News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

fredman

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

These 5 Stocks Under $10 Could Make You a Lot of Money

Here's a technical look at how to trade several under-$10 stocks triggering breakout trades

Another under-$10 biotechnology player that's starting to move within range of triggering a big breakout trade is Proteon Therapeutics (PRTO) , which focuses on the development of pharmaceuticals to address the needs of patients with renal and vascular diseases. This stock has been destroyed by the sellers over the last six months, with shares collapsing by 75.7%.

If you take a glance at the chart for Proteon Therapeutics, you'll notice that this stock recently gapped-down sharply lower from around $10 a share to under $2.50 a share with monster downside volume flows. Following that move, shares of Proteon Therapeutics went on to print a new 52-week low at $1.75 a share within a few weeks. This stock has now started to rebound off that $1.75 low and it's beginning to trend within range of triggering a big breakout trade above some key overhead resistance levels.

Traders should now look for long-biased trades in Proteon Therapeutics if it manages to break out above some near-term overhead resistance levels at $2.14 to $2.25 a share with volume that registers near or above its three-month average action of 208,676 shares. If that breakout develops soon, then this stock will set up to re-test or possibly take out its next major overhead resistance levels at $2.60 to its gap-down-day high from last December at $3.10 a share. Any high-volume move above $3.10 will then give this stock a chance to re-fill some of its gap-down-day zone that started near $10 a share.

Traders can look to buy this stock off weakness to anticipate that breakout and simply use a stop that sits right below some near-term support at $1.90 a share, or near its new 52-week low of $1.75 a share. One can also buy shares of Proteon Therapeutics off strength once it starts to move above those breakout levels with volume and then simply use a stop that sits a comfortable percentage from your entry point.

Source:

http://www.thestreet.com/story/13943826/2/these-5-stocks-under-10-could-make-you-a-lot-of-money.html

Buying ASTI hand and fist!!!

WE CAN DO THIS! LONG A $ T I

It is FREDMAN, not BIDMAN! Thanks for the cheapies! LONG ASTI GLTA

According to the December 13, 2016 conference call for Proteon Therapeutics PRTO the results of the study presented was "Top Line" data. The company expects to get additional data from the study over the coming weeks and this and other data is expected to be presented at a number of medical meetings in Q1 and Q2, 2017. The company was expecting a bigger effect in the study but the results were still promising. The company will continue to work closely with the FDA under fast track designation and will likely explore the opportunity of potential endpoint revision. The company expects to be in discussions with the FDA and will provide more specifics after the first of the year. The Patency-2 trial is expected to be completed by Q2 2018. The company has enough cash on hand until Q3 2018.

Source: http://ir.proteontherapeutics.com/phoenix.zhtml?c=253625&p=irol-eventDetails&EventId=5245007

I am optimistic of the results of the study and the data looks promising.

Any number of catalysts including a potential buyout / merger rumor or a few positive press releases from the company, and PRTO could easily fill the gap to ~ $5.38, if that resistance is broken, upwards of $10.00+ is very likely.

Long PRTO

All In My Opinion

Do Your Own Due Diligence!

Long PRTO Proteon Therapeutics could move quick to fill the gap with further FDA correspondence, imo.

Long UWTI for 2016 hang on because this is where it happens, imo.

Congrat$ to long$!

.90 is not too bad at all (my cost basis was .30)

GLTA EOM

I am guessing the FDA will ultimately require another re-inspection of the vendor.

WMGIZ going lower, imo.

UWTI will likely see new all-time lows in short order.

The drop in UGAZ being more controlled as of late is reassuring, all imho.

Averaging down in UGAZ today, long and strong, eom.

I would rather be long than short ugaz at these levels. Testing the bottom of the channel, imo.

In @ 2.01 out @ 2.15. Will rebuy under 2.00 after the report, imo.

I loaded the boat on Friday.

UGAZ headed back to $3.00 + in short order, imo. GLTA

WAG 07/23/2015 03:14:04 PM

I agree, the longer it takes for Augment to get approval, the less chance of obtaining the revenue milestone(s). I think $5.00 is still in the cards, but the market has to ask are current values worth the risk? It could take several years to obtain the milestone payment, is the risk worth a possible 20% ROI? In addition, CVR payouts are also potentially subject to withholding. IMHO, GLTA

I sold everything pre market this morning. I have a feeling UGAZ will go back to the 1.90's after tomorrow's EIA storage report @ 10:30, imo. GLTA

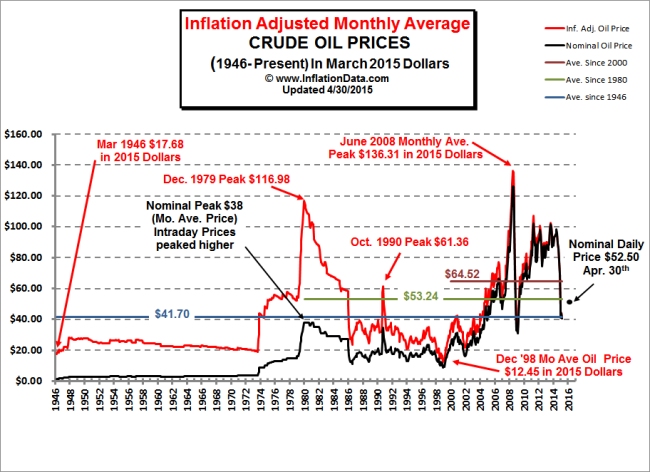

When Oil was $45, UWTI was @ $2.25 only a few weeks ago. Now oil is $48 and UWTI is @ $2.25 (Decay).

I think oil will go lower before it goes higher. All the talk lately has been centered on Iran, however the oversupply / storage issue is still looming. Smart money is staying on the sidelines. With decay, UWTI will likely see sub $1.50 as it retests lows in next few weeks, all imo.

Going lower, imo. Too much uncertainty in the air in regards to Iran oil exports, will buy back lower after the dust settles next month, eom.

It is difficult to spot on the UWTI chart due to decay / etf fees etc, a potential Double / Triple Bottom (reversal pattern) could be forming in Oil, with breakout occurring like clockwork upon increased spring / summer demand over next few weeks and/or months, in my opinion.

http://stockcharts.com/school/doku.php?id=chart_school:chart_analysis:chart_patterns:triple_bottom_reversal

Cool chart, thanks! USD is king

Strong dollar, oversupply, lower demand, oil was trading in the mid 20's not too long ago. The longer they try to hold oil up, the harder it will fall. In the near term, to mid 40's ultimately to the low 30's, or even back to the mid 20's again as history has a way of repeating itself, imo.

Source: http://inflationdata.com/Inflation/Inflation_Rate/Historical_Oil_Prices_Chart.asp

The numbers just do not add up, bleeding cash in hopes and dreams of a future turnaround. Massive dilution, reverse split, and lower prices are all likely outcomes in the near term. AMDA price target .30 (or lower) imo.

Lumber Liquidators will likely be forced into liquidation as a result of all the toxic flooring sold and installed over the years. As a result, I wouldn't touch this with a 10 foot piece of laminate flooring until the dust settles, all imo.

The FDA will likely require further action from the company on at least one or more issues in the form 483 response, resulting in further delay of Augment approval. Odds are WMGIZ will head lower, all imo.

Bob Palmisano - President and CEO

"The inspection that occurred at the vendor had 13 observations."

Source: http://seekingalpha.com/article/2951646-wright-medical-groups-wmgi-ceo-robert-palmisano-on-q4-2014-results-earnings-call-transcript?part=single

One of the things I am concerned about is that you are sort of in a race against time here for this month we have this toxic Black-Scholes provision in the warrants that were done with the recent offering through Dawson James. Have you calculated what potentially is the stock space at these levels, what kind of shares are going to be issued could be issued on a cashless basis?

Sonny Bal - Chairman and Chief Executive Officer

Yes so that's a 12/31 indicate that the amount of the dilutive impact of the shares would be about 13 million shares on a fully diluted basis related to warrant in addition to that there is some stock options outstanding out there and some RSUs for which shares need to be granted as well.

Unidentified Analyst

So in order to avoid that your stock has to reach a level of what by March 26?

Sonny Bal - Chairman and Chief Executive Officer

In order to avoid that it varies depending on the price of the stock. So kind of ranges from $0.80 or $0.50 to $0.80 or maybe a $1.50 would vary on how much stock will need to be issued if all the cashless exercise provisions were granted. So it's hard to predict exactly how much it would be but if it got to $1.85 then that would minimize it.

Unidentified Analyst

As far as your present financing Hercules which is like a strangle at the $9 million covenant. When do you think you will be in a position to -- some of these announcements hopefully get this back up and look to renegotiate and get rid of that debt?

Sonny Bal - Chairman and Chief Executive Officer

As we have indicated a lot of the reasons in focus for reasons for making the restructuring changes are in January, while as to allow us the runway as a company and as a management group to not have the distractions of needing to raise capital every three months. And so perfectly that's pushed the horizon out for us to bump up against the cash covenant that we have with the Hercules well on to quarter four which is as a management driven company we're focused over the next three months to four months, five months to execute on the strategy that we have outlined. At the same time we have discussions and that we will be more active in those discussions beginning in Q3.

Unidentified Analyst

Do you have any volume in the extremely high somewhat like somebody shorting into this cashless exercise? Do you have any idea where all these shares are coming from?

Sonny Bal - Chairman and Chief Executive Officer

We're unsure at this time of what is causing all of that, it’s little unclear as to what is occurring with the increased volumes that has happened over the last couple of weeks. So let’s say I am not sure what the answer is in with regards to that.

Source: http://seekingalpha.com/article/2977406-amedica-corporations-amda-ceo-sonny-bal-on-q4-2014-results-earnings-call-transcript?part=single

WMGIZ is trending lower as a result of the FDA finding a total of THIRTEEN Observations in the form 483. This seems like a big number of issues found in the inspection, and it is likely that any one of those observations could result in follow-up responses required from the FDA, causing further delay, decreasing the chances of revenue milestones being met in the future, imo.

WMGIZ CVR buyback is a good possibility, imo.

$533 million proceeds

- $51 million transaction expenses

- $292 million notes repurchase

Balance = $190 million

Total WMGIZ CVR value @ $6.50 = $190 million

"The Company estimates that the net proceeds of the offering will be approximately $533 million (or $613 million if the initial purchasers exercise their over-allotment option in full), after deducting the initial purchasers' discounts and commissions and estimated offering expenses. The Company expects to use approximately $51 million of the net proceeds from the offering (or $58 million if the initial purchasers exercise their over-allotment option in full) to pay the cost of the cash convertible note hedge transactions (after such cost is partially offset by the proceeds to the Company from the sale of the warrants). The Company also expects to use approximately $292 million of the net proceeds of the offering to repurchase approximately $240 million aggregate principal amount of the Company's outstanding 2.00% cash convertible senior notes due 2017 in privately negotiated transactions and the remaining net proceeds from the offering for general corporate purposes, including possible acquisitions."

Source: http://www.marketwatch.com/story/wright-medical-group-inc-prices-550-million-cash-convertible-senior-notes-offering-2015-02-10

I agree, the CVR's represent tremendous upside potential. We have over 4 more years to achieve the revenue milestones. Likely they will both be met, imo.

The merger with Tornier is hung up on the FTC in regards to lower extremities, maybe they need to tender the cvr's in order for the merger to proceed? The latest $400 million offering would definitely provide the means to do so.

"Wright is required to provide a product sales statement to the trustee that includes a calculation of the aggregate product sales for the Products during that calendar month and the 11 immediately preceding calendar months."

Source: http://www.nasdaqtrader.com/content/newsalerts/2013/infocircular/WMGIZcircular.pdf

Earnings release (Annual Report) and conference call is scheduled for February 25th. The tender offer should be priced somewhere in the range of $5.75 to $6.00, as the revenue milestones are based upon GLOBAL sales of Biomimetic products, imo.

"“Product” means any of the following medical products: (a) AUGMENT Bone Graft; (b) AUGMENT Injectable; (c) AUGMATRIX Bone Graft; (d) AUGMENT Chronic Tendinopathy; or (e) any other medical product that the Company, in its sole discretion, elects to offer for sale in any jurisdiction and that: (i) contains recombinant human platelet-derived growth factor BB; and (ii) is covered by patents or utilizes proprietary know-how that was owned or controlled by Achilles immediately prior to the execution of this CVR Agreement."

Source: http://www.lawinsider.com/contracts/5JXznltiLGu57a6ucWWJPJ/wright-medical-group-inc/contingent-value-rights-agreement/2013-03-01

The CVR Agreement does not prohibit Wright or any of its subsidiaries or affiliates from acquiring the CVRs, whether in open market transactions, private transactions or otherwise. However, prior to any acquisition of CVRs, Wright must publicly disclose the amount of CVRs which it has been authorized to acquire and Wright must report in each of its annual and quarterly reports the amount of CVRs it has been authorized to acquire as well as the amount of CVRs it has acquired as of the end of the quarterly or annual period reported in such quarterly or annual report.

Source: http://www.nasdaqtrader.com/content/newsalerts/2013/infocircular/WMGIZcircular.pdf

Potential CVR buyback of all outstanding shares of WMGIZ from Wright Medical prior to merger with Tornier, imo. 28.1 million contingent value rights (CVRs) were issued, and at $6.50 is approximately $190 million.

02/09/15 Wright Medical Group, Inc. Announces Proposed Private Placement of Cash Convertible Senior Notes

"The Company estimates that the net proceeds of the offering will be approximately $389 million (or $447 million if the initial purchasers' option to purchase additional notes is exercised in full), after deducting the initial purchasers' discounts and commissions and estimated offering expenses. The Company expects to use a portion of the net proceeds from the offering to pay the cost of the cash convertible note hedge transactions (after such cost is partially offset by the proceeds to the Company from the sale of the warrants). The Company intends to use the remaining net proceeds from the offering for general corporate purposes, including possible acquisitions and to repay up to approximately $250 million aggregate principal amount of the Company's outstanding indebtedness in privately negotiated transactions."

Source: http://www.marketwatch.com/story/wright-medical-group-inc-announces-proposed-private-placement-of-cash-convertible-senior-notes-2015-02-09

"I am also pleased to report that of the two pre-approval facility inspections the FDA indicated were required for final approval of AUGMENT Bone Graft, one has been completed with no 483 observations cited by the inspectors, and the other is in progress. Although final audit reports are still pending, based on the information we have today, final FDA approval for AUGMENT Bone Graft could potentially come as early as late first quarter of 2015"

Source: http://www.sec.gov/Archives/edgar/data/1137861/000113786115000002/wmgi1122015exhibit991press.htm

Company expects $300M market potential in the US and $1B+ market potential in the US for future uses of Augment product line.

Source: http://services.corporate-ir.net/SEC.Enhanced/SecCapsule.aspx?c=129751&fid=9848248 (Page 16)

STRONG BUY, imho.

Liquids that grow bone

Liquids that grow bone in humans? Sounds crazy but they are now commonly used in all sorts of Orthopedic applications. In addition, two weeks ago the FDA approved another product called Augment from Biomimetics (http://www.biomimetics.com/). Biomimetics was purchased by Wright medical in 2013.

Here is a little history. The “gold standard” in Orthopedics has long been bone graft harvested from the patient’s Iliac crest. The Iliac Crest is the top of the Illium. It is part of the pelvic bone that you can feel along your waist line. To harvest the graft the surgeon would make an incision over the bone and cut into the illium. Then scoop out bone to be used during the procedure.

Often the patients would complain that the graft sight was more painful than the surgery itself. Complications associated with this procedure include infections and continued pain. This was a problem that really needed a modern solution. Then in 2001 and 2002, the FDA approved the first liquid proteins for human use.

They were BMP-7 (Stryker) and BMP-2 (Medtronic) respectively. These BMP’s or “bone morphogenic proteins” trigger the body to grow bone where it is needed when implanted at the time of surgery. BMP-2 marketed under the brand name “Infuse” was a blockbuster product that quickly achieved $1 Billion in sales within a few years. Conversely, BMP-7 marketed under the brand name OP-1 struggled with a reduced use labeling from the FDA. It was sold off to Olympus Biotech and eventually they stopped producing it all together and is no longer available.

So the recent approval of Augment is the first new bone growing liquid approved in years. However, it too had a bumpy road getting through the FDA. After an extensive, expensive but well done study, the product was recommended by the Orthopedic panel that precedes the FDA approval. Typically, this means you are in! During this time, Medtronic was coming under fire for possibly hiding the cancer risk associate with Infuse during their trial.

This set off alarms at the FDA, so they were very careful to review this part of the Augment study with extra scrutiny. They decided that the product needed additional study and stunned Biomimetics with a “not approvable” decision.

During the run up to the FDA decision Biomimetics received an offer from Wright Medical to be purchased. This offered the insiders some hedge against the FDA risk. Wright offered the company $380 million, or $12.97 per share. However, the shareholders had to wait for half of their money.

They received an upfront payment of $6.47 per share. In addition, each BioMimetic shareholder received shares in a new tracking stock ticker WMGIZ which entitled its holder to receive additional cash payments of up to $6.50 per share, which would be payable upon receipt of FDA approval of Augment® Bone Graft and upon achieving certain revenue milestones. The payments were structured as follows:

$3.50 would be paid out per share upon FDA approval of Augment® Bone Graft;

$1.50 per share upon the achievement of $40 million in trailing twelve month sales for all products contributed by BioMimetic;

$1.50 per share upon the achievement of $70 million in trailing twelve month sales for all products contributed by BioMimetic.

On the day the FDA reached it’s decision the stock dropped from around $3 per share (shareholders believe the approval was coming) to near zero as everyone rushed to sell their shares. It would appear they were done. Or were they?

Wright medical is a big company with deep pockets. They decided to retrench with the FDA and asked them to review the data again. They felt they could address the FDA’s concerns without doing another big study. After trading at 20 cents or so from August of 2013 to March of 2014, the FDA announced they would give Augment one more look before sending them back to a clinical trial.

The stock jumped 200% on the day this was announced and continued to rise over the next few months. Investors speculated that they just might pull it off even though an FDA reversal had only occurred a few times before in its history. On October 27th, the FDA approved Augment for use. The stock, trading around $1.88 per share shot up to $4.50.

On the same day as the approval, Wright agreed to be sold to Tornier for $3 billion. Assuming the product is as good as the study suggests the tracking stock will finally top out at $6.5 as the final milestone payments are paid out.

An amazing story that ends well for shareholders and I believe patients too. These liquids are a vast improvement for those undergoing surgery that requires a bone graft procedure. For once it seems that everyone wins.

Source: http://www.innov8med.com/liquids-that-grow-bone/

Switching now to last week's positive news regarding the receipt of an approval of letter for Augment Bone Graft. This major milestone paves the way for ultimate commercialization in the U.S. for foot and ankle or hindfoot fusion procedures, and it further underscores our strength in Biologics. Our focus now is on completing the requirements outlined in the approval of letter and bringing Augment Bone Graft to the U.S. market. Final approval was subject to customary preapproval facilities inspections, which we expect to be completed in the December to January time frame. Over the next few months, we will also train our U.S. foot and ankle sales organization in preparation for U.S. commercialization.

Although the exact timing of the Augment launch is not known, a conservative time frame is the first half of 2015, assuming satisfactory approval -- preapproval inspection activity. We expect to be ready to launch Augment in the U.S. immediately upon receipt of the final approval order from the FDA.

We agreed with the FDA on 2 postapproval studies: one, is a fairly typical 24-month conditions of actual use study, which follows the result of surgeons who did not participate in the original pivotal trial; and other -- and the other is a onetime 5-year evaluation of certain number of pivotal study patients. Since virtually, all of the -- those pivotal study trial patients are now 5 years postsurgery, this is not owners. I believe Augment will become a valuable new therapeutic option as an alternative to order graph and ankle and hindfoot fusion procedures, especially as it can eliminate potential complications, morbidity and pain associated with order graph harvest. In addition, Augment provides a platform technology for future new product development, particularly in various upper extremity areas. We look forward to addressing that -- these with additional clinical studies.

I think that we've -- since we announced that we've gotten this approval letter, we've gotten tremendous response from physician community that they just can't wait to get their hands on it, and we just have to kind of like hold them back right now until we can actually get it approved into market.

Brad Mas - Needham & Company, LLC, Research Division

Great. And then just one last quick one. I'm wondering if you guys have any plans to begin additional trials for the injectable form of Augment.

Robert J. Palmisano - Chief Executive Officer, President and Director

Yes. We have an idea on that, and I think that some work has begun on that -- had begun on that, and then we'll continue. As I said in my prepared remarks is that we look -- we see this as a platform technology. And we have other -- we have clinical work ahead of us to expand out of the -- where we're headed in hindfoot and new foot infusions. But we think it's appropriate in different areas. We -- I would say, particularly, in upper extremity. We will -- so we will be doing clinical work starting, I think, sometime in 2015 on other indications. We have -- now with the merger with Tornier, we have a large upper extremities sales force that, hopefully, we can provide them with a terrific biologic for that area as well.

Source: http://seekingalpha.com/article/2646295-wright-medical-groups-wmgi-ceo-robert-palmisano-on-q3-2014-results-earnings-call-transcript

Our initial clinical development program for Augment Injectable has focused on securing regulatory approval for open indications in the United States and in several markets outside the U.S. Recently, we have focused our efforts on securing FDA approval of Augment. The amount of time and cost to complete the Augment Injectable project depends upon the nature of the approval we ultimately receive for Augment, but we currently estimate it could take one to three years.

Our international biologics sales increased 24% as the result of a 49% increase in Asia as the result of the addition of a new distribution partner in China in the second quarter of 2013, and a 19% increase of sales in Australia, primarily related to sales of Augment® Bone Graft acquired from the BioMimetic acquisition in the first quarter of 2013

On October 27, 2014, we received an Approvable Letter from the U.S. Food & Drug Administration (FDA) for our Premarket Approval Application (PMA) for Augment® Bone Graft. The approvable letter indicates the FDA determined Augment® Bone Graft to be safe and effective as an alternative to autograft for ankle and/or hindfoot fusion indications and is approvable subject to customary preapproval facilities inspections. We currently anticipate that we will be able to sell Augment® Bone Graft in the United States beginning in the first half of 2015.

On October 27, 2014, we announced that we had received an Approvable Letter from the U.S. Food and Drug Administration (FDA) for our Premarket Approval Application (PMA) for Augment® Bone Graft. Following this announcement, the fair value of the CVR's increased significantly and traded at an average value of approximately $125 million in the four days following announcement. Approximately $98 million of the liability associated with the CVR's will be payable shortly after receipt of final approval from the FDA for Augment® bone graft.

Source: http://www.sec.gov/Archives/edgar/data/1137861/000113786114000051/wmgi930201410q.htm

Great thank you! Hopefully it is a relatively speedy process with the FDA at this point moving forward. Odds are Wright management will likely buyback the outstanding CVRS prior to the upcoming merger with Tornier.

566k shares traded so far out of 28.1 million outstanding shares of wmgiz. Longs are in control... Management sees $300 million market share in the US ALONE in Augment so both revenue milestones will likely be met with ease now that Augment has achieved FDA approval. I am just curious as to when the Augment $3.50 payout will occur???

At the Morgan Stanley conference call today, Wright Management stated that they are looking into the possibility of buying back some WMGIZ CVR shares. WMGI is in a great cash position to do this. STRONG BUY! imho.

Our international biologics sales increased 21% as the result of a 44% increase of sales in Australia, primarily related to sales of Augment® Bone Graft acquired from the BioMimetic acquisition in the first quarter of 2013, and a 20% increase in Asia as the result of the addition of a new distribution partner in China in the second quarter of 2013.

Source: http://www.sec.gov/Archives/edgar/data/1137861/000113786114000039/wmgi630201410q.htm