News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

investor15

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Taibbi: The Vampire Squid Strikes Again: The Mega Banks' Most Devious Scam Yet

Banks are no longer just financing heavy industry. They are actually buying it up and inventing bigger, bolder and scarier scams than ever

By Matt Taibbi

February 12, 2014

(special thanks to basserdan)

Call it the loophole that destroyed the world. It's 1999, the tail end of the Clinton years. While the rest of America obsesses over Monica Lewinsky, Columbine and Mark McGwire's biceps, Congress is feverishly crafting what could yet prove to be one of the most transformative laws in the history of our economy – a law that would make possible a broader concentration of financial and industrial power than we've seen in more than a century.

But the crazy thing is, nobody at the time quite knew it. Most observers on the Hill thought the Financial Services Modernization Act of 1999 – also known as the Gramm-Leach-Bliley Act – was just the latest and boldest in a long line of deregulatory handouts to Wall Street that had begun in the Reagan years.

Wall Street had spent much of that era arguing that America's banks needed to become bigger and badder, in order to compete globally with the German and Japanese-style financial giants, which were supposedly about to swallow up all the world's banking business. So through legislative lackeys like red-faced Republican deregulatory enthusiast Phil Gramm, bank lobbyists were pushing a new law designed to wipe out 60-plus years of bedrock financial regulation. The key was repealing – or "modifying," as bill proponents put it – the famed Glass-Steagall Act separating bankers and brokers, which had been passed in 1933 to prevent conflicts of interest within the finance sector that had led to the Great Depression. Now, commercial banks would be allowed to merge with investment banks and insurance companies, creating financial megafirms potentially far more powerful than had ever existed in America.

All of this was big enough news in itself. But it would take half a generation – till now, basically – to understand the most explosive part of the bill, which additionally legalized new forms of monopoly, allowing banks to merge with heavy industry. A tiny provision in the bill also permitted commercial banks to delve into any activity that is "complementary to a financial activity and does not pose a substantial risk to the safety or soundness of depository institutions or the financial system generally."

Complementary to a financial activity. What the hell did that mean?

"From the perspective of the banks," says Saule Omarova, a law professor at the University of North Carolina, "pretty much everything is considered complementary to a financial activity."

Fifteen years later, in fact, it now looks like Wall Street and its lawyers took the term to be a synonym for ruthless campaigns of world domination. "Nobody knew the reach it would have into the real economy," says Ohio Sen. Sherrod Brown. Now a leading voice on the Hill against the hidden provisions, Brown actually voted for Gramm-Leach-Bliley as a congressman, along with all but 72 other House members. "I bet even some of the people who were the bill's advocates had no idea."

Today, banks like Morgan Stanley, JPMorgan Chase and Goldman Sachs own oil tankers, run airports and control huge quantities of coal, natural gas, heating oil, electric power and precious metals. They likewise can now be found exerting direct control over the supply of a whole galaxy of raw materials crucial to world industry and to society in general, including everything from food products to metals like zinc, copper, tin, nickel and, most infamously thanks to a recent high-profile scandal, aluminum. And they're doing it not just here but abroad as well: In Denmark, thousands took to the streets in protest in recent weeks, vampire-squid banners in hand, when news came out that Goldman Sachs was about to buy a 19 percent stake in Dong Energy, a national electric provider. The furor inspired mass resignations of ministers from the government's ruling coalition, as the Danish public wondered how an American investment bank could possibly hold so much influence over the state energy grid.

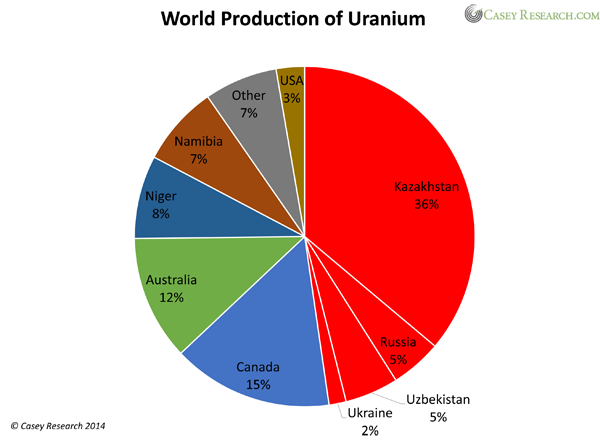

There are more eclectic interests, too. After 9/11, we found it worrisome when foreigners started to get into the business of running ports, but there's been little controversy as banks have done the same, or even started dabbling in other activities with national-security implications – Goldman Sachs, for instance, is apparently now in the uranium business, a piece of news that attracted few headlines.

But banks aren't just buying stuff, they're buying whole industrial processes. They're buying oil that's still in the ground, the tankers that move it across the sea, the refineries that turn it into fuel, and the pipelines that bring it to your home. Then, just for kicks, they're also betting on the timing and efficiency of these same industrial processes in the financial markets – buying and selling oil stocks on the stock exchange, oil futures on the futures market, swaps on the swaps market, etc.

Allowing one company to control the supply of crucial physical commodities, and also trade in the financial products that might be related to those markets, is an open invitation to commit mass manipulation. It's something akin to letting casino owners who take book on NFL games during the week also coach all the teams on Sundays. (my bolding for emphasis)

The situation has opened a Pandora's box of horrifying new corruption possibilities, but it's been hard for the public to notice, since regulators have struggled to put even the slightest dent in Wall Street's older, more familiar scams. In just the past few years we've seen an explosion of scandals – from the multitrillion-dollar Libor saga (major international banks gaming world interest rates), to the more recent foreign-currency-exchange fiasco (many of the same banks suspected of rigging prices in the $5.3-trillion-a-day currency markets), to lesser scandals involving manipulation of interest-rate swaps, and gold and silver prices.

But those are purely financial schemes. In these new, even scarier kinds of manipulations, banks that own whole chains of physical business interests have been caught rigging prices in those industries. For instance, in just the past two years, fines in excess of $400 million have been levied against both JPMorgan Chase and Barclays for allegedly manipulating the delivery of electricity in several states, including California. In the case of Barclays, which is contesting the fine, regulators claim prices were manipulated to help the bank win financial bets it had made on those same energy markets.

And last summer, The New York Times described how Goldman Sachs was caught systematically delaying the delivery of metals out of a network of warehouses it owned in order to jack up rents and artificially boost prices.

You might not have been surprised that Goldman got caught scamming the world again, but it was certainly news to a lot of people that an investment bank with no industrial expertise, just five years removed from a federal bailout, stores and controls enough of America's aluminum supply to affect world prices.

How was all of this possible? And who signed off on it?

By exploiting loopholes in a dense, decade-and-a-half-old piece of financial legislation, Wall Street has effected a revolutionary change that American citizens never discussed, debated or prepared for, and certainly never explicitly permitted in any meaningful way: the wholesale merger of high finance with heavy industry. This blitzkrieg reorganization of our economy has left millions of Americans facing a smorgasbord of frightfully unexpected new problems. Do we even have a regulatory structure in place to look out for these new forms of manipulation? (Answer: We don't.) And given that the banking sector that came so close to ruining the world economy five years ago has now vastly expanded its footprint, who's in charge of preventing the next crash?

In this Brave New World, nobody knows. Moreover, whatever we've done, it's too late to have a referendum on it. Garrett Wotkyns, an Arizona-based class-action attorney who has spent more than a year investigating the banks' involvement in the metals markets and is suing Goldman and others over the aluminum case on behalf of two major manufacturers, puts it this way: "It's like that line in The Dark Knight Rises," he says. "'The storm isn't coming. The storm is already here.'"

To this day, the provenance of the "complementary activities" loophole that set much of this mess in motion remains something of a mystery. We know from congressional records that a vice chairman of JPMorgan, Michael Patterson, was one of the first to push the idea in House testimony in February 1999 and that, later that year, an early version of the bill put forward in the Senate by Phil Gramm also contained the provision.

But even one of the final bill's eventual authors, Republican congressman Jim Leach, can't remember exactly whose idea adding the "complementary activities" line was. "I know of no legislative history of the provision," he says. "It probably came from the Senate side."

Moreover, Leach was shocked to hear that regulators had pointed to this section of a bill bearing his name as the legal authority allowing banks to gain control over physical-commodities markets. "That's news to me," says the mortified ex-congressman, now a law professor at the University of Iowa. "I assume no one at the time would have thought it would apply to commodities brokering of a nature that has recently been reported."

One thing that is clear in the public record is that nobody was talking, at least publicly, about banks someday owning oil tankers or controlling the supply of industrial metals.

The JPMorgan witness, Michael Patterson, told the House Financial Services Committee at the 1999 hearing that his idea of "complementary activities" was, say, a credit-card company putting out a restaurant guide. "One example is American Express, which publishes magazines," he testified. "Travel + Leisure magazine is complementary to the travel business. Food & Wine promotes dining out?.?.?.?which might lead to greater use of the American Express card."

"That's how insignificant this was supposed to be," says Omarova. "They were talking about being allowed to put out magazines."

Even apart from the "complementary" provision, Gramm quietly added another time bomb to the law, a grandfather clause, which said that any company that became a bank holding company after the passage of Gramm-Leach-Bliley in 1999 could engage in (or control shares of a company engaged in) commodities trading – but only if it was already doing so before a seemingly arbitrary date in September 1997.

This meant that if you were a bank holding company at the time the law was passed and you wanted to get into the commodities business, you were out of luck, because the federal law prohibited banks from being involved in physical commodities or any other forms of heavy industry. But if you were already a commodities dealer in 1997 and then somehow became a bank holding company, you could get into whatever you pleased.

This was nuts. It was a little like passing a law that ordered you to leave the Army if you were gay in November 1999 – but if you were a heterosexual soldier as of September 1997 and then somehow became gay after 1999, you could stay in the Army.

To this day, nobody is exactly clear on what the grandfather clause means. If a company traded in tin before 1997 and then became a bank holding company in 2015, would it have to stick with tin? Or did the fact that it traded tin in 1997 mean the company could buy oil tankers and pipelines in 2020?

In 2012, the Federal Reserve Bank of New York – the most powerful branch of the Fed, the primary regulator of bank holding companies and the final authority on these things – put out a paper saying it had no clue about the exact meaning of the provision. "The legal scope of the exemption," a trio of New York Fed officials wrote in July that year, "is widely seen as ambiguous." Just a few weeks ago, the Fed's director of banking supervision, Michael Gibson, told the Senate, "I'm not a lawyer," and that it's "under review."

It almost didn't matter. For nearly a decade, this obscure provision of Gramm-Leach-Bliley effectively applied to nobody. Then, in the third week of September 2008, while the economy was imploding after the collapses of Lehman and AIG, two of America's biggest investment banks, Goldman Sachs and Morgan Stanley, found themselves in desperate need of emergency financing. So late on a Sunday night, on September 21st, to be exact, the two banks announced they had applied to the Federal Reserve to become bank holding companies, which would give them lifesaving access to emergency cash from the Fed's discount window.

The Fed granted the requests overnight. The move saved the bacon of both firms, and it had one additional benefit: It made Goldman and Morgan Stanley, which both had significant commodity-trading operations prior to 1997, the first and last two companies to qualify for the grandfather exemption of the Gramm-Leach-Bliley Act. "Kind of convenient, isn't it?" says one congressional aide. "It's almost like the law was written specifically for them."

The irony was incredible. After fucking up so badly that the government had to give them federal bank charters and bottomless wells of free cash to save their necks, the feds gave Goldman Sachs and Morgan Stanley hall passes to become cross-species monopolistic powers with almost limitless reach into any sectors of the economy.

And they weren't the only accidental beneficiaries of the crisis. JPMorgan Chase acquired the commodity-trading operations of Bear Stearns in early 2008, after the Fed pledged billions in guarantees to help Chase rescue the doomed investment bank. Within the next two years, Chase also acquired the commodities operations of another failing bank, the newly nationalized Royal Bank of Scotland, which included Henry Bath, a U.K.-based company that owns a large network of warehouses throughout Europe.

As a result, entering 2010, these three companies were newly empowered to go out and start doubling down on investments in physical industry. Through a fortuitous circumstance, the cost of financing for bank holding companies had also dropped like a stone by the end of 2009, as the Fed slashed interest rates almost to zero in a desperate attempt to stimulate the economy out of its post-crash doldrums.

The sudden turning on of this huge faucet of free money seems to have been a factor in an ensuing commodities shopping spree undertaken by all three firms. Morgan Stanley, for instance, claimed to have just $2.5 billion in commodity assets in March 2009. By September 2011, those holdings had nearly quadrupled, to $10.3 billion.

Goldman and Chase – along with Glencore and Trafigura, a pair of giant Swiss-based conglomerates that were offshoots of a firm founded by notorious deceased commodities trader and known market manipulator Marc Rich – all made notably coincidental purchases of metals-warehousing companies in 2010.

The presence of these Marc Rich entities is particularly noteworthy. According to famed Forbes reporter Paul Klebnikov, who was assassinated in 2004 after years of reports on Russian corruption, Rich made a fortune in the early Nineties striking crooked deals with the Soviet bosses who controlled the U.S.S.R.'s supplies of raw materials – in particular commodities like zinc and aluminum. These deals helped create a fledgling class of profiteers among the bosses of the crumbling Soviet empire, a class that would go on years later to help push Russia out of its communist past into its kleptocratic present.

"He'd strike a deal with the local party boss, or the director of a state-owned company," Klebnikov said back in 2001. "He'd say, 'OK, you will sell me the [commodity] at five to 10 percent of the world-market price?.?.?.?and in return, I will deposit some of the profit I make by reselling it 10 times higher on the world market, and put the kickback in a Swiss bank account.'"

Rich made these reported deals while in exile from the United States, which he fled in 1983 after the U.S. government charged him with tax evasion, wire fraud, racketeering and trading with the enemy after being caught trading with rogue states like Iran, among other things. The state filed enough counts to put him away for life, and he remained a fugitive until January 2001, when a little-known Clinton administration Justice Department official named Eric Holder recommended Rich be pardoned. A report by the House Committee on Government Reform later concluded that Holder had not provided a credible explanation for supporting Rich's pardon and that he must have had "other motivations" that he didn't share with Congress. Among other things, the committee speculated that Holder had designs on the attorney general's office in a potential Al Gore administration.

In any case, in 2010, a decade after the Rich pardon, Holder was attorney general, but under Barack Obama, and two Rich-created firms, along with two banks that have been major donors to the Democratic Party, all made moves to buy up metals warehouses. In near simultaneous fashion, Goldman, Chase, Glencore and Trafigura bought companies that control warehouses all over the world for the LME, or London Metals Exchange. The LME is a privately owned exchange for world metals trading. It's the world's primary hub for determining metals prices and also for trading metals-based futures, options, swaps and other instruments.

"If they were just interested in collecting rent for metals storage, they'd have bought all kinds of warehouses," says Manal Mehta, the founder of Sunesis Capital, a hedge fund that has done extensive research on the banks' forays into the commodities markets. "But they seemed to focus on these official LME facilities."

The JPMorgan deal seemed to be in direct violation of an order sent to the bank by the Fed in 2005, which declared the bank was not authorized to "own, operate, or invest in facilities for the extraction, transportation, storage, or distribution of commodities." The way the Fed later explained this to the Senate was that the purchase of Henry Bath was OK because it considered the acquisition of this commodities company kosher within the context of a larger sale that the Fed was cool with – "If the bulk of the acquisition is a permissible activity, they're allowed to include a small amount of impermissible activities."

What's more, according to LME regulations, no warehouse company can also own metal or make trades on the exchange. While they may have been following the letter of the law, they were certainly violating the spirit: Goldman preposterously seems to have engaged in all three activities simultaneously, changing a hat every time it wanted to switch roles. It conducted its metal trades through its commodities subsidiary J. Aron, and then put Metro, its warehouse company, in charge of the storage, and according to industry experts, Goldman most likely owned some metal, though the company has remained vague on the subject.

If you're wondering why the LME would permit a seemingly blatant violation of its own rules, a good place to start would be to look at who owned the LME at the time. Although it eventually sold itself to a Hong Kong company in 2012, in 2010 the LME was owned by a consortium of banks and financial companies. The two largest shareholders? Goldman and JPMorgan Chase.

Humorously, another was Koch Metals (2.32 percent), a commodities concern that's part of the Koch brothers' empire. The Kochs have been caught up in their own commodity-manipulation schemes, including an episode in 2008, in which they rented out huge tankers and used them to store excess oil offshore essentially as floating warehouses, taking cheap oil out of available supply and thereby helping to drive up energy prices. Additionally, some banks have been accused of similar oil-hoarding schemes.

The motive for the Kochs, or anyone else, to hoard a commodity like oil can be almost beautiful in its simplicity. Basically, a bank or a trading company wants to buy commodities cheap in the present and sell them for a premium as futures. This trade, sometimes called "arbitraging the contango," works best if the cost of storing your oil or metals or whatever you're dealing with is negligible – you make more money off the futures trade if you don't have to pay rent while you wait to deliver.

So when financial firms suddenly start buying oil tankers or warehouses, they could be doing so to make bets pay off, as part of a speculative strategy – which is why the banks' sudden acquisitions of metals-storage companies in 2010 is so noteworthy.

These were not minor projects. The firms put high-ranking executives in charge of these operations. Goldman's acquisition of Metro was the project of Isabelle Ealet, the bank's then-global commodities chief. (In a curious coincidence commented upon by several sources for this story, many of Goldman's most senior officials, including CEO Lloyd Blankfein and president Gary Cohn, started their careers in Goldman's commodities division.)

Meanwhile, Chase's own head of commodities operations, Blythe Masters – an even more famed Wall Street figure, sometimes described as the inventor of the credit default swap – admitted that her company's warehouse interests weren't just a casual thing. "Just being able to trade financial commodities is a serious limitation because financial commodities represent only a tiny fraction of the reality of the real commodity exposure picture," she said in 2010.

Loosely translated, Masters was saying that there was a limited amount of money to be made simply trading commodities in the traditional legal manner. The solution? "We need to be active in the underlying physical commodity markets," she said, "in order to understand and make prices."

We need to make prices. The head of Chase's commodities division actually said this, out loud, and it speaks to both the general unlikelihood of God's existence and the consistently low level of competence of America's regulators that she was not immediately zapped between the eyebrows with a thunderbolt upon doing so. Instead, the government sat by and watched as a curious phenomenon developed at all of these new bank-owned warehouses, in the aluminum markets in particular.

As detailed by New York Times reporter David Kocieniewski last July, Goldman had bought into these warehouses and soon began pointlessly shuttling stocks of aluminum from one warehouse to another. It was a "merry-go-round of metal," as one former forklift operator called it, a scheme of delays apparently designed to drive up prices of the metal used to make the stuff we all buy – like beer cans, flashlights and car parts.

When Goldman bought Metro in February 2010, the average delivery time for an aluminum order was six weeks. Under Goldman ownership, Metro's delivery times soon ballooned by a factor of 10, to an average of 16 months, leading in part to the explosive growth of a surcharge called the Midwest premium, which represented not the cost of aluminum itself but the cost of its storage and delivery, a thing easily manipulated when you control the supply. So despite the fact that the overall LME price of aluminum fell during this time, the Midwest premium conspicuously surged in the other direction. In 2008, it represented about three percent of the LME price of aluminum. By 2013, it was a whopping 15 percent of the benchmark (it has since spiked to 25 percent).

"In layman's terms, they were artificially jacking up the shipping and handling costs," says Mehta.

The intentional warehouse delays were just one part of the anti-capitalist game the banks were playing. As an incentive to get metal under their control, they actually paid the industrial producers of aluminum extra cash to store the metal in their warehouses, fees reportedly as much as $230 a metric ton.

Both Goldman and Glencore reportedly offered such incentives, which not only allowed the companies to collect more rent (Goldman was charging a daily rate of 48 cents a metric ton) but also served to discourage industrial producers like Alcoa or the Russian industrial giant Rusal (which has Glencore CEO Ivan Glasenberg on its board of directors) from selling directly to manufacturers.

The result of all this was a bottlenecking of aluminum supplies. A crucial industrial material that was plentiful and even in oversupply was now stuck in the speculative merry-go-round of the bank finance trade.

Every time you bought a can of soda in 2011 and 2012, you paid a little tax thanks to firms like Goldman. Mehta, whose fund has a financial stake in the issue, insists there's an irony here that should infuriate everyone. "Banks used taxpayer-backed subsidies," he says, "to drive up prices for the very same taxpayers that bailed them out in the first place."

Dave Smith, Coca-Cola's strategic procurement manager, told reporters as early as the summer of 2011 that "the situation has been organized to artificially drive up premiums." Nick Madden, the chief procurement officer of Novelis, a leading can-maker, said at roughly the same time that the delays in Detroit were adding $20 to $40 a metric ton to the price of aluminum.

Coca-Cola was the first to file a complaint against Goldman over the warehouse issue, doing so in mid-2011, and many people in and around the industry weren't surprised that it was the world's biggest and most powerful corporate consumer of aluminum that came forward first. Other manufacturers, many believe, kept their mouths shut out of fear the banks would punish them. "It's very likely that commercial companies deliberately avoided an open confrontation with Goldman because it was a Wall Street powerhouse with which they had – or hoped to establish – important credit and financial-advisory relationships," says Omarova. One government official who has investigated the issue for Congress said even some of the country's largest aluminum users have been reluctant to come forward. "When some of these huge transnationals don't want to talk about it, it makes you wonder," the aide noted.

SStill, a few days after the Times published its aluminum-storage exposé in late July 2013, Sen. Brown held hearings to investigate the causes of the alleged manipulation. (One executive, Tim Weiner of MillerCoors, would testify that global aluminum costs for manufacturers had been inflated by $3 billion in just the past year.) After those hearings, and after word leaked out that regulatory agencies had launched investigations, Goldman curtly announced new plans to reduce the delivery times of its aluminum stocks. The bank has consistently maintained that its interest in the warehouse company Metro is not "strategic," that it only bought the firm "as an investment," and will sell it within 10 years. JPMorgan Chase and other banks announced that it might be getting out of the physical commodities business altogether. The LME, meanwhile, had already come up with plans to force its member warehouses to increase their output of aluminum.

A few weeks later, on August 9th, 2013, a company called CME Group – one of the world's leading derivatives dealers – announced that it would henceforth be selling a new kind of aluminum swap futures contract. The new instrument, the firm said, would be "the first Exchange product that enables the aluminum Midwest premium to be managed."

What this signaled was that before that moment, no one in the financial sector wanted to get within a hundred miles of selling price insurance against the Midwest premium, because it was so obviously corrupt. But then the Times let the cat out of the bag, and next thing you knew, now that everyone was watching, a major derivatives purveyor suddenly felt confident enough to sell a hedging insurance against the Midwest premium, given that it was now presumed, once again, to be free from manipulation and subject to market forces.

"That should tell you a lot about how completely people in the business understood that the metals market was broken," says Wotkyns.

One other bizarre footnote to the aluminum scandal: According to the Bank Holding Company Act of 1956, any company that becomes a bank holding company must divest itself of certain commercial holdings it may own within two years. To that two-year grace period, the Fed may add up to three additional years. This was done for both Goldman and Morgan Stanley. The aluminum scandal broke, coincidentally, just a few months before Goldman's five-year grace period was scheduled to end. There was some expectation that the Fed might order the banks to divest some of their commercial holdings.

But there was a catch. "Congress in its infinite wisdom left an ambiguity," says Omarova. Although the Bank Holding Company Act mandated that the companies had to be compliant at the end of the review period, it didn't actually specify what the Fed had to do if they weren't. When Goldman's review period passed, "the Fed took the position that nothing had to happen," says Omarova. "So nothing happened."

The aluminum delays were not just an isolated incident of banks scheming to boost rent revenue. Recently, evidence has surfaced that the same kinds of behavior may be going on across the LME. In order for a parcel of metal to be traded on the LME, it has to be what's called "on warrant." If you are the owner of a metal that you no longer want to be traded, you can "cancel the warrant" – essentially taking it out of the system. It's still in the warehouse, but in a kind of administrative limbo.

When the world LME supply of a metal features high percentages of canceled stock, that typically means someone is moving metals around a lot even after they've been put into storage – perhaps in a Goldman-style "merry-go-round," perhaps for some other reason, but historically it has not been something seen often in functioning, healthy metals markets.

In January 2009, before the American too-big-to-fail banks and the shady Swiss commodities giants bought into all of these warehouses, less than one percent of the total global supply of LME aluminum was "canceled warrant." Today, with world supplies of aluminum about double what they were then, 45.2 percent of the total stock is classified as canceled. In Detroit, where Goldman is supposedly cleaning things up, the percentage is even crazier: 76.9 percent of the aluminum stock has canceled warrants.

You can see hints of the phenomenon in other LME metals. Five years ago, just 1.3 percent of the LME's copper stocks had canceled warrants. Today, 59 percent of it does. In January 2009, just 2.3 percent of zinc stocks were canceled; it's at 32 percent today. Zinc incidentally has something else in common with aluminum – a shipping-and-handling-like premium, called the U.S. zinc premium in the United States, which has skyrocketed in recent years, increasing by 400 percent between the summer of 2012 and the summer of 2013, when the price plateaued just as the aluminum scandal broke.

Then there's nickel. Thirty-seven percent of the global stock is now classified as canceled. Five years ago, 0.5 percent was. One industry insider, who is very familiar with and utilizes the nickel market, says that despite the fact that there is a massive global oversupply of the metal, prices are being artificially propped up as much as 20 to 30 percent.

He blames the banks' speculative weigh stations, saying that nickel producers, despite low global demand, are cheerfully selling their stocks to bank-run warehouses, which are paying above-market prices to put raw materials into the merry-go-round. "They are happy to sell to the banks and to the warehouse supply, while they pray for demand to pick up," the insider said.

This leads to the next potentially disastrous aspect of this story: What happens if the Fed suddenly raises interest rates, and the banks, their access to free money cut off, can no longer afford to sit on piles of metal for 16 months at a time?

"Look at nickel," says Eric Salzman, a financial analyst who has done research on metals manipulation for several law firms. "You could see the price drop 20 to 30 percent in no time. It'd be a classic bursting of a bubble."

But the potential for wide-scale manipulation and/or new financial disasters is only part of the nightmare that this new merger of banking and industry has created. The other, perhaps even darker problem involves the new existential dangers both to the environment and to the stability of the financial system. Long before Goldman and Chase started buying up metals warehouses, for instance, Morgan Stanley had already bought up a substantial empire of physical businesses – electricity plants in a number of states, a firm that trades in heating oil, jet fuels, fertilizers, asphalt, chemicals, pipelines and a global operator of oil tankers.

How long before one of these fully loaded monster ships capsizes, and Morgan Stanley becomes the next BP, not only killing a gazillion birds and sea mammals off some unlucky country's shores but also taking the financial system down with them, as lawsuits plunge the company into bankruptcy with Lehman-style repercussions? Morgan Stanley's CEO, James Gorman, even admitted how risky his firm's new acquisitions were last year, when he reportedly told staff that a hypothetical oil spill was "a risk we just can't take."

The regulators are almost worse. Remember the 2008 collapse happened when government bodies like the Fed, the Office of the Comptroller of the Currency and the Office of Thrift Supervision – whose entire expertise supposedly revolves around monitoring the safety and soundness of financial companies – somehow missed that half of Wall Street was functionally bankrupt.

Now that many of those financial companies have been bailed out, those same regulators who couldn't or wouldn't smell smoke in a raging fire last time around are suddenly in charge of deciding if companies like Morgan Stanley are taking out enough insurance on their oil tankers, or if banks like Goldman Sachs are properly handling their uranium deposits.

"The Fed isn't the most enthusiastic regulator in the best of times," says Brown. "And now we're asking them to take this on?"

Banks in America were never meant to own industries. This principle has been part of our culture practically from the beginning of our history. The original restrictions on banks getting involved with commerce were rooted in the classically American fear of overweening government power – citizens in the early 1800s were concerned about the potential for monopolistic abuses posed by state-sponsored banks.

Later, however, Americans also found themselves forced to beat back a movement of private monopolies, in particular the great railroad and energy cartels built by robber barons of the Rockefeller type who, by the late 1800s, were on the precipice of swallowing markets whole and dictating to the public the prices of everything from products to labor. It took a long period of upheaval and prolonged fights over new laws like the Sherman and Clayton anti-trust acts before those monopolies were reined in.

Banks, however, were never really regulated under those laws. Only the Great Depression and years of brutal legislative trench warfare finally brought them to heel under the same kinds of anti-trust concepts that stopped the robber barons, through acts like Glass-Steagall and the Bank Holding Company Act of 1956. Then, with a few throwaway lines in a 1999 law that nobody ever heard of until now, that whole struggle went up in smoke, and here we are, in Hobbes' jungle, waiting for the next fully legal catastrophe to unfold.

When does the fun part start?

This story is from the February 27th, 2014 issue of Rolling Stone.

http://www.rollingstone.com/politics/news/the-vampire-squid-strikes-again-the-mega-banks-most-devious-scam-yet-20140212

The Smog of Fraud

James Howard Kunstler

February 10, 2014

(special thanks to basserdan)

Team Obama pulled a cute one last week nominating Blythe Masters, JP Morgan’s commodity chief, to an advisory committee of the Commodity Futures Trading Commission (CFTC) which supposedly regulates activities on the paper trades in corn, pork bellies, cocoa, coffee, wheat, corn — oh, and gold, too, by the way, in which JP Morgan has been suspected of massive gold (and silver) market manipulations and other misconduct lately. That would include the 2011 MF Global Fiasco in which nearly a billion dollars from “segregated” customer accounts somehow ended up parked over at JP Morgan as a result of bad derivative bets on tanking Eurozone bonds. MF Global, primarily a commodities trading brokerage, was liquidated in 2011. The CFTC never issued referrals for prosecution to the Department of Justice in the matter and, of course, MF Global’s notorious CEO, Jon Corzine remains at large, enjoying caramel flan lattes in the Hamptons to this day. Such are the Teflon transactions of the Obama years: nothing sticks.

There was such a Twitter storm over Blythe Masters that she withdrew from consideration for the committee before the day was out.

JP Morgan is one of the specially privileged “primary dealer” banks said to be systemically indispensible to world finance. Supposedly, if one of them is allowed to flop, the whole global matrix of global debt obligations — and, hence, global money — would dissolve in a misty cloud of broken promises. They are primary dealers to their shadow partner, the Federal Reserve, and their main job in that relationship is buying treasury bonds, bills, and notes from the US government and then “selling” them to the Fed (earning commissions on the sales, of course). The Fed, in turn, “lends” billions of dollars at zero interest back to the primary dealers who then park the “borrowed” money in accounts at the Fed at a higher interest rate. This is, of course, money for nothing, and even small interest rate differentials add up to tidy profits when the volumes on deposit are so massive.

This “carry trade” was started because the primary dealer banks were functionally insolvent after 2008 and needed to build “reserves” up to some level that would putatively render them sound. But that was a sketchy concept anyway since accounting standards had been officially abandoned in 2009 when the Financial Accounting Standards Board (FASB) declared that banks could report the stuff on their books at any value they felt like. In short, the soundness of the biggest banks in the USA could no longer be determined, period. They were beyond accounting as they were beyond the law. At the same time, the banks began the operations of shifting all the janky debt paper, mostly mortgages and derivative instruments (i.e. made-up shit like “CDOs squared”), value unknown, from their vaults to the a vaults of the Federal Reserve, where it resides to this day, rotting away like so much forgotten ground round in the sub-basement of an abandoned warehouse of a bankrupt burger chain.

All of these nearly incomprehensible shenanigans have been going on because debt all over the world can’t be repaid. The world’s economy, as constructed emergently over the decades, can’t function without repayable debt, which is the essence of “credit” — the fundamental trust implicit in banking. You have “credit” because other persons or parties believe in your ability to repay. After a while, this becomes a mere convention in millions of transactions. What’s happened is that the conventions remain in place but the trust is gone. It’s gone in particular among the parties deemed too big to fail.

Everybody knows this now and everybody is trying desperately to work around it, led by the Federal Reserve. Trust is gone and credit is going and debt is sitting between a rock and a hard place with its grubby hands pressed together, praying that it will be forgiven, forgotten, or overlooked a little while longer. By the way, the reason trust and credit are gone is because oil is no longer cheap and world economies can’t grow anymore. They can’t afford to run the day-to-day operations of a techno-industrial society. They can only pretend to afford it. The stock markets are mere scorecards for players who can only lie and cheat now to keep the game going. Somewhere beyond all the legerdemain and fraud, however, there remains a real world that is not going away. We just don’t know what it will look like when the smog of fraud clears.

http://kunstler.com/clusterfuck-nation/the-smog-of-fraud/

Prepare Now for When the New MyRA Becomes "TheirRA"

By PETER KRAUTH, Resource Specialist,

Money Morning

February 10, 2014

In his recent State of the Union Address, President Obama unveiled something new: a retirement savings account to "help" Americans build a nest egg, coining it the "MyRA."

Something immediately felt wrong about the proposal... but I couldn't put my finger on it.

So I researched the new MyRA and found details to help you understand just how it works.

But I also saw some potential dangers there that you need to prepare for now...

What MyRA Really Means

Like most government programs, getting to their essence can take some sifting. So I've distilled here what I think are the principal components of MyRA.

- Individuals earning up to $129,000 and couples earning up to $191,000 are eligible if their employers offer the account;

The minimum initial contribution is $25, then at least $5 through payroll deductions;

- The maximum contribution is $5,500 per year ($6,500 if over 50 years of age);

- Once the balance reaches $15,000 or has existed 30 years, it must be rolled into a Roth IRA;

- Total contributions to a person's IRAs cannot exceed $5,500 annually;

- Like a Roth IRA, withdrawals will grow and be redeemable tax-free;

- Principal can be redeemed any time, but earnings withdrawn before age 59 ½ are taxable and subject to 10% penalty; and

- Only one investment available: Treasury bonds paying variable interest-rate return

MyRA Is Set to Lose the Inflation Battle

Essentially, the MyRA is like a Roth IRA that your employer opens for you, allowing for low individual contribution requirements.

But if that's what you want, you can already set up your own Roth IRA with a no-fee, no-minimum account requirement at discount brokers like TD Ameritrade or E*Trade. And then your investment options are practically limitless.

In his speech, Obama said that "MyRA guarantees a decent return with no risk of losing what you put in." So let's look at the underlying investment a little more closely.

Your MyRA contributions would go into a variable interest rate bond investment, comparable to the Government Securities Fund in the Thrift Savings Plan (TSP) for federal employees.

That fund's recently been paying 2.5%, which admittedly is way better than the 1% you can get from the highest yielding savings accounts. And that looks OK, until you consider... inflation.

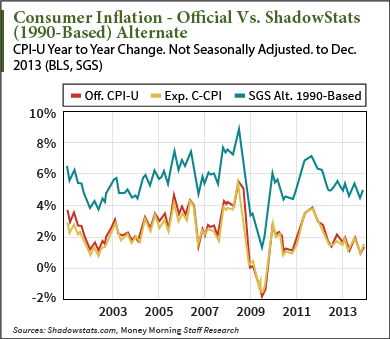

Consumer InflationRight now official U.S. inflation has been 1.5% through the 12 months ended December 2013. If instead we look at a truer inflation rate, like the more realistic one calculated by ShadowStats, the emerging picture is altogether different.

Shadowstats finds inflation running at 5%, rather than the more benign "official" 1.5%. At 5% inflation, MyRA investors will be losing 2.5% annually.

With interest rates near all-time historic lows, odds are rates will go higher, not lower. And as interest rates rise, the MyRA could find it increasingly challenging to offer an attractive return to investors.

You've Just Become the Government's New Lender

It's no secret that the United States is running out of buyers for its bonds.

China, the largest foreign owner, has been reducing its purchases and has repeatedly said it has enough. Nations worldwide engaged in their own quantitative easing are busy buying their own bonds. Now, the Fed itself has begun the tapering process.

As the U.S. debt and deficits continue to balloon, the government is desperate for a new source of funding. Obama's proposed MyRA looks to Americans to buy up its "junk bonds."

In fact, new demand for bonds is so badly needed, it's easy to see how the MyRA could eventually move from voluntary to mandatory.

Account holders would automatically contribute through payroll deductions, funding the government's IOUs. And those won't pay out for decades until retirement.

This sounds a lot like another government scheme from which Americans can't opt out: Social Security.

Eventually, the need to fund a mushrooming debt could lead to compulsory government bond buying in retirement accounts. At first, it might be 10% to 20% of all new contributions, then perhaps 10% to 20% of existing balances. With over $5 trillion in U.S. retirement accounts, it's easy to see how a mandate for 20% (or more) directed into Treasuries will help extend and pretend.

Consider that Japan's debt to GDP ratio is 140%, already way above the 100% level considered problematic. This is possible in large part because so much of the national debt is held by its own citizens rather than foreigners.

So it's not a huge stretch to imagine America heading down the same path.

Eventually, retirement accounts could even be at risk of partial or even outright confiscation as debt levels become increasingly unsustainable. A desperate government will look to take desperate actions.

If you think I'm exaggerating, consider what's happened elsewhere.

In just the last five years, there have been government confiscations of retirement assets in no fewer than six countries, including Argentina and Poland, as I alluded to in a November article.

In that piece, I said:

Back in January 2010, Bloomberg BusinessWeek reported, "The Obama administration is weighing how the government can encourage workers to turn their savings into guaranteed income streams following a collapse in retiree accounts when the stock market plunged."

Then in February this year, the Washington Times reported: "Consumer Financial Protection Bureau director Richard Cordray recently mentioned these [401(k)] accounts in a recent interview, stating 'That's one of the things we've been exploring and are interested in, in terms of whether and what authority we have.'"

As follow-up, I mentioned that the International Monetary Fund (IMF) was considering the potential of a "'capital levy' - a one-off tax on private wealth - as an exceptional measure to restore debt sustainability."

And if you think this could never happen in the good ol' U.S. of A., consider that back in 1933, President Roosevelt seized privately held gold by signing into law Executive Order 6102.

FDR's official motive was to "provide relief in the existing national emergency in banking, and for other purposes." Desperate times, desperate measures.

The Best Way to Keep Your Retirement Yours

What can you possibly do to protect yourself? Here's where thinking "outside the box" is vital.

The alternatives are simple, but they do require some effort and planning.

There are updates to some key points I've alluded to in the past: there are three basic things to do, and they apply equally to both good and bad times.

- Own and invest in hard assets like gold, silver, energy, and real estate. You can buy physical precious metals; you can buy physically backed ETFs; you can own quality resource equities, including your own home; and you can own income-producing properties and land. Assets in non-retirement accounts are more difficult to expropriate.

- Hold plenty of cash. Cash is king, despite the risks of inflation. Hold it as a bank balance, but watch FDIC deposit insurance limits, and consider diversifying into other currencies. Be sure, however, to hold some physical cash as well, as this could be crucial during a "bank holiday."

- Hold assets internationally. This is largely the same as in owning hard assets, as above, but in another country. Consider opening a foreign bank account. It's not easy for Americans - thanks to FATCA - but holding something outside your country of residence makes it tougher for a desperate government to grab.

Remember, as government debt grows to even more unmanageable levels, and interest rates cause most government income to service the debt, they will become increasingly desperate.

Sidestep the trap.

Don't let your MyRA become Uncle Sam's.

http://moneymorning.com/2014/02/10/prepare-now-new-myra-becomes-theirra/

Our Two Most Onerous Taxes: College Tuition and Healthcare Insurance

By Global Research News

Global Research, February 04, 2014

Max Keiser Report

by Charles Hugh Smith

It is not coincidence that these two unofficial taxes–healthcare and college tuition–are soaring in cost, outpacing all other household expenses.

I have long argued that to make an apples-to-apples comparison of real tax rates in the U.S. and other equivalently developed advanced democracies, we have to include two enormous expenses that are funded by the central state in countries such as Denmark and France: healthcare and college tuition/fees.

In The Real-World Middle Class Tax Rate: 75% (July 5, 2012), I estimated that healthcare insurance (if paid out of gross income, as we self-employed workers do) in the U.S. is roughly equivalent to a 15% tax.

Now that the Orwellian-named Affordable Care Act (ACA) is raising costs and deductibles, the true cost of healthcare (a.k.a. sickcare, because being chronically sick is so darned profitable for the cartels) is more like 20% in America.

Correspondent Tim L. (whose daughter is attending a prestigious STEM–science, technology, engineering, math–university) recently called $40-$50,000 per year college tuition what it really is: a tax:

College tuition is just another tax. If you can afford to pay it, you have to. If you cannot, you do not. Anytime you have to pay more for something because you can, you are paying a tax. Between traditional taxes, the college tuition tax, and the health insurance tax (also paid only by those who can afford to), I figure this year and the next three I’m in a 100+% tax bracket.

Middle-class Scandinavians famously pay around 65% to 75% of their gross incomes in taxes, but these taxes fund national healthcare for all and nearly free college tuition and fees. Add $200,000 (four years of tuition/fees at $50,000/year) in tax to the already-high U.S. real tax rate, and the real tax rate for middle-class households exceeds 100% of gross income.

Since only those with significant savings can possibly afford to pay a $200,000 tuition tax, the average-income household is left with one choice: the debt-serfdom of student loans. This is the acme of a morally bankrupt system of higher education: you need a college degree to have any hope of succeeding in America, but the only way to get that degree is to enter debt servitude, with no guarantees of future income needed to pay off the debt.

It is not coincidence that these two unofficial taxes–healthcare and college tuition–are soaring in cost, outpacing all other household expenses. The only other household item that is skyrocketing is debt:

The two unofficial taxes–paid by debt, either student loans, or Federal deficits– have no restraints: if you can’t pay, then the upper-middle class taxpayers who are paying most of the Federal tax will, one way or another:

Meanwhile, guess what’s been flat to down for the past 40 years–yup, the earned income of the bottom 90%:

With an unofficial tax rate for healthcare and college tuition that makes Scandinavian countries look like low-tax havens, no wonder the middle class in America is vanishing like mist in Death Valley. The political class is now bleating about the erosion of the middle class and rising wealth inequality. There are two primary sources of rising inequality in America: the Federal Reserve and the higher-education and healthcare cartels that so generously fund the campaigns of the bleating politicos.

Copyright Charles Hugh Smith, Max Keiser Report, 2014

http://www.maxkeiser.com/2014/02/our-two-most-onerous-taxes-college-tuition-and-healthcare-insurance/#e6C2w6vYbZ5CFeRA.99

Goldman Sachs Sued for Selling Libya Billions in “Worthless” Options

By Richard Smallteacher

Global Research, February 05, 2014

Goldman Sachs, the Wall Street investment bank, is being sued in London for selling Libya “worthless” derivatives trades in 2008 that the country’s financial managers did not understand. Libya says it lost approximately $1.2 billion on the deals, while Goldman made $350 million.

At the time, the Libyan Investment Authority (LIA), which invests profits from the country’s oil and gas exports, had assets worth $60 billion under former dictator Muammar Gaddafi.Goldman Sachs convinced LIA to buy long-term call options on six companies: Allianz, a German insurance and investment company; Banco Santander, a Spanish bank; Citbank, a U.S. bank; Électricité de France, a French state utility; ENI, an Italian oil company; and UniCredit, an Italian bank.

What the Libyans did not understand was that if the stocks in these six companies did not rise, their investments would become worthless. Instead the LIA executives weretaken in by a trip to Morocco as well as “small gifts, such as aftershaves and chocolates” and an offer of an internship for Mustafa Mohamed Zarti, the brother of the Libyan fund’s deputy executive director, in Dubai and London.

“The unique circumstances allowed Goldman Sachs to take advantage of the LIA’s extremely limited financial and legal experience to deliberately exploit its position of influence and to take advantage in a way that generated colossal losses for the LIA but substantial profits for Goldman Sachs,” said LIA Chairman AbdulMagid Breish in a statement.

For example, LIA paid $200 million to gamble on the value of 22.3 million Citigroupshares. At the time, these shares were worth $5.7 billion and so long as they rose in value by at least $200 million, LIA stood to get its money back and the full value of the shares. But since Citigroup’s shares did not rise by at least $200 million, LIA lost its wager.

The timing of the bets was particularly bad. Since the deals were struck in early 2008, just before the last financial crisis when most share prices tumbled, the Libyans lost their wagers.

“We think the claims are without merit, and will defend them,” Fiona Laffan, a Goldman Sachs spokeswoman in London, told Bloomberg news service.

However, the bank recently claimed that it had retrained its staff to ensure that customers are no longer blind sided by sales pitches[color=red][/color] for complex products. “For all of our employees, the experience of initiating, approving and executing a transaction for a client at Goldman Sachs is now fundamentally different,” Goldman claimed at its annual meeting last year.

Goldman Sachs is not the first Wall Street bank to be accused of taking advantage of naive foreign investors. Morgan Stanley was sued for selling bundled sub-prime mortgages to China Development Industrial Bank (CDIB) from Taiwan that they knew would fail. Even Standard & Poors (S&P), Wall Street’s top ratings agency, has been accused of helping banks to sell “collateralized debt obligations” that they knew were likely to go sour.

But this is not the first time that Goldman Sachs has been happy to help governments carry out dodgy deals. Back in 2001, Goldman reportedly charged Greece $300 million to engage on “‘blatant balance sheet cosmetics” to help the country join the European Monetary Union.

Photo (right) Andy Stern of SEIU International addresses protestors at a rally outside Goldman Sachs office. Credit: SEIU International. Used under Creative Commons license.

Members of the union were required to have government debt under 60 percent of gross domestic product and a budget deficit to gross domestic product ratio of under 3 percent. Unfortunately, Greece debt exceeded 100 percent and deficits were at 3.7 percent

Goldman Sachs took advantage of a loophole that allowed countries to enter the EMU if they could demonstrate that they were lowering their debt and their budget deficit. To do this, Goldman Sachs sold Greece a “cross-currency swap” that gave the government cash up front in return for a big payment at the end of the loan period. The beauty of the arrangement was that since such currency swaps were permitted by the European Statistical Agency (Eurostat), the debt and deficit appeared to shrink.

http://www.globalresearch.ca/goldman-sachs-sued-for-selling-libya-billions-in-worthless-options/5367509

Why is the Fed tapering?

January 30, 2014

Paul Craig Roberts and Dave Kranzler

(special thanks to the cork)

On January 17, 2014, we explained “The Hows and Whys of Gold Price Manipulation.” http://www.paulcraigroberts.org/2014/01/17/hows-whys-gold-price-manipulation/

In former times, the rise in the gold price was held down by central banks selling gold or leasing gold to bullion dealers who sold the gold. The supply added in this way to the market absorbed some of the demand, thus holding down the rise in the gold price.

As the supply of physical gold on hand diminished, increasingly recourse was taken to selling gold short in the paper futures market. We illustrated a recent episode in our article. Below we illustrate the uncovered short-selling that took the gold price down today (January 30, 2014).

When the Comex trading floor opened January 30 at 8:20AM NY time, the price of gold inexplicably plunged $17 over the next 30 minutes. The price plunge was triggered when sell orders flooded the Comex trading floor. Over the course of the previous 23 hours of trading, an average of 202 gold contracts per minute had traded. But starting at the 8:20AM Comex, there were four 1-minute windows of trading here’s what happened:

8:21AM: 1766 contracts sold

8:22AM: 5172 contracts sold

8:31AM: 3242 contracts sold

8:47AM: 3515 contracts sold

Over those four minutes of trading, an average of 3,424 contracts per minute traded, or 17 times the average per minute volume of the previous 23 hours, including yesterday’s Comex trading session.

The yellow arrow indicates when the Comex floor opened for gold futures trading. There was not any news events or related market events that would have triggered a sell-off like this in gold. If an entity holding many contracts wanted to sell down its position, it would accomplish this by slowly feeding its position to the market over the course of the entire trading day in order to avoid disturbing the price or “telegraphing” its intent to sell to the market.

Instead, today’s selling was designed to flood the Comex trading floor with a high volume of sell orders in rapid succession in order to drive the price of gold as low as possible before buyers stepped in.

The reason for this is two-fold: Driving down the price of gold assists the Fed in its efforts to support the dollar, and the Comex is running out of physical gold available to be delivered to those who decide to take delivery of gold instead of cash settlement.

The February gold contract is subject to delivery starting on January 31st. As of January 29th, 2 days before the delivery period starts, there were 2,223,000 ounces of gold futures open against 375,000 ounces of gold available to be delivered. The primary banks who trade Comex gold (JP Morgan, HSBC, Bank Nova Scotia) are the primary entities who are short those Comex contracts. Typically toward the end of a delivery month, these banks drive the price of gold lower for the purpose of coercing holders of the contracts to sell. This avoids the problem of having a shortage of gold available to deliver to the entities who decide to take delivery. With an enormous amount of physical gold moving from the western bank vaults to the large Asian buyers of gold, the Comex ultimately does not have enough gold to honor delivery obligations should the day arrive when a fifth or a fourth of the contracts are presented for delivery. Prior to a delivery period or due date on the contracts, manipulation is used to drive the Comex price of gold as low as possible in order to induce enough selling to avoid a possible default on gold delivery.

Following the taper announcement on January 29, the gold price rose $14 to $1270, and the Dow Jones Index dropped 100 points, closing down 74 points from its trading level at the time the tapering was announced. These reactions might have surprised the Fed, leading to the stock market support and gold price suppression on January 30.

Manipulation of the gold price is a foregone conclusion. The question is: why is the Fed tapering? The official reason is that the recovery is now strong enough not to need the stimulus. There are two problems with the official explanation. One is that the purpose of QE has always been to support the prices of the debt-related derivatives on the balance sheets of the banks too big to fail. The other is that the Fed has enough economists and statisticians to know that the recovery is a statistical artifact of deflating GDP with an understated measure of inflation. No other indicator–employment, labor force participation, real median family income, real retail sales, or new construction–indicates economic recovery. Moreover, if in fact the economy has been in recovery since June 2009, after 4.5 years of recovery it is time for a new recession.

One possible explanation for the tapering is that the Fed has created enough new dollars with which to purchase the worst part of the banks’ balance sheet problems and transfer them to the Fed’s balance sheet, while in other ways enhancing the banks’ profits. With the job done, the Fed can slowly back off.

The problem with this explanation is that the liquidity that the Fed has created found its way into the stock and bond markets and into emerging economies. Curtailing the flow of liquidity crashes the markets, bringing on a new financial crisis.

We offer two explanations for the tapering. One is technical, and one is strategic.

First the technical explanation. The Fed’s bond purchases and the banks’ interest rate swap derivatives have made a dent in the supply of Treasuries. With income tax payments starting to flow in, fewer Treasuries are being issued to put pressure on interest rates. This permits the Fed to make a show of doing the right thing and reduce bond purchases. As a weakening economy becomes apparent as the year progresses, calls for the Fed to support the economy will permit the Fed to broaden the array of instruments that it purchases.

A strategic explanation for tapering is that the growth of US debt and money creation is causing the world to turn a jaundiced eye toward the US dollar and toward its role as world reserve currency.

Currently the Russian Duma is discussing legislation that would eliminate the dollar’s use and presence in Russia. Other countries are moving away from the dollar. Recently the Nigerian central bank reduced its dollar reserves and increased its holdings of Chinese yuan. Zimbabwe, which was using the US dollar as its own currency, switched to Chinese yuan. The former chief economist of the World Bank recently called for terminating the use of the dollar as world reserve currency. He said that “the dominance of the greenback is the root cause of global financial and economic crises.” Moreover, the Federal Reserve is very much aware of the flight away from the dollar into gold, because it is this flight that causes the Fed to manipulate the gold price in order to hold it down and in order to be able to free up gold for delivery.

The Fed knows that the ability of the US to pay its bills in its own currency is the reason it can stand its large trade imbalance and is the basis for US power. If the dollar loses the reserve currency role, the US becomes just another country with balance of payments and currency problems and an inability to sell its bonds in order to finance its budget deficits.

In other words, perhaps the Fed understands that a dollar crisis is a bigger crisis than a bank crisis and that its bailout of the banks is undermining the dollar. The question is: will the Fed let the banks go in order to save the dollar?

Paul Craig Roberts is a former Assistant Secretary of the US Treasury for Economic Policy.

Dave Kranzler traded high yield bonds for Bankers Trust for a decade. As a co-founder and principal of Golden Returns Capital LLC, he manages the Precious Metals Opportunity Fund.

http://www.paulcraigroberts.org/2014/01/30/fed-tapering/

A New Audio Interview With Elston Johnston, Director and Chairman of the Board of Valdor Technology International Inc., is Now at SmallCapVoice.com

AUSTIN, Texas, Jan. 30, 2014 (GLOBE NEWSWIRE) — SmallCapVoice.com, Inc. (SCV) announced today that a new audio interview with Valdor Technology International Inc. (“Valdor”) (TSX:VTI-V) (OTC:VTIFF) is now available. The interview can be heard at http://smallcapvoice.com/blog/1-29-14-smallcapvoice-interview-with-valdor-technology-international-inc-vtiff

Elston Johnston, called into SmallCapVoice.com to provide the listening audience with a comprehensive overview of the Valdor history, the Company highlights for 2013, as well as his own candid insights into the fiber optics industry.

“We are excited about Valdor and we know that our shareholders and new investors want to learn about our plans for the future,” stated Johnston. “Audio presentations disseminated through the web are a powerful way to develop an audience for Valdor.”

About SmallCapVoice.com: SmallCapVoice is a full service corporate investor relations firm located in Texas, USA. They have clients throughout North America and are recognized for their ability to help emerging growth companies build a following with retail and institutional investors. SmallCapVoice uses its newsletter to feature daily stock picks, audio interviews and client news releases. They offer individual investors the tools needed to make informed decisions about the stocks in which they are interested. Tools like stock charts, stock alerts, and Company Information Sheets can assist with investing in stocks listed on the TSX Venture, OTC QB, OTC QX and OTC Pink. To learn more about SmallCapVoice and their services please visit: http://www.smallcapvoice.com/services.html.

About the Fiber Optics Industry: Fiber optics is the future of communications. The signal transmission business is in the early stages of a fiber optics bull market. All signal transmission, in their many and various forms, are being converted from electrical to fiber optics. A comprehensive global report on the fiber optic components market projects that it will reach US$42 billion by the year 2017.

About Valdor Technology International Inc. (www.valdortech.com): Valdor is a high technology fiber optic components company specializing in the design, manufacture, and sale of fiber optic connectors, laser pigtails, splitters, and other optical and optoelectronic components, including some that use the Valdor proprietary and patented Impact Mount(TM) technology. Valdor specializes in harsh environment products and in particular splitters and connectors. Valdor’s business plan incorporates growth by acquisition. For information on Valdor’s product lines please visit www.valdor.com.

Twitter: http://twitter.com/ValdorTechInt

Facebook: http://www.facebook.com/valdortech

For SmallCapVoice.com

Stuart T. Smith

512-267-2430

http://smallcapvoice.com/blog/a-new-audio-interview-with-elston-johnston-director-and-chairman-of-the-board-of-valdor-technology-international-inc-is-now-at-smallcapvoice-com/

Enough Is Enough: Fraud-ridden Banks Are Not L.A.’s Only Option

by Ellen Brown

Posted on January 29, 2014

(special thanks to basserdan)

“Epic in scale, unprecedented in world history.” That is how William K. Black, professor of law and economics and former bank fraud investigator, describes the frauds in which JPMorgan Chase (JPM) has now been implicated. They involve more than a dozen felonies, including bid-rigging on municipal bond debt; colluding to rig interest rates on hundreds of trillions of dollars in mortgages, derivatives and other contracts; exposing investors to excessive risk; failing to disclose known risks, including those in the Bernie Madoff scandal; and engaging in multiple forms of mortgage fraud.

So why, asks Chicago Alderwoman Leslie Hairston, are we still doing business with them? She plans to introduce a city council ordinance deleting JPM from the city’s list of designated municipal depositories. As quoted in the January 14th Chicago Sun-Times:

The bank has violated the city code by making admissions of dishonesty and deceit in the way they dealt with their investors in the mortgage securities and Bernie Madoff Ponzi scandals. . . . We use this code against city contractors and all the small companies, why wouldn’t we use this against one of the largest banks in the world?

A similar move has been recommended for the City of Los Angeles by L.A. City Councilman Gil Cedillo. But in a January 19th editorial titled “There’s No Profit in L A. Bashing JPMorgan Chase,” the L.A. Times editorial board warned against pulling the city’s money out of JPM and other mega-banks – even though the city attorney is suing them for allegedly causing an epidemic of foreclosures in minority neighborhoods.

“L.A. relies on these banks,” says The Times, “for long-term financing to build bridges and restore lakes, and for short-term financing to pay the bills.” The editorial noted that a similar proposal brought in the fall of 2011 by then-Councilman Richard Alarcon, backed by Occupy L.A., was abandoned because it would have resulted in termination fees and higher interest payments by the city.

It seems we must bow to our oppressors because we have no viable alternative – or do we? What if there is an alternative that would not only save the city money but would be a safer place to deposit its funds than in Wall Street banks?

The Tiny State That Broke Free

There is a place where they don’t bow. Where they don’t park their assets on Wall Street and play the mega-bank game, and haven’t for almost 100 years. Where they escaped the 2008 banking crisis and have no government debt, the lowest foreclosure rate in the country, the lowest default rate on credit card debt, and the lowest unemployment rate. They also have the only publicly-owned bank.

The place is North Dakota, and their state-owned Bank of North Dakota (BND) is a model for Los Angeles and other cities, counties, and states.

Like the BND, a public bank of the City of Los Angeles would not be a commercial bank and would not compete with commercial banks. In fact, it would partner with them – using its tax revenue deposits to create credit for lending programs through the magical everyday banking practice of leveraging capital.

The BND is a major money-maker for North Dakota, returning about $30 million annually in dividends to the treasury – not bad for a state with a population that is less than one-fifth that of the City of Los Angeles. Every year since the 2008 banking crisis, the BND has reported a return on investment of 17-26%.

Like the BND, a Bank of the City of Los Angeles would provide credit for city projects – to build bridges, restore lakes, and pay bills – and this credit would essentially be interest-free, since the city would own the bank and get the interest back. Eliminating interest has been shown to reduce the cost of public projects by 35% or more.

Awesome Possibilities

Consider what that could mean for Los Angeles. According to the current fiscal budget, the LAX Modernization project is budgeted at $4.11 billion. That’s the sticker price. But what will it cost when you add interest on revenue bonds and other funding sources? The San Francisco-Oakland Bay Bridge earthquake retrofit boondoggle was slated to cost about $6 billion. Interest and bank fees added another $6 billion. Funding through a public bank could have saved taxpayers $6 billion, or 50%.

If Los Angeles owned its own bank, it could also avoid costly “rainy day funds,” which are held by various agencies as surplus taxes. If the city had a low-cost credit line with its own bank, these funds could be released into the general fund, generating massive amounts of new revenue for the city.

The potential for the City and County of Los Angeles can be seen by examining their respective Comprehensive Annual Financial Reports (CAFRs). According to the latest CAFRs (2012), the City of Los Angeles has “cash, pooled and other investments” of $11 billion beyond what is in its pension fund (page 85), and the County of Los Angeles has $22 billion (page 66). To put these sums in perspective, the austerity crisis declared by the State of California in 2012 was the result of a declared state budget deficit of only $16 billion.

The L.A. CAFR funds are currently drawing only minimal interest. With some modest changes in regulations, they could be returned to the general fund for use in the city’s budget, or deposited or invested in the city’s own bank, to be leveraged into credit for local purposes.

Minimizing Risk

Beyond being a money-maker, a city-owned bank can minimize the risks of interest rate manipulation, excessive fees, and dishonest dealings.

Another risk that must now be added to the list is that of confiscation in the event of a “bail in.” Public funds are secured with collateral, but they take a back seat in bankruptcy to the “super priority” of Wall Street’s own derivative claims. A major derivatives fiasco of the sort seen in 2008 could wipe out even a mega-bank’s available collateral, leaving the city with empty coffers.

The city itself could be propelled into bankruptcy by speculative derivatives dealings with Wall Street banks. The dire results can be seen in Detroit, where the emergency manager, operating on behalf of the city’s creditors, put it into bankruptcy to force payment on its debts. First in line were UBS and Bank of America, claiming speculative winnings on their interest-rate swaps, which the emergency manager paid immediately before filing for bankruptcy. Critics say the swaps were improperly entered into and were what propelled the city into bankruptcy. Their propriety is now being investigated by the bankruptcy judge.

Not Too Big to Abandon

Mega-banks might be too big to fail. According to U.S. Attorney General Eric Holder, they might even be too big to prosecute. But they are not too big to abandon as depositories for government funds.

There may indeed be no profit in bashing JPMorgan Chase, but there would be profit in pulling deposits out and putting them in Los Angeles’ own public bank. Other major cities currently exploring that possibility include San Franciscoand Philadelphia.

If North Dakota can bypass Wall Street with its own bank and declare its financial independence, so can the City of Los Angeles. And so can the County. And so can the State of California.

____________

Ellen Brown is an attorney, chairman of the Public Banking Institute, and author of 12 books including The Public Bank Solution. She is currently running for California state treasurer on the Green Party ticket.

http://ellenbrown.com/2014/01/29/enough-is-enough-banksters-are-not-l-a-s-only-option/

Nigel Farage - Horrifying New “Orwellian” Control Of Citizens

Jan. 29, 2014

Today MEP Nigel Farage broke the news first to King World News that horrifying new “Orwellian” technology is in the process of being put in place in Europe to further tighten government’s grip and control its citizens. He also discussed a rebellion that is taking place in Europe that has the powers that be deeply troubled. Below is what Farage had to say in this breaking news story.

Farage: “Between May 22nd and May 25th, all 28 member states of the European Union will be returning members back to the European Parliament, and there is no doubt that there is quite a strong mood of rebellion in the air. The authorities are very, very scared that they may have a European Parliament that is very difficult to control....

“We’ve got (Euro-sceptic) parties in France, the United Kingdom, Finland, and the Netherlands that are really performing strongly. In fact, the commentators are now tipping euro-skeptic parties to win in Britain, to win in France, and to win in the Netherlands. This is very, very significant political rebellion that will dominate politics for the next three months.”

Eric King: “Nigel, you’ve been leading this rebellion in Europe and it seems to be gaining tremendous headway. How shocked are the powers that be as they watch this rebellion begin to grow?”

Farage: “They’re scared and they are calling on every favor they can from big business and from the one or two big banks whose role in this has not been very pretty. One particularly thinks of how Goldman Sachs almost owns the governments in much of the Mediterranean area. So they are fighting back.

And similarly with the conventional media, by which I mean the established newspapers now launching pretty relentless attacks on those that question the current setup and structure in Europe. So the battle is getting pretty dirty and pretty nasty. So it’s going to be time to put the tin helmets on (laughter ensues) because it’s going to get a bit rough.