News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

On the other side of the world.

BonelessCat

![]()

On the other side of the world.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

On the other side of the world.

What complete bullshit! The decision not to use Dana Farber again was IPIX's as the first trial went far more slowly than it should have after a rough start and delay due to problems in the final inspection and checklist. Then there was the delay in p53 assays after the death of the lead lab person and no one trained to replace him. DF passed? A complete fabrication.

There is every chance of great data in this trial. Efficacy signals are all over the place if one is inclined to look at more than just tumor shrinkage. But, there is also some of that in the Phase 1. But, the great data I'm looking for is MoA and fuller characterization for better use in individualized combination therapies.

Thanks. Should have read the protocol, again. Still, cervix, not fun.

Types of cervical biopsies

Three different methods are used to remove tissue from your cervix:

Punch biopsy: In this method, small pieces of tissue are taken from the cervix with an instrument called “biopsy forceps.” Your cervix might be stained with a dye to make it easier for your doctor to see any abnormalities.

Cone biopsy: This surgery uses a scalpel or laser to remove large, cone-shaped pieces of tissue from the cervix. You’ll be given a general anesthetic that will put you to sleep.

endocervical curettage (ECC): During this procedure, cells are removed from the endocervical canal (the area between the uterus and vagina). This is done with a hand-held instrument called a “curette.” It has a tip shaped like a small scoop or hook.

The type of procedure used will depend on the reason for your biopsy and your medical history.

Don't see anything there about being done with a needle. Indeed, biopsies are not fun, even when they can be done with a needle.

It's likely that Leo didn't mention interim results for P just in case they are not ready in time for Sept 8. What could be worse than a great update only to have the trolls jump on missing data which would then be further overshadowed by troll negativity when released a few days later.

Thanks for searching for and finding all those 2017 partnership quotes. So, partnership by end of 2017? I hope so, but there are two sides to the negotiations and final agreement. The timing of the deal close is not entirely up to Leo. Assuming these last trials are part of what has already been agreed upon, there is still final review by BP's legal and a few other entities (final CFO and COO input comes to mind). These may or may not be already mostly in place, and that is my point to saying 2018.

So, if Jan 1 roles around and there still isn't a deal, y'all go ahead and raise a ruckus. I'll have a few more bucks to put in for stink bids as neighing and crying takes over for the month or two before an announcement and gap open. I could use a few more thousand shares at 30 cents.

B-OM was a cancer related trial. Of course it took two years, not to mention it competed with other trials for patients.

Bullshit. No one moved anything. I am using realistic timing that takes into account broad targets quarters, three month periods just to complete trials. Since all trials end in the 3rd and 4th quarter it's unreasonable to expect a deal in the same quarter when it takes 6 weeks just to get top line data prepared. No one is setting same quarter goal posts except those looking to create false deadlines (know what I mean?) BP deal in 2018. Yeah, earlier would be very nice, but not at all reasonable.

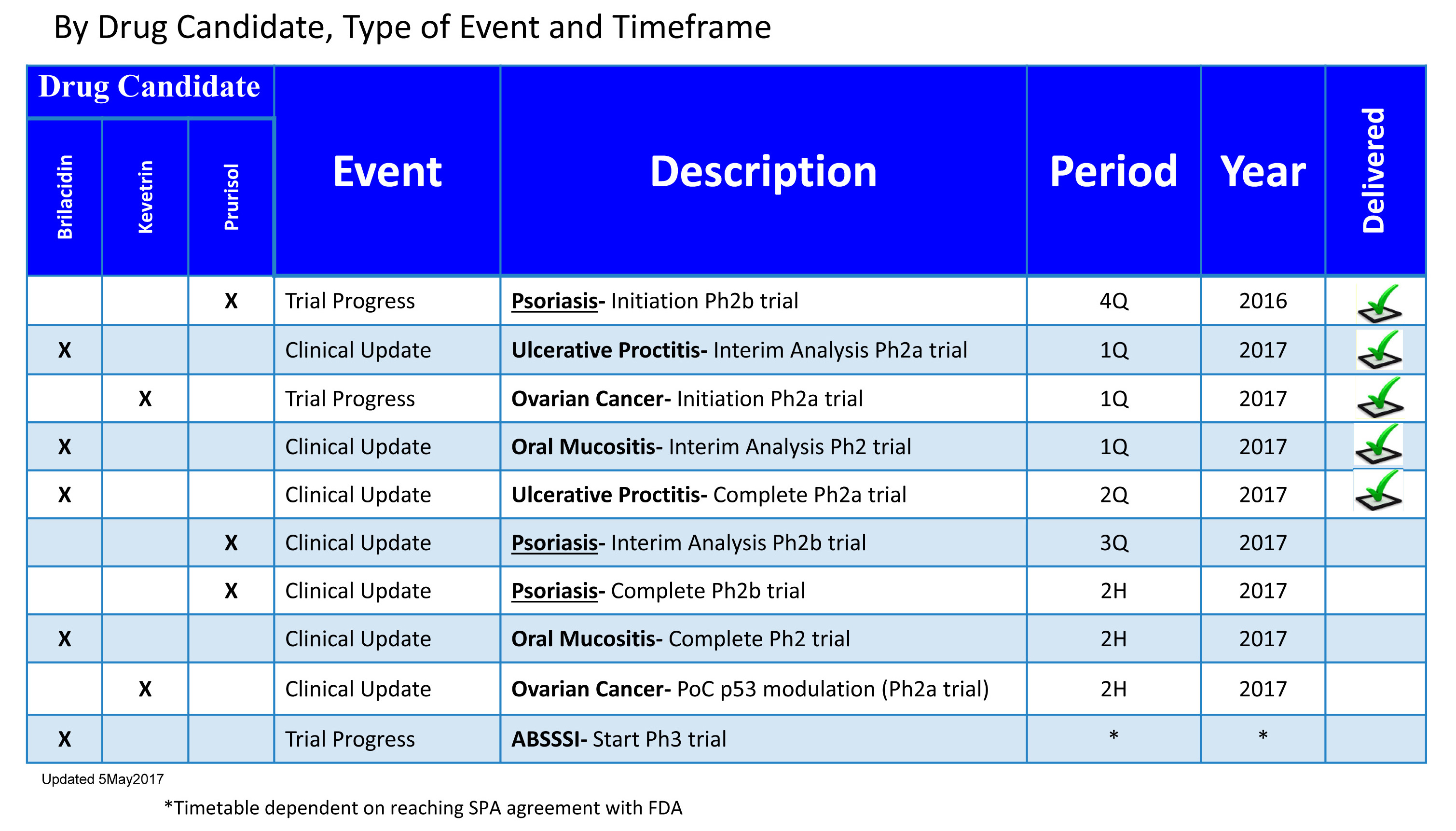

All the trials in prep for a partnership(s), are advancing on time. Of the remaining 4 remaining milestones, there is every indication Prurisol will complete before end of second half, and the Aug 15 PR indicated interim data might be soon after the Sept 8 showcase.

OM and OC are also on track to complete before end of 2nd half. Of course, to be safe add 3 months or another quarter, so all should be wrapped up with data on the way within 6 months. Some BP will want a piece of IPIX in 2018.

There is nothing misleading in that statement, it is merely an error. The premise still remains true, none of the FOUR officers have sold any shares. Calling it misleading, that is something I also object to, and something I would call an attempt to shift focus of the statement from the truth of the premise to some inconsequential detail. A simple question of "are there not still 4 officers?" followed by the source or link would have been sufficient to set the record straight.

Nonsense. Why would Prurisol wait for OM? A P license will fund the B platform through phase 3. Licensing B later will then pay for all of the K development and trials.

Dr. Frei of Harvard didn't think so. Beverly Teicher, with whom Menon coauthored a dozen or so peer reviewed papers didn't think so. Eli Lily didn't think so.

By the way, Kerala is in the top 50 universities nation wide for India. That includes a lot of universities from whom top top researchers are hired in the US and U.K.

Kerala University ????????? wtf is that? it sounds like a witch doctor school on the internet!

Menon earned his PhD while working under Dr. Frei at Beth Israel. He earned it from Kerala University while working as an assistant to Dr. Frei.

He also has a PhD in pharmacology that he earned while working under Dr. Frei at Harvard as well as a certified toxicologist.

CTIX was the entity set up to take the IP from preclinical stage to clinical stage. Dr. Menon separated IPIX from KARD a few years back. The name change to IPIX happened 2 months ago. IPIX now has 7 drugs in clinical trials. That's some ghost company. If you really were a chemist for KARD, you would know this.

I don't believe it for a second.

I'm long but very disappointed.

I think I have been suckerd.

Except for the part where he has 8 trials underway or completed since 2012. With no failures, I should add.

so Leo can be totally BSing with no way to fact check him!

What does an NDA have to do with the business plan to prove the platforms before a deal, as stated in PRs, their website, in the blog, and in financials?

First, you're wrong. BP has been shelling out 10s of millions up front and hundreds of millions in milestones for preclinical stage drugs for several years now. There is no reason they won't do the same even for a small PoC trial like OM. Thinking otherwise has no evidence.

No, Leo is not a "carnival barker." He's not even close to being one. If anything he is very understated and lacks such promotional qualities (something I like about him). I've been in several Bio-startups, and those CaeOs were definitely all hat and no horse, or all bluster and no substance. Leo now has 6 trials and no failures. That's not a barker; that's the real deal.

Bertilino didn't sell! Bertilino DIDN'T sell! BERTILINO DIDN'T SELL!!!

he watched Bertilino's sale

If they did a phase 3, everyone would complain about not advancing anything else and putting everything else on hold for an expensive, long, large population trial. Leo can't win.

Leo doesn't read this board. If he did he would actually have fluff PRs and not just be accused of fluff PRs when he reports milestones, trial progress and interim events. I love how posts just make shit up.

I have fast accumulated about 14 K shares now. doing ok , but still bargain hunting. and later some trimming probably.

Agree, the biggest benefit of partnering in late trials is the higher back end returns. Partnering early increases perceived risk to BP and whatever added cost is multiplied through lost future revenue. Licensing Phase 3 greatly reduces shared risk and increases royalties by a factor of at least double.

My point is to show that Phase 3 royalty is usually higher than Phase 2 royalty so the Phase 3 total royalty will catch up in a few years. I can use 10% royalty for Phase 2 and 20% royalty for Phase 3 and the logic is the same.

Where is deal for the all cancer cure K?

no one, except you, said it was a cure for cancer. It is a p53 modulator for treating cancer. The first deal is waiting for K-OM study with a completion of characterization. Management has made that clear. Maybe you missed all the memos?

Other companies are selling their pre-clinical compounds for potential $ 1 B payments.

Other companies aren't developing entire platforms of drugs to treat multiple diseases each.[/I]

K being in P1 for 4 years but no one looks at it or even mentions it.

Again, it's currently in a characterization study.[/I]

" Bristol-Myers Squibb Co said it would buy privately held IFM Therapeutics for an upfront payment of $300 million, as the drugmaker looks to bolster its cancer portfolio after losing ground to Merck & Co's rival treatment Keytruda.

The acquisition of IFM, whose backers include Novartis, will give Bristol-Myers access to the company's preclinical cancer programs.

Yes, and a similar plan exists for Prurisol. This requires patience. $300 million for a preclinical drug. Imagine what IPIX will get for a Phase 3 drug.

IFM investors are also eligible to additional contingent payments of up to $1.01 billion upon the achievement of certain milestones, the companies said on Thursday.

Imagine what we will get for milestones.

Yes, patient reports began with the first recruitment. That was indeed 2012 so not at all ridiculous.

Not as ridiculous as you saying "near ten years". Kevetrin started in 2012 remember?

https://clinicaltrials.gov/ct2/show/NCT01664000?term=cellceutix&rank=7

30% PASI75 has already been planted by trash-talkers as insufficiently robust regardless of truth. However, there will be a number (45% PASI 90?) that just can't be dismissed and dissed. If it hits that number, whatever it might be, yes, I see $2 followed by a BP deal and significantly higher SP.

Bullshit. Complete fabrication. No such missed deadlines or promises.

What bullshit. 6 trials with no failures. WTF do you want a CEO to do to give hope? Maybe what other CEOs do: issue dividends as shares or hire pump and dump teams using S8 shares to start posting false info.

Never mind all the trials, 100% success across 5 indications, and huge pipeline of 3 drug platforms, what's the share price this moment? That's the tail of a true CEO! Oh, I mean tale.

Every bit of guidance to shareholders has been calendar quarters. Only filing deadlines have been in fiscal quarters. Why would they suddenly change? Maybe some are looking to get low info SH to sell thinking they've got 6 more months? Likely.

Comparing Phase 2 results SGX942 and Brilacidin-OM:

"Patients with higher incidence of severe oral mucositis had a greater benefit from SGX942, although a reduced duration of ulcerative oral mucositis was also observed. Depending on the type of chemoradiation received, the 1.5-mg/kg dose decreased the duration of severe oral mucositis by 50% and 67% among patients at highest risk. The drug did not interfere with tumor treatment, and tumor status at the 1-month follow-up visit favored the 1.5-mg/kg treatment group. Nonfungal infections also decreased in the patients receiving SGX942."

http://www.valuebasedcancer.com/issue-archive/2016/november-2016-vol-7-no-10/sgx942-decreases-duration-of-severe-oral-mucositis-in-patients-with-head-and-neck-cancer/

"Preliminary efficacy and safety data from 19 patients who met the criteria for evaluation were reviewed. To be included, patients needed to have reached or passed the planned visit at the end of 5 weeks on study, and have received a cumulative radiation dose of at least 55 Gy. Patients receiving Brilacidin, as compared to patients on placebo, showed a markedly reduced rate of Severe OM (WHO Grade ≥ 3). Additionally, Brilacidin was generally safe and well-tolerated.

Primary Efficacy Results Incidence of Severe OM (WHO Grade ≥ 3)

• Active Arm (Brilacidin): 2 of 9 patients (22.2 percent)

• Control Arm (Placebo): 7 of 10 patients (70 percent)"

http://www.ipharminc.com/new-press-release/2017/3/26/cellceutix-reports-very-encouraging-interim-analysis-of-phase-2-drug-candidate-brilacidin-for-severe-oral-mucositis-om-in-head-and-neck-cancer-patients-high-potential-for-preventative-treatment

So, SGX942 decreased the duration of severe OM, while B-OM reduced the severity and (if I recall correctly) the duration.

Groundhog Day would be other posts and not the slimiest ones to which I was referring.

I feel like Bill Murray in Ghostbusters, slimed by a nasty little spud. I need a shower.

Please explain how Francis A. Farraye, MD, MSc became a leading gastroenterologist without touching a patient? Talk about misleading posts. I'm sure he would be happy to explain how he has more than 20 years of clinical experience.

From his profile:

He is Associate Professor of Medicine at the Boston University School of Medicine. Dr. Farraye has been recognized as “Top Doctor” in Gastroenterology by Boston Magazine and U.S. News and World Report since 2010.

Dr. Farraye's clinical interests are in the care of patients with inflammatory bowel disease, irritable bowel syndrome as well as the management of colon polyps and colorectal cancer.

https://www.bloomberg.com/research/stocks/private/person.asp?personId=60750508&privcapId=129358614

$IPIX - Innovation Pharmaceuticals Stock May Be A Triple-Crown Winner With Brilacidin By Year End

https://seekingalpha.com/article/4088788-innovation-pharmaceuticals-stock-may-triple-crown-winner-brilacidin-year-end

In theory, the Russell Indexes are included in institutional portfolios. When an institution includes it, it's all but required to include all components. So, no they are not being foolish; they are investing in all components of an index.

Contrafect is on the NASDAQ. When it comes to institutional owners, your comparing apples to not apples.

"Danger"? What nonsense. What hyperbole. Yeah, painted close, .92 posted 12 minutes earlier, and no last trades. Friday closing action traders might want to pay attention. This time of year, the kids start logging off around 3:00, and the few remaining enjoy low volume into the close. The past half dozen weeks the dominant Friday close has been to shove the price down. I suspect MMs will take it up on low volume to sell into any news next week. However, if down, then the plan is to pretend there are new resistance lines to break through should there be exceptional news.

You don't need a fancy chart to see this shit.

I would think worldwide use would be a bit higher for OM. When IPIX applied for orphan drug the application is as rejected because the US population alone was over 300k a year. I don't know where the 500k number came from, but for neck, shoulder and head cancers, >500k per year sounds right, and that would be only a large fraction of OM at risk cancer patients in the US. For EU, UK, US and Asian populations the number probably exceeds 1 million candidates for OM control or prevention.