News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

markanthony

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

http://www.finanznachrichten.de/nachrichten-2014-02/29408285-pressetext-de-s-t-ag-eroeffnet-cloud-kompetenzzentrum-in-der-adria-region-s-t-kroatien-richtet-hp-cloud-center-of-excellence-ein-015.htm

Linz (pts011/13.02.2014/11: 20) - The Croatian subsidiary of S & T AG in collaboration with Hewlett Packard opes a cloud center of excellence. S & T Croatia offers with the certified HP Cloud Center of Excellence (PESO) the possibility of a wide range of "out-of-the-box" solutions from to show the cloud environment in use. The company was due to the extensive expertise in the design, implementation, operation and maintenance of Cloud computing systems as the first partner in the Adriatic region a

Certification as "Gold HP Cloud Builder Specialist".

The CCoE of equipment includes servers, storage and networking products which, together with a wide variety of services and software products, in work together seamlessly and the cloud companies help the user to be able to accelerate business processes more flexible or cost reduce by expensive investments in equipment operational through ongoing Expenses are compensated.

Products and services in the cloud area are available for several years the very successful business and development priorities of S & T AG, the settled since 2010 including collaborating partner in Hagenberg Software Park Christian Doppler Laboratory, a scientific institution in the field "Client Centric Cloud computing" is.

With approximately 1,500 employees and offices in 19 Central and

Eastern European countries is one which is listed on the Frankfurt Stock Exchange (ISIN AT0000A0E9W5, WKN A0X9EJ, SANT) of the three largest IT solution providers and system houses in Eastern Europe and was in the last fiscal year, about 340

EUR million revenues. Due to the continuous expansion of business with Proprietary technologies for vertical markets in the current year is primarily a disproportionate earnings growth planned.

Released by: S & T AG

Contact: Valentin Trummer

Tel: +43 732 7664 0

E-mail: valentin.trummer @ snt.at

Website: www.snt.at

Source: http://www.pressetext.com/news/20140213011

© presse news agency http://www.pressetext.com - The

textual responsibility for editorial messages (pte) is

press text, press releases (pts) with the respective emitters. More

Information, please visit at our editorial team

info@pressetext.com or Phone +43-1-81140-300. (END) Dow Jones NewswiresFebruary 13, 2014 05:20 ET (10:20 GMT)

February 20, 2014

"The Letter of Intent provides them exclusivity until 20 February 2014. If Cloudeeva comes to the conclusion that they wish to make a takeover bid for S & T, the Company would inform us by that date formally about it."

http://boersengefluester.de/interview-st-wahrscheinlichkeit-bei-50-bis-70-prozent/

Maybe Adesh Tyagi is waxing his carrot in anticipation of the big news...

Super Stock!!! Great Buy!!!

Were all going to buy islands....soon.

New directors to join HEMP soon.

Just heard a tip? HEMP @$1000 by next month!!!

HEMP to his $1000/share by next month!

Oh yeah! He couldn't afford himself a decent suit for the interview.

Oh sorry, I forgot to mention, he said that his t-shirt was made of hemp.

I PLAN TO TURN MY LIFE AROUND TOO...and start a OTC company.

Probably a new company will be set up by someone more experienced in the Marijuana trade than Bruce Perlowin.

Maybe everyone should save up to buy shares here

HEMP is fool's gold.

A company started by a Ex-Con and Drug Runner....??

Wow!!

The price should dip to $0.09 - $0.10 today

$0.50 by Friday? I would have to be smoking a bong to buy that...I see $0.09 - $0.10 today

Need to get out...

HEMP could go down to $0.10 today

From your lips to God's ears....

SYAI acquisition of S&T is more like this.....

Definitive Documents/Agreement

Looks like the definitive documents should be done by 2/19 or 2/20, 2014. That's next week.

The definitive agreement is a more solid document than the letter of intent.

https://www.inkling.com/read/applied-mergers-and-acquisitions-robert-bruner-1st/chapter-29/definitive-agreement

ok, there. Did a number on the 5's. Your call next.

I feel the dividend by S&T AT was deliberately announced following the takeover negotiations by Cloudeeva, Inc in order to make it more attractive. S & T AT(formerly Quanmax) has been looking for an investor to take them over for some time. It looks like Grosso Holding GmbH and Hannes Niederhauser (CEO) have already sold a significant portion of their stockholding. Possibly, bought up by Cloudeeva either from the open market or through investment banks in the EU. S&T AT is part of the larger S&T Group, which acquired Quanmax.

More than getting into the EU markets, Cloudeeva is probably looking to acquire the 1500 skilled software professionals who are currently employees of S&T AT. From the multitude of job postings every day by Cloudeeva, it seems like it has more software consulting job orders than it can meet through recruiting in the US and India. Following the take over of S&T AT; the S&T AT employees can expect to be placed on revenue earning consulting projects at client sites in the US. Seeing H1B cap hurdles, Cloudeeva possibly plans to use the L1 visa route to transfer these highly skilled software professionals to the US. It seems like S&T is eagerly looking forward to its takeover by Cloudeeva. Possible reason being that Quanmax grew to €100 million with 150 employees. After being acquired by S&T the number of employees grew to 1500 but revenues grew to just €350 million. So S&T AT is saddled with a huge payroll resulting in thin margins given the current economic situation in the EU.

On an average, revenue of any software company in the US with around 300 consultants on sites is about $50 million. Currently, the software consulting business in the US is booming and exceeds the days of Y2K many fold. Assuming Cloudeeva manages to place all 1500 at US client sites would be adding about $250 million to its existing revenues. Currently Cloudeeva has about 900 consultants in the US, which possible gives them about $150 million in revenues. Thus the combined group would bring in revenues to upwards of about $400 million.

It seems like Cloudeeva, Inc., is following the footsteps of the Cognizant success story.

A win-win for Cloudeeva.

SYAI (Cloudeeva, Inc) News

Feb 19 or 20, 2014 is the date then..

Great news!!

Cloudeeva plans to delist the S & T stock in the medium term after the takeover and wants to re-introduce it on Nasdaq as Cloudeeva.

http://boersengefluester.de/interview-st-wahrscheinlichkeit-bei-50-bis-70-prozent/

At $0.06 this stock is still very cheap.

A company without a freaking Website to its name?

http://www.newamericaenergycorp.com/

Everytime I look at the following page, I can't stop laughing. Its freaking hillarious........they look like specimens from a lab!

http://www.cloudeeva.com/about-cloudeeva/management-team

When filing for current hits everyone will be chasing.....

When are the final filings going to hit? This has been the case for the past 12 months....

The supposed CFO Mark Vitcov is not even a full-time employee.

Maybe Adesh Tyagi should spend more time putting together the financials rather than spruce up his personal Facebook pages with "selfies."

Financial Times - Analysts' forecast - BUY 02/01/2014

http://markets.ft.com/research/Markets/Tearsheets/Forecasts?s=SANT:FRA

S&T Revised analysts' consensus - BUY

www.4-traders.com/ST-AG-5465591/consensus/

Reuters update Feb 04, 2014 - BUY

S&T "Buy" rating.

http://www.reuters.com/finance/stocks/analyst?symbol=SANT1.DE

Merger/Acquisition

What's life without a little fun?

I like being pragmatic rather than stupid.

Analyst opinion as of Feb 01, 2014.

http://markets.ft.com/research/Markets/Tearsheets/Forecasts?s=SANT:FRA

Analyst opinion as of Feb 01, 2014.

http://markets.ft.com/research/Markets/Tearsheets/Forecasts?s=SANT:FRA

Looks like the MA with S&T is a done deal...at least that's what the German analysts say.

22hrs ago.

http://www.aktiencheck.de/exklusiv/Artikel-Bechtle_Aktie_Struktureller_Gewinner_Bankhaus_Lampe_raet_weiterhin_zum_Kauf_Aktienanalyse-5499654

Bechtle share: Structural winner! Bankhaus Lampe advises continue to buy - stock analysis

03:02:14 15:11

aktiencheck.de

Neckarsulm (www.aktiencheck.de) - Wolfgang Specht, an equity analyst of Bankhaus Lampe advises the Bechtle share (ISIN: DE0005158703, WKN: 515870, ticker symbol: BC8) continue to buy shares in a recent analysis.

The analyst did (+11%, +25% EBT sales) and an improved outlook for the industry significantly increased its revenue and earnings estimates for a strong Q4.

Bechtle was based on a recently improved outlook for the IT market and significant rise in orders (Q3 +15.9%) continues to grow faster than the relevant sub-markets (+5.9% vs. BHL 2014e. Relevant market +2.0%) and sustainably benefit from a rising concern about high-performance IT infrastructures. The increasing complexity of IT solutions speak for the increasing use of system houses that multi-local presence would connect with a wide range of services in the solution business. Bechtle should grow in this process at the expense of smaller computer retailers.

Even a planned withdrawal of T-Systems from various business areas could have a positive impact. A comfortable liquidity position (BHLe FY 2013e: 71 million euros) should allow next bolt-on acquisitions and an attractive dividend. The analyst expects an increase of 1.00 euros in 2013 to EUR 1.20 for FY 2014 and 1.30 euros for 2015.

Acquisitions would remain an integral part of the business model. In addition to an expansion of our regional presence, solution expertise and access to new customers should thereby facing shortage of skilled workers in the IT industry increasingly attracting staff play a role. The analyst expects 2014/15 the expansion of retail business to one or two new country markets. Growth in cloud computing solutions and mobile devices / services in the long term should more than compensate for a possible decrease in the trading business.

With submission of full-year figures 2013 on 18 March should announce its outlook for 2014 Bechtle. The analyst expects with the aim to increase sales by 5 to 7% (BHLe +5.9%) and an EBT margin of at least 4% (BHLe: 4.3%) to achieve. The recent M & A activity in the industry (Cancom / Pironet, Cloudeeva / S & T) could Bechtle build a takeover premium.

At the level of the target price would share for 2014 (2015) 9.8 x (8.6 x) EBITDA, (15.5 x) rated x 23.1 (19.1 x) FCF and a PER of 17.5 x. The analyst estimate EBITDA CAGR 2012-15 on solid compared to the industry 10.3%.

The equity analyst from Bankhaus Lampe, Wolfgang Specht, confirms its buy rating for the Bechtle share. The target price has been raised from 53.00 to 63.00 euros.

Exchanges Bechtle share:

Xetra share price Bechtle share:

54,70 EUR -0.02% (03/02/2014, 14:55)

Tradegate's share price Bechtle share:

54.672 EUR -0.20% (03/02/2014, 15:12)

ISIN Bechtle share:

DE0005158703

WKN Bechtle share:

515870

Ticker symbol Bechtle share:

BC8

Short Profile Bechtle AG:

Bechtle AG (ISIN: DE0005158703, WKN: 515870, ticker symbol: BC8) is active with her 65 system houses in Germany, Austria and Switzerland, and one of Europe's leading IT e-commerce providers. With this combination, the company is headquartered in Neckarsulm on a strategy that combines system house services to the direct marketing of commercial IT products. Since its founding in 1983, Bechtle is constantly to expand and 2012 has achieved a turnover of around 2.1 billion euros. Its more than 75,000 customers in various industrial and service sectors, as well as the public sector, the company offers vendor-independent a complete range of products for the IT infrastructure from one source. (03.02.2014/ac/a/t)

Disclosure of potential conflicts of interest:

Possible conflicts of interest can be viewed on the site of the creator / source of the analysis.

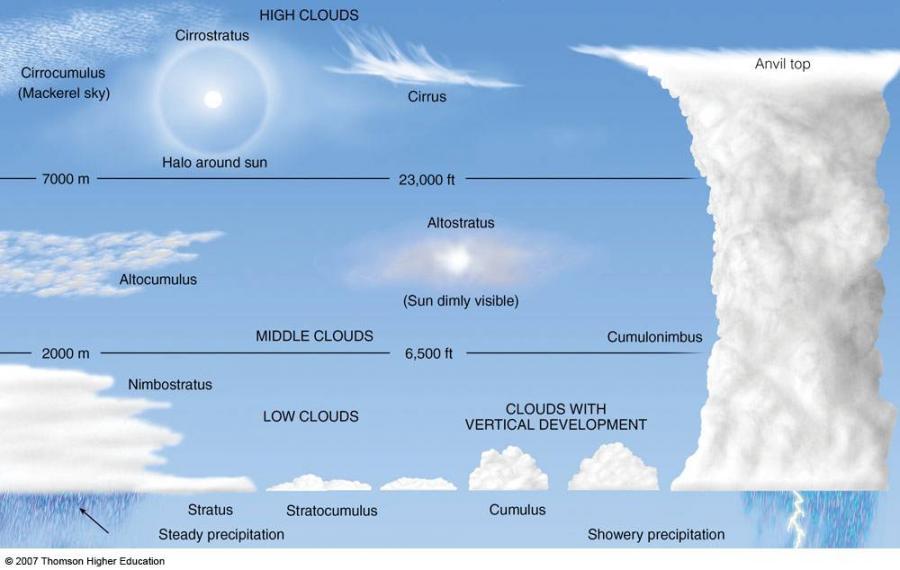

Cloudeeva (SYAI) is more like a Cirrocumulus cloud (mackerel sky)

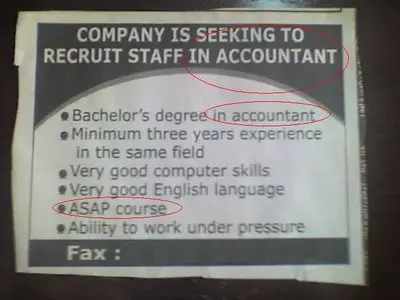

SYAI latest job skills

Accountants required to complete long overdue financial audits since 2012!

I guess I was wrong by a few zeros. I think SYAI to hit $1000 per share. Big hits coming, $1.5 billion dollar company after the S&T take over, Now I could stand up here and say, let’s get everybody together, let’s get unified because the sky will open, the light will come down, celestial choirs will be singing!!

Go SYAI, SYAI...

But first let me check if they found their financials in the pile of papers.