News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Jimmy Quick

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Have you even read that blurb he posted, it's absolutely nothing of substance. Some guy dissatisfied with his investment choices. The one who posted the link, posted it for the very same reason. Can't live with the sell at $.019. And once again it does not pertain to RXMD and it's business.

You talk big about destroying shareholder value, but when I first invested here it was $.005. Since it has ran to $.26 and $.20 and still sits at $.05+ When I first invested they were at $10 million revenues annually and now they are at over $40 million revenues and still expanding.

The only one's who saw true destruction in shareholder value were those that sold at $.019 and had very little faith in the long-term value of the company.

I am saying it is irrelevant to RXMD and their business.

$APRE Can this get back to $30 levels off of yesterdays news of Trial Success for drug on treatment of Luekemia? This won't be immediate, but maybe 2nd half of 2021.

Aprea Therapeutics Announces Phase 1/2 Trial of Eprenetapopt + Venetoclax + Azacitidine in TP53 Mutant AML Meets Complete Rem...

June 16 2021 - 08:00AM

GlobeNewswire Inc.

Aprea Therapeutics, Inc. (Nasdaq: APRE), a biopharmaceutical company focused on developing and commercializing novel cancer therapeutics that reactivate mutant tumor suppressor protein, p53, today announced that the Phase 1/2 trial evaluating the frontline treatment of eprenetapopt with venetoclax and azacitidine in patients with TP53 mutant AML has met the pre-specified primary efficacy endpoint of complete remission (CR) rate.

In 30 patients who were evaluable for efficacy at the time of the analysis, the CR rate was 37% and the composite response rate of CR plus CR with incomplete hematologic recovery (CRi), CR/CRi, was 53%. The trial met the primary efficacy endpoint of CR, which is based on a Simon 2-stage design. As of the data cut, 11 patients remain on study treatment and continue to be followed for safety and efficacy. The Company plans to discuss the dataset with the U.S. Food and Drug Agency (FDA) in the second half of 2021 and expects to present data from the trial at a future scientific or medical conference.

“We are pleased with these results from the combination of eprenetapopt with venetoclax and azacitidine in this very difficult-to-treat TP53 mutant AML population, a patient group with significant unmet medical need,” said Eyal Attar, M.D., Chief Medical Officer of Aprea Therapeutics. “These data, which follow the recent granting of Fast Track and Orphan Drug designations by FDA, provide further demonstration of the potential for eprenetapopt in the treatment of myeloid malignancies. We continue to make excellent progress across our myeloid malignancies program and look forward to providing an update in July 2021 on our Phase 2 trial evaluating eprenetapopt with azacitidine as maintenance therapy in TP53 mutant MDS and AML patients who have received allogeneic stem cell transplant.”

About Aprea Therapeutics, Inc.

Aprea Therapeutics, Inc. is a biopharmaceutical company headquartered in Boston, Massachusetts with research facilities in Stockholm, Sweden, focused on developing and commercializing novel cancer therapeutics that reactivate mutant tumor suppressor protein, p53. The Company’s lead product candidate is eprenetapopt (APR-246), a small molecule in clinical development for hematologic malignancies and solid tumors. Eprenetapopt has received Breakthrough Therapy, Orphan Drug and Fast Track designations from the FDA for myelodysplastic syndromes (MDS), Orphan Drug and Fast Track designations from the FDA for acute myeloid leukemia (AML), and Orphan Drug designation from the European Commission for MDS and AML. APR-548, a next generation small molecule reactivator of mutant p53, is being developed for oral administration. For more information, please visit the company website at www.aprea.com.

The Company may use, and intends to use, its investor relations website at https://ir.aprea.com/ as a means of disclosing material nonpublic information and for complying with its disclosure obligations under Regulation FD.

About p53, eprenetapopt and APR-548

The p53 tumor suppressor gene is the most frequently mutated gene in human cancer, occurring in approximately 50% of all human tumors. These mutations are often associated with resistance to anti-cancer drugs and poor overall survival, representing a major unmet medical need in the treatment of cancer.

Eprenetapopt (APR-246) is a small molecule that has demonstrated reactivation of mutant and inactivated p53 protein – by restoring wild-type p53 conformation and function – thereby inducing programmed cell death in human cancer cells. Pre-clinical anti-tumor activity has been observed with eprenetapopt in a wide variety of solid and hematological cancers, including MDS, AML, and ovarian cancer, among others. Additionally, strong synergy has been seen with both traditional anti-cancer agents, such as chemotherapy, as well as newer mechanism-based anti-cancer drugs and immuno-oncology checkpoint inhibitors. In addition to pre-clinical testing, a Phase 1/2 clinical program with eprenetapopt has been completed, demonstrating a favorable safety profile and both biological and confirmed clinical responses in hematological malignancies and solid tumors with mutations in the TP53 gene.

A pivotal Phase 3 clinical trial of eprenetapopt and azacitidine for frontline treatment of TP53 mutant MDS has been completed and failed to meet the primary statistical endpoint of complete remission. Additional clinical trials in hematologic malignancies and solid tumors are ongoing. Eprenetapopt has received Breakthrough Therapy, Orphan Drug and Fast Track designations from the FDA for MDS, Orphan Drug and Fast Track designations from the FDA for AML, and Orphan Drug designation from the European Medicines Agency for MDS and AML.

APR-548 is a next-generation small molecule p53 reactivator. APR-548 has demonstrated high oral bioavailability, enhanced potency relative to eprenetapopt in TP53 mutant cancer cell lines and has demonstrated in vivo tumor growth inhibition following oral dosing of tumor-bearing mice.

About AML

AML is the most common form of adult leukemia, with the highest incidence in patients aged 60 years and older. AML is characterized by proliferation of abnormal immature white blood cells that impairs production of normal blood cells. AML can develop de novo or may arise secondary to progression of other hematologic disorders or from chemotherapy or radiation treatment for a different, prior malignancy; secondary AML carries a worse prognosis than de novo AML. Mutations in TP53, which are associated with poor overall prognosis, occur in approximately 20% of patients with newly diagnosed AML, more than 30% of patients with therapy-related AML and approximately 70-80% of patients with complex karyotype.

Totally agree, I have been loading up at these prices. This was a $30 stock pre-failure of the last trial back in December 20. With yesterday's news of trial success for a different disease, I think we could move back to those levels in 2nd half of 2021.

Some 3 years ago an RXMD shareholder sold all his 2 million shares at $.019, before the quick rise to $.26. Is this still relevant today, it appears so? LOL

Doesn't relate to RXMD at all. Next

Notes Payable - Actually Doing Really Good

I acquired a significant number of shares today.

Totally Agree. No one disagrees, all shareholders have said we need to get away from using them and any company like them. It's funny though, because when I go to look at whether we have done any deals with them recently, I have to go all the way back to March 6, 2019. And when the company had the opportunity to reduce the debt, they did so.

Entry Into Material Definitive Agreement: Iliad Research and Trading

Entry into a Material Definitive Agreement | 03/12/2019

March 12, 2019

This release includes additional documents. Select the link(s) below to view.

Material Agreement Progressive Care - Iliad Research and Trading.pdf

01_Securities_Purchase_Agreement_-_RXMD3_(3.6.19).docx.pdf

Exhibit_A_-_Note_-_RMXD3_(3.6.19).docx.pdf

Exhibit_D_-_Investor_Note_-_RXMD_(3.6.19).docx.pdf

Exhibit_E_-_Security_Agreement_-_RXMD3_(3.6.19).docx.pdf

The Company, released from escrow $1,000,000 on June 1, 2019, leaving a remainder of $900,000 to be released from escrow prior to November 15, 2019. The remaining $400,000 held in escrow is to be returned to Iliad Research and Trading, reducing the balance on the note without pre-payment penalty.

A listing of Ongoing Business Operations - Or Are These Expansion Initiatives????

On November 8, 2019, the Company entered into that certain Amendment to Stock Purchase Agreement (the “Stock Purchase Agreement”) with five investors (each individually a “Seller” and collectively the “Sellers”), pursuant to which the Company, has agreed to amend the terms which includes an adjusted purchase price of $1,900,000 (the “Purchase Price”), for 100% of the issued and outstanding shares of common stock of Family Physicians Rx, Inc., a Florida corporation d/b/a Five Star, RX (“Family Physicians”). The closing of the Amendment to the Stock Purchase Agreement shall occur on or before November 15, 2019. Under the Amended terms, the adjusted Purchase Price shall be paid to Sellers immediately upon closing. The Company, released from escrow $1,000,000 on June 1, 2019, leaving a remainder of $900,000 to be released from escrow prior to November 15, 2019. The remaining $400,000 held in escrow is to be returned to Iliad Research and Trading, reducing the balance on the note without pre-payment penalty.

A significant aspect of our business plan is the development and launching of new and innovative technology solutions to deliver personalized patient-centered care. We completed a significant component of that plan through the launch of our ClearMetrX subsidiary, the Company’s first wholly-owned data management company with services designed to support health care organizations across the country. We believe in the power of Artificial Intelligence (AI) to improve preventive healthcare by helping physicians make informed decisions in the medication therapy management process. Through ClearMetrX, the Company has increased its third-party administrative and data management fees to over $700,000 in 2020. These fees have gross margins significantly greater than those generated from our pharmacy operations. The new subsidiary focuses on providing insights, data security, and technological development. The Company has transitioned data service customers from the pharmacies to the ClearMetrX platform to better scale the products and improve the capabilities of existing analytics options.

The core products of ClearMetrX include data management and Third Party Administration (TPA) services for 340B covered entities, Pharmacy Analytics, and programs to manage HEDIS Quality Measures such as Medication Adherence. These offerings cater to the glaring need of frontline providers to understand best practices, patient behaviors, care management processes, and the financial mechanisms behind these decisions. The Company aims not just to provide data access, but also actionable insights that providers and support organizations can use to improve their practice and patient care.

Another important aspect of our business plan was the development and provision of health IT, HIPAA-compliant software development, HL7 integrations, and virtual healthcare services on a business-to-business (B2B) basis, delivering these services directly to consumers and through channel partners. We planned to do this through a series of major acquisitions, beginning with the entry into a letter of intent with MyApps Corp., a leading developer of healthcare software. Although the parties ultimately determined not to complete the acquisition, we engaged MyApps Corp. to accelerate development of software platforms for ClearMetrX.

In September 2020, we further enhanced our industry-leading contactless delivery service by entering into a new partnership with DeliverSTAT, a provider of an all-in-one pharmacy delivery logistics solution. The new platform will allow PharmcoRx to compete and possibly partner in the future with pharmacy delivery apps such as Capsule, PillPack, NimbleRx and UberHealth in terms of functionality and technology. The platform connects directly with the pharmacy to help manage the prescription delivery process from end to end, reducing overhead, simplifying operations, and improving both patient and physician satisfaction.

During the third quarter 2020, the Company launched an aggressive expansion of its COVID-19 testing service registered through the FDA under its Emergency Use Authorization (“EUA”) guidelines, featuring Polymerase Chain Reaction (“PCR”) and Antigen testing systems that produces rapid detection of the SARS-CoV-2 virus with market-leading accuracy in 15 to 45 minutes. The systems we use for Rapid Detection of the SARS-CoV-2 virus is a molecular test using a lab technique called PCR, an antigen-based testing system designed to detect proteins from the virus that causes COVID-19. The Company provides these new testing systems to patients at its North Miami Beach location and provides Antigen testing at Palm Springs and Orlando pharmacies. To date, the Company has successfully tested over 5,000 patients and built a reputation as a preferred provider for in-patient and out-patient COVID-19 Rapid Testing solution.

By the end of the third quarter 2020, new contractual relationships with not-for-profit clinics and health care institutions began to come online and drive revenue growth. The collection of the buying power of all of our locations (North Miami Beach, Davie, Palm Springs, and Orlando) allowed us to negotiate more favorable discounts and purchasing terms.

You may recall that just over a year ago, we closed 2019 on a positive note, when our administrative division moved to our flagship building in Hallandale Beach, Florida. Our plan at that time was to convert this facility into a modern state of the art fulfillment facility and operational center. In June 2020, we began the work of consolidating our North Miami Beach and Davie locations into a single large-scale pharmacy operation. We entered into a construction contract with a local contractor and construction activities began in the summer. In December 2020, the Company completed its move into its new 11,000 sq ft pharmacy space in Hallandale Beach, Florida and completed the move to its new 3,700 sq ft Orlando location in January 2021. Our expanded facility in Orlando should drive important performance gains, advances in productivity, volume, and market reach due to the expanded space and anticipated efficiency.

To sum up the year 2020, in response to the challenges posed by the COVID-19 pandemic, the subsequent lockdown in Florida and the severe negative effects on the Florida economy, the Company was nevertheless able to respond with flexibility and strong execution, capitalizing on Progressive Care’s built-in competitive advantages, including its established delivery infrastructure, to drive a seamless transition into a pandemic-ready operational strategy.

The Company’s strong results owe in part to its ability to shift in stride to a model centered on contactless prescription delivery, a range of digital solutions, and an overall experience for providers and customers that met the needs of its surrounding communities during an uncertain and unpredictable period. We experienced record quarterly revenue results. We filled more than 530,000 prescriptions in 2020, the highest in Company history. We had over $40.6 million in sales, the highest in Company history. The Company recorded over $600 thousand in revenues related to rapid results COVID-19 testing in the last six months of 2020, providing testing to over 5,000 patients. 340B revenue was $2.8 million, representing year-over-year growth of 323% compared to the year ended December 31, 2019.

All of these results continued our trend of year-over-year growth for the last 5 years. Our cash flow dramatically improved, as did our profitability, reputation, and ability to execute on new levels. We began to execute on our long-term business plan of expanding our footprint in the healthcare data management market by expanding our 340B Third Party Administration (TPA) service.

Outlook

Looking forward to 2021 and beyond, we look to continue progress on expansion of our ClearMetrX 340B TPA services, as well as our other data analytics platforms. At the end of the first quarter of 2021, we expect the ClearMetrX digital platform will be fully operational, which will allow us to expand our third-party administration services to 340B covered entities nationwide. The Company expects that growth in this revenue component will continue at a level at or above the record growth experienced in fiscal year 2020.

In February 2021, we entered into a service agreement with EagleForce Health, LLC to integrate its proprietary telehealth platform, called “myVax”, and develop a platform for the Company’s Digital Passport for COVID-19 Testing and Vaccination Results. We expect that this platform will be operational in the second quarter of 2021, and that it will include complete patient scheduling, telehealth, and tele-pharmacy platform services. The platform will manage an individual’s COVID-19 Vaccine and Test Journey documenting all transitions, including healthcare appointments, billing, and telehealth services. This will also include a Digital Passport or Digital Wallet that is QR-coded for registration, verification, and documentation of COVID-19 vaccination and/or test results.

This is expected to provide a powerful tool for various processes that the Company believes will come to depend upon accurate real-time virus spread risk abatement, including merchants such as cruise lines, airlines, sports venues, high-population-density, manufacturing, packing, or shipping facilities, and institutions such as school districts, universities, court proceedings, public transportation systems, and other service providers.

Upon completion of our 2020 audit, we intend to carry on with the process of uplisting to a national exchange, which will provide us with access to a much larger, more diverse pool of prospective investors, including a much wider institutional investor audience.

Management has the following 2021 Strategic Goals:

• Strive to achieve over $50 million in sales.

• Expansion of COVID-19 testing and vaccination programs.

• Completion of telehealth integration with the roll out of the Eagle Force Digital Passport program.

• Nationwide launch of ClearMetrX 340B TPA services.

• Secure additional not-for-profit healthcare contracts and long-term care facility relationships.

• Achieve full enterprise profitability and earnings growth.

• Become SEC-registered and fully reporting.

• Complete an uplist to a national exchange.

I think the ones that made bank are the ones that held past $.019 with their millions of shares. What do you think about that?

That's me and many others here. WooHoo!

Except Management hasn't sold any of their shares. So that doesn't jive at all. Thanks for playing though.

Wow that is some deep stuff there. So definitive in how the loan proceeds are being utilized. Total sarcasm of course.

Pharmacy Hot Info

Hot topics from April

HRSA 340B update

This week brought another significant milestone to the 340B program. The program's governing body, Health Resources and Services Administration (HRSA), sent letters to the following six pharmaceutical manufacturers stating that the restrictions these manufacturers placed on 340B program pricing to covered entities dispensing medications through contracted pharmacies has resulted in overcharges in direct violation of the 340B statute:

• AstraZeneca

• Eli Lilly

• Novartis

• Novo Nordisk

• Sanofi

• United Therapeutics

HRSA has requested a response by June 1 from these organizations as well as a plan on how they would provide these overcharges back to the covered entities that were impacted.

This is a link HRSA 340B to a brief overview of key recommendations that our members can follow related to this latest action.

I would speculate as in the past, that you are incorrect in your assessment of RXMD and management.

Just submitted my list of 12 questions to Stuart Smith. See how many they can actually respond to.

I guess some bet on $.01 instead of $.26 back in 2018 when 2 million shares were sold @ $0.019.

You are correct good sir, and maybe that is relevant because that was just 3 years ago when all RXMD shareholders witnessed that disaster.

Lack of knowledge about stock also resulted in unpleasant sell of 2 million shares @$.02, actually it was less than that, but who is keeping track of this historical stuff that doesn't matter anymore.

That doesn't explain a sell of 2 million shares @$.02 before it went to$.26

First quarter report due in less than 15 days. Will be nice to get that financial update.

Great possibility that that is the scenario here. Really be a great day when the quiet period is over.

I will be really happy when this quiet period is over.

Not likely. But we will eventually see it in reporting. 1st quarter report due in 29 days.

Yes, that could be shares that they already had in hand from the TA, because I think there was more than $1.1 million outstanding in debt yet. It's possible we negotiated a cash offer for any other that might have been outstanding as was mentioned in the Conference Call, or at some point it was mentioned to pursue that. Is yesterday's T-trade work, possibly Star Capital?

Awesome layout of RXMD potential stock price Value there Insta. Great work.

Yes, maybe you touched on this, but why would they have to do a confidential S-1. I guess the obvious answer is that includes a merger or acquisition with another company that they may themselves be going through final steps of another deal and the divesture of that company. Otherwise, why a confidential S-1?

I have mentioned this to others before, but I think we have individuals focused on profit in charge right now. I don't think the previous CEO was concerned as much about profit as she was servicing the community, charitability, etc. Don't get me wrong, I liked her, but that was my thought on several occasions after hearing her calls and articles, and maybe it was a bad read. But, in healthcare you have to have both, this I know being in the Pharmacy market myself and if you look at below. Something is taking shape, and that was done during COVID.

Noteholders are restricted by volume, 10% in fact, if someone would swipe up the ask in fail swoop, they would be in breach of volume limitation defined in contract. And any excess would be deducted from the outstanding amount. They would then lose their conversion benefit.

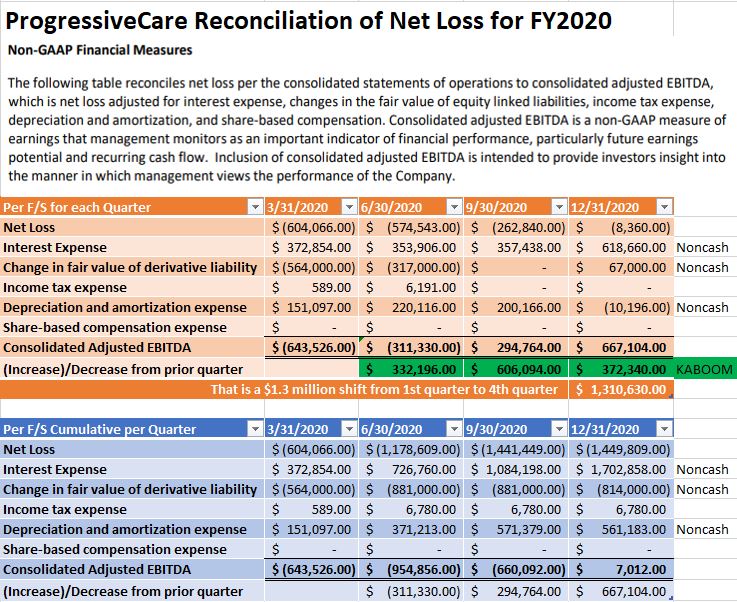

Check my update on it. It may have even been better in 4th quarter, without Depreciation and Amortization Expense Change.

It's ASTOUNDING!!!! 2020 EBITDA Breakdown by Quarter

$667K positive EBITDA in 4th Quarter Alone

To be honest, it looks like they changed their Depreciation and amortization practices with new Auditing Firm. If that would have remained consistent at $200,000, it would have been $887K for 4th quarter. 4th quarter showing a $(10,000).

S1 and NASDAQ are the speeding pole vaulter, those deals are the pole going to propel this company to new heights.

Yes, that's phenomenal news, I will try to work on creating a spreadsheet with that information tomorrow.

And $200k prior to end of year.

BINGO INSTA! And welcome back to the board.

It has to be!

4.99% is correct.

13. Ownership Limitation. Notwithstanding anything to the contrary contained in this Note or the other Transaction Documents, if at any time Lender shall or would be issued shares of Common Stock under any of the Transaction Documents, but such issuance would cause Lender (together with its affiliates) to beneficially own a number of shares exceeding 4.99% of the number of shares of Common Stock outstanding on such date (including for such purpose the shares of Common Stock issuable upon such issuance) (the “Maximum Percentage”), then Borrower must not issue to Lender shares of Common Stock which would exceed the Maximum Percentage.

I personally didn't realize they had converted that many shares, we could be much closer than I thought, and if we are considering cash payment to clear the debt, then we are definitely much closer.

If that is the case, that is exactly what we all as inventors have been hoping for. Some cash payments for a portion of the notes left. That would be fantastic and was a lift for this stock last time it happened as well.