, futures on these metals. If the price of metals is expected to rise, futures prices for those metals will rise too. (This part gets a little technical, but hang in there with me. The payoff is big.)

When you go out on a “term basis” (in time) in the futures market and prices of further and further out delivery months are progressively higher and higher the more distant the futures expiration date, that’s called “contango.”

Metals futures prices are in contango for this reason. If you bought metals today that you needed to store, and you had the option of not buying and storing the metal today but buying the same amount via a futures contract for delivery to you in six months, the person selling you the futures contract might be the owner of the metal today, and he’s being charged for storage. So he will charge you a higher price for the futures contract to make things even. That’s part of what causes contango.

Now think about that.

If I own metals, and I store them in shadow warehouses, and the true amount of that metal in all warehouses isn’t known, but it’s believed to be less than there is (because I’m hiding mine), the price today will be higher. And since I’m charging a lot to other metals stockpilers in my LME warehouses and delaying delivery to collect more rent, which also raises the price of the metal today and therefore raises the futures prices across all delivery months, with the further out being more expensive… guess what. I can sell (short) long-dated futures contracts that I’ve artificially helped manipulate higher to finance my storage of the same metals in all my warehouses. That reduces my cost and increases my profit.

By manipulating stockpiles, smart operators can make money lots of ways.

Another way is by trading the volatility they create in the pricing structure. After all, they are manipulating the prices. If they want to dump stockpiles and trounce prices, don’t you think they’ll short the overpriced futures to profit from falling prices they force down? If you short enough, so what if the price of what you have stockpiled goes down? You will make more on your futures short if you’re a smart cookie. And these guys are smart.

And then they will buy more physical stock and futures at the bottom of the panic-selloff and profit from the price rise too.

What we have here is the freely manipulated market owned by giant banks and corporations freely manipulating everything they can because of their massive size and because they own the means of production, storage, pricing, and the officers of the armies that protect their wealth.

Welcome to the big bank- and mega corporation-owned banana republic of Earth.

Shah

http://www.wallstreetinsightsandindictments.com/2013/12/look-big-banks-hiding-now/#deeplink

Look What Big Banks Are Hiding from You Now

Dec 30th, 2013

By Shah Gilani

WallStreetInsightsandIndictments.com

Remember the outrage last July when we found out owners of giant metal storage warehouses, folks like Goldman Sachs and JPMorgan Chase, were delaying delivery of stocks of aluminum so that they could collect more rent on them?

We learned that, since Goldman took over some industrial warehouses in Detroit, the delivery time for aluminum went from six weeks to 16 months.

That got a lot of people mad because, in case you can’t add two and two, raising metal storage costs increases the prices producers who use the stuff pay for it. And of course, they pass those price increases along to consumers.

The CFTC began an investigation. The Justice Department is looking into it too. But not wanting to wait, the London Metal Exchange (LME) acted right away.

The LME is the world’s largest metal exchange. And they oversee the 778 privately owned warehouses (75% of which are owned by just five companies) that stockpile metals traded on the LME. So they got a lot of bad publicity from the fiasco. The LME threatened warehouse owners with a slap in the face if they don’t cut back delayed delivery times to only 50 days, starting April 1, 2014.

Too bad they were a day late and a few million tonnes of metal balls short.

The warehouse owners, it turns out, were already fixing the problem themselves – and have been for three years. Not because they were hell bent on getting ahead of LME rule changes and applying a market solution to a regulatory problem…

But because there’s more money in smarter manipulation.

Since 2010, warehouse owners have been building huge warehouses that aren’t governed by LME rules. According to a Wall Street Journal article from Friday, they’re storing hundreds of millions of tons of metals – like aluminum, copper, nickel, and zinc – in these “shadow warehouses,” as opposed to in LME-sanctioned warehouses.

Let’s use aluminum as an example. Analysts estimate that while there’s about 5.5 million tons of aluminum in authorized, LME-approved warehouses, there’s even more in shadow warehouses – probably between seven and 10 million tons.

Now, here’s the part where I tell you why they’re really doing this, so you don’t get fooled by what you read anywhere else.

Some analysts will postulate that storing millions of tons of metals in “off-exchange” shadow warehouses – while the world looks to spot and future prices posted at the LME as indicative of “real world” prices – will cause price collapses if huge stockpiles of warehoused metals flood the market.

Oh the fear of deflation! I’m shivering in my boots.

Don’t worry. The chance of that happening is exactly between slim and none.

It doesn’t mean metals prices won’t go down. They sure could. It means don’t expect them to go down and stay down, because that ain’t gonna happen unless we get another 2008 meltdown.

Here’s the real reason shadow warehouses are stockpiling metals…

By keeping the true levels of stockpiles from the public metals miners, financiers of metal stockpiles and warehouse owners (of course I’m talking about some giant banks and behemoth metals mining and trading corporations, like Glencore Xstrata Plc., that run this monster game) can profit from information others don’t have.

By casting stockpiles into the shadows and reducing transparency, manipulators can increase volatility, which of course is the essence of trading profitability.

How? Two ways.

First of all, if metals are taken out of the market, removed from the numbers that are counted that determine prices in a supposedly free market price discovery exchange, prices will go up. Now, if you own warehouses full of the stuff, that’s a good thing, right?

Second, there’s a futures market. That’s what they trade at the LME, futures on these metals. If the price of metals is expected to rise, futures prices for those metals will rise too. (This part gets a little technical, but hang in there with me. The payoff is big.)

When you go out on a “term basis” (in time) in the futures market and prices of further and further out delivery months are progressively higher and higher the more distant the futures expiration date, that’s called “contango.”

Metals futures prices are in contango for this reason. If you bought metals today that you needed to store, and you had the option of not buying and storing the metal today but buying the same amount via a futures contract for delivery to you in six months, the person selling you the futures contract might be the owner of the metal today, and he’s being charged for storage. So he will charge you a higher price for the futures contract to make things even. That’s part of what causes contango.

Now think about that.

If I own metals, and I store them in shadow warehouses, and the true amount of that metal in all warehouses isn’t known, but it’s believed to be less than there is (because I’m hiding mine), the price today will be higher. And since I’m charging a lot to other metals stockpilers in my LME warehouses and delaying delivery to collect more rent, which also raises the price of the metal today and therefore raises the futures prices across all delivery months, with the further out being more expensive… guess what. I can sell (short) long-dated futures contracts that I’ve artificially helped manipulate higher to finance my storage of the same metals in all my warehouses. That reduces my cost and increases my profit.

By manipulating stockpiles, smart operators can make money lots of ways.

Another way is by trading the volatility they create in the pricing structure. After all, they are manipulating the prices. If they want to dump stockpiles and trounce prices, don’t you think they’ll short the overpriced futures to profit from falling prices they force down? If you short enough, so what if the price of what you have stockpiled goes down? You will make more on your futures short if you’re a smart cookie. And these guys are smart.

And then they will buy more physical stock and futures at the bottom of the panic-selloff and profit from the price rise too.

What we have here is the freely manipulated market owned by giant banks and corporations freely manipulating everything they can because of their massive size and because they own the means of production, storage, pricing, and the officers of the armies that protect their wealth.

Welcome to the big bank- and mega corporation-owned banana republic of Earth.

Shah

http://www.wallstreetinsightsandindictments.com/2013/12/look-big-banks-hiding-now/#deeplink

Fourteen ways you can avoid being forced into Obamacare.

Business Insider

Dec. 30, 2013

There are 14 different ways you may qualify for a 'hardship waiver.'

Last week, the Obama administration announced that anyone whose health plan was cancelled due to the Affordable Care Act and believe other plans offered are unaffordable will receive a 'hardship waiver.' This waiver exempts them from the individual mandate and allows them to purchase a cheaper catastrophic plan that was previously available only to those under the age of 30.

But losing your health insurance is not the only experience that qualifies a person for a waiver. In fact, there are 13 other ways that people qualify.

Here are all 14 straight from the Centers for Medicare and Medicaid:

1. You were homeless.

2. You were evicted in the past 6 months or were facing eviction or foreclosure.

3. You received a shut-off notice from a utility company.

4. You recently experienced domestic violence.

5. You recently experienced the death of a close family member.

6. You experienced a fire, flood, or other natural human-caused disaster that caused substantial damage to your property.

7. You filed for bankruptcy in the last 6 months.

8. You had medical expenses you couldn't pay in the last 24 months.

9. You experienced unexpected increases in necessary expenses due to caring for an ill, disabled, or aging family member.

10. You expect to claim a child as a tax dependent who's been denied coverage in Medicaid and the Children's Health Insurance Program (CHIP), and another person is required by court order to give medical support to the child.

11. As a result of an eligibility appeals decision, you're eligible either for: 1) enrollment in a qualified health plan (QHP) through the Marketplace, 2) lower costs on your monthly premiums, or 3) cost-sharing reductions for a time period when you weren't enrolled in a QHP through the Marketplace.

12. You were determined ineligible for Medicaid because your state didn't expand eligibility for Medicaid under the Affordable Care Act.

13. received a notice saying that your current health insurance plan is being cancelled, and you consider the other plans available unaffordable.

14. You experienced another hardship in obtaining health insurance.

http://www.silverbearcafe.com/private/12.13/avoid.html

The Art of Giving

Bob Moriarty

Archives

Dec 30, 2013

I traveled a lot during 2013 visiting projects. By far the most interesting and rewarding visit was one I made to Mexico with Gordon Holmes of The Au Report and Jeff Phillips of Global Market Development. We were in Mexico to give hundreds of wheelchairs away. I learned a lot about the Art of Giving.

Gordon Holmes started a foundation named the Lookout Ridge Foundation https://sites.google.com/site/thelookoutridgefoundation/ years ago. It donates wheelchairs to needy persons all over the world. Jeff Phillips began a foundation he calls the India Phillips Foundation http://indiaphillips.com/ in memory of his daughter India who died literally overnight two years ago. Gordon and Jeff donated wheelchairs on their behalf and Almaden Minerals also contributed. I was asked along as part of a site visit to Almaden.

The UN estimates that 150 million people in the world need wheelchairs and cannot afford them. Neither can their governments afford even the cheapest of wheelchairs for them. Jeff and Gordon give wheelchairs to a few when they can. It is part of the art of giving.

I think that everyone can remember some gift in their life that carries substantial memories. It might have been a bike when you were five or an engagement ring in your twenties. You remember back fondly with the thoughtfulness and wonder that came with the gift.

Multiply that by 100 and that’s what these wheelchairs mean to those who receive them. Gordon has asked me a couple of times to come on a trip where he was giving away a trailer load of wheelchairs but something always came up until this last May when I went to Mexico and participated in one of their mass distributions.

Since the cost of transportation is such a large part of the total price of the wheelchairs, Gordon waits until he can fill a container with wheelchairs. He collects the ages and sizes of those the chairs are intended for. Wheelchairs are sized for the person getting the chair and for the type of terrain they will be used with.

Lookout Ridge has donated over 10,000 wheelchairs through various programs it is associated with. Gordon has personally distributed wheelchairs in Mexico, Ghana, Mali and the Philippines. On the trip I went on, Almaden Minerals paid for a number of chairs as part of a corporate contribution.

We did distributions in two different towns. All I can say about the distributions was that it was heart wrenching to see the gratitude the people showed who got them and family members. I saw people almost crawling in who were in their 70s and forced to use a tree branch to stumble along. Children who had never had mobility all of a sudden could zoom around for the first time in their lives. Old women with one leg could now visit shops without pain. It was moving, the most moving experience I have ever seen.

150 million people still need wheelchairs and without the generosity of Gordon Holmes, Jeff Phillips, Almaden Minerals and you, they will do without. Every donation, no matter how large or how small will go into chairs, not administration. Donations are tax deductable in both Canada and the US.

If you want to know the Art of Giving, try giving. You can donate here before January 1 and take a deduction for 2013.

###

Bob Moriarty

President: 321gold

Archives

http://www.321gold.com/editorials/moriarty/moriarty123013.html

The Art of Giving

Bob Moriarty

Archives

Dec 30, 2013

I traveled a lot during 2013 visiting projects. By far the most interesting and rewarding visit was one I made to Mexico with Gordon Holmes of The Au Report and Jeff Phillips of Global Market Development. We were in Mexico to give hundreds of wheelchairs away. I learned a lot about the Art of Giving.

Gordon Holmes started a foundation named the Lookout Ridge Foundation https://sites.google.com/site/thelookoutridgefoundation/ years ago. It donates wheelchairs to needy persons all over the world. Jeff Phillips began a foundation he calls the India Phillips Foundation http://indiaphillips.com/ in memory of his daughter India who died literally overnight two years ago. Gordon and Jeff donated wheelchairs on their behalf and Almaden Minerals also contributed. I was asked along as part of a site visit to Almaden.

The UN estimates that 150 million people in the world need wheelchairs and cannot afford them. Neither can their governments afford even the cheapest of wheelchairs for them. Jeff and Gordon give wheelchairs to a few when they can. It is part of the art of giving.

I think that everyone can remember some gift in their life that carries substantial memories. It might have been a bike when you were five or an engagement ring in your twenties. You remember back fondly with the thoughtfulness and wonder that came with the gift.

Multiply that by 100 and that’s what these wheelchairs mean to those who receive them. Gordon has asked me a couple of times to come on a trip where he was giving away a trailer load of wheelchairs but something always came up until this last May when I went to Mexico and participated in one of their mass distributions.

Since the cost of transportation is such a large part of the total price of the wheelchairs, Gordon waits until he can fill a container with wheelchairs. He collects the ages and sizes of those the chairs are intended for. Wheelchairs are sized for the person getting the chair and for the type of terrain they will be used with.

Lookout Ridge has donated over 10,000 wheelchairs through various programs it is associated with. Gordon has personally distributed wheelchairs in Mexico, Ghana, Mali and the Philippines. On the trip I went on, Almaden Minerals paid for a number of chairs as part of a corporate contribution.

We did distributions in two different towns. All I can say about the distributions was that it was heart wrenching to see the gratitude the people showed who got them and family members. I saw people almost crawling in who were in their 70s and forced to use a tree branch to stumble along. Children who had never had mobility all of a sudden could zoom around for the first time in their lives. Old women with one leg could now visit shops without pain. It was moving, the most moving experience I have ever seen.

150 million people still need wheelchairs and without the generosity of Gordon Holmes, Jeff Phillips, Almaden Minerals and you, they will do without. Every donation, no matter how large or how small will go into chairs, not administration. Donations are tax deductable in both Canada and the US.

If you want to know the Art of Giving, try giving. You can donate here before January 1 and take a deduction for 2013.

###

Bob Moriarty

President: 321gold

Archives

http://www.321gold.com/editorials/moriarty/moriarty123013.html

Obamacare Showdown: Missouri Bill to Gut Obamacare, Ban Penalties, Ban Healthcare Exchange; How Would Obama Respond?

Friday, December 27, 2013

Mish's Global Economic Trend Analysis

If enough states act, we are on the way to a constitutional showdown over Obamacare. The Washington Times reports Missouri bill would gut Obamacare