News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

OMOLIVES

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Add to that via Somerley:

"The above report also makes reference to the view that China landborne hard coking coal imports are expected to rise by approximately 75% between 2016 to 2022, which is based on a third-party mining, metals and energy-focused research and consultancy firm"

http://www.mmc.mn/upload/2017-05-25_e_00975cir-20170526.pdf

This is the most bizarre situation I have ever seen. If these are debt holders(entitled to scheme)....then they are complete idiots(not all of course).

Never mind...it's here...just not anywhere else:

http://www.mmc.mn/upload/2017-06-08_e_00975ann-20170609.pdf

The Company is pleased to announce that the Company’s case under Chapter 15 of the United States Bankruptcy Code concerning the Debt Restructuring has been closed and that the Joint Provisional Liquidators have been discharged from office and released from the performance of their duties by order of the Cayman Court made on 8 June 2017 (Cayman Islands time). Accordingly, the Company is no longer subject to any bankruptcy proceedings in the United States and is no longer in provisional liquidation in the Cayman Island

!!!!!!! Now let us move forward...eh?

Where's the news release?

Thanks for that.

He's correct though..eh? On another note....what ever "water rights" information I read previously must have confused the hell out of me. From the JPL:

The Consortium must, within 2.5 years of being granted the licence, expand coal processing capacity in TT region

to at least 30mt of coal per year and sell the produced coal into at least two foreign markets. The fact that the

Group already has facilities with coal processing capacity of 15mt per year near the UHG mine places it in an

advantageous position as it is able to leverage the same facilities for the TT mine, given that the UHG and the TT

mines are adjacent to each other

The first and second modules of the CHPP commenced commercial operations in June 2011 and February 2012, respectively. MMC’s total name plate ROM coal processing capacity reached 15 Mtpa by the successful commissioning of the plant’s third module in June 2013.

This is interesting:

I also heard a rumor that ETT stopped selling from their East Tsankhi deposit over a price dispute with Chalco. If true, that would have affected the total numbers at GM through May.

Yes....I do think it is a big deal with regards to focus. An expanded sales team is needed for expanded sales...eh?

On another note...I have MMC at a rough 1.5 mnt @ end of May(total from jan start). May being light(as I thought)... through Ganqimaodu border.

Conservative of course..very. This is of course lacking sufficient data.

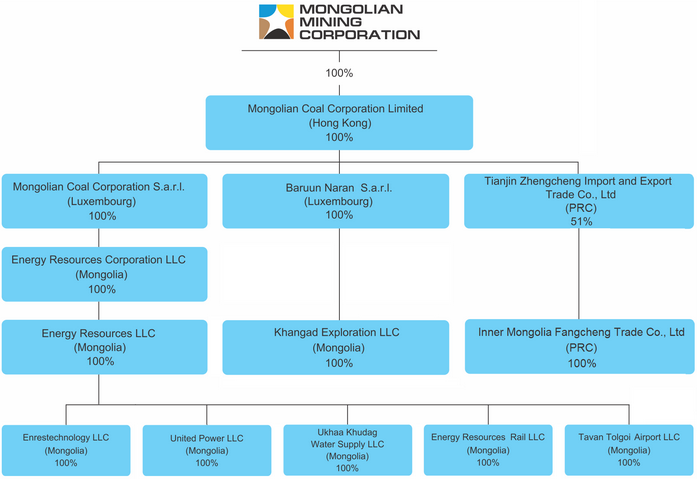

! group structure has changed:

Interesting to note..."Inner Mongolia Fangcheng Trade co Ltd"

It is way beyond the time for reality to set in. Let us hope that the reality check is finally in..eh?

I think I am letting too much noise in...reviewing what I said here:

It is my understanding that there needs to be a separate facility to wash coal due to given water sources et al(location thereof..etc).

!! http://www.mmc.mn/upload/2017-06-05_e_00975ann-20170605.pdf

On 2 June 2017 (Cayman Islands time) the Joint Provisional Liquidators (the “JPLs”) filed papersin support of an application seeking, amongst other things, an order dismissing the winding-up petition filed on 7 July 2016 (the “Petition”) and seeking the JPLs’ discharge from office. Thehearing of the application will take place before the Cayman Court on 8 June 2017 at 9:30 a.m. (Cayman Islands time). Upon a dismissal of the Petition and release of the JPLs (if so ordered by the Cayman Court), the provisional liquidation will be terminated and the Board will resume full control over the affairs of the Company.

The Company and the JPLs would like to take the opportunity to express gratitude to all parties for their efforts in the Debt Restructuring.

No...but then again.....I'm not sure that is a given until I see proof. It is my understanding that there needs to be a separate facility to wash coal due to given water sources et al(location thereof..etc).

Enrestechnology LLC(CHPP) is a sub of Energy Resources llc. If Shenhua is to hold 49% of Energy Resources llc(if that is still the plan)....then i am just not sure.

I tend to believe that the term "incremental" has as much weight as the term "goodwill". I get it...just do not apply it.

There is to be a new facility. I read previously that it was to handle 30 Mnt.....but can not find that piece currently. I did find one that stated a 15 Mnt facility though.

But you have to consider the fact that Energy Resources llc would be giving up 49% to Shenhua

Yep...very busy June ahead.

Election...the court finalization in June..and :

We have reviewed the mining production volumes in 2016 and the first quarter of 2017, and noted that the Group has been in the process of increasing its production since the second half of 2016, with production of hard coking coal in the first quarter of 2017 representing an increase of approximately 212.3% when compared to the same period in 2016. As a secondary check, we have made reference to a report published by the Joint Provisional

Liquidators in August 2016, which sets out projections for the Group’s hard coking coal output, amounting to 4.5 million tonnes in 2017 and 6.1 million tonnes in both 2018 and 2019, under a conservative scenario. It was assumed, under a conservative scenario, among others, that (i)the current operating structure of the Group remains unchanged, and (ii) sales volumes will increase on the basis of a growth in hard coking coal demand from China. The above report also makes reference to the view that China landborne hard coking coal imports are expected to rise

by approximately 75% between 2016 to 2022

! Baogang pushes on with steel expansion

By Meng Fanbin in Beijing and Yuan Hui in Hohhot | China Daily USA | Updated: 2017-05-25 06:58

http://usa.chinadaily.com.cn/epaper/2017-05/25/content_29496969.htm

Steel giant Baogang Group is planning to integrate its overseas operations and expand its market share through the Belt and Road Initiative.

The State-owned iron and steel company will set up an international division from its Baotou headquarters in the Inner Mongolia autonomous region.

This is all part of a push by the group to seek overseas financing as it brings together its offices in the United States, Singapore, Japan and Hong Kong.

"We will not only explore increasing global sales for our steel products, but also try to expand our role as an integrated trade service provider in the steel sector," said Wu Yongbo, deputy director of strategic development at Baogang.

......Other company plans include expanding iron ore operations in the Tumurtei mine in Mongolia as well as the anthracite project in Jargaland and the coking coal operation in Tavantolgoi, Mongolia.

Now I am just sick!.....my temperance diluted my judgement today. Oh well......it goes both ways...but damn!!!!!!!

yep....and I should have bought way more than I did today....up 24% currently on that spike.

IMF was the hitter

!IMF Executive Board Approves Financial Arrangement for Mongolia

http://www.imf.org/en/News/Articles/2017/05/24/17193-imf-executive-board-approves-financial-arrangement-for-mongolia

Man...I have been walking in the past few days.....and it looks like this will continue.. :)

I'm starting to get pretty excited!

Clause 13.3 ... http://www.mongolianmining.ky/downloads/Petition-17-February-2017-filed-and-sealed.pdf

So surplus is just that,,,surplus. Whoever failed to come forward becomes the surplus...apparently.

I originally thought that there would be five tranches to be distributed on the initial date...and 4 quarters thereafter(essentially). The trustee would hold the entire lot to be distributed accordingly. Need to go back and review such...because I am just not following this surplus thing.

It's here....(page 26/or page 38 on pdf view):

http://www.mongolianmining.ky/downloads/Petition-17-February-2017-filed-and-sealed.pdf

Still do not get it. My take is that all is held by trustee...and the surplus is what has not been distributed. As in...those that have not come forward???....have to look into it more...because I'm not following.

Also....they are following SEC 3(a)(10) Exemption ... so from review ..no holding period...

Also....don't see any eligibility to short...:

https://www.hkex.com.hk/eng/market/sec_tradinfo/ds_list20170523.htm

https://www.hkex.com.hk/eng/market/sec_tradinfo/dslist.htm (main page)

I ran 10/20/30 percent dilutive inventory 9 day turn on volume and get this:

10%...26.4 mill

20%...52.8 mill

30%...79.2 mill which equates to rough 8% of initial distribution

All based on 9 days @ 264.04 total volume. So in my head....it is mainly just foolish hands.

The word "apparently" is what I am looking at right now...i.e....distribution dates/surplus.

[edit]..Getting close to capitulation(HK). Breached the bottom of DEC....where will it close?...eh?

GO GUINS'!

I don't think it was a trial with regards to MMC...in as much...as a trial from Tavan Group. There is no rail ...so....it was assuming such until ..."such".

Yes...they have also been doing trial runs with Sumitomo. I believe this has been within the last 12 months.

Total available market/served available market....and share of market. You see it mainly in startups....amid ways to garner cash.

But to be fair...that is what Tavan is...in a sense. Here's a recent wire via reuters:

Nippon Steel looks to mixed-length deals, new suppliers to buffer coal volatility

Yuka Obayashi and Ritsuko Shimizu

6 Hours Ago

http://www.cnbc.com/2017/05/22/reuters-america-interview-nippon-steel-looks-to-mixed-length-deals-new-suppliers-to-buffer-coal-volatility.html

Sounds like a good study. This may sound strange...but how about TAM/SAM/SOM with regards to Tavan Tolgoi?

i.e. ...:

"JFE Holdings Inc, Japan's second-biggest steelmaker, aims to buy more coking coal outside of Australia to offset price risks for the steel ingredient that were made evident by a big cyclone in March, its president said on Wednesday.

"The biggest reason for volatility of coking coal prices is geographic risk, with a major part of global production coming from the east coast of Australia," JFE President Eiji Hayashida told a news conference. "

http://www.reuters.com/article/us-japan-jfe-holdings-coal-idUSKCN18D14W

Need that rail..eh?

It's not correct...it's just bizarre.

1,145,672 Mnt.....of which:

Jan/326,872

Feb/430,000

March/388,800

I found my error here:

OMOLIVES Friday, 05/19/17 03:24:24 PM

Re: OMOLIVES post# 299

Post # of 302

Damn it....right in front of my face:

This was the highest level of shipments from Indonesia to China since December, and it's possible the April figure could be revised higher in coming days as cargoes that arrived at the end of the month get added to the count.

www.reuters.com/article/us-column-russell-china-idUSKBN17Z0XM

Can't believe I missed that originally....that's the difference.

Mongolia Apr coal export up 71pct on mth

?2016-05-18 14:30:49 ?Import & Export, International ? sxcoal.com

Mongolia exported 5.56 million tonnes of coal in April, surging 71.12% from March, the latest data from the Mineral Resources Authority of Mongolia showed.

During the month, Mongolia exported 3.64 million tonnes of coking coal, up 52.94% month on month. Of this, washed coking coal exports stood at 530,000 tonnes, up 50.84% on the month; raw coking coal exports 2.14 million tonnes, up 111.36%; while exports of semi-soft coking coal down 5.18% from the previous month to 970,000 tonnes.

Meanwhile, thermal coal exports stood at 1.9 million tonnes in April, soaring 120.89% month on month.

In April, the country's output and sales of coal stood at 7.98 million and 8.41 million tonnes, rising 56.37% and up 50.15% month on month, respectively.

Over January-April, Mongolia's coal exports stood at 11.4 million tonnes; total coal output at 18.99 million tonnes; and the sales at 19.24 million tonnes.

Mongolia's domestic coal consumption reached 2.85 million tonnes in April, up 21.22% from March, and total coal consumption during the first four months amounted to 7.84 million tonnes.

(Writing by Evie Feng Editing by Harry Huo)

I'm going to hold up on that news(April exports)........can not clarify it.

Damn it....right in front of my face:

This was the highest level of shipments from Indonesia to China since December, and it's possible the April figure could be revised higher in coming days as cargoes that arrived at the end of the month get added to the count.

http://www.reuters.com/article/us-column-russell-china-idUSKBN17Z0XM

Can't believe I missed that originally....that's the difference.

I think that's a well weighted speculation. So where did the coal come from? Mongolia exported 3.44 Mnt in April. Yeah...it was a 7-8% increase from March and double what it did last year....just confused as hell where China got that extra coal from. Too much noise..eh? ... or should I say ...not enough info provided

Thank the Lord.....!.....was getting concerned.

Now that is what I call Déjà vu via a December HK Friday.. It better not go up 20 points...be it a 30 point swing! If such.....gonna' be really pissed.

!!...say it ain't so.....

I've been watching futures mainly....:

http://www.cmegroup.com/trading/energy/coal/australian-coking-coal-platts-low-vol-swap_quotes_settlements_futures.html#tradeDate=05/17/2017

Also loving the rain currently ..down under. Wanted to apologize for ranting with regards to other. I am just so sick and tired of scattered information ... and jumping to false or skewed assumptions. And here I did the same thing.....skewed my assumption before reading the entire piece.

The company is not under creditor control. It is though under scrutiny given the restructuring. Scrutiny may be a bit harsh...but you get what I mean.